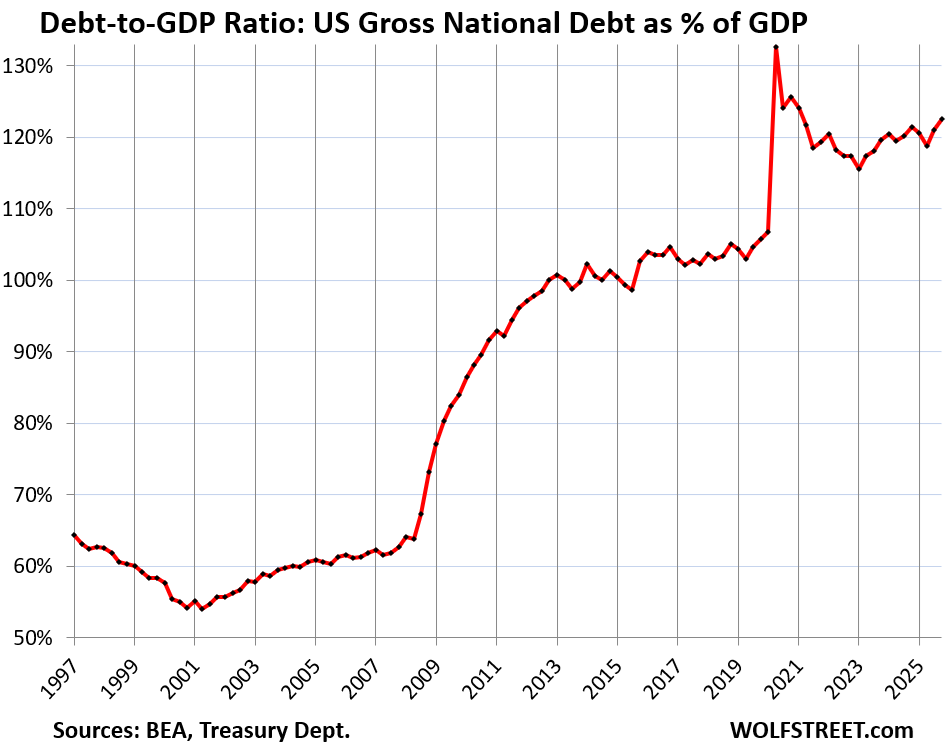

But debt doesn’t exist in a vacuum: The Debt-to-GDP and Deficit-to-GDP ratios provide (ugly) context.

By Wolf Richter for WOLF STREET.

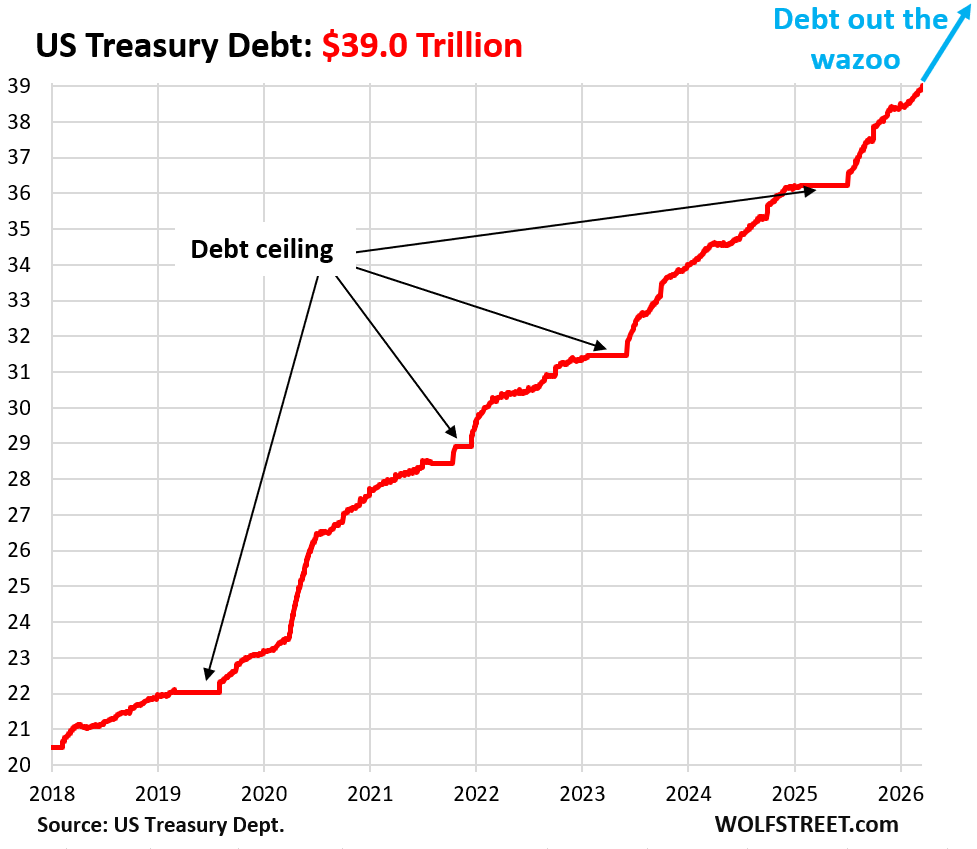

The US Treasury debt – all Treasury securities outstanding – jumped by another $1 trillion in five months, and by $2 trillion in 7.5 months to $39 trillion now, just a few months away from the glorious $40 trillion milestone, as tax cuts, spending increases, and now the war in Iran are speeding up the process.

Since the debt ceiling in early July, the debt has exploded by $2.8 trillion, with those trillions flying out the window at huge auctions every week so fast they’re hard to see. The illusory flat spots occur during the debt ceiling.

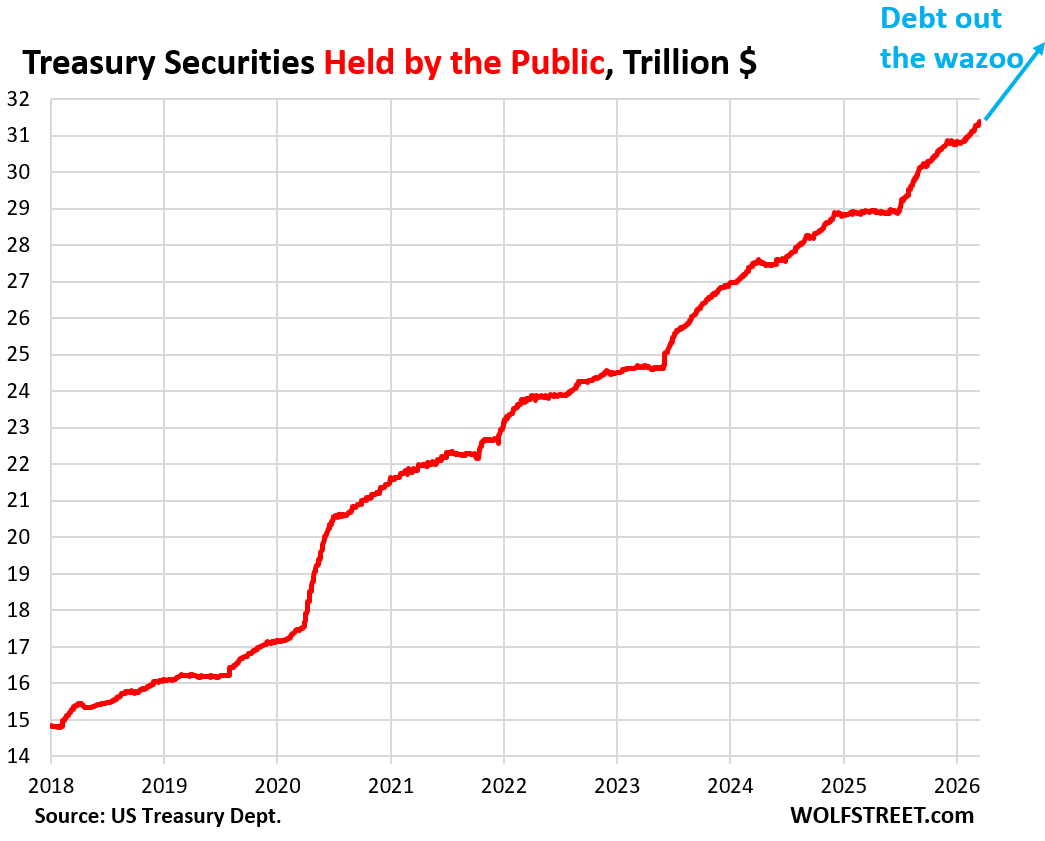

Of that $39 trillion in Treasury securities, $31.4 trillion are “held by the public” – up by $940 billion in five months. They’re the publicly traded Treasury securities held in accounts in the US and around the world, in brokerage accounts, by banks, by insurance companies, at financial centers, by central banks, by the Fed, etc.

That $940 billion increase is the additional supply that bond-market investors had to absorb over those five months.

The remaining $7.6 trillion of the debt is held in federal government pension funds, Social Security Trust Funds, and other “internal” government accounts, and they’re not traded.

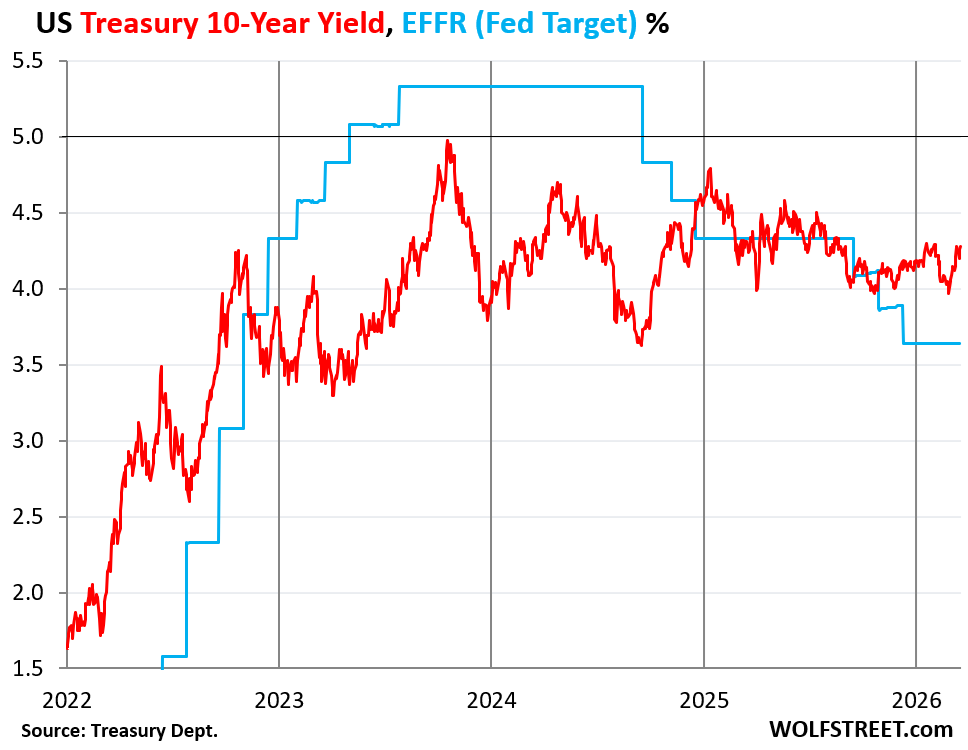

There is always enough demand, but at what yield?

Yields rise until there is sufficient demand for the sales to take place. Higher yields create demand. And so there will always be demand for Treasury securities, but the yield might be higher, and those higher yields (= higher interest expense) would then add to the fiscal problems of the government.

But given the current fiscal situation and the prospects for higher inflation for years to come, yields on longer-term securities are still relatively low:

The 10-year Treasury yield at 4.29% currently is only 1.5 percentage points above the PCE inflation rate (consumer-facing inflation) of 2.8% that is going to soar in coming months on the energy price spike, and 0.5 percentage points above the domestic Q4 GDP inflation rate of 3.8% (overall inflation generated domestically in the economy, excluding imports) that is also going to soar on the energy price spike.

There is a lot of uncertainty about inflation now and how it will develop in future years, with the White House leaning heavily on the Fed to cut rates despite inflation and let inflation do its thing.

All this indicates that there is still ravenous demand for Treasuries, despite all these issues, or else yields would be higher. Over the past few years, any time the 10-year yield approached 5%, demand just exploded and brought yields back down.

That 5% line is the sound barrier that the 10-year yield hasn’t been able to break and stay above for more than a few days since 2000. But in the 35 years before 2000, 5% was the low end of the range.

But debt doesn’t exist in a vacuum.

The debt exists within the economy, so it’s useful to look at the relationship of the Treasury debt to GDP, and at the relationship of the federal deficits to GDP (Treasury debt = cumulative federal deficits funded through issuance of Treasury securities; deficits are the annual flow; debt is what accumulates and remains).

The Debt-to-GDP ratio rose to 122.5% at the end of Q4. So that was Q4 nominal GDP and the debt at the end of Q4. But since the end of Q4, the debt has grown by another $500 billion.

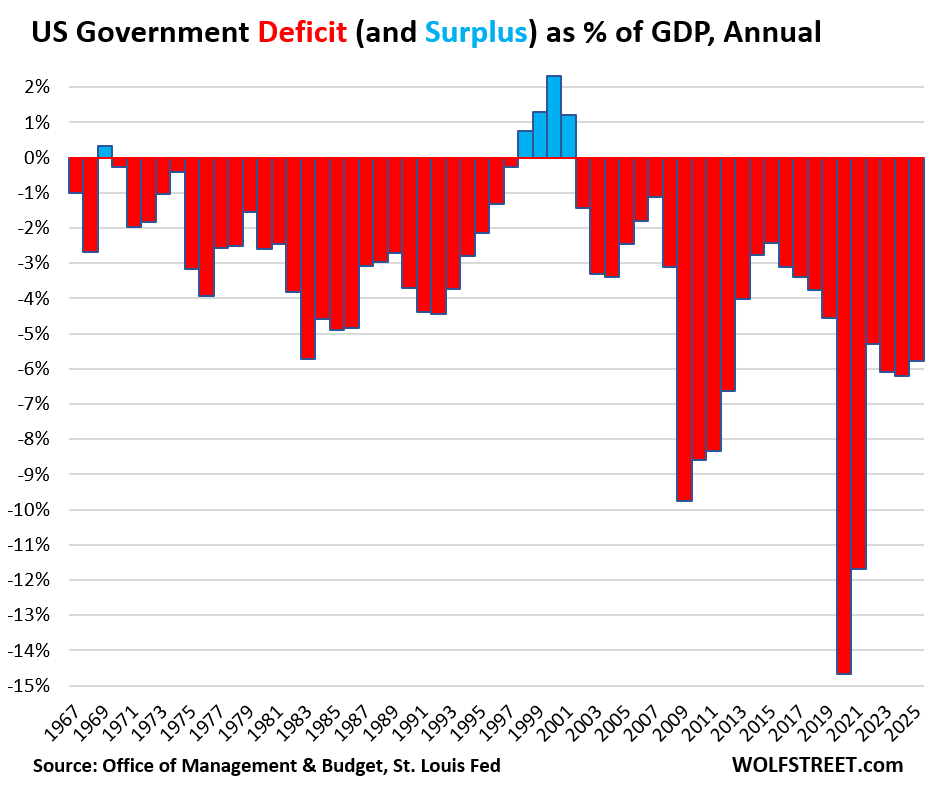

The deficit-to-GDP ratio at the end of 2025 was 5.8%. A slightly smaller deficit and a faster growing economy would improve the situation over time. But a “slightly smaller deficit” seems to not be in the cards any time soon:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Stop pussy footing sround, Raise rates and crash prices.

The market will force the Fed’s hand. America is no longer a creditor on the world stage. The dollar “milkshake” isn’t going away immediately but the math is what it is and I see no evidence that congress will suddenly become fiscally responsible. In fact, I suspect that our owners will have their political puppets institute all kinds of communistic policies (price controls etc.) in order to “save capitalism”. Remember George Bush’s “I had to abandon free market principles in order to save the free market system.” comment after the great financial fraud?

LOL! New world order, same old lies/criminals.

Wb,

I am all for the dictatorship of the proletariat but none of that will happen here. Billionaires will own their massive compounds in Idaho, Montana, Colorado and other places and the bulk will be forced to turn them into trillionaires. Our system doesn’t need saving but replacing and that can be achieved with a dialectical approach focused on the working class. Not rocket science just no way to overthrow the power structures that enforce the current status quo.

Da, comrade. How is weather in Moscow?

America turned from a creditor nation to a net debtor nation in 1985.

Thanks wolf

Te party is over. The drunkards just don’t know it yet.

And Hegseth just asked for an extra $200B for the DoW. I though the number I was hearing a week ago was $50B.

Yikes!

The real kick in the teeth was when Pete said the war was “on behalf of the American people”.

This is complete bullshit Pete, CONgress (the voice of the American people) has NOT weighed in on this war.

What an idiot, but why in the hell aren’t any journalists calling this stuff out?

Because MSM is partners with the Uniparty, duh.

Congress is not the voice of the American people. It is the voice of big money, graft, and corruption. Sorry to pop your balloon.

The $200 billion is just the starting point. IRAQ cost 5 Trillion.

Those four blue surplus lines in the last chart kind of look like a big middle finger.

Isn’t saying always like saying never? Will there really always be investor demand for treasuries? Or is there likely a point down the road where investors lose confidence in the treasuries / dollar such that the treasury can’t afford to sell debt to the public? In other words, the yields will rise so high (whatever that number is) that Fed will have to step in & start buying the vast majority of treasuries?

I’m not suggesting this is just around the corner, but the chart of our total treasury debt doesn’t appear to be far from the rate of change having a very steep slope.

2030’ish, the year I plan to retire seems like fair a bet when there will be a major economic problem.

You have to look at the debt to GDP chart. That’s what matters. It’s bad, at 122%, but not that bad yet. Japan was at 250%.

(Going off memory)…BoJ holds about 50% of Japanese Government bonds outstanding. Fed holds <20% of US Government bonds outstanding.

That’s the primary reason Japan debt to GDP can run so high…Do we want the Fed to own 50% of US Government bonds as well?😄

From April 1,2025 St Louis Fed paper by YiLi Chien:

“as of the second quarter of 2024, Japan’s net public liabilities on the consolidated balance sheet amounted to only 78% of GDP. While gross liabilities stood at 270% of GDP, the government also held substantial assets totaling 192% of GDP.”

This implies the US, currently 122%debt/gdp is in much worse shape than Japan. I think on a consolidated basis we are 100% debt to GDP.

I need your guidance. Can you please help?

I keep hearing this notion that the Japanese have twice our debt/gdp and they are doing fine so why should the US worry about going deeper in debt. I’m not convinced that Japan sets our upper limit.

The US government also has a huge amount of assets, just not on its books: massive amounts of fabulous and hugely expensive real estate that it could sell.

Whenever I think that a bond crash may be coming, I start wondering where would all those dollars, proceeds of bond sales, go?

No one can sell a bond without someone else buying that bond for the exact amount that the seller gets. So all those dollars that the sellers would get during a “bond crash” come from the buyers, and no dollars go anywhere else.

Ah, the mysterious ways of financial markets… Thank you for bringing common sense back to my mind!

What would it take to get something like a “failed auction”, where the dollars go to some other asset besides US debt, regardless of yield? Would that require hyperinflation? Our leaders seem to be betting the farm on TINA.

That’s not going to happen here because the primary dealers are required to buy the remaining securities at auction that other buyers didn’t buy. Then they sell those securities to their clients and in the market over time.

in Germany, when an auction “fails,” the Bundesbank buys the remaining securities at auction and then sells them to investors fairly quickly. Every country has its own system to where even a “failed auction” still gets all the debt sold.

Wolf,

I understand Primary Deals need to buy unsold Treasury securities at auction; So there will be no failed auction per se.

But can Primary Dealers determine yield/price for this forced purchase?

I am assuming yes otherwise they will have huge losses or might even go bankrupt.

The yield/price is determined through the bidding process at the auction, and then everyone that is awarded any securities gets the same yield/price,

If this scenario continues unabated, then the Fed will become the buyer of last resort. No one knows when that will be but there are trends in place to make it sooner than any of us wants.

That is in essence what occured during the SVB blowup. The Fed didnt actually buy treasuries but by backstopping them with loans they removed immense risk from holders.

No one got stuck holding the bag on the devalued asset under that scenario.

This implied insurance policy is most likely helping to depress the current market rate and maintain high levels of demand.

Should a liquidity event repeat, financial instituions can place their notes at the Fed and take the cash. If rates dont stabilize and the market value of those treasuries continues to decline the banks just pay the interest to the Fed, differing the loss over time, while the Fed holds the notes until they mature.

That interest rate, slightly more than fed funds, may be well below the rate of inflation if the Fed is trying to stimulate a weak economy.

In an high inflationary environment cash today is way more valuable then the cash at maturity as it can be converted to another asset class that isnt steadily or rapidly losing real value.

Andes Frank

You got the SVB story completely wrong. BS-level wrong. The Fed blew up the INVESTORS in SVB. They lost ALL their money. Then the FDIC sold the assets (Treasuries and MBS) at huge discounts to other banks. This was very widely discussed, including on this site. I have no idea how you can now concoct this king of manipulative BS. Your whole theory, based on this lie is complete BS.

The 60/40 portfolio again will not work. Longer term bonds “only” worked magically for our parents/grand parents. That setup of 90, 2000-ties will not be repeated anytime soon. QE is not coming for the rescue.

Short TLT.

Buying at the rates on offer over time, surely has been a bad bet, looking back?

The bet now is, will rates really get cut when it’ll fire up inflation? And will Gov get their numbers making more sense any time soon?

The rock and hard place took 15 years to arrive but it’s here and people still gleefully buy the inflation trade AND debt at what feel like cheap rates of return given what’s happening.

Everyone can’t be right.

Right. People buying 10 year treasuries at 4.3% believe the Fed will get inflation mostly under control. People buying stocks at moronic P/Es believe that inflation will continue unabated and real assets will serve as a hedge, and worst case, the Fed will print its way out of trouble.

They both can’t be right. My personal opinion is that the Fed will throw the stock market under the bus to protect the bond market. And printing will destroy the bond market, so they won’t be able to do that.

I am trying to confirm that the tariff refund liability has not yet been added to the Treasury’s balance sheet.

The monthly treasury balance sheet that I found online did not include footnotes/disclosures. Has this already been added as a liability or are they considering this currently an off balance sheet contingent liability. I am trying to figure the mechanisms for this to flow-through into the data. (possible restatements vs recognizing the liability when timing and amounts become more certain.)

1. Your point about the liability on the balance sheet is fundamentally wrong. The government uses “cash accounting,” not “accrual accounting,” and it will show the tariff refunds as part of its deficit when it makes the actual cash payments and as part of its debt when it borrows the money. The liability the government has is the total outstanding pile of Treasury securities and agency securities. It’s cash accounting, not accrual accounting.

2. This debt here is the sum of all actual Treasury securities outstanding. When the government starts borrowing the money by selling more Treasury securities at auction to get the cash to pay the refunds, then these newly issued Treasury securities will be part of this pile here of total Treasury securities outstanding, and we’ll se that pile jump.

Wolf, I just want to personally thank you for taking the time to answer many of our questions. It is reassuring to have a site like yours where I feel the utmost confidence in the information I am getting. True thanks!

Wolf, thanks for the follow-up, sorry, I was looking at the Balance Sheet, not the Monthly Statement of Public Debt or the MTS.

I think that I pulled up balance sheets for FY2025 and misread the date and thought it was released monthly. Anyway, sorry for causing a confusion.

—————————————————-

My self inflicted research, sharing to avoid confusion on this issue

1. Federal Govt and Departments only release annual reports.

2. The Federal government’s Balance Sheets are mostly accrual. One exception is tax and tariff revenue, which is modified cash.

FASAB SFFAS 7:

“Nonexchange revenues include income taxes, excise taxes, employment taxes, duties, fines, penalties, and other inflows of resources arising from the Government’s power to demand

payments, as well as voluntary donations. Nonexchange revenue is recognized when a reporting entity establishes a specifically identifiable, legally enforceable claim to cash or other assets. It is

recognized to the extent that the collection is probable (i.e., more likely than not) and the amount is measurable (i.e., reasonably estimable). In the case of taxes and duties, inherent and practical limitations on the assessment process serve to delay the time when the power to demand payment becomes a legally enforceable claim to cash or other assets. For this reason, the method of accounting for taxes and duties can best be characterized as a modified cash basis of accounting, rather than an accrual basis. This basis of accounting amends the standard for the recognition of accounts receivable for taxes and duties.”

3. Tariffs & Duties are collected by U.S. Customs and Border Protection (CBP) as part of DHS as custodial revenue

4. On the DHS 2025 Balance Sheet they did not include any contingent liability for a potential tariff refund:

DHS 2025 Balance Sheet: Note 20 B:

“Duty and Trade Refunds

There are various trade-related matters that fall under the jurisdiction of other federal agencies, such as the Department of Commerce, which may result in refunds of duties, taxes, and fees from CBP refunds and drawbacks. Until a decision is reached by the other federal agencies, CBP does not have sufficient information to estimate a contingent liability amount. All known duty and trade

refunds as of September 30, 2025 have been recorded.”

so the annual balance sheet you’re talking about is a complete joke. It doesn’t have the government’s biggest assets on it: its vast land holdings (it owns 30% of the entire US land, hugely valuable). It’s mentioned but doesn’t come with a figure. It doesn’t have its military equipment and installations on it, which is also hugely valuable. It doesn’t have the valuables in federal museums on it. The biggest asset on that balance sheet is the federal student loans, LOL. It’s just a joke.

With Iran, we could have a future where we stop drilling our expensive oil and import Iranian oil paid for by Treasuries. Perhaps we could expand that to other countries where these Persian Gulf states (USA lake) get paid by other nations and we exchange that for Treasuries to hand these oil producers, greatly leveraging our financial control of the region and improving our financial situation.

“…just a few months away from the glorious $40 trillion millstone” – fixed that for you.

Great work, as always Wolf!

1:04 PM 3/19/2026

Dow 46,021.43 -203.72 -0.44%

S&P 500 6,606.49 -18.21 -0.27%

Nasdaq 22,090.69 -61.73 -0.28%

VIX 24.15 -0.94 -3.75%

Gold 4,656.60 -239.60 -4.89%

Oil 95.02 -1.30 -1.35%

It seems like gold is trading like a stock these days, not a supposed “inflation hedge.”

“We’re going to need a new chart!”

I think Wolf is just messing with us. If you flip the debt charts upside down, it matches his Imploded Stocks ™ chart darn near perfectly.

🤣❤️

After few years when we’ have debt a $100 Trillion, we’d have similar conversation going on.

The US Gov can print ad infinitum and debasing the currency is the only way out.

Nope.

Am I nervous….hell yeah and sometimes I think I am the only one that is. Seemingly all the experts and talking heads rarely consider bringing up this topic each time politicians promise voters new and shiny programs.

I’m old enough to remember having discussions in the 90s about getting the budget balanced and paying off the debt. It was probably BS, but at least people pretended it was a possibility. Now, no one pretends anymore.

The Federal budget was balanced during the final year of Clinton’s presidency. Bush 43 didn’t care about balancing the budget and it has not been balanced since then.

Stock market – down

gold – down

silver – down

housing prices – down

Crypto – down

oil prices – up

utility bills – up

gas prices – up

homeowners ins – up

auto ins – up

airline fares – up

interest rates – up

inflation – up

lines at airports – up

traffic jams – up

homeless – up

Conclusion:

Everything that you’d like to see go UP is going DOWN. Everything that you’d like to see go DOWN is going UP! This is what I would call a repeat of the Jimmy Carter malaise. ENJOY

I agree that debt does not exist in a vacuum, but I would offer that debt/GDP exists in a haze that can become a navigation hazard.