Mortgage balances barely ticked up, but HELOCs soared.

By Wolf Richter for WOLF STREET.

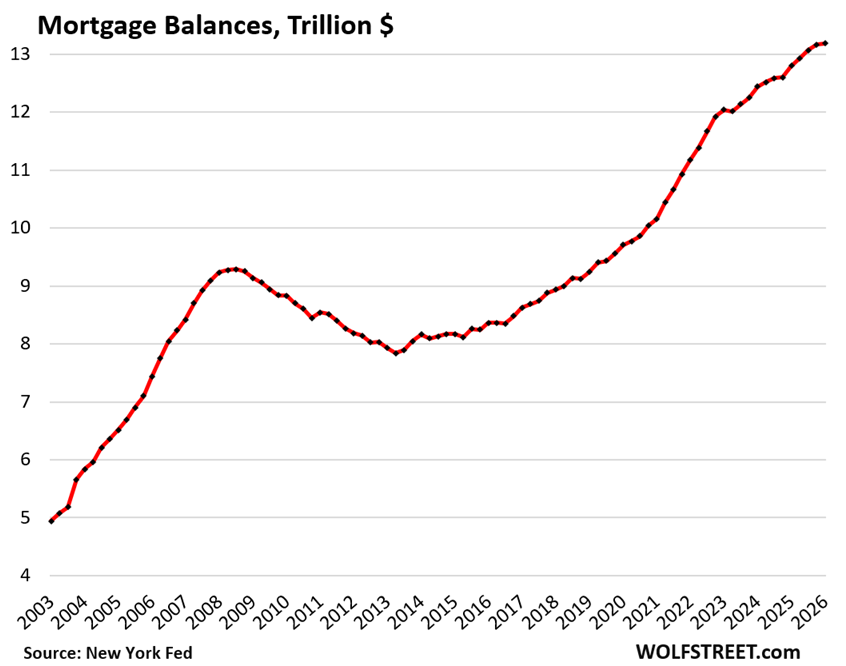

Mortgage balances barely inched up as sales of existing homes remained in the freezer and sales of new homes – while decent — occurred with big price cuts and incentives that kept a lid on the mortgages needed to finance them. And new home sales accounted for only 17% of total home sales.

But HELOC balances soared.

Mortgage balances inched up by 0.16% (by $21 billion) in Q1 from Q4, to $13.19 trillion, according to the Household Debt and Credit Report from the New York Fed, which obtained this data via its partnership with Equifax. Year-over-year, mortgage balances rose by $387 billion (+3.0%).

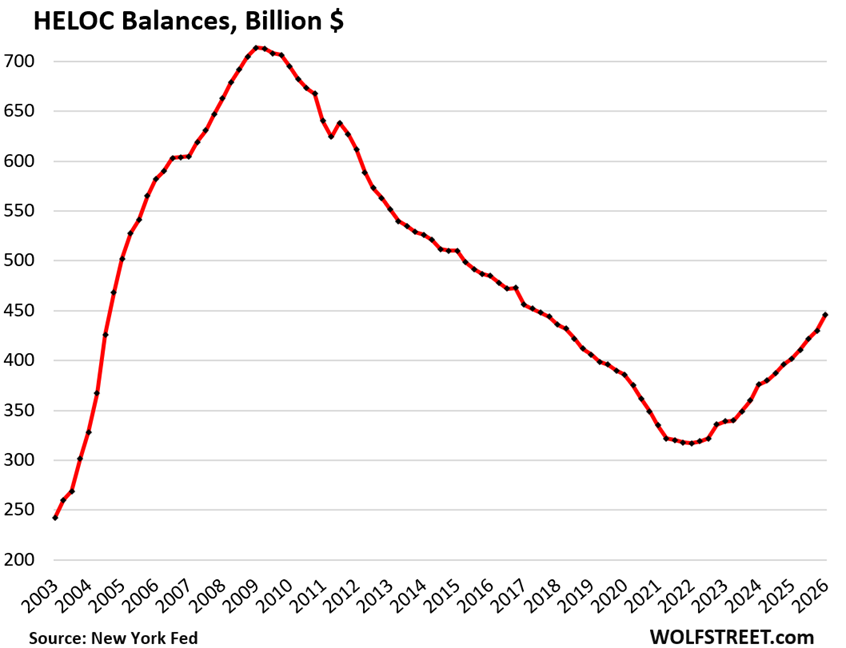

Here come the HELOCs: +41% since Q1 2021.

Balances of Home Equity Lines of Credit spiked by 3.7% in Q1 from Q4, and by 10.9% year-over-year, to $446 billion.

Since Q1 of 2021, the low point, HELOC balances have surged by 41%.

These are actual balances drawn on HELOCs and do not include the unused portion of those lines of credit.

A HELOC is a second-lien loan on the home that increases leverage and that, if defaulted on, can lead to foreclosure and loss of the home, even if the first-lien mortgage is current, which is why HELOCs add risk to the mortgage market and did some additional damage during the Housing Bust and Mortgage Crisis.

HELOCs and mortgages grow for different reasons:

Why HELOC balances are now soaring. If homeowners want to draw cash out of the home’s equity, thereby adding leverage to the home, they have to choose between refinancing the existing 3% mortgage with a larger 6% mortgage; or keeping the 3% mortgage and adding a much smaller HELOC at 8% or 9%. And that math has been tilting in favor of HELOCs for more and more homeowners, and HELOC balances have surged.

Why mortgage balances are still rising though sales of existing homes are in the freezer:

- Growth of the housing stock: buyer finances the purchase of a newly constructed home, and no mortgage gets paid off, and the total outstanding balance increases by the mortgage.

- Reshuffling the existing housing stock: Buyer of an existing home gets a big new mortgage to finance the purchase, while seller had only a small or no mortgage (40% of the homes are owned without mortgage) to pay off. And the total increases by the difference between the new mortgage and the payoff, if any.

- Increasing leverage: Homeowner cash-out refinances an existing mortgage, ending up with a larger mortgage on the same home. And the total increases by the difference of the two.

But mortgage balances are reduced by the principal portion of mortgage payments and other mortgage paydowns and mortgage payoffs; and by foreclosures that cause the remaining mortgage balance to be written off after the sale of the home, which was one of the factors behind the drop in mortgage balances during the Mortgage Crisis.

Measuring the risks of default.

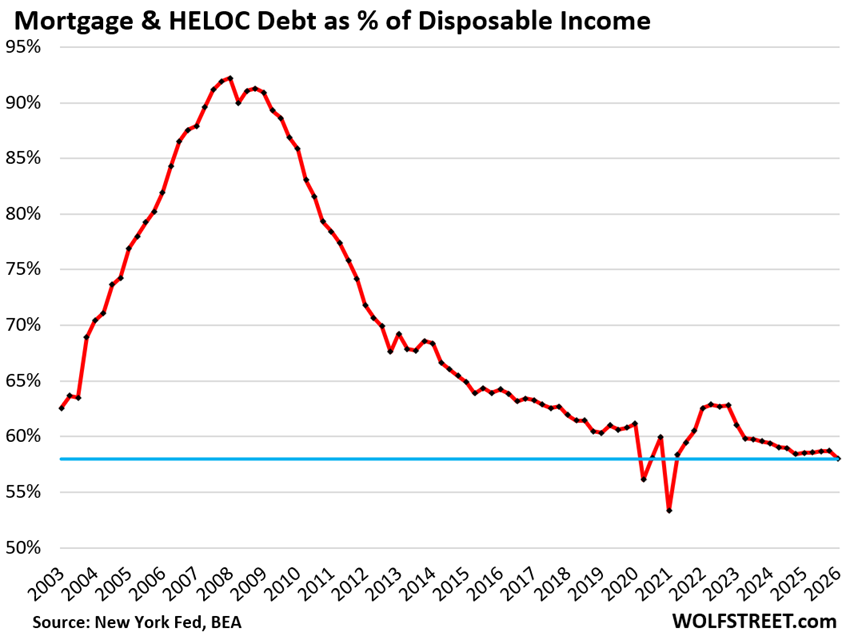

Some definitions: For this debt-to-income ratio – a standard metric to evaluate credit risk – we use “housing debt” that combines all mortgages and HELOCs. For household income, we use “disposable income” (Bureau of Economic Analysis).

Disposable income consists of after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

But it excludes capital gains, which is where the wealthy make most of their money. Excluded are thereby income from stock-based compensation plans and capital appreciation where billionaires make their billions. And this upper crust of income is excluded here and doesn’t skew the data.

The housing-debt-to-income ratio in Q1 dipped to 58.0%, the third-lowest on record, behind only the two freak quarters Q2 2020 and Q1 2021 when government payments rained down upon households and distorted disposable income out of all proportion.

The chart shows the foundation of the Mortgage Crisis: Consumers were way overleveraged with housing debt because home prices had exploded, and households kept chasing after them with ever bigger mortgages, and they made it worse by taking equity out of their homes via refis and HELOCs, and so housing-debt balances had exploded far beyond the growth of disposable incomes.

The serious delinquency rate started surging in 2007 with a lag of about two years to the debt-to-income ratio which started surging in 2005. The surging debt-to-income ratio was a warning sign – one of many – of things to come.

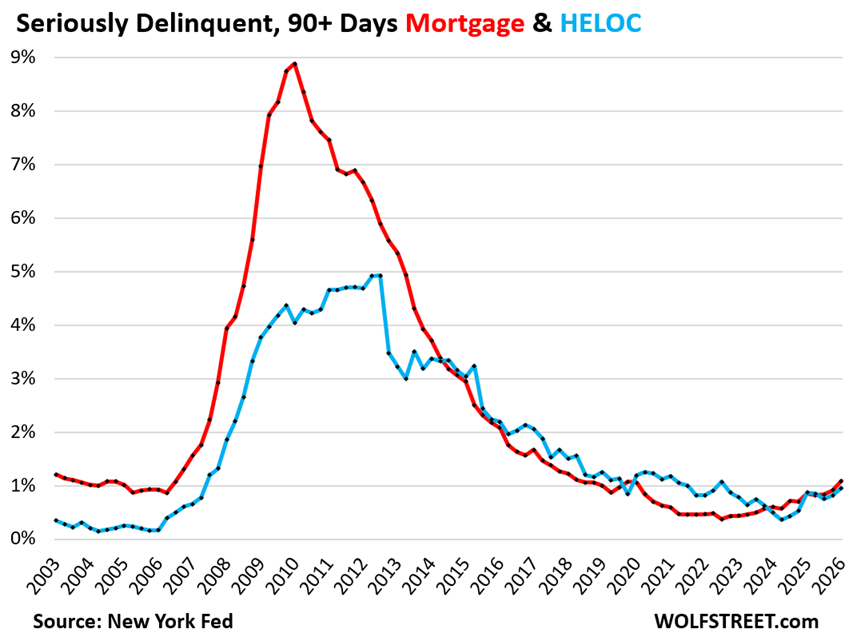

Delinquencies and foreclosures are low, in line with the low debt-to-income ratio.

The 90-plus day delinquency rate for mortgages and HELOCs edged up from the near-0% levels during the pandemic’s forbearance programs, when almost nothing counted as delinquent, but remained low in a two-decade context.

For mortgages, the 90-plus-day delinquency rate in Q1 rose to 1.09% (red in the chart below); for HELOCs it rose to 0.95% (blue). Both are roughly back where they’d been during the Good Times in 2018 and 2019.

The rates = balances of 90-plus days past due divided by total balances outstanding.

Looking forward: what could drive up delinquency rates on a large scale are the two factors that drove up delinquency rates during the Housing Bust:

- Home prices that plunge back to earth, after having exploded, when people, especially mom-and-pop landlords, including accidental landlords, strategically default on a property that would sell for far less than the outstanding mortgage balance;

- An unemployment crisis. But during the Housing Bust, the unemployment crisis started a couple of years after the Housing Bust had begun and was a result of the Financial Crisis that was in part a result of the Housing Bust.

But those two factors are not playing out on a large scale at this point.

On a micro-scale, every default has its own reasons, including a strategic default and unemployment. The legal system and lenders are equipped to deal with those, and they expect a small number of them and have built them into their business models. And so that’s not a problem for the economy until the process takes on a very large scale, as it did last time.

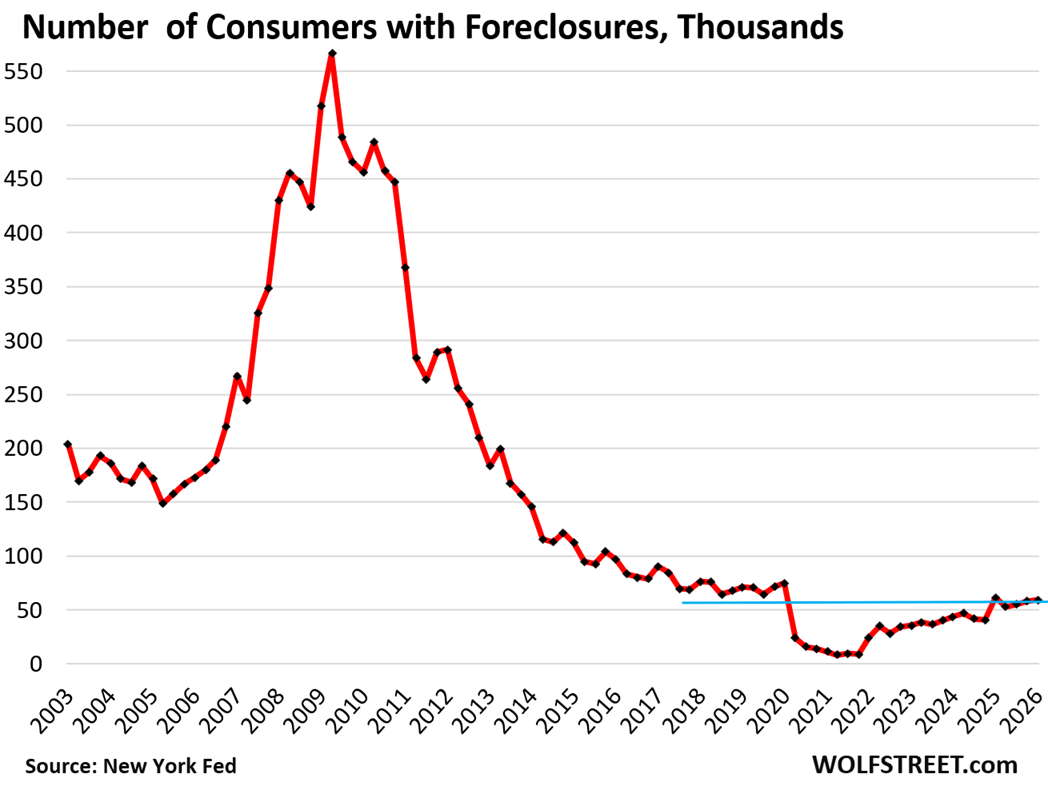

Foreclosures edged up to 59,160 consumers with foreclosures on their credit reports in Q1, but that was down by 4.1% year-over-year.

The number of foreclosures is still below the low points of the Good Times in 2018-2019, and far below those in prior years.

The increase over the past serval years comes off the near-zero levels during the era of mortgage-forbearance and foreclosure bans when foreclosures were essentially impossible.

In normal times – defined here as times without foreclosure bans and government-imposed general mortgage forbearance programs – there will always be some foreclosures.

But the surge of foreclosures that occurred during the Housing Bust won’t happen unless there is a widespread sharp decline of home prices that makes it impossible to pay off the mortgage with the proceeds from the sale of the home.

Reminder: the taxpayer is on the hook this time, not the banks.

The majority of mortgage risks, including nearly all subprime mortgages, have been transferred from banks to taxpayers – that was one of the most fundamental changes coming out of the Financial Crisis.

These mortgages are guaranteed or insured by the Government Sponsored Enterprises (GSEs such as Fannie Mae and Freddie Mac); or by government agencies, such as Ginnie Mae; or the FHA which insures subprime mortgages even with low down payments; by the VA, etc. They account for about 65% of all mortgages outstanding.

The investors are on the hook for the mortgages that didn’t qualify for government backing and that were securitized and sold as “private-label” mortgage-backed securities (MBS) to bond funds and pension funds around the world. They account for about 15% of the total.

The 4,000 banks and over 4,000 credit unions hold only about $2.7 trillion in mortgages and HELOCs (Federal Reserve data), less than 20% of the total. If there is another mortgage meltdown, banks will feel some pain, but it won’t threaten to take down the financial system, like it did last time; it will take down the taxpayer, and the taxpayers doesn’t care, that’s the tragedy.

And in case you missed it: Household Debts, Debt-to-Income Ratio, Serious Delinquencies, Foreclosures, Collections & Bankruptcies in Q1 2026

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“ Mortgage balances barely ticked up, but HELOCs soared.”

This is a sign of two things – homeowners being desperate for cash. It’s also a sign that the housing market is a ticking time b0mb. It’s going to make the housing crisis and housing crash much more severe.

I knew I shouldn’t have put that in the subtitle, because someone who didn’t bother to read the rest of the article, or prior articles, was going to spin a whole new the-consumer-is-collapsing-crisis theory out of it, and sure enough, fist one.