The spike of the “non-traditional reserve currencies.”

By Wolf Richter for WOLF STREET.

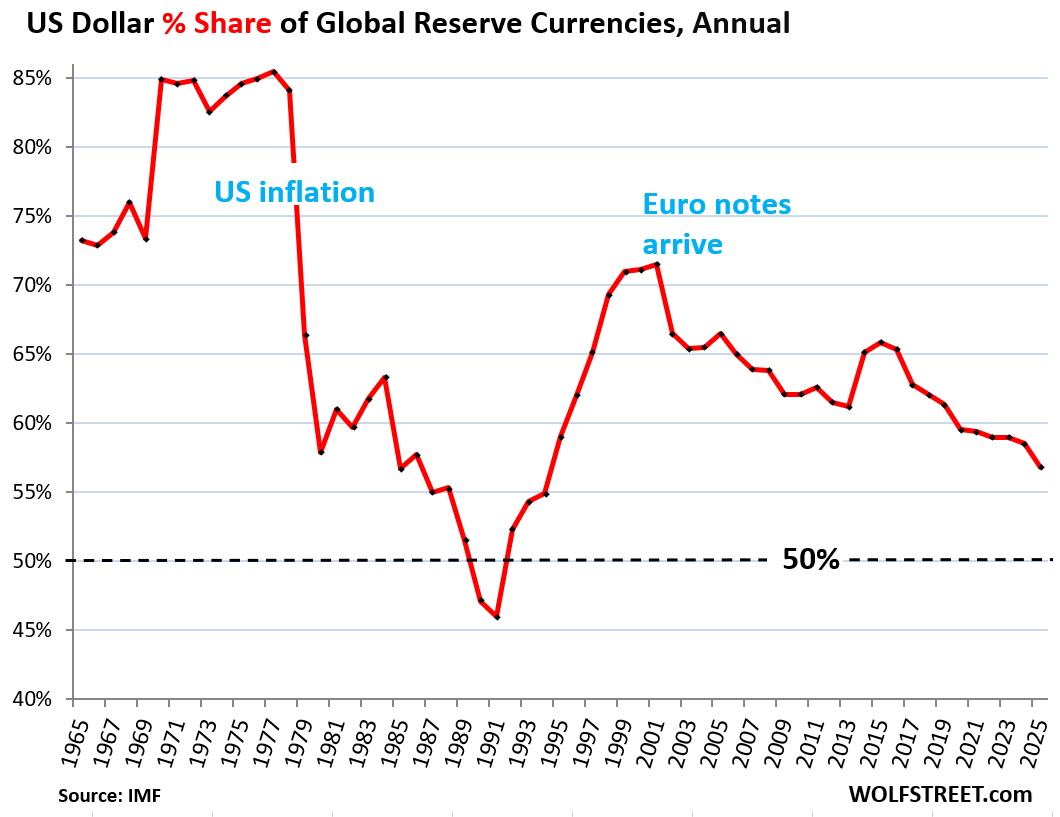

Foreign central banks have not been dumping US-dollar-denominated assets. But they’ve been loading up on assets in other currencies, and their total holdings of foreign exchange reserves have ballooned, while their USD-assets have remained nearly flat for over 10 years. So the share of USD-denominated exchange reserves dropped to 56.8% of total foreign exchange reserves in Q4, the lowest since 1994, according to the IMF’s data on Currency Composition of Official Foreign Exchange Reserves, released on Friday.

It has been zigzagging down toward the 50% line for years. It does have consequences. And it has been there before.

USD-denominated foreign exchange reserves are US securities held by central banks other than the Fed. They include US Treasury securities, US mortgage-backed securities (MBS), US agency securities, US corporate bonds, and other USD-denominated assets.

After a long plunge from a peak share in 1977, the dollar’s share broke through the 50%-line in 1990 and dropped further in 1991. This period from the mid-1970s through 1991 was accompanied by waves of sky-high inflation and interest rates, four recessions, including the nasty Double-Dip recession, and high unemployment. And other central banks lost confidence in the US dollar.

But then the economy picked up, inflation calmed, the Dotcom Bubble began to perform miracles on a daily basis, confidence returned, and USD denominated assets became desirable again.

Enter the euro. European politicians were talking about “parity” with the dollar until the Euro Debt Crisis began in 2009. Since then, the euro lost share and then stalled, as central banks diversified into other currencies, and since 2021, into dozens of smaller “non-traditional reserve currencies,” as the IMF calls them. Throughout, the dollar’s share zigzagged down toward the 50% line.

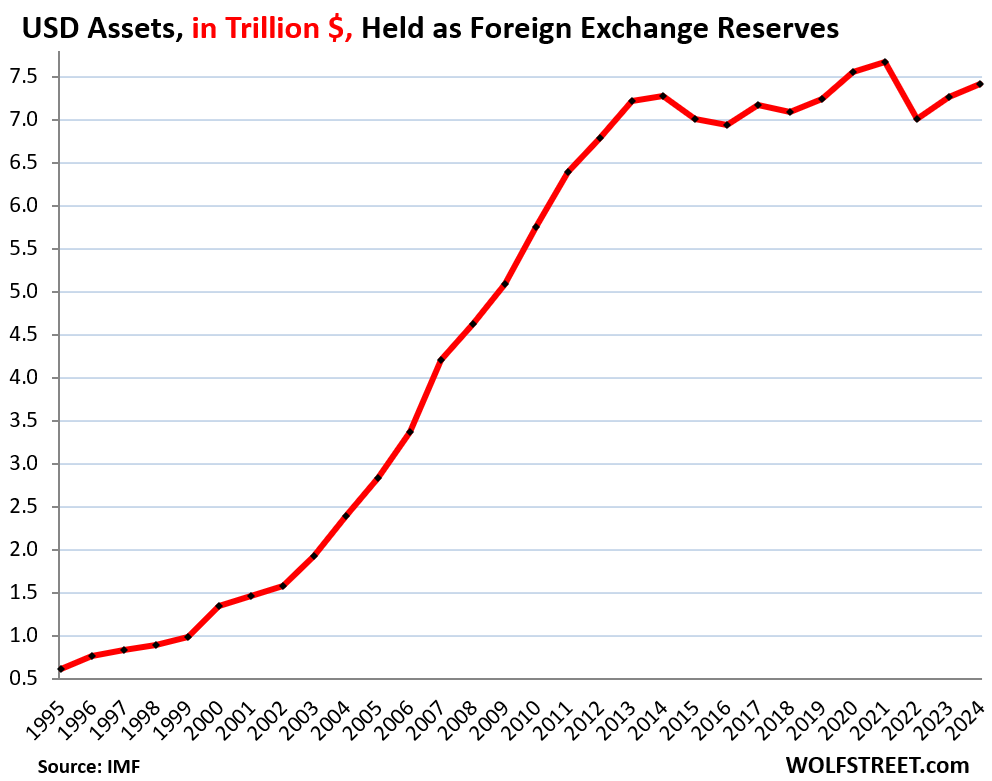

But central banks didn’t dump USD securities.

Since 2013, foreign central banks have roughly maintained their holdings of USD-denominated assets. In Q4 2025, their holdings of $7.46 trillion of US securities were up just a hair from 2014, but below 2020 and 2021.

What has caused the share of USD assets to decline over these years was the surge of assets denominated in dozens of other smaller currencies.

Why this matters: the “twin deficits.”

When foreign central banks buy US Treasury securities and other US securities, they in essence provide some of the funding for the huge twin deficits the US has: the trade deficit and the federal budget deficit. Being the top dog in terms of securities that other central banks buy – having the dominant reserve currency – has enabled the US to run those twin deficits for decades.

This path is obviously not permanently sustainable. And the “twin deficits” need to be brought down substantially before something goes off the rails, such as a surge of inflation and much higher bond yields, and all the issues that come with it.

Foreign exchange reserves by currency.

Central banks’ combined holdings of foreign exchange reserves in all currencies, and expressed in USD, rose to $13.14 trillion in Q3.

Excluded are any central bank’s assets denominated in its own currency, such as the Fed’s Treasury securities or the ECB’s euro-denominated securities.

Top holdings, expressed in USD:

- USD assets: $7.46 trillion

- Euro assets (EUR): $2.66 trillion

- Yen assets (YEN): $0.76 trillion

- British pound assets (GBP): $0.58 trillion

- Canadian dollar assets (CAD): $0.33 trillion

- Australian dollar assets (AUD): $0.27 trillion

- Chinese renminbi (RMB) assets: $0.26 trillion

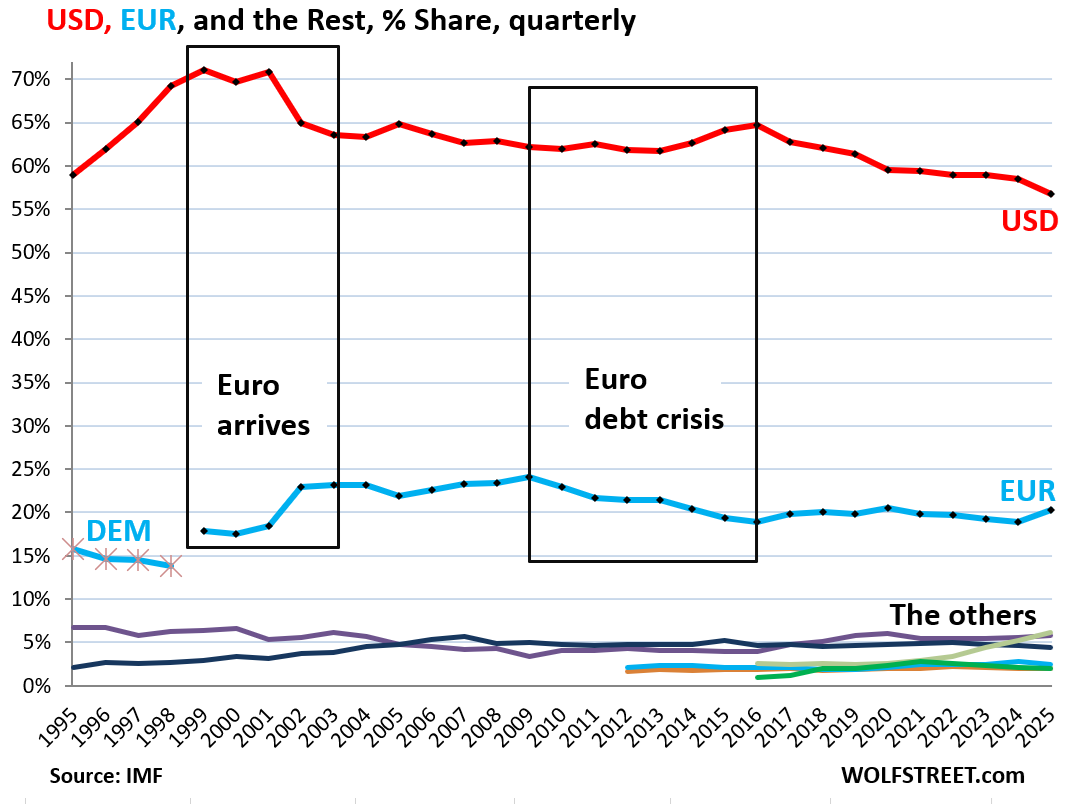

The euro’s share has been around 20% for the past 10 years. Just before the Euro Debt Crisis, it had risen to nearly 25%.

Note the blue “DEM” on the left – that’s the Deutsche mark with a share of about 15% in the mid-1990s. It became the dominant founding currency of the euro.

The rest of the reserve currencies are clustered at the bottom of the chart. But that’s where the action is (more in a moment).

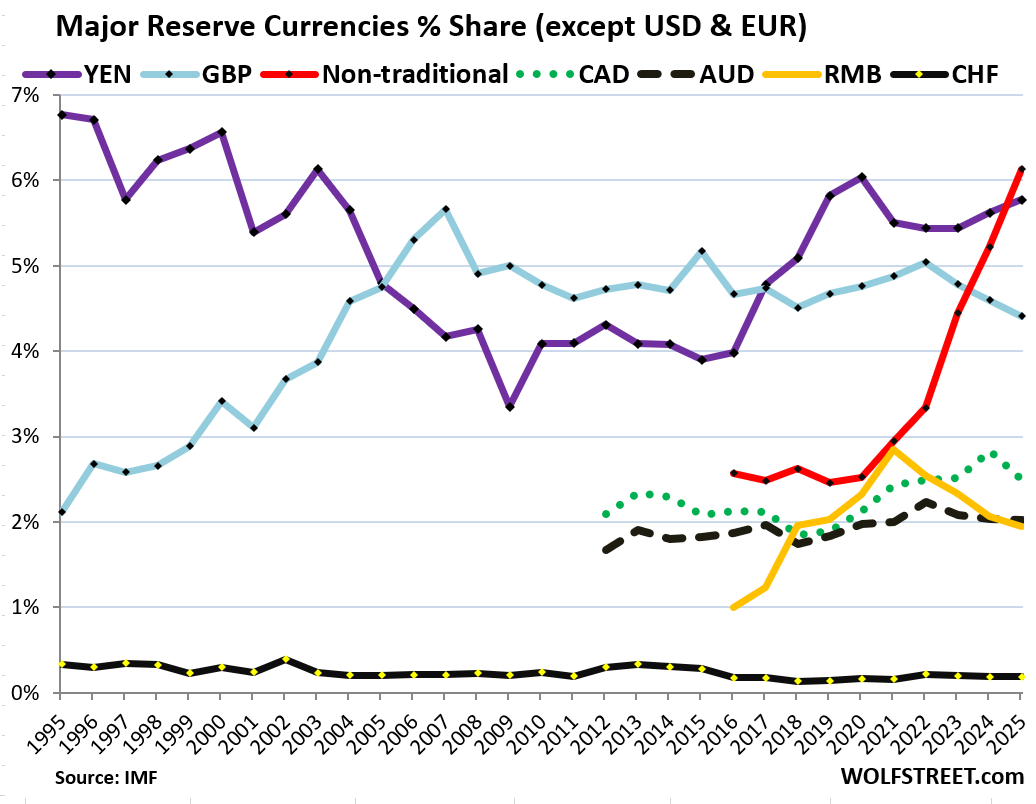

The spike of the “non-traditional” reserve currencies.

The chart below magnifies the cluster of lines in the chart above.

The soaring red line represents dozens of “other currencies” – other than the ones the IMF specifically names here. These dozens of smaller currencies are what the IMF calls the “nontraditional reserve currencies.” Each has a minuscule share, but their combined share has more than doubled since 2021 and hit 6.1%, surpassing the yen.

These “non-traditional” currencies are where much of the diversification away from the USD has occurred.

The share of the RMB (yellow) ticked up to 2.0%, after declining since Q1 2022. China has the second-largest economy in the world, and is hugely interwoven in international trade. But its RMB-denominated assets are not sought-after by other central banks, amid ongoing capital controls, convertibility issues, and other issues.

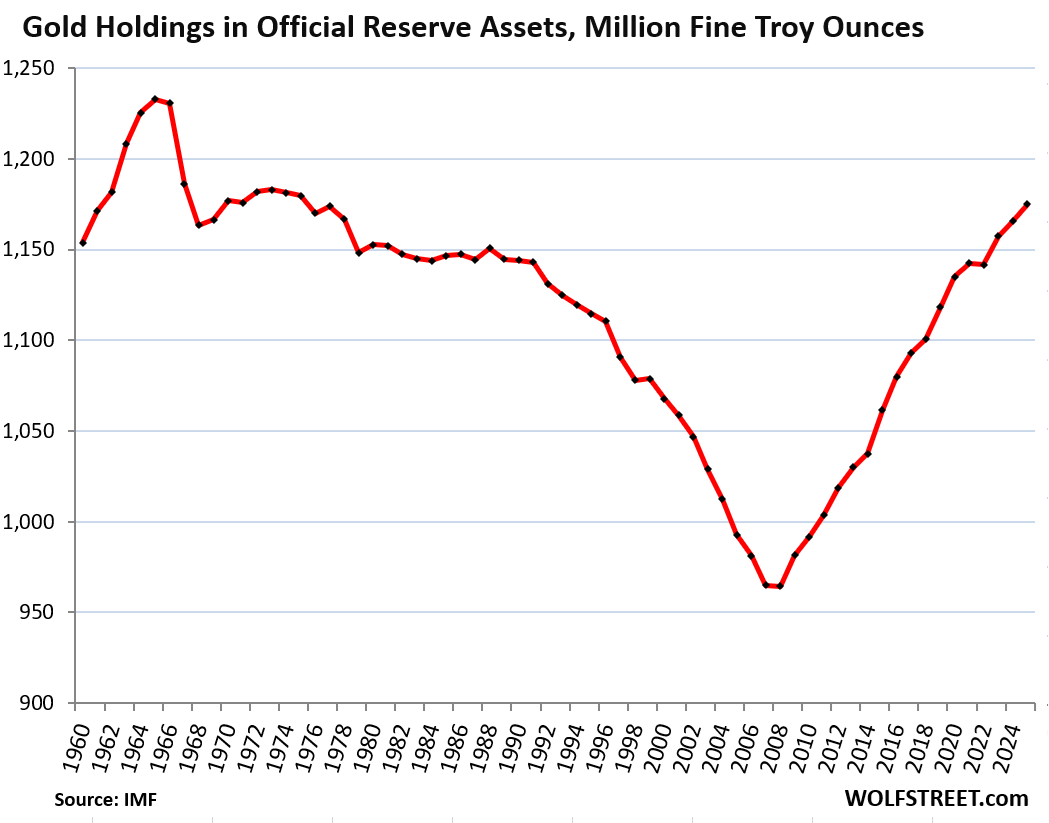

Gold, the non-currency diversification.

Gold is not a “foreign exchange reserve” asset of central banks, it does not involve a foreign currency, and it is not included in the data above, so it doesn’t belong in a discussion of reserve currencies. But it’s part of the broader “official reserve assets” that foreign exchange reserves are also part of, and it is an asset that central banks are diversifying to, as they ease away from the USD, and in that respect, it fits in.

Gold holdings by official authorities rose by 0.8% year-over-year to 1,175 million troy ounces at the end of Q4, back where they’d been in 1977, according to the IMF on Friday.

In 2008 and 2009, when the global financial system seemed to be at risk, these central banks changed their minds about gold and started buying hand-over-fist, after having spent the prior four decades dumping their gold holdings.

In 2025, the price of gold lost its oomph. After a huge years-long rally, it topped out at $5,627 on January 29 and today is down 20% from its all-time high. Despite the drop, gold is still up by 44% from a year ago and by 100% from two years ago. Part of this years-long price surge may have been driven by central-bank buying and by the intense hoopla and hype around it.

Official gold holdings at the end of 2025 would be valued at $5.27 trillion at today’s price, compared to $13.0 trillion in total foreign exchange reserves, and $7.46 trillion in USD-denominated foreign exchange reserves:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not to worry, USD denominated stable coins will keep up demand for the dollar for years to come (s)

While US treasury would have given you ~120% since 2008 @ 4.5% anually, gold has returned 550% in the same time.

You can all see why chart for treasury held by other central banks is flat while the chart for gold keeps rising.

From the end of 2012 to now, gold returned barely more than 100%, with a 50% plunge in between. That is “risk.” You don’t understand what risk is. Investors need to get paid adequately to take risks like that.

I guess that is why they say diversify??i

Maybeeee??

An arbitrary choice to start in 2012 just before a long decline. Let’s use Aug 15, 1971 (end of Bretton Woods). What this tells me is that dividend reinvestment makes a huge difference, as otherwise the S&P basically kept pace with silver. The S&P 500 does have the benefit of periodic rebalancing, otherwise the dogs would drag it down dramatically. Not bad for the barbarous relic, given all that.

S&P 500 total-return (dividends reinvested)

1971-08-15 TR index: 39.12

2026-03-29 TR index: 14,203.24

Cumulative return = 36,270%

S&P 500 price return (no dividends)

1971-08-15 price index: 101.33

2026-03-29 price index: 4,247.22

Cumulative return = 4,092%

Gold (XAU/USD spot)

1971-08-15: $40.62/oz

2026-03-29: $4,507.70/oz

Cumulative return = 11,096%

Silver (XAG/USD spot)

1971-08-15: $1.62/oz

2026-03-29: $69.78/oz

Cumulative return = 4,207%

Lets pick a starting point and end point that suits your narrative. That was my point in my reply to J Pow

MELANIN EXTRACTION RESEARCH IS THE FUTURE OF ARTIFICIAL INTELLIGENCE ENERGY, IT’S ALIVE AND ORGANIC…

Gold returned over 500% for about 20 years, when it became extremely cheap relative to oil. This is the time the Russian central bank started to buy gold based exactly on that ratio. The annual return for the gold bought back then is 20%, mas or menos. That is still a pretty good return. If we go back ten more years gold, when the gold price plunged to about 200 per try ounce, gold is now twenty five times more expensive and returns are just incredible.

The price has now been chopped by about one-fifth.

When I think of the stability of stable coins clearly beyond the hoopla I can’t seem to get beyond the mathematical fact that they are worthless.

A well-run stablecoin is backed dollar for dollar by good assets, such as Treasury securities. A well-run stable coin buys $1 of assets for each $1 of stablecoins it sells. Think of it like a money market mutual fund. Stablecoins are different from cryptos. The only thing they have in common with them is that they’re on the blockchain.

The biggest USD Stablecoin (Tether): is “fully” backed. or so. mostly. sometimes.

Yes, so backed by equity stakes in startups, etc. In addition to T-bills.

The crypto landscape is full of cowboys shooting it out. But well-run means “well-run” not “Tether.”

If a stablecoin wants to become a broad payments method, not just a way to trade in and out of other cryptos (which is what Tether is for), then it will have to be “well-run,” such as common money-market funds.

but zero inflation protection from holding stable coins, and it’s illegal for stable coins to pay holders any of the interest they collect from the treasuries they hold, so it’s not exactly like a mutual fund. And they aren’t FDIC insured, so who knows what happens if there’s ever a run on the treasuries they hold and they dump them into dropping market. Maybe they get to be called Too Big To Fail and get a taxpayer bailout, like a mutual fund company might

“And they aren’t FDIC insured, so who knows what happens if there’s ever a run on the treasuries they hold and they dump them into dropping market.”

Same with money market mutual funds. And we know what happens… they “break the buck,” the NAV falls below $1.00, and stablecoins will do the same, depending on the quality of their assets.

If they’re into other stuff, such as illiquid equity in crypto startups, they can collapse like a bond fund.

Fantastic post Wolf, thank you!

such a great analysis. thanks. i think with turmoil in mideast the gulf states princelings…… just conjecture, must be selling gold to move to safer mansions they own in london, nyc…….

I would like to hear rational thoughts on:

1) Alternatives to the US Dollar that are safe

2) How would unwinding from the US Dollar take place, given the current world exposure to the US Dollar

3) Timeframe of a new world currency

I have been around for a while and have heard about the demise of the dollar, but it has never happened.

If it did, the US would be forced to eliminate its Trade and Budget deficits, so maybe a change would not be so bad.

People waiting for the “demise of the dollar” will have to be very patient. The play, “Waiting for Godot,” captures that.

There is nothing wrong with the “dollar.” It’s just a currency. What is wrong are the structural issues, including the twin deficits.

It doesn’t matter fundamentally how people pay for stuff, whether it’s by bank transfer, some other electronic means (credit/debit cards, PayPal, etc.), or stablecoins. It makes no difference to the economy or the dollar, but it matters to companies in that industry that extract fees. If payments shift to stablecoins, then banks, credit card companies, PayPal et al. lose out on the fees.

But the US will face some structural issues with its twin deficits when the world is no longer willing to fund them. Those structural issues could be pretty rough, such as high inflation and high interest rates, and the issues they cause. If the Fed tries to keep interest rates low by buying bonds while government-borrowing goes haywire in an inflationary period, inflation will spiral out of control, and the Fed knows that, which is why it won’t do that. Americans have a relentless history of evicting anyone from the White House who they see responsible for this inflation. The way forward for anyone in the White House, Congress, and at the Fed will be to keep inflation in the moderate range and deal with the structural issues. And when foreigners are no longer willing to fund the twin deficits, it will eventually force the government to deal with the twin deficits. And there still won’t be the “demise of the dollar.” (Spoiler alert: Godot never showed up).

Was going to get a personalized license plate that read GODOT but it’s been issued to some other clever person.

Digital ccys will disintermediate payment systems like credit cards, PayPal etc outside the US. Stablecoins are miniscule and not really a thing outside of USD.

The Chinese don’t seem to be in any hurry too take on the mantle required of a reserve currency. A thankless honor for anyone else besides the USA, A society who were bred too kill the golden goose because life was too easy.

At least that is what I think of as a macro economic issue which is not a free market in any sense of the word

Good times lead to weak men…

…hedge accordingly.

I know you probably wanted Mr Wolf’s thoughts, but here are mine just in case you care. I think it’s worth keeping in mind how big the financial system of the world is and how important US debt is in its plumbing. I often hear unduly complacent commentary trying to compare this to the fall of the British Pound or even the Dutch Guilder (not pointing any fingers at anyone around here, just commenting in general), but that totally underestimates the size of the current financial system. There are 10 times as many people in the world, the economy is hundreds of times bigger, and actually those currencies were confined almost entirely to Europe. There are too many pension funds, insurance companies, etc, that are required to hold safe assets, and the system works by them using US bonds right now.

It seems like this is happening in slow motion, but it is a much bigger change than it appears. Container ships take a long time to turn around (so I am told), and in the modern economy, there just aren’t enough German bonds to go around to replace USD right away. That doesn’t mean the current situation is sustainable. Also, realistically, the US was 40 percent of world GDP in 1960, now it’s around a quarter, depending on how you measure. Even though I don’t personally expect China to continue such a dramatic rise, I do think the world will continue to grow faster. It’s just not in the long term possible for the USD to remain the world’s reserve currency, and I think a multi polar world is inevitable. Though this particular 3D chess move of starting a war with Iran, right after poking the US’s allies’ in the eye, does surpass my understanding of good strategic policy, I must admit. I could see how it may cause that transition to happen a little faster than it otherwise would have.

As for practical advice, I would follow the central banks by diversifying. Buy low cost index funds across the world economy (weighted slightly to your home country). Keep in mind that there are treaties that affect how dividends are taxed (depending on your jurisdiction), so hold international stocks in accountants that are exempt when possible. Never buy a ticker symbol that you read about in a comment section (except low cost ETFs). Personally, I see no reason to hold other countries’ bonds, but am a firm believer in holding their equities. I still think having some bonds is worth it, because you aren’t trying to beat the market (you should make your money having a job that you are good at, unless being a trader is your job). The point of bonds is that you are hedging against wide risks, including some that may not have ever happened yet, so just because bonds have historically not performed as well as stocks (even in downturns), doesn’t mean they aren’t worth it.

It’s worth keeping in mind that our financial system has changed considerably over the years, and isn’t very old yet. I don’t care very much about what happened in the 80s and 90s, let alone what happened while we were still using the gold standard.

Finally, speaking of gold, I don’t like it. I prefer assets that at least pay me something, and I consider good sovereign debt safe still (I know not everyone does). If you do like it, hold a little.

“Finally, speaking of gold, I don’t like it” – neither does the FED. The last thing in the world they might want is a monetary role for Gold.

“I prefer assets that at least pay me something” – the fact that they pay you something means there is a creditor on the other end. In the last 5 years we’ve learned that, that creditor can decide to “freeze” the debt and pay you neither interest or return the principle.

The attraction of Gold is that there is no counter party if you hold it in your vault.

General Gold is not held by individuals as an investment, it’s held as insurance. In the current emergency in Iran, we’ve seen a 20% drop in gold priced in USD. We also find that Turkey sold 58 tons of Gold to try and keep Lira afloat. Other Gulf State holders of Gold are probably also selling since their USD revenues have dried up. Dubai has been a major hub for physical Gold settlement where gold was routinely flown in and out. Air flights into Dubai are not happening since like all the gulf countries, they are being “protected” by the US.

Gold will find it’s bottom, either here or around 3500.

Iran’s only possible strategy is to hold out, keep the strait closed and shoot back once in a while with the aim of disrupting the global economy which will tip over the equity and bond markets and make it more difficult for the US to fund itself.

Irans strategy then is to create a monetary crisis. Everyone scoffs at that idea, they are ragheads after all and Islamic madmen, medievalists etc…But it’s week 4 and “Whats going on with Shipping” provides daily hard data on the number of ships entering and leaving the Gulf. Normal traffic is 100+, now it’s a few and those are passing through Iran toll booth between Queshem and Larek islands. The pipeline that allows loadings in the RedSea and offshore Oman are maxed out. So 5-6 million BPD out that way and maybe another 2 or 3 MBPD of Iranian oil – normal flow is 20 MBPD.

None of us should imagine that we really know whats going to happen. In the near term, I hold my Gold and cautiously buy more and enjoy the slightly improved yields on my Cash.

I hold gold for insurance too, but it does not seem to work for all catastrophes. Ones which force other holders to cash in, for example. I also have real estate, utilities, telecoms

Still need to figure out when I’d ever cash in on the gold and what other insurance I need.

Danf51

“General Gold is not held by individuals as an investment, it’s held as insurance”

I purchased gold a handful of years ago, and then I sold it.

It was a pure profit investment play that worked as hoped. It was not insurance, because I was not for sure.

Nobody else is for sure either…. They just would like to think they are for sure about things and stuff and whatevers. But anyone that says they are for sures is blowing some smoke.

It is all just risk vs. gain….

calculated risk…

diversify…etc.

It will probably be just fine…maybe

Who are you speaking about when referencing “madmen and medievalists”?

I disagree with your assertion that the wall street gyrations are random

More like the mob’s preferred outcome

Gold prices decrease when real returns increase – when bond yields increase and / or when it is believed that inflation is decreasing.

What is interesting is that in past flight to safety events the USD strengthens and bonds yields decrease – both with have not happened this time as much as expected.

Gold may be becoming the new canary in the coal mine of the state of the global economy.

Some are selling gold to de-risk, others are selling to pay off margin calls, or protect currencies.

The Fed appears to have re-Started QE last December which could be inflationary.

It will be interesting to see whether this war ends up causing inflation or a recession.

Personal alternative to USD? Try looking at the Singapore dollar.

Initially this made my teeth curl, but not as much as an IPA.

But from what you wrote, it appears the US dollar is just fine. For fun, I did a deep dive into SWIFT and discovered the US dollar as a percentage of SWIFT payments has increased quite a bit, and that SWIFT payments have increased overall. The EU had their percentage share of SWIFT payments in Euro drop by nearly 50% though. Interesting. China edged up a bit.

I though the China CIPS or mBridge might have made a dent but it appears the US economy and currency remains pretty dominant. It’s a pretty impressive and powerful economy. Good article, made me think. Thanks

Lol. IPA is the same for me.

I do think given the relative shortness of duration of the American empire we don’t get the long game. We are celebrating 250 years like it is some historically long empire duration. China on the other hand is an empire that knows the ups and downs and builds and executed 5 year plans. The US plans basically change every 2 to 4 years outside of a few key things like military spending. I honestly think the US has never had a grand plan, just a lot of wealth and resources and of course WWII greatly helped us or in some ways made us as relevant as we are today. Today, for example. Oil and defense are doing great, but hard to really put others in that position, certainly not average citizens.

Digital ccys will disintermediate payment systems like credit cards, PayPal etc outside the US. Stablecoins are miniscule and not really a thing outside of USD.

“ China has the second-largest economy in the world, and is hugely interwoven in international trade. But its RMB-denominated assets are not sought-after by other central banks, amid ongoing capital controls, convertibility issues, and other issues. “

To add, China never intended to become a dominant reserve currency or even try to replace the dollar. However, in very recent times, it seems they have decided to become the number one in finance as well, in the coming years, given all the abuses and misuses of western oriented driven int. based economy (ie. Sanctions , etc).

The unnecessary war in PG may only accelerate the change from petro dollar, as the oil transaction (~5%) are taking place in rmb, right now. Once the dust settles, the oil and gas are expected to be in rmb (~20%). Not just those, also urea, helium and other relevant petro based industrial essentials produced from PG based entities. This would also include all other int. based related transaction from the PG based economies to be conducted outside of dollar. This does not indicate the end of dollar reserve currency. It just means the dollar would no longer be the only dominant reserve currency.

This unnecessary war may very well be the Sues Canal Moment. Just ask the pitiful briteesh barons, whose sorry a$$es was kicked all the way back to their lil’ islands by the forefathers. Sun eventually sat down. These for ever wars and imperial ambitions too, will come to an end.

There are no “petrodollars.” They vanished many years ago because the US has a HUGE surplus in the energy trade, it has a surplus in petroleum and petroleum products (gasoline, diesel, jet fuel, etc.) trade, it has a gigantic surplus in the natural gas trade and is the largest exporter of LNG in the world. The surplus brings some of the dollars back to the US that left the US due to the trade deficit in other goods, such as in consumer goods. Now go back and re-think your theory.

Maybe in opening myself up to getting roasted here )I doubt I’ll go back to this thread to read it anyway)

But how can you really say that. If the gulf countries / OPEC decide to do business directly with countries in their currencies.. wouldn’t that damage the dollars value, make it less appealing?

Makes zero difference. People misunderstand what a currency is. Countries have always traded in their own currencies. Oil might have a price tag that’s in dollars, but when a German refiner wants to buy a tanker of oil, it can pay in euros just fine. The currency will be part of the sales contract. Happens all the time. Companies in China and Russia have long done business with each other in one or the other currency, as specified in the contract. Why would a Chinese company pay in dollars for Russian lumber? They don’t need to. Hardly any trading gets done in Africa in dollars.

Assets is another matter. If the rest of the world refuses to buy US assets (such as Treasuries), then that’s an issue.

Will you invest in Bonds that you have problems to swap?

Chinese currency is not free traded then will never be an option.

Our dollar, your problem

After enough time and abuse, “their” solution to “their” problems caused by “our” dollar is to use and rely on “our” dollar less and less.

It has been a long time since the US has had to adapt to the consequences of running an unreliable currency (one rooted in frequent debasement).

I enjoyed Mr. Rogoff’s latest book.

The growth of the E-$ market negatively affected the U.S. $. It used to be larger than the domestic market. It now stands c. 12 trillion dollars vs. 22 trillion for M2.

The contraction of the E-$ market has been going on since 2007. It was accelerated by Basel III’s LCR, and Sheila Bair’s assessment fees on foreign deposits, which changed the landscape of FBO regulations.

It helped make E-$ borrowing more expensive, less competitive with domestic banks (the exact opposite of the original impetus that made E-$ borrowing less expensive, when E-$ banks were not subject to interest rate ceilings, reserve requirements, or FDIC insurance premiums). And now Powell has eliminated required reserves.

In terms of a relative valuation I do not understand why/how GBP and EUR seem to ,maintain relative strength vs. USD ? For that matter why CAD and AUD (resource countries) are mainly suppressed via the USD.

The demographic bomb facing the 10 largest global economies (with the exception of the US) is likely to significantly impact the status of the US dollar.

China’s economy is already a mess leading into a horrific demographic collapse.

The German and Italian economies are beyond repair with miserable demographics across all EU countries.

Japan, Canada, Australia, the UK, and nearly all other major economies are going to roll over in breathtaking fashion within my lifetime and I’m an old guy.

The US stands out due to imigration. Peter Zeihan details the global carnage coming our way!

Immigration is spelled with two m’s. The US is finished as a destination for immigrants. Better rethink your theory.

the immigration has been iced out.

People have finally figured out that endless population growth is insane and ultimately self-destructive to the species. Nature knows how to deal with overpopulations. It’s a common occurrence on this planet. Nature is brutal.

When I was born, there were 2.5 billion people on this planet. Now there are about 8.5 billion, in just my lifetime. Humans have gone complete nuts, and it’s time to think about this seriously. And thank God people are thinking about it seriously.

You don’t really believe we’re in the driver’s seat on this one, do you? Whatever Nature is, it has been running experiments since Day One. Hopped up monkeys are just the latest version of the lab rats for something we can’t possibly know. You gotta know by now how this is more than likely to play out over time. We’re just getting stupider by the minute.

We are getting stupider how? We literally have the knowledge and ability to rip atoms apart and create mini suns

Let me see your lab monkeys do that

As you say Wolf, Nature always has the last say as to what is possible. Unlike the laws of men (like eCONomics), the laws of Nature are what they are, and they are brutal. If any one of the elemental cycles slows down, and they all require tremendous energy input, life on this planet changes very quickly. A bunker in New Zealand won’t matter. Go ahead, google nitrogen cycle, or sulfur cycle, or carbon cycle, or phosphorus cycle, etc. etc.

no and nope. welcome to the new world order.

Wolf; if you are tired, sick, or just not in the mood, do you have AI write an occasional article now and then? (“AI, do your thing!”)

Come to think of it, I wonder if the (occasional) Grumpy Wolf in the comment section could just be an AI persona.

Grumpy Wolf could be Grok. Maybe Wolf was once corporeal walking around SF writing pithy articles but now he’s data centre 0s and 1s keeping us occupied whilst we write silly comments until the final convergence takes over and GoDot finally shows up.

It’s static data right? not dynamic. It doesn’t show the value of currency against currency only nominal numbers. Technically with enough time only 2 options the dynamic USD will make a new high above 1985 level of 164.72 or a new low below from 2008 at 70.70. It may take decades to find out. I see a series of lower highs and lower lows since 1985. Recently the USD appears to go up with the price of oil. We will see if that continues. If the usd makes a new low reserve holdings may go up, correct?

Not sure what you’re talking about. The USD-denominated assets are expressed in USD. So that’s foreign holdings of US Treasuries and other US securities – they’re expressed in USD obviously. Non-USD-denominated assets (such as yen assets) are expressed in USD at the exchange rate at the time of the report. When the exchange rate of a currency pair changes, such as USD-YEN exchange rate, it doesn’t change the USD-denominated assets, but it does change the YEN-denominated assets that are expressed in USD.

Despite huge ups and downs of the USD against a basket of currencies, such as the Dollar Index DXY, the USD is back where it had been in the 1970s.

Yep, simply confirms that we are in 1976-78 again…

…not a good thing with this amount of debt.

I was referring to the value of the USD converted to their(other nations) local currency. From their perspective as a store of value compared to their domestic currency holdings vs our perspective( as a support of our currency or our currency in holding by other central banks). Thanks as alway. $USD resistance is at 101.67 if it can’t clear that level I am guessing it could break lower and take out the 2008 levels.

It seems like CB’s buys gold when its high and sells when its low. Regardless if their transactions are causing most of the price swings. Its inefficient. What am I missing?

Wolf,

As usual great article. Thanks for explaining that it doesn’t matter if countries stop trading in dollars and trade in their own currency. I don’t know why folks keep bringing this fear that dollar is no longer going to be choice of currency in international trade. On the other hand you have touched based countless times that if demand for treasuries goes down by foreign banks and private investors then we have a major problem as we cannot fund our own debt.

I have few questions and I am hoping you can dive little deeper to explain.

Do we really need foreign countries to buy treasuries or can we keep buying our own treasuries and keep funding ourselves. I believe we own lot of treasuries ourselves and I remember you covering that portion in one of your article last year.

What is a solution to reduce this debt? Is it really financially possible to increase tax rate and we can reduce our debt by 50%? Our expenses are more than our income and endless wars and trying to solve every problem in the world is never going away no matter who sits in White House.

Is there any other option or idea on the table to reduce debt other than tax increase? Increase in productivity and GDP is not going to cut it and we are also not global manufacturers and exporters like china or India.

You have said repeatedly that our debt is in our own currency so we will never default as we print our own money. We are $35 trillion in debt now and in few years we will be $50 trillion. Wha options really we have other than keep doing the same thing and expect different results? Which president is going to come in power and say I am reducing by our military budget in half and I am increasing our taxes by 30 percent until we resolve our debt situation. I see countless posts on this channel where folks are complaining about our debt but how many are going to support increase in taxes?

Show me they can not only identify fraud,

but also eliminate it and prosecute.

Then we can talk taxes.

It does not help when political parties villify the IRS. Desiring low taxes is one thing, curtailing tax enforcement is something else.

U.S. Dollar Index (DXY)

Closed

Last Updated: Mar 27, 2026 4:59 p.m. EDT

100.19

0.29 0.29%

Previous Close

99.90

Interest rate pressures / differentials are lifting the U.S. dollar.

mw: U.S. stock futures sink, oil prices surge as Iran war shows no signs of letting up

Over half of S&P 500 sectors are in correction. How much longer until the index itself is too?

US Treasuries see weakest auctions in over 3 years as Iran conflict anxiety grows

But a correction is only -10%, that’s nada. That would still leave it up over 10% yoy.

It was -50% in 2002 and again -50% in 2009.

Beat me to it Wolf. Us “seasoned” folks have seen two 50% drops in our lifetimes already. We also remember 15% interest rates and a time when the DOJ actually prosecuted, convicted, and sent banker/financiers to prison. If you reward bad behavior, don’t be surprised when people start behaving badly.

Alot of young retail “investors” never experience a long downturn before. Yes, there was a big crash during COVID but that was quickly rescued due to QEs. Will the FED let the markets go down big and without QEs this time?

Your favorite guy Powell has completely lost his marbles. He’s abandoned hard date for polls on what people think? I can save hi the trouble. People think prices are through the roof. Maybe he should go The View and get some feedback.

“The Federal Reserve’s response to the US-Israeli war on Iran largely hinges on how the conflict affects Americans’ expectations about inflation, Chair Jerome Powell said Monday.

“The tendency is to look through any kind of a supply shock,” he said during a moderated conversation hosted by Harvard University. “But a critical, essential aspect of that is you have to carefully monitor inflation expectations.”

Should not the dollars be referred to, more often, as Federal Reserve Notes?

The gyrations of the dollar, the wobbly status as a reserve currency all falls upon the Federal Reserve and their notes, and how the Fed has exploded the amount of their notes in the system.

Good lordy, No. Stop this goldbuggery BS here.

The dollar is a “currency.” A currency measures the value of something. No one owns dollars. People own “assets” that can be denominated in dollars or whatever currency. You can measure your gold holdings in dollars or any currency, or in weight (troy ounces), or in volume (cubic inches or cubic millimeters or whatever) if you want. When you sell it, you measure your gold in the currency that you get in return.

Federal Reserve Notes are dollar bills (printed paper), which are assets for the holder (dollar bills in your pocket or under the mattress), and a liability for the Fed… they’re in effect an interest-free loan that the holder provides to the Fed (which is why they’re called “notes”), and the Fed invests the proceeds in Treasuries and gets the interest. The spread between 0% on FRNs and 3.7% on T-bills is the Fed’s profit. This is the “right of seigniorage,” look it up, which is how central banks normally fund themselves.

I think I would rather have gold than an interest free loan to the U.S. government or the Zambian government or any government for that matter. Guess that makes me a “gold bug” or someone with half a brain.

I’m so tired of your kind of BS. You people don’t understand the difference between investments that investors own (stocks, bonds, CDs, etc.) and dollar bills they have in their pockets. You keep comparing gold to dollar bills, you goofballs. Compare gold to stocks, bonds, etc. and then add the risk factor of each to it.

So roughly $7T held in reserve in 2012 and ~15yrs later, it’s still roughly $7T held in reserve, having held constant around this number over all that time.

During these ~15yrs, we have had a little inflation, a little global economic growth and some growth in .fed note sales.

Hmmm.

Wolfman, my educated deduction from reading your comments is that your paychecks are being signed by one J. Po well. Either that, or you’re one first rate free cheerleader.

I’m just looking at the actual data instead of fabricated goldbuggery BS, if that’s what you mean.

Something should be said about gold and silver rising against all currencies, I say truth is finally bubbling to the surface.

I’ve been gone for while but I’m back.

gold has fallen against all major currencies. Silver has plunged against all major currencies. Have you not looked in a while?

W.R.: It seems you missed out on the quote of the century. The big man, Jay himself, stated “it will not end well if we don’t do something fairly soon” on March 30, 2026, referring to the trajectory of the $39 trillion U.S. national debt.”

(note: This was said after this article was posted).

Quite an ominous statement! I wonder how soon ‘fairly soon’ is? And what does ‘it will not end well’ mean?

He wasn’t talking about reserve currency status, but about the sustainability of the trajectory of the debt. Two different things.

And that’s one of Powell’s standard lines. He gets asked this at nearly every meeting, and he always says the same thing: The current debt is sustainable, but the path/trajectory is not. And that’s true, and everyone knows that, and the people who could do something about it (White House & Congress) ignore it.

Interesting that CANZAC currencies consists of approx. 1.2 Trillion of foreign holdings – or about half that of the Euro.