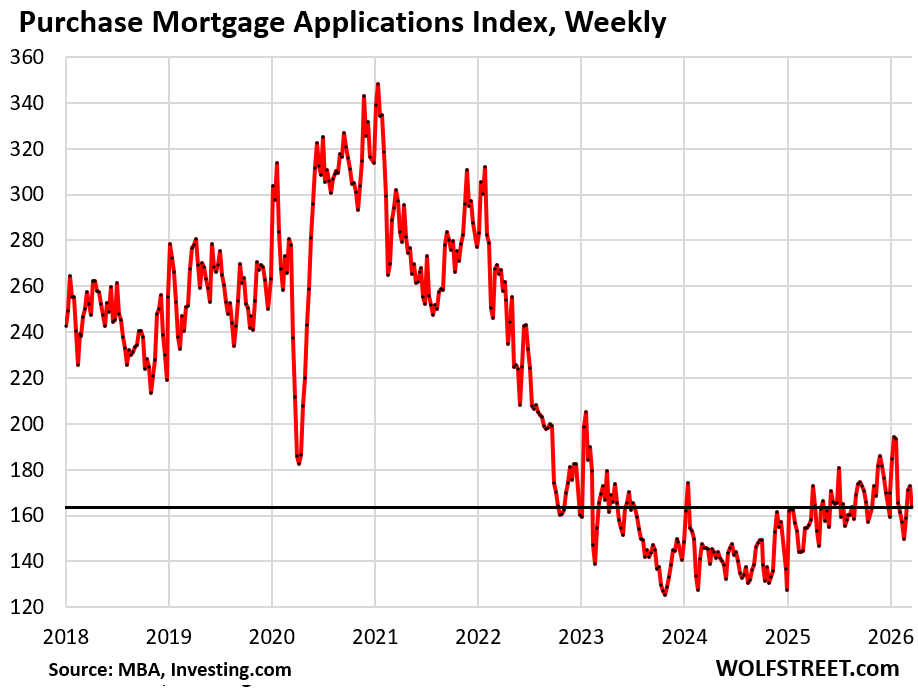

Mortgage purchase applications are down by 35% from the same period in 2019 in a housing market that remains frozen.

By Wolf Richter for WOLF STREET.

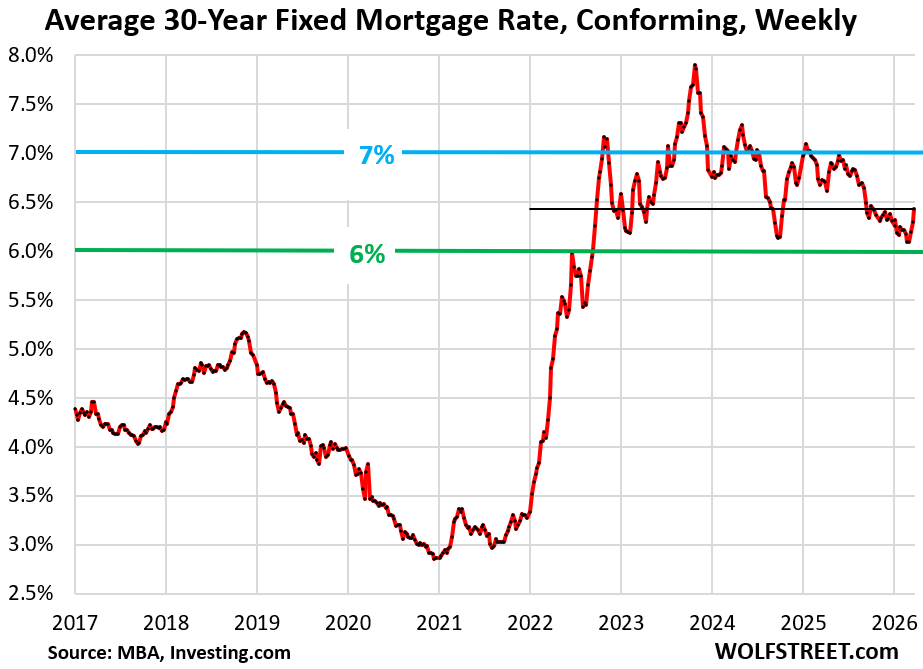

The average weekly mortgage rate for conforming 30-year fixed mortgages rose to 6.43%, the highest since October 2025, according to the Mortgage Bankers Association today.

This weekly measure of mortgage rates is once again solidly in the middle of the 6% to 7% range that has prevailed since mid-2022, and that before 2008 was considered relatively low to normal.

It’s just that the Fed’s QE, which included the purchase of trillions of dollars of mortgage-backed securities, had repressed overall interest rates, and specifically mortgage rates, to recklessly low levels – 30-year mortgage rates below 3% even as inflation was shooting toward 9% – which had triggered the fantastical home-price explosion through mid-2022 that left prices beyond where they make economic sense.

And so annual home resales have plunged by 23% from 2019 in each of the past three years, mortgage applications to purchase a home have collapsed by 35% from the same period in 2019, the industry has been decimated, and the housing market has been frozen, now in its fourth year, while supply of resale single-family homes surged to the highest in 9 years and inventories of new completed single-family homes reached the highest since 2009.

And the much hoped-for and hyped spring selling season, on the expectations of miraculously lower mortgage rates, is already turning into a dud once again.

Mortgage applications to purchase a home fell in the current survey week for a miserably low beginning of the year and remain near rock-bottom levels, down by 35% from the same period in 2019.

That drop of roughly 35% from the same period in 2019 has prevailed in February and March, after a slight improvement late last year and into January.

Purchase mortgage applications are a measure of demand for homes that may become actual home sales in the future and are therefore a forward-looking indicator of home sales. And it’s not looking good for the spring selling season.

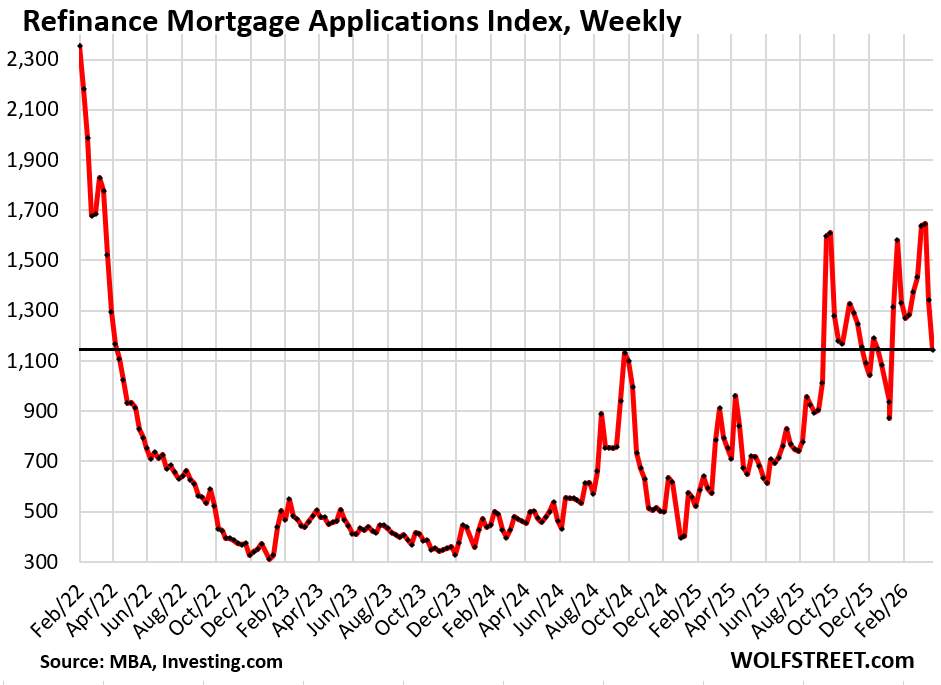

Mortgage applications to refinance a home plunged for the past two weeks from their spike in early March, as mortgage rates have risen.

When mortgage rates dropped even a little, refi applications spiked as if homeowners were sitting at their screens, just waiting for the right second to pull the trigger. This process has been repeated several times since October 2024. Any dip in mortgage rates brings out new waves of homeowners that pounce on refinancing a mortgage at a lower rate, or to pull out some cash. And when mortgage rates bounce off that dip, demand fizzles.

Refinancing a mortgage is not free. There are up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – and those fees are then added to the loan amount and increase the payment, which reduces the advantage of lower mortgage rates. Homeowners who want to refi a mortgage to lower their payment do a breakeven analysis with online calculators or through brokers and mortgage lenders, to see if refinancing the existing mortgage is even worth it. When results tilt their way, they pounce, creating these brief spikes in refis.

Mortgages also count as refis when homeowners that no longer have a mortgage get a mortgage to take that amount of cash out of the home they own.

But even the highest refi activity this year was relatively low compared to the refi boom of 2019-2021.

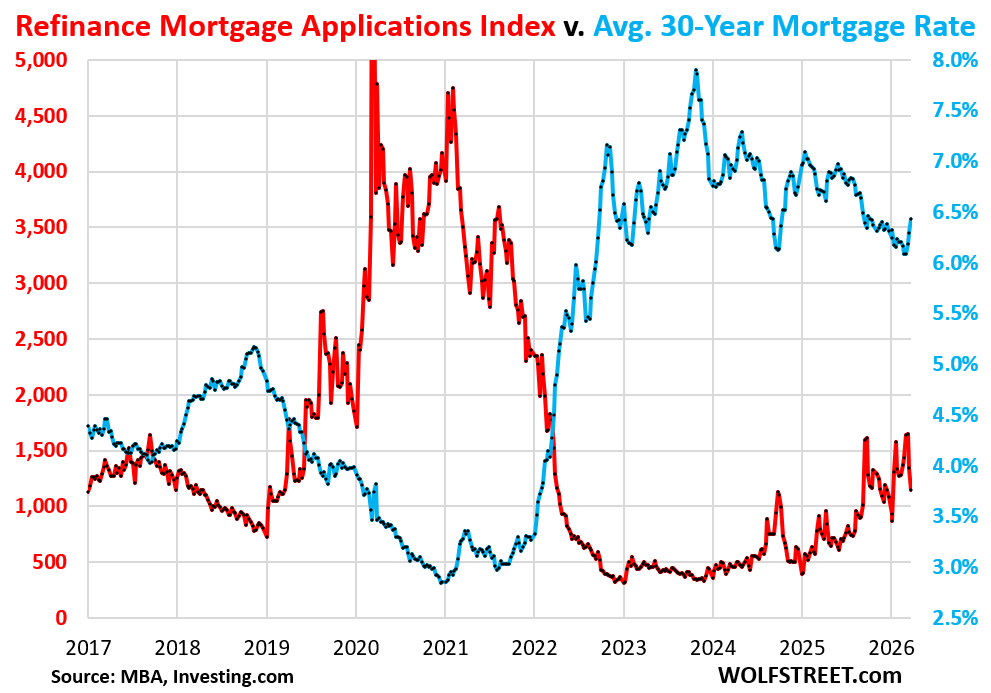

This decade-long view shows the tight inverse relationship between mortgage rates (blue) and refi applications (red):

In case you missed it: Whatever it takes to sell lots of homes in this frozen market? Homebuilder Lennar Cuts Average Selling Price by 24% to 2017 Level.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– I see a releationship between the closure of the Strait of Hormuz and these rising interest rates. When the oil stops “flowing” then it undermines the PetroDollar system.

– I am still not too worried. I still think long term rates will / could go down in the near future.

There is no petrodollar system. It died years ago. the US has become a net-exporter of crude oil and petroleum products and has a massive trade surplus in the energy trade, and there are no petrodollars to recycle. Instead the US is bringing dollars back to the US with its energy trade surplus.

Indeed. Add Guyana with, if they secure it beyond the initial effects of president poaching, Venezuela, to the US energy sphere and there’s going to be a a deep well of dollars over many years.

Maybe enough for the odd game of middle eastern whack-a-mole or other disruptuon of Mackinder’s heartland.

Is this satire on what you think Keynes would say or your opinion? Tom Lehrer claimed satire was obsolete after Kissinger won the Nobel peace prize. Just saying

Timberrr !!!!

For housing prices that is.

My guess is the Iran war is the biggest reason.

I have been anticipating a general housing bubble pop since 2004 based on mortgage rates exploding higher and plunging sales.

Except for a few specific markets, it has been the wrong call.

2026 may be the year!

Depends on the market. For many markets, the top was in mid-2022, and price have plunged since then, including Austin, Oakland, New Orleans,

https://wolfstreet.com/2026/03/17/the-most-splendid-housing-bubbles-in-america-price-drops-gains-in-33-big-expensive-cities-february-2026/

Long overdue. However, lots of dollars coming back to the U.S. and wealthy people often will park money in real estate, so good rentals or nice vacation properties will not see much of a price decline. Mid and low-end housing will definitely drop in price.