It’s already in the works and goes far beyond subprime.

The auto industry is crucial to the US economy and jobs. Auto sales account for 21% of total retail sales so far this year. They’re up 4.5% year-over-year. New Vehicle sales in 2015 hit an all-time record, even as the rest of brick-and-mortar retail was weak.

The industry – including component makers and other suppliers – account for a good part of US manufacturing. Transporting over 17 million new vehicles a year from assembly plants or ports of entry to cities around the country is big business for struggling railroads. Transporting them from rail yards to dealer lots is big business for specialized trucking companies. They also haul millions of used vehicles every year to and from auctions where rental-car and leasing companies dispose of their vehicles. Many of the jobs across the industry pay well.

Auto sales involve services, such as finance and insurance. They’re a significant source of revenues for local and state governments. Wall Street salivates because it gets to extract fees during many stages of the process – particularly in financing these sales and then securitizing the loans.

And all of it has been booming for years!

But if the flow of money slows, the entire growth machine starts grinding down. Pressures are already building up – and far beyond subprime auto loans.

The New York Fed’s Household Debt and Credit Report, released today, shows that total household indebtedness rose 1.1% over the first quarter, to $12.25 trillion, just 3.3% below the peak of the last credit bubble in Q3 2008 that blew up with spectacular fanfare.

But this time the distribution is different: housing debt is lagging behind (due to the presence of institutional and foreign investors), but non-housing debt has jumped far ahead, led by student loans, which more than doubled since the Financial Crisis to $1.26 trillion, and auto loans which soared 29% to an all-time high of $1.07 trillion.

While overall “serious delinquency” rates (90+ days delinquent) improved a bit, they have begun to deteriorate for the $1.07 trillion in auto loans.

At 3.5% of outstanding auto loan balances, serious delinquencies are still way below their peak of 5.3% in Q4 2010 when the employment fiasco was coming to full fruition. But during the prior recovery leading up to Q2 2007, they ran between 2% and 2.5%. So already, consumers are more stressed with their auto loans than they were during the prior recovery. And these are the good times, with interest rates at historic lows!

The higher delinquency rate today compared to the prior recovery shows that the auto boom over the past few years was obtained by pushing auto loans to the max.

Regulators have been publicly fretting about auto loans, including the Office of the Comptroller of the Currency. In its most recent Semiannual Risk Perspective, released last fall, the banking regulator warned:

Underwriting practices and weak loan structures in auto lending are most concerning in banks with high concentrations of auto loans. Strong auto loan growth alone does not pose systemic risk; however, the level of concentrations and rate of growth at individual banks are an increasing focus for OCC. Even as banks have increased capital levels, auto loan portfolios represent greater than 25% of capital at about 15% of banks.

OCC worries that the rapid growth of auto loan balances reflected not only booming auto sales, which wouldn’t be a problem per se, but the “extended durations of loans caused by lengthening maturity schedules” and the ever-rising loan-to-value ratios. Together, they “create a longer period of time banks and consumers are in a negative equity position.”

Consumers with a 60-month loan are on average 27 months upside down. But consumers with an 84-month loan are on average 50 months upside down. And this longer period of negative equity “increases the loss exposure if a borrower defaults.”

And there’s another kink, according to OCC:

In addition to an increased exposure from lengthening terms, used-car values remain well above the historical average. The Manheim Used Vehicle Index (MUV Index) over time reflects a historic average index of 113.5, compared with a recent MUV Index of 124.3 in August 2015….

That was last fall. Used car values plunge during recessions. During the 2001 recession, the index bottomed out at 103. During the Financial Crisis, the index bottomed out at 97. Meanwhile, the index has been heading down, as OCC feared, though there was an uptick in April. It now sits at 122.8 (chart).

The Manheim Index added this comment for April:

Fundamentals suggest that the Index’s rise in April will be temporary, but they do not suggest a near-term collapse in pricing. A modest easing in wholesale pricing would not be unwelcomed by dealers, and it would not be overly painful for commercial consignors. A bigger, say 5%, decline would be harmful to both.

The OCC fretted last fall about the risks if “values revert to historical levels.” Those fears are beginning to play out. But in a recession, used car values don’t revert to historical levels. They plunge way below. And negative equity goes through the roof.

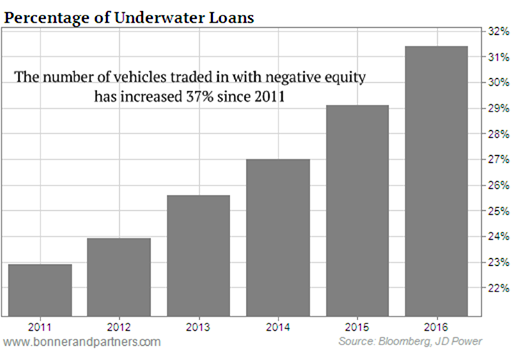

So just how big is the problem of negative equity? Since 2011, the number of vehicles traded in with negative equity has ballooned by 37%, to where underwater auto loans now afflict a record 31% of all vehicles traded in (chart by Chad Champion, analyst at Bonner & Partners):

Here’s the problem for auto sales and manufacturing: Bill wants to buy a new car. His current car has a trade-in value of $20,000. But he owes $25,000 on it because when he bought it new a few years ago, he financed it for 84 months to keep the payment down. Because he was strapped for cash, he asked the dealer to roll the amount for tag, title, and license fees into the loan, along with the $2,000 he was upside down in his trade at the time. So now that negative equity of $5,000 will have to be rolled into the new loan, along with the amount of title, taxes & license fees, dealer profit, plus some dealer fluff-and-buff….

And lenders, with the hot breath of the OCC on their necks, balk.

Bill ends up driving what he has for five more years. If enough people have to defer a purchase because lenders won’t finance their new vehicle – that’ll be a huge problem for auto sales and manufacturing!

It gets worse. Used vehicle values (trade-in values) are still historically high. But in a recession, they plunge. And Bill’s trade-in might suddenly be worth only $18,000. When that happens, negative equity skyrockets, and new vehicle sales spiral to heck.

OCC is worried about the lenders. But these lenders can strangle one of the largest sectors in US manufacturing and retail – along with all the industries and services that have spawned around it. This goes far beyond subprime. This is what happens when the good times of easy credit simply front-load sales and profits, thus paving the way for the inevitable reckoning.

Even with auto manufacturing still booming, overall manufacturing is already in trouble, and references to 2009 & the Global Financial Crisis keep popping up in the reports because that’s how bad it has gotten. Read… Manufacturing Recession Goes Global as Demand Withers

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Impressive boom to spectacular bust, this show brought to you courtesy the US FED.

From personal experience I know the only thing that makes people default on the car payment is a job loss. If the lenders were smarter, they would have a provision that allows every loan to skip 3 payments during the course of the loan. This would give people who lose a job some room to maneuver without defaulting on the loan. We had a car repossessed when we were two weeks late with a payment. If they had waited two more weeks they would have been paid.

That’s a very good idea.

that’s why it’ll never be instituted…..it’t too rational an idea!!

IIRC they used to allow you a certain number of months over the life of the loan where you could pay only the interest and not the principle and not run into default.

Maybe this was mortgages. I haven’t had a mortgage or loan payment in 23 years so I don’t know if they still do this.

WOW that’s crazy amazing, I’ve never heard of anyone having a car repossessed ever after only 2 weeks. That is totally amazing..

Who was the lender?

I’d rather not say, but DQ would not be surprised.

Starts with an S?

Uhhh……’grifter’……

I had no idea either, only 2 weeks is Gestapo. Maybe you weren’t upside down on that one….

It was a GM car, they actually did us a favor.

like I said…’grifter’…..

I don’t begrudge the bank taking back the car. But they were stupid to take it back so soon, when they would have been paid back, penalties and all.

And they let peeple stay in their homes without paying their mortgages. Maybe that’s an idea for the next time, and oh, there will be next time.

I am a vehicle lender. While it is not impossible you got repoed at 2 weeks, it is VERY unlikely your story is true. I hear this constantly and people are always very late once you see the docs.

The only realistic way you got picked up this early was you broke another contractual requirement – such as maintaining insurance – and that you had been warned if you did it again you would be picked up.

Lenders make money from the customers we don’t have to spend endless time on. A repo is the ultimate time suck and I’ve yet to see a company repo quickly without a good reason. We also lose A LOT of money if you don’t redeem and we have no idea if someone is going to get their car back.

http://www.zerohedge.com/news/2016-05-21/americas-advanced-stupid-2-stunning-charts

“The automakers, their finance divisions, and Wall Street have “sold” a new $40,000 vehicle to every Tom, Dick, and Lakesha in Amurica with subprime loans, 7 year 0% interest “deals”, and low payment leases. Now, tens of millions of these dumbasses are underwater on their auto loans. But wait. These people are so fucking stupid they NEED a new vehicle and are trading in their underwater 3 year old vehicles for another $40,000 ride. Gotta keep up with the Joneses. Just roll the old loan into the new loan and drive off the lot underwater from the get go. Simply brilliant. Meanwhile, auto loan delinquencies are soaring.”

These are the advanced problem solvers that’s better than every Chinese out there.

Muricans: PhD in Advanced Delusion is more appropriate.

The average human has never been good at math – and never will be. Humans are, essentially, the same critter for the last several thousand years (minimum). Just because we have cars (that we individually don’t know how they work) and cell phones (which we don’t individually know how they work) and heavy industries (which we don’t know individually how they work) doesn’t mean that tomorrow we will. Across the population, there are individuals that do – and they direct ones that don’t – but that isn’t the same thing as everyone knowing. Most humans are just stupid. Dumb as a box of rocks. Dull as a hammer. Sharp as a lead weight.

Give the species 100 years and it will be largely back to drag racing plow mules in the summer to survive winter or raiding the village next door due to population growth.

Regards,

Cooter

If the average human was smart, there wouldn’t be any ultra rich people. Extreme profit has always been generated on the backs of mentally or physically (i.e. you are “physically weaker” if you hold a stick, while I hold a firearm) weaker people.

The difference between the mentally weak people and the physically weak ones is that the latter usually understands the scheme against them, whereas the former don’t even bother to understand it. There are plenty of books, documentaries, articles, stories out there (the internet makes it easier than ever to find them!) that explains the scheme. And I have tried to get some people around me acquire a different perspective of the world. But sadly, most of them are too “busy” for that — they prefer watching funny videos on youtube or work harder so that they can afford that thing they don’t really need. But the worst are the ones so gullible that they are skeptical and file the idea as a conspiracy theory!

Unfortunately, it is just getting worse, i.e. people are getting dumber. The environment is conducive to create “dumber people”, i.e. uneducated, constantly distracted, consumers. They consume “news” on Facebook, they walk to work looking down to their phone, texting futility to their friends, they work more and harder so that they can consume more and keep up with the Jones, and after an exhausting day of work, they crash on the couch, enjoying cheap entertainment. Ignorance is bliss… until some major catastrophe occurs. These ignorants, as usual, will constitute the majority of the victims; the rest of them happens to be lucky enough to find themselves in the ark built by the few in the know.

I was about to write a critical analysis of your comment, but I came across this really cute cat video………….. :)

@night-train

Well, you’re not too bad since you somehow found yourself here on this site. :)

uhhh…….what were you saying………I was too busy looking at Kimmies huuuuge butt on my Ishite to groak what you just said—————————-could you repeat that…………later!

What happened to dumb as a doorknob?

Anyways, here are some of my thoughts as another packaging of the same idea.

It has to do with the bell curve.

On the one side, there is a very tiny minority of geniuses (or idiots savant, it does not matter) that can imagine things noone else can at the time. Then there is another small minority that can transform those ideas into products.

The big bulge in the bell curve are the hordes that can do nothing but use the products and as a result overpopulate the earth. They are also fondly called the sheeple.

Flatten the bell curve, and the earth would be inhabited by about one million humans, happily living in caves and totally oblivious of culture.

Shades of Alitsa Rosenbaum! What is wrong with being s consumer? There is absolutely no point to coming up with ideas for products and making them if you have nobody to buy them!

Those of us who roll over an underwater car are not as stupid as you think. When the car has a lot of miles on it and is due for major repairs, you might as well trade it in, and roll over the debt. Financially, the rolled over debt and potential repairs, will be a higher number than the rolled over amount. This is the economics of poverty. You get a new car, with a lower payment. It’s stupid not to do it.

It is stupid to buy a car (depreciating asset) on credit. Perhaps you should buy a car you can afford – for cash. Save the money you would have put towards a payment… and then buy an even nicer car…. for cash. (Rinse, repeat…)

A car is a productive item. It’s practically required to function in most parts of the country. It allows you to go to work and earn an income, buy groceries, etc. Good use of credit: you borrow money for productive purposes (such as earning an income).

So borrowing money for a car is NOT stupid. And with interest rates this low, it’s even SMART (for the consumer)!

But it may not be smart of the industry … that’s what the article is saying.

Wolf,

You are becoming my knight in shining armor, thanks again.

Shadow,

How disconnected from reality can you get. Poor people cannot save for anything. They/we live from paycheck to paycheck and pray nothing goes wrong because it could put them/us on the street.

Here are some examples of the things they/we put off because we have no money: dental work, doctor visits included needed surgeries, glasses, and even underwear. Do you honestly think we could save up for a car these days.

BTW, in the past I have purchased cars for cash, but those days are long gone.

And the productivity for the individual would be enhanced, if the depreciation were recovered. Which is can be, with a little ingenuity.

Sorry, the car is NOT a productive item, it is a luxury, a toy and form of entertainment.

A taxi, delivery truck, railroad train, barge, farm tractor, construction vehicle (etc.) are productive, their use provides a direct return. The personal driver is a non-remunerative status symbol that has to be paid for with debt, either the buyers’ debt or that of their employers (by way of the employers’ customers’ banks. You cannot pay for the car by driving it …

… multiplied times a billion cars since the end of World War Two and you might be able to see the scale of our onrushing (financial) calamity. It has cost the economy hundreds of trillions of dollars to support the non-productive autos and all the crap (big governments, militaries, real estate, operating infrastructure, fuel supply, finance, insurance) that goes with them. Most of these things aren’t productive, either, in other words, militaries (for instance) cannot retire the loans taken on to maintain them.

Nothing in nature … makes the car necessary, to go to work or otherwise. It was a plan from the beginning of the twentieth century to make over the United States into a ‘car habitat’ that would allow their smooth play and necessitate them at the same time. Humans have lived for millions of years without cars and know how:

http://www.abruzzoholidayinformation.com/casoli%20views%203.JPG

It’s called walking distance … past and future.

Petunia, you have a very valid point. Depending on the car of course. I Run an auto repair shop. I can tell you these cars made since 2007 are damn near UNfixable. The time, skill & money involved exceeds the abilities of the customer to pay, And the technicians to repair. I have always bought the type of car you would trade in, do the repairs and maintenance & get another 100K miles with no loan. But with VVT engines, and 5-6-7 speed transmissions, 15 different computer modules or more. It now cost a fortune just to fix the stupid turn signals.

Funny you should mention ‘Turn Signals’. We have an Isuzu NPR, and the left turn signals quit working. We took it to an auto/truck electrical specialty shop which diagnosed the problem as the Turn Signal Flasher.

In the process of getting to the Flasher, they damaged the dashboard and told us we would need to order the Flasher ($82) from Isuzu as it was a ‘dealer only item’. This diagnoses and advice cost $100.

Several weeks later when the Flasher arrived we returned to the shop. It didn’t solve the problem so they told us it was either the Emergency Flasher Switch or the Turn Signal Lever. That advice cost another $100.

We ended up figuring out that we could pull out the Emergency Flasher Switch, insert a jumper wire between two of its many connections, and the left turn signals would function properly.

We jerry rigged the thing to where the driver can touch the wires together when making a left turn. It’s not like at the factory, but it works and even allowed the vehicle to pass state inspection.

We hope and pray nothing new goes wrong that some wire and electrical tape can’t solve.

Especially if you are leasing a new vehicle that has an incentivized lease. The money factor in the lease is close to zero and the residual is probably $2-$3 thousand higher than the probable wholesale actual cash value at lease end. You only pay “use” tax on the gross cap cost down to the residual(state specific). In most cases, you are under the manufacture’s warranty during the lease. My wife’s vehicle smoked an ECM at 14k miles. A $2k++ thousand repair. Covered.

And it wouldn’t be covered at 14K miles on a new purchase?

My ex kind of screwed around on Nissan re her 2014 Versa. Stopped getting oil changed there- had brakes done at Midas to save $50 (brakes not a warranty item after a year or something) and yet they still replaced water pump (800) at 56K

I drive a vintage Volvo. I live on a street full of Mexican immigrants in a nice rural setting. They all have new SUV’s and trucks. I’m the only one I know driving an old car. Sometimes, I feel shame about it, but it runs great & is paid for. Looks good too, no body damage or rust. I have no idea how people afford their new cars. A student with a brand new Subaru told me her payments were $450/month and she wanted a car like mine. People don’t think about what they’re doing much, it seems. Delusional is the right word.

Hey, no worries!

These auto manufacturers just invest in Lyft, Uber ect… And presto!

New driver “Contractors” are created, to step into leased vehicles, volunteering

their Time, as nonprofits, driving trustafarian hipsters around, less their fixies, now

what could go wrong?

It’s a beautiful thing!?

yup! That is going to be one interesting thing to watch… “what could possibly go wrong?” rofl

Throw in the ‘self-driving’ car…and walaa…mayhem ensues!

It gets worse.

I took a 50% 30-yr mortgage on a property. The banks asked me if I wanted to roll in a vehicle or two.

So two brand spanking new vehicles went into the package.

I expect civilization to collapse long before the 30 year mortgage gets paid and the cars end up rusted away (in fact the only reason I took a mortgage at all is because I don’t believe I will be required to make payments for much longer….) so it’s all moot.

I suspect the central banks know what I know. So they have no problem with these loans

I think you are right. There is no way all the bad debt can be paid off and they will use NIRP to write it off on the backs of savers.

Everybody wants some, I want some too.

.

“”””” The auto industry is crucial to the US economy and jobs. “”””

Mexico as a New Capital of the Automotive Industries

Mexico is the fourth-largest exporter for the automotive industry, only after Germany, Japan and South Korea. Mexico is almost reaching Japan to become the number 2 supplier of vehicles to the U.S. market.

To support this information, in 2014, Mexico manufactured four out of every 100 cars in the world. With this speed of growth in the industry and attraction of investments, Mexico could reach the 4th position in automobile producers after China, USA and Japan.

2015 Was a Significant Year in the Automotive Sector in Mexico

The Automotive industry was “la Joya de la corona” of Mexico in 2015, with impressive numbers never seen before.

Currently, Mexico has eight automotive producers in Mexico: Ford, Chrysler, GM, VW, Toyota, Nissan, Mazda, and Honda[1].

According to Mexican Automobile Industry Association the list of vehicles destinations of Mexico’s exports in the first quarter 2015 were 70% to the United States, 1.8% to Canada, 2.6% Germany, 2.4% Brazil, 2.1% Colombia, 2% to China, 1.3% Saudi Arabia, 0.9% Argentina and 0.5% to Italy.

============================

they sold it long ago – they just did not tell anyone.

.

.

.==================================

Mexico Free Trade Agreements (FTA)

There are many reasons and qualities that Mexico provides as a great place for auto manufacturers:

Mexico is strategically located close to the U.S., Canada and Latin America (NAFTA).

The Mexican government has negotiated extensively in order to increase the list of countries that Mexico has agreements with.

An organization in Mexico called ProMexico acknowledges that Mexico can boast of a network of 13 Free Trade Agreements (FTAs) with 45 different counties where 32 of these agreements are Reciprocal Investment Promotion and Protection Agreements. There are also 33 countries involved with Mexico of which 9 have trade agreements within the framework of the Latin American Integration Association (LAIA). Mexico expects to see more partnerships with the Trans-Pacific Partnership Agreement. With that, Mexico has access to over 60 percent of the world’s GDP because of their relationships through these agreements[2].

https://tax.thomsonreuters.com/blog/onesource/mexico-as-a-new-capital-of-the-automotive-industries/

.

.

.

According to Mexican Automobile Industry Association the list of vehicles destinations of Mexico’s exports in the first quarter 2015 were 70% to the United States

.

.

.

.

FREE TRADE?

In most other nations, whth whom we signed “free trade” agreements, they are FREE to hire and fire who they want and deal will less “Anti-Free” legislation.

Can I hire who I want? No. Can I fire who I want? No. I am not free, which means MY business is not FREE and which means there is no FREE Trade. It is a joke.

What about all the regulations a US company has to endure while their competition, overseas, does NOT have to comply, yet they can import their products into America without any of the legislation that is killing America?

Free, my @$$

The main attraction of Mexico are wages about a third of US or Canada.

And you don’t have to heat the plants/buildings? The heat you use is the heat you loose.

oops, forgot a/c

Tim: when Hyundai first got serious a new hire was a Brit manager who toured the factory but said ‘where’s the heat’

Reply: first profits, then heat.

But he insisted and got (some) heat

Here in lies the fundamental flaw of our trade system … when we export manufacturing jobs to places such as Mexico we lose the purchasing power of all those people who used to have those jobs in the US. So what to do … Right! – make credit cheap and easy in the US so some working stiffs can leverage themselves even more in order to buy this shiny new car. To be sure, these people are foolish but the system relies on foolish people to go deeper into debt in order to fuel this doomed system. All pretenses of balance are out the window.

The methodical and constant hollowing of middle class wealth, or what’s left of it. Between exporting jobs and automation, profit margins grow for global corporations as the customer base is being subsidized by debt.

The logical conclusion is that the debt will not be sustainable by the customers as the source of income is constantly diminished.

Outcome: America is recalibrating its expectations to a life of lower debt. Hence the growing popularity of the younger people to a “tiny houses” and rationalizing not going to college. I guess it’s just a reversion to the mean of a standard of living in the US.

How about this idea:

If you want to sell something in America, you have to make it in America.

The cars cost less to produce in Mexico, but the price never goes down in America. Just like the pharmaceutical business. At least the Chinese pass the savings back to us.

Anybody with a pulse, and some with none, got a car loan in America. The car business can’t be expanded any more.

You could offer anybody with a pulse 2 CAR LOANS.

Combine this with WAY easier repo today (just disable the vehicle remotely and go pick it up) and you have a recipe for a collapse in used vehicle prices.

And…. there’s still that pink elephant in the room.

That hardly nobody notices!

Collateralized Loan Obligations (CLO)

Wall street has taken all those car loans and packaged them up, all wrapped really nice looking with a triple A “investment” rating and sold them over-the-counter (OTC) all around the globe.

What is an OTC CLO you might ask? Does DERIVATIVE ring a bell?

I know right?… and it’s all good…just ask B of A who’s getting off the hook for packaging billions in trashy garbage home loans in the exact same way and making them look, smell and taste good..even though they absolutely knew they were trash and the rotting stench would eventually rise to the surface.. but they didn’t care.. they even admitted it..but they’re off the hook..so all is good right?

Sigh…it’s depressing reading finance blogs. People here are the ones that want to get how things work but are still clueless. There is nothing inherently right or wrong about an OTC CLO (which is NOT a derivative btw).

If I personally sell you a $100k first position note on a $2MM house that is an OTC transaction. If I personally sell you a few of these bundled then you have an OTC CLO.

Selling loans with bad collateral is the issue.

I haven’t been in the market for a car for more than 10 years now. Are they really offering 84-month car loans nowadays? CRAZY! But then when I was shopping for a car, 48-month was the usual.

I know I’m an old fart, but my first and last car loan was for a new 1980 VW Rabbit. I put down 50% and paid it off early.

Debt is a cancer. I don’t want either.

Not necessarily.

Depends on the %. Imagine an 84 month loan at 2%. That is cheaper than a house and WAY cheaper than credit cards.

AND, if you plan to keep the car that long, if not longer, then it may be a smart move.

I keep ALL my cars for 10 years of more. Always have, always will and I’m old enough to have purchased a few. I always buy new for 2 main reasons? How was it treated before me, and I get EXACTLY what I want since I keep it a long time.

So, do the Math. Now, I realize that you can buy a really nice car about 2 years old (especially the Japanese cares, HONDA, and save on my concept, BUT, if you want what you want, it can be hard to find it.)

To some people, not having all the toys, bells & whistles (you young folk won’t understand that slang), means alot. I take a great pride in buying what I want, when I do buy.

Over my life, I have learned to work hard, think clearly and buy things that are what you want, when you buy.

84 month Auto loans. Madness.

Purchaser would be better off with a double balloon full service lease, including insurance, and registration with a wright to purchase at the end of the term. Which they generally exercise as it is worth more than the end term purchase price.

Then the lessor get to claim depreciation, purchase sales tax rebate, service costs, and primary finance costs.

Like the other man said you should only be able to get 48 as 60 is 100% depreciation. From a book point of view, after 60, a car has only residual scrap value.

d: As a young man, I traded every 3 years. Then as I got older, I realized the quality of the product was better and started keeping them until they became undependable. Now the wife and I drive a 2001 & 2002. We are ready to purchase a new vehicle and for the first time ever, I am considering leasing. Mainly, because I don’t won’t to raid my savings to the tune of a new car or to have a really high car payment for 4 years or a high payment for more than 4 years. I think I will lease something I want on a two or three year lease and see how it goes.

Night train. Don’t be a fool. You are then trading on debt which is the currency of slaves.

Banks and other financiers will also be wildly optimistic valuing lease returns. A whole lot of leasing going on and it almost took my bank under after the last party. The good news is that local auction lists are not very long (and majority clunker) so far this year. I’m driving an old lady special which I paid cash for, less than 30K miles on it, waiting for the crash when I might be able to justify trading it for something snazzier.

It won’t surprise me if the Feds repeat “cash for clunkers.” The technocrats have yet to explore all the implications of 21st century Keynesianism (Bernankeism).

Mr. Colson: “I’ve seen more of this state’s poor cowboys, miners, railroaders and Indians go broke buyin’ pickup trucks. The poor people of this state are dope fiends for pickup trucks. As soon’s they get ten cents ahead they trade in on a new pickup truck. The families, homesteads, schools, hospitals and happiness of Montana have been sold down the river to buy pickup trucks!… And there’s a sickness here worse than alcohol and dope. It is the pickup truck debt! And there’s no cure in sight.”

Movie Rancho Deluxe (1975)

THE CURE? A Newer Truck.

A newer and “BIGGER” truck !!…….VROOM,VROOM……”HEY…..LOOK AT MEEEEEEEE”

YEAH, you’ve got it !!!

Sun roof? Yep. Bluetooth, Yep…..leather, of course. Heated seats and heated steering wheel and heated vibrator, yep……..just sign here and here are the keys!!!!!!!!!!!!!!!!!!

I estimate that the average pick up in my city hasn’t had anything in the box in months. A poker buddy who has lots of bucks bought one and when he wasn’t around I tossed a bale of straw in the box- told him it was so he could pretend to be a pretend rancher.

Throw in a bale of Colorado weed……………………….

Still waiting for the recession and the Kaboom…

Even used cars are inflated… I often see a 10 year old POS car with 150K miles mazda they want 8-9K for it…. WTF

the ‘car’ is one of the those inventions in ‘progress’…..at will help to push humanity into a totally degraded biosphere…….all for the sake of CONvenience………

we diverged off a sustainable path 100 or so years ago..

WE F#CKED UP !!

Free Trade = Coming to a theater near you featuring Low Wage, no benefits and a handy community sewage pit located in your front yard where the river used to be, no more waiting lines for running water or access to sanitary pedestals. Everyone must dig their own hole or find a river somewhere to poop in.

Free Trade for Haiti, the poorest nation in the western hemisphere, or Solomon Islands or Malawi, tied for the the poorest nation in the world. Puerto Rico catching up with the Jones’.

um, strikes me used car prices have been coming down for a while.

cars aren’t houses, unless you buy……ah, wait, you can buy a good doublewide for the price of an f-150.

meanwhile, i’m on year 17 of my ride. got it used.

point of pride? not really, necessity, just don’t care.

What is the downside of leasing an auto if you have the money to pay cash, but don’t want to lower your savings by a large amount. I thought the main downside of leasing was to use it as a way to drive more car than you could afford otherwise. Your thoughts on this will be appreciated.

night train, you should read my book, TESTOSTERONE PIT, insider view on what happens in a car dealership… :-]

The big UPSIDE of leasing is that the dealer makes a huge profit and you never know because there is no purchase price to check. The leasing company also makes a big profit. That’s why the industry LOVES leasing and pushes it hard.

YOU, however, pay for this. You NEVER build up equity. You’re just renting a car. You always have to pay a lot for required insurance to protect the car (since it’s not yours). Leases with low monthly payments require a massive upfront payment (“at inception”) that you’ll never get back (read the fine print on leasing ads and pull out your calculator). And if you drive more than figured into the lease, you will have to pay a large amount when you turn the vehicle back in.

The benefit for businesses is that they easily get to write off the entire cost of the vehicle. But they get to do that with an acquired vehicle as well, it’s just a little more complicated.

True, American Auto leasing like everything else Financial in America is a huge racket.

America is promoted as a, consumer friendly place.

BIG LIE.

Wolf: Thanks for the analysis. And I do need to read your book.

This is the price for not prosecuting the Fannie Mae fraud, more of the same.

Jamie Gorelick recommended our current AG Loretta Lynch, the prior X AGs, the last 3 Supreme Court justices, and multiple senators including “R” Ted Cruz and “R” Ben Sasse.

Sub Prime cash put Obama in office.

What’s really going to sink the auto industry is self driving cars. In the city who needs to own a car with it’s expensive monthly payments, insurance costs and repair bills when you can just call up a inexpensive (since there are no drivers to pay) taxi to take you where you want to go. This will happen within 10 years with car sales dropping accordingly. And within 30 years owning a car will be as rare as owning a horse is today.

For all the abuse cars take, they have played a lifesaving role in disasters.

In Katrina many folks escaped via car. The huge fires burning now in Alberta forced 80,000 to evacuate- 90% plus by private car. There is no possibility of having this capacity to move people this fast except by private car. The density of shared cars would never be enough to move everyone at the SAME time.

Little history trivia: an odd fact about WWI is that Germany almost won in the first month and then almost won in the last 4 months. In both cases they got thirty miles from Paris and fought the first and second Battles of the Marne (the Marne is a river)

In the first one, where it looked really like it was over, the French used the taxis of Paris to move several thousand troops to a weak point. At the time it was the largest military move by motor.

The meters ran the whole time and the bills were paid.

Regardless of whatever “practical” effects owning your own car may have under what are obviously the extreme, and very rare, circumstances you mention, the reality is if given a choice many, if not most, in the city would prefer not to have the hassle of owning one. The future will tell, but I certainly wouldn’t want to hold onto auto stocks (or their suppliers) in the long term.

Interesting debate which I believe is partly existential- it’s not resolvable like a scientific question- some folks just LUV carz.

My nephew- millionaire at 30 via stock options in his employer ( Avigilon, listed on TSX) just got his FIRST car at 34.

I had been thru at least 15 by that age, so you know where I am come from.

My sister, his mum, thinks he drives like an 18 year old.

He doesn’t use car day to day- but pays 150 a month to park it!

(Vancouver, Can)

So go figure, but it’s humans, not math.

Want to see another real threat to the economy besides upside down car loans? If congress ratifies the TPP, many of those American auto industry suppliers, and the transport industry that depends on their business, will be decimated with substitution of parts from suppliers in countries like Malaysia and Viet Nam, thanks to TPP provisions that permit much higher content in American-made autos from participant countries.

So yea, it’ll be a one-two punch to jobs and the economy.

Anti TPP rubbish.

Job’s will move from china to Vietnam and Malaysia they already are.

GM is paying more tax in china 900 + Million, than it is in the US 5 Million. And making Buick’s in china to sell in AMerrica.

There are no more US supply chain Auto jobs to move GM and Chrysler moved all theirs and Ford has kept most of their in house production in the NAFTA area.

Your auto Job horse is long gone, you are a bit late to close the stable door now.

In reality you are simply hitting on TPP because its easy.

Go and buy a sack of wheat, and peck at that instead.

A reason the MUV average is up is the nightmare Cash For Clunkers program, which took the bottom out of the market. Duh! Another well-intentioned (or otherwise) liberal/left/academic notion paid for by the working poor. Fiscal conservativism is always the friend of those with the most to lose.

The same can be said for the growth in the disgraceful payday loan space, which owes so much to Dodd-Frank. It feeds upon the least among us.