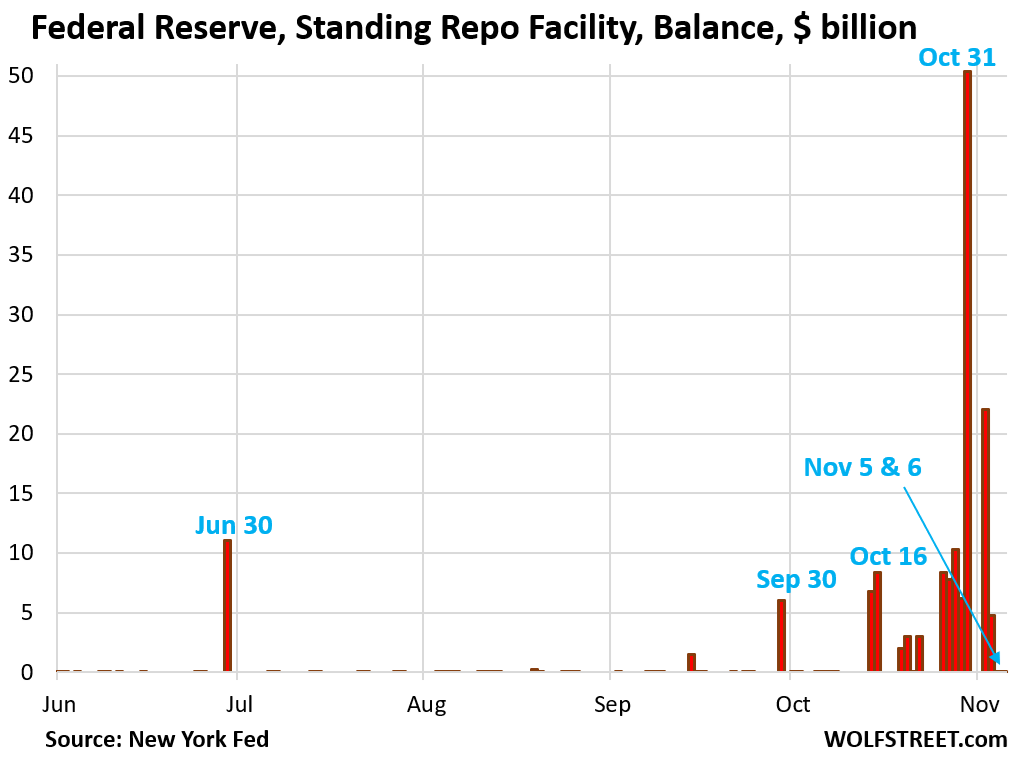

The SRF did its job. Month-end repo market turmoil, exacerbated by effects of the government shutdown, has settled down.

By Wolf Richter for WOLF STREET.

QT ends on December 1, but until then, it continues. The QT assets of Treasury securities and MBS declined by $20 billion combined in October, as per the Fed’s weekly balance sheet today. In addition Unamortized Premiums declined by $2 billion, for a total of $22 billion. The SRF had a zero balance, same as the month before, as the turmoil last week has settled down.

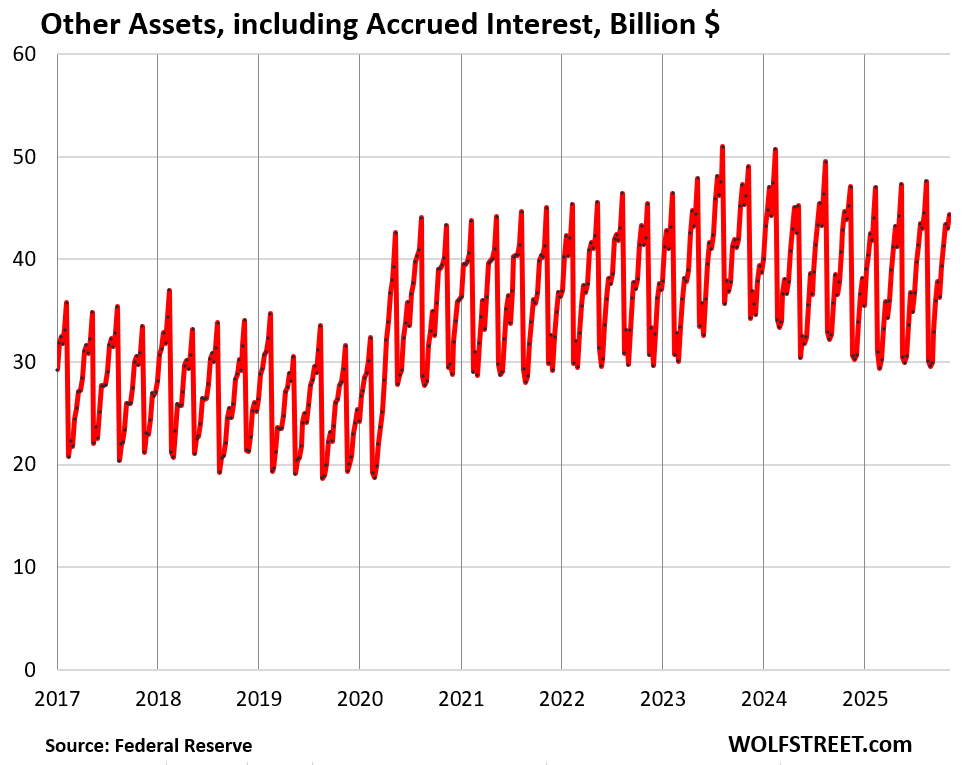

But “other assets,” rose by $8 billion due to accrued Interest, an accounting entry that has been flipping up and down on a quarterly cycle within the same range for five years (more in a moment).

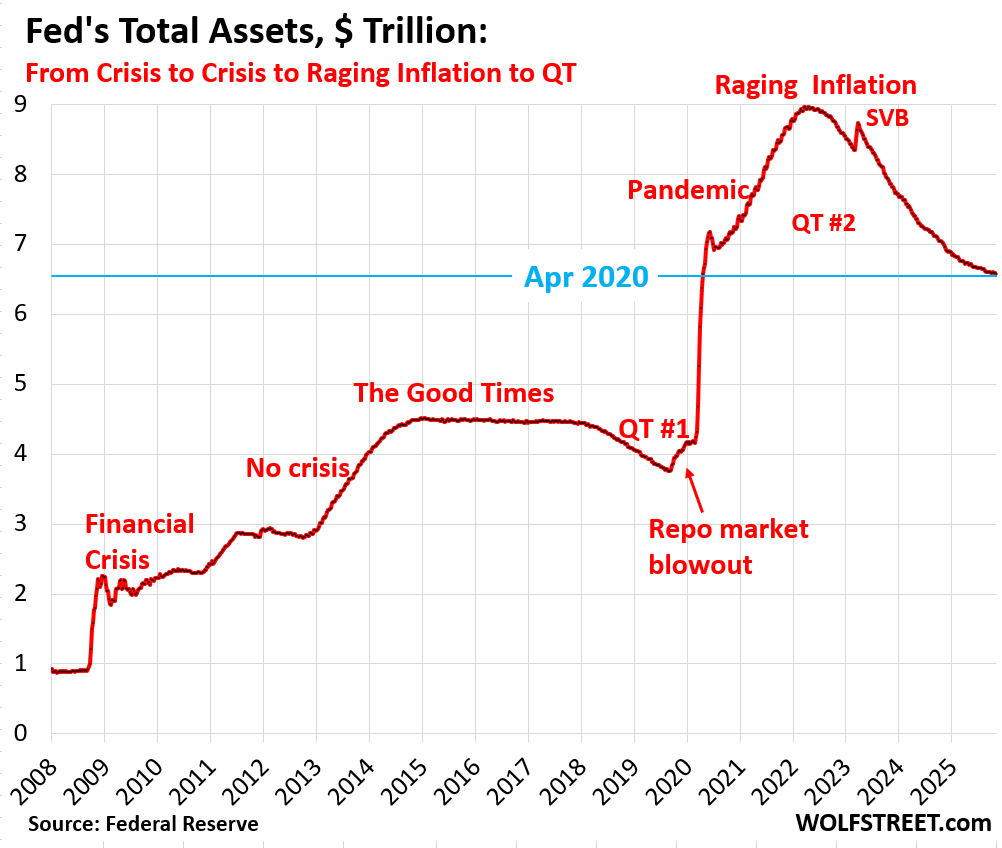

All combined, the total balance sheet declined by $14 billion (-$22 billion +$8 billion) to $6.57 trillion. Since the peak of its balance sheet in April 2022, the Fed’s QT has shed $2.39 trillion, or 26.7% of its total assets. Since the reduced pace of QT began in June 2025, the balance sheet has declined on average by $20 billion per month.

QT assets.

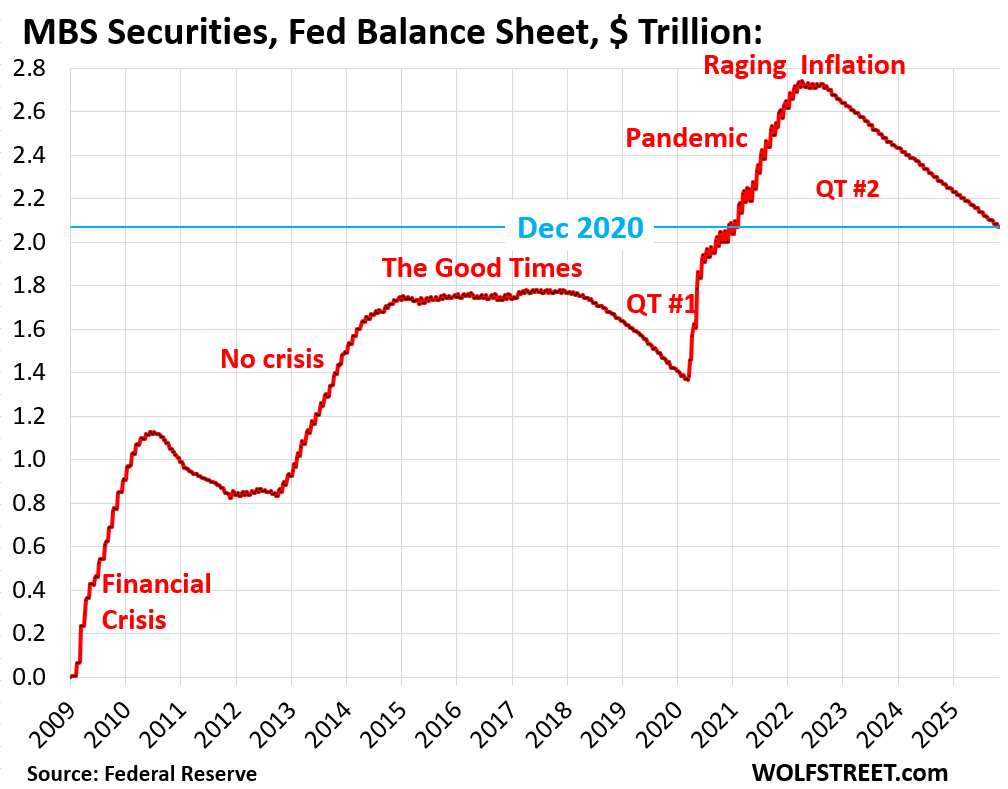

Mortgage-Backed Securities (MBS): -$16 billion in October, -$670 billion (-24%) from the peak, to $2.07 trillion, where they’d first been in December 2020.

Even after QT ends, MBS will continue to come off the balance sheet until they’re gone, and will be replaced by Treasury bills (mature in one year or less), according to the Fed’s plan outlined in the October meeting.

The Fed holds only “agency” MBS that are guaranteed by the government (issued by Fannie Mae, Freddie Mac, Ginnie Mae), where the taxpayer would eat the losses when borrowers default on mortgages.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and as mortgage payments are made. But sales of existing homes have plunged and mortgage refinancing has also plunged, and far fewer mortgages got paid off, and passthrough principal payments to MBS holders have slowed to a trickle.

As a result, ever since QT started, MBS have come off the Fed’s balance sheet at a pace that has been mostly in the range of $15-19 billion a month. The MBS runoff is no longer capped.

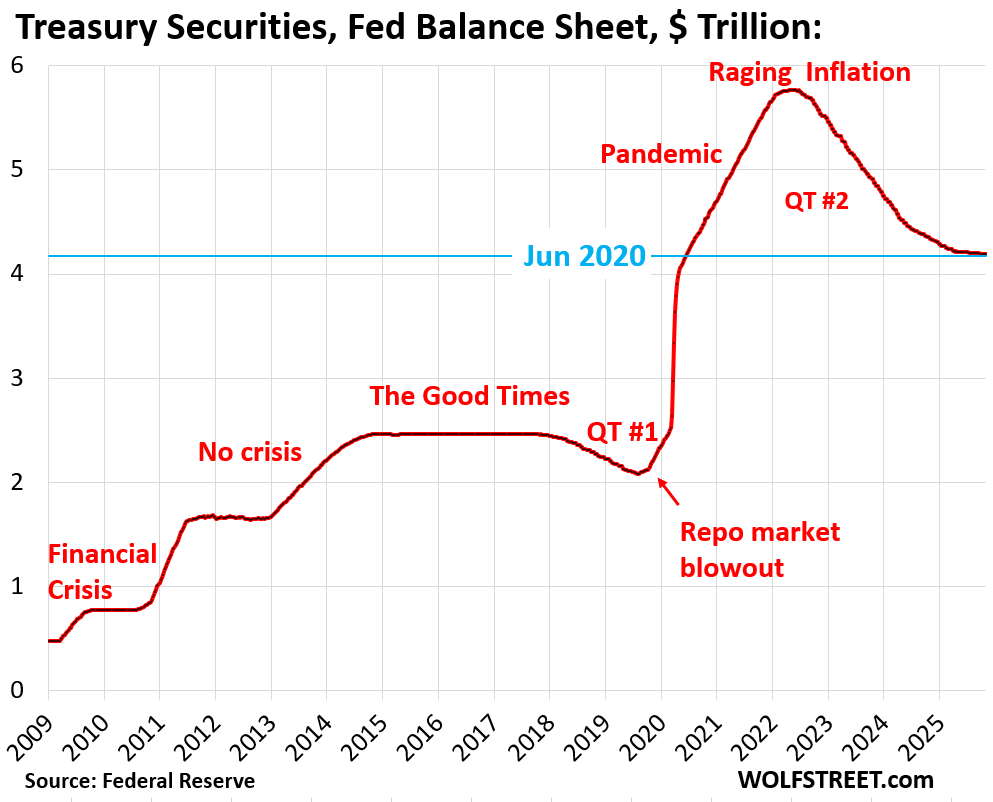

Treasury securities: -$4 billion in September, -$1.59 trillion (-27.4%) from the peak in June 2022, to $4.19 trillion.

The $4 billion decline was in line with the $5 billion a month pace of QT for Treasuries, the difference being the inflation protection the Fed earned on its holdings of Treasury Inflation Protected Securities (TIPS), which is added to the principal of the TIPS, instead of being paid in cash.

Bank liquidity facilities:

- Standing Repo Facility (SRF) had a zero balance again, after the turmoil last week in the repo market, see below.

- Central Bank Liquidity Swaps ($0.0 billion)

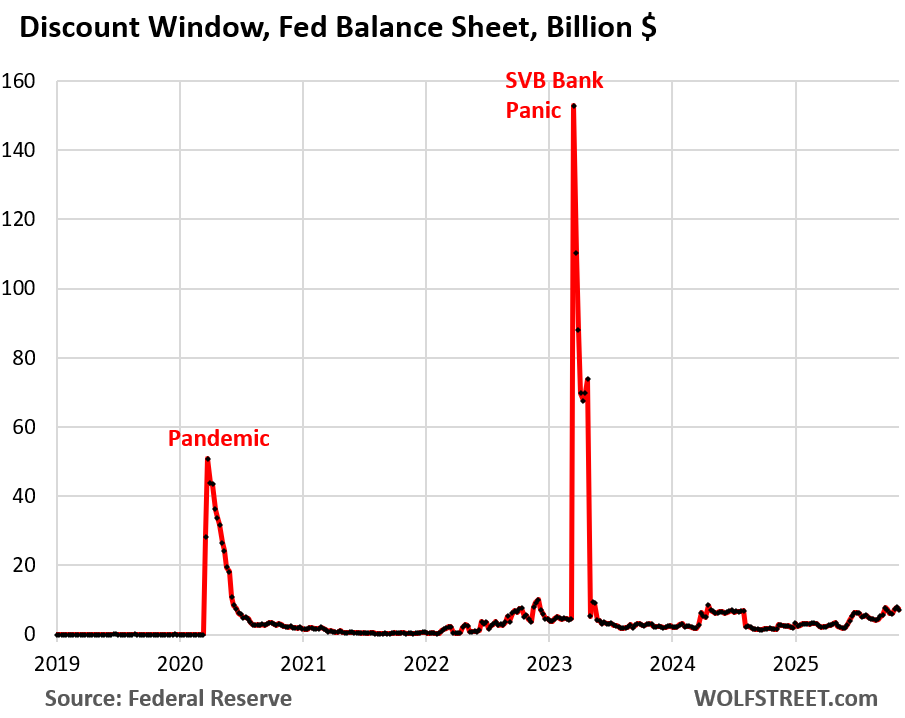

- Discount Window: no change, balance at $7.1 billion.

The SRF: The Fed has been exhorting its approved 40 or so counterparties, all of them big banks or broker-dealers, to use its new SRF, implemented in July 2021, to borrow at it via repos overnight and to lend to the repo market overnight when yields in the repo market rise above the rate at the SRF (4.0% currently).

Last week, there was turmoil in the repo market as month-end liquidity pressures met with the government shutdown, which caused the government’s checking account at the Fed, the TGA account, to swell with cash that wasn’t getting disbursed. And within a couple of weeks, this sucked $200 billion in liquidity out of reserves and money markets, and repo market yields began to spike.

Banks stepped in and borrowed at the SRF and lent to the repo market to profit from the spread. On October 31, Friday, the SRF balance spiked to $50 billion.

These are overnight repos that unwind the next business day, when the Fed gets its money back and the banks get their collateral back.

On Monday, that $50 billion got unwound, and banks took up a new $22 billion, which got unwound on Tuesday, and banks took up a new $5 billion in repos, which got unwound on Wednesday, and no repos were taken up on Wednesday and the balance was zero, as by then repo market rates had dropped well below the SRF rate, and today, the balance was also zero with no activity. And the repo market has calmed down. The SRF had done its job.

I discussed this in detail on Tuesday, including charts of the repo market rates, here.

The Discount Window: Essentially no change in October, at $7 billion. The Fed has been exhorting banks to use its Discount Window, or at least get set up to use it and pre-position collateral so that they can use it to help manage their daily liquidity needs.

What else…

“Unamortized premiums”: –$2 billion in October, to $228 billion.

With these regular accounting entries, the Fed writes off the premium over face value it had to pay for bonds during QE that had been issued earlier with higher coupon interest rates and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortizes that premium over the life of the bond.

“Other assets”: +$8 billion to $44 billion. This $8 billion consisted mostly of accrued interest from its bond holdings. The Fed set up the accrued interest as a receivable (an asset) in October that will be paid in November, at which point the Fed destroys that money, and the balance drops again.

This account fluctuates up and down on a quarterly cycle, on these interest accruals and interest receipts, but has stayed in the same range for five years. The peak of the current cycle will be next week, after which this account balance will plunge back to the bottom of the range, and this plunge will show up here on my monthly update on Thursday December 4.

The Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid, and so when it gets paid the interest, it destroys that money, and the balance sheet drops by that amount.

This account of “other assets” also includes “bank premises” and other accounts receivables and will always have a balance.

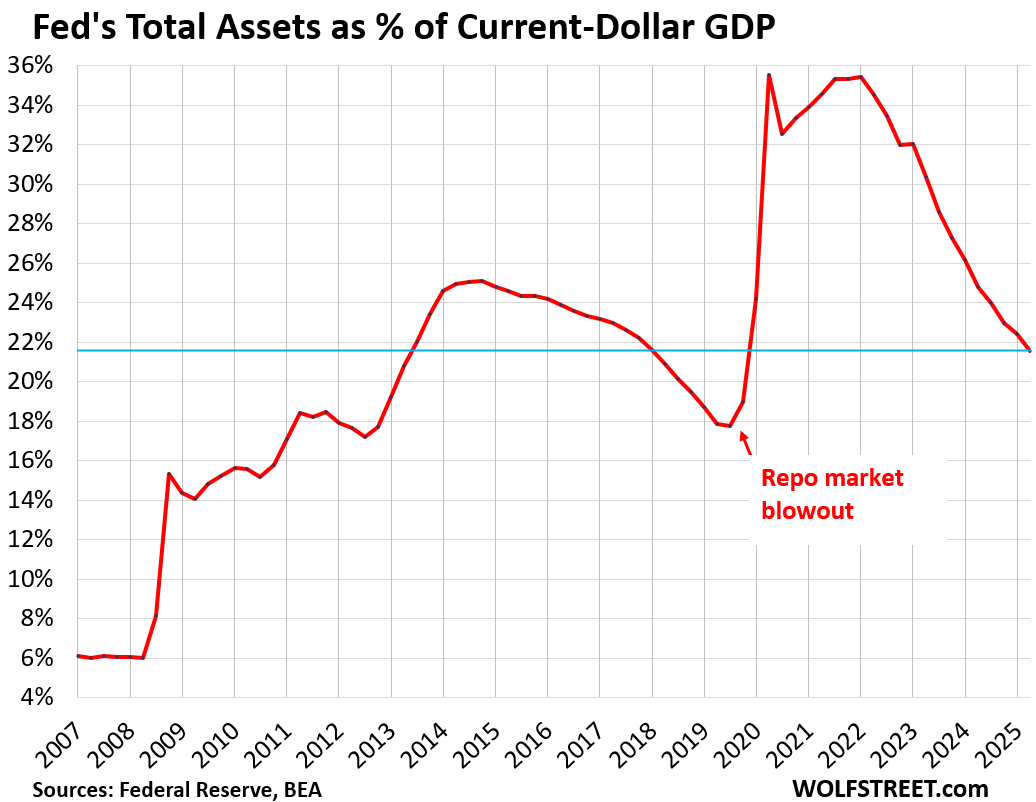

Fed’s balance sheet compared to GDP.

Powell talked about this when he discussed the end of QT during the press conference after the October FOMC meeting: the size of the balance sheet as a percent of GDP. He said it was one of the indications that it was time to end the asset roll-off.

The balance sheet has always grown as a function of currency in circulation and more broadly as a function of the size of the economy and the banking system.

But the structure of the balance sheet changed during the Financial Crisis because the Treasury Department’s checking account was moved from private sector banks to the Federal Reserve Bank of New York. This Treasury General Account at the Fed is a liability on the Fed’s balance sheet. As a balance sheet always balances, this means that assets had to grow with it over the years. There are currently $943 billion in the TGA. The addition of the TGA during the Financial Crisis has permanently increased the size of the balance sheet.

The Fed-assets-to-GDP ratio dropped to 21.6% in October, where it had first been in Q3 2013. If the Fed holds the balance sheet flat for some time after QT ends as the economy grows, this Fed-assets-to-GDP ratio will drop further (total assets divided by “current dollar” GDP).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks Wolf.

Will FED honor its commitment to freeze the balance sheet amount on Dec 1 is to be seen. e.g. Lets say when 10 B Treasury security matures. FED gets 2B in TIPs interest added to its TIP principal in same month. Will they re-invest 8 B or 10 B? This will truly tell us are they serious they are.

At this point, we should be watching what they do than what they say.

The FED balance sheet would accrue TIPS coupon interest & OID/CPI adjustments on a daily basis, so there wouldn’t be a “lump” of $2B in value on the TIPS maturity date as you suggest in your example.

You are missing the point. It is about freezing the number and staying honest to it.

Interest accrue on daily basis. But securities matures and get accounted twice in a month. FED definitely how much they made in those interest. That is there in Balance sheet. If you see Wolf’s explanation for this article,

“The $4 billion decline was in line with the $5 billion a month pace of QT for Treasuries, the difference being the inflation protection the Fed earned on its holdings of Treasury Inflation Protected Securities (TIPS), which is added to the principal of the TIPS, instead of being paid in cash.”

So if you see the Net result in balance sheet drop was 4 B and not 5 B. So question is when FED stop QT, will they invest 5B or 4 B in T-Bills?

Sandeep,

I think I finally understand your original question. The question you’re really asking is what happens to the inflation protection when the TIPS mature and the Fed gets paid this inflation protection.

The next TIPS issues mature in January 2026. One of them, for example, has $8.9 billion in par value and $5.7 billion in accumulated inflation protection. Throughout the life of the TIPS, the inflation protection is added to the principal value of the TIPS, and the total value of the TIPS grows, and when the TIPS mature, the original principal (“par value”) and the inflation protection get paid at the same time.

So the Fed will get paid $14.6 billion for this TIPS issue in January. But that $14.6 billion is already on the Fed’s balance sheet as an asset, and it’s split out so you can see it. When the Fed gets paid the $14.6 billion, the entire amount comes off the balance sheet, and the balance sheet drops by $14.6 billion. To keep the balance sheet flat, the Fed would have to replace the entire $14.6 billion.

What I’m talking about in the article is the inflation protection that the Fed accrues every week under the asset account “inflation compensation” (currently $112 billion). This inflation compensation is added to the principal value of the TIPS and causes the TIPS combined value on the balance sheet to increase with the rate of CPI inflation until the next TIPS matures and comes off the balance sheet.

So when the Fed accrues $1 billion in inflation protection for October, while also shedding $5 billion in Treasuries, the total Treasury roll-off amounts of $4 billion ($5 billion rolled off and $1 billion in inflation protection was accrued to the TIPS value).

Note that the Fed did NOT get paid the $1 billion in inflation protection in October. It was just an accounting accrual. It will get paid the accumulated and accrued inflation protection when the TIPS mature.

TIPS are complicated to explain. I hope this makes it a little clearer.

Thanks Wolf.

They won’t freeze it. They will be forced to start slowly growing it. Just don’t know how fast.

It can’t go any lower as a percent of GDP under the current fed framework.

My question is similar. Will the Fed sterilize the inflation compensation increases after December 1st? To keep SOMA holdings plus inflation compensation constant.

Inflation compensation is NOT paid. It’s just an accounting entry, an “accrual.” It’s not cash, it’s just an accounting number. There is nothing to sterilize. I thought I made that clear.

On the 10-year TIPS, I mentioned as example, the Fed gets PAID 10 years’ worth of inflation compensation all at once in January 2026 when the TIPS matures, and the Fed destroys that inflation compensation when it gets it, and it comes off the balance sheet (reversing the accrued inflation compensation entries going back 10 years for this security).

If in January, the Fed keeps the balance sheet flat, it will purchase securities in the amount it got paid for the entire TIPS, as I pointed out in my comment above.

One would think that the Fed officials would have anticipated the scenario that you proposed and had an off the shelf solution.

I don’t think the Fed, stuffed full of finest AI human candidates, has exhibited a decision making process that, where was one to flip a coin, they would actually have done better.

The worst thing one would think the Fed should do when inflation, like a forest fire is what they did. cut interest rates. As if the problem is liquidity while the asset prices increase while sales volume plumbs historic lows. We are already in a recession.

After exploding the Fed’s Balance sheet following the Great Financial Fraud (call it what it really was), Ben Bernanke sat before congress and flatly stated that the Fed “would never monetize the debt”. He went on to sate that the Fed’s actions were “temporary”.

It should be clear to everyone that the Fed is not independent nor are they interested in serving the best interests of the American people.

Risk (trust) is now being repriced globally and the math and demographics are what they are.

Hedge accordingly.

Sounds about right. If the Fed will not accept a recession, they have no choice but to run inflation hot for many years and maintain enough liquidity to keep the speculation going strong.

The only way I can think of to hedge against the future, redundant, is too diversify.

So much for “slower for longer”. This really disappoints me. Was this level their in their minds all along, or have things changed that much?

The Fed’s balance sheet is just over $6.5 trillion per the article.

Wolf’s estimate of the lowest possible level the balance sheet could be at was $5.8 trillion.

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

It’s reasonable for the Fed to think $6.5 trillion is the balance sheet target rather than $5.8 trillion given the recent liquidity issues in the repo market and the RRP hitting effectively zero.

I disagree. We shouldn’t base liquidity levels on a desire to support artificially inflated asset prices and leveraged speculators. If asset prices were reasonable in relation to incomes, how much liquidity would be needed? The answer is a lot less than what the Fed currently thinks we need.

Recessions are good when they follow periods of massive inflation and asset price run ups.

Cervantes

Yes, but that $5.8 trillion was based on figures of March 2024 (publication date of the article).

That $5.8 trillion would have to grow with the economy (such as nominal GDP, same as assets-to-GDP chart). At that growth rate (=7% Q1 2023 through Q2 2024), the balance sheet minimum would have to be $6.2 trillion now.

So I think the Fed got pretty close to the lowest possible level of its “ample reserves regime” with not much of a safety buffer, and we can see that in the repo market.

It could go lower by maybe $1 trillion if it reverts to a “scarce reserves regime.” So that might bring it to $5.2 trillion at the absolutest lowest so to speak.

Thanks for prodding me to do that math on this just now. I didn’t realize that the balance sheet was this close already to the minimum. Turns out, this requires an update on the article, which I will do soon.

If the securities holdings drop much more, the SRF will go up by that amount. This is what the Bank of England is doing. It’s running off its bond holdings by selling them outright (some of them don’t mature until 2070), and it lets its repo facility take the heat. The uptake at the repo facility now roughly matches the decline in its bond holdings. But what it does accomplish is it sheds the long-term bonds and replaces them with overnight assets (repos). I think that’s a good policy. The Fed might head that way eventually. That’s how it used to be.

Wolf, you might be interested in an interview with Joseph Wang (formerly a trader at the NY Fed) by Jack Farley at Monetary Matters that was released on Oct 29. Wang argues the Fed is moving in the direction of more short-term assets. IIRC he also argues that for the Fed to maintain control over short-term rates, given the size of the deficit and its funding at bill maturities, the Fed may have to start expanding its balance sheet sooner rather than later.

Wolf, can you explain briefly why you think Bank of England’s policy is better? Why replacing long term bonds with overnight repos makes sense?

It makes sense for many reasons.

One is that holding long-term bonds messes with the bond market. The BOE brackets short-term rates with its policy rates, so the repo activity has little or no impact on short-term rates, but it pulls the BOE away from the long-term market. You can see that in the 10-year yield in the UK, which is quite a bit higher than the US 10-year yield. Both countries are a fiscal mess.

Another reason is that from the central bank’s point of view — this is something the Fed has said many times in explaining why it will shift from long-term to short-term assets — it reduces the interest rate risk for the central bank. So that when it hikes rates, and long-term bond yields rise, that it doesn’t suddenly have $1 trillion in unrealized losses plus actual operating losses as the income from the long-term bonds that it bought when yields were low is lower than the interest it pays on its short-term liabilities.

And there are other reasons, including flexibility, as short-term securities and repos come off the balance sheet quickly and painlessly on their own; and can be added quickly and painlessly.

The Fed has been enabling bad behavior for years. Don’t believe me? Remember Ben “we will never monetize the debt” Bernanke? LOL! I would what would happen to a small business owner if the lied to congress…

Hedge accordingly.

“have things changed that much”

Look at the SRF.

Yeah, the FED caved in. They should just drain reserves and kill bitcoin.

Bingo. Bitcoin has been a very convenient “pressure release valve” that many wall street/financial sector big dogs adopted very early. Without Bitcoin where would that 2-3 trillion dollars have gone? My guess is that physical assets and energy would be considerably more expensive.

The Fed sure seemed to benefit quite a bit from the crashes and downturns in the economy. They went from having assets equaling 6% of GDP to 36% of GDP. US citizens got inflation and the bank apparatus grew and profits grew. On top of that, the risk isn’t centered at the Fed’s feet. It’s not bad work if you can get it.

What benefit do you think the Fed gets from having assets? Do you think they buy a mega yacht or a social media platform with it?

The employees get regular salaries that are relatively high but not higher than those same bankers could be making at a private business. Those salaries are completely unaffected by the Fed assets.

The way I see it, the Fed bought trillions in assets, made a fortune on arbitrage, and then sold the assets to shift risk to other entities in the economy. They booked their profits and didn’t have to absorb any default risk to do it.

I think it’s about control over the global economy, not yachts and clicks.

Wolf:

Good article. Board SRF working as you did predict.

It was good to see in the last chart of Fed assets as % of GDP back down to 21.6% and 2013 level. Can it go to pre 2008 level? Can you expand the chart back to 1960’s?

Now my harder question. When is “temporary liquidity “ which most people probably agree is a good thing to avoid fire sales……too temporary and actually a moral hazard which encourages over leverage in the marketplace? Prudent owners need to maintain a reasonable amount of liquidity in their portfolio. Community banks are no longer allowed to use access to borrowing lines as liquidity. Regulators want on balance sheet liquidity. Cash and short term treasuries that have broad and deep markets and transparent minutely electronic pricing and trading. So again , please explain FEDS role in providing temporary liquidity versus and opposed to making a market or influencing market prices?

The Fed has always provided “temporary liquidity” to banks when needed through the Discount Window and during my lifetime also through repos. Those are classic tools. What was new since WWII (when it was first used) was QE… non-temporary liquidity: buying long-term bonds that stick on the balance sheet for years and decades.

Yes, as you state in terms of on-balance sheet liquidity, banks in general, not just community banks, must have enough instant liquidity in form of cash and reserves to meet regulations. But they can briefly overdraw (for a few hours) their reserve accounts as payments don’t come in exactly at the same time as payments go out. And they can draw on the Discount Window and now the SRF for short-term liquidity if needed. The SRF is specifically designed for very short-term needs or wants as it’s for overnight repos only. The Discount Window provides loans with longer terms.

Temporary liquidity to solvent banks when needed allows the banking system to function and be stable. Banks are by definition unstable (borrowing short, lending long). But they’re considered an essential utility through which the money flows and on which the economy relies, hence heavy regulation and a central bank that can provide liquidity, for example when there is a run on the bank. As a rule, the Fed doesn’t provide liquidity to insolvent banks but lets them be taken over by the FDIC, see SVB et al. But in dealing with the Financial Crisis, just about all rules were broken.

Providing short-term liquidity to banks if needed, at a cost to the banks (currently 4% and against good collateral), is not a moral hazard. It’s a lot more expensive for banks to borrow that way than to borrow from depositors at almost no cost and without collateral.

Does m3 or cash in the economy fall with the shrinking of the Feds balance sheet. Also if the housing market gets bad enough will the fed pivot on buying MBS? I sure wouldn’t tie up $500k in a mortgage for 30yrs @ 6.5% with the inflation wild card.

Good question. Unfortunately, in the current system the devaluation of the currency is a mathematical certainty. It that or a hard default/debt jubilee.

With the Fed shut down we seem to be chugging along ok except for air traffic. Maybe we should shut down state and city and county govverments also. Put everyone on unemployment benifits. We would save a ton of money.

Shut down the Snap program and have the churches pass out Top Ramon. Over 8 billion a month goes out in the snap program. Wtf. 1 billion could hire 10.000 people for a year at $100.000.00. Wtf!

Maybe if we quit making penny’s we wouldn’t be so deep in debt.

That which cannot be sustained, won’t be. Risk (trust) is being repriced globally. Mathematically, his process is best captured by Earnest Hemingway’s quote on how to go broke; “Gradually and then suddenly”

Hedge accordingly.

Ahh yes, the prospect of not minting the penny (which costs more than the market value) has been with us for most of my life.

It’s a clear example of how our government DOESNT CARE about being effective or solvent.

Where was DOGE on this?

I don’t imagine the red tape to accomplish this is anything to be trifled with.

I have a feeling the US Mint is fairly well protected by bureaucracy.

motorcycle john

1. “Does m3 or cash in the economy fall with the shrinking of the Feds balance sheet.”

Yes. It tracked the Fed’s balance sheet and dropped with the Fed’s balance sheet. But the Federal Reserve discontinued it in 2006, though the St. Louis Fed continued collecting the data and published it until 2023, and you can see it there through Oct 2023. It’s considered not useful (just look at the Fed’s balance sheet).

2. “will the fed pivot on buying MBS?”

No, unless they sun doesn’t rise, and then it doesn’t matter. They hate MBS because they’re so unpredictable and such a mess to deal with because of the uneven flow of passthrough principal payments and the call feature.

My aeration is unless the Fed pivots on MBS the mortgage rates will rise and fall slightly within the ” normal rates ” of the pre ZIRP range guided by inflation so if the real estate market is to recover over time NET pricing will have to fall.

M3 is not money. It’s a confusion of money with liquid assets. It’s called the Gurley-Shaw thesis. But today’s Ph.Ds. don’t know a debit from a credit.

I was just thinking, the good thing about replacing them with short-term t-bills is that, if a new Fed decides to resume QT by letting bills run off, they won’t be waiting years like they would if they had long-term bonds on the balance sheet.

Hey Wolf, you had previously written that these MBS securities have an expected “lifetime” of about 7 years. Does the recent collapse in refinances affect that timeline? Or would it be expected to lengthen? The rate of decline in MBS holdings looks like they’ll be held for decades otherwise.

1. “The rate of decline in MBS holdings looks like they’ll be held for decades otherwise.”

At the current rate, it would take 10 years. QT has already been going on for over 3 years. So 10 years isn’t all that long.

But the Fed has been considering selling MBS outright and replacing them with T-bills to speed up the process. So it might take another five years?

2. “you had previously written that these MBS securities have an expected “lifetime” of about 7 years.”

That’s not what I said. What I said was that the typical 30-year mortgage gets paid off on average in 7 years (via refi or sale of the home).

So yes, the average life of a 30-year mortgage likely lengthened a little since the 3% mortgage rates. But people still move and sell homes, and refis are still going on, but at a slower rate.

And this does impact MBS in that it lowers the passthrough principal payments and pushes out when the MBS is called. Which is why the roll-off has been so slow. But that’s already included in the figures, that’s what we’ve been seeing for three years. It’s not new.

1. 10 years out isn’t so bad. It was 13 years from 0 to the peak in 2022. 13 years total to get back to zero isn’t bad. Even faster if they sell outright, as you said.

2. Ah, yes. I was thinking about the time until the MBS would be called. I expected that to have been pushed out, but conflated the individual mortgages with the MBS call.

By what nebulous criterion does the FED stop QT and restart asset purchases? What’s the definition of abundant vs. ample?

The SRF is doing a good job of redistributing reserve balances, but how evenly are precautionary reserves actually held in the system?

The only type of bank asset that the FED can constantly monitor, and absolutely control are interbank demand deposits held at the reserve banks (like the ECB). The FED should target reserves, not reserve bank credit. Monetarism has never been tried.

“By what nebulous criterion does the FED stop QT and restart asset purchases?”

1. It hasn’t started the asset purchases yet, and when it starts, it would only keep the balance sheet growing with the economy (demand on its liabilities), which is always how the Fed has done it from day one 100 years before QE. But QE was different, it grew the balance sheet far faster than the economy, which started in 2009.

2. It’s not nebulous. It’s math.

Cash in circulation = $2.5 trillion

TGA = $1 trillion

Combined: $3.5 trillion.

With zero reserves in the banking system (impossible, see below), the minimum is now $3.5 trillion

But zero reserves are impossible, and never were possible. Reserves are the checking accounts of banks at the Fed. They’re at the core of the US payments system. Your mortgage payment goes from your bank through the reserve account of your bank to the reserve account of the other bank. Any payment, including for buying/selling stocks and entire companies, go through the reserve accounts, and just that daily flow of cash through the reserve accounts shows up as reserve balances at the end of the day, and it’s big. Maybe with just the transaction amounts, reserves might amount, just guessing, to maybe $2 trillion, just the daily transactions moving through the accounts. That would bring the balance sheet down to $5.5 trillion. That would leave absolute zero buffer in the payments system.

Also note what I posted here a minute ago in reply to Cervantes who said:

Wolf’s estimate of the lowest possible level the balance sheet could be at was $5.8 trillion.

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

To which I replied in part:

Yes, but that $5.8 trillion was based on figures of March 2024 (publication date of the article).

So I think the Fed got pretty close to the lowest possible level of its “ample reserves regime” with not much of a safety buffer, and we can see that in the repo market.

It could go lower by maybe $1 trillion if it reverts to a “scarce reserves regime.” So that might bring it to $5.2 trillion at the absolutest lowest so to speak.

Thanks for prodding me to do that math on this just now. I didn’t realize that the balance sheet was this close already to the minimum. Turns out, this requires an update on the article, which I will do soon.

As Dr. Milton Friedman posited; From Carol A. Ledenham’s Hoover Institution archives: “I would make reserve requirements the same for time and demand deposits”. Dec. 16, 1959.

I was barely alive back then, LOL

Wolf,

Did you see the news that New York Fed Bank President John Williams has said today that QE will resume soon?

Seems like the Fed is going all-in with rate cuts and now QE when all the state level initial claims reported today show zero downturn, and GDPnow is guessing we’re at 4.0% GDP growth. And all this with inflation rising.

I might short TLT and ZROZ because if this planned recession doesn’t occur, there’s going to be very high inflation next year.

Powell said that too during the press conference.

What they’re saying is to let the balance sheet grow with the economy rather than keeping it flat. If they keep it flat, reserves will continue to drop, and they’re already at the “ample” as we can tell in the repo market. They’re NOT talking about QE, and people who say that’s QE are nuts.

That Fed’s balance sheet, even before 2008, has ALWAYS grown with the economy (specifically current in circulation) except during QT.

Presidential plunge protection team chairman John Williams of the New York Federal reserve comes out with “we may have to expand our balance sheet to provide ample liquidity” before the market opens, the buying didn’t come until later in the day. Williams is definitely aware of the charts and the programming of the master algorithm for Wall Street. That is his job, keep the bubble intact. We have to wait until next week to get confirmation that this blowup, melt down is happening or delayed. Have a great weekend!

Powell said that too during the press conference.

What they’re saying is to let the balance sheet grow with the economy rather than keeping it flat. If they keep it flat, reserves will continue to drop, and they’re already at the “ample” as we can tell in the repo market. They’re NOT talking about QE, and people who say that’s QE are nuts.

That Fed’s balance sheet, even before 2008, has ALWAYS grown with the economy except during QT.

Wolf…..how do you know all this shit? I couldn’t understand most of what you said, but I know this….If you print trillions in new money in a little more than a year, there’s going to be trouble. And it’s a really bad precedent….which is why America has been off the rails for years.

Would there be value in showing a graph of percentage of GDP, except it was “normalized” without the TGA?

No, it doesn’t make sense for two reasons:

1. The chart shows assets as a percent of GDP, and the TGA is a liability, not an asset.

2. The TGA has been “normal” since 2009. That’s just how it is, and there is nothing to “normalize.”

Wolf-

Could you elaborate (or have you already) the reasons and pro’s/con’s of the c. 2009 shift of TGA to Fed balance sheet?

I can’t help but think that there was a reason that the Treasury Department’s checkbook was at one time separated from the nation’s money management function.

Thanks

I don’t know if they ever gave a reason, but it was obvious: The government didn’t want its checking account stuck in a bank that might collapse during the Financial Crisis or the next one. The NY Fed cannot collapse. So the funds are safe there, and the government can continue to operate even if some banks fail.

All funds get disbursed through that checking account, even bank bailout funds, interest payments, and bond redemptions. And when that checking account is in a bank that itself collapses, the government has no way of bailing out banks, this bank, or anything else, and cannot even pay interest to bondholders or redeem maturing bonds, or make any other government payments. It was a crazy risky situation to have this account at private banks, and moving it to the Fed was the right thing to do.

like the graph of the linear decline in real GDP growth since 1980 or so. From 5 pct back then to an anemic current 1.2 pct made possible by issuing debt. Ensuring that the sovereign will issue currency to prevent the decline in asset prices.

Because that would be deflationary.

Like now.

LOL. Real GDP: growth:

https://wolfstreet.com/2025/09/25/what-slowdown-q2-gdp-growth-revised-up-to-the-hot-zone-of-3-8-on-stronger-consumer-spending-private-fixed-investment/

As long as it is profitable for borrowers to borrow and commercial banks to lend, money creation is not self regulatory. This observation would be valid even though the Fed did not use interest rates as a guide to open market operations.

By using interest rates as the monetary transmission mechanism, the Fed is actually pursuing a policy of automatic accommodation. That is, additional & costless excess reserves are made available to the banking system whenever the bankers and their customers see an advantage in expanding loans.

The member banks, lacking excess reserves (clearing balances), will just bid up the SRF rates to the top of the bracket thus triggering open market purchases, free-gratis bank reserves, more money creation, larger monetary flows, higher rates of inflation – and higher interest rates, more open market purchases, etc.

Does it make sense to put reserves at a level that supports rampant speculation, at a time when asset prices are at all time highs, and when GDP is being artificially elevated by 6-8% deficit spending?

I think reserves should be set to accommodate reasonable growth, not bubbles. Maybe a little pressure in the repo market is not a bad thing. Maybe it’s just the invisible hand trying to do it’s work.