Ugly trifecta that spooks the bond market. To soothe bond yields and mortgage rates, the Fed needs to hike, not “look through” inflation.

By Wolf Richter for WOLF STREET.

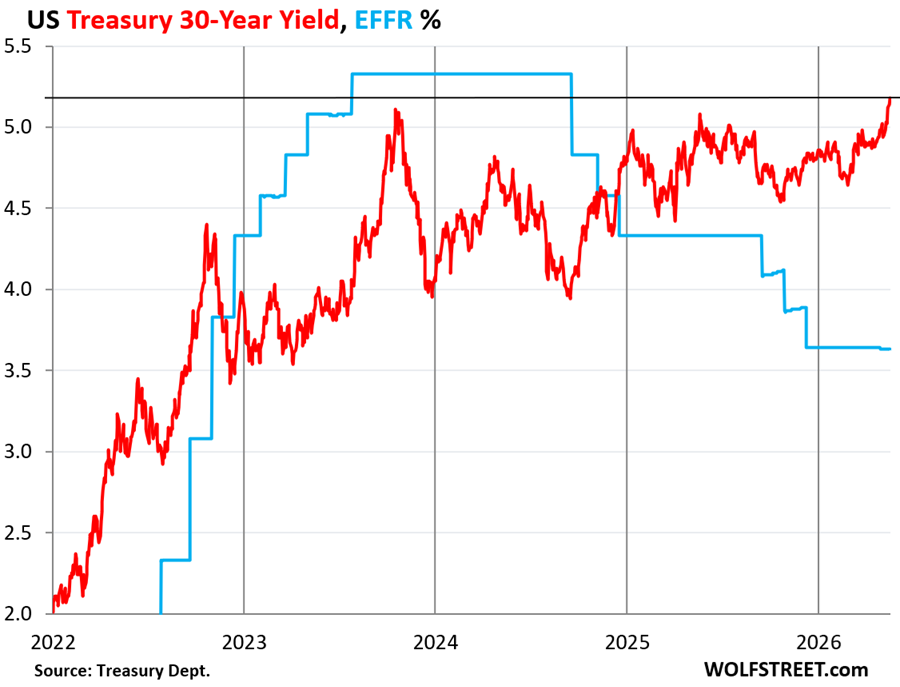

The 30-year Treasury yield rose by 5 basis points on Tuesday, and by 23 basis points over the past seven trading days, to 5.19%, the highest since June 2007. When yields rise, prices of those bonds fall, and existing bondholders take losses. It’s been a bloodbath – an orderly methodical bloodbath – in bond land.

The long-term bond market has completely blown off the Fed’s rate cuts. The more the Fed cut, the higher the 30-year yield rose: There is now a spread of 156 basis points between the 30-year Treasury yield and the Effective Federal Funds Rate (EFFR, 3.63%, blue line), which the Fed targets with its policy rates. Before the Fed started cutting rates in 2024, the 30-year yield was below the EFFR.

At the auction on Wednesday last week, the Treasury Department sold $31 billion of 30-year bonds at a yield of 5.046%, and those hapless buyers are now already substantially underwater.

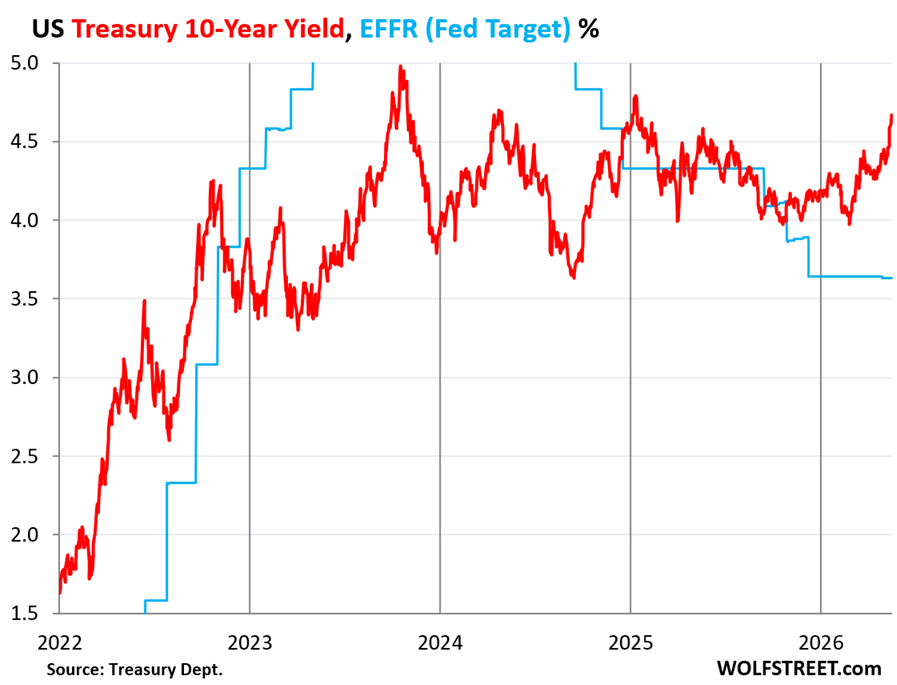

The 10-year Treasury yield rose by 6 basis points to 4.67% on Tuesday and by 29 basis points over the past seven trading days. At the end of February, it had dipped to 3.97%, and since then has risen by 70 basis points.

At the auction last week, the Treasury Department sold $52 billion of 10-year notes at a yield of 4.468%, and those buyers are now also substantially underwater.

The long-term bond market has been spooked by a trifecta of very ugly problems:

Surging inflation, with consumer-facing inflation spreading beyond gasoline into services, electricity (AI), and food, and with business-facing inflation that is now raging at 6.0%, driven by services inflation.

A lax Fed that has threatened to “look through” the surge of inflation and that is still recklessly talking about delaying rate cuts, instead of pounding home the message of multiple rate hikes. So, that raises the question: How many more mentions of rate cuts amid surging inflation can the bond market handle before the 30-year yield hits 6%?

The tsunami of new debt that the bond market has to absorb by enticing new buyers to step in with higher yields as there are no efforts underway in Congress and the White House to deal with the ballooning deficits that need to be funded with new debt. The recklessness in Washington is beyond the graspable. But the thinking is that it won’t blow up before the next election, and so no problem.

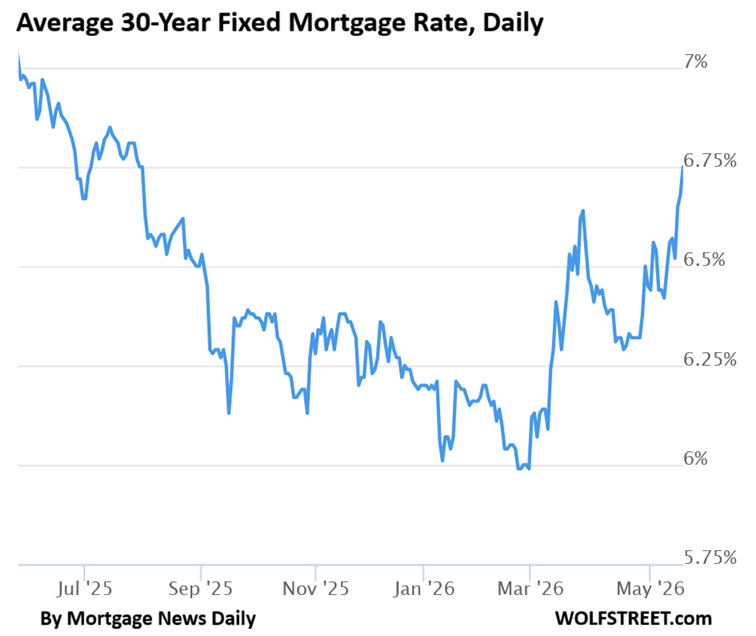

Mortgage rates, oh dear.

The 30-year fixed mortgage rate tracks the 10-year Treasury yield but is higher, and that spread varies.

The government has been trying to reduce that spread, and therefore hopefully reduce mortgage rates, by having Fannie Mae and Freddie Mac buying back their own MBS that they issued and guarantee. The idea is that the additional demand for MBS – the second-largest bond market behind the Treasury market – would reduce the yields of MBS, and therefore reduce mortgage rates.

But, but, but… To fund those purchases of MBS, Fannie and Freddie invest their cash flow from operations into MBS, instead of Treasuries, and they sell down their substantial Treasury holdings to raise the cash to buy MBS.

While the buybacks have reduced the spread between mortgage rates and the 10-year Treasury yield, the 10-year Treasury yield has shot up due to the reasons above, and… the fact that Fannie Mae and Freddie Mac, big holders of Treasuries, have now become net-sellers of Treasuries, two big institutional investors that are dumping Treasuries and are exiting the Treasury market! So the purchases may have narrowed the spread a little but pushed up the 10-year Treasury yield in the process?

And the net effect is that the average 30-year fixed mortgage rate on Tuesday rose to 6.75%, according to the daily measure of Mortgage News Daily, demolishing dreams in the real-estate industry of below-5% mortgages.

To soothe the bond market, the Fed needs to get hawkish on inflation. It needs to talk about multiple rate hikes for a couple of months, and then it needs to start hiking, and it needs to hike at every meeting, and it needs to fear inflation, not “look through” inflation. Warsh, Trump’s trusted man at the Fed, needs to get Trump on board. Voters hate, hate, hate inflation, and they have a history of throwing Presidents out over inflation. That shouldn’t be so hard to explain.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, does the old adage that the stock market falls as bond yields rise still hold true? There seems to be a view that stock market is a hedge against inflation. What is historical true and how have things changed?

One thing we know: A lot of the dynamics that held up in the past have fallen apart in this new era of craziness.