All of it to fund the ballooning debt that hit $38.4 Trillion.

By Wolf Richter for WOLF STREET.

This week, even during the relatively quiet pre-holiday period, the government sold $602 billion in Treasury securities spread over 9 auctions on four days (there are no Treasury auctions on Fridays), including 10-year Treasury notes and 30-year Treasury bonds.

Of these auction sales, $483 billion were Treasury bills with maturities from 4 weeks to 26 weeks.

The auction yields are in the right column. The rate cuts have pushed down the yields of T-bills, and of the 3-year Treasury notes, but have done nothing for the yields of the 10-year Treasury notes and the 30-year Treasury bonds:

| Type | Auction date | Billion $ | Auction yield |

| Bills 6-week | Dec-09 | 78.2 | 3.650% |

| Bills 13-week | Dec-08 | 89.7 | 3.650% |

| Bills 17-week | Dec-10 | 69.2 | 3.610% |

| Bills 26-week | Dec-08 | 80.3 | 3.580% |

| Bills 4-week | Dec-11 | 85.3 | 3.610% |

| Bills 8-week | Dec-11 | 80.3 | 3.614% |

| Bills | 483.0 |

And $119 billion of the auction sales this week were notes and bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Dec-08 | 58.0 | 3.614% |

| Notes 10-year | Dec-09 | 39.0 | 4.175% |

| Bonds 30-year | Dec-11 | 22.0 | 4.773% |

| Notes & bonds | 119.0 | ||

| Total auction sales | 602.0 | ||

The $39 billion of 10-year Treasury notes were sold at the auction on Tuesday at a yield of 4.175%.

They replaced the $21 billion of 10-year notes that were issued on December 15, 2015 at a yield of 2.23% and that matured in November. So nearly double the debt, at nearly double the interest rate. US government finances are not for the faint of heart.

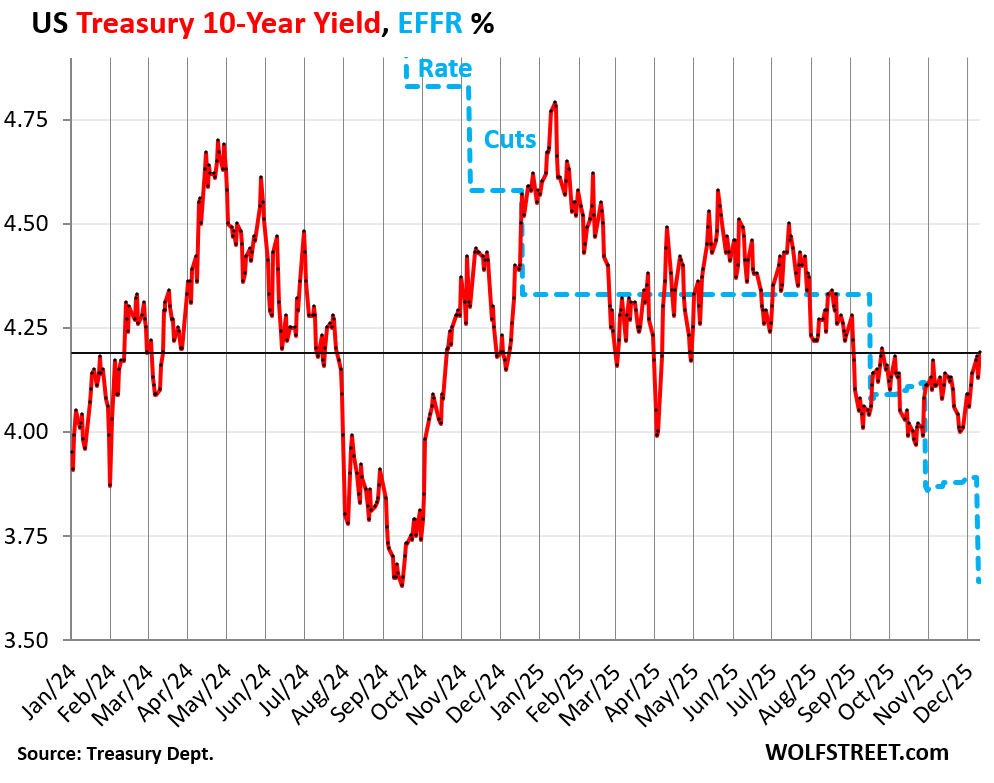

By early Wednesday, in the secondary market, the 10-year Treasury yield had gone over 4.21%. Then came the FOMC meeting, the rate cut, the T-bill purchases, and Powell, and the yield dropped 10 basis points but bottomed out at 4.10% by early Thursday. Then it bounced off and rose, and at the moment, Friday morning, was back to 4.20% (hourly chart via Investing.com).

So around the 25-basis-point rate cut announcement by the Fed, the 10-year Treasury yield fell in the secondary market but then rose again on Thursday, and by Friday morning, the 10-year Treasury yield was 54 basis points higher than the Effective Federal Funds Rate (EFFR, blue in the chart), which the Fed targets with its policy rates.

The daily chart below doesn’t show all the hourly drama of the 10-year yield around the FOMC meeting.

In normal credit markets, long-term yields, such as the 10-year Treasury yield, are quite a bit higher than short-term yields, such as the EFFR, and are not driven by the Fed’s short-term rates.

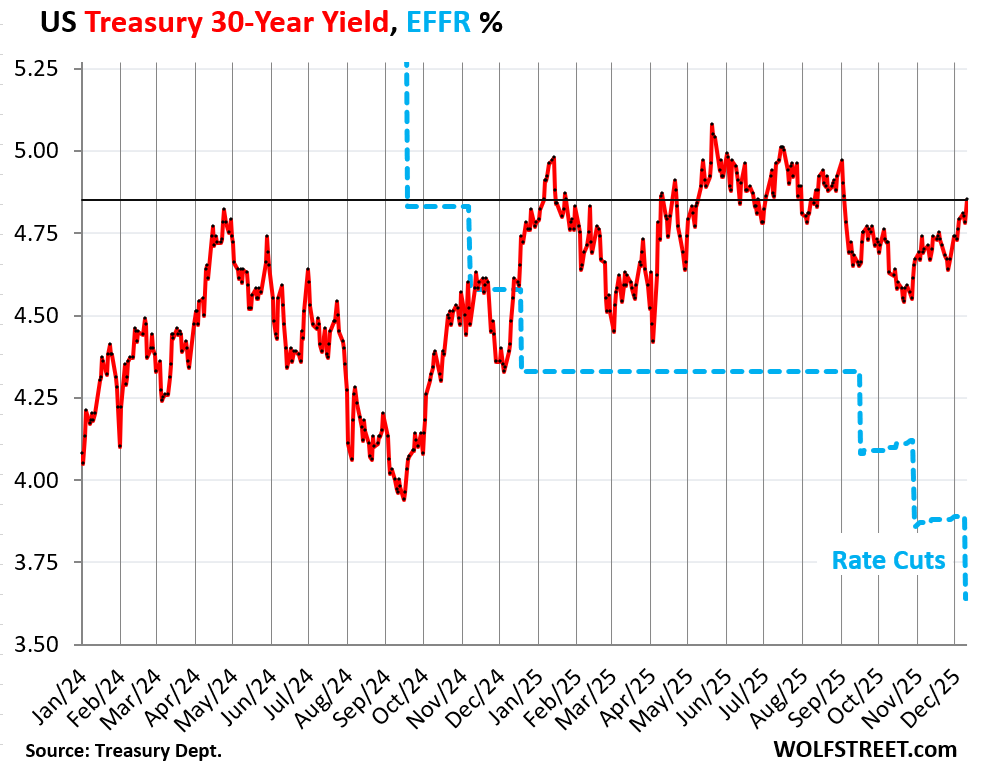

The $22 billion of 30-year Treasury bonds were sold at a yield of 4.773% at the auction on Thursday.

By Thursday evening, in the secondary market, the 30-year Treasury yield was back at 4.80%, and by this morning it rose to 4.86%, the highest since September 4. It’s almost funny how the 30-year yield blows off the Fed’s rate cuts. It’s all about inflation fears and supply fears:

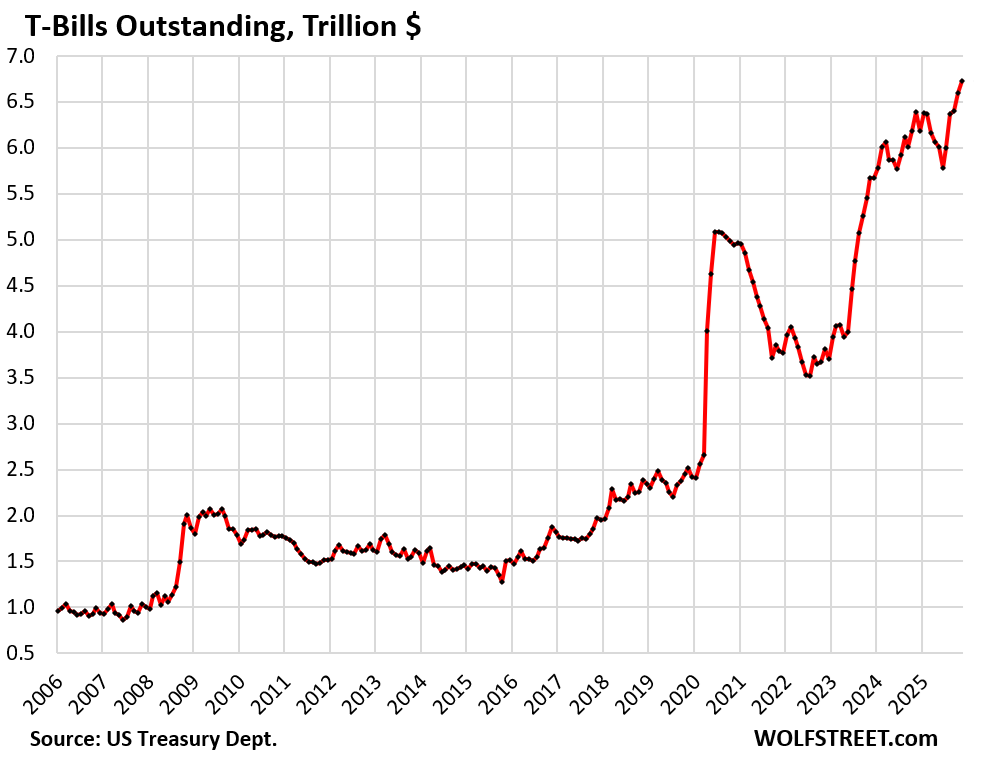

T-bills outstanding hit a record $6.7 trillion at the end of November, up by 18.6% from a year ago.

The Treasury Department is beginning to shift more issuance to T-bills, and the Fed is starting to buy them in the secondary market to replace the MBS that are coming off its balance sheet, and as part of its Reserve Management Purchases.

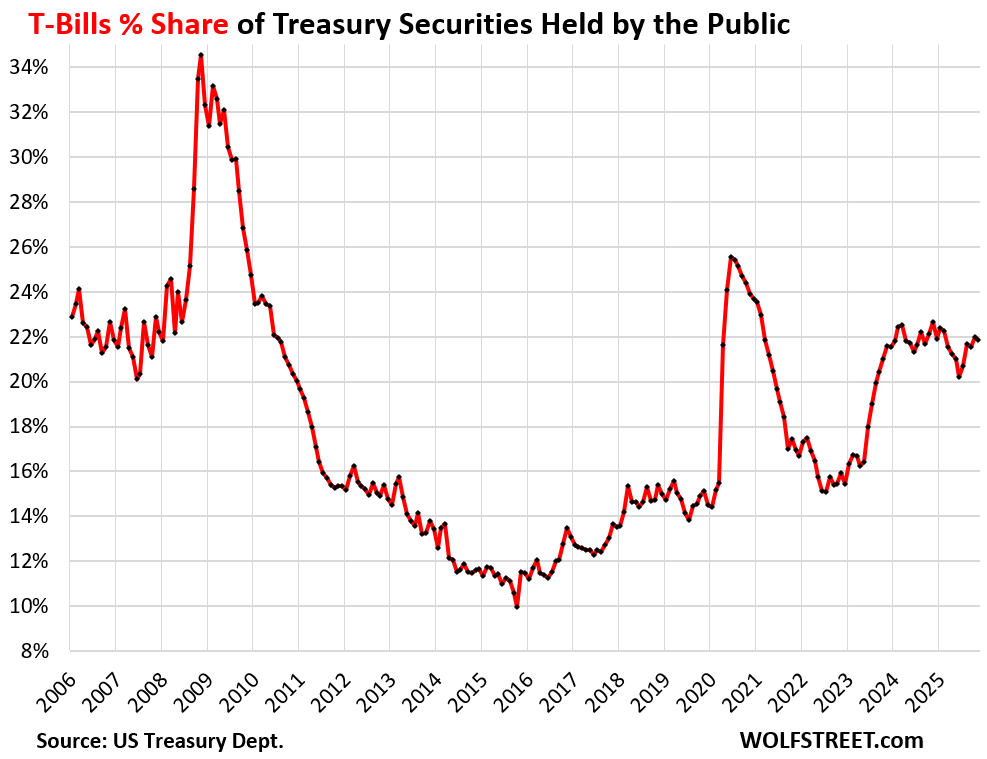

But the total amount of “Treasury securities held by the public” – not including those held by government entities, such as government pension funds and the Social Security Trust Fund – also ballooned to a new record of $30.8 trillion at the end of November, on substantial new issuance, and month-to-month, the share of T-bills actually dipped a hair to a share of 21.8% of all Treasuries held by the public.

During past crisis events, the government issued huge amounts of T-bills quickly which caused T-bills’ share of the total debt held by the public to spike for short periods, such as to a 34.4% share in November 2008 during the Financial Crisis, or to a 25.5% share in June 2020. During panic times, there’s lots of demand for T-bills. Then over time, the government replaced maturing T-bills with notes and bonds, helped by the Fed’s massive QE operations at the time, and the share of T-bills declined again.

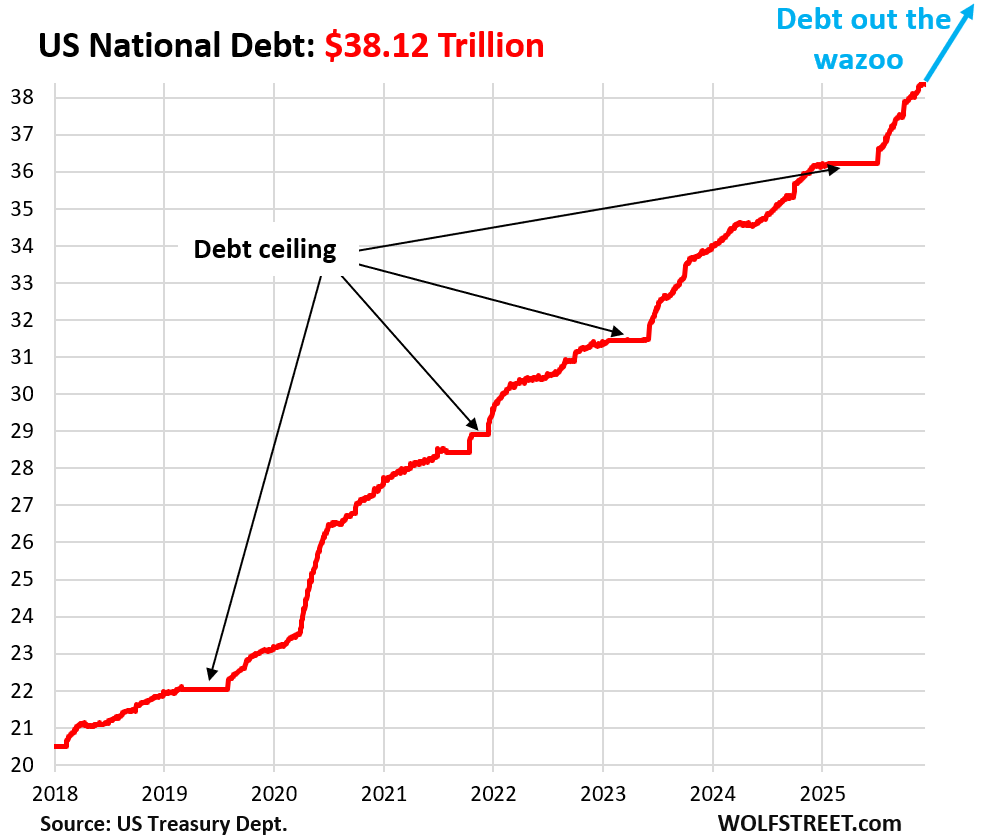

The Treasury debt that drives all this and that has to be funded and refunded through these auctions hit $38.35 trillion as of December 10, up by $2.2 trillion from a year ago.

This is the total debt, in all its glory, consisting of $30.79 trillion of Treasury securities held by the public and $7.56 trillion of Treasury securities held internally.

The portion of the issuance that replaces maturing debt does not add to the debt. But the additional issuance to fund the new deficits adds to the amount of the debt.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Let’s go 10y to 6%+ and 30y even higher.

Would you even buy then though? That’s true death cycle territory and the US would be unable (they ain’t hiking taxes or cutting benefits in near the magnitude needed) to service the new debt without a funcational default: fiscal dominance.

It’s a spending vs revenue problem that needs to be fixed ASAP. The American people need to wake up.

The portion of the issuance that replaces maturing debt does not add to the total debt, but might they need to replace an increasing portion of the shorter term maturing debt with long term debt, leading to higher interest expense, which would?

My question is: does the $38.35TR include debt of states/cities, etc.? It seems to me that when European countries report their debt to Eurostat, the total national debt includes federal, regional and local public entities. How is that in the US?

It does not. The states and local governments have another $5-6 trillion, collectively, if I remember correctly.

Theoretically, I would think additional state and local debt could cause the federal debt to increase as well, as if the states and local governments issue tax-free municipal bonds, investors in those wouldn’t pay federal taxes on the interest income. But I suspect the relationship is fairly tenuous.

“Treasury debt” = “National debt” = “Treasury securities outstanding” = Treasury debt”

State and local government debt in the US is about $6 trillion all combined.

Klaus Kastner, no the Federal supposed “debt” is basically a savings account for private enterprise, and the interest paid upon renewal is in the sovereign dollar, produced by the full trust in the U.S. Federal Government. Europe’s currency, again interest payment is the Euro, which is not the sovereign currency of any of the Countries, but of the European Union. Hope that helps.

…. Legal action of the currency in the U.S. is under the jurisdiction of the U.S. Congress, and the Federal Reserve Bank. Each in It’s own can be dictated by the popular vote of only citizens of the U.S.. in essence. Individual Countries in the European Union do not have that, they can be the minority vote on the value/use of the Euro. I personally think England’s goal toeave the E.U. is a good thing for them. The E.U. monetary system hasn’t helped Greece in substance for their citizens.

The Fed continues to attempt water to run uphill.

More supply, in a free market, would depress prices.

The conclusions are obvious.

4.2 should be the pivotal point for trading ten yrs….and likely the Fed will find a way to protect those who took down the auctions…for a while.

Tremendous article in mises.org regarding the societal and generational impact of pumping assets. In an inflationary environment labor trades at a discount compared to assets and durable goods. Services are beginning to catch up, but can they continue?

Looks like I will be exiting the treasury market. It used to be a better deal considering no need to pay the 9.3% CA state tax but now my savings account even with that pays more. Might as well have that money fully liquid if not making additional money on locking it up. Hopefully long term goes up but my sense is just way too much money and people will purchase even if not much more than inflation and nice to have sideline money to put back in market whenever downturn eventually shows up. Definitely a challenge right now as I start getting ready for retirement in a few years.

I mean…do you really think your savings account interest rate isn’t going down as a result of this???

When the fed was raising rates, I would get a crowing email from my bank that they raised my account rate (weeks if not months after the fed raise!).

Now that rates are falling, my bank lowers my account rate within a week or two, and sends no email.

It’s pretty funny!

Where is the money (Cash) that financed $38.35T national debt?

Wow, we’re up $2T since the debt ceiling, great work to all our leaders in DC! Phenomenal growth, very inspiring to us all.