The Fed has also struggled in dealing with this labor market.

By Wolf Richter for WOLF STREET.

On one side, there are the tech layoff announcements, often to clean up what tech CEOs widely called “over-hiring” to describe what they’d done in 2020-2022, when their payrolls exploded; Block CEO Jack Dorsey was the latest on X, “yes we over-hired during covid…,” after Block announced that it would lay off nearly half its staff, which had more than tripled in 2020-2022 (from 3,900 to 12,500).

At the same time, there is helter-skelter hiring for AI-related jobs with huge compensation offers leading to what’s locally called a “mansion shortage” in AI epicenter San Francisco.

And there is very tepid hiring in other parts of the private sector, accompanied by massive layoffs at the federal government, and job reductions at state governments.

These currents come amid a crackdown on illegal immigration and the tightening up of some legal immigration that have led to a drop in the total supply of labor.

This is not a labor market the US is used to. It’s a labor market of low unemployment despite low job creation in the private sector and job destruction at the federal government.

Job creation in the private sector is low because there is less demand for labor in some industries, including because AI is being deployed to do things that college graduates entering the labor market would have done, making this job market very difficult to enter for recent graduates.

And job creation is also low because of labor shortages in other industries, such as skilled labor in the trades, including those needed in construction, which has started a whole discussion of how it would have been better for some young people, instead of going to college and loading up on student loans, to go to trade school and then train to be auto technicians or electricians or HVAC technicians or carpenters or welders.

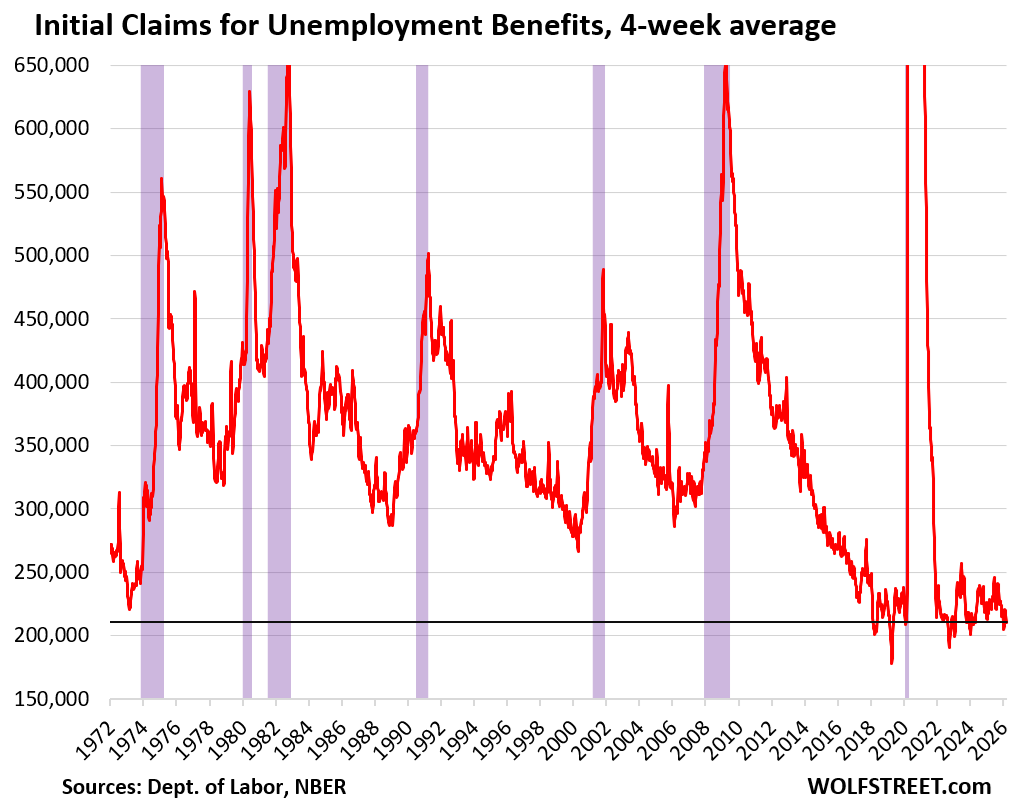

The latest piece of the puzzle in these countercurrents: The four-week average of initial applications for unemployment insurance benefits in the week through Saturday ticked down to 210,500, according to the Labor Department today.

There were only a few weeks in the decades from the 1970s till the pandemic when the four-week average was even lower.

What this shows is that, despite all these announcements, relatively few employees in the US are actually getting laid off without already having another job in the same company or elsewhere lined up:

These historically low figures track freshly discharged people who filed for unemployment insurance compensation at their state unemployment agencies. The agencies then report them to the US Department of Labor by the weekly deadline, which then publishes it. This is not survey-based.

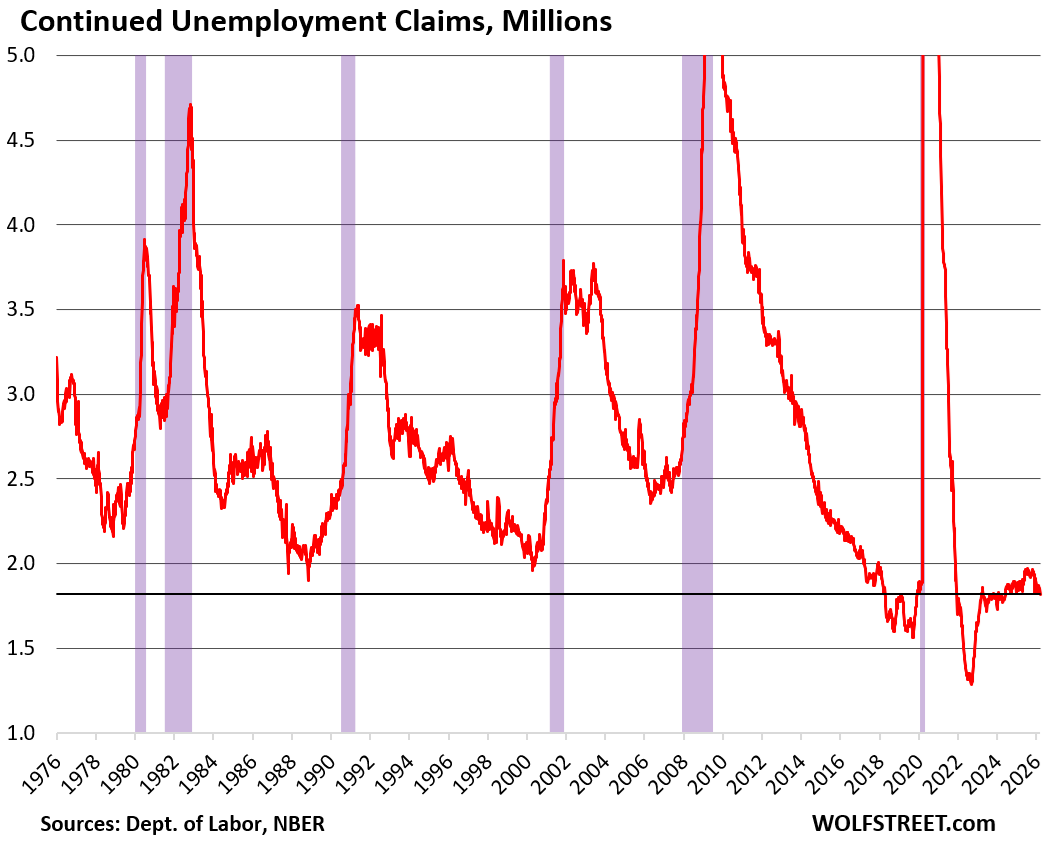

And here is another piece of the puzzle: The four-week average of continued weekly claims for unemployment insurance benefits fell to 1.847 million, according to the Labor Department today.

Over the past five decades, it’s only during the tight labor market in 2018 and 2019 and in the years of the labor shortages in 2022 through early 2023, that the level was ever lower.

This reflects the total number of people who’d initially applied for unemployment insurance at least a week earlier and are still claiming unemployment insurance because they still haven’t found a job.

It shows that overall, private-sector employers are hanging on to their workers despite some global layoff announcements at some big companies, though these announced layoffs don’t all happen in the US, and some don’t lead to actual layoffs, but elimination of “roles” with workers shifting to different jobs in the same company. And some of these layoffs hit remote jobs, while workers for in-office jobs are getting hired.

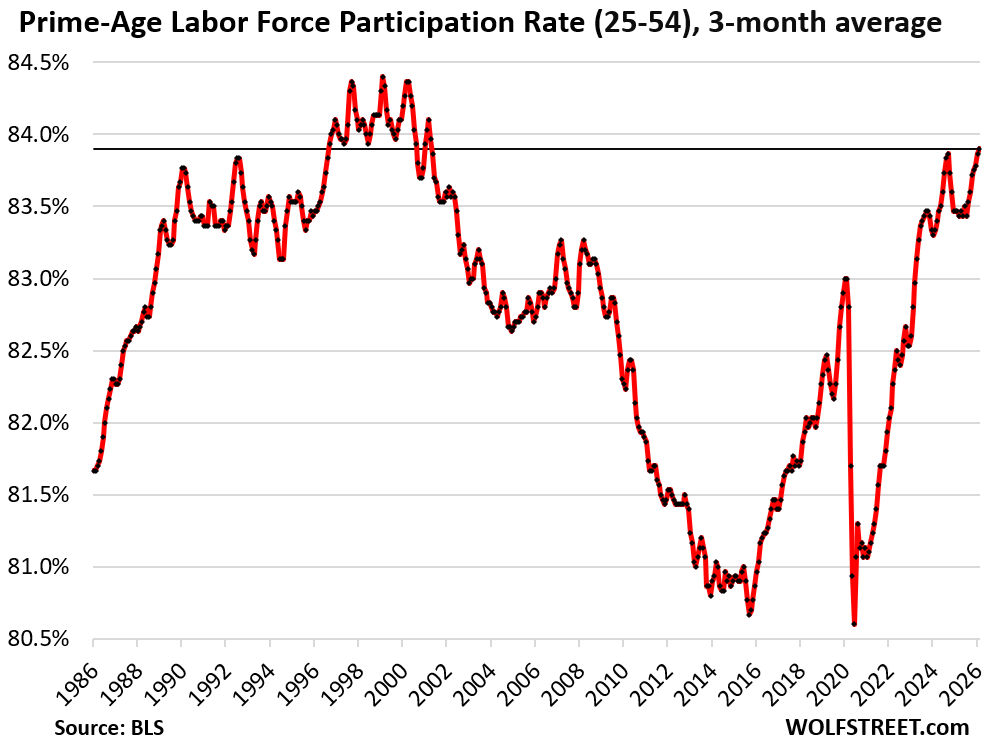

The convoluted strength of this labor market amid the crackdown on illegal immigration and the drop in the supply of labor shows up in the prime-age labor force participation rate (25-to-54-year-olds), which has been running at 25-year highs, lower only than during the extraordinary period of the Dotcom Bubble (data via the BLS on March 6).

The prime-age labor force participation rate eliminates the issue of the retiring boomers. The overall labor force participation rate shows the percentage of the population that either has a job or is looking for a job. When people retire, they’re no longer “participating” in the labor force but remain in the population until they die. The surge of boomer retirements, which started about 15 years ago, has pushed down the overall labor force participation rate, as these retired boomers are still in the population but no longer “participating” in the labor force.

The Fed has also struggled in dealing with this labor market. And Powell expressed those struggles during the last FOMC press conference. It’s not a weak labor market in the typical US sense with big layoffs and a rise in unemployment; and it’s not a strong labor market in the typical US sense with lots of job creation either. But it may be the new normal labor market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good article, but it completely misses the biggest structural shift in the modern labor market: gig workers. Leaving them out makes every historic indicator look “normal” when the underlying reality is anything but.

I just looked it up: you made 3 comments over the past 18 months on my site, and all 3 were exactly the same stupid BS about the gig workers, and each time, I wasted my time shooting it down, and you never looked at it. You’re clearly an experimental AI agent that got lost in its own hallucinations:

Job creation shortages due to a lack of skilled trades is the massive gap imho. Last I checked, we are sitting around 500k to 700k unfilled open positions in the manufacturing industry right now; good, well paying jobs.

Also, seeing a lot of job creation on LinkedIn; this is anecdotal but I’ve never seen my network buzzing like this before. Last I saw, can’t claim anything to support or verify, but the talking heads said something about AI actually creating jobs.

Maybe the issue is that the Quiet Quitting crowd has a lot of free time on their hands to complain about how the government hasn’t issued them a job yet 🤔

There has never been a technology that has “eliminated” jobs in human history, in a well functioning economy. Every efficiency gains allows for a labor pool that can now do other things.

My biggest fear with AI is it’ll somehow allow stupid ideas like guaranteed basic income to artificially raise labor costs and increases cost of executing innovation. That kills and economy long term

I am aware of a several IT personnel who have been laid off but haven’t applied for unemployment benefits. They haven’t applied since they have significant assets, they got nice severance packages, they don’t anticipate being unemployed for long, and they view the unemployment benefits in their state as being not worth the application effort. Do you think, Wolf, that some of these labor market anomalies could be due to widespread adoption of behaviors like this?

1. No, because it’s a minuscule number of people out of the 160 million employees who’d walk away from free money.

2. As I said in the article, people who already have a job lined up, and essentially just switch over, they don’t apply for unemployment insurance, and they don’t qualify either because they already have a new job, and this is a much more common scenario.

3. If you got laid off as a wealthy tech person, and now decide to finally start your own VC firm or startup or whatever, well then, that’s a new job, and you’re not out of work, you just switched jobs.

I know two tech people with massive assets who got laid off and didn’t have a job lined up, and they immediately filed for unemployment insurance, because it’s free money, and it’s not means-tested, and you can do it online.

why would anyone walk away from say ~$2K/month unemployment benefits for 6 months as part of unemployment benefits ?

I am in IT, my friends , ‘rich’ friends, lost their jobs and did apply.

Pride

It’s stupid. Unemployment is an insurance program, for which you’ve paid premiums through your employer. If you are in a car accident, do you not make a claim out of pride?

Your friends and former colleagues don’t know you filed unless you tell them. So “pride” doesn’t come into play here. It’s just “stupid,” as TSonder305 said so eloquently.

“In conducting monetary policy, we will remain highly focused on fostering as strong a labor market as possible for the benefit of all Americans. And we will steadfastly seek to achieve a 2 percent inflation rate over time.”

—Chair Powell, Aug. 27, 2020 speech

The labor market is clearly fine since unemployment is essentially all time lows.

Powell won’t address the inflation elephant in the room. He needs to go sooner rather than later.

TNX 4.42

Maybe Powell is gonna let the bond market do his job for him.

“The possibility of rate hikes came up during the Fed’s March policy meeting, Fed Chair Jerome Powell said. The committee decided to keep the central bank’s key interest rate steady on Wednesday for the second meeting in a row.

Powell confirmed that a committee member had proposed including language in the policy committee’s official statement about the risks to the central bank’s dual mandate being “two-sided.” That is, the Fed might have to raise interest rates to crush inflation or lower them to boost the job market.

“The possibility that our next move might be an increase did come up at the meeting, as it did at the last meeting,” Powell said. “The vast majority of participants don’t see that as their base case. And of course, we don’t take things off the table.”

My pet theory is that quits are low because pandemic stimulus gave people a chance to change jobs and end up in jobs that are a much better fit for them. So that will disrupt what was the “normal” quit rate for a while.

And the pandemic also forced a lot of people to find new jobs, for example by unemploying service workers. Some percent of those people found better, more stable jobs outside service industry, so they are not appearing in the quits like they would have in a world without the pandemic.

If the USA separated health insurance from employment, I bet we’d see the quit rate fall even lower over time, as people had more freedom to try out job searches for better fits.

What’s funny to me is that my company could save at least 10K on me if they allowed me to work from home

I have friend that’s a data scientist at LinkedIn. There appears to be a growing concern among the highly paid that the rug could be pulled out from under their feet. The smart ones are saving money because when the bubble pops those who get paid the most and are expendable will have nowhere to run except a mansion with exuberant property taxes.