Quantitative Tightening has shed 25% of total assets from peak and 46% of pandemic QE.

By Wolf Richter for WOLF STREET.

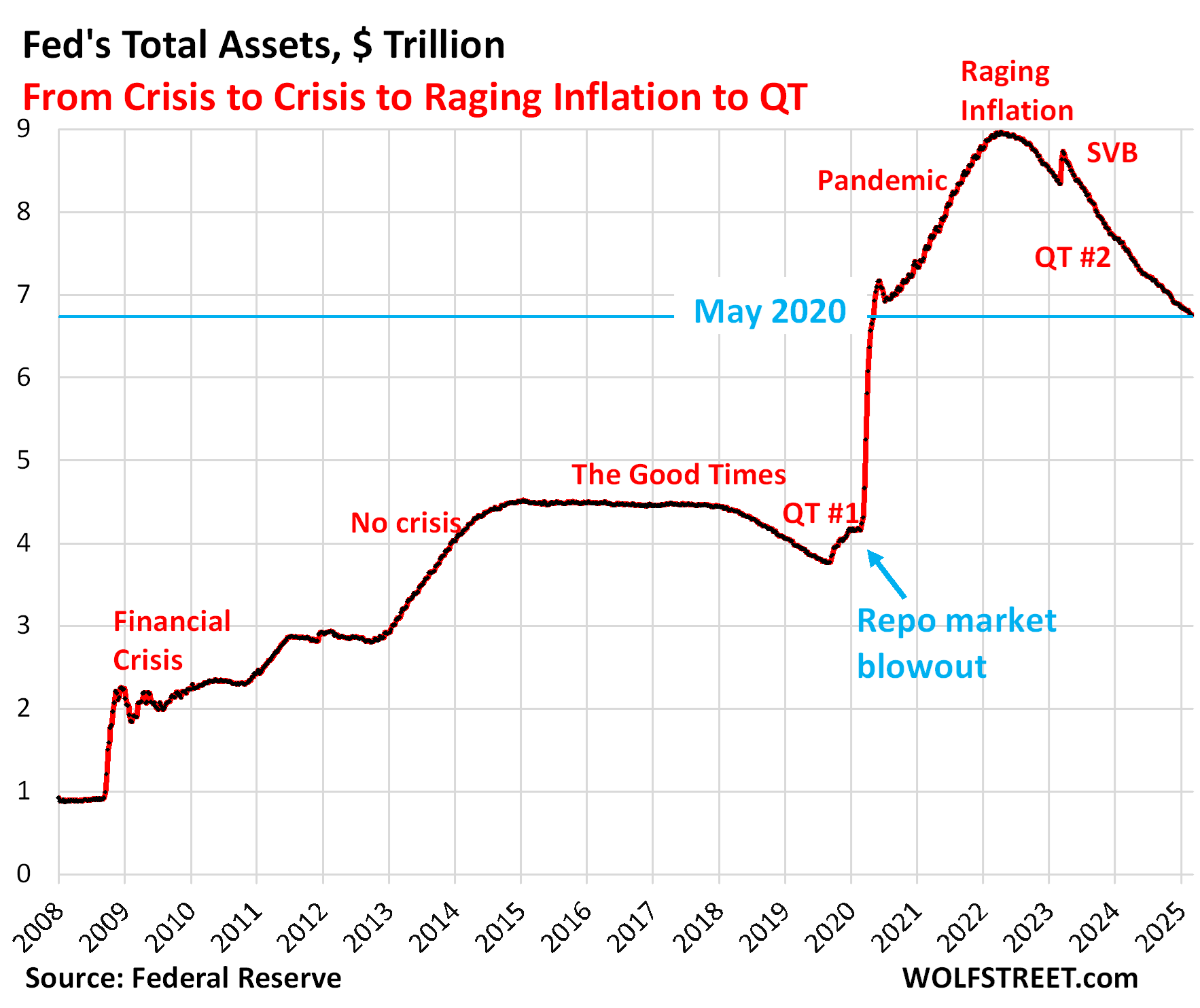

Total assets on the Fed’s balance sheet declined by $54 billion in February, to $6.76 trillion, the lowest since May 2020, according to the Fed’s weekly balance sheet today.

Since the end of QE in April 2022, the Fed has shed $2.21 trillion, or 25% of its assets. And it has shed 46% of the $4.81 trillion it piled on the balance sheet during pandemic QE from March 2020 through April 2022.

QT assets.

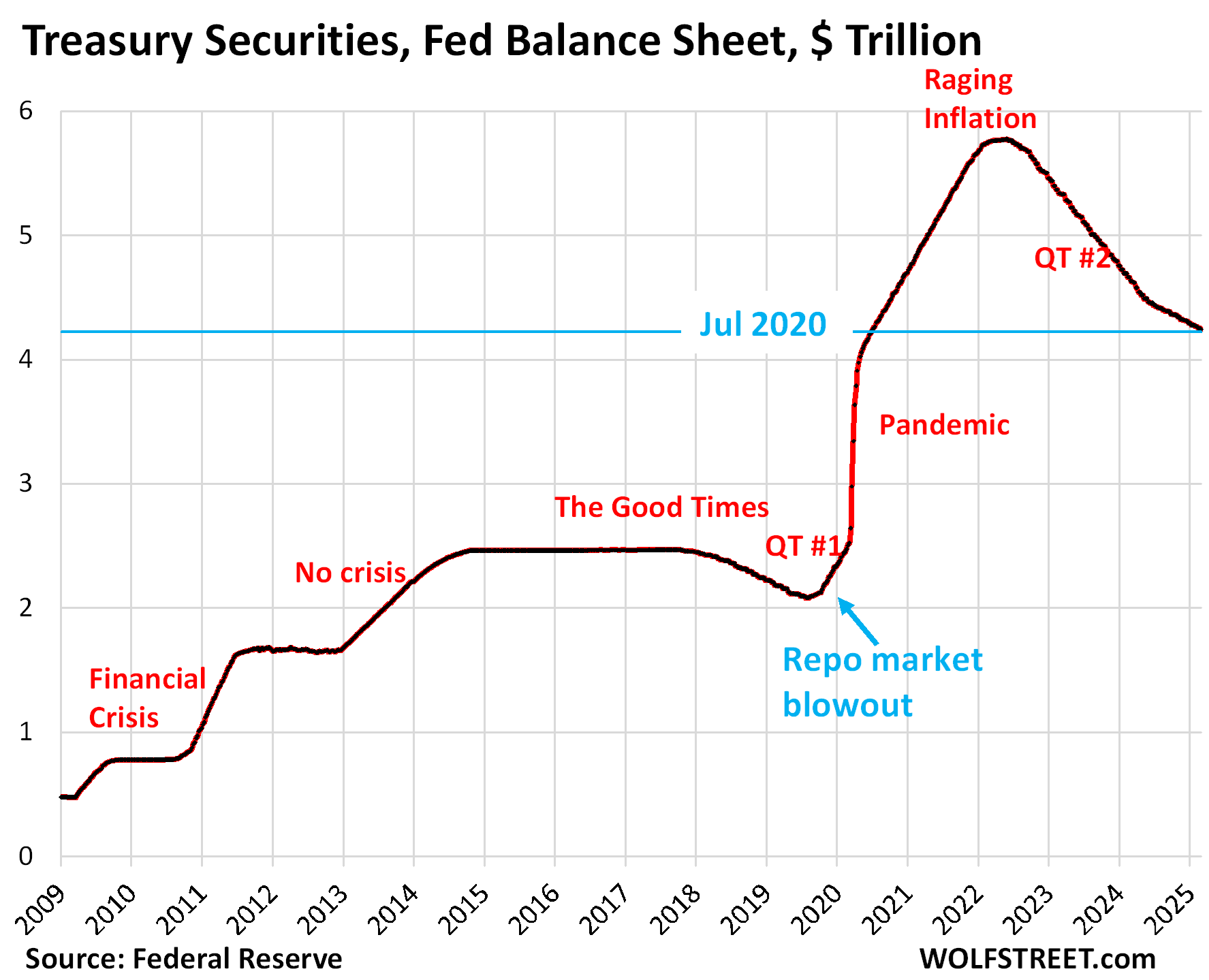

Treasury securities: -$24.3 billion in February, -$1.53 trillion from peak in June 2022, or -27% since the peak, to $4.24 trillion, the lowest since July 2020.

The Fed has shed 47% of the $3.27 trillion in Treasuries it piled on the balance sheet during pandemic QE.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. Since June 2024, the roll-off has been capped at $25 billion per month. About that much has been rolling off, minus the amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that is added to the principal of the TIPS.

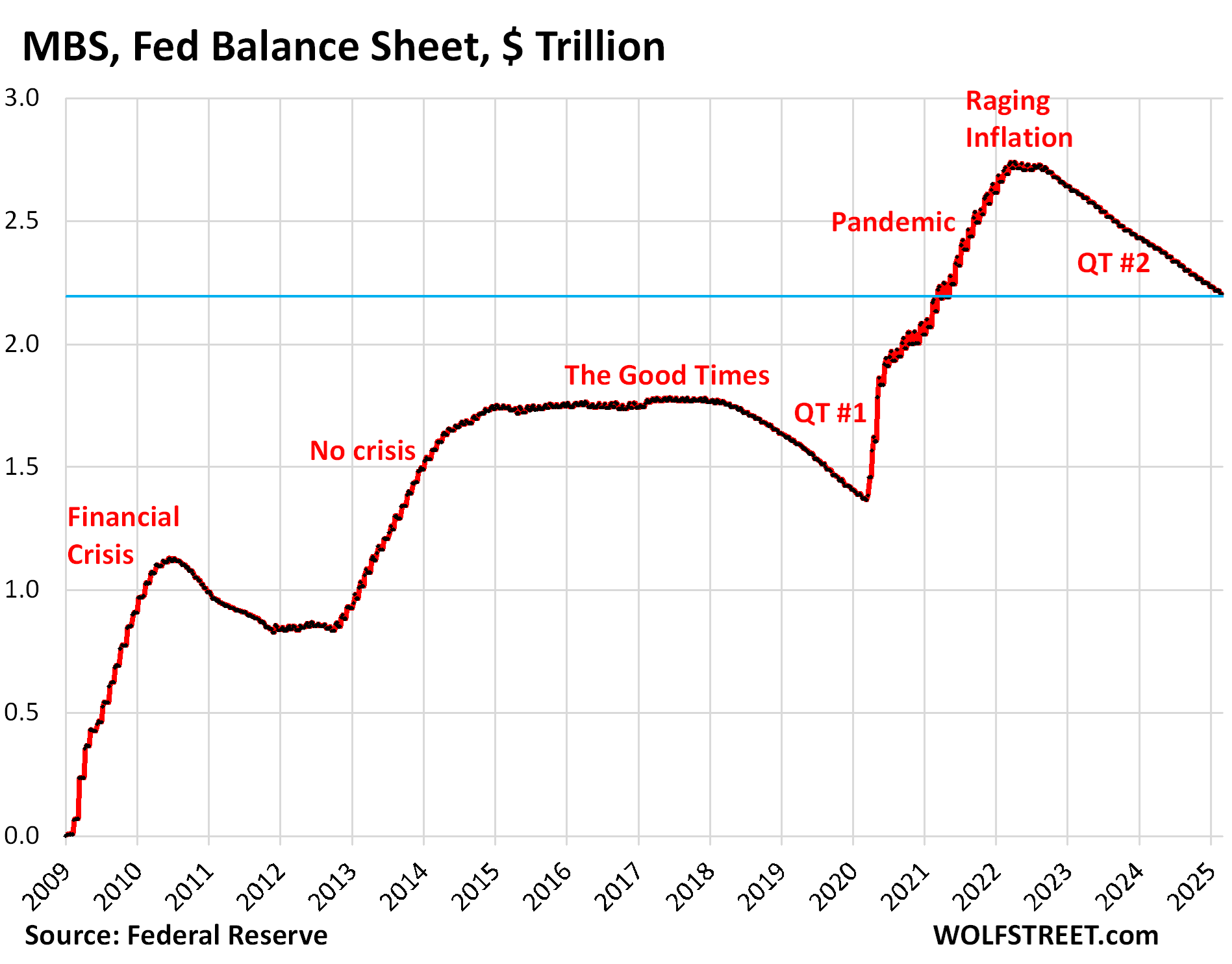

Mortgage-Backed Securities (MBS): -$14.2 billion in February, -$537 billion from the peak, to $2.20 trillion, first seen in March 2021.

The Fed has shed 19.6% of its MBS since the peak in April 2022, and 38% of the MBS it had piled on the balance sheet during Pandemic-QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But as sales of existing homes have plunged and mortgage refinancing has collapsed, far fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have become a trickle. As a result, MBS have come off the Fed’s balance sheet at a pace that has been mostly in the range of $14-17 billion a month.

The Fed is not exposed to credit losses if borrowers default on mortgages because it holds only “agency” MBS that are guaranteed by the government, where the taxpayer would eat those losses, not the Fed.

Bank liquidity facilities: inactive.

The Fed has five bank liquidity facilities. Four of them have either no balance at all anymore or a balance that is so small by the Fed’s scale that’s essentially zero. All of them were heavily used after the SVB collapse, and two of them – the FDIC facility and the BTFP – were specifically set up to deal with the SVB fallout but are now shut down.

- Central Bank Liquidity Swaps ($133 million)

- Repos ($84 as of the close of the balance sheet on Wednesday evening, today at $0)

- Loans to the FDIC ($0).

- Bank Term Funding Program BTFP ($79 million in remaining loans to be repaid by March 11).

- Discount Window: unchanged in February at $3.1 billion. Qualifies as “near zero” as during the SVB panic, it had spiked to $153 billion.

What else caused total assets on the balance sheet to drop?

The balance sheet declined in total by $54 billion in February. Above, we accounted for $38.7 billion:

- Treasury securities: -$24.4 billion

- MBS: -$14.3 billion

And another $16 billion came off the balance sheet in February largely in these two accounts:

“Other assets” fell by $14 billion. This consisted mostly of accrued interest on its bond holdings that the Fed had set up as a receivable (an asset), and that it got paid in February, which reduced the receivable. When it gets paid interest, the Fed destroys that money (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid). By destroying the cash, the Fed reduces its assets.

Conversely, when it accrues the interest it earned before it receives it, it increases its assets. So the balance moves up and down on a weekly basis in a range currently between $28 billion and $47 billion.

Since this account also includes “bank premises” and other accounts receivables, it will always have a balance.

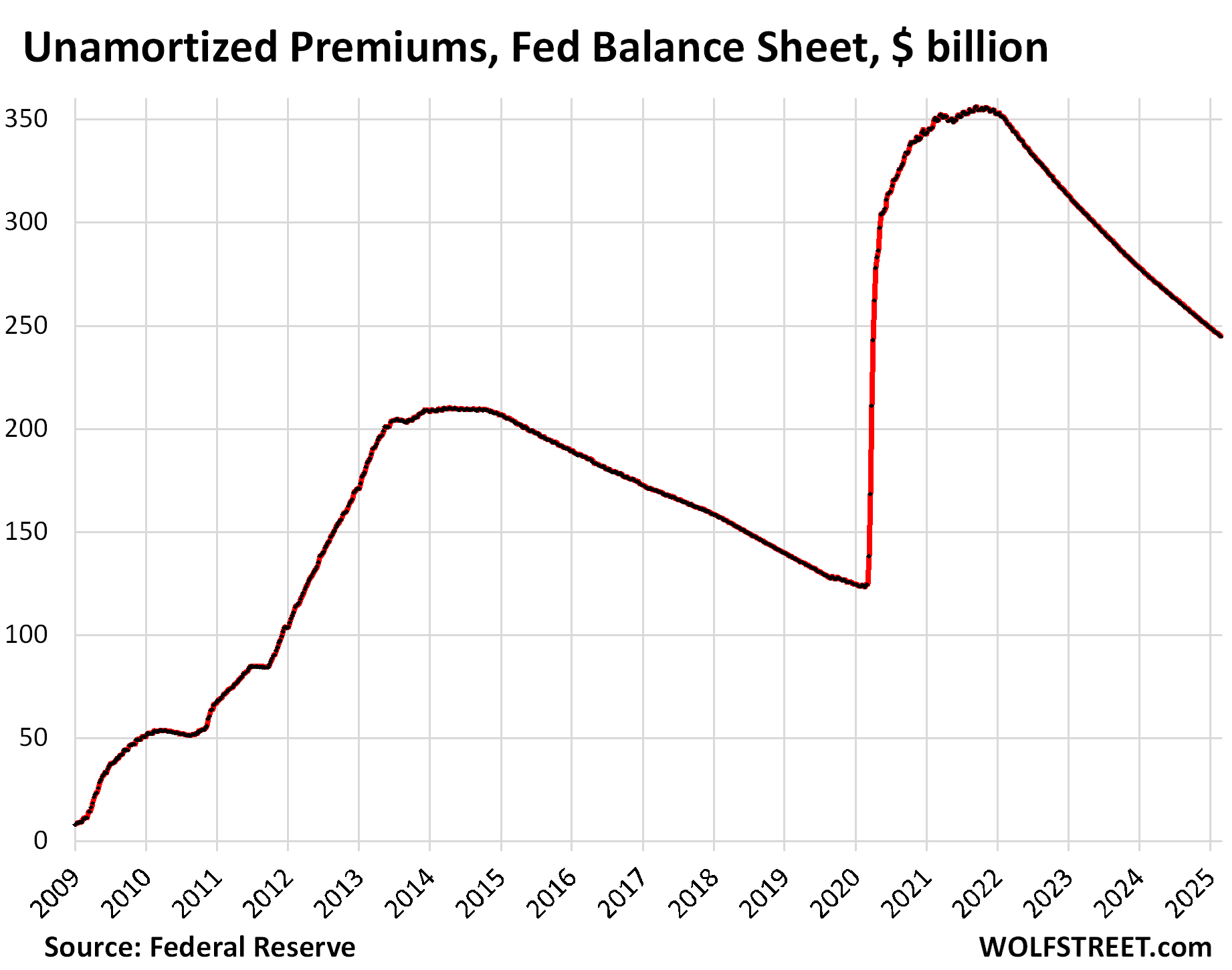

“Unamortized premiums”: $2.1 billion. This is the regular amount the Fed writes off every month to account for the premium over face value it had to pay for bonds during QE that had been issued with higher coupon interest rates earlier and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortizes that premium over the life of the bond. The remaining balance of unamortized premiums is now down to $245 billion, from $356 billion at the peak in November 2021:

And it case you missed it: The Future of the Fed’s Balance Sheet: Fed’s Logan on How Assets Might Shift from Longer-Term Securities to Short-Term T-Bills, Repos, and Loans after QT Ends. MBS Entirely Off the List

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

At roughly 1T per year we have about 7 years to go. Everything in the US is going so smoothly these days, what could go wrong?

So far FED has done good job by staying the course on QT. Powell has shown courage to stand up against Wall St and Political demands. After his term expires, what comes next? So all this will be depend upon next incoming chair.

Suspending or slowing QT talks already mentioned in FOMC Jan 2025 Meeting Minutes. We have seen this before. They started talking before meeting. In Mar 2024, Powell said we are discussing, May 2024 meeting he said we will slow down QT from June 2024. I wont be surprised if they do that again in 2025. Sure FED Members always have some or other excuses to slow down or pause QT. If TGA balances goes down and sudden refill may cause Repo/Reserve troubles etc. But that should be easily manageable through SRF. No need to further slow down QT for that.

Rather FED should quickly act on Logan’s talk. FED should start balance sheet calibration now itself. Anything above QT monthly limit should go to T-Bills. Start selling MBS to meet Monthly limits. But I guess those are NOT going to happen.

The problem is the debt-ceiling fight. It will drain the $800-billion TGA (government’s checking account) on the Fed’s balance sheet which will inject liquidity into the money markets, potentially close to $800 billion, and that’s not the problem, the problem is when the debt ceiling is over and the government replenishes the TGA by offering lots of T-bills – that may suck $600 billion out of the money markets in three months (it did last time), but last time, there was lots of cash in ON RRPs, and that $600 billion came out of ON RRPs. Now the ON RRPs are nearly gone, and so the $600 billion may come out of reserves in three months. This is like doing 15 months of QT in three months. Liquidity may not be able to move that fast, and if it doesn’t something may blow up like it did in 2019 after QT, and when they had to undo part of QT. They want to avoid that. They want to get through the TGA replenishment without anything blowing so that they then can continue with QT. The term they use is “slow or pause QT” until the TGA is replenished.

I’m going to have to write an article about this because it keeps coming up in a twisted manner.

I am curious about this to. Does your comment above mean that the fed “pausing QT” is more like preparing their asset holdings in this “pause” time to be able to help fill the liquidity demand created by the refilling the TGA?

They don’t want to add to the problems that rise from refilling the TGA so quickly, they want to make sure there are enough reserves to refill the TGA smoothly without causing liquidity strains.

Look, there is no playbook for this. No one has ever done anything like this. There has never been $2.2 trillion in QT. And the TGA is now huge… $800 billion desired level. Drawing it down to near zero and then replenishing it quickly moves the needle. And Congress is unpredictable in their charade of the debt ceiling. All kinds of things can go wrong. And the Fed is just trying to be careful. I would be nervous too.

yes like if it gets drawn out this happens,if they agree quickly this happens.

And you’re not going to take it anymore?

Yessir!

Please do write that article as discussed on another article a few days ago.

Thanks Wolf!

I’m always worried when I write this stuff that no one reads this stuff. This stuff is dry.

I’d read it! And I’ll get an army of bots to inflate your traffic stats so you’ll write more of them :)

I for one love this stuff, since you can’t really understand today’s economy without really understanding the biggest player in it.

Wolf – Count me in as one of the people who learned a lot from this article. When you write about the mechanics of Fed actions and about U.S. government debt, I read every word. Sometimes I read the same sentence several times because you cause a light bulb to go off in my head. Today’s thunderbolt:

“… the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid.”

Until today I never internalized this basic yet incredibly important point. Please, please keep writing about the Fed, U.S. government debt, inflation, etc. Thank you.

The wonky stuff is the best stuff you do. Nobody else is writing about it.

The stuff about the debt ceiling is fascinating stuff for central bank policy nerds like you and me :)

Your proposed solution (continue QT and current pace and then pause when the Treasury refills its account) is only one option.

Why can’t the Fed *accelerate* QT once the debt ceiling hits, and then pause QT when it’s raised, so as to smooth out the fluctuations and still keep its average rate of QT the same?

As much as the sudden refill of the TGA is rapid QT, the month before, during the ceiling, is QE, since the govt is spending money into the economy without selling new debt. Why can’t the Fed sell t-bills during that time, then buy them back after the ceiling is raised.

The Fed is still way too timid about these things. They are willing to flood the market at a moment’s notice if there’s too little liquidity (since that tends to hurt Wall St) while being sanguine and cautious about too much liquidity (which hurts savers and poor people without many assets).

This is not a surprise like covid and the Fed has plenty of time to prepare for it. The fact that the only solution they can think of is the exact solution that has messed up our economy for almost a generation now is supremely frustrating.

Since 2003, real GDP has increased 1.5X. During the same interval the Fed balance sheet increased 10X. There is no justification for such an extreme divergence yet no one asks Powell about it. Actually one person did last FOMC and Powell got very nervous. Regular Americans would very much like the BS to return to 1.5X of 2003. They suffer the deleterious consequences of inflation, mal-investment and extended wealth inequality. And by the way, it’s our bank.

1. Make sure to use not-inflation adjusted GDP (“current dollar GDP”) and not-inflation adjusted Fed balance sheet. You can also adjust both for inflation, and the results are the same; but you cannot adjust only one of them. Keep it apples to apples.

2. Neither adjusted for inflation: “current dollar” GDP grew by 2.7x since 2003; Fed balance sheet grew by 9.3x.

So not “1.5x to 10x,” but “2.7x to 9.3x.”

3. So yes, 2.7x to 9.3x is still a huge distortion. But that’s why the Fed is doing QT. See chart below.

5. Also, since the Financial Crisis, the government moved its checking account from banks such as JPMorgan to the New York Fed. And the balance in that checking account, normally around $800 billion, is part of the balance sheet now, and it wasn’t before. So that is a big change but it has nothing to do with money printing. It’s just a checking account, a big one. And the balance sheet will always be bigger by that amount in that account.

5. Chart shows Feds assets to GDP, neither adjusted for inflation. If you adjust both for inflation, the chart looks the same; but you cannot adjust only one of them. Keep it apples to apples:

Powell also let inflation spiral out of control by claiming that inflation was transitory. He was a year late to tightening.

Powell is one member of a board, not a dictator.

And in hindsight, the Fed made a mistake which it eventually corrected.

So what is your point? Do you have a constructive idea? A novel observation? Or do you just enjoy pulverizing dead horses?

Grant:

But you don’t really think these Fed Governors are going to go off on their own and dispute when Powell says inflation is transitory?

They tow the line unless it is so obvious that they cannot, without embarrassment, tow the line. So, in that sense, within a certain band, he is a dictator (Remember, he has all the data. . .)

To berate someone for criticizing Powell when he made one of the gravest misjudgments in recent Fed history, is just a bit churlish.

Stylites2,

Saying Powell made one of the gravest misjudgements in history is hyperbole.

Yes, inflation absolutely was not transitory. No doubt. However that statement pales in comparison to statements by Greenspan, Yellen, etc.

There hasn’t been a Fed chairman more wrong about the economy than Greenspan. He just got bailed out by circumstances.

Powell’s statement about transitory inflation was refuted by action within a month or two. Hardly grave.

I concur. I too am happily surprised QT has lasted this long.

But then again, with hyperinflation, it would be insulting to go back to NIRP-ZIRP.

Us common folk are getting eviscerated every week at the grocery store. My grocery bill $350 per week. That’s for a family of 5.

in Petaluma,

Congratulations! I am a family of one, and thought I was eating as simply as is humanly possible (consistent with health), but my grocery bill per capita is much higher.

Where do you live?

California grows 33% of the nation’s food & we have the highest food prices.

The humongous problem is the $2 TRILLION A YEAR FEDERAL DEFICIT that is being run as far as the eye can see and not the balance sheet of the Federal Reserve which buys a relatively small amount of the total outstanding and increasing Federal government debt of $36 trillion.

The Federal Gov needs to tax at the same rates it did in the 1950’s (with an adjustment for inflation). Nobody is going to “fix” the deficit when someone working at the minimum wage is paying more in taxes than some Billionaires. (One caveat: I do count Social Security as a tax).

I think that Gary Stevenson is on the money about this.

OK. I am done ranting.

The fiscal conservatives in charge of the government will *never* agree to a tax increase.

Instead, there will a tax cut to the wealthy. This tax cut will trickle down and generate more revenue for the government. I mean this time, its bound to work, right?

I have yet to meet a taxpayer of any income level truly willing to pay out, commensurate with the benefits received (directly or indirectly). Resentment against taxation is so deep in the DNA of the USA, it goes back to the very beginning. Depression and WW2 caught the wealthy off-balance. The postwar era was exceptional (with widest wealth distribution somewhere around 1968-72), and I know the wealthy vowed to never let anything like THAT happen again. So now inflation is the actual taxation, affording some relief for even the modest asset holders such as myself, and certainly to the financially flush and adept.

Those rates from the 50s are essentially fake, there were massive tax shelter schemes to work around taxes, and at the time, the US was literally the only developed country in the world that wasn’t a smoking ruin. A top rate of 90% is impossible and also really counterproductive. What we need is a flat rate around 25% for everyone with a small exemption, and then a vastly vastly smaller Federal government.

That ignores the fact that the ultra-extreme wealthy pay so little on proportion to the common man.

If Elon Musk (literally one of the wealthiest people ever) paid even proportional to Warren Buffett’s secretary, the U.S. would be in far better shape fiscally.

How in the heck does a person go from nothing to one of the richest people ever and barely pay any taxes? That is the sign if an unfair tax system.

Higher top end tax rates on the unjustly earned super profit corporations will level the playing field with the ordinary profit corporations without calling in the Federal Trade commission or Justice Department. Maybe 5% GDP growth in the 50’s.

Jay has a pile of ammo so he fired off a few warning shots with his pistol and he’s still loading bullets in his rifle to help slay deflation.

but stagflation? Pushing on a string? The only healthy way out (I’m aware of) is lower input costs (e.g. energy), and productivity rises. Will the bots save us?

“The Fed is not exposed to credit losses if borrowers default on mortgages because it holds only ‘agency’ MBS that are guaranteed by the government, where the taxpayer would eat those losses, not the Fed.”

Whether or not there is $1 dollar thrown on the taxpayer, just reading that makes me want to puke that it ever came to be.

Yeah. Would have been nice to get the government out of the mortgage business.

Considering the vast overlap between “home owner” and “voter”, i’m not surprised that the voting public disagrees with you, and would prefer the US Gov’t continues subsidizing the risk on their home purchases thankyouverymuch

i do agree it’s smelly business for the fed to get involved.

I got my subsidies, tank you. Ready to pull up the drawbridge.

Wolf, so the fed lets mbs gains be privatized when they are paying out on time, but ‘socialized’ when they are incapable of paying out on time? We didnt Sign off on that, did we? Say it ain’t so…

However it’s kinda like saying, I’m insulated from credit losses because my wife is backstopping them. They are the same entity for all financial purposes.

Except that the government guarantee is done mostly via Fannie Mae’s and Freddie Mac’s mortgage insurance guarantees, which gather decent and generally profitable insurance premiums to provide the mortgage insurance. Whether that insurance is priced correctly for tail risk and whether Fannie Mae and Freddie Mac should be spun back out from receivership, ok, fair discussion items. But it’s not like the government is just sitting out there handing out free money.

Yes it is. Underpricing insurance premiums is the same as a subsidy I. E. Handing out free money.

You can be sure that the govt insurance is underpriced, because otherwise, there would be private players willing to provide the same insurance. Think about it: if the premiums allowed for a profit after accounting for all risks, you can be sure that JP Morgan or Goldman Sachs would be first in line to offer it. After all, there’s no rule that a bank has to sell it’s mortgage to Fannie Mae. They could sell it to some other firm if they’re able to offer similar guarantees at a similar price.

Even tail risk can be managed. After all, home owners insurance manages tail risks of big hurricanes or wildfires. Either they manage it themselves or find a reinsurer, but it can be managed.

Of course the home buyer will not like paying market rate to insure their default risk, and they happen to vote, which is why Fannie Mae exists in the first place.

There is a great book: When All Else Fails: Government As The Ultimate Risk Manager. It goes so far and wide.

Monsieur Lune, you have no evidence, i.e. numbers, showing the mortgage insurance premiums are underpriced. You only have an inference based on the lack of private market participants.

There actually are companies that offer mortgage securitization services outside Fannie Mae, Freddie Mac, and Ginnie Mae. They just have a very small portion of the market. This group was larger and had more market share before the financial crisis.

There are a number of other reasons that these private market participants may not directly compete with Fannie Mae and Freddie Mac for market share. One, it is technically a different product. Having a guarantee that is directly backstopped by the federal government is a different product from a prudentially regulated private entity. Fannie Mae’s bonds will always be cheaper as long as they have a government guarantee, even if the mortgage insurance is priced correctly. And this arrangement might actually be a better product than a prudentially regulated private entity. Insurance always involves extreme “tail risk,” so a single insured investor (or other person) can never really insure 100% of their risk since a sufficiently extreme scenario can put the prudentially regulated private entity underwater. Having a government backstop can’t even insure 100%, but it might move ruin from a fifth standard deviation event to an eighth standard deviation event, which I might rather have as an investor.

Two, there is a certain level of scale needed just to diversify risk and spread out costs at a competitive level. It could be that the market only supports 2-3 entities at this scale. To have somebody else come in to compete with Fannie Mae and Freddie Mac would require 1) setting up the regulation, 2) getting relationships with banks and setting out underwriting standards for them, and 3) finding a bunch of investors to come on board and start buying insured mortgage securities despite little track record. As an analogy, right now State Street, BlackRock, and Vanguard are the only companies who have scaled very large index funds. Other market participants nibble around the edges with specialty ETFs. Is that evidence that State Street, BlackRock, and Vanguard are underpricing or subsidizing their ETFs?

I could go on.

“But it’s not like the government is just sitting out there handing out free money.”

Did you miss the TARP? The same thieves that sold liar loans ended up owning the best of 7,000,000 foreclosed homes. The next home-pocalyse will see that record played as an “oldies but goodie”.

No, I did not miss TARP. TARP was a one-off program that came with strings attached, including financial interests in the affected companies. AFAIK the only part of TARP that was actually a net accounting cost to the government was the auto industry. We’re talking about banks and mortgages here. TARP was literally not free money.

I don’t envy the position of the Fed. With the threat of stagflation they really can’t sell off MBS and bonds and what not to get inflation back to 2% (which imo should be a range of 2 to 3%). If inflation comes roaring back, they won’t have that weapon to use. The only thing would be to raise interest rates again.

Problem is if we enter a straight up recession, they already have too much on the books and printing more money will risk sudden inflation.

Then again, if tariffs ever do truly materialize, I don’t think there is anything the Fed can do fight back against inflation.

If there is a recession, they can cut rates. They have room to cut this time. Lots of room.

Where is the floor of any potential future rate cuts? If they go to zero then…. here we go again with ZIRP. Once it’s in place, nobody has the wisdom to raise it off of zero until something breaks.

People can always hope for ZIRP. We’ve had this stuff here since March 2022. Even the ECB doesn’t want to go back to ZIRP or NIRP. It’s already talking about ending the rate cuts, with its deposit rate now at 2.5%. And the economy there is a lot weaker than the economy here. There is no appetite from central banks for ZIRP. Generally, recessions last two or three quarters, and rates would be very low for a brief period, not years, and then get raised again toward something more neutral. That’s the classic playbook, and it looks like central banks are trying to play by it again.

Wolf,

I remember your article explaining why long-term interest rates in the US rise when the Fed lowers short-term rates.

The same is happening in the EU right now.

Yes, and suddenly and hugely. But this is not normally the case. It’s the case this time. In prior rate-hike episodes, this was unusual, and I believe that the 100-plus basis point jump of US 10-year yields in the months after the first rate hike was a fist-time-ever thing.

Markets in the US and Europe see increased inflation in the near future. In the US, this is already indicative. In Europe, with an 800 billion euro rearmament plan, markets expect inflation to jump.

In addition, France is in big deficit.

There was logic in your article that long-term interest rates are determined by the markets’ view of inflation, not by central bank policies and their impact on short-term interest rates.

I got the impression that this is a pattern that you simply share with your readers.

Wolf, if we are already in an inflationary environment, what happens economically if the fed cuts rates into that situation?

You gotta be more specific. Depends on how much inflation and how high the rates. Right now, rates are quite a bit higher than inflation. But if inflation is accelerating further and gets closer to Fed rates, and then the Fed cuts, that would be stimulative. But all the talking heads at the Fed, including Powell today, said they are not interested in cutting if inflation rises further. They’re on hold because they want to see where this is going.

And why is it your opinion to have inflation at 2-3%? Better for citizens would be 1-2% so savings and wage increases actually mean something.

Better still might be 0% but because the true value varies around the target and negative numbers (I,e, deflation) is very bad, the target needs to be just hight enough that these variations don’t go there. Hence: 2%

Here here!

The definition of good and bad is inherited, rather than *inherent*

Deflation is “bad” because we have a debt based economy.

Were we to have a production based economy, would it be defined as bad? It’s hailed (by the consumer) as a good thing that durable goods have been in deflation. The “good” could be seen in industry as a motivation towards greater efficiency and “on demand” manufacturing and sales.

Deflation is great for a saver: today’s dollar will become stronger tomorrow. It sucks for the world’s biggest debtor, so we have managed to codify the “bad” definition by living on the end of a limb for half a century.

The reality? “The rules are made up, and the points don’t matter” -Jim Carrey

DREW Carey… brain fart

Deflation is horrible for an economy. Absolutely terrible. All deflation does is encourage people to.stop spending.

Period. Full stop.

It doesn’t matter if you are a saver or a debtor. There is going to be pain in the future because the economy is going to shrink due to people collectively spending less. Everyone hurts. Plus it spirals. It encourages further non-spending.

Saying savers benefit during deflation means that they just get hurt a little bit less.

No one wins.

jimL says, “All deflation does is encourage people to.stop spending.”

He’s correct. When people get into the idea that things will be cheaper tomorrow (the very definition of deflation), they wait instead of buying today.

That hurts the economy which encourages further deflation.

It’s this positive-feedback loop that makes deflation so dangerous and why the target is 2% rather than something lower.

JimL and Brian,

You guys are thinking in extremes, which is never healthy. Spending will never just STOP. Deflation is a gradual process on the margin. There are times when people should be encouraged to curtail spending, like when debt and deficits are running out of control and threatening stability.

When we avoid recessions ( deflation) as a long term habit, we set ourselves up for massive displacements down the road. Recessions are healthy, particularly after huge unanticipated price run ups.

We need a good recession, we need some good deflation.

Where has that commenter been named “J Pow” (or similar), who always told us what he was really thinking?

I miss that guy.

Seems like they are getting close to stopping Treasury QT. Debt ceiling fights of course but just the overall level of balance sheet holdings. I think the next step could be “Maintain Treasuries around $4T and let MBS roll off naturally”.

At the pace of the last year it will be 10-12 years before all the MBS is gone and I don’t see why they’d sell them early just to speed the process. That forgotten pile of old Pandemic Mortgages will just whittle itself down and nobody is going to notice $15B a month of liquidity being removed.

I’ve suggested before that maybe if the Fed REALLY just wants to get that slop off the balance sheet could sell it for 70 cents on the dollar to the social security trust fund, book the loss against future Treasury profits, and call it a day.

Now that’s a clever idea. Shift the general US taxpayer from being on the hook to SS recipients and future recipients. Accelerate the shrinkage of the SS trust fund if mortgage holders go underwater. Could be a mortal blow to the SS program with Congress reevaluating its inflows and payouts as part of the program. Could lead to significant restructuring.

Since I have decades to go before SS eligibility, I’m open to the idea. It’d be good to hear others’ thoughts on the matter.

MR. Bear. FYI Social Security only buys US Gov bonds.

They do not buy mortgages.

Wall Street has long wanted to manage the $2 Trillion dollar trust fund (a 5% management fee will buy a lot of beer). Handing over that Trust Fund to the Private Sector is…… well, lets just say not a good idea.

The Treasuries that Social Security buys had their rates cut to next to nothing during and after the 2008 meltdown. That’s

why SS is in rough shape. The Big Banks always come first with

the FED.

Sporkfed

Thankfully, Social Security had the higher rates locked in via the long-term Treasury securities it had bought before the financial crisis. So the average interest rate fell gradually as those old securities matured and were replaced with low-yield new ones. But yes, that is part of the problem:

https://wolfstreet.com/2024/11/04/social-security-update-fiscal-2024-trust-fund-income-outgo-and-deficit/

Better to just abolish the FHA. The government should not be encouraging home ownership over renting. This isn’t the 1920’s. The economy requires mobility and flexibility.

If you draw a line through the data, it suggests they will end QE in this general vicinity. It appears the balance sheet needs to rise in the long term. As asset prices rise and inflation rises, transaction prices increase. More liquidity is needed to support the same volume of goods and services.

It’s a positive feedback cycle in some respects. Additional cash in the system is a hot potato.

Meant to say, they will end QT/QE in this general vicinity.

Well, I did say at a discount to reduce the risk. Those mortgages are paying, just slowly. It’s just that the SS fund can wait a decade where the Fed seems to want to get out of the mortgage business fast – and they should – and never get back in.

“Your access to this site has been limited by the site owner'”

Sweet Jesus big guy. I didn’t mean it. I didn’t do it. I was never there.

I am loyal. Must have been somebody else, in fact, I’ll collect names and turn them over to you.

I’m your biggest fan. I mix your name in my prayers.

Mercy, mercy, mercy.

Have I been dumped by DOGE(doggy)?

When this happens, turn off your VPN or change the city to get a different IP address. VPNs are doing business with comment spammers, which I block at the IP address, and then the VPNs assign the IP address to others like you, and you’re blocked.

Your VPN outfit knows you and your entire internet traffic. How do you know they’re not selling this info?

I get a huge amount of comment spam via VPN servers, such as yours. It’s a slimy business.

I explained this here and what to do when you get blocked: turn off your VPN or choose a different city to get a different IP address. Anyone who uses a VPN or thinks of using a VPN needs to read this:

https://wolfstreet.com/2025/02/24/dear-wolf-street-readers-are-you-using-a-vpn-heres-why-you-might-get-blocked-and-what-you-can-do-if-you-get-blocked/

MW: Powell says Fed can ‘wait for greater clarity’ on economic outlook

HI Wolf, If we look at Item 2 on the H.4.1 Release: “Maturity Distribution of Securities, Loans, and Selected Other Assets and Liabilities” It shows $1.426 trillion for Treasuries over 10 years in May 2022 (peak) and $1.551 trillion today. Does that mean the Fed has been doing surreptious QE at the long end – not rolling off any very long term bonds?

This stupid BS keeps circulating, doesn’t it? Don’t go back to websites that tell you, “the Fed has been doing surreptious (sic) QE at the long end” – they’re lying to you. And they’re totally clueless about bonds.

1. The Treasury roll-off is capped at $25 billion a month. Any amounts that mature over $25 billion are reinvested in new securities.

2. With these replacements, the Fed has been following the principle to replace like for like. So, when a 10-year note matures, the Fed replaces it with a new 10-year note.

3. A 10-year note that was issued 9 years ago has a remaining maturity of 1 year, not 10 years. It counts like a one-year security.

4. So when you replace a maturing 30-year bond with a new 30-year bond, the average remaining maturity of your portfolio goes up, and your holdings op 10-year-plus securities go up because you’re replacing a security that has zero remaining maturity with one that has 30 years remaining maturity. So you didn’t remove any 10-year plus maturities because the maturing 30-year bond fell out of that group 10 years ago, but you’re adding a new 30-year bond with 30 years of remaining maturity to the 10-plus years group.

5. This maturity creep has been publicly discussed by the Fed many times. It is now working on a plan to address it, namely by going away from its principle to replace like for like, and replace maturing notes (2-10 years) and bonds (20 and 30 years) with T-bills (1-12 months). This will bring down the average maturity of its holdings. I discussed this here:

https://wolfstreet.com/2025/02/25/future-of-the-feds-balance-sheet-feds-logan-on-how-assets-might-shift-from-longer-term-to-short-term-t-bills-repos-and-loans-after-qt-ends/

Thanks. “Surreptitious” may have been wrong in spelling and application, but the effect of “following the principle of replacing like for like” is, whether by design or co-incidence, to goose the long end of the curve (in the words of a former Treasury Secretary). Isn’t that right? The proposed practice of rebalancing the portfolio toward T Bills is going to hurt the long end and steepen the curve. Right?

Good to see the NFCI finally begin to tighten a bit! Is it due to QT or the recent market volitility?

Any thoughts Wolf on why QT didn’t have a more dramatic impact on liquidity? Seems like a long duration response in the markets. Maybe too much $$$ sloshing around?

The ON RRP was useless excess liquidity that couldn’t be put to work anywhere else, $2.2 trillion. So QT cleaned that out first, without consequences on needed liquidity. Now ON RRPs are largely gone, and QT is starting to drain reserves, and reserves are critical liquidity in the banking system. But the TGA is also now draining due to the debt ceiling, and part of that liquidity is going into reserves, and it’s temporarily covering up the drain on reserves from QT. After the debt ceiling is resolved, the government will refill the TGA very quickly, and this sucks liquidity back out of reserves. The Fed is very worried about the speed with which this happens after the debt ceiling. Article coming.

“Quantitative Tightening has shed 25% of total assets from peak”

Reckless FED stubbornly maintains 75% of total assets from pandemic high in spite of rampant inflation, continues to encourage widespread speculation and asset price bubbles.

There, fixed it.

You’ll never be happy, we’ve all come to accept that as a fact 🤣

I will be happy. Get rid of all MBS. Never do QE again, disavow the 2% inflation “target” bullshit and go back to the practices pre-Greenscum.

There was a LOT more inflation during long periods pre-Greenspan than there is now. And the balance sheet ALWAYS grew pre-Greenspan. It always grew with currency in circulation, which is demand-based… people wanting paper dollars (aka Federal Reserve Notes). And it’s the Fed’s job to provide them. They’re on the Fed’s balance sheet as a liability, and banks have to pay for them, and that money goes into Treasury securities on the asset site of the balance sheet so that the balance sheet always balances.

Wolf, and Wolfpack, Thank you for the core lessons (1st & foremost) and the added colorful comments. The matters around “that may suck $600 billion out of the money markets in three months (it did last time),” seems deeply concerning with retail PM responsibilities: so definitely as a mere wanna-be-student, i am very interested in info on the TGA and the lack of the ON RRP for the FED to lean on now daze. All the best of regards!!