Inflation and the deteriorating yen pushed the Bank of Japan into a hawkish stance, and bond yields are on their own.

By Wolf Richter for WOLF STREET.

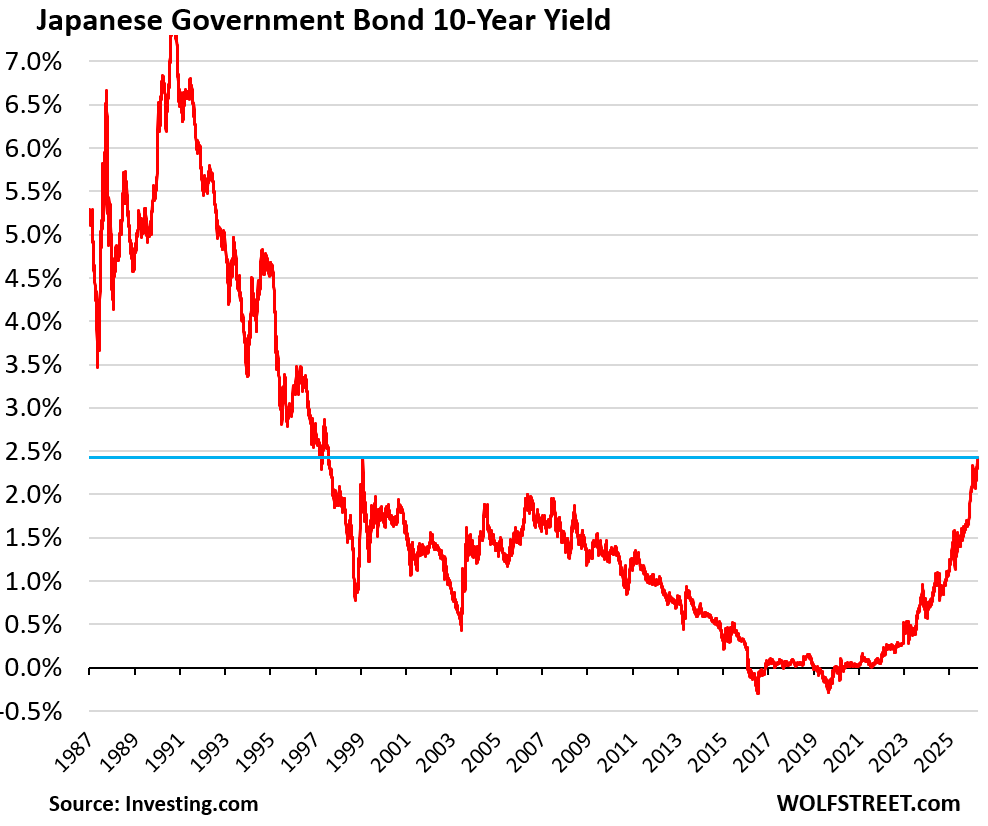

The crucial 10-year yield of Japanese Government Bonds (JGBs) rose by 5 basis points on Monday, to 2.432%, a hair higher than in February 1999, and the highest since July 1997.

Despite the four-year spike up from around 0%, this yield doesn’t adequately compensate investors for the risks they’re taking over those 10 years and is extremely unappetizing during inflationary times and for a country that is in the worst fiscal position among developed economies with by far the largest debt-to-GDP ratio.

Projections of debt issuance over the next few years, including to fund rising interest costs, are now being ratcheted higher. New investors will need to be enticed to wade into Japan’s fiscal morass, and higher yields may be needed to do that.

Inflation in Japan’s overall economy – not just consumer price inflation – was 3.4% year-over-year in Q4, as measured by the GDP deflator in Japan’s GDP figures, barely below where US inflation in the overall economy was in Q4 (3.8%).

Japan’s credit rating by Fitch (‘A’) is five notches below ‘AAA’ while S&P’s rating (‘A+’) and Moody’s rating (‘A1’) are four notches below ‘AAA’ (my cheat sheet of bond credit ratings by rating agency).

To deal with inflation and the yen, which has become a wet rag, the Bank of Japan stopped increasing its JGB holdings at the end of 2023. It started QT in 2024 and has been reducing its holdings of JGBs and other assets. As of the quarter ended December 31, the BOJ reduced its total assets by 10.4% and its JGB holdings by 8.1%.

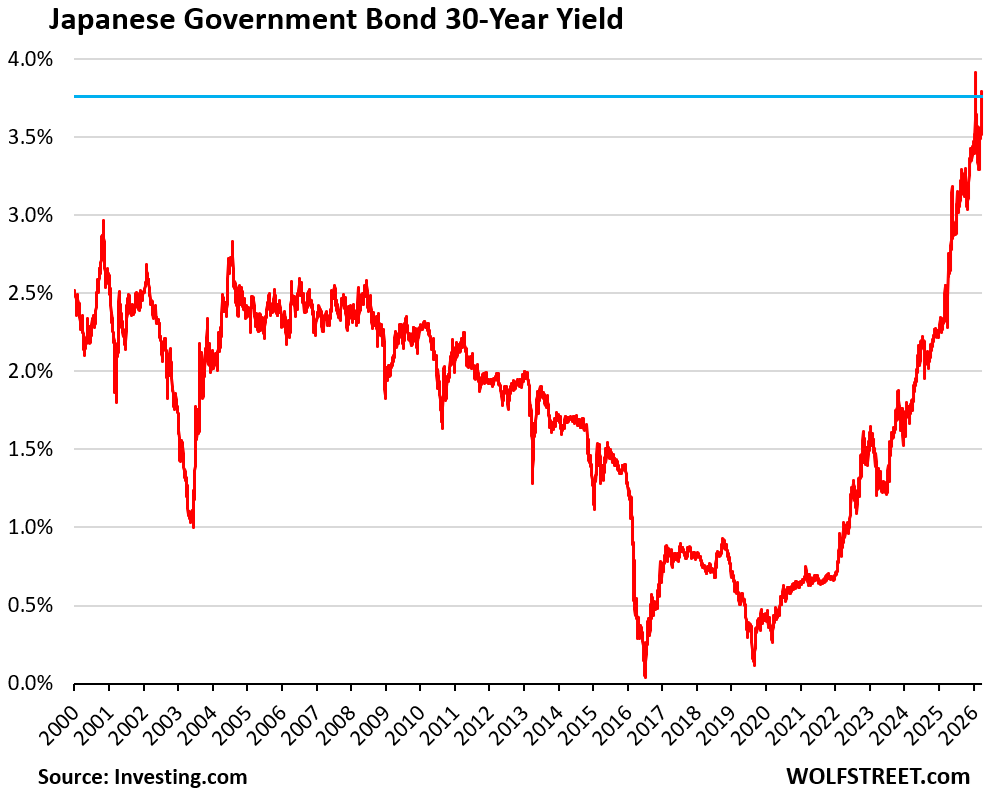

The 30-year JGB yield jumped by 8 basis points on Monday to 3.76%. Over the past seven trading days, it has vacillated up and down around that range.

Since July last year, the 30-year JGB yield has been moving around at all-time record levels in the life of the 30-year bond which was introduced in 1999.

In the two trading days through January 20, the 30-year yield had exploded by 42 basis points to 3.91%, after the new Prime Minister Sanae Takaichi called for increased government spending with simultaneous tax cuts by pausing the 8% consumption tax on food purchases.

After numerous efforts by authorities to calm the waters in January – including by Bessent in the US where Japanese bond yields had begun to roil US Treasury yields – the 30-year JGB yield declined and dropped by over 60 basis points to 3.29% by February 24.

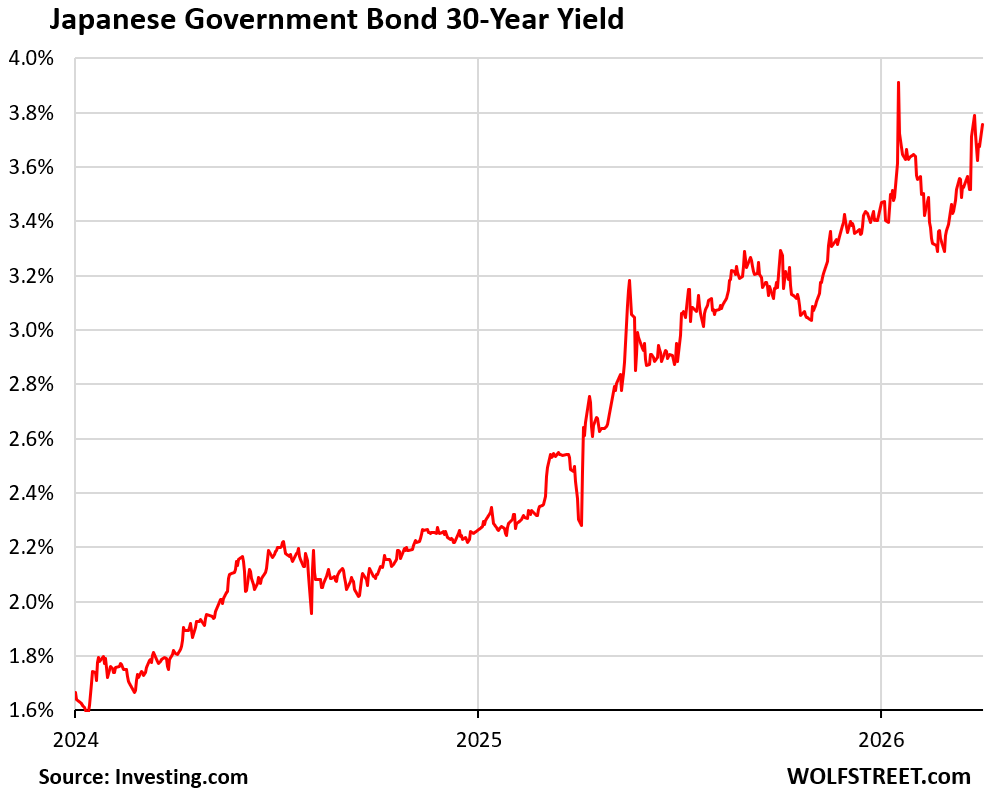

But then it turned around and has been marching higher again. Here’s a close-up of the situation:

But still dead are the “bond vigilantes” – big institutional investors that refuse to buy government bonds because risks are too high and yields too low. Decades of QE killed them. The BOJ still holds 50% of all JGBs outstanding.

Government-linked institutions hold another big junk, including Japan Post Holdings which is 35% owned by the government and includes majority stakes in Japan Post Bank, the fourth largest megabank in Japan, and Japan Post Insurance, one of the largest life insurers in the world. Institutions that the government can lean on are not going to gang up with the bond vigilantes.

Another big chunk is held by the Government Pension Investment Fund (GPIF), one of the largest pension funds in the world, and part of the government.

JGB holdings as of the end of Q3, figures by the Ministry of Finance:

- Bank of Japan: 50.0%

- Insurance companies, including Japan Post Insurance: 16.2%

- Banks including Japan Post Bank: 14.6%

- Foreigners: 6.6%

- Public pension funds, including GPIF: 6.5%

- Private pension funds: 3.0%

- Households: 1.7%

- All others: 1.5%.

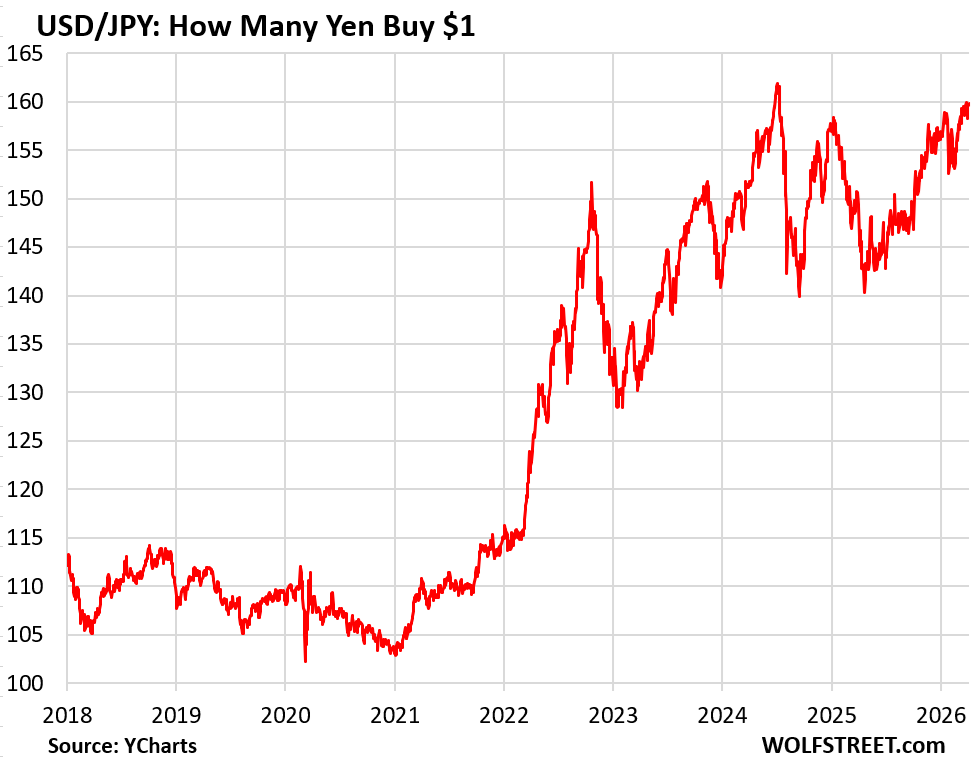

The yen has been tiptoeing around the 160 line for days, despite threats of “decisive” intervention by Japanese authorities a week ago. Currently, the yen trades at 159.77 to the USD.

The MOF with intervention talk: “We are hearing that speculative moves are increasing in the currency market, in addition to the crude futures market. If this situation continues, it may be time to take decisive measures,” Atsushi Mimura, the vice-finance minister for international affairs at the Ministry of Finance, told reporters. “We are prepared to respond on all fronts, and our focus is broad and comprehensive,” he said. But it didn’t help.

The BOJ with hawkish talk: Also on Monday a week ago, Bank of Japan governor Kazuo Ueda told Parliament: “We don’t guide monetary policy directly to control foreign exchange rate moves…. But currency market moves are obviously among factors that hugely affect economic and price developments.”

When asked by a lawmaker if the BOJ could raise rates to staunch the yen’s bleeding, which has been driving up the costs of imports and fueling inflation, Ueda replied: “We will guide policy appropriately by scrutinizing how currency moves could affect the likelihood of achieving our growth and price forecasts, as well as risks.”

Since the beginning of 2021, the yen has lost 34% of its value against the USD. Since the beginning of 2012, when the massive QE started, it has lost 46% of its value against the USD.

To put a lid on the currency’s deterioration, the BOJ started QT in 2024, shedding 10% of its assets, accompanied by timid baby-rate hikes to a whopping 0.75%, with more rate hikes expected.

And with the yen where it is and might be headed, and with inflation where it is and might be headed, any efforts by the BOJ to push down long-term bond yields with another round of QE or yield-curve control would have a brutal effect on the yen and on inflation. And those options are off the table. Instead, there’s this hawkish talk.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The “Yen Carry Trade” is kaput?

Best Freudian slip I’ve seen here in awhile 😂💹

Government-linked institutions hold another big junk…

Why would BOJ raising rates strengthen the Yen against the USD?

Is the idea that some capital would move out of USD and into Yen to chase the higher rate, increasing the demand for Yen and raising its relative value?

Trying to learn.