Double-digit increases in employee health insurance costs hold down wage increases.

By Wolf Richter for WOLF STREET.

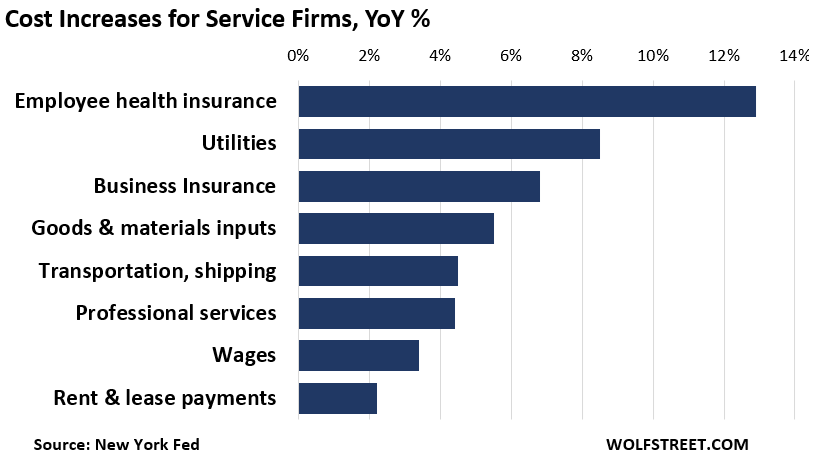

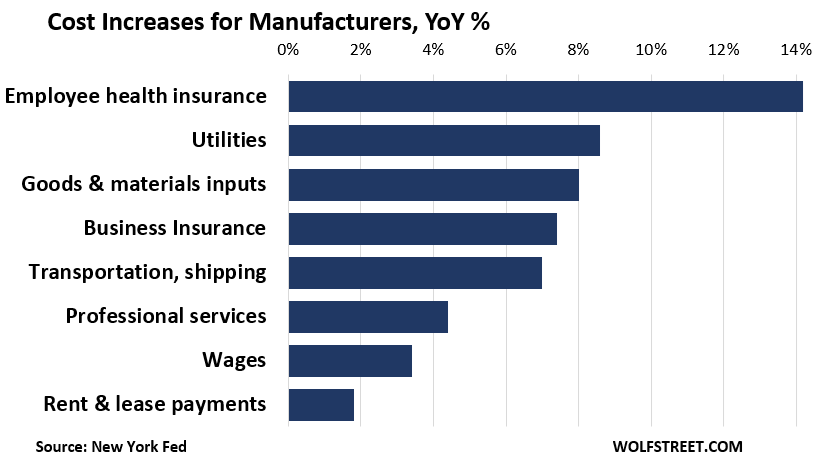

Manufacturers reported that the costs of health insurance for employees shot up by 14.2% on average; service firms reported an average increase of 12.9%, according to a report by the New York Fed based on a survey of companies in the New York-Northern New Jersey region.

These are averages, but “some firms reported increases of between 25% and 50% when they renewed their coverage,” the report said.

Manufacturers and service firms both reported that the costs of utilities jumped by about 8.5% on average. About one-fifth of the companies reported increases of 20% or more. “Indeed, sharply rising utilities costs in some areas have been tied to the explosive growth of AI-related data centers,” the report said.

For service firms, the third worst cost increases were in business insurance, which jumped by 6.8%. This includes liability, property, auto, and workers’ compensation insurance.

For manufacturers, business insurance increases were the fourth-worst, with an average increase of 7.4%.

Nearly one in ten of these companies reported massive spikes of 20% or more in business insurance costs.

For manufacturers, the third-worst increases were goods and material inputs, which jumped by 8.0%. They reported substantial increases in the costs of tariffed inputs, such as aluminum, steel, equipment, electrical supplies, auto parts, coffee, and cocoa, etc.

For service firms, cost increases of goods and material inputs averaged 5.5%.

“A greater exposure to tariffs may be part of the reason manufacturing firms faced a sharper increase in goods and materials costs” than service firms, the report said.

These are very serious cost increases.

The Producer Price Index (PPI), which track prices paid by companies, has also shown sharply accelerating cost increases across a wide range of industries, with big price increases for both services (which dominate the PPI) and goods. The price increases in goods were driven by companies shuffling the costs of the tariffs around to each other, but they’re having trouble passing them on to consumer-facing companies, which are having trouble passing them on to consumers without losing sales.

But wages increased by only 3.4% at both service firms and manufacturers, amid indications that soaring employee health insurance costs – average annual premium for employer-sponsored family health insurance rose to about $27,000, according to the NY Fed – were putting downward pressure on wage growth.

“Businesses providing insurance to their workers indicated that absent these cost increases, they would have raised wages by roughly an additional percentage point, on average, (so an overage by 4.4%), suggesting that rising health insurance costs resulted in a drag on wage growth for workers at these firms,” the report said.

But increases of rent & lease payments were relatively modest at 2.2% for service firms and 1.8% for manufacturers – thanks to the depression in Commercial Real Estate.

This chart shows the cost increases by category for service firms. Note, business insurance in third position (+6.8%):

This chart shows the cost increases by category for manufacturers. Note, goods & material inputs in third position (+8.0%), and business insurance in fourth position:

The report also pointed out that service firms and manufacturers were impacted differently by these cost increases:

“For example, utilities and materials inputs would represent a larger share of costs for manufacturers compared to, say, a consulting firm, where labor costs would have more of an impact. Thus, cost increases for any category could have more of an effect on some firms than others.”

Costs overall for service firms jumped by 7% in 2025, an acceleration from the 5% increase a year earlier.

Costs overall for manufacturers jumped by 8.5%, a hot acceleration from the 5% increase a year earlier.

These are just indications based on companies in the New York and Northern New Jersey region, and not national indications. Firms in other parts of the US may experience cost factors that are somewhat different, such as the average increase in the costs of utilities, which are the newest hot button in many places.

So inflation is raging beneath the consumer-level surface again. It has also shown up in the GDP inflation adjustments: The Price Index for Gross Domestic Purchases, which reflects inflation adjustments in GDP except for imports – so a measure of overall domestic inflation for consumers, businesses, and governments – jumped by 3.7% in Q4, the worst in three years.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

OK. I thought I had been hallucinating, because until this report, the majority of what I read kept telling me that inflation is low. However, my costs have continue to increase, with insurance increasing the most. Some of this, like supplemental health insurance (to cover the portion Medicare doesn’t pay) is expected as I get older. However, auto and home insurance have gone up 15% this year.

Yeah, I have never really been a fan of insurance.

A person pays premiums for decades, with no claims with the agreement that if something unlucky happens there will be some coverage.

The insurance company collects for decades while raising rates, and without paying, hoping they don’t have to pay for coverage.

Then something unlucky happens, and the insurance company finds every reason they can to refuse coverage, raise rates, cancel policies etc. to be able to default on their end of the agreement.

Not a fan. It is kind of government mandated scam in favor of insurance companies.

A false insurance claim by a policy holder is a felony, and the government supports this.

But if an insurance company does not pay a “valid” claim to a policy holder, good luck to the policy holder finding the same level of government support that the insurance companies enjoy.

If you wreck your car they replace it.

Without insurance, you are SOL.

If you are injured in the car wreck Health Insurance saves you over $200,000 in hospital bills.

Without insurance, you are SOL and losing your home.

If someone sues you, an umbrella liability policy will pay to protect your net worth.

Without insurance goodbye net worth, goodbye nest egg.

What’s not to understand? It’s a freaking modern marvel of financial invention.

It would be, truly, if it hadn’t been packaged up as an investment vehicle answering to shareholders demanding growth and spawning 8 figure salaries for execs.

Car insurance sure. Health & home…lots of efforts to not pay and extremely difficult for one to change that decision

Car insurance sure. Health & home…lots of efforts to not pay and extremely difficult for one to change that decision

I am not silly about it. I have basic liability insurance that is required for vehicles.

I have been driving the same 3 trucks, a 1972 chevy blazer for 32 years, 1994 GMC Sierra 31 years, and a 2008 Duramax for 17 years. All covered with liability insurance only the whole time.

I have saved untold thousands not purchasing full coverage, and money I save is put aside for in case I wreck and have to repair or replace a vehicle. I have not wrecked.

If someone else wrecks me, they pay.

If someone else injures me, they pay.

If I injure myself, well all hospital bills are negotiable. You can negotiate a far far less total price than what the bill says. And payments can be made without interest charged, and you are not sent to claims as long as you make minimal agreed payments. You won’t just lose your house.

And even if insured, it could be very easy to rack up far over $200,000 in medical bills.

If I am killed, well… I suppose I am not available for the bill or the savings.

The insurance company does not always just pay. They don’t just give you a new car or house. The very few dealings I have had with claims, I have been on the losing end.

Umbrella policies are not all they a hacked up to be either. If someone has a good lawyer they can still clean you out. House, cars, savings, retirement, all of it. I have seen it.

Being an insurance minimalist has saved me thousands over the decades and works for me. I just do not see it as quite the marvel that you do.

And don’t even get me started on med. insurance…haha.

I know a young man who was injured in a collision and now can not live independently. AAA has been paying his grandmother a good sum for years to care for him, and when she passes they will pay someone else, for the rest of his life. This is a no fault state, so I assume this is paid for from insurance he or his family had purchased.

Injuries like his are not unusual in a collision. That’s why I keep a high level of personal injury coverage on my vehicle.

Love the individual whining.

“Inflation” is increased sharing of the middle class lifestyle with the rest of the world….but….

“What is happening is that the global middle class is growing, and it’s growing extremely rapidly,” said co-author Eileen Crist, a professor at Virginia Tech’s Department of Science and Technology in Society.

That comes from the very positive outcome of getting people out of poverty. But there’s a catch.

“But what sometimes people miss … they miss what’s happening in the middle,” Crist said. “Which from an ecological perspective of the planet is the most significant event: the rapid rise of the global middle class, which is now more than three billion people in the world and it’s expected, by 2050 or so, to rise to five billion people.”

And it’s the middle class where people begin to increase their carbon footprint: they buy appliances and cars, eat more meat and travel.

Growth for growth’s sake is the ideology of a cancer cell……F the bean counting “problems”……this planet is as good as destroyed for most mammals……extinction event #6……we should be proud of ourselves for using the planet so profitably.

Proud to be a MINIMAL consumer BY LIFELONG CHOICE….at least by USA pig standards…….

Enjoy rearranging the deck chairs.

But a good portion of that hospital bill is due to insurance-related costs. You could cut it in half if not lower in other countries.

If the population as a whole were actually capable of taking better care of themselves and saving a healthy amount, maybe we could get by without insurance. And in this theoretical world I’m 6’2″ and married to Jessica Alba.

You’re confusing something that many people do. The insurance contract (homeowners, car, most policies) has a time limit. You buy an insurance policy to cover you for X amount of time. (typically a year). At the end of that year, the insurance company (and you) reevaluate the risks and the pricing of those risks. You pay for 30 years and them not paying out has NOTHING to do with the current year’s pricing of risk. It’s 30 different one year contracts and for those 30 years, you received coverage and were protected against any claims (of which you didn’t file any) and those contracts closed out each year.

Don’t confuse those things (many people do).

READ the contract. most denials (not always, some companies are slimey) are pretty clearly stated in the contract and what’s covered and what isn’t is usually (not always) pretty clear.

Unregulated insurance is a racket. I don’t care how you logic it out. When you spend 35 years as I have paying homeowner’s premiums & never filing a claim, it’s a very hard pill to swallow to have your premiums increase without any consideration of zero claims. Saying they’re one-year contracts is just a crock, because boy let’s file a claim & see what happens to your premiums for 3-5 years.

Everyone knows insurers spread risk costs across every state that they provide policies. People like myself that live in very low risk areas are paying for fire claims out west, hail damage in the Midwest & hurricane damage along the gulf coast.

IMO, this shouldn’t be allowed to happen. Heck, we just went through last summer without a single hurricane hitting the US coast, and my guess is that didn’t slow down premium increases one bit. It’s just money in the insurers pockets.

And like EVERYTHING, inflation keeps raging when you don’t have a periodic nasty recession. We’re now 16 years on since the GR which is the #1 reason why prices across all levels are so out of whack.

LCG

I was hit head on in a car accident. Person ran a red light, when I was turning left on a green arrow. Both of our cars were totaled and my leg was broken.

2 impartial witnesses, two police officers and their accident report, the other driver’s admission at scene, myself and my passenger all said she was at fault, by running the light, crossing over and hitting me.

The at fault driver’s insurance company, one of the big companies would not pay anything. The adjuster said I should have avoided it, and the adjuster laughed at me, said I could submit again if I wanted, and hung up.

The other driver had paid their one year insurance contract and was liability covered.

The trick here is that the insurance company just decided not to honor the contact. Not due to a clause in a contract. Just decided not to.

I had to hire a lawyer to force them to honor the contract and pay for my car and my medical bill.

Insurance companies will not get fanfare from me, and I will purchase the least amount of their products as legally possible.

So Buck, you got a bad representative

You forced them to follow the law and their contract. Good.

The insurance still worked for you.

Medical insurance increases are driven by lack of a free market in healthcare. The corrupt US Medical-Industrial Complex totally captured the system and destroyed the free market with Obamacare.

significant amount of Americans are now morbidly obese or significantly over their acceptable BMI, people continue to smoke continue to drink, people don’t eat healthy, this is not new it’s been happening now for the last couple decades. people expect very best healthcare and diagnostics for almost any ailment that they have. is there any reasonable explanation to believe that these have not been factored into rising insurance rates

Eh. We got Obamacare because the free market wasn’t working and people already weren’t happy.

Insurance is a math thing. There aren’t really separate products. There is nothing to “improve”. A free market will not help. Hoping for profit won’t help.

I was happy with my insurance before Obama care. I’ve always been self employed. I bought catastrophic coverage. $10k deductible and set aside money every month to cover normal health care costs and the deductible. The coverage protected me and HSA tax benefits let me self insure the gap with a little less pain.

Somehow, after Obamacare, that insurance more than doubled and then became unavailable.

There is a reason why Insurers were big supporters of ObamaCare. But now it’s blowing up in their faces and it’s probably going to end with some sort of Medicare for All.

I’m on medicare now. It’s the best insurance I’ve ever had. It covers 80% and I self insure for the 20%. But the most important benefit of Medicare is the contract prices they impose on providers. In most cases, those contract prices cannot cover the providers costs (as inflated as those might be). It’s unjust in that those costs are then shifted to other payers. But there you are.

When I take my dog to the vet, there is no insurance and if he’s sick enough I would just put him down rather than pay thousands. The vet bills are reasonable and we all expect to self pay. And interestingly, most Vets are still owners of their own practices as opposed to being corporate employees and their litigation costs are pretty low.

There is something between vet medicine and human medicine that might help us figure out whats wrong and how to fix it.

I was very happy with my high deductible private health insurance plan. It cost me $50 a month to insure up to $2 million. A nice cheap safety net. Then the “Affordable Care” act forced insurance companies to accept pre-existing conditions with no cap. My insurance went to $250, then $500, then my insurer left the market. I’m healthy and take care of myself so I said screw it I’ll take the risk without insurance. To add insult the government wanted me to pay $900 penalty for not having insurance!

Healthcare and risk mitigation tools (insurance) are two different things. Government intervention ruined both!!!

A few reasons why vet medicine is less expensive:

1. Veterinary service is far less regulated, with a much lower barrier to entry. It’s far easier to become a licensed vet, become a vet tech, to get a new medicine authorized, to open an animal hospital, than it is to do the human equivalent. There are far lower associated costs, and much more competition.

2. Veterinarians provide, and owners purchase, a much lower level of service than the human medicine providers. No extended life support, no extreme levels of life saving intensive care, no dozens of options for effective cancer treatment. It’s rare to purchase months of care and therapy for a recovering pet. Typically an owner will do what humans did a hundred years ago: purchase basic treatment, get discharged, and do their best to self manage the recovery at home. At the most, a devoted pet owner may opt for thousands of dollars in emergency surgery or chemo.

3. Human care is constantly innovating and arguably works miracles. There is a constant attention, across the dozen plus medical disciplines, to avoiding complications and improving outcomes. Fall behind, and the customers – you, me, and our neighbors – will demand better, and may even sue for malpractice.

There are signs that veterinary care may start to trend this direction as well. If so, expect vet costs to rise exponentially in the same manner.

The main problem with Obamacare was that the individual mandate was struck down (due to likely being unconstitutional). The thing is, in order for the whole thing to work, you absolutely have to have larger risk pools, and an abundance of younger, healthier people within those pools. With this current mess of a program, you have the healthier, lower risk people sitting out on the sidelines, while unhealthy people with pre-existing conditions comprise a huge chunk of the Obamacare risk pool. it’s simply not sustainable. Literally the worst possible situation for all parties.

Right there in your reply is why it doesn’t work

Insurance cannot possibly cover a pre-existing condition. That’s simply a giveaway. Why would I insure your pre-wrecked car? or your already burnt down house?

Agreed!

individual mandate was struck down Under the Tax Cuts and Jobs Act of 2017.

The Supreme Court ruled the Individual Mandate was constitutional as it was in effect a tax.

to DanF51

cruising along as usual

enjoying the comments

until i read your cruel

callous comment about

a dog not worth thousands

if you could save its life ..

your a f cking tool

@LGC

What do people do with pre existing conditions then? If I am born with Type I diabetes, does that mean I am doomed to financial ruin by paying for my own Healthcare? Who determines whether being born with a genetic disorder us pre existing or not?

great point i try to bring this up as much as possible. Also a hack of the system is you can carry no health insurance for years and bank the money. If you get sick you wait till enrollment and viola no pre existing conditons. I Dont but you could.

I own a small portfolio of single family rentals. My insurance premiums just DOUBLED with no claims. Some more than doubled. It’s insane.

I’m sure the value of your properties doubled in the past few years, and rent income also went up, but you ain’t crying about that.

And that’s what happens when you go 16 years without a REAL recession & the government keeps inflating away its debt crisis.

It’s going to be really interesting to see what Warsh does. Will he actually find creative ways to destroy money & get Fed’s balance sheet under control?

Will he be more vocal to Congress about their getting their fiscal house in order?

I just don’t see a recession coming along without something very unexpected happening. whatever that may be.

The elephant in the room is the fastest increase is the cost of health insurance. An American cartel created by the Congress of the United States of America

Who are they working for ? Apparently it ain’t us.

Because good health care is the minimum standard that a democratic government would establish

Insurers are gouging without restraint. Their recent underwriting profits have soared in some states while investment gains have skyrocketed. There has been no effort to rein in insurers by politicians who get paid off by them.

Apparently there have been some huge judgements handed out by juries.

People drive like bats out of hell nowadays.

They are probably trying to recoup their losses for their private credit lending activities. Pardon the sarcasm.

Yeah. Just look at the wild succes of CA’s efforts to “rein them in”. So successful…

Buffett Berkshire Hathaway said insurance is his best business. He loves the insurance business.

“The underwriting profits are nice, but the real value is the insurance float (over $170B+) that Berkshire invests in stocks and businesses.

That’s why Buffett says insurance is the “engine” of Berkshire Hathaway.”

It’s cuz he uses the float, which I guess was a new approach to investing.

He also always has tons of treasuries to backup the float, just in case.

Or now greg does, Warren enjoys reading and soft pillows

The pressure on oil prices is presently intense, and looks to get worse before getting better. The Fed will end up RAISING interest rates if these indications of inflation pan out. That will obviously kill any economic improvements that Trump has bragged about will happen. It is always much harder bringing down entrenched inflation than if it were stopped in the first place. Fed chairman Powell will be vindicated if this hot inflation continues. Even though his early “transitory” statements were rediculous.

I’m a hawk, and yet even I don’t see that raising rates would do much of anything to help with oil-driven inflation.

Nor will cutting rates do anything to help unemployment, due to structural AI changes. Yet the Fed will use excuses that don’t apply, anyway, when making rate adjustment announcements. The Fed has no credibility left at this point, as they have ignored their 2% inflation target for about five years now.

If you raise them high enough the economy fumbles and oil demand goes down.

I’d rather have expensive oil. That slows the economy plenty of its own.

Gattopardo: Apparently the FRB agrees with you. No possible way to control the price increases, may as well cut!

JeffD: What “help” does near historic low unemployment need? May as well cut!

re: It is always much harder bringing down entrenched inflation than if it were stopped in the first place.

Hardly. Take Black Monday as an example. Legal reserves were drained at the fastest rate since the GD.

“Fed chairman Powell will be vindicated if this hot inflation continues.”

IMO Powell has nurtured inflation above the alleged target of 2 % to placate us dweebs whose pocket is being picked,

The way it works is that money held by the criminal banks that are paid the interest that I am paid on my savings that I have accrued these past years since my birth as a WW2 baby

Except the trillions of dollars they are being payed interest for is money that the Fed created to establish the most irresponsible monetary experiment, QE.

Of course we have gone 30 trillion in debt transferring the cash into the pockets of the fools that are now making the decisions for us

I feel the US economy right now is like driving a car at night, in the rain, full throttle, with bald tires, worn out brake pads, on a straight stretch, but with a tight curve ahead.

Really? Idk to me … just my opinion… this is sorta what equilibrium looks like. Full employment, mostly tamed inflation, market pushing consistent highs including highs in the DOW (usually a great sign).

We just started a war and the market reaction was to jumpstart back into gear. We can’t decide if we need more or less restrictive monetary policy so we hold rates steady. Layoffs are offsetting hiring, companies are invested in retaining talent and even low hire creeps the unemployment rate lower.

If you ignore who I would call “the people that must tell you (because they are paid to) that everything is going bad” it honestly looks incredibly robust and remarkably resilient.

Just my perspective 🤷♂️

Health Insurance is an outlier – the whole industry was shredded by PE and until we fix ACA the prices are just made up to feed greedy middlemen.

Good summary IMVHO Kirk.

Other than the very obvious increases in what used to be called the ”wholesale’ world” by us in the construction industry trying to estimate many millions, sometimes even billions for the years needed to finish a project of that size, WE, in this case the family WE have seen our food costs almost double or better in the last five years…

And, although our home has also doubled in both of the last five years,,, our income has not even gotten close.

”TROUBLE AHEAD,,, TROUBLE BEHIND” as was part of some song years ago, appears to be exactly right today.

Hedge accordingly has been seen on Wolf’s Wonder???

Things are great if you own a home, have lots of stock, have a good healthcare plan without huge premium increases, and are in a stable job field.

For lots of Americans the economy is a source of misery. Biden got booted for inflation and gas lighting the public by telling them things were fine. Let’s see if Trump if dumb enough to do the same.

YES! Exactly that. The percentage of the american public in that situation is important. IF that percentage is small then the situation cannot hold. I’m in that situation but most people I know are not. Interesting times.

65% of US households are homeowners; of the 35% who rent, a big portion are “renters of choice” who could own but don’t want to for various reasons, including flexibility, no hassles, and high-rise living in city centers.

Over the 60% of households are stockholders, directly, including over 72 million 401k holders. Others who don’t own stocks have other assets that have soared, such as PMs, cryptos, or real estate. Lots of RE investors don’t own stocks. Lots of people have savings and money market accounts but no stocks.

The portion of households who have no assets to speak of is somewhere in the 25% range.

This is precisely why the US economy is very vulnerable to big price declines in stocks and RE because they’re so widely held, and so many people would get scared and reduce spending when their asset prices tank. This would be widespread across the population.

So a majority of Americans are fine. Got it

@Wolf,

So “steady as she goes” with the debt fueled party?

JeffD

The debt problem is with the government and some segments of the corporate sector, esp. Private Equity owned firms, and Private Credit, and in some parts of the financial sector (hedge funds, etc.). the consumer is in pretty good shape when it comes to debt.

It’s not tamed At All.

Gas is about to go to $4.50 a gallon and all products and services will rise 5-10% because of the gas prices (transportation & uncertainty).

Equilibrium was December 2024, that was normal times. This is talking heads, burning down the house! 🔥

Inflation has not even remotely been “tamed”, as any regular reader of this site would know.

According to consumer sentiment you are in the minority.

I doubt new college graduates feel as comfy about the economy as you do.

Your perspective is respective of your situation but it lacks empathy and isn’t that the how we are in this mess!

But if the driver is a highly capable, trained expert driver, who is fully aware of any possible hazards, maybe the tight curve can be handled.

As someone once said, “We’re careening headlong towards… something.”

I agree except I would change the rain storm to a white out where the wind blows the desiccated snow whose free moisture has frozen in the 20 degrees below zero turning the snow like a dust storm

or not

For most business’ health insurance costs are compensation. To look at cash wages in isolation and say inflation is low is therefore misleading. One should look at compensation as a basket. Including healthcare insurance costs. When one does so, the compensation increases that Americans have been receiving over the last decade likely exceed inflation. The issue is that that compensation is being wasted by a horribly ineffective and fraud ridden industrial healthcare complex. While I am a conservative, the writing appears to be on the wall that the US healthcare complex needs to be nationalized. Not a “single payer” system, but a true nationalization like in Canada or the UK where it becomes a public health service with sovereign immunity. No more ambulance chasers suing for every misstep. And then aggressively use AI to remove large numbers of doctors, and unneeded testing from the system. If the US does not do so it will become more and more non-competitive as a nation.

Thank you for saying this. It is a ridiculous system where as a business owner I need to be responsible for choosing healthcare for my employees.

Wow- What a non sequitur – The US health system NEEDS to be nationalized… Sovereign immunity so they can’t be sued… AI doctors …unneeded testing…… you went from rational to ranting all in one post.

The US health system is far too expensive, mainly caused by market dislocations in that people who use it, aren’t directly charged for it, along with excessive end of life spending on a small number of people. The cost for tort’s is a rounding error- and is how a functioning society determines fault, prevents reoccurrence and dispenses monetary justice. Throwing that out and saying “sorry we sawed the wrong leg off, sovereign immunity” isn’t even remotely reasonable.

As far as my proposal to moderate costs, More doctors to start. Get rid of the cartel that exists now. Allow people other than doctors to do a more wide ranging number of procedures or prescribing and the ability for individuals and/or corporations to buy insurance from the government.

But it’s a hard problem no matter what- with no easy solution.

People scream about U.S. healthcare…

until the doctor drops -“you’re dying” . Then they’re first in line, begging for the best and that is here.

Same folks destroying themselves— burger in one hand, beer in the other, joint lit, glued to the couch. Hypocrisy much?

America tops the obesity charts—over 40% of adults obese.

Result? Flood of preventable chronic crap—diabetes, heart disease, the works. We spend fortunes treating instead of preventing.

Tiny European countries get thrown in our face for comparison.

Newsflash: 330+ million people here. Different laws. Different scale. System wired for breakthrough innovation and elite specialists. World-class talent ain’t cheap.

Obamacare? Forced one-size-fits-all mess. Piled on bureaucracy.

Ignored root rot—fraud, abuse, endless lobbying cash grabs.

Yet…

when it’s life-or-death, need the absolute cutting-edge treatment, rare specialist, or last-hope procedure? The world still flies here. Mayo, Cleveland, Johns Hopkins—packed with international patients chasing what nowhere else delivers.

Gripes are loud. Reality is louder.

I believe the EU has a larger population than the US and patients flock to their hospitals too … even from the US.

you hit on alot of simple solutions to parts of the problem. Problem is many many many ox will be gored see how that goes. Hey maybe ai will solve it all one day.

Easiest way to fix would be to separate categories of people in health insurance.

They already charge more if you’re a smoker. I’d love to see a system where if you’re obese, drink alcohol, do other drugs, do excessively risky hobbies, or similar, you also get charged more.

In addition the high cost of American healthcare in many cases is not (merely) the fault of insurers but also providers. American healthcare is not a monopsony, and wages for those working in the system are far higher than elsewhere. Not to mention the execs and other management that are technically nonprofits but in reality are for-profit corporations and should be recognized as such.

The problem is that the people who control the system have such a huge amount of control over the economy that few dare stand up to them. But it will fail, and when it does, the fallout on healthcare will be something to see.

And send those doctors north the the country you want to be more like where the government, notably Quebec, treats them like crap to the point where they leave and there is a 5y waiting list to get a personal physician.

Somewhere there has to be a good public/private combination for health care. I’ve heard the UK is good that way.

Switzerland and Uruguay have pretty highly regarded public/private systems. Also ~9MM and 3MM in population respectively so… scaling?

I lived in Switzerland for 5y and it was basically a “private” system except health insurance was mandatory and usually paid by the employer as a taxable benefit. I’m sure that’s part of the reason I had a 34% marginal tax rate compared to 52% here.

The care was truly excellent! Local doctors had MRI machines.

Of course, the cost of living was 2x that in Canada.

Well there is a good solution. It’s called medicare for all. I appreciate my medicare after experiencing the health insurance jungle. For 45 years staying in jobs that sucked for years so that my family had health insurance.

Until Obamacare I was paying 15000 per year for heath insurance after being laid off on a cobra extension of 18 months, Of course they denied every claim betting I would soon be gone.

Having worked on significant health care companies, I can only nod and agree.

It’s all been a massive scam to extract government cash outflows and get them into PE pockets.

The problem is they made the scam legal, it’s not really fraud, and some of the bad actors just sailed off to Costa Rica on 40’ yachts paid for with public healthcare subsidies

The gentleman I spoke with in Marbella who builds and designs , I recall told me the real yachts don’t start until 20m.

I do enjoy them parked in the dock or off the coast but out at sea no thanks.

Off course healthcare is a scam but the USA is nothing but a business to extract from them move away.

The gentleman from Marbella told you the lesser yachts aren’t real? You can get a decent blue water capable 40 ft sailing yacht for a couple hundred thousand. And there are plenty of $80m yachts that would capsize if they left the marina on a windy day.

When I retired 15 years ago, I paid nothing and the company was paying $1200 a month premium. It covered 80% of cost and 100% over $4000 out of pocket. Go to any doctor and hospital.

The younger generations have been raked over the coals. It’s a crime.

Obviously our current system is broken. This article brought up a point I didn’t consider. The increased costs from the middle man reduced employee’s wage increases (while not improving their costs or quality of care).

“then aggressively use AI to remove large numbers of doctors, and unneeded testing from the system” …OR, cut out the middle man that is health insurance. I don’t think we need to go full socialism to lower costs. We just need to sever the connection between our health insurance and our employer and send everyone into the open market to buy insurance. Next, we should make health “insurance” actually insurance (something you get to protect against a low probability/high severity event). Most health care transactions could be handled between the user and the providers directly. Both of these would increase competition and price transparency. If we could set policy to get to that place, we could let the free market cook.

Imagine having your car insurance tied to your employer and needing to make a claim every time you change the oil.

We already effectively have many elements of a nationalized healthcare system, which is the problem. Price transparency, health care effectiveness transparency and market driven access to medical degrees would be more in line with what a true conservative would endorse. My inflation question; AI integration in the medical field will continue due to its improvement of outcomes, but will is this drive up overall costs due to AI’s hefty implementation cost or will it drive down costs due to its increased productivity potential?

That would cause you never to get care, just FYI.

There are 72hr waits now in hospitals.

4 month waits for doctor appointments.

As someone who has worked in both Canada and the United States, US healthcare should absolutely not be “nationalized”. The NHS in the UK is nationalized, and Canadian healthcare is generally a public payor, but private delivery. Unfortunately, both systems suffer from significant underfunding and delays that would untenable to Americans.

Instead, we should look to a system like Australia. There should be a guaranteed health benefit for all and a network of public hospitals and clinics. There should then be private insurance available for purchase for those who choose to buy it or those above a certain income level. Having both a public and private system allows a safety net for all, while also providing choice for those who would like to pay more for expedited or non-formulary services.

Agreed, Canadian living in Australia. I found it weird at first paying to see a GP but it’s fair. Private insurance and Medicare work better than Canada and UK. Bulk billing GP’s and Medicare for less wealthy is slower for elective procedures but still good. Still I’m not sure rich Americans and over 65 would settle for anything less than the best which is what your current system favours. It’s complicated, mate.

I am in Canada and know a lawyer who specialises in suing hospitals and doctors. As for ‘sovereign immunity’ whatever that means in the US, folks and businesses here sue civic, provincial and the federal govt all the time.

Clearly the solution to healthcare is NOT eliminating the high- margin insurance companies, but rather eliminating: the doctors.

Replaced with? Computers and software!

Also, NOT over 40% obesity rates, but closer to 35%. Still more than 1/3 people.

Certainly the “food” supply is a factor. Many ingredients that are allowed in “food” products are illegal in other places.

BUT, chemical, pharmaceutical and insurance companies are great stocks to own, so you can sell their overpriced shares to buy a nice wooden box!

If the medical profession was appropriately tiered, prices would be nowhere near as high. 80% of doctor visits are for trivial issues. There should be a four year training program for “front line medical” (in place of a college degree), and the frontline can refer the 20% of “real” problems to specialists.

Interesting comparison. Annual costs for employer paid health insurance plans are now at $27,000 per family. Estimates for providing health care in Canada are about $7,000 (in USD) per person.

So roughly the same costs? 4×7,000 = $28,000 for a family of four costs in Canada?

The US annual cost for employer paid health insurance doesn’t include the employee contribution for the insurance, nor does it include the co-pays, deductibles, out of pocket costs. The Canadian figure is actually the average spent per person on providing/administering care. Better to look at healthcare spending per capita in my opinion.

Well there are a ton of details to do a real comparison. For example the Canadian number includes everyone including seniors who consume a disproportionate amount of resources. I’m assuming the US number is for covering people who have a decent job and presumably not in need of so many resources.l as the general population.

The USA has the world’s highest health expenditures per capita, but its life expectancy is far from the top, around 60th.

I’d love to see USA life expectancy broken down by whether a person has employer-paid versus self-paid health insurance.

It would also be interesting to know how much entrepreneurship (and other risky bets) never happens because people are afraid to leave their job and lose employer-paid health insurance.

Life expectancy rates are broken down for various factors, including sex (big difference universally) and by state (even huger differences). There is about 8 years difference between Hawaii and West Virginia, and about 5.5 years between California and Oklahoma.

1.Hawaii: 80.0

2. Massachusetts: 79.8

3. New Jersey: 79.6

4. New York: 79.5

5. Connecticut: 79.4

6. California: 79.3

7 Minnesota: 79.3

8. Rhode Island: 79.2

.

.

.

44. Arkansas: 73.9

45: Oklahoma: 73.8

46. Tennessee: 73.8

47: Alabama: 73.8

48: Louisiana: 73.8

49: Kentucky: 73.6

50: Mississippi: 72.6

51: West Virginia: 72.2

https://www.cdc.gov/nchs/data/nvsr/nvsr74/nvsr74-12.pdf

Your headline BLASTS something loud and clear – Everything is getting more expensive but workers are not getting compensated adequately to keep up with the raging inflation. Sounds like a winner.

@ Mario – Sounds like a winner –

Actually, since 2018 wages have outpaced inflation. Yep.

But more and more people will spend $10 in fees to get a $12 burger delivered. I’ve never seen so many folks paying for apps, subscriptions, overpriced coffee, and other lifestyle extras that could easily be cut from their budgets.

Yup. The tldr is that your standard of living is declining.

Wow. That’s crazy. I have never seen that list of disparity.

Notice what the bottom all have in common?

Poverty. Those are also the poorest states with the lowest incomes and wages.

Interesting, but not surprising. If you want to live a longer life, move to a blue state.

I am less inclined on longevity and more inclined on having better quality of life. I ‘d rather live a short but strong life than a long life full of misery and dependence on meds/machines.

Tht’s why I support euthanasia.

It has more to do with race than the actual state

I lived in a blue state for quite long enough, thank you, it was nothing to write home about.

Oh, if you ain’t got the do re mi, folks

You ain’t got the do re mi

Why, you better go back to beautiful Texas

Oklahoma, Kansas, Georgia, Tennessee

It ain’t the state partner, it’s the do re mi

awesome Woody Guthrie song. you made me listen to it again.

“high healthcare costs have significantly affected and reshaped the U.S. economy in multiple ways. The U.S. spends far more on healthcare than other wealthy countries, and that spending influences wages, businesses, government budgets, and overall economic growth. Here are the main economic effects:

Larger Share of the Economy

Healthcare now makes up a huge portion of the U.S. economy.

• In 1960: about 5% of GDP

• Today: roughly 18–19% of GDP

Pressure on Wages and Worker Income

Higher Federal Debt and Government Spending

Effects on Businesses and Entrepreneurship

Increased Household Financial Stress

Growth of the Healthcare Sector: Healthcare is now one of the largest sources of job growth in the U.S.”

@Rico-

Yeah, healthcare spending jumped from 5% of GDP in 1960 to 18% now. But we keep sicker people alive way longer and life expectancy rose from about 70 to 79 today.

Back then, diabetes or heart disease killed you fast. Now, expensive drugs, surgeries, and ongoing treatments let less-healthy folks survive decades. Kinda a good thing if it is you…

Plus, obesity tripled to now 40% of adults. In 1960 we moved more, ate less junk, stayed slimmer.

Today’s combo—longer lives for sicker people + modern obesity epidemic—fuels a huge chunk of the spending spike.

News flash, Rico — it’s the economic rents.

Not sure healthcare is the only (or even majority) component in longevity. Healthy lifestyle and a culture that supports that: walking and biking to get places…public trans supports that, healthy food not processed (US loves fast convenient and cheap) and finally time, US workers work a lot, little vacation, leave and long hours and long car centric commutes

Change those things and you’d see healthier people and ironically lower healthcare costs (maybe)

I really don’t know the solution to insurance premiums skyrocketing besides shopping around, which is nearly impossible if you get employer health insurance.

My home insurance was set to increase from 4200 to 4700, after a 3300 to 4200 increase the year before. Somehow I found a company to insure it for 3200 this year. I’m sure it will go up again.

The only insurance I have that hasn’t gone crazy is auto.

Health insurance is a ticking time bomb especially for a nation as unhealthy as the US. The vast majority of our problems stem from lifestyle diseases due to obesity including high blood pressure, high cholesterol, and type II diabetes. It’s a huge strain on the health industry that just continues to get worse because people are unwilling to change their lives. Perhaps it’s time for novel approaches to fix the system such as price caps for routine procedures and penalties for those who could revert their problems with exercise and diet. Those who are proactive about their health should not be penalized by subsidizing those who don’t care.

We need a massive public education campaign sustained over decades, as was done with tobacco. Unlike with tobacco, we need to educate not just on what foods to avoid, but what foods are good to eat. With exercise, emphasize that simply walking more is good, which is a great start for the least healthy. Show some shock footage of people losing feet, in wheelchairs, or wheezing from congestive heart failure due to unhealthy lifestyle, just as we were shown people on oxygen from emphysema, with tracheotomies, and other disfigurements from tobacco.

Too many Americans don’t take healthy eating seriously. I work in public health, and people will bring donuts to work meetings. I think to myself, “why don’t you bring some cigarettes while you’re at it?” Everyone knows this type of food is terribly unhealthy, and people will make jokes about measuring our blood sugar or lipids afterward. But if I joked about going out for a smoke break, no one would laugh. We need the public to view unhealthy lifestyle the same as smoking.

Auto premiums have also generally increased rapidly the last 5 years, almost 50% since 2020 nationally. Mostly attributed to inflation of cost and labor and increased severity of crashes (this I question.

Most of that increase is due to the 50%+ spike in used vehicle prices (replacement values for insurers) in 2021 and 2022, which I documented here at the time, and the spike in repair costs over the same period. The rest of that increase is due to much fatter profit margins now.

That makes much more sense, especially how used cars sometimes appreciated in value in my area, than “increased crash costs” which sounds like a convenient way to scapegoat the customer. Thanks for the insight!

Stocks struggle as oil surges and Treasury yields push higher amid market anxiety over Iran conflict

BX:TMUBMUSD10Y 4.146% CL00 +5.09% SPX -0.82%

Dealing with my insurance company at the time, Geico, for a recent hit & run accident was like dealing with gangsters like the mafia and the likes of Al Capone. The Hit & run driver had Geico also so my Geico insurance company claims adjusters decided to work with the Hit & run driver against us to avoid paying the claim. Most working people don’t have the time I had to fight the insurance company and give up. It took me 21 months to get paid for all our damages. Meanwhile we had to pay for everything up front until the final settlement was reached. I was retired to I had the time to do the litigation.

The time, and also the financial resources to cover the spread.

If this happened to some folks I know, it would be ruinous to their already stretched financial position.

These are Orwellian times. The data from real businesses and households point to raging inflation, while official numbers suggest everything is just great, reinforced by public declarations from the dear leader that prices are lower than when he took office. Plenty of media outlets now obediently parrot both. Good luck to everyone who hasn’t drunk the Kool-Aid.

I don’t know. I live in a large apartment complex that has had every unit rented for the last six years. Over the last six months, more and more units have been sitting empty, and for a long time. There are at least eight units sitting empty I know of, and that’s just on the walk from the street to my particular unit, without going out of my way to find empty units. Maybe inflation really is coming down, due to the arrival (finally?) of an actual buyer’s strike?

Alba,

You’re confusing cost inflation for businesses, with consumer price inflation.

This article here is about cost inflation for businesses and not consumer price inflation.

Businesses have had trouble passing on higher costs. How are they going to pass on higher healthcare costs? Well maybe by not raising wages as much — see the article.

PPI (from the hated government’s BLS) also tracks business cost inflation, it was also hot, and I said so:

https://wolfstreet.com/2026/02/27/services-ppi-inflation-explodes-goods-ppi-jumps-as-companies-shuffle-tariffs-to-each-other-food-energy-plunge/

Wolf – your second job isn’t at the circus, is it? You state “ You’re confusing cost inflation for businesses, with consumer price inflation.”

A little reality check: cost inflation for businesses leads to consumer price inflation.

🤣❤️🎇 Prices are set by the market. If the market participants don’t buy at the price the company wants, there is no sale, and no transaction. There has to be a transaction at that price for it to factor into inflation. Automakers have not been unable to pass on the tariffs and other costs, and they booked billions of dollars in losses for 2025. Companies go bankrupt all the time. Why? Because they cannot pass on their costs and keep making losses, you goofball.

Consider that every business ALREADY charges the maximum market price for their product or service. i.e. if they charge any more they lose sales.

Businesses love to whine about their costs at the same time bragging about their margins.

Margins are at record highs. They are threatened by rising costs. Which is not the consumer’s problem.

Good lord get a grip.

It’s pretty ridiculous that health insurance premium costs are higher than annual rent/mortgage costs for the majority of Americans across the US at this point. “Ridiculous” is the appropriate word, because a large portion of people paying that premium will not have a single doctor visit by any member of their family over the next year.

Ridiculous to say the least. My health insurance was more than my property tax, homeowners insurance, earthquake insurance, auto insurance and utilities COMBINED

And you pay it…

One thing just popped up. The current price for WTI and Brent is the same 80.50 for both. Why WTI is not (much) cheaper assuming the war does more effect on Brent customers?

Brent is below $85 right now (was $86 a few minutes ago).

WTI is below $80 now (was over $81 a few minutes ago).

The $5 difference doesn’t seem unusual. Sometimes the spread is a lot narrower, sometimes wider. Occasionally the spread is negative, with WTI higher than Brent.

Sometimes when prices move very fast, several dollars in minutes, the Brent data you see publicly might not have fully been brought up to the second, so that would also do a job on the spread if you calculate it yourself.

Today: 89 WTI, 86 Brent, per https://www.cnn.com/markets

Look somewhere else than CNN. It’s quoting apples and oranges in terms of futures contracts. For example, CNBC right now:

Brent 91.05

https://www.cnbc.com/quotes/@LCO.1

WTI 88.46

https://www.cnbc.com/quotes/@CL.1

OK, thanks.

The other thing to keep in mind with commodities prices and charts is: Who is paying that price, AND taking delivery?

My friend who “made a bunch of money in oil,” trading, is different from friend who manages an exploration company (and made a bunch of money).

The amount of derivatives out there dwarf the size of the REAL, tangible assets.

Interesting to think that some tariff and inflation costs are being passed on in the form of reduced raises for existing employees.

Is that also a partial explanation for reduced hiring?

Seems if employer portion of health is soaring, one response would be to reduce adding new payrolls.

Are there any statements about how many more hires there would have been without these cost pressures, similar to the statement that wages would have increased without them?

it is the death grip on the covid margins.

businesses will do anything to try to hang on to those juiced margins.

I still find it wild that a healthcare provider can largely not tell you what anything costs, often with significant after the fact billing. Even for simple straightforward stuff.

I’m not a proponent of legislature but I’d support a law that says if the facility is in-network, then everything associated with what you get done is also in-network.

I’m sure there will be negatives with that plan though.

California has this law in place, since July 1, 2017. On Jan 1, 2024, another such bill was passed in California, applying specifically to ambulance companies. I agree this kind of protection should be Federal, especially when you are paying $27,000 yr just for the premium, with covered services (like ambulance) still generating yet additional fees, after premium costs.

I just experienced that at Labcorp. I asked what a specific standard test would cost, if not covered by insurance, and nobody in the office had any clue.

Ridiculous.

Providers are able to sidestep this requirement. I tried this with Quest Labs a few years ago, when I went to the doctor without insurance. The doctor gave me an order for a basic workup that should have cost between 60 and 200. I took it to Quest and asked the cash price, and they quoted me at over two thousand dollars.

Imagine if any other business worked this way?

Hey what will this honda civic cost? I don’t know, go ahead take keys and we’ll bill you later.

And then you get multiple separate bills with various breakouts from companies you don’t even recognize for months and months later…unsure when you are actually done paying for said civic which now costs you $250k when your budget was $30k

It looks like another case when the small caps catch up cut short going forward. They do not like inflations, tariffs, and strong possibility of the rates raising.

Key Data Points on Colorado Home Insurance Increases:

Recent Trends: Rates increased by 11.0% in 2023, followed by 11.4% in 2024, and are projected to continue rising.

Cumulative Surge: From 2019 to 2024, Colorado home insurance rates increased by 76.6%, the highest in the nation.

Long-Term Impact: Between 2015 and 2024, the average premium increased by 137%, from $1,745 to $4,142.

Driver of Costs: While wildfire risk is a factor, frequent and severe hailstorms are the primary driver of rising premiums in Colorado.

Comparison: As of 2024, Colorado had the second-highest home insurance premiums in the U.S., behind only Florida. My 2025 renewal $2800 vs My 2026 renewal $5800. $3000 increase living 15 miles SW of Denver Airport. Don’t get started on automobile insurance in CO. #1 in car theft and uninsured motorists (migrants). I’m all wet.

Oil is essentially price inelastic. If the FED doesn’t accommodate the price rises, then there will be deflation in other prices.

If the Fed does accomodate the price rise with rate cuts, it will pull forward investment into AI by businesses, accelerating job losses.

Inflation in medical costs blows away most other tracked costs. The US spends more than double per capita on healthcare than other developed countries and healthcare costs in the US are far outpacing inflation and even with this high healthcare spend the US has one of the shortest lifespans in the G20, currently ranked #55 in the world. Medicare is a huge part of the US budget and cost of insurance a huge cost for businesses. It would seem that the US should take a look and find out how most of the world is doing healthcare for half and living longer

https://www.in2013dollars.com/inflation-cpi-categories#All-items|Housing|Medical-care|Gasoline-(all-types)

https://en.wikipedia.org/wiki/List_of_countries_by_life_expectancy

WTI Crude Oil is at $90.20/barrel and Brent Crude Oil is at $92.58/barrel today.

$100/barrel oil is just a heartbeat away.

Any further thoughts on this topic?