For the 4th year in a row: Normal-ish mortgage rates, too-high prices, and the “lock-in effect” from the Fed’s reckless interest-rate repression.

By Wolf Richter for WOLF STREET.

Late last year and early this year, the story was that dropping mortgage rates, powered by big rate cuts from the Fed, would unleash demand in the housing market in the spring – the key spring selling season – and that sales volume would take off and that Realtors’ commissions would rocket to the moon.

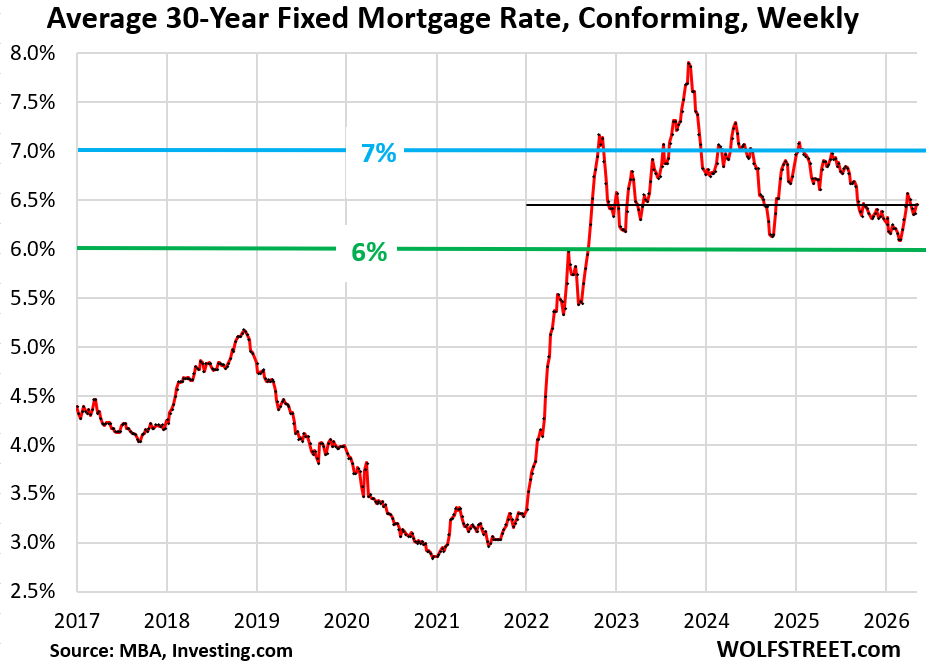

And so that didn’t happen. Inflation has been reheating for months before the war and before the energy price spike. The energy price spike in March and April then added to that resurgence of inflation. The Fed is now talking about a possibility of rate hikes as next move. And longer-term Treasury yields, such as the 10-year Treasury yield, rose in March and April in response to inflation fears. Mortgage rates, which track those Treasury yields but are higher, rose back to the 6.5% range. And the housing market remained in the same-old-same-old frozen pattern that it has been in for four years after the price explosion from mid-2020 through mid-2022. And it continued in the latest week.

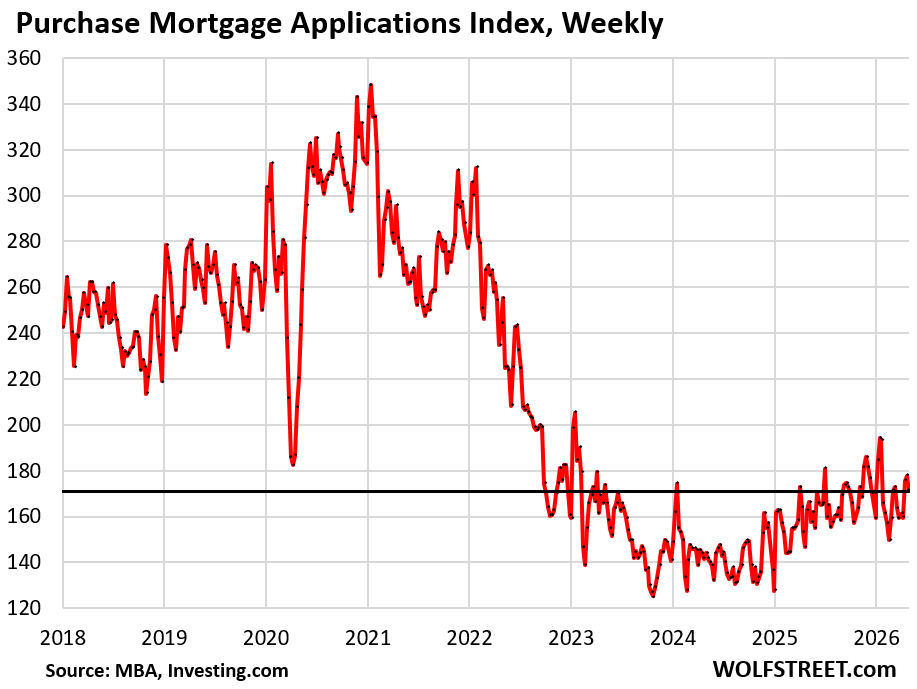

Mortgage applications to purchase a home – a measure of demand that may become actual home sales in the future, so a forward-looking indicator of home sales – dipped in the current survey week and remained near rock-bottom levels, down by 34% from the same week in 2019, according to data by the Mortgage Bankers Association today. That level of mortgage applications is below even the collapse of mortgage applications during the lockdown in the spring of 2020.

The average weekly mortgage rate for conforming 30-year fixed mortgages rose to 6.45% in the latest reporting week, according to the Mortgage Bankers Association today.

For the past 7 weeks, this measure of mortgage rates as been back in the middle of the 6-7% range, the range it has been in since September 2022, except for some breakouts to the upside.

These mortgage rates are not high in a historical context; they’re only high in the context of the Fed’s QE which started in 2009 and took on mega-proportions during the pandemic.

Under its QE programs, the Fed bought trillions of dollars of securities, including mortgage-backed securities (MBS), which repressed mortgage rates below 3%. But this massive amount of reckless money printing was part of the toxic mix at the time that triggered the worst inflation in 40 years. With mortgage rates below 3% and inflation at 9% – negative “real” mortgage rates, better than free money – home prices exploded and are now too high. And that inflation has refused to go back into the bottle.

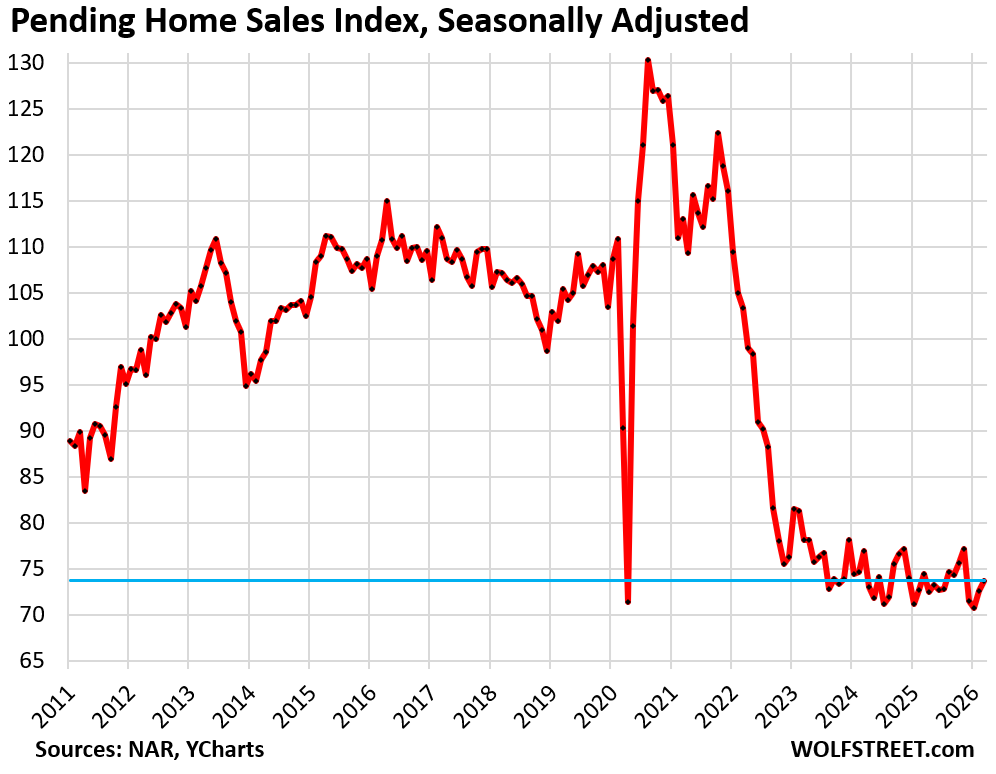

Pending home sales for March – deals that were signed in March but haven’t closed yet – also remained at rock bottom, down by 30% from March 2019. In January, they’d dropped to a record low in the data by the National Association of Realtors going back to mid-2010, and in February and March, they inched up from that record low.

And the much-hyped spring selling season has turned into the fourth dud in a row: 2023, 2024, 2025, and 2026.

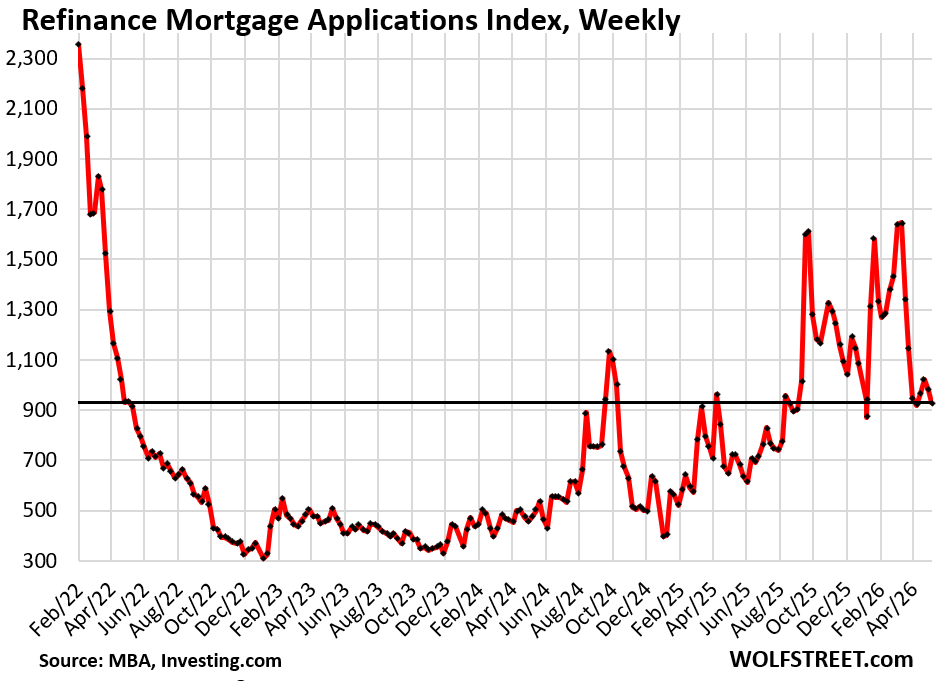

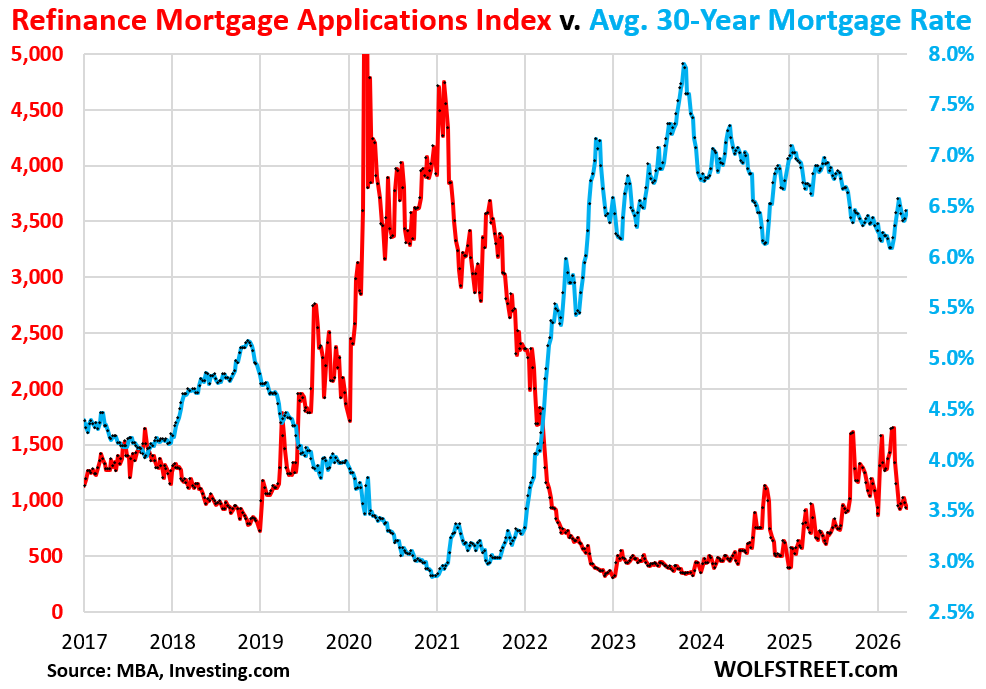

Mortgage applications to refinance a home instantly react to even small changes in mortgage rates. A dip in mortgage rates unleashes homeowners like a coiled spring to refinance a mortgage at even a slightly lower rate. And when mortgage rates rise after that dip, demand re-fizzles. These dynamics have been repeated several times since mid-2024.

Refis do nothing for the housing market, though they’re crucial for the income of mortgage brokers and lenders. But they may have a positive impact on consumer spending when they lower the mortgage payments and leave borrowers more money to spend on other stuff; or when they’re cash-out refis, the proceeds of which might then be used to pay down more expensive debts, or might be used for spending projects.

The up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – are generally added to the loan amount where they’re largely out of sight but increase the payment, which reduces the advantage of lower mortgage rates.

Homeowners can do a breakeven analysis with online calculators or through brokers and mortgage lenders, to see if refinancing a mortgage is worth it. When mortgage rates briefly drop and the breakeven analysis tilts their way, they pull the trigger, thereby creating these curious spikes in refis.

But even these spikes in refis since mid-2024 were relatively low compared to the two-year refi boom from early 2020 through 2021 when the Fed’s QE repressed mortgage rates below 3%, and everyone and their dog refinanced into these low-rate mortgages.

And now they’re part of the “lock-in effect,” when these homeowners avoid buying a new home, and thereby selling their current home, because the new home’s much higher price would have to be financed at a much higher mortgage rate, and that math doesn’t work very well for many people. But life does happen. My analysis: Update on the “Lock-in Effect” in the Housing Market: Below-3% & 4% Mortgages Fade Very Slowly

This longer view demonstrates the inverse relationship between mortgage rates (blue) and applications to refinance a mortgage (red):

In case you missed it: New Single-Family Home Prices Drop Further amid Inventory Glut. But Lower Prices Beget Higher Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When people rush to refinance after a measly 1% drop in mortgage rate, it tells me many people are financially squeezed and they think rates are going up, not down, in the future.

Generally, it’s beneficial to hold off refinancing until there is a significant benefit, so that if rates keep dropping, you don’t refinance multiple times. The costs of refinancing are somewhat hidden but costly.

It just makes financial sense in terms of cash flow if you can save $200 a month, so $2,400 a year — You expect to sell the house in a few years at a profit and pay off the mortgage with the proceeds. That calculus has been going on forever. What’s different now is that it’s easy to calculate the breakeven in real time and that refinancing a mortgage is much faster than it used to be.

For example, if the mortgage = $500,000 and rates drop by 50 basis points to 6.0% from 6.5%, and the refi fee = 1%, the mortgage balance goes to 505,000, your payment drops by about $133 a month, or by about $1,600 a year, every year for the term of the new mortgage.

You’re obviously still in the hole for 3+ years due to the fee that was rolled into the mortgage, but that’s on paper, not cash, and the hope is that you can sell your house for more a few years later and pay off the entire mortgage from the proceeds.

But if home prices drop enough in your market, a lot of these kinds of calculations don’t work anymore.

Obviously, you could save a lot more by not borrowing at all, and lots of people do that, but that’s not an option for the majority of people.

Thanks wolf

“…too-high prices, and the “lock-in effect” from the Fed’s reckless interest-rate repression.”

It’s the gift that just keeps on giving 5 years later. The FED absolutely destroyed the housing market, and all shelter prices. I know of a handful of personal friends and acquaintances who did cash-out refis under 3%, substantially lowered their monthly, then took that cash windfall and poured it into another house as an “investment.”

These people act like geniuses, and they are living large. They took the gift the FED gave them and ran with it. They are asset rich (also heavy into stocks and crypto) and are spending like crazy, propping up this economy. What’s so obscene about it all is that their prolific spending is also continuing to hurt those who have no assets. And the current administration wants to continue this “wealth effect.” We have a president cheerleading the stock market daily. Trickle-down eCONomics is a lie and a scam.

What a mess…

Thanks WR,

The prices are still too high and it needs to come down by 40% or so in my socal city.

But in socal, real estate is a like a religion. People would die before selling homes they have horded.

The FED did a criminal act by buying MBS when the housing market was on fire. By doing this, FED have locked out a generation of young Americans from the housing market.

Long delayed price capitulation (from all time highs, albeit!) is all the more weird when US demographics are taken into account.

The Baby Boom ran from 1946 to 1964 – so let’s say 1955 was the birth year of the median boomer (truth probably skews a little more towards 1964 but 1955 is pretty close).

That *median* boomer was 60 in 2015 and 70 in 2025 (not to mention the 50%’ish, pre 1955 boomers).

I think it is safe to say that a *lot* of analysts in the late 90’s thought that the great boomer home sell-off (spiking inventory supply, dropping prices) would have started a long, long, looonggg time before now.

Plenty of intervening factors (frequently crappy US economy, ZIRP, pandemic, etc.) but demographics tends to outweigh almost everything.

And, yet, here we are, with the oldest Boomers hitting 80…and still not seeing that demographics-driven SFH supply spike.

People generally want to stay in their homes until the end. Getting shuffled out of their homes and off to PE-firm owned assisted living centers is not what boomers always dreamed about.

If a Boomer is even remotely healthy and of sound mind, they aren’t selling $#@! — and even if not in good health, they’re still most likely not selling. Where are they going to go?

My father-in-law is 76 with Alzheimer’s and the mother-in-law, 73, has her own host of issues. They have no where to go and we won’t support them (based on previous life choices). They will claw and fight tooth and nail to stay in their home until there is no other alternative — either grave or Medicaid facility.

Just wait until people are locked in at 6%

Love the inverse relationship graph!!! Great job Wolf!!!!

SingleMaltScoth, something to think about.

After a certain age, our parents slowly become our children. They ask simple questions, repeat stories but depend on our patience the way we once depended on theirs. Very few understand this role reversal when it most matters. What looks like innocence or inconvenience is really time coming full circle. Don’t correct them harshly. Don’t rush them. Simply care for them the way they once protected us. This isn’t a burden. It’s repayment quietly wrapped as love.

Howdy Folks. Love the last paragraph about our Prisoners…HEE HEE

Wanna Get Away??? You can t.