BOJ tries to put a floor under the yen and a lid on inflation through QT, rather than with rate hikes.

By Wolf Richter for WOLF STREET.

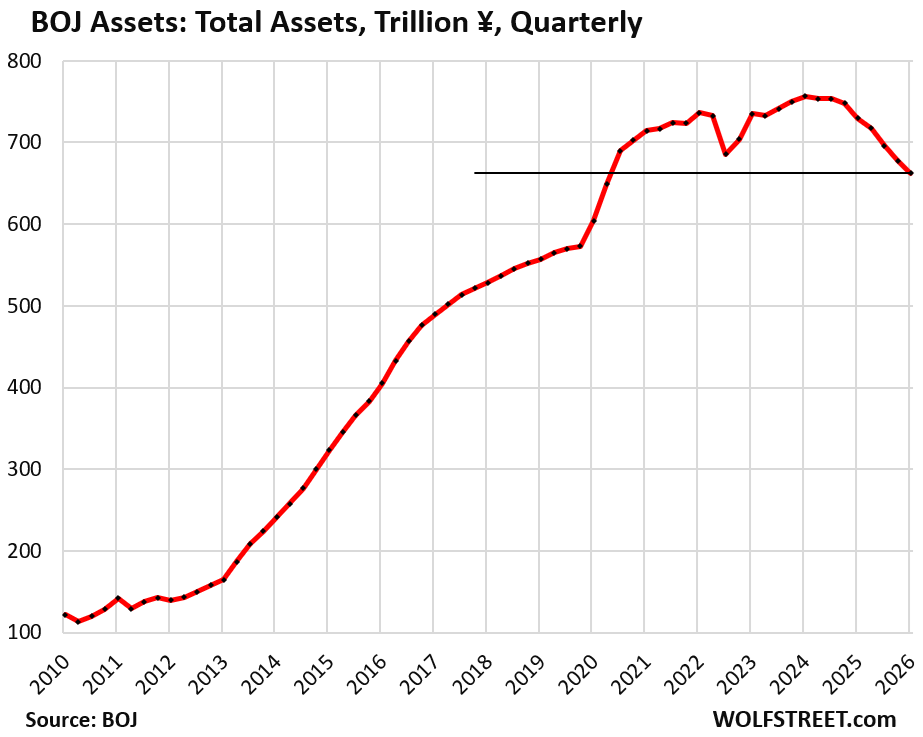

Under its QT program, the Bank of Japan reduced its total assets by another ¥15.6 trillion (-$9.8 billion) in the quarter through March 31, and by ¥67.6 trillion (-$42.3 billion) year-over-year, to ¥662.1 trillion ($4.14 trillion), the lowest level since Q2 2020, according to the BOJ’s balance sheet data on Tuesday.

Since the peak in the quarter through March 2024, the BOJ has shed ¥94.3 trillion (-$59.0 billion), or 12.6% of its total assets.

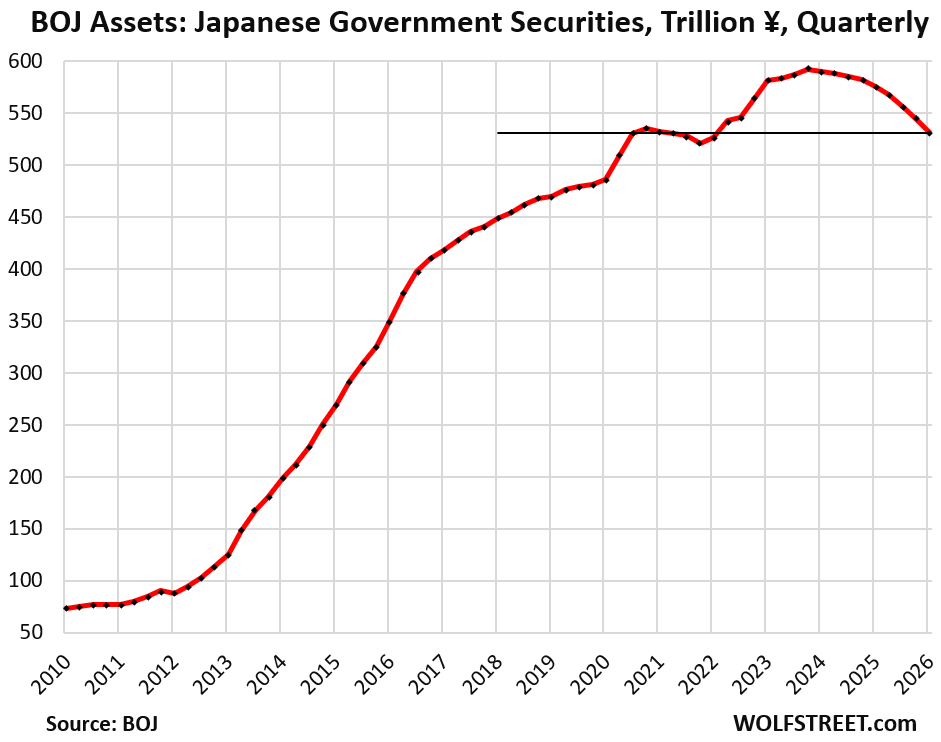

Japanese government securities on the BOJ’s balance sheet declined by ¥13.5 trillion in the quarter through March (-$8.5 billion), to ¥531 trillion ($3.32 trillion), where they’d first been in Q3 2020.

QT continued to accelerate: That quarterly decline of ¥13.5 trillion was the biggest quarterly decline yet since QT started.

All of them are Japanese government bonds (JGBs); the last Treasury bills (terms of one year or less) matured off the balance sheet last year and were not replaced.

Since the peak in 2023, holdings of Japanese government securities have dropped by ¥61.4 trillion or by 10.4%.

QT instead of bigger rate hikes. With this quantitative tightening, instead of with steeper rate hikes, the BOJ is attempting to put a floor under the yen, which has been plunging for years against the dollar.

The BOJ is also trying to deal with inflation, which rose by 3.4% in the overall economy as measured by the GDP deflator.

It has only minimally hiked its policy rates, in tiny steps spread far apart, to only 0.75% currently.

But QT has been more assertive, though with a late start. And it has allowed long-term interest rates to rise sharply: The 10-year JGB yield has soared from 0% in 2023 to over 2.4%, the highest since the 1990s. The 30-year JGB yield has soared to record highs near 4% (which I discussed here on Monday).

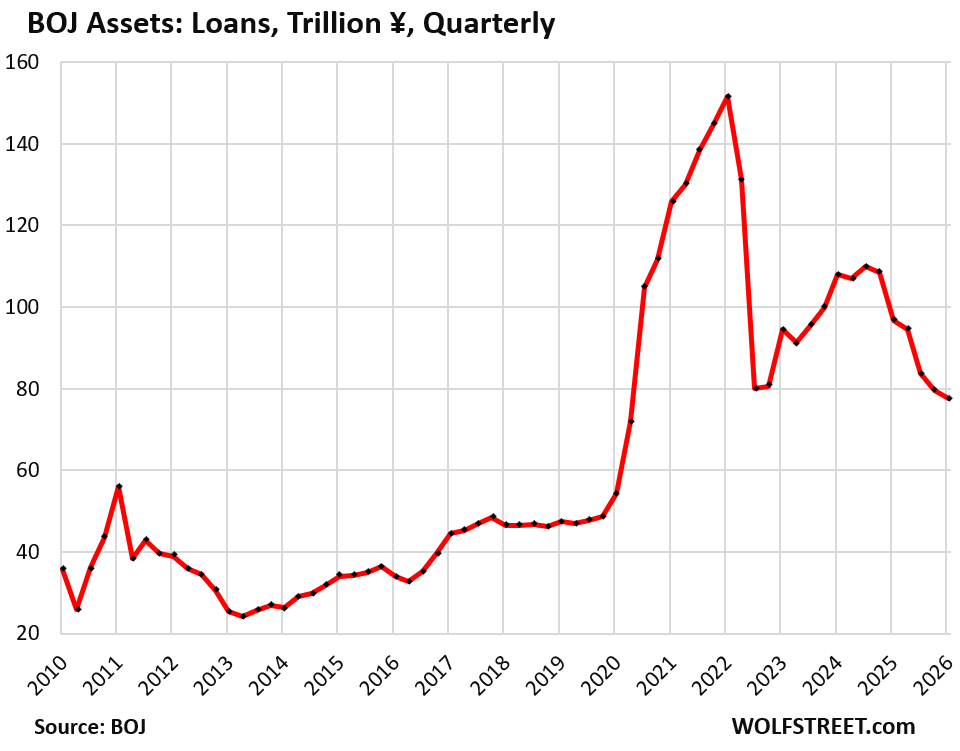

Loans declined by ¥1.8 trillion in the quarter, and by ¥19 trillion year-over-year, to ¥77.7 trillion ($486 billion).

Since the peak in Q1 2022, the outstanding loan balance has fallen by ¥74.0 trillion, or by 49%.

These loans now account for 11.7% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that had caused the total amount of loans outstanding to more than triple in two years:

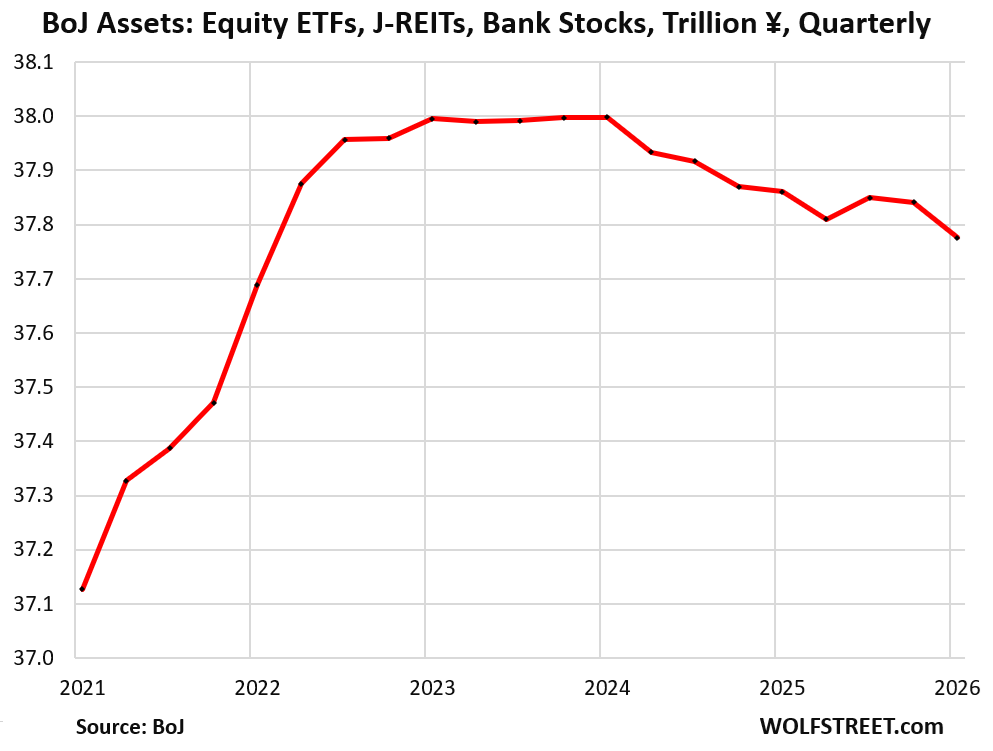

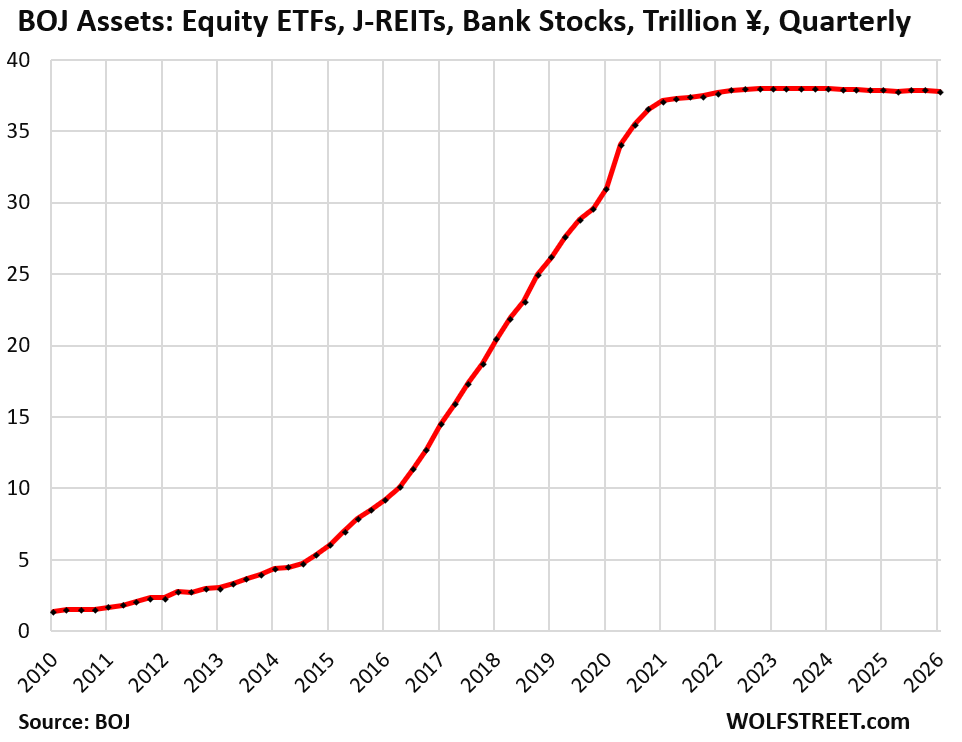

The BOJ started selling its equity ETFs and J-REITS.

The BOJ started selling its equity ETFs and J-REITS by minuscule amounts in the quarter through March, after announcing in September that it would do so, at an initial pace would be glacial: ETFs at a pace of ¥330 billion a year ($2.2 billion) and J-REITs at a pace of ¥5 billion per year ($33 million).

In Q1, it reduced its ETF and J-REIT holdings by ¥66 billion to ¥37.78 trillion ($236 billion).

But that pace of sales is faster than it seems: The BOJ carries ETFs and J-REITs at acquisition cost and has not marked them up to market since it started buying them in 2012, while the Nikkei 225 has soared by 500%.

The pace of decline is shown at acquisition cost, but market prices of its holdings are far higher, possibly two or three times higher, and in actual terms, that pace of sales at market prices is far faster than the stated sales at acquisition cost.

The BOJ sold off its last bank stocks in the September quarter. It had purchased them in the early 2000s and again in 2009-2010, and started selling them in 2016.

So the decline in the chart through the September quarter was due to the sales of its last remaining bank stocks. Sales of equity ETFs and J-REITs began in 2026.

This chart looks at the situation with a magnifying glass, or otherwise the declines wouldn’t even be visible:

In the zoomed-out version of the above chart, the declines in 2024, 2025, and in the March-quarter of 2026 are so small that the line appears nearly flat.

But these holdings account for only 5.7% of its total assets.

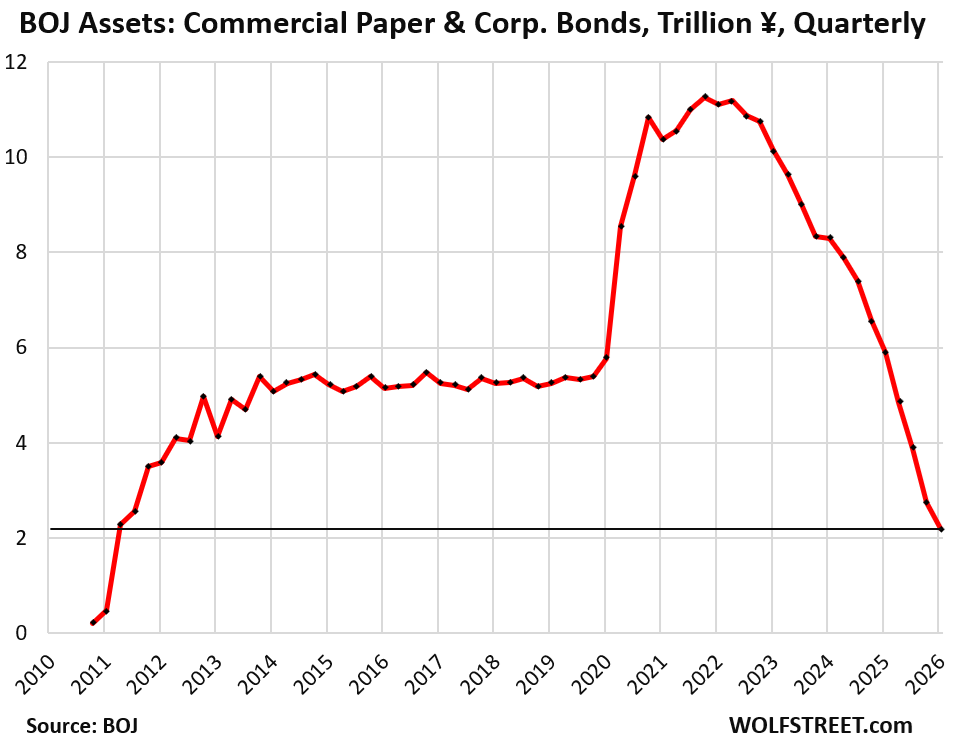

Commercial paper and corporate bonds fell by ¥550 billion in the quarter to just ¥2.2 trillion ($14 billion), all of them being corporate bonds; the BOJ shed its last commercial paper in the quarter, and they’re down to zero.

They were always just a tiny part of the BOJ’s QE operations, at their peak accounting for only 2.2% of the BOJ’s total assets. They’re now down to just 0.3%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If the tightening was accomplished by BoJ roll-off of 1 year Japanese Treasuries previously bought (and held) that is kind of interesting.

You wouldn’t think that the earlier BoJ purchases of such short term Japanese Treasuries would have had much of a restraining effect (then) on longer term Japanese interest rates (kinda the whole point of “quantitative easing”).

This is sort of an important basic question now that Central Bank money printings (QE to buy Gvt Treasuries) are becoming more and more common (if not respectable) around the world.

Namely, just *how much* Central Bank QE printing (read, inflation) is necessary to keep an artificial cap on market interest rates (by acting as a non-economic purchaser of Government Treasuries) – and what term Treasuries do such CB purchases have to target in order to keep the desired interest rates (presumably long-term) under the desired artificial ceiling?

You would think the QE would have to buy long term Treasuries to artificially restrain long term rates – but is that what the BoJ did? Can CB’s influence/control *long term* rates by buying short-term Treasuries?

Nonsense. You’re making up BS theories based on nonsense. I said in the article: “the last Treasury bills (terms of one year or less) matured off the balance sheet last year and were not replaced.” The amounts were already minuscule before QT officially started. The BOJ never held more than minuscule amounts of bills. The purpose of QE and YCC had always been to buy long-term bonds to bring 10-year yield down to 0%. In mid-2024, before QT started, the BOJ held just ¥2 trillion ($12 billion) in bills, compared to ¥580 trillion ($3.65 trillion) in JGBs.