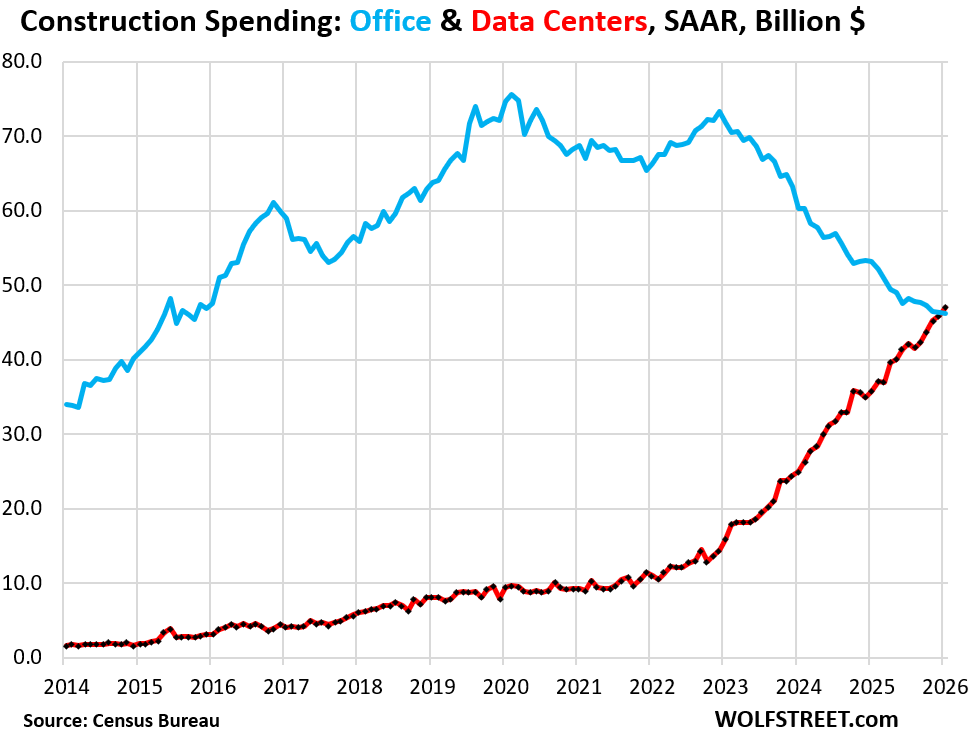

Explosive spending on data-centers exceeded plunging spending on office buildings for the first time ever.

By Wolf Richter for WOLF STREET.

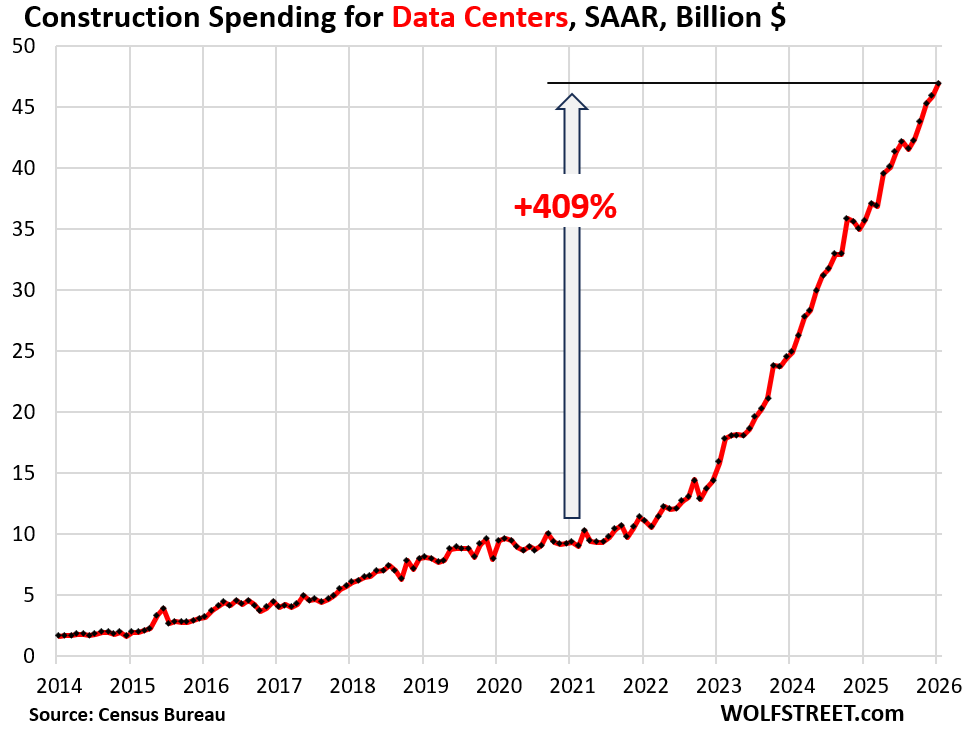

Construction spending on data centers soared by 31% in January from the already spiking levels a year ago to a seasonally adjusted annual rate (SAAR) of $47 billion, up by 409% since the beginning of 2021 – it more than quintupled! – and up by 670% since the beginning of 2018, according to data from the Census Bureau today.

Spending on the construction of data centers is reportedly limited by various supply constraints and bottlenecks, ranging from labor, especially electricians, to electrical equipment and of course power – grid power and on-site power generation equipment when grid power is not available. No one was ready for this sudden boom.

This construction spending on data centers does not include the amounts spent on the immensely expensive AI-specialized servers, networking equipment, etc. inside those facilities, which have reached astronomical levels.

Five companies alone announced $700 billion in capital expenditures in 2026, the bulk of which are related to AI with a focus on AI infrastructure – data centers and everything in them and around them, from AI servers to onsite power-generation equipment if the utility cannot supply the juice.

- Amazon: $200 billion

- Alphabet: $175-185 billion

- Meta: $135 billion

- Microsoft: $145-150 billion

- Oracle: $42 billion

Other companies also boosted their capital expenditures, and the overall capex figures are much larger. But only a small portion of it will go into actual construction costs of data centers (Here’s where they get the money to do all this).

Office construction spending fell by 13% year-over-year in January, to a seasonally adjusted annual rate of $46 billion, the lowest since 2015, and has plunged by 37% since the beginning of 2023, as the commercial real estate sector of office began to spiral into a depression.

Spending on data center construction (red line) exceeded spending on office construction (blue line) for the first time ever in January. Boom and bust in one chart:

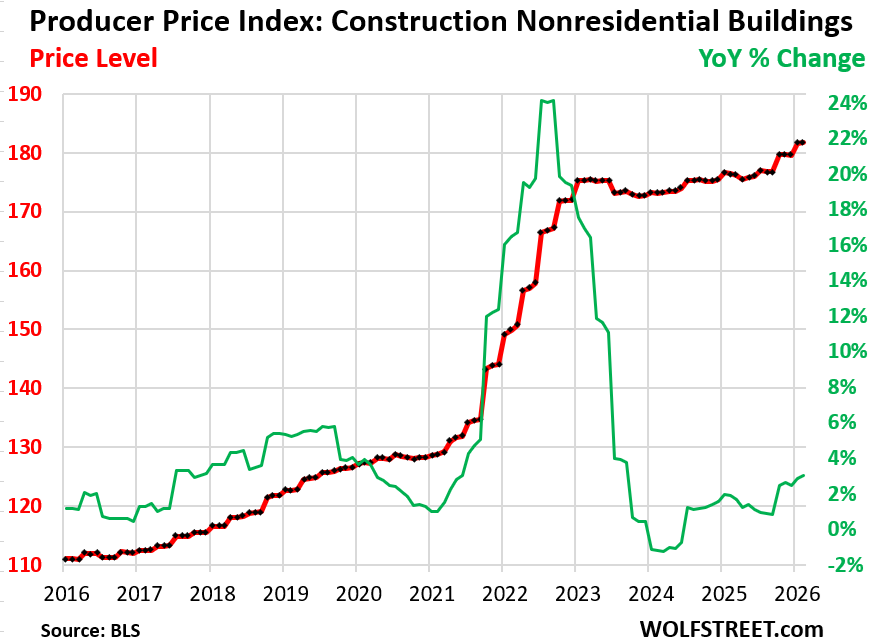

Construction cost inflation: The Producer Price Index for Construction of Nonresidential Buildings, which was part of the hot PPI data released last week, edged up by 0.1% in January from December, and on a year-over-year basis accelerated to +3.1%.

Construction costs had been relatively stable in 2023 through mid-2025, after the huge two-year 36% spike in 2021 and 2022. In October 2025, the PPI for nonresidential construction started to accelerate again.

The chart shows the PPI for the price level (red line, left scale) and the year-over-year percentage change of that price level (green line, right scale).

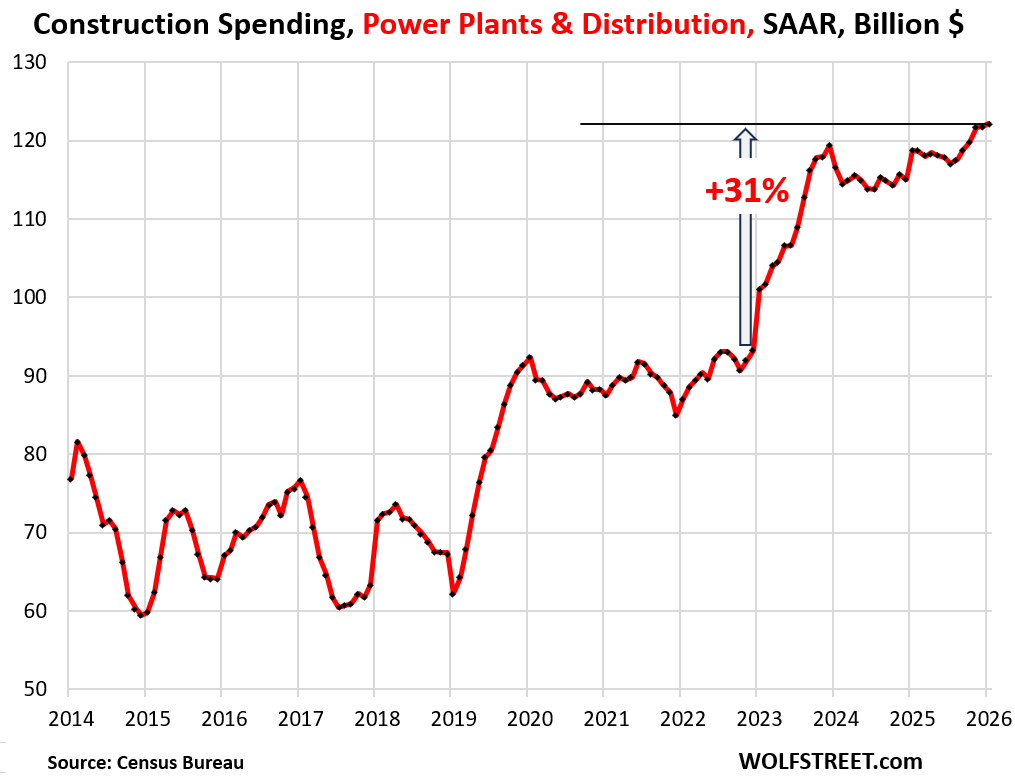

Spending on Power Plants & Distribution rose by 2.9% year-over-year to a seasonally adjusted annual rate of $122 billion, up by 31% since the beginning of 2023. This includes construction spending on power plants and transmission infrastructure.

Data centers require prodigious amounts of power, and utilities or the data center providers themselves have to invest in new generating capacity and in transmission infrastructure to get the power to the data centers. But the process of planning and getting permits for a power plant or a transmission line takes a long time, and the construction spending won’t show up here until construction actually starts.

And utilities, before spending billions of dollars to provide 500 megawatts of power to a cornfield owned by a fly-by-night hedge fund, want to make sure the infrastructure will not become a stranded asset when the AI bubble implodes. They’re proceeding with some prudence because they have to live with the consequences.

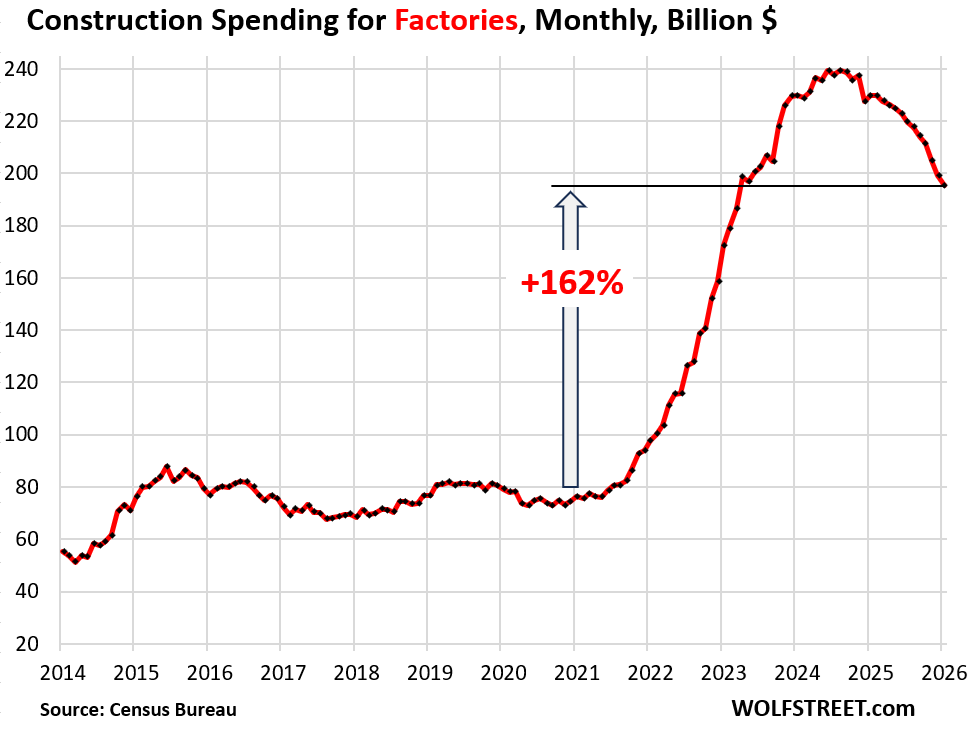

Construction spending on factories declined further from the huge boom, as spending on the construction of semiconductor plants and battery plants has slowed sharply.

Spending on factory construction fell 15% year-over-year to a seasonally adjusted annual rate of $195 billion, still up by 162% from the beginning of 2021, and over four times as much as spending on data centers or offices.

The largest two components of factory construction are factories for Computer, Electronic, and Electrical Equipment (39% of total factory construction in January) and factories for the Chemical industry (23% of total factory construction spending), and we’ll look at them separately below.

These are just the construction costs of the buildings and do not include the cost of the production equipment in the building that dwarf the costs of the building.

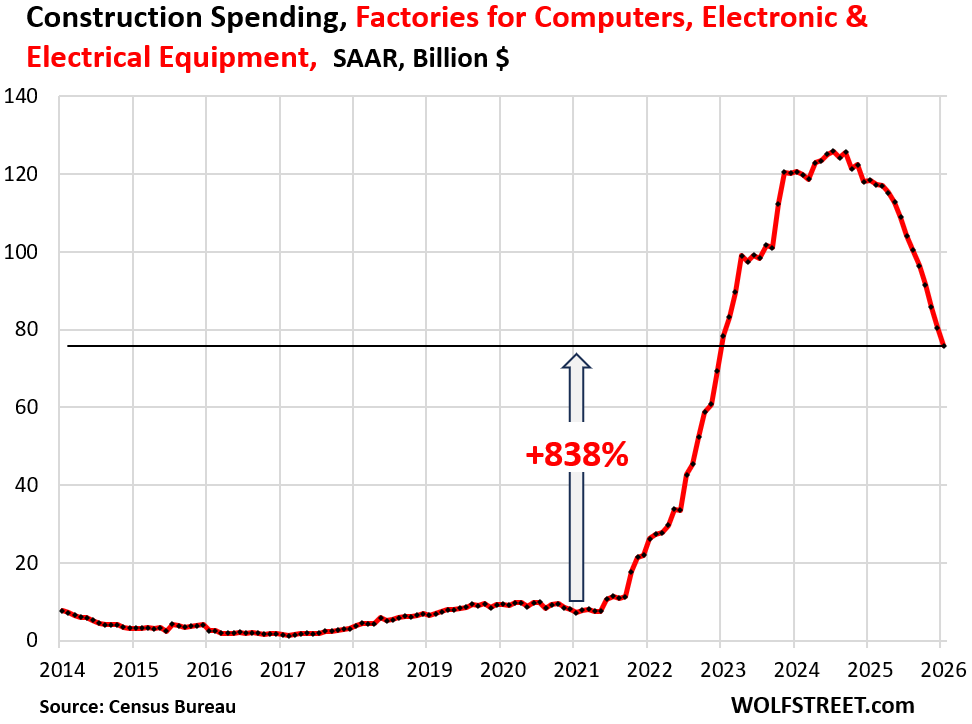

Factories for Computer, Electronic, and Electrical equipment, which include semiconductor plants and battery plants, were the driver of the boom in factory construction and now are the driver behind the partial unwinding of the boom.

While spending has dropped sharply from the peak in mid-2024, and by 36% year-over-year, to a seasonally adjusted annual rate of $76 billion, that is still up by 838% from the beginning of 2021 and by 1,871% from the beginning of 2018. These are still huge numbers.

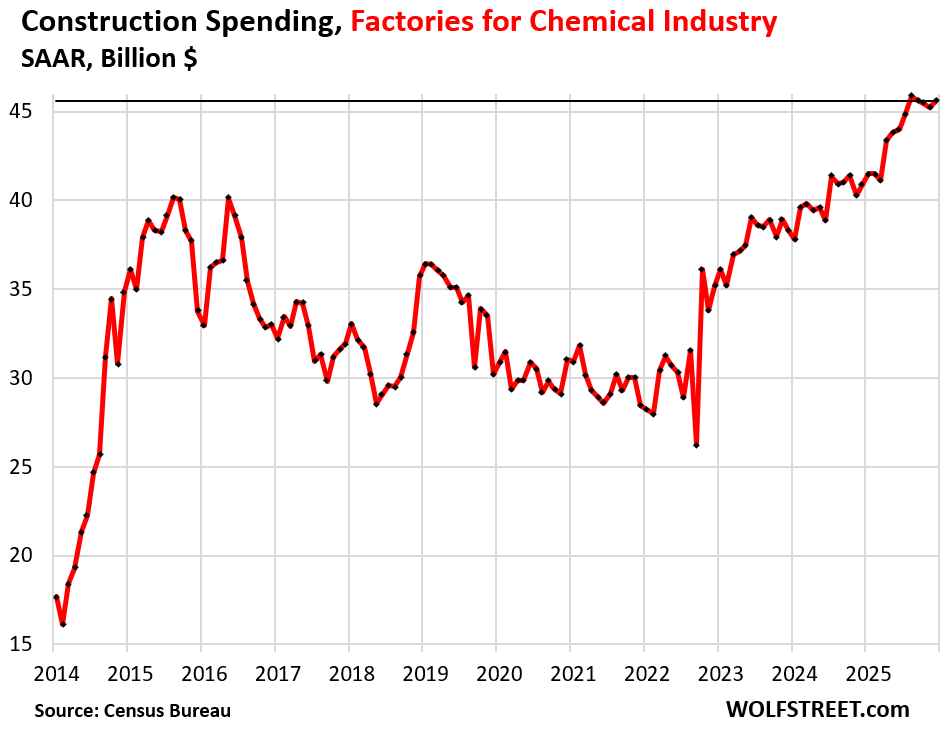

Construction spending on factories for chemical products jumped by 12% year-over-year to a seasonally adjusted annual rate of $46 billion in January, up by 57% from the beginning of 2021.

Factories built in the US will all be highly automated plants with relatively little or no low-skilled manual labor. No one is building a sweatshop factory in the US as labor is too expensive. But automated production equipment costs the same anywhere in the world; it’s the great equalizer.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I remember when I was a kid in the 60s. I would hear that a structure, such as a stadium or factory, costs $50M to build, and I couldn’t believe anyone could get that much money.

When I became an adult in the late 70s, early 80s, the construction of commercial and public entities cost several hundred million dollars. Oh my!

Today, we use billions of dollars as a starting point, especially for fabs, stadiums, and data centers!

I guess I now understand how my parents felt when they bought their first home for $10K and were blown away when they saw their kids buy homes costing hundreds of thousands of dollars.

Geeze seems office buildings are becoming a stranded asset. Difficult to repurpose to residential, but can be done at cost. What else can they be used for?

meant to say, at “a” cost….

Do we have any sense of how dependent blue collar work has become on the data center expansion?

If there’s a bubble implosion, will it hit blue collar really hard, like an oil bust situation?

Most concern about the bubble burst seems to be about a white collar recession from the high-flying firms having to fire lots of people. But it seems there could be a blue collar problem lurking there, too.

Not really. We’re already extremely understaffed on construction labor due to boomer retirements. Deportations and data centers are just salt in the wound.

Investment that doesn’t produce a high number of job openings. We will have stagflation.

These data centers will go the way of the malls after the AI implodes as I expect. They’ll have to find some other uses for the properties out in the middle on nowhere. Maybe ICE detention centers?

In a recent YouTube video, musician Rick Beato showed how he downloaded an LLM to one of his computers. Instead of running his AI queries through something like Chat GPT, he just fires up his computer app.

Takeaway: All of those data centers will soon become as obsolete as the recording studios that bands used to need to record anything.

I don’t know if I can post the YouTube link here, so I’ll just say that the video title is “How AI Will Fail Like The Music Industry.”

The Chinese LLMs are open source and taking off all over the place. They are easy to install on a personal computer and run much leaner. Once the Chinese go after Taiwan and capture the chips market, it’s game over for US LLM platforms. We could have headed that situation off but didn’t.

I can run Excel on my computer. But increasingly, computer users run Office 365 or Google Sheets, powered by datacenters in some other part of the US.

Datacenters were a growth business before LLMs came on the scene. Even if roll-your-own AI becomes trendy, the majority of Americans will use the datacenter-based version.

My Office 365 is “powered” by my laptops, a huge piece of software on my SS hard drives, and works offline just fine all day long without internet connection, and I won’t know the difference. It doesn’t need data centers. I turned off backup to the cloud, because I don’t want my stuff on a MS server. When online, I can read my Outlook emails no matter which laptop I’m using, but that’s just email, which is cloud-based. But I cannot share files between laptops because I have no files in the cloud.

The only major difference between now and when I used to buy the software from MS is that I pay an annual subscription fee which gives me a license to put the software on five devices. I always have two active laptops and the most recently retired spare, and my wife has one laptop, so that’s four laptops on one annual fee. Financially, it works for us since I go through laptops pretty quickly and I used to buy the software each time for each new laptop, and that adds up.

And the updates are automatic, and largely unnoticeable (unlike Windows updates).

But if you’re into document sharing with a scattered team, you can have all your huge corporate files in the MS cloud, but the software is still on your device, and your device still powers all the processing of the data.

But I think that the AI processing you do largely takes place in a data center.

Google Sheets is different; it does run on a server.

Good call Wolf, I have invested in SSD Drives and stopped using the cloud a couple of years ago. Who would have known that these $79.00 drives a few years back, would be going for $189.00 today! It seems that Moores Law is not working anymore?

I worked as a laborer on the Anheuser-Busch brewery in Fairfield in 1975-76 and as a laborer and carpenter on the Kaiser-Permanente cement plan near Cupertino in 1979. Both have now closed. I have to wonder how long all of these data center locations are going to be able to maintain viability in the face of rapid change and competition.

The recent data from Wolf Street reveals more than just a market shift; it’s a physical eviction of the human worker. For the first time ever, spending on the “digital brains” of our economy has overtaken the space once reserved for human bodies, as office construction has plunged 37% while data center spending has quintupled. We are stoping building for people who need desks and coffee breaks, and instead pouring hundreds of billions into silicon “residents” that require prodigious amounts of power but no physical supervision. As highly automated factories replace manual labor and server racks take over the landscape, the message is clear: the economy is moving out of the office and into the machine, leaving the traditional workspace as a hollow relic of a carbon-based past – written with AI.

To this point, if all AI bets pay off and the concentration of wealth accelerates with jobless thought mining centers…at what point does the trickling velocity of money stop the day to day economy? We are already feeling the effects in food prices and energy costs. They are biting further and further the hand that serves them. They would be wise to head that warning.

Or people are just working from home? I read that’s a thing now. So less need for office building space (but larger homes with home offices).

Amazon: $200 billion

Alphabet: $175-185 billion

Meta: $135 billion

Microsoft: $145-150 billion

Oracle: $42 billion

These companies are going to need an army of H1Bs every year for doing “AI”. American college kids can’t do these jobs; it requires a degree from Kolkata, and a cousin/uncle who already works for Amazon IT dept.