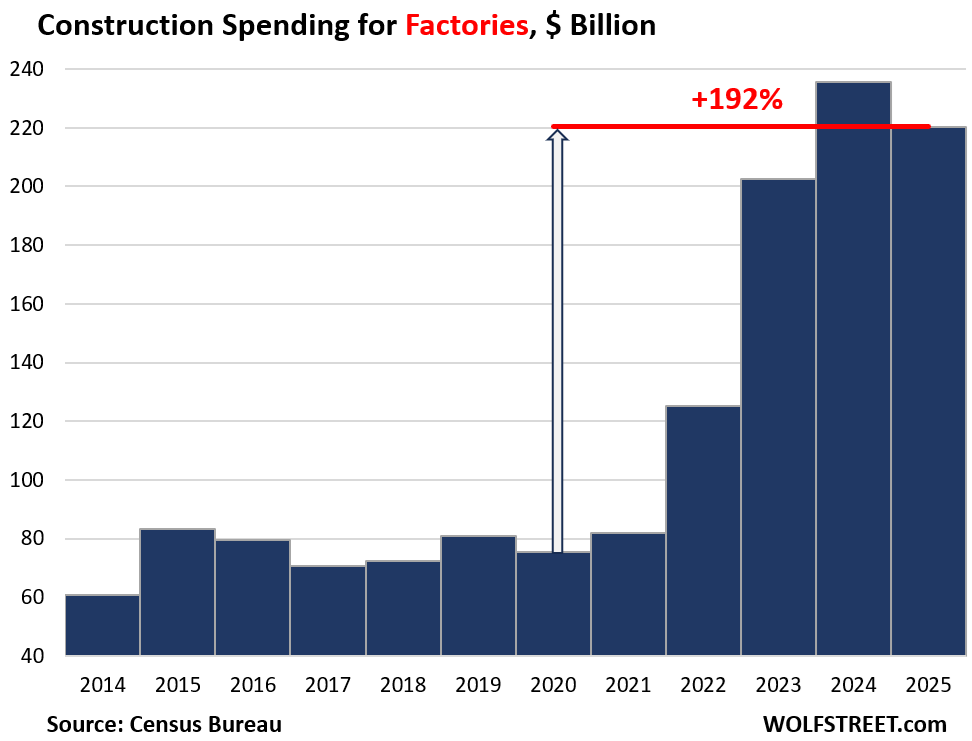

Despite the hoopla about data centers, spending on factory construction was five times larger.

By Wolf Richter for WOLF STREET.

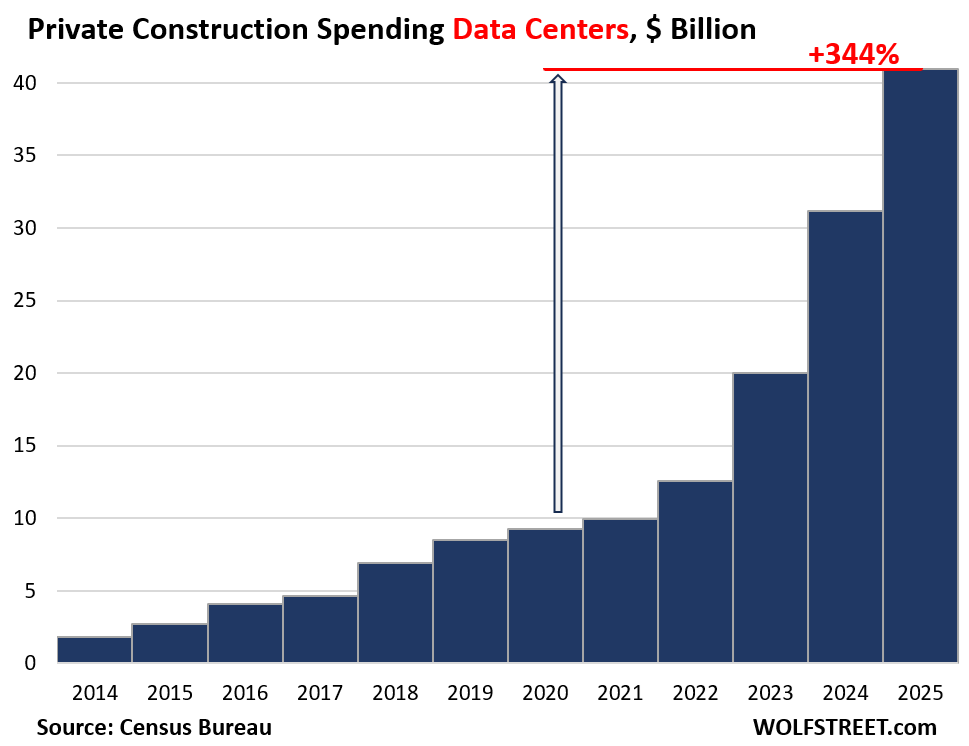

Construction spending on data centers in 2025 exploded by 32% from the prior year, by over 100% in two years, and by 344% from 2020, to $41 billion, according to the Census Bureau on Friday. Spending on construction costs of data centers used to be buried in office construction and was minimal compared to office construction. But more recently, the Census Bureau split out data-center construction spending going back to 2014.

Construction costs of data centers are only a relatively small portion of the immense amounts spent on AI infrastructure, most of which goes into electronic and electrical equipment, from AI servers to power generation equipment. Construction spending on data centers does not include the costs of the servers and racks but does include the cooling systems in the building and other built-in electrical equipment.

It takes years from the decision to build a data center to the data center being actually operational. And the massive amounts of capital expenditures announced by AI-related Corporate America in 2025 and the plans for 2026 haven’t yet shown up in the construction costs.

The amounts of capital expenditures being thrown around for 2026 are fantastical. Five companies alone – Amazon, Alphabet, Microsoft, Meta, and Oracle – have announced plans for $700 billion in capital expenditures for 2026, largely for AI-related projects. And how will they get this cash next year?

So this construction boom is not slowing down, unless tripped up by further the shortages of all kinds, such as power from the grid, power generators when there is no grid power, electrical equipment, electricians, specialized labor, etc.

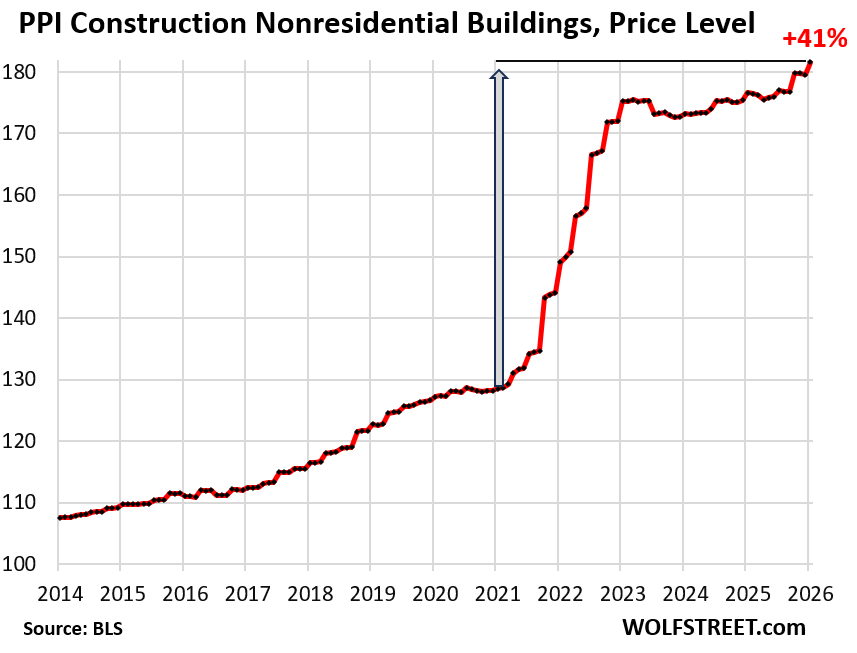

Inflation for construction costs for nonresidential buildings jumped by 1.1% in January from December, according to the Producer Price Index (PPI) for nonresidential construction, released by the Bureau of Labor Statistics on Friday (it was hot all around). Year-over-year, the nonresidential construction PPI was up by 2.8%, almost all of which occurred over the past four months.

From January 2021 through December 2022, over those two years, prices had exploded by 34%. From the beginning of 2023 to mid-2025, prices flattened out. But they’re now taking off again.

Over the years 2021-2025, the PPI for nonresidential construction rose by 41%. With spending on data center construction up by 344% over the same period, the red-hot construction spending boom is not a result of inflation – but of the AI investment mania.

Construction spending on manufacturing plants has soared coming out of the pandemic. In 2025, at $220 billion, it was up by 192% from 2020.

This $220 billion in 2025 is over five times the amount spent on data centers ($41 billion).

The production equipment in the plant, such as the industrial robots, is not part of the construction costs. And they’re much more costly than the building itself.

Though still running at a red-hot pace, construction spending on factories has backed off from the spike in 2024, possibly as construction resources have been pulled away by the boom in data center construction, and amid reports of bottlenecks, shortages of skilled labor, and ICE hauling off workers from construction sites.

After decades of globalization, there is now a widespread rethink underway about production in the US.

These factories will all be highly automated to where manual labor is only a relatively small part of the product costs. Every year, year after year, decade after decade, automation improves, and companies try to cut their labor costs by expanding automation.

Within factory construction, spending on factories for computers, electronic, and electrical equipment exploded by 1,300% since 2020, from $9 billion in 2020 to $104 billion in 2025. This includes semiconductor plants and plants that build electrical equipment for the AI infrastructure boom.

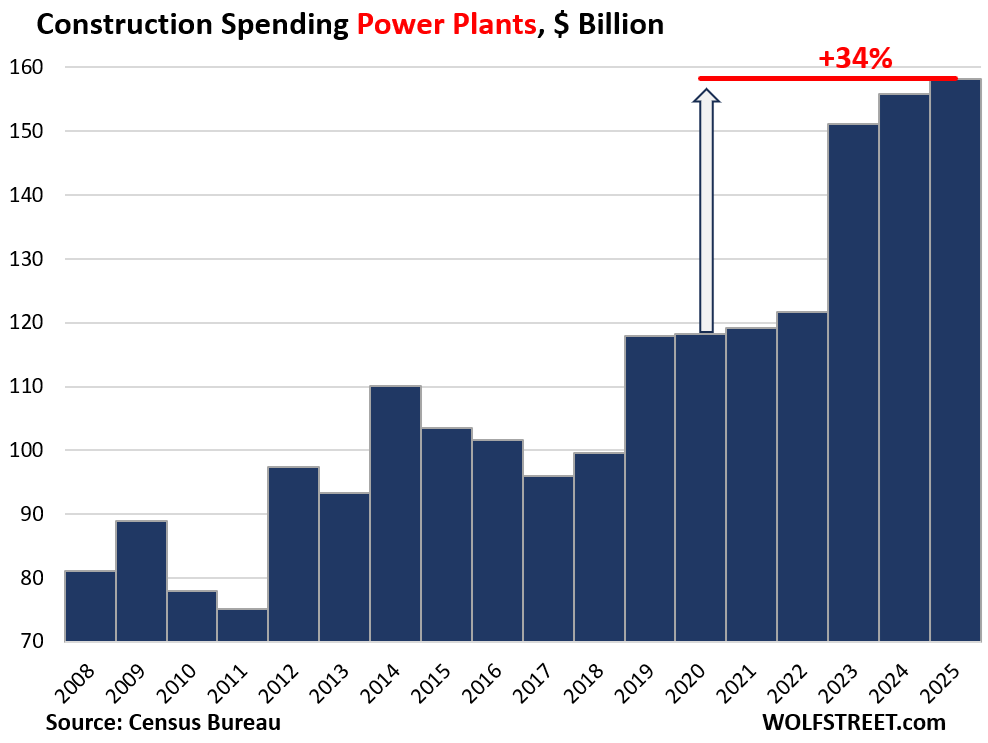

Powerplant construction is a highly regulated process in terms of permitting and approvals, and it takes years from the decision to build a power plant to having a functional power plant hooked to the grid.

In 2025, a record $158 billion was spent on building power plants, up by 34% from 2020.

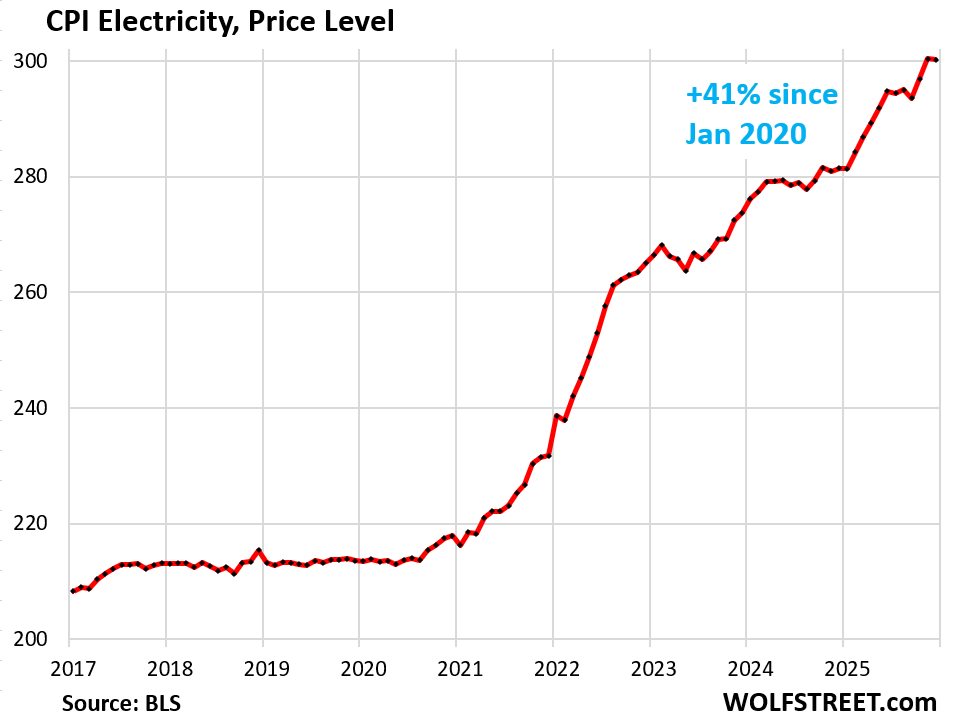

Electricity prices have soared by 41% over the past five years as demand for electricity has surged, after being roughly flat for 14 years. This increase in demand was largely driven by the new data centers.

But utilities and power generators are leery of spending billions of dollars on generation and distribution capacity for data centers that might never work out after the AI investment mania fizzles, which would turn these investments into stranded assets.

This leeriness is fed by the many hedge funds with ag land that want a utility to commit billions of dollars to run a high-voltage powerline to it, and possibly build a power plant to supply it with power, so that the hedge fund can then sell the ag land at a huge profit as data-center ready to some hyperscaler. If that deal doesn’t happen, the utility ends up with an expensive stranded asset.

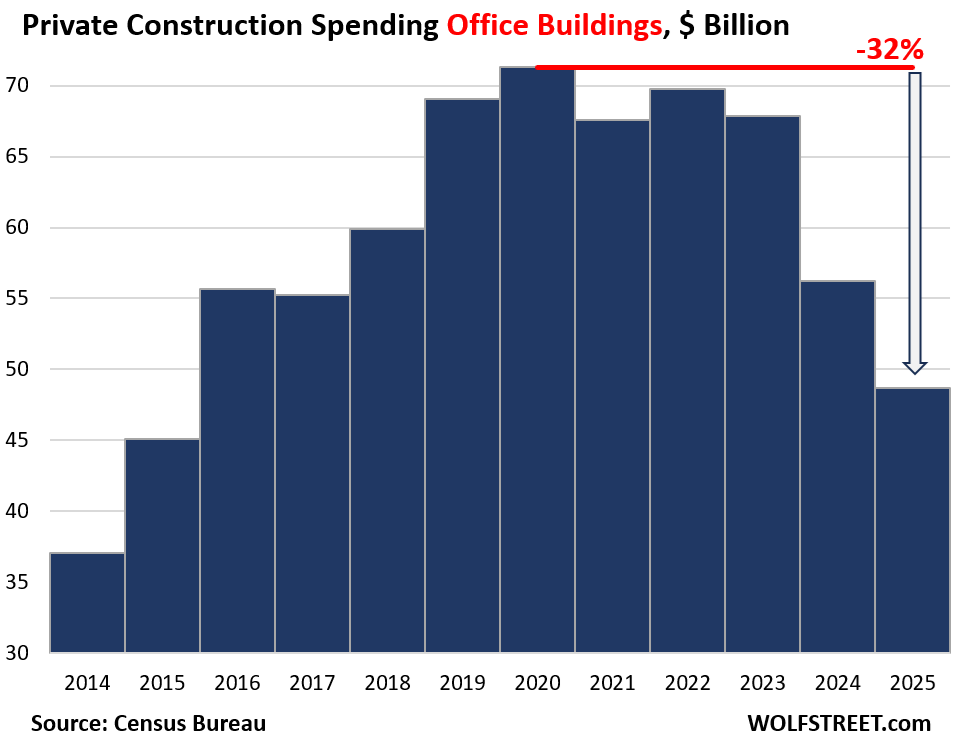

Office building construction has taken a massive hit after it became clear that office landlords were getting into serious trouble as demand for office space collapsed during the pandemic. Countless landlords defaulted on their office mortgages, and numerous buildings were seized by lenders and sold in foreclosure sales for cents on the dollar. The going rate for office building transactions is now at discounts of 30% to 70% from pre-pandemic prices. The delinquency rate for office CMBS spiked to record 12.3% in January. And there are efforts underway in expensive markets to convert office towers into residential towers, while smaller office buildings get torn down and replaced with housing. Office CRE has been in a depression since 2022.

In a way, it seems surprising that anyone would still spend good money on office buildings, but it’s the old office towers that are in trouble, while the latest and greatest office towers see more demand from the flight to quality that high vacancy rates made possible.

So spending on office construction (not including data centers) dropped further in 2025, to $49 billion, the lowest since 2015, and down by 32% from the peak in 2020.

Some of this spending is for buildings that were planned years ago and that are being completed now. For example, JP Morgan’s $3-billion tower at 270 Park Avenue in Manhattan was announced in 2018, was formally topped off in November 2023, and had its grand opening in October 2025.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Out of curiosity, I thought public utilities (like electricity) had to have public commissions and public debates about all rate increases and then have the rates approved by an appointed committee.

“Electricity prices have soared by 41% over the past five years…”

Check the California PUC. Totally in the pocket of PG&E. Over the past two years, rates were hiked multiple times. Gangster organizations. There should be no investor-owned monopolies. It does not work. Make them ratepayer-owned or municipally owned.

PGE is in the pocket of Sacramento. PGE was decoupled after the bankruptcy in 2001. Google that, please. But you have one thing right, the state government is a gangster organization. If you make SCE, PGE, SCE and SDGE rate-payer and municipally owned, good luck with funding grid improvements, veg management, build outs for new load. Another propostion every election asking for funding.

Another battle for you, half of the POU’s employees are union.

You don’t make PG&E a publicly owned utility (POU). You break it up and each municipality buys its piece of the assets. Sacramento did that some years ago, bought out PG&E’s assets in Sacramento. Works a lot better than the mess we have in San Francisco. SF is trying to buy out PG&E’s assets here, but it has been a long fight so far, but making some headway.

In terms of funding growth: Public utilities issue high-grate low-interest-rate bonds with which to fund expansion projects, and those interest payments are funded for decades by the revenues from those projects. That’s the business model of a utility. Those bonds are sought-after. That’s how it has always been done. Well-run utilities don’t have a funding problem.

There are 40+ POUs in California, providing power for about 25% of utility customers in the state, including in Sacramento and Palo Alto, whose rates are half ours here in San Francisco, and whose reliability is far greater. These are high-growth areas.

Search (or do an AI deep research) Mark Ellis and utility bills. He’s exposing the whole sordid underbelly of how the deal making works.

That’s how it is in northern Colorado. Owned by 4 different cities and then everyone in Denver is pretty much Xcel. Guess who doesn’t have power outages in wind storms and who does?

Near where I live there was a deal where an expanding conglomeration of hospitals bought a former mall. They kept the parking garage, and actually added at least one additional taller parking building, and are building a brand new satellite hospital campus where the former mall used to be.

Sure seems like a good use of the real estate, and especially, the parking-

Oh the hospital bills you will see…

Maybe a silly question.

So if construction spending for manufacturing does not include the cost of industrial robots, does the cost of data centers not include costs of the productive equipment the building ?

If the building cost is only counted, where is the cost of all the equipment counted?

Second paragraph:

“Construction spending on data centers does not include the costs of the servers and racks but does include the cooling systems in the building and other built-in electrical equipment.”

the cost of the building and the cooling system is only 25% to 40% of the total cost to make a data center operational excluding electricity capacity

Building & Cooling 25% to 40%

I/P 60% to 75%

Electricity capacity:

20MW = $15 to $50 million

to 100 MW = $130 to $300 million

trump has demanded the data centers pay for their own electricity capacity needed to run them

the gpus in the data centers will become obsolete in five years or less

95% of the companies using AI have not figured out how to pass on the cost to their customers

AI investment will be a disaster for the majority of the companies spending the money they will have no return on their investment

data centers increased the demand for baseload dispatchable electric power\

the supply of such power in the US went down one GW in 2025 while data centers added 11 gigawatts of additional demand. a similar supply demand gap is expected in 2026

data centers cannot run on 100% intermittent solar and wind power

“the supply of such power in the US went down one GW in 2025”

People who say that as if it were a problem don’t understand the concept of “base power,” how the grid works, and why there is even a grid. But it sounds smart?

“data centers cannot run on 100% intermittent solar and wind power”

All electricity generation is 100% intermittent. Try to run a gas turbine generator with no gas storage tank, regular gas deliveries, or pipeline connection.

What you mean is that data centers can’t run unless they have constant power.

Constant power = generation + storage.

The “renewables are intermittent but fossil fuels aren’t” omit the storage part of the analysis.

No, you fail to understand the term “intermittent” as applied to electric generators. Certainly, fossil fuel plants and nukes have planned outages, and also unplanned outages, but that is far different from solar (planned outages every night), and wind (highly variable and sometimes drops to nothing), which also have planned outages due to the need for mainenance, and unplanned outages due to equipment failures, just like other generation.

Storage for short time periods, like 4 hours, or long time periods, like 7 days? Big, big difference there, especially for batteries.

The US has three grids, the largest two are the Eastern Interconnection and the Western Interconnection, and they’re connected. Then there is the Texas Interconnection, which is not connected to anything, which was part of the problem in 2021. In addition, the Eastern and Western Interconnections are connected to the Canadian grid. Power generators send their electrons into that grid, and with enough transmission infrastructure, it doesn’t matter on which end a generator adds electrons, a user can draw electrons out anywhere on that grid. The wind always blows somewhere. Power plants are always running somewhere. Sun, wind, hydro, etc. are free fuels, and they bring the fuel costs down. The only thing that matters is that there are overall enough electrons in the grid to satisfy overall demand and enough transmission lines to distribute the electrons.

A data center or a household doesn’t need “base power.” They need reliable power, the amount they need when they need it. “Base power” is a concept that only applies to describing types of power plants (plants that cannot ramp up generation quickly, such as nuclear and coal). The old-fashioned gas plants were used as peakers, not base power plants, because they could ramp up quickly but were costly to run. A modern combined-cycle gas plant can ramp up the gas-turbine cycle of its capacity quickly. The steam-turbine cycle takes longer to ramp up because it takes a while to produce high pressure steam from the gas-turbine exhaust, but once both are running at a steady state, it makes for an efficient base power plant. Utilities switch between power generators all the time depending on which provides the cheapest electrons at the time, but the actual electrons they end up with don’t come from the specific power generator they made a deal with, but from the electrons in the grid. All this is highly regulated and controlled so that the grid doesn’t blow up.

You have a misunderstanding of AI.

“ 95% of the companies using AI have not figured out how to to pass the cost to their customers”

I dont know what “companies” you are referring to, but if you are talking about hyper scalers- they 100% have that figured out, and it’s helping drive their current record results.

If you are talking about companies implementing AI – then you are incorrect since most of what they are doing is automating work which used to be done by more people. It’s about an 80% reduction in most of these.

If you are talking about the foundational models (EG Open AI)- yep they haven’t quite figured it out, but a 700 billion private market valuation and the entire western world switching to AI says they are likely to find a way.

They have indeed figured it out: tokens. At my employer, AI tokens are being bought and consumed by the bucketful.

If there is so much spending on construction of manufacturing, can this be viewed as evidence that Trump’s strategy of bringing manufacturing back to the US is working?

No. When a company makes a decision to build a new manufacturing plant, it then has to find and buy the land, make the plans, get the permits, etc., before funds get spent on construction work. That takes a while, usually well over one year.

Spending on construction in 2025 is still the result of corporate decisions made when Biden was President.

But 2021-2023 was largely based on decisions following Trump 1’s trade policies of 2018 and fully implemented by 2019. But the corporate decisions made in 2019 in response to the trade policies were then delayed by the lockdown in 2020 and the uncertainty that followed. So the first big boost of spending is from the policies of the Trump 1 era. Biden’s policies then added to it in 2024 and 2025. Trump 2’s policies might show up in construction spending at the earliest in 2026 and likely in 2027/8.

Actually, what you’re looking at is a continuum. The administrations Trump, Biden, Trump roughly had the same trade policy: re-building the manufacturing base in the US. Trump 1 imposed tariffs. Biden kept most of Trump 1’s tariffs, but then piled incentives paid to manufacturers on top of them. And Trump 2 piled tariffs and incentives on top of them. Trump was the first President to acknowledge in 2018 that globalization has gutted the manufacturing base in the US, and that it was a huge problem, including a strategic problem, as we found out in 2022 during the shortages. This is the one area where both administrations were in agreement.

But AI spending is totally separate from White House policies. It is driven by its own rationale.

Thank you! Most informative!

I’m a bit confused, you said that construction for factories is a lot more than for data centres, but then turned around and said that it’s the data centres that are causing the electricity price increases. What amount of the electricity price increase is from the increase in USA manufacturing?

The size of the biggest data centers being planned today, such as Meta’s planned data center in Indiana, is now expressed in gigawatts, the required capacity of electricity one data center needs. So the Meta data center in Indiana, when operating, will needs a capacity of 1 GW of power. Data centers built some time ago and operating require hundreds of megawatts EACH.

Most commercial operating nuclear reactors in the US have a capacity of around 1 GW. So it would take 1 standard nuclear reactor in use today to supply electricity to 1 data center. They’re gigantic power hogs. Nothing comes even close.

That’s astounding. And that’s one company. Weren’t all these guys concerned about global warming and carbon credits like 5-minutes ago?

Now they need their own nuclear power plant. Quite a change.

“Weren’t all these guys concerned about global warming and carbon credits like 5-minutes ago?”

They were when it was fashionable, and didn’t really interfere with future plans or revenues. Net Zero has effectively died (except in some countries, like UK and Australia, and some US states, like California and NY), and the big AI companies have been happy to help kill it because, as Wolf noted, they need LOTS of power. And renewables won’t cut it because they aren’t reliable enough, and data centers must run 24/7, not 20-22/7.

even more astounding is that a lot of those planned data centers and data centers under construction are zombies.

There is simple not enough manufacturing capacity to fill all those data centers with servers. And even if they pay the premium to be one of the ones able to fill their building with equipment, they might not have power.

They need so much power that the local grid simply can’t supply them without expanding supply. And expanding supply takes quite a few years longer then some of those tech bros expect.

Especially all those announcements regarding SMRs are just coping.

Right now the waiting times for new gas turbines is apparently 90 months!!! The data center can power on just as the chips inside are obsolete.

Some are turning old airplane turbines into static turbines to produce power. Thats neither cheap nor efficient nor low maintanace. And high profile Musk is powering his data center for X/Grok illegal without permits inside a city. But no one tells him no.

Designing and manufacturing chips to drive AI used to be done manually when the complexity of the circuits was low.

As complexity increased, companies (IDMs) hired engineers to develop tools for automation. Over time, independent companies began to see these tools to replace the internal tool development teams. These companies that sell the automation tools are now, in some cases, billion-dollar revenue generators. The manufacturing Fabs are some of the most high-tech places in the world.

I suspect the same will happen for other high-value, high-complexity problems being solved by AI. Manufacturing will become even more dependent on technology.

In the future, manufacturing will become a larger part of the US and other leading economies and will require more AI- driven plants to be built.

What’s the relationship between automation (substituting labor with capital) and interest rates?

If we see interest rates go up to address inflation, would that also increase the human labor used in US factories by making automation more expensive?

I’m guessing there is not a simple relationship here, but I’m wondering how we get more labor to be a part of the reshoring in manufacturing.

4hens, Automation (substituting labor with capital) –> cheaper labor –> lower inflation –> lower interest rates.

Unsure how to get more labor to be part of reshoring in manufacturing…

Automation and interest are indeed linked in the way you describe although the link is somewhat weak as compared to global labor competition.

For manufacturers the primary benefit of automation is to transfer variable costs (labor) into fixed costs while reducing the total. You need high production volume to make that work.

That said even in an automated facility you do employ people. Maintenance, operations oversight, QA, and logistics still require people. Even if the production line is fully automated, those jobs don’t go away. A factory near me employs several hundred people to run a facility where the production line itself is automated.

The thing is that the number of jobs new factories will create is very fixed as compared to the past. The most relevant information in terms of employment impacts from a factory boom is the number of factory facilities. The more kinds of product you make, the more employment you’ll have. Production ramping up by itself doesn’t employ more people as labor will act more like a fixed cost than a variable cost.

US manufacturing will therefore be focused on high-volume products coming from massive facilities, and also facilities that can make many different kinds of product without needing to build new facilities for each one. The former implies movement in specific industries like steel production and forming, mass-market chemicals, and mass-market goods whilst the latter implies outputs from such things as machine shops.

In terms of adding more (variable-cost) labor to manufacturing, that won’t happen here unless the dollar starts being manipulated in currency markets. So I don’t expect many new manufacturing facilities that deal with small volume and need specialized facilities to create product of low value. Math doesn’t work in favor of automating that, and US labor costs are too high to compete against places like India.

Building all these data centers makes sense. While large scale LLMs are the current model, perhaps to learn or sell their ideas, they will only scale physically and economically so far. As we are starting to see small specialized AI models who sell those services for specific purposes will succeed and data centers can partition resources any way they like and very dynamically.

We are seeing a depression in traditional office CRE alongside a desperate scramble for data center space. Beyond the obvious power and cooling hurdles, what is the primary ‘data-driven’ reason we aren’t seeing a massive wave of adaptive reuse converting failed urban office towers into edge data centers? Is it purely a floor-loading and HVAC limitation, or is the ‘flight to quality’ in offices making those buildings too expensive even in ‘distress’ for data center economics?

Data centers don’t need to be near anything, need wide open space and at least +16ft clear space for the servers and all the trades and data cables. Data centers don’t need bathrooms, stairs nor access to a abundant workforce… Almost the opposite of what is needed for office space.

the building is the cheap part of an data center. suboptimal layout would be more expensive than any money saved. And more importently, cooling would be impossible.

Automation will reduce labor (which most probably will not be replaced somewhere else, contrary to historical evidence). What remains is the need to fund the social programs (social security, etc.) paid for by taxing/exploiting labor. One answer is to tax a robot like human labor plus remove the depreciation deduction.

MW: Any chance of a Fed interest-rate cut in 2026 is ‘evaporating before our very eyes’ with Iran war set to stoke oil prices