Fitch Ratings is fretting about junk-bond defaults. “After five issuer defaults already this month accounting for nearly $2 billion in new volume,” Fitch now expects that the default rate will hit 3.5% by year-end, up from 2.5% to 3% a few days ago. Through September, the trailing 12-month default rate was already 2.9%.

Worse: a 4% default rate by year end is “more likely” than a 3% default rate. And it’s “set to rise further in 2016.”

In non-recessionary periods, the default rate averages 2%. During recessionary periods it averages 11%. That’s why recessions are terrifying for junk-bond holders. Junk bonds are called “junk” for a reason.

The energy and metals & mining sectors are getting there: in September, their default rates were 5% and 10% respectively. Fitch: “These sectors experienced three consecutive months with over $4 billion in defaults, a level not seen since 2009 when monthly volume in the entire market exceeded $4 billion for seven straight months.”

There is a period before default when investors are picking up on the troubles the company is having and demand higher yields in return for taking on the risks. Debt is considered “distressed,” when the spread between its yield and the yield of US Treasuries surpasses 10 percentage points.

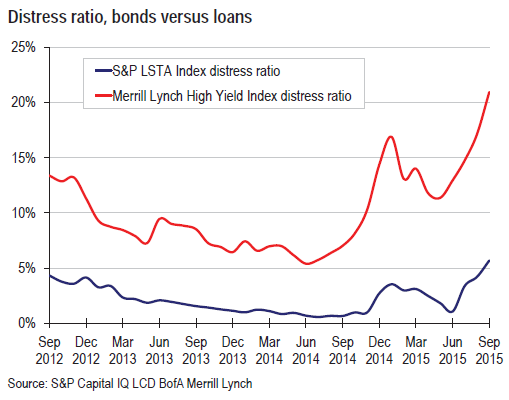

The toxic miasma of “distressed debt” is engulfing more and more junk bonds and leveraged loans. Back on September 24, Standard & Poor’s announced that the “distress ratio” for junk bonds, after rising since late last year, had hit 15.7%. It was the worst level since December 2011. It was terrible. But now, the distress ratio for junk bonds has soared to 21%.

This chart from LCD HY Weekly shows the distress ratio of junk bonds (red line) and of leveraged loans (blue line). Leveraged loans are generally secured by collateral and hold up better in bankruptcy than bonds, so their yields remain lower even if unsecured bondholders are headed for a total wipeout. Now the distress levels of both are soaring:

This has led to a peculiar situation: after a record year of junk bond issuance in 2014, and a strong beginning this year, junk bond issuance is now collapsing.

Two weeks ago, no new junk bonds were issued at all. The sole daredevil to even try, bearings manufacturer NN Inc., withdrew its offering because it couldn’t live with the yields investors demanded. S&P Capital IQ LCD described it this way:

Indeed, aside from holiday weeks and the unofficial breaks of late August and December, the new-issue market hasn’t recorded a zero US dollar supply week since the week ended February 20, 2009….

Last week, it was only slightly less terrible.

With huge media hype, Carl Icahn had earlier released his video that hammered on junk bonds. He must have been short. By Monday, the manipulative effects had worn off, and a big rally ensued. Yields fell back to where they’d been ten days earlier. And new money washed over bond funds, the first major inflow since mid-July, following relentless weekly outflows. But it wasn’t an all-clear signal. LCD:

The net inflow masks an underlying dynamic that could suggest market-timing, hedging strategies, and fast-money investors in the asset class. Indeed, the mutual fund segment was negative $675 million this past week, but it was filled in and overblown by a whopping $1.4 billion infusion to exchange-traded funds….

So there was a “bear-market rebound” early in the week. “Market participants cited short covering after the September slump,” as heavily shorted sectors, such as chemicals and energy, “notched big gains,” LCD HY Weekly reported. It was also driven by “forced buying as money flowed into the asset class.” But then it “petered out.”

So in this somewhat less terrible week, only one company was able or willing to sell new bonds: fertilizer and grass-seed specialist Scotts Miracle-Gro priced $400 million of eight-year notes (it’s also syndicating a senior secured line of credit of $1.6 billion and a term loan of $300 million). But the bonds were the first and only pricing action since September 25.

The other daredevil to try to face this market, SunOpta Foods, a supplier to the organic-foods industry, withdrew its bond offering “due to market conditions.” Pricing guidance on Tuesday had been at a 10% yield. But even that wasn’t enough to get investors interested.

Seven deals have been withdrawn from the market so far in 2015, for a total of $4.56 billion in issuance, though two of the earlier fails, Fortescue Metals and Presidio, ended up returning to the market later.

Including this meager week, year-to-date junk-bond issuance came to $225.9 billion, a 14% plunge from the same period last year.

The proceeds from junk bonds and leveraged loans are rarely invested in productive activities these days, such as adding capacity or developing new technologies. Ironically, the few sectors that were investing the proceeds in productive activities – energy and metals & mining – are in a depression and have been locked out from the junk bond market.

For the rest, junk debt is used to fund acquisitions, share buybacks, or special dividends to the company’s private equity owners (a form of financial strip-mining). But now, junk-rated companies face increasing difficulties in funding share-buybacks and M&A, two of the big powers behind inflated stock prices. Financial engineering works. But now stocks are in the process of losing that support.

It was a data set we didn’t need. Not one bit. It mauled our hopes. It mucked up our rosy scenario. Read… Last Time that Ratio Soared like this, Stocks Crashed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Excellent information as always!

My anecdotal evidence of impending recession concerns commercial leasing.

I was walking through Manhattan yesterday and noticed that the number of vacant stores for rent seemed unusually high.

Mike

It depends on the neighborhoods. Empty stores on Madison Ave. means the rich have stopped spending. On Fifth Ave. it means the tourists have stopped coming. Almost everywhere else it means the residents are staying home. The real indicator in NYC is the restaurants because everybody eats out. When they start to close en mass it is really bad.

Similarly, rents on the shopping High Street of Hong Kong have dropped 45% as shops close. But this may be a paradigm shift. Landlords refused to innovate assuming their cash inflow from rents would last a 100 generations. Then the internet happened and people no longer needed a High Street front store to sell their goods. These tollbooth capitalists with their monopoly on locations for goods trading have been handed their hats and told to keep their precious locations. Today, a little girl with a bright fashion idea and a skilled pair of hands can go direct to the consumer and bypass the parasites.

This sentence says it all and leaves on the table a question or two.

“The proceeds from junk bonds and leveraged loans are rarely invested in productive activities these days, such as adding capacity or developing new technologies.”

Instead, we have buybacks, M&As, executive salaries/bonus schemes, and dividends. On the surface it seems like everyone is simply too lazy to work anymore, and is simply looking for a scam at the expense of everyone else. All this, courtesy of ZIRP and the failure of the Bush and Obama years to prosecute banksters. Instead, these ‘exceptionals’ have been rewarded with shady opportunities and a rigged system. (Something for Nothing, but because I live in the Hamptons they call me a Job Creator. Hah!!)

I just hope ‘they’ don’t point fingers when average Joe decides it is easier to stay home from work and collect some kind of pogey. Everyone else is doing it, right? Somehow I don’t think phone calls making deals is an honest days work, no matter how many are doing it. Petraus is now a Wall Street exec. from what I hear. Says it all, doesn’t it?

And Trump, the consumate deal maker flim flam artist is going to make America great again. Right?

Oh well, when this BS all crumbles some of us will get back to work and get something done. This afternoon I should finish off a house I am working on. When I lock up I will know it was a good days work well done. And there wasn’t a junk bond or ‘investor’ in sight.

regards

Petraus is now coming out in the media to talk up ww3 with Russia. I think that may confirm your assertion, somewhat, Paulo. Congrats on the house, too.

I would like to see an autopsy on one of these defaults to see where the money actually went. I suspect it was mostly siphoned off by management as compensation. I would like to be wrong, but I doubt it.

The Mitt Romney playbook of wealth creation.

So something is now finally getting escape velocity. Too bad it is the distress ratio, defaults to follow.

“…Carl Icahn had earlier released his video that hammered on junk bonds. He must have been short. By Monday, the manipulative effects had worn off, …”

In the concealed and tortured phraseology of finance, I’ve heard this type of thing being called ‘announcement effects’. Market power is always called something else.

I don’t care for Icahn theatrical antics but he is 1 astute investment guru with track record. Saw his video as he was spot on if not early on many things including upcoming junk bond implosion.

Soon the ordinary folks and especially the yield starved retirees will learn a HARSH lesson noted on the “fine” print that they can lose their principal and yes there is no free lunch as any fund paying well above the market rate is fraught with risk of losing capital…

Demographics are still king! When you have lots of people on the cusp of retirement, or in retirement, they are busy paying off personal debt, and preserving what (little) most accumulated after a life time of working. That helps explain the lower workforce participation rate.

Junk Bond dough was rather heavy into energy (fracking), oil sands etc. was it not?

Well, we see the return there at below $50 per barrel is a loser. When whatever the investment returns less or, nothing people get fearful, rightfully. They tend to delay purchasing. Main St. suffers, be it Madison Ave, 5th Ave, or Main St. USA. Consumers have just not had ‘adequate’ raises, seniors ‘adequate COLA’s this cheapening of the indexes by government to ‘save’ their printing press $$ has been an exercise in bullshit! Wake me when the collapse begins in earnest, huh?

I’m primarily a bond investor, and I wouldn’t touch a junk deal for less than 12-15% right now. It’s just not worth it. Managements issue junk bonds mostly to pay for overvalued buyouts, special dividends, and management compensation. The proceeds are generally not used for productive activity that can generate cash flow to pay the interest and/or principal on the junk bonds.

Paulo hit the nail on the head with the comment “everyone is simply too lazy to work anymore “… I think the new paradigm for the US economy is to find scams that will succeed at flimflamming the hoi polloi out of their money.

I think third quarter earnings will be mediocre at best. If that is the case, it will be interesting to see how Wall Street justifies last week’s absurd stock rally. I know it is based on the prospect of no Fed rate hikes and more money-printing. But “moar” money-printing from central banks will not make revenues or earnings look good. Central banks don’t have enough lipstick to make this ugly pig of a world economy look good.

A report from the road. Been on a Pennsylvania to Kentucky and back track this week. Over the weekend (granted a holiday weekend, sort of) the truckstops here in PA have been jammed even in the daytime. The truckstop at Claysville (used to be a Petro) is closed now and being used for equipment storage. We are still moving but freight has too much time on it, which means the pressure is off somewhat, and they are moving loads early to keep us at least under a load. Will probably get my minimum 10,000 miles but not the 11 or 12,000 I’ve been getting of late. Saw a big sign on I-70 advertising ‘BIG SALE’ on oilfield safety equipment. Yah sure you betcha!