This solid recession indicator is starting to concern me again.

By Wolf Richter for WOLF STREET.

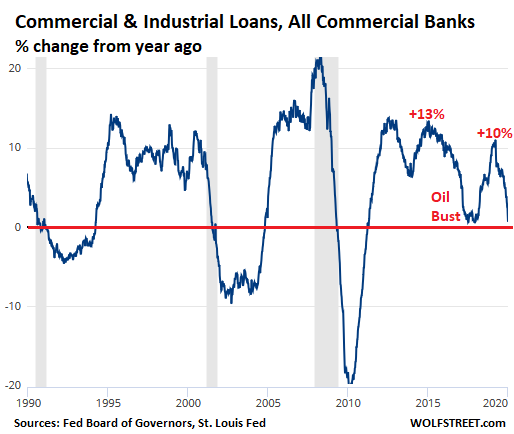

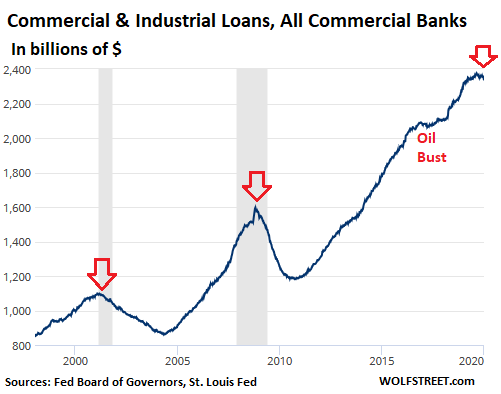

Commercial and industrial loans (C&I loans) at all commercial banks fell to $2.33 trillion as of January 1, the lowest since March 2019, according to Federal Reserve data on commercial banks, released on Friday. C&I loans peaked in August last year at $2.38 trillion and have since fallen 1.7%. This has occurred despite three rate cuts by the Fed over the period.

C&I loans are used by businesses for working capital or to finance capital expenditures. Working capital loans are usually collateralized by receivables and inventories. Capital expenditure loans are collateralized by equipment and the like.

These loans are often credit lines with floating interest rates – which are very low and very appealing for borrowers. And banks are eager to extend these loans and are offering them aggressively, even to my little company. So there is no issue at this side of the equation.

But demand from businesses for these loans is a sign of economic activity, a sign that businesses are expanding or curtailing their activities. And demand is sinking.

The chart shows the year-over-year percentage change of these loan balances. Note the relationship between the year-over-year declines (below the red line) and recessions. If loan demand suddenly bounces back over the next two or three months, I’d say the US economy has cleared this particular hurdle. But if the trend since August continues to go south and ends up in the -3% or worse neighborhood, a different scenario would emerge:

Year-over-year growth rates were in the red-hot neighborhood of 10% from late December 2018 through March 2019, then demand began to fizzle. By January 1, 2020, year-over-year growth was down to 0.6%.

The drop in 2015-2016 was associated with the Oil Bust and the industries related to oil and gas extraction, including manufacturing, trucking, and specialized segments of the tech and services sector. The balance of C&I loans dropped by $30 billion from the peak in November 2016 through March 2017, before beginning to rise again. But the growth rate never turned negative on a year-over-year basis, and a recession was averted. In 2016, GDP growth was only 1.6%, the slowest since the Financial Crisis.

Now we’re back in the same scenario, only worse: So far, loan balances have dropped by $42 billion in four months, from the peak in August 2019 through January 1, 2020.

The rekindled left-over oil bust has something to do with it, though the price of oil remains over twice as high as during the low point in 2016, and the oil bust today is not nearly as ferocious as it was back then.

Today, there are additional elements triggering the lack of demand for C&I loans, such as the broader slowdown in manufacturing and in the freight sector (outside of last-mile delivery for ecommerce). C&I loans are a broader measure of the economy, not limited to manufacturing. Many services businesses have C&I loans to fund equipment purchases or for working capital, collateralized by receivables.

C&I loans, in a growing economy, are growing at a good clip because they’re directly tied to business activity, for a broad range of businesses. And in the past, when loan demand declined significantly, a recession loomed. As for now, C&I loan balances have dropped 1.7% from the peak in August and are still up from a year ago, but barely, 0.6%. And if loan demand doesn’t bounce back soon and continues to head lower, it will be time to revive recession talk:

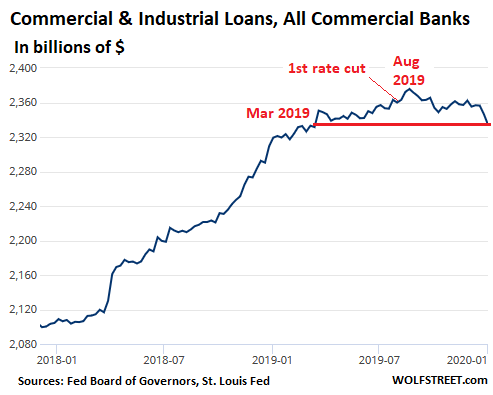

And more rate cuts won’t help in this respect. Interest rates are already low, and it’s not the cost of debt that keeps businesses from taking out C&I loans. It’s the lack of business on their part. C&I loan balances were surging in 2018 and 2019, even as interest rates were rising. But balances began to decline only weeks after the first rate cut at the end of July. This is a close-up of C&I loan balances over the past two years:

However, what happened during the Financial Crisis was special, in terms of my lifetime: Credit froze up; banks, some of which were collapsing, stopped lending; businesses stopped asking for loans; and C&I loans plunged off a cliff. This is not the scenario on the horizon at the moment.

The typical scenario would be something like in the prior two recessions where the business cycle does its thing, where a wave of business debt restructurings and bankruptcies reduce outstanding debts at the expense of investors and banks, and where businesses are hunkering down, and loan balances shrink because of declining demand, tightening credit standards, and debt restructurings.

The US economy is not there yet. C&I loans haven’t reached that stage yet, and might bounce back over the next few weeks or months. But if they continue to head south, the recession scenario is a big step closer.

Amid a shakeout among trucking companies and production cuts and layoffs among truck makers, orders for heavy trucks, which collapsed last year from the boom, refuse to bounce back. Read... Truckers Take “Wait and See Approach”: Equipment Orders, After Having Plunged, Stall at Low Levels

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Even if the US economy never officially enters a recession again, 90% of Americans will continue to become poorer as the cost of living outpaces any real wage growth. Recessions just accelerate this process. Nonetheless, the impoverishment of the country is progressing quite well during this “longest expansion” in US history. My point is, what difference does it really make if we officially enter a recession when we are all becoming poorer even when our economy is not officially contracting?

Excellent point.

I appears the oft repeated Fed scramble to avoid technically statistical “recessions” as American working living standards free fall, is just cover for permanent QE and rate suppression to benefit the ruling class at the expense of the broad majority of non rich working Americans.

real culprit is continual DEVALUATION of $dollar via govt INFLATION(ie stealing value)

wages have been stagnate since NAFTA and WTO – ie globalization of u.s. wages

never to return

and soon to make paupers out of 99%

The even greater culprit is there are only a few enormous corporation monopolies running each sector of the economy who are continually edging prices up, producing in China and cutting employees and/or their benefits for the sake of soaring stock valuations. Good luck in this micro-controlled financial slave market.

Exactly.

QE and zero interest rates have boosted some folks 401ks with very nice returns.

But. In return.

Housing is unaffordable

Property taxes are unaffordable

Medical costs are unaffordable

College costs are unaffordable

Pensions are unaffordable in a zero interest world

The net is a massive loss for poor to middle class.

Those first in line – banks, wall street houses and the uber rich make out like bandits.

And we wonder why the wealth gap is so large.

You’re starting to sound like a “socialist”, 2banana. Certainly there’s no hope for “central planning” by government to correct things. What magical solution (“Libertarianism”??) can you suggest? Everyone become engineers???

First let me say that I believe in true/classical capitalism…not this crony garbage orchestrated by the FED and it’s owners.

The solution is simple: bankruptcy instead of bailouts. Bailouts allow these zombies and vampire squids to continue. Crooks, not smart and honest people folks brought us to this point when they broke the system in 2008….seeds were laid years before. These crony crooks were bailout instead of allowing to go bankrupt. Sure there would have been pain, but now we would be truly humming. Bankruptcy is the cleansing process of true capitalism. If “you” take on too much risk and fail, then someone else gets your assets and we start fresh. With that said, I expect continued bailouts as we are seeing until the proverbial pitchforks start coming out.

The ”solution” is really very clear IMHO,,, and that is to continue to level the playing field by increasing the rate of increase of availability of communication so that everyone has the same level that JP Morgan had and better…

That would include the elimination of all of the corruption, legal and otherwise, (currently called ”crony” capitalism in the world of finance,) that obscures the gazillions of paper profits by which the rich pay their political puppets to control the rest of us.

Start education back on the path to actually educating children to think instead of simply indoctrinating them as is currently the case.

Stop, by any means necessary, the verifiable dumbing down of the population in the public schools, an easy fix by making all teachers once again the absolute arbiter of behavior in their classroom, subject only to the proviso that they do no violence, but have complete veto over presence of trouble makers as was the case when I went to public school.

Without an acknowledgement by the oligarchy, (oligarchy by birth or by crook or by honest effort makes no difference,) that they are not going to be safe behind any walls, walls of steel or electronics, etc., without at least some measure of actual equality for all, this trend, really starting from the establishment of the FED (in USA at least, much older elsewhere of course) for any wage gains by working folks to be offset quickly by inflation of money that hurts only working poor and middle classes, will continue until we do have massive death and destruction, which eventually helps no one.

It can be done, and must be done for our species to continue.

For making housing affordable again (MHAA!)

Without costing a dime in taxpayer funding.

1. Get government completely out of the mortgage loan guarantee business.

2. Get government completely out of housing lending business.

3. Enforce fraud and GAAP laws.

4. Make banks eat their bad loans.

5. Put bankers in jail, with bonus clawbacks and perp walks, for violation of fraud and GAAP laws.

6. Raise interest rates to at least nominal inflation rates (5%)

Housing will be affordable once again.

NOTE: This will not buy votes. So you can guess who might be against it.

The same solutions, with some tweaks (such as enforcing monopoly laws and forcing health care providers to publish costs), will work with college costs and medical costs.

“You’re starting to sound like a “socialist”, 2banana. Certainly there’s no hope for “central planning” by government to correct things. What magical solution (“Libertarianism”??) can you suggest? Everyone become engineers???”

A solution to the wealth gap would be a capital tax like in Switzerland.

Average Capital Tax payable on net assets in Switzerland is 0.2% per annum.

“CashBoy” solution is to tax people who do save, great idea, let’s having have a greater dis-incentive not to save, let’s tax all people who have any asset whatsoever say 1%/year, that way in 72 years in a lifetime, the 1/2 life of their family assets go to zero.

Hell let’s not save at all, lets all just go on welfare

Then we can tax say Iraq, and all us in the USA can live like kings? Right?

Money for nothing, chicks for free.

It’s inflation for young people as well as two things they need become more expensive to purchase: 1) housing and 2) 401K assets. You can see where the socialist desires come from as the current system has made getting started in life pretty tough unless they are dual income couple.

But the irony – “young people” want more of the same.

Bigger and bigger government, higher and higher taxes and more and more regulations.

And wonder where the “American Dream” went.

‘dual income’ is doing a lot of, um, ‘work’ in your comment. dual income in say, the SiliCON fortress would suffice in securing, somewhat, a reach for the brass ring of affluence … but dual incoming baristas, not so much … and there are a LOT moar baristas/bartenders/burger jockeys … with a heaping helping of teachers, and other services-related lumpen folk … then there are “coders” by far, doubling-up in rentals likes sardines, or experiancing the joys of car, and/or tent living. Yes, I’m referring to The SF Bay Area specifically, but similar could be said for the country as a w(hole). Our vaunted leaders, at the Fed, in that exclusive club known as CONgress, and in corpserate boardrooms across the land think it grand to procure billion/trillions for their socialist buds in the Big Mic, Big Ag, Big Med/Pharma/Hospital .. to name but a few big playas …. but have the gall to scream bloody redrum when the plebs want their due ! I have unsettled dreams of Citizen ( anyone remember That word ??) Militias manning lamposts !

Had some hope for ya 2B…..a couple comments back….but HN went and used the “S” word.

I’ll be investing all of my 409k money into companies that will be getting contracts to build the new government wall along the Colorado border. I will achieve financial security and the nation will finally be safe from the hoards attempting to flee from Colorado. Build the Wall! Build the Wall!

If your 409k isn’t up at least 80% this year what are you doing wrong? The market was in a big fat ugly bubble just 3 years ago but now we are in the midst of the most magnificent bull market in history, our only worry now is how to spend all of this newly accumulated fortune.

Van, you may be right.

I’ll just wait until my broker tells me to sell.

;-)

No recession means people are kept busy working. Without work, people get bored. They might get stupid ideas like another Occupy Wall Street. Better to keep them working so they don’t complain.

No recession means that successfully managing the Consumer Price and Unemployment numbers, among many others, we may never again have a recession.

I, myself, look forward to negative unemployment when everyone has three jobs reported.

You should be teaching Economics…..a great concept!

UofWS

This ‘strong economy’ data is always relying on healthcare increases….you know the thing that people cannot afford? I was watching CNN the other day about the latest jobs report and C Romans was babbling on about the numbers and said, (paraphrase) “another indicator of a booming economy, despite manufacturing being down and job losses in that sector”.

Receivables as collateral for working capital loans? I’ve seen many large companies go broke over the years and seems to me local suppliers are always the last to know. They carry the losses for awhile until accountants figure out how to get them off the books, if they can.

What collection agency will banks use, Guido’s kneecapping services?

By the way, my Uncle Guido makes an honest living…more than I can say for the FED/banksters who have brought us this mess and “booming economy”.

Based on 2008, they transfer bad debts onto one or 2 banks that will be sacrificed and a couple insurance companies get shut down. The wealthy are transferred to safe spots. the poor and the middle class lose any assets left in the bad banks. The good banks pick up those assets for next to nothing and then rinse and repeat. Wealth transfer 101 at this point.

Nice observation. Mass media has convinced the masses to follow GDP growth and stock market indicators, instead of their own savings account balances and job prospects.

The US has focused exclusively on corporate health for way too long now. At a time when corporation profits are near all-time highs and the wealth gap is highest ever, it’s time to worry about Average Joe’s financial health. Instead, we continue to push ineffective measures like interest rate repression and tax cuts for the wealthy.

Aren’t the big banks and big tech healthy enough now?

2018 operating cash flows:

Apple = $73B

Microsoft = $48B

Google = $48B

Amzn = $32B

Walmart = $27B

JP Morgan = $50B

Bank of America = $40B

And all of these profits levels are growing fast.

So we still need to baby these guys, or is it time for some tough love?

tough love … yeah, as in a shove right off the gallows …

As widespread destitution continues, and the mopes get increasingly more desperate, the above, or similar ‘remediations’ are not out of the question ! Tangentially related is the impending firearms-grab keffuffle being pushed by the weasely government honchos in the State of Virginia !

My point being the lowly plebs will eventually be pushed and streched too far. As Gerald Celente has opined .. “When the people have nothing to loose – They Lose It !!!

The modern consumer has many advantages. They live in bigger homes, travel more, entertain themselves constantly, and have access to a quality of health care that was unimaginable. Perhaps it’s wrong to concentrate on the 1% paper wealth and observe how the 99% has improved their standard of living, and not just the US but China and the EM. In the 60/70’s inflation hurt people on fixed income, probably because they had less access to credit. Wages were rising concurrent with credit availability. Taco Bell wants to pay its managers 100K. The rise in living standards will be most impressive in the lowest socioeconomic deciles. We’re all debt slaves, even the 1%.

you make some outrageous assumptions. When $100k/yr for managing a fast food drive up becomes normal an average home will still be unaffordable because it is the underlying inflation of assets that is the problem, not the wages. Most people today can’t access the miracles available in our health care system so other than for those well off, it is just a sham. As long as there is inflation, the inequality will continue to grow as will the numbers of those who can’t access that rising std of living. As for bigger homes, ask a homeless person how they are enjoying theirs? You do know that the homeless population is grown very rapidly.. because of all the benefits you speak of… going to fewer and fewer.

In California anyone who shows up in th ER of a hospital will receive whatever treatments necessary to save their lives, regardless of ability to pay. Blame the lawyers for driving up medical costs, since almost all doctors practice defensive medicine, to look good in court, even if, for practical purposes, the patient doesn’t really need the tests.

1) A larger house does not equal improved living standard, it equals more empty space to climate control. In most urban areas the land is so inflated that developers cannot build normal size houses but instead must build McMansions impractical for the typical wage earner – big improvement.

2) Access to quality healthcare is a myth. Access to more and more useless drugs is a fact. What has your “quality healthcare” achieved? The gains made from a reduction in smoking are played out and American lifespans are once again in decline.

3) Most Americans lack the qualifications to manage a Taco Bell so the advertised (but not yet materialized) $100,000/year has no significance in the larger economy.

Sorry to not go with the flo, folks, but Ambrose has a point. I bought a can of very good quality soup today at the supermarket: $1.20. I bought a very powerful, very small fully-capable computer (board, linux) for $35. This economy has its issues, and there are many of them, but it’s also producing amazing things at very low cost.

Another example: where I am, gasoline costs $2.55 per gallon. That gallon of gas can propel a 2-ton car, up and down hill and dale, for 20-some miles…for $2.55! If you’ve ever tried to push your car for 100 feet, you’ll understand how wonderful that is.

There are issues – environmental / selfish & short-sighted peple using steal-from-the-commons to enrich themselves @ expense to others (weak, unborn, etc.), but it must be emphasized that our economy is very effective in some very key/useful ways.

Let’s concentrate on fixing what’s busted (e.g. our motivations), and also on affirming the value of what we’re doing well.

An answer to your question:

1) We are all not becoming poorer.

2) Those who have or control capital will tighten their operation before or once an “official” recession develops. This would have a big effect. Not out of the woods on this for the next 6 mos. IMHO

In Europe – the Land of NIRP and QE (which includes private corporate debt) they pat the themselves on the back for avoiding official recession or negative growth. Bankers who declare they will do “whatever it takes” are made to be super hero human icons and God like figures to be admired.

Never mind they escape negative growth, because the actual positive growth they have been achieving is some like 0.000000000001% annual or something like that for many/most of them.

So there they are – these saviors Super human God like saviors of Banking policy – bragging about doing what it takes to achieve their spectacular awe inspiring 0.00000000001% annual growth as unemployment among some segments of their population approaches 50%, workers incomes fall, and the rich get richer.

And of course they couldn’t care less about that part.

When I was young, it was said the US is 30 years behind Europe. Those who decried Socialism were usually the ones who said it.

Well in terms of central banking policy, that just might be right.

Where is all this leading to? How much of this will Americans take? Or have they given up all their hope, fight and freedom?

My generation grew up during the Vietnam War and I honestly thought things would change after that. I was poor and spent my youth avoiding. Moved to Oregon away from what I thought was insanity and city life just to watch the government lie and mismanage the forests on an industrial scale.

Being poor meant I spent all my time trying to make a living. I guess everyone in their own way did something similar because the system never changed. Most of us did have the time or resources to continue the fighting.

Endless war led to endless need for other people’s money to fund them. The endless need for money led to unbelievable financialization and fraud.

How much longer can this continue? Seems forever already.

And all most of us want to do is to pursuit our own happiness. Humans are so good at believing their insanity is actually in some way beneficial.

Every wonder why legal drugs became such a problem? I alway wondered if they were purposefully sedating/killing the plebeians that weren’t up to being a cog in the system.

Purposeful or not, it definitely works exactly as you describe, and generates plenty profits, too. Every little bit helps. Lot of people that don’t fit in still out there, and I bet there are think tanks working at it.

EconMinor: It has seemed like forever, already. I’ve been reading your posts – one place and another – for years. It’s amazing how long this metastatizing (implied: cancerous) economy has lived.

But you and I are counting the years in our-lifetime-scale, and some of this stuff takes more than that time to play out. Our instincts are right, but our expectations and time-scale might not be .. um, calibrated. This is bigger than we are.

A little while ago, I decided to exit the timing-expectation business. I do what I think needs to be done, and I’ve somehow become agnostic about timing.

The one useful thing I ever heard Robert Rubin say, and I’m paraphasing, was that “you can’t predict the market. You can estimate probabilities, but not certainties”.

And with respect to coping-mechanisms…one can pursue personal happiness, and that’s great. A person could also, concurrently, build the tools and perspectives necessary to live the life your instincts tell you to live, and be happy with that (wonderful) accomplishment.

Keep up the good work, EM. You’re a good person. I (and many others, no doubt) wish you well.

Why this should be a surprise?

There are TWO Economies in USA! One for the top 10 %(may be 20%?!) another one for the rest!

The top 1% own almost of 50% and the top 10% almost of 90% wall st WEALTH! For them Life is a paradise but most of the remaining it is life barely from one pay check to another!

Unless you have a zombie business, you will probably think three times before you borrow and expand or spend on capital goods. It just ain’t New Year’s anymore and we all have a hangover.

Add to that the “Chinese” veracity of the statistics supplied by our own government, and we clearly have some interesting times ahead.

Tariffs, plane crashes, fugitive CEOs?

In 2016 though there was no recent yield curve inversion. The inversion last year in itself followed by reliable indicators like C&I loans looking to go into negative growth rates indicates to me it is more likely than not we are going into recession finally. The zombieland movie should have been about American corporations. Who wants to bet how much bbb gets downgraded to junk? Will people be shocked if they find out a significant number of the bonds in their retirement funds are junk? Does junk properly describe what the average American can afford without access to perpetual credit?

I track ~2000 mostly senior unsecured bonds underlying LQD EOD, and BB ratings are slowly creeping up going up while BBB is going down…

Everyone can track them themselves:

>> `curl -O ‘https://www.ishares.com/us/literature/holdings/ishintop-etf-early-holdings.csv’`

>> `curl -O ‘https://nga.finra.org/bondfacts/api/bond/[CUSIP]’`

current tally:

Aaa 48

Ba1 84

Baa1 330

Baa2 337

Baa3 259

N/A 47

A1 205

A3 331

A2 251

Aa1 31

Aa3 53

Aa2 65

NR 1

debt type:

S-DEB 32

1RM-BND 4

1RM-NT 1

B-BNT 6

S-NT 1822

SBN-NT 10

S-BND 3

S-BNT 11

1LN-NT 15

SSC-BND 4

UN-BND 1

SSC-NT 26

1M-BND 6

UN-NT 3

SB-BNT 2

UN-DEB 1

B-DEB 1

B-NT 24

SB-NT 70

LQD etf price at or near the top with so many BBBs waiting to be not investment grade. Guess you are paying more to get less quality.

GotCollateral – this is interesting, thanks for sharing! So, first link is to get the list of CUSIP’s, and then you run second link for each CSUIP to get data, where you are extracting (is it JSON?) keys: “credit_quality”: & “debtType”: did I get this correct?

Few questions, in document from first link many CUSIP’s are missing, so I’m assuming, those are just being skipped/ignored

Is there a limit how many requests you can make with second link so my IP don’t get banned. I’m assuming you are running it in a loop for each CUSIP per download

Increasing number of less credit worthy rankings is a concern (Baa3) since next, lower step is junk, correct?

What debt type numbers tells you? I see most of them are senior notes. What trend changes are you looking here?

I’m trying to learn some basic programming (Python) and I find this as a great learning project while trying to keep an eye on finances, so thanks again for sharing!

P.s.

Are you frequently posting these numbers on some blog/site…?

After scraping, what to do with the data? You realize the price of lower quality ratings went up? Now what to do?

in order of your questions:

>did I get this correct?

yes

>Few questions, in document from first link many CUSIP’s are missing, so I’m assuming, those are just being skipped/ignored

No, you can create CUSIP from an ISIN, they all have an ISIN: (python syntax if you use the csv lib, with DictReader) “`d[“CUSIP”] = ”.join(d[“ISIN”][2:-1])“`, the only ones that should fail are a few international ISINs against the firna api. you might get lucky with the intl ones here: http://www.boerse-berlin.com

>Is there a limit how many requests you can make with second link so my IP don’t get banned. I’m assuming you are running it in a loop for each CUSIP per download

Not that i could tell, i haven’t run into any yet and I run this everyday

>Increasing number of less credit worthy rankings is a concern (Baa3) since next, lower step is junk, correct?

Yes, Baa3 is in the BBB bucket according to moodies (which firna uses): https://en.wikipedia.org/wiki/Bond_credit_rating

>What debt type numbers tells you? I see most of them are senior notes. What trend changes are you looking here?

An unsecured note is a loan that is not secured by the issuer’s assets AKA good look getting your money back if they default and your holding the hot potato. look up “TRACE-CA-debt-web-api-Specs-v4.9.pdf” in duckduckgo on the firna website, they have definitions for all this stuff and more.

>Are you frequently posting these numbers on some blog/site…?

Not really, I just bum out here on here occasionally.

I don’t pretend to know a great deal about bonds but know an investor (CA) who does and a look at a bond rating is a step roughly equivalent to reading a listing in a real estate catalog.

He has regaled me a few times with the ‘hindsight’ downgrades: an outfit misses a payment and gets multiple downgrades the same day from the same rater.

Much more likely than any fundamental improvement in the triple- B sector justifying better ratings is increased competition for their business within the rating sector. Any savvy outfit teetering on the junk cliff is going to do careful shopping before hiring a rater.

What i typically look at are the prices changes and a current distribution from par of the underlying (which i will use to tweak option pricing models). Once in a while i’ll look the correlations between them and what actually trades on a given day, d/d downgrades and how that compares to stuff that has some threshold correlated trades over time, aggregated current value/par per company (or sector) and comparing against latest 10-q/10-k from the sec.

There was a film a few years ago called the Great Storm, basically two storms hit each other in the North Atlantic. The impression I get from the financial world today,( and most of the people who talk about it) is that they fear we are heading into a time when all the financial storms arrive at the same time and so they are tying to make as much dosh as they can now…. Interesting times

I think u mean

Perfect Storm

Book turned into a George Clooney movie

The longest expansion in U.S, history is to be followed by the longest recession?

The Fed is running out of Ammunition. Perhaps more QE but it won’t have the same effect without being able to lower interest rates in tow.

China can’t save capitalism this time around, they are spent.

Europe has a worse demographic problem than the US and Asia.

Brexit is just the start of the EU unravelling.

The gig economy is mostly smoke and mirrors.

Service economy? One Doesn’t need insurance after ones car has been repoed and house forclosed. Who can afford health care when they are unemployed?

Debt and deficit explosion. As tax revenue dry up and debt’s explode so goes the dollar.

“The longest expansion in U.S, history is to be followed by the longest recession?”

May be.

Look at the chart and see the inequality of peak in 1928 and inequality restart ca. 1978, fifty years later. The “Great depression” started in 1929.

https://20somethingfinance.com/the-top-1-percent-and-income-inequality-united-states/

” .. inequality of income peak in 1928 …”

“China can’t save capitalism this time around, they are spent.”

What does this phrase mean? If China ever saved Capitalism, (when and how did they do that), why couldn’t they do it again? And what does it mean that “they are spent”? Are they not stronger than they have ever been?

It means they “spent”’ a

Lot post 2009, and that they have maxed out on the amount of debt they can take on too. The latter years of their growth has come via massive debt.

I would think that would depend on how much debt there is,how the debt was created, how the debt is collateralized, who the debtors are, who the creditors are, what currency(ies) the debt is in, and how easily the debt could be dismissed.

If the CFOs are sour then they are going to be looking for loans https://www2.deloitte.com/us/en/pages/finance/articles/downturn-concerns-dampen-2020-revenue-earnings-investment-and-hiring-expectations.html

“The good news is that only three percent now say they expect a true recession, well down from Q1 2019. But 97 percent say a downturn has either already begun or will occur in 2020. Moreover, expectations for consumer and business spending have fallen sharply, and CFOs are less likely than last year to expect higher industry revenue and prices. And they cite much more defensive action around expenses and hiring than in Q1 2019”

should have been “aren’t”

Thanks, Lance, for the link. Everyone on this site should read it. I like his point that we should not “demonize” those who have done the best financially/economically over the last 50+ years. It’s really a problem with the system. And the system is under the control of those who have done the best, unfortunately. That needs to change and in spite of the distractions of immigration, tariffs, Roe v Wade and the rest of the sh*t that gets paraded out, we need to start thinking about campaign finance reform among other problems. Income inequality correlates to tax reduction from Reagan on. That’s the simple truth. Demonizing isn’t necessary.

Ok, y’all, you can start ranting…

Yes. Captives should never demonize their captors; much better for the captives to just take their beatings.

When is the next update scheduled for ?

I did a lot of research into Martin Zweigs trading strategies and I believe he coined the “don’t fight the fed” message. One of the cornerstones of his market timing model (aka the Supermodel) was looking at non seasonally adjusted consumer instalment debt.

I suppose C&I loans is on the same wavelength: when people start requiring loans to manage consumer instalment debt spikes (signalling recession) and when businesses stop lending and borrowing C&I drops (signalling recession)

It’s weekly, David. Every Friday afternoon around five eastern. The Fed will even send it to your inbox, I believe.

So, how do you get them to send it to your inbox?

Don, first step would be to open an account…

https://fred.stlouisfed.org/?gclid=EAIaIQobChMIreO9zsuA5wIVA77ACh1QzAj6EAAYASAAEgLtbvD_BwE

Then I believe you can subscribe to a certain feeds, with an option to be notified upon release. Not sure where they’re at on that anymore honestly, as I just check it by habit (usually) on weekends…

Actually just checked – you can do email notifications.

Thanks Wolf! I’ve been watching these numbers as well, as it’s arguably the best weekly data point for recession watchers. This week’s drop does look suspiciously like a tipping point, doesn’t it? I figured if it drops below 2.3 (even) there’s absolutely no coming back, unless it’s the first anomaly of that sort in the existing record.

The other thing about these declines is that they seem to mirror the rate of the previous rises, which suggests it may accelerate by springtime (just in time for an election cycle). I’m just astonished that you’re the only one watching this! That’s baffling, honestly. There’s only a handful of weekly releases by the Fed – none as well correlated with recessions as this one – and yet Wolfstreet is the only media outlet which seems to be keeping an eye on it. Collective cognitive dissonance, perhaps.

Keep howling, Wolf. This wacky world needs you now more than ever.

The World Bank just issued a lower world growth rate with the US a 1.8 growth rate. Larry Summer’s stagflation guess likely correct. It’s here folks. In his recent Bloomberg interview he warned of a tepid decade. Adjust your expectations accordingly.

Wolf, Steve Graves – what page you are looking at, page 2 or 4 (seasonally adjusted or not adjusted) or any other page?

Page 2, seasonally adjusted.

Thank you!

Why invest in products and services that help the peons? They don’t have any money. Their wages have been stagnant for over 40 years. The only way they can keep up is to pile on the debt.

Now, investments that screw the peons, in things they need, there’s still some money in that. Cell phones, college, health care, these things enslave them, make them profitable, at least until they can’t afford these things either.

So the real money is in financialisation, in gaming asset prices higher, paid for out of the proceeds of parasitism. Besides, economic statistics are organised in such a way that liquidating the real economy makes it look like it’s growing when it’s not. Even boarded-up brick-‘n-mortar stores are still assets on the books. And so forth.

Sarcasm off. There was a time when the activity of the financial economy was not included in GDP statistics, so as to provide an accurate picture of the real economy by distinguishing between the parasite and the host. Nowadays the statistics of the two have become so conflated that one has to do rather a lot of analytical gymnastics to get an accurate picture of the real economy, which is how Big Finance likes it. They just can help themselves while pretending to help the real economy.

The essential and best investment, very profitable, is in saving the planet and restoring what’s been lost. Sustainable too. At least it was, while it could still be saved and restored. Unfortunately all the incentives now are to do the opposite, with a bit of window dressing to make it appear otherwise. Huge opportunity, biggest ever, but that ship has sailed. Then it sank. Sorry.

The real economy sat on a wall.

The real economy had a great fall.

All the king’s tax cuts

And deregulation

Won’t get the economy

Going again.

Are FIRE (finance, Insurance and real estate) activities parasitic?

What would get the economy going again?

Maybe there is truth in “never a lender or borrower be”.

A big change has taken place during the proliferation of the credit card industry, since the early 70’s. Coincidence?

Also since the 60’s/70’s, expanded government support and backing of debt expansion — VA loans, FHA loans, Fannie Mae, Freddie Mac, Ginnie Mae, student loans, etc. Coincidence?

And of course, the larcenous FED …………….

a lot of debt slaves out there, and unfortunately their borrowing activities diminish the position of their competitors, their competitors being up and coming workers.

cb

“What would get the economy going again?”

Unfortunately:

A war followed by a rebuild would get the economy going again as well as eliminating the pension deficit.

Didn’t the Great Depression end when the USA started manufacturing war equipment for the UK with the UK gold that was sent to the USA at the start of World War 2 ?

CB, that was back when there were vast reservoirs of near surface conventional oil to tap, which provided a huge boost of activity in our post war economies.

We now have nothing that can provide such a relative infusion of almost free energy to drive increased economic activity, increased exploitation of ever more difficult resource sources and ever more complex and specialised long distance, global value chains. Today we essentially possess vastly overbuilt infrastructures, and we lack the energy to keep entropy at bay in our overly complex and large societies. Thus the decline of both physical and societal infrastructure will continue, and should accelerate when the debt bubble deflates.

The only thing that is keeping up the illusion of prosperity these days is the rapidly growing debt bubble that has motivated the exploitation of non viable energy sources based on promises of getting more back in the future. But that is showing ever more obvious signs of saturation, as ever more units of new debt are required to produce additional units of ‘growth’.

a speculation:

Well if war spending would works, it seems internal projects should work just as well. And who needs gold, when you can just print. It seems the only importance is to direct the new dollars to those who actually work and produce ,,,,, and not in finance.

The “war recovery” hasn’t worked since WWII. And it only worked then because that war was big enough to require a massive expansion of our manufacturing base. And of course the US was the only one left unscathed and standing when the war ended. None of that is going to happen in any of the Middle East conflicts or “New Cold War” proxy conflicts we might get ourselves into.

Plus, don’t forget what funds a war buildup of manufacturing: Even more debt.

All VERY good points Saltcreep…..I keep thinking back to the wrath of the gods when Prometheus stole fire. All that stuff let loose when the punishment box was opened….all that was left when it was quickly shut was Hope.

We are on our own and most are (or prefer) to remain clueless about our real physical situation.

Leader types should at least be trying (green new deal, etc), but no, they think enough money will somehow allow them to build nice safe castles again, so that’s what most do.

Financial details, although good indicators, are actually the least of our problems.

Well….. not “our’s”…more like “somebody’s”….because at 73 I’m pretty much out and done, so the least I can do is minimize my personal fight against entropy, and if that CPAP lie is true and I die in my sleep, so what?

How true: the most environmentally destructive scheme here is fully-certified ‘Green and Clean’ -same everywhere, a concept totally subverted by corporate interests.

Not unlike they did to “Organic”

Hey marketing types aren’t stupid, and who is to say they didn’t create the fad in the first place?

Most fads post 1920’s were in fact created by marketing MSM

“Marketing” is the creating a need, where sales is delivering or fulfilling the sale.

But if the ‘need’ isn’t first created then nobody knows to buy the ‘widget’/stuff

Same with ‘Green&Clean’, make it hip, then everybody wants to trade their guzzler, for a green-machine, eventually the gig is up, people realize that ‘green’ costs more, and doesn’t last as long, and ends up in the same dump. But for the corporations these fads help sell/unload junk, keep the machine wheel turning.

Who is to say the entire ‘green’ movement, even earth-first is not created by the MSM? I would argue that just about every fad on earth, has a start by some MSM source. Target kids who want to be hip, and this stuff always goes viral.

I just broke down and took a back pain pill (my ONLY reason to visit a doctor, barring unforeseen traumatic injury), I am quite capable of deciding my own health care, and still follow Biochem/Physiology, etc.

So I am less grouchy/stressed when not in pain. Thanks for doing the website (it is getting even better) and letting me put my 2 cents in, even though I am just learning financial things.

Keep it up, Unamused. I hope you’re getting through.

“The essential and best investment, very profitable, is in saving the planet and restoring what’s been lost”.

The most valuable asset we humans have is our planet and its biosphere.

To sentient beings around the globe: Take up station somewhere, and defend that ground.

Wolf, may I ask a favor? Pls forward, if you can and will, my e-mail addr to Unamused.

Thx

Thank you Tom. I appreciate that. I don’t believe WR is going to do that, but he is welcome to do so if he likes. That is up to him.

You are right to seek out people of goodwill. There are a lot of us around, and they will be easier for you to find than I am. In the end it is people who matter, family and friends.

Does this statistic report outstandings or commitments? To the extent that availability is up on committed asset-based revolvers that is a good thing…And it may be an incomplete number, missing non bank finance companies, BDCs etc. and re capex a separate rolling 24-36 month capex stat might be more informative

These are outstanding loan balances, not commitments.

problems with wordfence

What kind of problem? Is it blocking you? Giving you some kind of error message?

1) FERD : the delinquency rate LT trend is down.

2) From 6.75% in the first quarter of 1987 to a nadir of 0.73% on Q1 2015, and up to 1.13% in the latest data on Q3 2019.

3) The worse of 2009 was a spike to 4.39% on Q3 of 2009.

4) If Q1 1987 was 6.75%, 1980/82 might have been worse.

Perhaps the long downward trend is because if you’re big enough you just roll it over by borrowing more. Never pay today when you can put off paying until tomorrow. Or, from classical neo-economics “I will gladly pay you Tuesday for a hamburger today.” The wealth effect has made many very rich and very, very, very apprehensive, not necessarily in that order.

Please Wolf, we need WS shotglasses. My drinking may be about to pass from contemplation to self-medication.

You can use the mugs. Just don’t fill them up all the way. If you fill them up to the 1/3 level, you’ll be self-medicating with about 5oz :-]

The concern definitely has to do with the more broad-based nature of this move vs. the previous similar one.

The other economic indicator everyone should be watching is employment. As long as it stays strong we’re probably ok. Once it starts rolling over though… watch out! Also, given its lagging nature compared to other indicators (unemployment starts rising pretty much with the onset of a recession), by the time it starts deteriorating it means a major slowdown is already in the works.

Employers announced plans to cut 592,556 jobs from their payrolls in 2019, 10% higher than the 538,695 cuts announced in 2018. It is the highest annual total since 2015, when 598,510 cuts were announced. 2019 was the fourth-highest year for job cut announcements this decade.

Year Annual Total

2009 1,288,030

2011 606,082

2015 598,510

2019 592,556

2018 538,659

2010 529,973

2016 526,915

2012 523,362

2013 509,051

2014 483,171

2017 418,770

Source: Challenger, Gray & Christmas, Inc. ©

And if it crosses the LH threshold (see above) what then?

Way way above….

It seems likely that the uncertainty of China tariffs and the unsigned USMCA trade agreement have been a significant cloud over business decision-making regarding investment.

Hopefully we will see more CFO optimism in the next few months as we clear these two hurdles.

If C&I loans continue to contract after Phase 1 is signed and USMCA is signed then I’d say the recession fears are justified.

1) Brokers & dealers loans : $840B.

2) Market value : $25,000B.

3) Warren Buffett & friends B&H total assets : $25,000B minus $850B.

As far as I know, that C&I loan number comes from h.8 meaning it’s from BANKS. But how about business loans from NON banks. Their very competitive now and a major source of loans. They are not tied up with the same rules (eg. LCR) as banks.

Iamafan,

Yes, nonbanks have always done working capital loans that fall into the category of banks’ C&I loans. This hasn’t just happened over the last few months. These nonbanks have been a factor since Adam and Eve. But what we’re looking at here is the sudden change in C&I loans.

For example, Ford Motor Credit and the other captive finance companies of automakers have always funded their dealers’ inventories of new and used vehicles via “floorplan” lines of credit. Each individual vehicle is collateral, tracked by VIN. When a vehicle is added to inventory (for new vehicles when invoiced by the manufacturer), the amount is automatically added to the floorplan and the source of the vehicle is paid. Then when the vehicle is sold, it comes off the floorplan.

This is very efficient these days, done mostly by integrated computer systems. The collateral for floorplan is excellent and liquid: in case of default, for new vehicle floorplans, the collateral (new vehicles) can be transferred to other mostly nearby dealers at cost, with practically no loss for the lender other than perhaps transportation costs. This is why floorplan interest rates are among the lowest available for working capital loans.

The amounts are fairly large. For example, if a mid-size dealer has 200 new vehicles on the lot, at an average invoice of $30,000, this inventory is valued at $6 million. Plus that dealer’s used vehicle inventory. So for this mid-size dealer, the floorplan might be $10 million.

Banks are offering floorplan funding as well. But the captives are very aggressive, and for smaller and mid-size dealers, the captives are hard to beat. Big publicly traded dealers, such as Auto Nation, may have even cheaper options available for their floorplan that regular dealers don’t have access to.

So yes, non-banks have always played a role in C&I lending — and this market share of C&I loans doesn’t change very quickly.

What’s important here is the sudden change, over a period just a few months, from hefty growth in C&I loans to a decline in C&I loans.

wolf,

“from hefty growth in C&I loans to a decline in C&I loans.”

Maybe it is just a lag effect from when Fed tried it’s tiny tighten starting in Fall of 17 – which sent the ZIRP addicted US economy (or at least stock mkt) into cardiac arrest by the last qtr of 2018 – the Fed then panic changed course in 2019 to loosen…but that has not had enough lag time to be felt yet.

Bottom line, businesses panicked at the thought of any tiny tightening of interest rates (after a decade – really two – of ZIRP) and cut way back on any expansion plans/borrowing.

The Fed has led the nation into the Dead Zone – any move from ZIRP is going to lead to asset value implosions and 20 pct plus drops in the faux GDP souffle that DC has pumped into being.

Good point/question. Wolf, can you clarify? Because P/E firms, like Oaktree et al, make massive principle loans to start-ups and other bond-related, longer term non-bank loans.

C&I loans are secured (by collateral) loans. They’re relatively low risk. When a PE of VC firm or a hedge fund lends to a startup, there is most often no collateral, and it’s high-risk lending, often backed by equity, and that’s why startups can’t borrow from a bank. So these loans would not be in the category of C&I loans.

C&I loans are a specialized category of loans, secured by inventories, receivables, or equipment. There are many other types of loans, unsecured and secured, that are NOT C&I loans.

Wolf, is there anyone that tracks the private invoice factoring business? Not exactly floor plans, but similar?

Lisa_Hooker,

Yes, factoring of receivables is similar to a working capital loan — but it’s a VERY expensive way (and a very old way) to fund working capital, and only companies with no access to a bank line-of-credit secured by receivables would use it. Factoring and vehicle floorplans are at opposite ends of the spectrum in terms of costs of the loans.

1) FRED showing signs of weakness on consumer loans :

delinquencies on all loans & leases to consumers by all

commercial banks (ex shadow banks) :

2) Up from 5077M on Q4 1994 to a 10Y TR that lasted from Q4 1996

til Q4 2006.

3) Delinquencies JUMP above the 10Y TR in Q4 2006 to 13436M

to formed a bubble that peaked @ 39250M on Q4 2010.

4) It spiked under the 2006 level on Q2 2015 @ 12434M, forming

a Spring Board. Since 2015, in the last 5Y, the trend is clearly up

to the 21000 level

Do you happen to have link at hand for FRED delinquencies on all loans, I always get lost on that site when searching for something ;-)

Maybe there is some of this:

https://www.theinstitutionalriskanalyst.com/post/are-us-banks-facing-a-credit-trap

If repo is a problem then why expect C&I of banks to increase? Money problems maybe?

How would they hide these money problems? In subsidiaries? In the fine print? In plain sight? Deception? Prevarication?

Can you short their stock? Why or why not?

I wonder if year end window dressing causes these numbers. After all business loans are 100% in risk weightings.

I also track h.8 but prefer y-o-y comparisons to smooth out these biases.

There is one interesting ticker for playing on Mortgage delinquency rates – ASPS.

If you are shorting something, your upside is limited. Here if you go long ASPS, and if mortgage delinquency rate starts increasing, your gains can be several fold.

P.s.

Disclosure, I have a small position already, and watching now…

The foreign film “Parasite” says alot about how all of this works. In both an entertaining and frightening way.

No sign of a recession yet.

https://imarketsignals.com/wp-content/uploads/2020/01/BCI-Fig-1-1-9-2020.png

Stock market behavior since 2008 is a series of soft landings, and stock P/E ratio has rolled over again.

Still a little early.

My base case is the bull market keeps going for 2-3 more years drunk on the punch bowl.

The FED put in a huge save on par with QE3 and that save gave the markets a 3 year push.

Dow will hit 30k before any significant pull back.

Being short rarely pays off.

I don’t foresee any recession this year.

Ignore the Fed with exorbitant powers to juice the economy at your own risk.

It’s a new area, when the Fed can openly monetize government debt and buy assets at will.

Oversupply, brought on by the low cost of financing E&P is causing a drop off in the rig count which further restricts supply. At first it seemed that the sector had to bottom out completely before prices would rise, but it appears they are rising now in anticipation. There is also the matter of China buying 100M BBLs a month. They would prefer to buy from Iran, which is under US sanctions. When oil prices fall in half, investment and jobs go south, and there is your recession, or worse. The two best solutions politically are to raise interest rates, start a war, or both.

Bank Credit and C&I compared:

https://fred.stlouisfed.org/graph/fredgraph.png?g=pTXT

We had a serious decline of Bank Credit during the GFC from 2008-10.

But Bank Credit has always usually gone up.

The interesting thing is C&I looks like it has peaked or is taking a nap.

This is an election year, so I expect some pumping by the Fed.

In the last few years, Commercial and industrial loans has been around 23-24% of Loans and leases in bank credit (8) in h.8 .

Overall, Bank credit itself and Loans and leases in bank credit have been increasing yearly. I am not sure we need to get worried, yet.

Iamafan,

You knew this would be coming:

Note that in the chart you linked, total bank credit (blue line, left scale) includes C&I loans. So:

In your chart, during the 2001 recession, total bank credit just flattened out or rose slowly (hard to tell from the chart) but didn’t decline. But C&I loans dropped sharply. This means that bank credit without C&I loans continued to rise.

During the Great Recession and financial crisis, the data of total bank credit, as you can see in your chart by the huge straight line up in the last week of March 2010, was adjusted in a massive way.

Between Oct 2008 (peak) and June 2011 (post adjustment bottom), total bank credit dropped by $522 billion. Over the same period, C&I loans dropped by $357 billion. So Bank credit without C&I loans dropped $165 billion.

Turns out, in all recent recessions it took the Financial Crisis to get “total bank credit minus C&I loans” to drop at all. During the prior recessions, total bank credit minus C&I loans just flattened out or kept rising. Here is the chart for that, covering the past three recessions (note the big adjustment in March 2010):

In other words, if you remove C&I loans from total bank credit, during past recessions, bank credit without C&I loans continued to rise. The only exception was once when the banking system was about to collapse.

So total bank credit doesn’t indicate anything in terms of a recession. It’s the C&I component that does. And so you might as well look at C&I loans as a separate item.

I Agree.

Actually the last two recessions were accompanied by year-over-year negative growth of C&I loans, despite sometimes growth of total bank credit. This happened in 2001-03 and 2009-2010. Usually the growth in the year following the recession is very weak (like 1% from an already negative growth number).

2009 was particularly severe because we had declines in Assets, Bank Credit, Securities in Bank Credit, and C&I. There was no growth in Real Estate loans either.

While 2017 and 2019 C&I loan growth was very weak (0 and +3%, respectively) it was also accompanied by only a 1% very weak growth of Total bank assets in 2018. Total Loans and Leases also registered a -1% decrease for 2017. Cash Assets (which were very high right after the crisis) fell -19 and -15% repsectively for 2018 and 2019.

The effect of Q.E. was only felt for C&I in 2012, 2014 and 2015 were it grew 11 to 13% (I guess that was mainly fracking in the oil patch). The real effect of QE was seen in the massive increase of Gov’t Securities Holdings and Cash by the banks. They far outweighed the growth of Loans and Leases in bank credit. That is why you are seeing the stagnation in Main Street.

Pray that we don’t see a decline of year over year in C&I.

We need a massive Fiscal Stimulus that will help Main Street directly.

How can we get some stimulus to Main Street without using helicopters?

I saw (on local Ch 10 news) REAL helicopter money once.

The merchants of East Bakersfield CA, once the center of town, (where the road from Tehachapi came in) but now pretty much a poverty area, decided to try to boost business by dropping thousands of ping pong balls, most empty, but a lot containing various amounts of specific store credits and even a few with cash prizes. Credits and cash were said to go up to $100, maybe some with more (can’t recall, was in grammar school, but it was definitely BIG money at the time). All promoted in advance. Us kids begged for rides over there that Saturday AM but parents wisely nixed it. Anyway, as you would guess it was a blood bath and I’m sure someone got in trouble for it.

1) Boing became market makers king. Market makers own a lot of

Boing inventory, making a lot of money. Boing in the sky with Dia…

2) Until market makers clear inventory from the shelves, BA will float in the air.

3) Media help a lot, thats their job & gov pump tons of military orders.

4) Boing inventory is so big, it takes time to unload ==> on u mr. Momeno mori.

5) The repo market GRUDGINGLY accept low quality collateral.

6) When the DOW will turn down, collateral will become junk (besides fake collateral)

7) What was accepted yesterday, will not be accepted tomorrow.

8) That’s how the market got clogged in 2008.

9) The plumber….

It looks like as the bank reserves go down, C&I loans become lukewarm.

Talk about liquidity pumps.

https://fred.stlouisfed.org/graph/fredgraph.png?g=pTY7

Solution is more money printing. Beware what you ask for.

I think, regardless of what Powell has said, we are looking at future lower rates because of the debt overhang. As a saver, I’m screwed.

One stocktwitter comment said the REPO crisis is JPM balking at reserve requirements and rules post 2008. (They want the rules changed and they will probably get their wish.) The reason for reserves ostensibly is absurd, a run on the bank circa 29′. In that case the Fed prints money, or simply types the numbers in a computer. (Which is what they are doing, while not even a shadow of a banking event is evident.) Did the 2008 rules serve to firewall investment banks from deposit accounts, and are banks being crybabies while the markets melt up and the asset inflation bubble goes parabolic? Do they believe the rules mean they are missing out? Or is JPM givng FED blowback for walking back the rate hikes and prematurely ending a return to a normal yield curve? The chain of command is Prez>SecT>FedCh>Jamie Dimon. All weak links, when the crisis manifests.

The REPO ‘Crisis” was because the rates jumped from 1% to 10%

The FED of course had to flood real-cash into the pool, as the people holding cash, wanted a real return for their risk.

This gorilla will return, if the FED really once again steps back.

Yes, the JPM was the principal party that popped the rate.

Certainly rates should be higher, good money should cost, and not be free, but the FED steps in with more bad-money, at nearly free rates

Unless the FED permanently steps in with cheap money forever, why will this not happen again?

Also last time it was largely FED owned REIT companys that were flipping the cash, which is needed to rollover deals, again the FED couldn’t tolerate their low-interest world to blowup.

Has anything changed? NO

I want to see interest rates float free to their real value, tired of 1% returns on cash :(

It’s a fragile system, but like everything the GOV has to step in and ‘fix’ and always make it worse. Problem now of course is that everybody wants the ‘fix’, so it never comes clean, just gets worse, and worse, and worse … until there is nobody there to provide free cheap cash

C&I loans to build massive rental units based on unsustainable rent rates.

As I drive about Utah the only industry I see being built is rental and residential housing. No sustainable business, no industry is being created just unsustainable housing…

The problem I see is that there is no supporting industries to support the inevitable decline in home building. Mortgage brokers, loan officers, RE agents can’t simply migrate to Home Depot or Amazon to sustain their expected incomes…

I would love to see a report on the breakdown of where C&I Loans are actually being spent. If it is all housing related then it is an eventual bust.

That’s CRE loans not C&I. But, I share your opinion on these white elephants.

Real estate loans are like the eveready rabbit. EXCEPT for 2009, you’ll see y-o-y growth.

It is inevitable that bad decisions and behavior will accompany overly easy credit. It is known as moral hazard. C&I loans are no different. Easy money always encourages mal-investment, embezzlement, and over confidence and spending.

Economic recessions happen as a result of unsustainable debt levels.

Debt can only be repaid when it is carefully and intelligently invested to ensure organic growth and productivity.

Commercial loan delinquencies are low MRQ. This is not a recession. The expansion rolls on.

Are you sure that the reduction in loans is due to lack of demand for loans by companies and not the case that banks do not want to risk lending?

cheap loans have been mainly buying stock, maybe that gig has run its course??

cheap easy money, made sense to buy-back stock, and make stock-holders richer, but how long could that artificial scam have lasted?

Cashboy, Seems to me that your two options amount to the same thing. There’s always someone willing to borrow, but unless they look like they can pay the loan back, banks aren’t supposed to lend to them. In honest times they don’t and are limited entirely by the number of financially sound borrowers willing to borrow. That’s why making sure that banks have plenty of capital is not as stimulative as we might expect – like pushing with a rope.

Some participants are “managing” the income on valuations. Cap rates are so low that deals are more difficult to DSCR, so while the value may provide adequate LTV, the deals don’t “debt service.” You now have almost 10 years w/o any pain and no one went to jail last time. The crooks and scammers have profited greatly and are again running some of the asylums. Its discouraging and worse all the loan officers and the like that have come up in the ranks over the past year have never seen a “no bid” market. The last time I felt this way I took revenge shorting WAMU. The MFD market has been on fire for many years. Young apt brokers have entered the biz and become FI on this cycle alone. What is tad different this time is that many of the solid participants are older and being forced out and afraid to speak up lest they get booted. I can say from my view that deal flow has slowed and the property quality is generally skankier. As a result, there is more pressure to close deals and maintain “relationships.” Over the past 20 years or so, whistleblowers and dissenting voices have been marginalized or crushed and since there seems to be no repercussions, more and more are toeing the line.

A bit off topic but very interesting news.

Fed Pays $54.9 Billion to Treasury. Just unbelievable craziness.

https://bankingjournal.aba.com/2020/01/fed-pays-54-9-billion-to-treasury/

Looking at that link; this is what was shocking:

The Federal Reserve System paid $54.9 billion out of its annual net income to the U.S. Treasury

Dividend payments to Federal Reserve member banks totaled $714 million.

Any idea how much the member banks have in the share capital?

Maybe Donald Trump should Nationalise the Federal Reserve.

I thought, in effect, the Federal Reserve had bailed out the banks in 2008.

Honestly I think we need a good old fashioned mild cyclical recession to flush out some of these bad loans and bad companies. Maybe mixed with some good old fashioned Teddy Roosevelt style Monopoly busting for good measure.

My concern is that there is so much junk in the attic that where we would normally flush bad loans and companies out every 3 or 4 years to keep markets clear, a significant downturn could start an avalanche of zombie companies and ones that would immediately go DOA.

Nothing has been cleaned out in a decade that saw plenty of unicorn investing by hedge funds and tech capital el jefes.

The Fed has poured in so much counterfeit paper that when it comes, the downturn is going to clamp on to the economy like a pair of vice grips.

just remember the government’s the biggest borrower. If interest rates were to ever normalize deficits would explode. Then the government would have to be like Japan and buy all of the long bonds. This is going to come down to confidence in government . This recovery is now going on 11 years. It’s going to roll over at some point. I think this C&I indicator is as good as any. Thanks Wolf!

Breamrod,

“If interest rates were to ever normalize deficits would explode.”

This is badly underappreciated – at 100 pct debt to GDP, each 1 pct hike in interest rates (and the US is at least 4 pct below normal interest rates), requires a 1 pct hike in GDP if the debt to GDP ratio is not to get *worse*.

So instead of 2 to 3 pct GDP growth (which has been about the best the US could hope for), the US would need 6 to 7 pct growth (which the US has not hit in decades) – otherwise the gvt debt problem automatically gets worse and heads into a death spiral.

So the US gvt will never voluntarily allow interest rates to rise again – the dollar isn’t dying…it is dead. Murdered by decades of government shittiness.

The Fed will print however much money is required to keep interest rates from ever rising again – otherwise the gvt will die.

Money printing (known as forgery if citizens do it instead of our gvt betters) converts the gvt’s huge debt problem into its citizens’ huge inflation problem.

Therefore the US gvt will enthusiastically do it.

It is basically like playing Monopoly with a criminal sociopath.

This is one of the more succinct and accurate reports of our collective situation I’ve read. Well done.

One of the interesting quotes I’ve read recently in the fin press was the remark by Ms. Legarde when she said:

“We Should Be Happier To Have A Job Than To Have Savings”.

She has a good point. Now , all you armchair econs, pls explain how you’re going to give Mr. Detroit his good job back.

Till you work that out, we get Central Bank’s hand on the scale. and when that doesn’t work anymore, they’ll come up with another Twist. It’s what they do, and it needs doing.

Back to you, Cas127. Are you ready to report on the Path Out for the plebes? This is a respectful question, not snarky. You’ve got the chops to ID the problem, so likely you can noodle it enough to gen up some possibles for solution.

Just askin’.