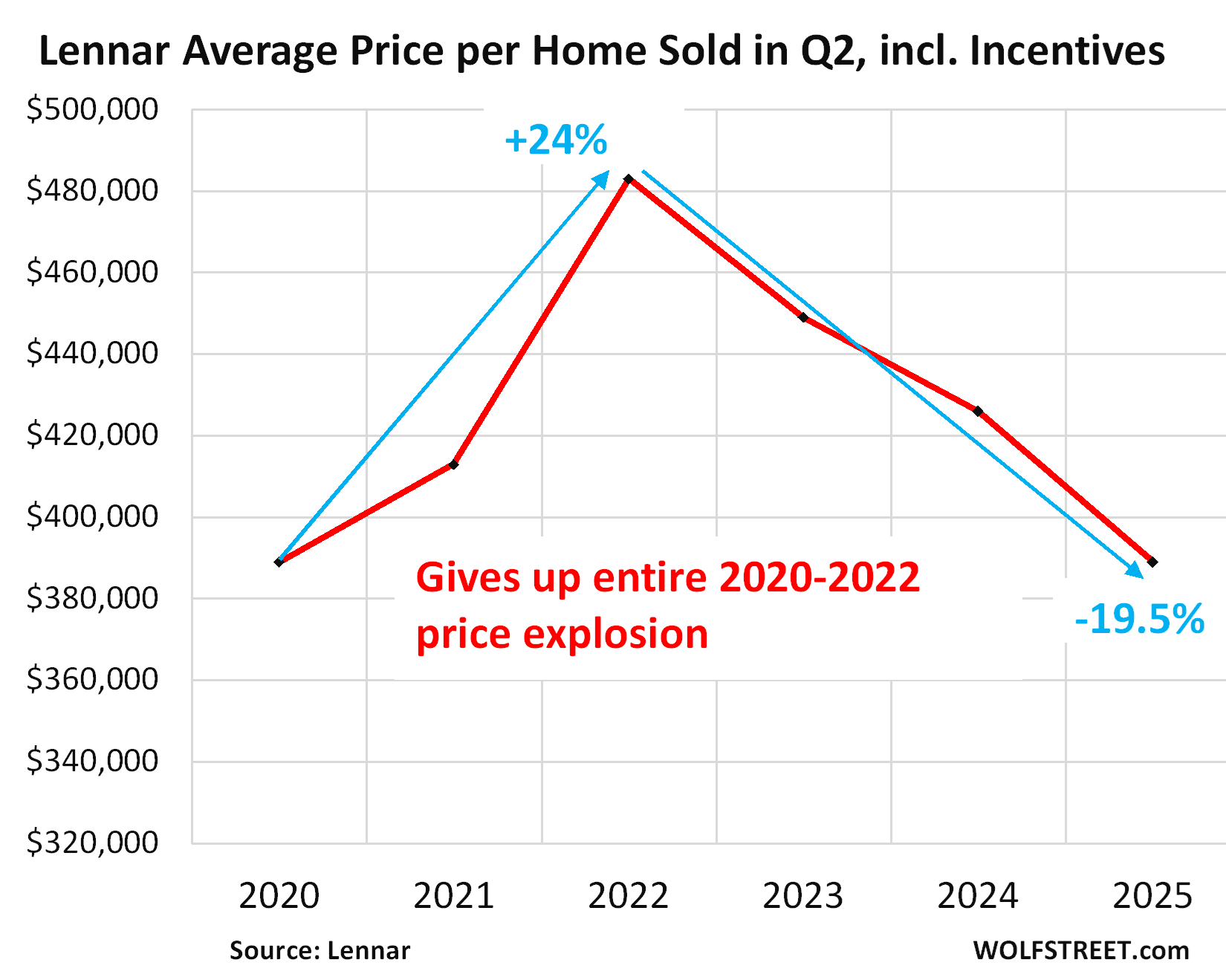

Homebuilder Lennar’s average selling price has dropped by 19.5% from the peak three years ago.

By Wolf Richter for WOLF STREET.

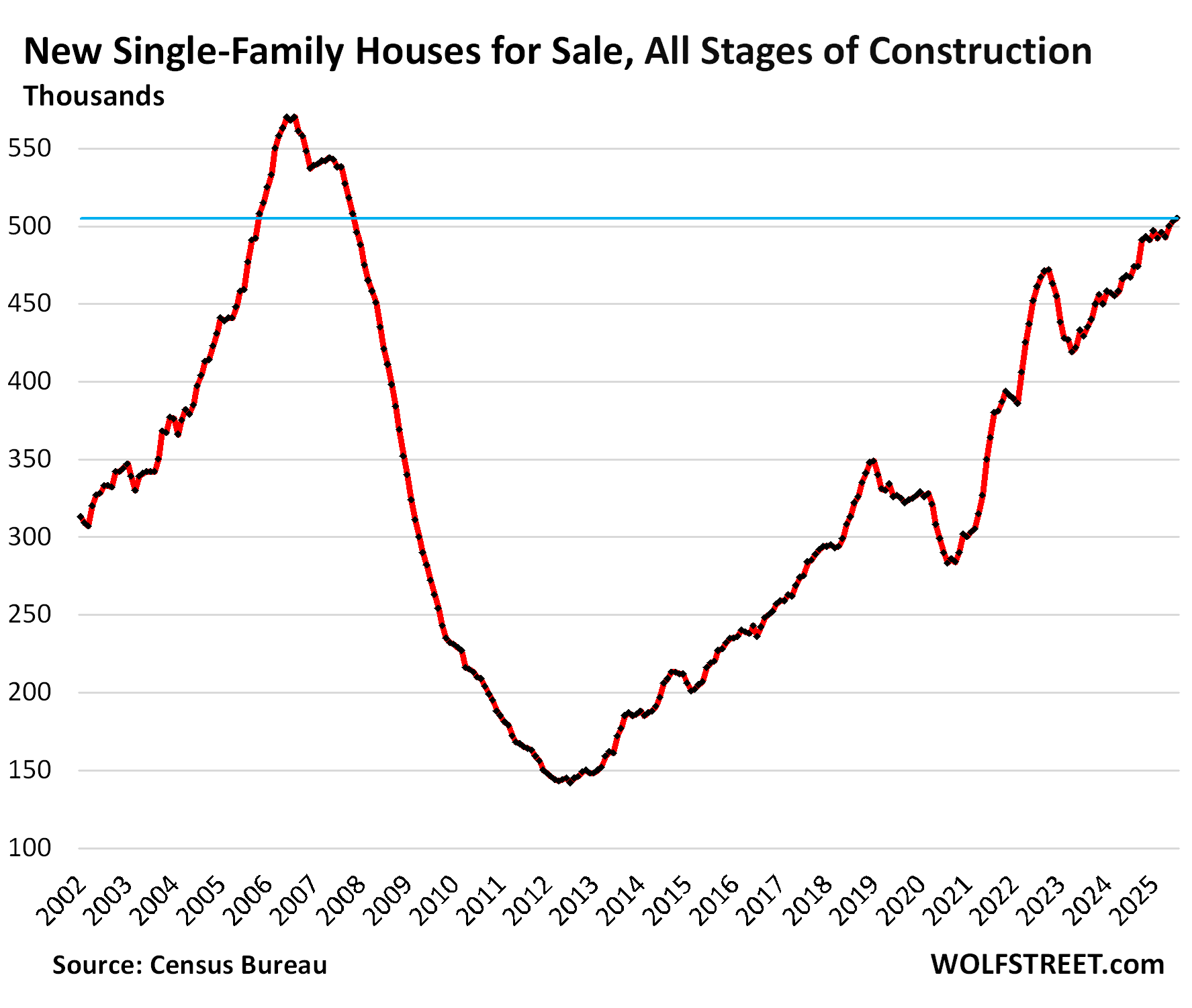

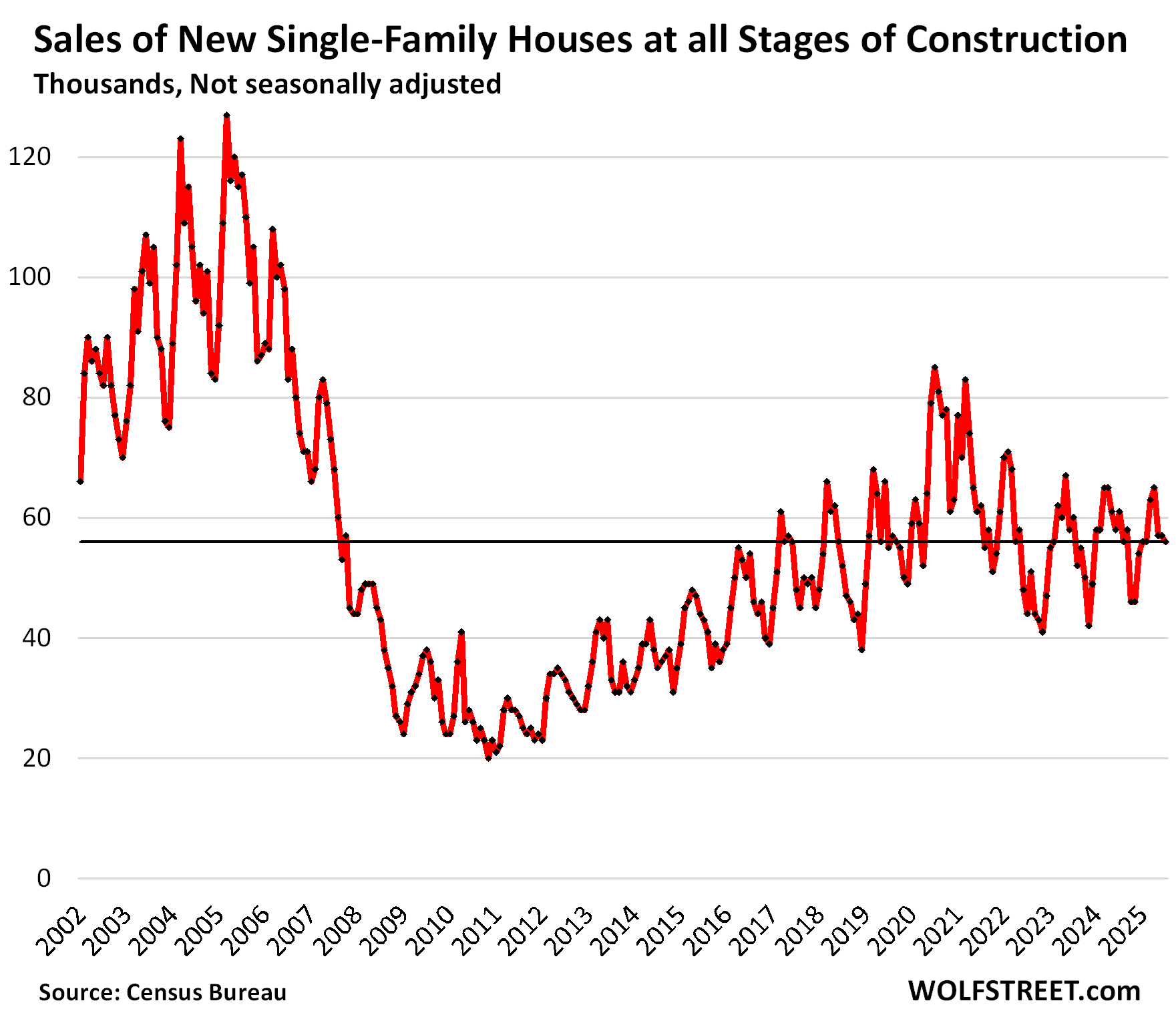

New single-family homes for sale at all stages of construction rose to 505,000 homes in July, the highest since October 2007. But back then during the Housing Bust, inventories were on the way down, as homebuilders were trying to stay alive by cutting back construction.

Compared to a year ago, inventories were up by 8.1%, compared to July 2019, inventories were up by 54%.

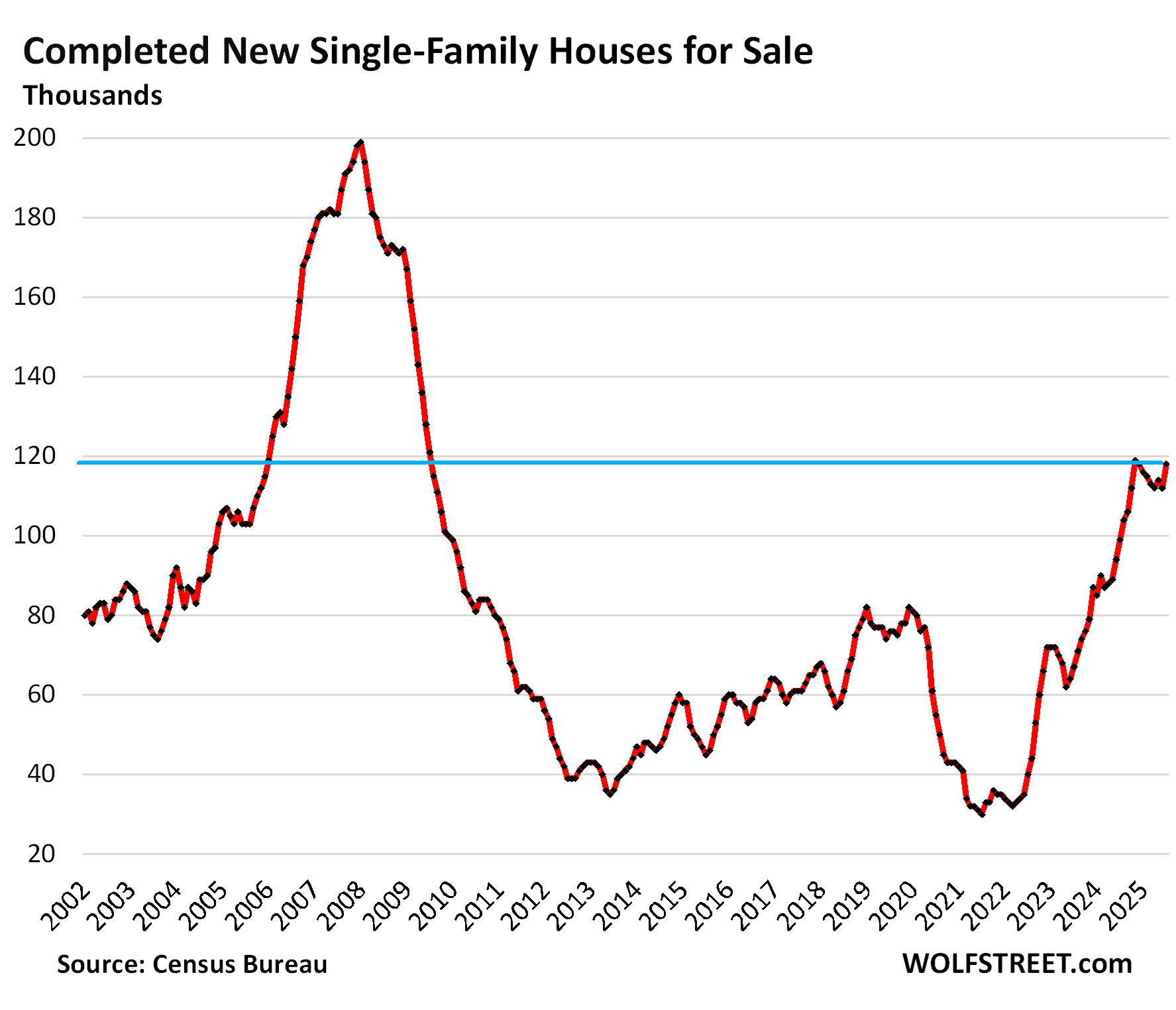

New completed single-family homes for sale jumped to 118,000 homes in July, up by 55% from July 2019, just behind November 2024.

Inventory for sale of these “spec homes” has been in this range since October 2024.

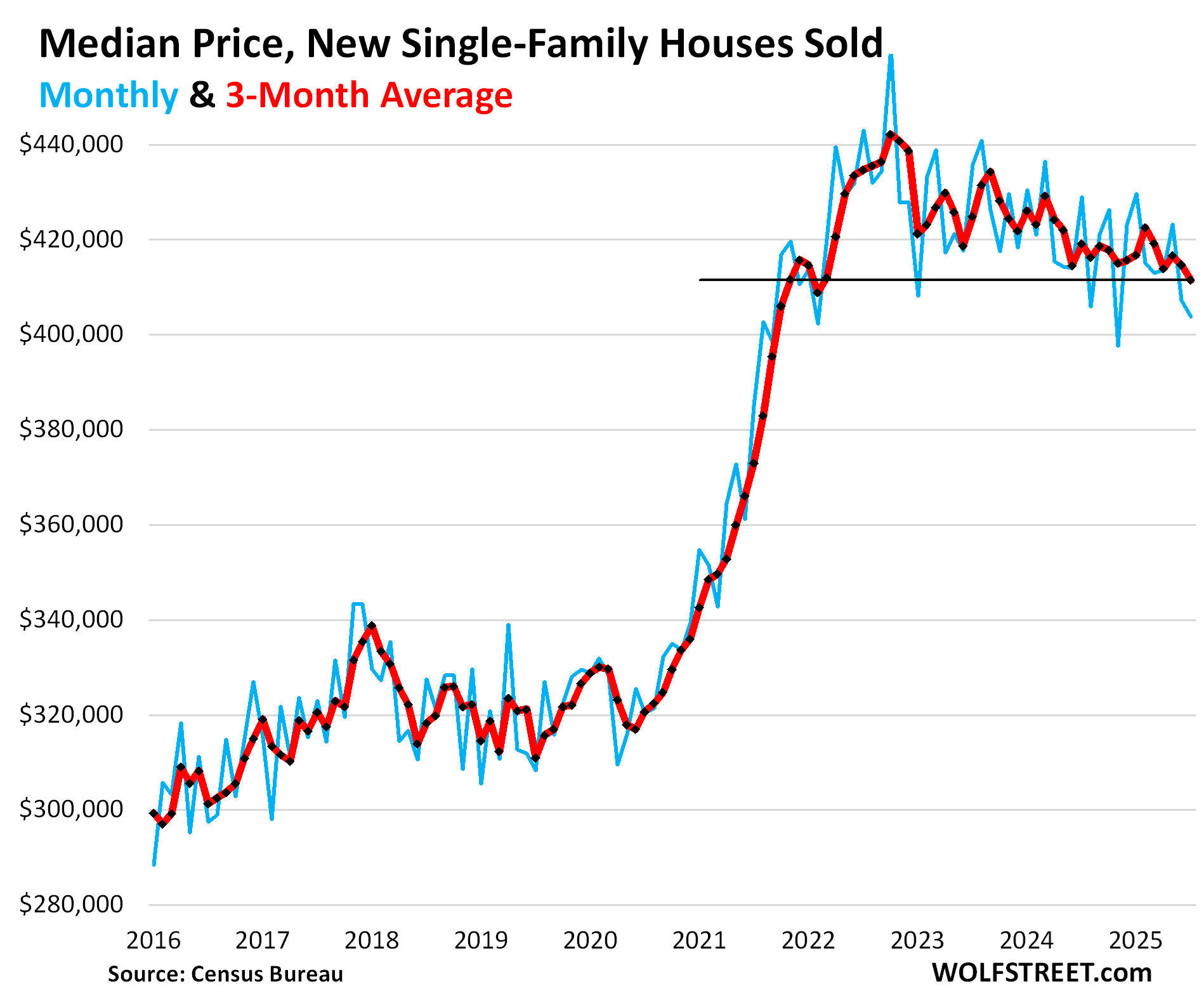

Prices fell, even without including incentives.

The median contract price dropped by 5.9% year-over-year to $403,800 in July (blue in the chart below).

The three-month average, which irons out some of the month-to-month squiggles, dropped to $411,400 (red), down by 1.8% year-over-year and by 5.9% from the peak in late 2022. This price level was first seen in November 2021.

But the Census Bureau tracks sales prices of new houses by the prices written into purchase contracts that buyers signed. These contract prices do not include the costs of mortgage-rate buydowns and some other incentives. With the costs of the buydowns and incentives included, home prices fell far further – we know that from builders quarterly financial reports (for Lennar and D.R. Horton, see below).

So these contract prices overstate the effective sales prices and understate the effective price drops. And still, they’ve been coming down, even with massive incentive costs not included.

The price explosion during the pandemic, when people were willing to pay whatever, had led to a explosion of profit margins at homebuilders. Those profit margins are now getting trimmed back, and net profits have fallen.

And including incentives…

Homebuilders have been trying to stimulate demand with big incentives and costly mortgage-rate buydowns.

Lennar disclosed that its incentive spending jumped to 13.3% of revenues in Q2, “primarily” due to mortgage-rate buydowns, the highest incentive spending rate since 2009.

Lennar’s average sales price dropped to $389,000, down by 19.5% from the peak in Q2 2022 and is back where it had been in Q2 2020, having given up the entire 2020-2022 price explosion. Average selling price includes the incentives.

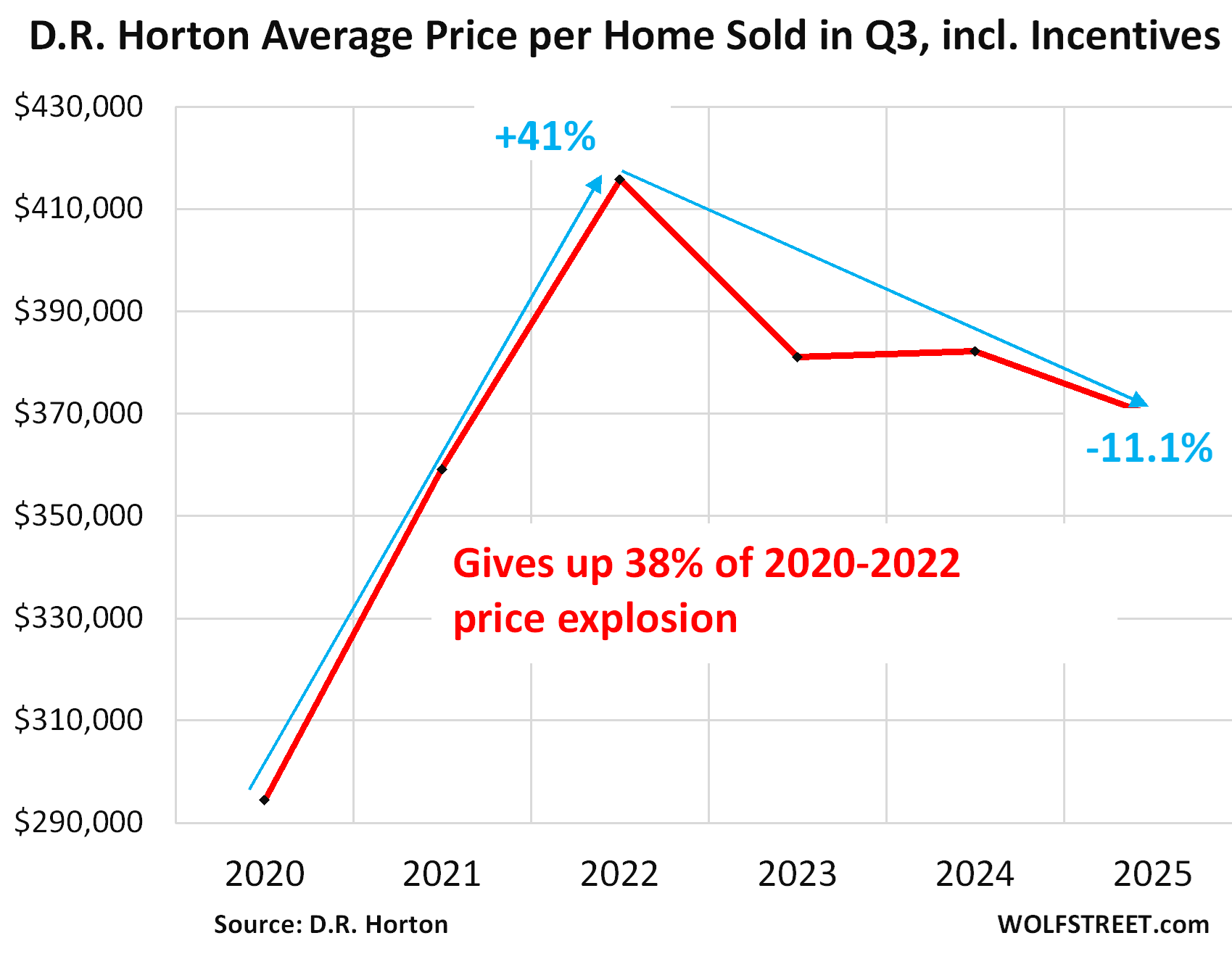

D.R. Horton reported that the average selling price per home sold declined by 3.3% year-over-year, and by 11.1% from the peak in its fiscal Q3 2022, to $369,600 in the quarter ended June 30. Average selling price includes the incentives:

Sales have hung in there, thanks to the deals.

Sales of new homes fell by 8.2% year-over-year to 56,000 contracts signed in July, not seasonally adjusted, and were down by 1.8% from July 2019 – still in a mediocre to decent range, rather than in the deep-plunge to rock-bottom range of existing homes.

So efforts by homebuilders to stimulate demand via lower prices, mortgage-rate buydowns, and incentives have worked to some extent to prevent the kind of plunge in demand for existing homes. See: Sales of Existing Single-Family Homes Crushed, Supply Highest since 2016. Condo Sales Near Low in the Data, Supply Highest since Housing Bust. Prices Begin to Bend

Homebuilders have to maintain their businesses, and they have to find the mix of price points and incentives at which they can sell, and they sacrifice some of their fat profits to get there. They cannot decide to just outwait this market.

Inventory for sale by region.

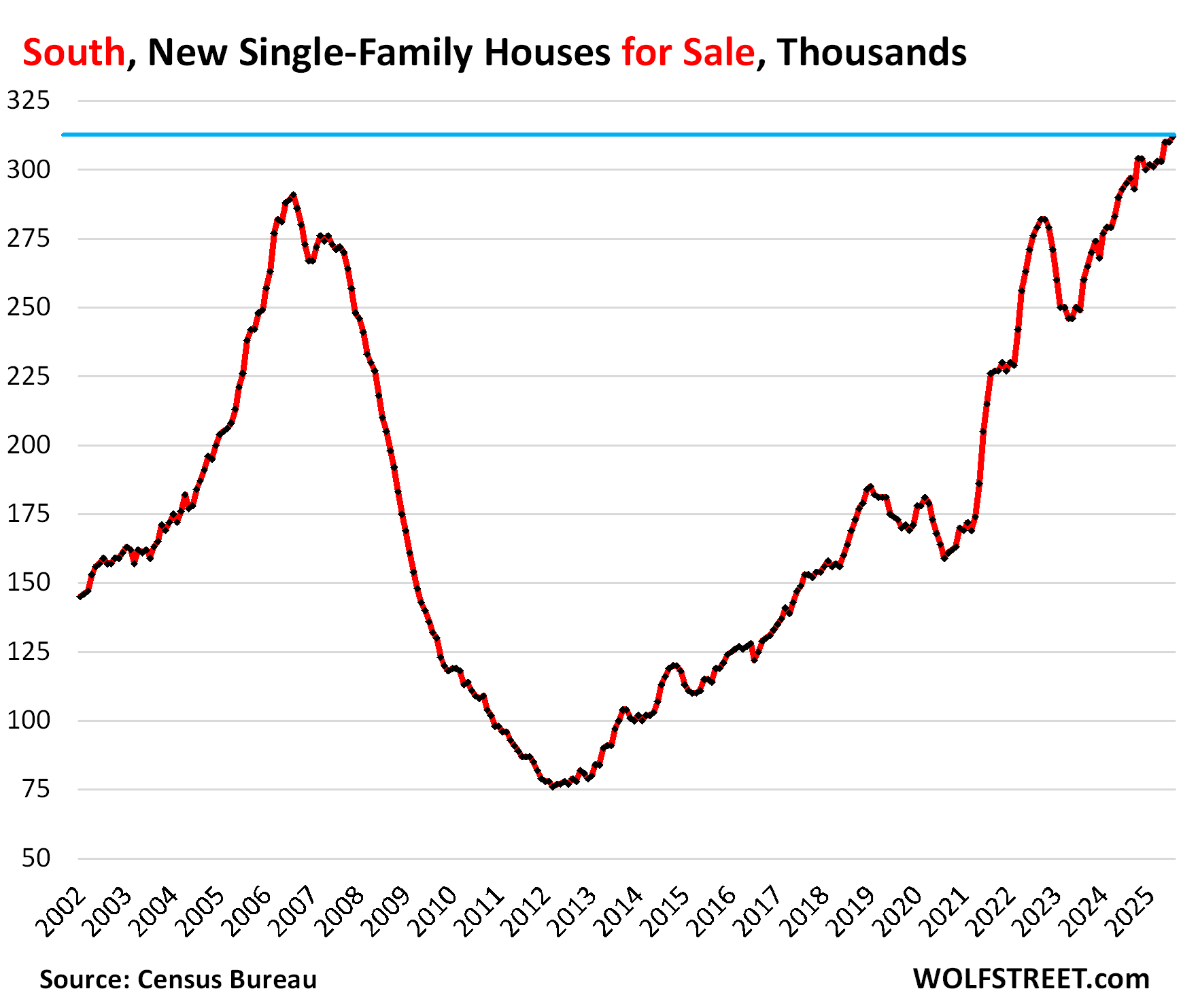

In the South, inventories of new houses for sale spiked to a record of 312,000 in July, up by 79% from July 2019. Inventory has been above the Housing Bust peak for over a year.

The Census region, which is dominated by the mega-housing markets of Texas and Florida, accounted for 62% of total US new-home inventory, and for 57% of total US new-home sales (a map of the four Census regions is below the article at the top of the comments).

Sales dropped by 6% year-over-year to 32,000 new homes, and also by 6% from July 2019. The incentives that homebuilders are piling onto this market are keeping sales at decent levels.

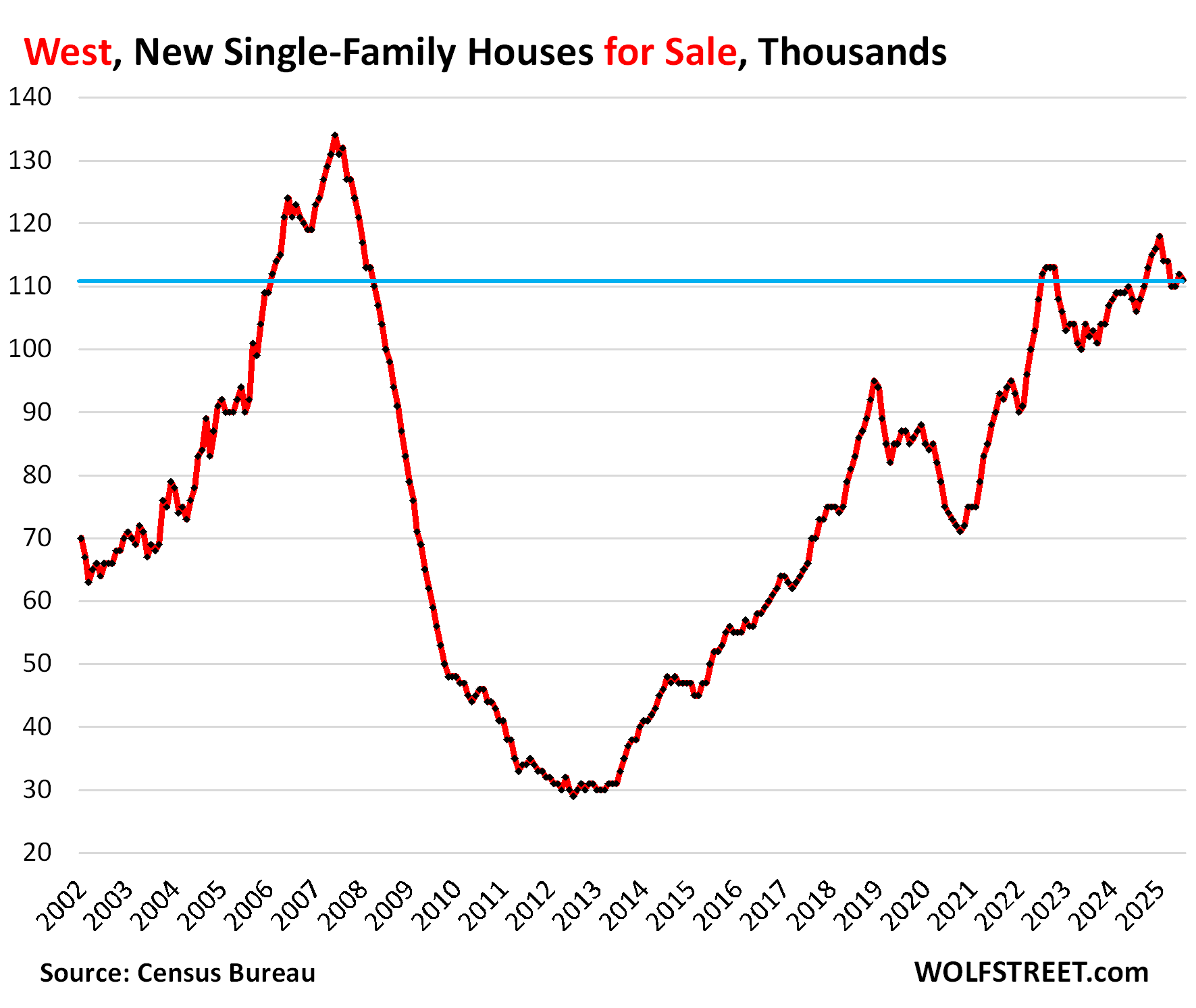

In the West, inventories of new homes for sale have declined somewhat since the end of 2024, to 111,000, but were still up 4.7% year-over-year, up by 28% from July 2019.

Sales in the West dropped by 19% year-over-year to 13,000 new homes but were level with July 2019. Here too, lower price points and incentives have helped keeping sales at mediocre to decent levels.

The West, dominated by California, accounted for 22% of the total US inventory and for 23% of total US sales.

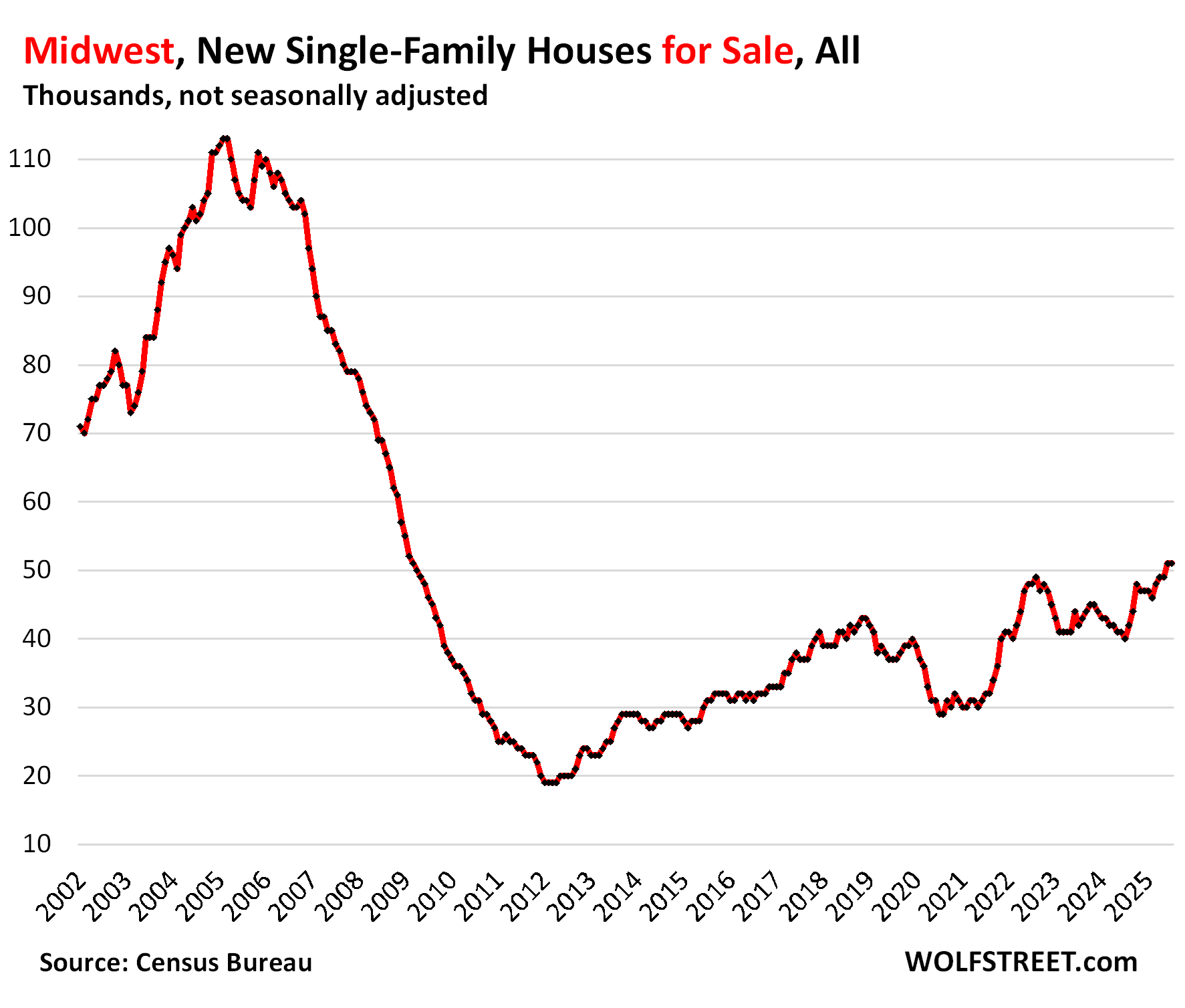

In the Midwest, inventories of new homes for sale in July jumped by 27.5% year-over-year and by 38% from July 2019 to 51,000 new homes, the highest since February 2009:

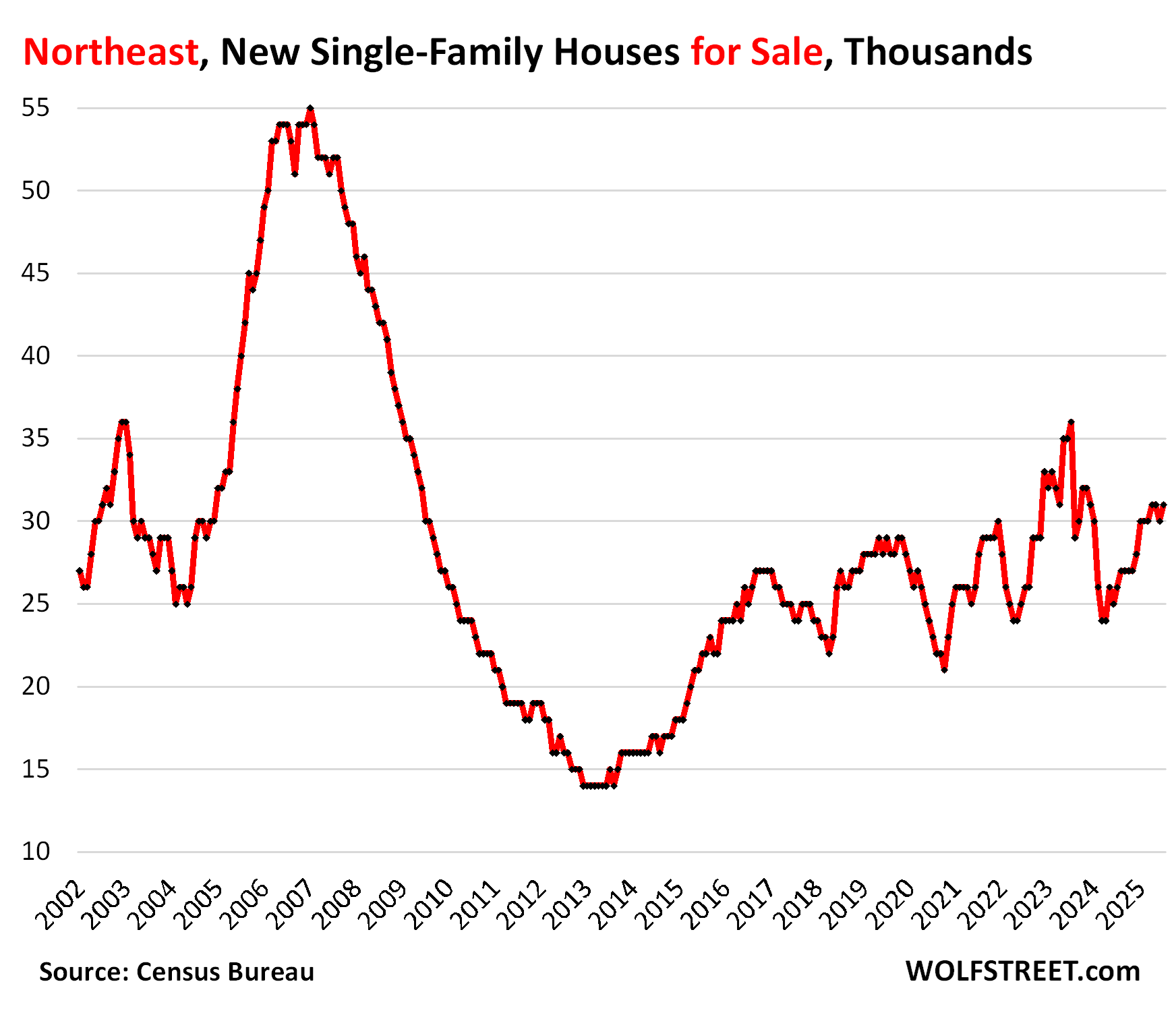

In the Northeast, inventory jumped by 19% year-over-year and by 7% from July 2019, to 31,000 new homes.

The Northeast is a relatively small area with big densely populated cities where multifamily housing (condos and apartments) is a far bigger part of new construction than single-family housing.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

A more detailed evaluation would be welcomed.

All you have to do is read my housing articles. There are lots of them. You can find them here:

https://wolfstreet.com/category/all/housing/

In time, people will realize that this is the housing bubble of all housing bubbles. The mother of all bubbles. The Great Financial Abomination. Thr bubble to end all bubbles. TEOTWAWKI in housing.

Nah this time is different and people in many areas will also day their area will be different and immune to correction or crash as well.. Time will tell

If inflation really takes off then many of us holding low interest loans might just ride it out on the sidelines. If money moves out of stocks, I suspect a good portion might just head into real estate. Never underestimate the power of property to bubble higher.

I dont think so.

Extreme un affordability with job insecurity would paly a major role in prices going down and down.

Lot of tech companies are paying off in thousands despite their earnings being very good and stocks at ath.

Inflation fixes many purchase mistakes.

Also, every month that passes is another month with slightly fewer 3% mortgages and slightly more 7% mortgages.

Eventually the “I can’t sell because my cheap mortgage is too valuable” group will only be a trivial factor in the real estate market.

Waiono, money doesn’t “move out” of stocks and “into” bonds, or real estate. Every seller has a buyer. So all the money “stays in” on any transaction. It might not be your money but it’ll be someone’s!

What most people also overlook is that the value of all shares rises and falls with the price of just the most recent shares traded. If 100 shares trade down 10% as a result of adverse news, EVERY share is down 10%. That shareholder “wealth” doesn’t “go” anywhere, it is vaporized.

Also, human nature is such that people are much more reluctant to buy things whose prices are clearly declining.

Now that housing prices have started falling, buyers will hold back waiting for better value, and sellers will get more aggressive to avoid losing their gains.

Prices will continue to fall until they better reflect fundamental values rather than anticipated speculative growth.

None of that paper wealth will be “going into” anything else, it will be obliterated.

The headwinds on real estate are going to accelerate. Costs of building materials will make it less appealing to just update vs move, same with labor costs for construction.

The job destruction from AI still hasn’t really hit yet, but it’s coming and everyone knows it’s coming for the generation of people who sit behind a computer all day. Young people have already gotten the memo and are rediscovering the trades, but it will take quite a few years to rebuild the losses from decades of pushing kids into college vs HVAC school.

Factor in the deportations and drastic reduction in number of people legally moving to the US, lower birth rates, enthusiasm for Airbnb dropping off, etc..

Housing has always been a relatively safe bet, but no one really knows how the AI bubble and housing bubble are going to play out, so it’s all speculation at the end of the day.

If monetary inflation really takes off in earnest the value of assets will still go down relative to simple things like labor and food because no private entity will be issuing credit denominated in dollars, especially not on 30 year terms. Assets’ nominal prices are tied to predictable returns on investment and inflation makes it anything but predictable. Unless you can turn a profit in a predictable time frame the investment isn’t made and there are better inflation hedges than real estate.

Bagehot’s Ghost “Waiono, money doesn’t ‘move out’ of stocks and ‘into’ bonds, or real estate. Every seller has a buyer. So all the money ‘stays in’ on any transaction. It might not be your money but it’ll be someone’s!”

When in doubt, check your assumptions. This is a fallacy continually repeated in business schools, on Wolf Street, and elsewhere.

(1) Money may move out of stocks or other asset classes and into bonds or other asset classes. Happens all the time.

Regarding point one: For just one obvious example, companies may buy back common equity (retire the shares from the public market).

Example:

Consider a retail investor or, better yet, a big pension fund or Berkshire Hathaway, who wants to sell Coca-Cola (KO) shares. If Berkshire (or retail investors) wants to exit KO, the stock would likely plummet in price. However, Coca-Cola could decide to buy the shares and retire the common stock. Would the money that Berkshire received from Coca-Cola stay in the stock market? Not if the seller of the KO shares (Berkshire) decided to redeploy the cash from the sale of KO stock into a different asset class such as Treasuries. The seller of KO stock, say a retail investor or institution, would have cash from Coca-Cola to deploy elsewhere outside of the stock market. Coca-cola would have less cash available on its books, and fewer shares outstanding in the market. In this scenario, the stock price could remain stable, perhaps even increase. Going private (public company is acquired by private company, etc.) can have a similar effect. Consider Elon Musk buying Twitter. Did the $44 billion he paid for Twitter stay in the stock market? Maybe, maybe not. It depends on what the sellers of Twitter stock decided to do with the cash proceeds. This goes to point two.

(2) Secondly, the price at the margin (in real estate and corporate M&A, it’s comps; similar with equities/bonds.) may be manipulated, which is exactly what firms like Blackstone have, and still are doing, in the residential real estate markets.

Stock market:

In the KO example, Coca-Cola could bid up the price of its shares while buying back shares (especially in privately negotiated transactions with institutions like Berkshire – and the latter is notorious for buying and selling public shares in privately negotiated transactions), and essentially supporting the stock price/share, or even putting upward pressure on the stock price/share, because fewer shares will be available as outstanding. This happens all the time in the stock market.

Residential real estate:

In residential real estate, Blackstone and others have been shown to buy entire neighborhoods of 500-1,000 houses, hold that inventory while making some cosmetic updates to some houses, but not put any of the houses for sale in that small market. A year or so later Blackstone sells, say, six homes for 2x what it paid to set the new market comps for the neighborhood. However, it “sells” those six homes to a related Blackstone investment fund (or another private equity firm in on the scam). Now it has set the “comps” at the margin at a substantially higher price in the neighborhood.

Liz,

1. Yes, share buybacks take cash out of the stock market. They also reduce the share count.

2. But IPOs, direct listings, follow-on offerings, secondary stock offerings, etc. pull new cash into the stock market. They increase the share count.

But #1 and #2 are the two types of events that move cash out of the market or into the market, but they’re not part of investors buying and selling stocks, bonds, or RE in the market, which is what Bagehot’s Ghost referred to (“money doesn’t ‘move out’ of stocks and ‘into’ bonds, or real estate. Every seller has a buyer…”)

3. Anything the Fed buys puts cash into the market (including QE); anything the Fed sheds pulls cash out of the market (including QT).

4. Acquisitions via shares don’t change the cash in the market, but increase the share count. This includes Alphabet buying a startup with an all-share deal, or one railroad buying another in an all-share deal.

5. Stock-based compensation also increases the share count without changing the cash in the market.

#4 and #5 dilute existing shareholders.

6. Leverage to buy stocks doesn’t move cash into the market because someone else is still selling you those shares and getting the same amount of cash out of the market that you borrowed to put into the market.

Part II (since there is no edit option of my original reply at the moment) — Continuation of my response about how money may leave an asset class and move into another asset class:

…As such, Blackstone (or other shady firms) may value its portfolio of 500-1,000 houses in the neighborhood at 2x the value based on the manipulated comps.

It may further leverage that pool of assets (the houses) as collateral to borrow more money from banks to either invest in more real estate…or take the money out of the real estate market by paying itself a big, beautiful dividend to invest in Treasuries, gold, international markets, etc.

In this example, again, the money could leave the asset class (residential houses) while the asset class itself is re-valued at a higher price (or at a price that might be marginally lower but much higher than it would be otherwise – meaning it helps prevent a valuation crash, at least temporarily, providing ample time for the organizer of scam to extract its capital from the asset class).

In a way, the markets are a shell game that your Average Janes seem to not understand or simply ignore. Blackstone might refer to them behind closed doors as the proverbial “bag holders.”

Somewhat off topic …

Cook was canned this evening for falsifying loan docs. Trump is gaining control of the Fed Board.

The long end of the Bond market is sniffing inflation and nudging higher. Trump has time for two cuts this year which could easily send the TNX yield to 5ish by EOY. That could put home rates well up in the 7’s….That should shake up the real estate market.

Should be an interesting week.

There are 7 members on the Federal Reserve Board of Governors including Chairman Jerome Powell. All interest rate policy decisions are made by the FOMC (Federal Open Market Committee) which is comprised of all 7 members of the Federal Reserve Board of Governors plus 5 of the 12 Federal Reserve Regional Banks Presidents in the US. Replacing a single BOG member will not change the vote on the FOMC in September.

(Bloomberg) — President Donald Trump’s campaign to oust Federal Reserve Governor Lisa Cook, if successful, would give him the opportunity to exert more influence over the US central bank by securing a majority on its seven-member board of governors.

Yes, he will need another 3 votes. But so far Trump is finding ways to get what he wants. He ousted Cook. I wonder how the other 5 voting members are feeling tonight? I did not vote Trump, but I can honestly say he’s not the floundering newbie he was 8 years ago. He has nothing to lose and he is going all in to get his way. Today, South Korea joined the ever longer list of countries that rolled over to Trump, no matter what bluster they came up with prior to meeting face to fave at 1600. 100 Boeing airplanes is a big win for Washington State. Boeing’s been on the ropes.

56 minutes ago · SEOUL, South Korea (AP) — Korean Air has announced a $50 billion deal to buy more than 100 Boeing aircraft and several spare engines and obtain engine maintenance for 20…

The 10-year yield has made up the entire Powell-speech drop this evening. It’s back to 4.31%, from 4.24% after Powell’s speech.

“Somewhat off topic”

Not really… because mortgage rates are going in the same direction.

Yippee… Keep it up, 10 yrs yield going up unlike the housing market is where I hope will continue and this is just the beginning.

After all, gotta have an alternative soon when T Bill will eventually inch closer to lower and lower… Either that or I might just buy a share of BRK-A and call it a day if neither shirt or long term moving closer to TINA

I’d look for a technical buy point in bonds.

We just got assigned our first foreclosure appraisal here in the swamp in over 4 years. These are hard to do. You have trouble getting into the property and they are usually in terrible condition. I believe this is just the beginning of a repeat of the 2008/2009 RE meltdown.

Wouldn’t a meltdown on that level take some black swan event like the subprime mortgage banking crisis? 2008/2009 wasn’t solely due to overpriced housing.

There are foreclosures happening here in Bend, OR as well.

“everyone wants to live here, prices will never go down”.

~every homeowner in Bend, and every other nice place in America

@WHill I think the black swan even will be AI. While I think it’s going to take some software jobs, I think most of those will survive because it’s terrible at problem solving. Where I see it is any job that has repetitive tasks. Back when I was a CPA I automated my job thinking I’d get to leave early and do things I wanted with my free time. I took 60 hour weeks down to 5 hours most weeks and 10-20 for one week at quarter end. My boss gave me my some of my colleagues work, I was told this usually takes 1-2 weeks. I got it done in 2 hours and set it up in a way that would take 5 min a month going forward. My boss stopped giving me work at this point and told me to just sit in my office and do whatever I wanted… there’s lots of jobs like this out there. Any repetitive tasks can be automated. Talking with my PA friend the other day, she was complaining about her medical assistant – my response was I’m really surprised they don’t just have a boy for that. Like 90% of that work could be automated.

I’m not saying I hope people lose their jobs. I hope they don’t. I do see a massive reduction in any job that has a lot repetitive tasks. HR, paralegals, medical assistants, real estate agents, tax accountants etc. people have savings so I’m not saying they’ll lose their houses – but I think it’s going to keep a lot of buyers on the sidelines

Also while I agree the first housing bubble had a black swan event (arguably the failing of Lehman Brothers) that caused panic – our way of dealing with bubble 1 was keeping rates artificially low to reinflate the bubble then throw COVID on top of that – here we are with significantly overvalued assets again

He cannot fire her. Not within his remit.

He did. The letter is out there.

I’m sure there is something in her work contract that alludes to fraud!

There will be a huge court case…more uncertainty.

There was no ‘mortgage fraud’ whatsoever in Lisa’s matter.

awww..how cute…are we still pretending to live in a world where there’s a remit to his power and executive orders? like a kid saying “Hey you can’t do that!”

We have seen all the not-within-his-remit action so far; how many got absolutely shut down and reversed without further pursue? Best we can hope for is going to the Supreme Court; even then, it’s 50/50, and if it’s not favorable to his decree, can also ignore the court’s order…

The only thing that will actually change course is unintended consequences, if his action end up blowing up the long term yield opposite to what he wants, that’s the only hope you’ll see any pivot. Time will tell..

Maybe we are there already then…

Ah yes, the “lying on a mortgage application by a Fed chair is okay when they do it but not for anyone else” argument. By contrast several Fed chairs resigned with just a hint of stock trading impropriety.

Sorry to burst your bubble Fed chair lying on her mortgage application and not resigning out of duty, then ignoring the elected president doesn’t play well with the common person on the street. If she really valued the reputation of the Fed she would step aside – the paperwork showing lying (best case) on an application is already out there.

@whatever. If that’s the case then why doesn’t Ken Paxton, AG of Texas, also resign? He’s claimed 3 primary residences.

According to reporting, and correct this if it’s wrong, Cook is accused of filing two mortgage applications that claimed the house as a primary residence, before she became Fed Governor. For this sort of thing to be illegal it has to be intentional and it has to financially impact the lender in some way. If it does, and it goes to court, then normally these cases are settled with a payment to the lender. Trump can only fire her for cause in the neglect of her *job*, which this has nothing to do with. If he had anything better to use against the Fed members he wouldn’t have to go trawling through old mortgage applications. All he wants is to lower interest rates at all costs because he’s an idiot, and if he gets his way then we’re going full Turkey and this is all going to blow up in his face.

Whatever: Trump grossly exaggerated the size of a property.

Donnie is NOT ‘gaining control of the Federal Reserve Board’ at all, and Lisa Cook’s term is valid into 2038 and she will not be leaving before then.

These Fed positions have way to long terms.

Everyone who claims two primary residences on any property tax or mortgage document, and everyone who claims tax exemptions on their second homes and rentals listed as primary residence should absolutely go to jail. Every real estate fraud from the presidency on down should be fired and prosecuted. That’ll drive down home prices everywhere.

Quick, build more nursing home prisons for the millions! I’m sure everyone on this site is safe.

Preach brother. Send all the mortgage fraudsters to alligator Alcatraz

That place has been ordered shut down by the courts this week and no new folks can be sent there and the government has 60 days from the date of the ruling to entirely clear it out.

It seems like we are going the wrong direction when people on “both sides” keep trying to “explain away” illegal things people on “their side” My GOP friends tell me that rich Republican farmers are “forced” to hire illegal aliens to pick crops and I got a email from a (super rich super white) Democrat friend this morning telling me that Ms. Cook was “forced” to lie on her loan application due to “racism” and “redlining” and that Trump fired her because of racism. I almost hit reply and reminded him that he forgot to mention “sexism” but then I remembered that my wife likes it when he invited us to play tennis at the Circus Club and that he will be the guy to ask if my kids ever want a letter of recommendation to GSB.

Now, mortgage interest rates and 10-year and 30-year mortgage rates are set to soar as any and all respect for the Federal Reserve’s independence has been shaken to the core and thrown into utter turmoil.

“any and all respect for the Federal Reserve’s independence has been shaken to the core and thrown into utter turmoil”

Compared to Bernanke?

Yes, that is sarcasm

They need to fire the 200 PHds (stands for Piled High & Deep) that work on the staff of the Fed across the country. They have led the country into ruin. Bring back Musk for a special assignment or better yet let “Big Balls” do it.

Naw, Big Balls got beat badly by 15 yo girl. He is not up to the task…

Swamp Creature jealous of the educated! Needs his rich daddy to go punish them.

Some clown has a home for sale in Aspen Colorado for $300 million. Are you frigging kidding me? Not long ago, you could buy a nice corporation for that amount of money. It seems that the dollar is a dead man walking.

Any seller can ask whatever he or she wants from a real estate property and that has nothing whatsoever to do with the value of the US Dollar.

“I got a little place in Aspen.” ~Smug white people

That Aspen episode of South Park really nailed it.

The most relevant and true SouthPark episode ever is “the f word”.

I also love the one where they fight hippies with the Almighty Slayer.

Yes? That’s Aspen and it is a micro market that has nothing to do with the rest of the country.

The fact that Aspen and other ultrarich towns with outside money are stratospheric affects real estate prices within a two-hour radius, driving up dumps in not-so-great towns (if I name names, the Boebert fans will come out). That housing run-up in turn helps drive politics in the whole half of the state, and immigrant workers and legal, immigrant, licensed contractors for the rich are scapegoated.

And the Aspenites are smug, yes.

After Senator Feinstein died her kids sold her place in Aspen for $25 million and her place in Tahoe for $36 million. Nobody seems to wonder how so many “public servants” end up with $100 million-dollar real estate portfolios (maybe they all get low loan rates by lying on their loan applications) and outperform Warren Bufffett when invesing money…

Going to be hilarious when existing-home sellers realize their homes aren’t even worth half of what they think they are worth, and they’re forced to sell (recession, divorce, death etc.)

Until that happens (and that may take a while), the home builders are going to get to eat their lunch in terms of market demand, and make a ton of money off the stupidity of existing-home sellers. Why, exactly, should anyone wanting a home go with an existing home when they could buy a new home for less?

Location, build quality, schools, etc…lots of reasons

PCE ex housing is up 20+% in the past 5 years. Housing therefore has lost at least 20% relative, if nominal prices are generally flat.

Location, location, location. Obviously.

Do they build new neighborhoods without HOAs? If I were in the market, I’d pay a premium for a non-HOA house.

Still licking my wounds from 2012 – Misery loves company – Schadenfreude!

I really shouldn’t feel like this: it’s not nice but I just can’t help it.

How much will prices have to fall to regress to the long term trend line in each region?

Not sure about per region but about 45% nationally.

What it shows was homebuilding never recovered from the Great Crash, and slow building has allowed them to pull back on pricing and still move product while slowing their pipelines. In short, they still are running off those lessons from 15 years ago, when stupid high leverage killed a lot of competition. Vultures made a lot of money off that leverage when they bought entitled and prepped acreage that had no immediate demand. And the survivors kept those lessons as the next boom began. And now that it has ended, they will be standing around waiting for the next boom.

Meanwhile, Trump thinks the Fed can ultimately control interest rates, not really understanding how the bond market is really in control. But just another day in paradise. And interest rates for mortgages could still fall, if the compression between the long T bonds and mortgage rates falls.

All I know is that the foundations of the financial and monetary systems are under stress, and something will break in a bad way as a result of all this.

Someday this war’s gonna end…

Here’s what Lennar is offering in south Texas (hundreds of new homes available):

🎉 SPECIAL BUYER INCENTIVES — $12,000 OFF the price of a home OR toward additional closing costs! 🎉

✨ 3.99% FHA (fixed) + Up to $6,000 in Closing Costs

✨ Fridge, Washer, & Dryer INCLUDED!

📍 Magnolia & Montgomery — North Houston

We have brand-new Lennar homes in the Magnolia and Montgomery areas, priced from the low $220s up to the $500s — with FHA payments starting in the $1,620s per month!

🔹 From the Low $200s

• Magnolia Ridge — from the $220s | FHA from the $1,670s/mo

• Magnolia Springs — from the $230s to $240s | FHA from the $1,690s/mo

• Moore Landing — from the $230s to $330s | FHA from the $1,620s/mo

• Chapel Run (Montgomery) — from the $230s to $260s | FHA from the $1,690s/mo

✨ For Higher-End Buyers

• Colton (Todd Mission) — from the $370s to $400s

• Kresson (Montgomery) — from the $470s to $500s

Harrris county median household income is $72k/year.Seems quite affordable.

There is a reason TX is one of the fastest growing states, it sure isn’t the weather or physical geography.

Appliances aren’t normally included with new homes?

Usually not a fridge or things like garage door openers, window blinds.

Decent prices but if the HOAs don’t allow people to repair their own vehicle in their driveway, it’s a no go for me.

Very much aware that (a) this article is about New SFH prices, not Existing SFH prices and (b) Case-Shiller isn’t the preferred index here, but I found one element of today’s release quite interesting: Going back to 2015, this is the *first and only* June in which the 10-City and 20-City Composite Indices experienced pre-seasonally adjusted MoM declines. I thought that pre-seasonally adjusted MoM declines were supposed to be an AUG/SEP through JAN thing…and that home prices only go up…

“June’s results mark the continuation of a decisive shift in the housing market, with national home prices rising just 1.9% year-over-year—the slowest pace since the summer of 2023,” according to Nicholas Godec, S&P Dow Jones Indices.

“Looking ahead, this housing cycle’s maturation appears to be settling around inflation-parity growth rather than the wealth-building engine of recent years”

Waiono write your own blog. If I wanted to read msm propaganda I wouldn’t be here.

log!

that helpful?

I meant Blog…see, that’s why I don’t have my own blog

Out of curiosity, does this data only count new homes built on previously undeveloped lots, or does a complete demo and rebuild of a new house get counted in these numbers?

If it requires a building permit, it’s in the survey. In a few places (2% of total residential construction), no building permits are required to build a house. And estimates are included for those.

Here is the more detailed methodology:

http://www.census.gov/construction/soc/methodology.html

“The Survey of Construction includes two parts: the Survey of Use of Permits (SUP), which estimates the amount of new construction in areas that require a building permit, and the Non-Permit Survey (NP), which estimates the amount of new construction in areas that do not require a building permit. Less than 2 percent of all new construction takes place in non-permit areas. Data from both parts of SOC are collected by Census field representatives. For SUP, they visit a sample of permit offices and select a sample of permits issued for new housing. These permits are then followed through to see when they are started and completed, and when they are sold for single-family units that are built to be sold. Each project is also surveyed to collect information on characteristics of the structure. For NP, roads in sampled non-permit land areas are driven at least once every 3 months to see if there is any new construction. Once new residential construction is found, it is followed up the same as in SUP.

The Census field representatives use interviewing software on laptop computers to collect the data. Facsimiles of the computer-based questionnaires are provided to respondents to familiarize them with the survey. These facsimiles show the questions that are asked for housing units in single-family buildings on Form SOC-QI/SF.1 and in multifamily buildings on Form SOC-QI/MF.1. In addition the Census field representatives provide an introductory letter explaining the survey. Field representatives also use Form SOC-QBPO.1 to collect information regarding procedures for handling building permits in building permit offices (BPOs) sampled for the SUP.“

What if the Fed surrenders to the current administration and severely cuts rates? Would this help to prop up the bubble by giving people the chance to borrow at lower rates?

Mortgage rates might hit 9% if inflation worries and worries about a lax Fed collide. Last year, the Fed cut 100 basis points and mortgage rates soared 100 basis points to the surprise of everyone, esp. the RE industry.

9%? I would love to see that and I guess anything is possible, but I probably won’t expect it in my lifetime (hope to be proven dead wrong).

Just imagine that, at 9%, if you take out a million-dollar mortgage, which seems to be pretty common around nicer parts of LA or OC/South OC, it’s almost a cruel joke how little it goes towards principle after even 10 years. Coupled with less than 20% down and PMI, you really are only betting on the market powering up double-digit gains every year to come out ahead. Yikes…

Year Date Interest Principal Ending Balance

1 8/25-7/26 $89,723 $6,832 $993,168

2 8/26-7/27 $89,082 $7,473 $985,695

3 8/27-7/28 $88,381 $8,174 $977,521

4 8/28-7/29 $87,614 $8,941 $968,581

5 8/29-7/30 $86,775 $9,779 $958,801

6 8/30-7/31 $85,858 $10,697 $948,105

7 8/31-7/32 $84,855 $11,700 $936,405

8 8/32-7/33 $83,757 $12,798 $923,607

9 8/33-7/34 $82,557 $13,998 $909,609

10 8/34-7/35 $81,243 $15,311 $894,297

@Phoenix_Ikki Almost every home and apartment loan in the 80’s (when I first started buying investment property) was over 9% so I would not be shocked to see 9% rates again.

I am shocked at how few people seem to do the math and realize how much they could save by paying down loans faster. The loans secured by a property are public record and I’m amazed how many of my neighbors now owe more than $1 million MORE than they paid for the homes.

I have never taken more than 18 years to pay off a “30-year loan”. I recommend everyone get a loan with a 30-year am but since almost no home loans have prepay restrictions you can throw all your extra cash at it and be in a great place with a paid off home before you retire.

9% isn’t even that high by historical standards.

@ ShortTLT absolutely agree, but keep in mind, we’re talking about the general public that has very short-term memory, and for all of the younger millennial buyers, double-digit mortgage rates might as well be reading about the civil wars in history books, not something they expect will ever happen again hence why people are kicking and screaming when interest rates are over 5%. To be fair, though, with these insane prices right now, the blame game is always on interest rates but not the actual fundamental pricing, and we have been conditioned to accept that is the norm…

@Phoenix_Ikki, no doubt.

Prices are what need to come down, not interest rates.

10.75% for my first home, decades ago in California.

The sky didn’t fall

Not all of us were surprised that cutting short rates drove up long rates…

Correct, here in this joint.

Just how high do you want to see mortgage interest rates go? Back to where they were in the early 1980s? You do realize that the only rates that the Federal Reserve sets are short term overnight interest rates, don’t you? Mortgage interest rates are based on the yields (interest rates) of 10 year US Treasures and will quickly factor in much higher expected inflation.

In my market of Northwest Indiana, Lennar and DH Horton started building in 2020. Together, they are now building around 1,000 homes per year.

What is driving their growth is the never ending stream of homebuyers leaving Illinois and moving to Northwest Indiana to escape high property taxes, incompetent government, poor schools, etc. Even with relatively high mortgage rates, the in-migration continues. These new homeowners tend to keep their higher paying jobs in Illinois and daily commute to and from home to work in Illinois or Chicago. The traffic in the area is terrible, with subdivisions being built along former two-lane county roads with very little public roadway improvements occurring.

The growth of Lennar has come at the expense of smaller builders in the area. Lennar can offer the incentives that smaller builders can’t or won’t and are undercutting them by as much as $50,000-$100,000 per house. These small builders who rely on local bank financing, are slowly being strangled out of the market.

This is all about maintaining national market share.

While Lennar is struggling in FL, GA, TX and AZ, in 5 years they have become the dominant homebuilder in NW Indiana.

I don’t see this ending anytime soon. I read where Lennar has a $2.3 billion national line of credit. They are buying any and all available farmland in the area and aggressively going through the planning process to make the sites buildable as fast as possible.

In St. John, IN, just across the border from Illinois, they are developing a subdivision called Astoria. Purchased the farm in October of 2024, built all the infrastructure over the winter and paved the streets in Spring of 2025. (Building permits can’t be granted until primary asphalt is installed.)

So far, all they are building are spec houses. Last count last week was 9 under construction and several foundations being prepared.

Existing homeowners in the area trying to sell also can’t compete with them for the same reason that small homebuilders can’t compete.

Within a two mile radius of this subdivision, there are over 1,050 lots going through the planning stage in adjacent communities by several developers. My take is that most will end up selling to Lennar although at a bulk price discount.

Wolf, keep up the good work.

Lennar bought out the small developer that built my house a few years ago and is developing the remaining few un-built lots. They are like Piranhas gobbling up everything in their path around here (south Texas).

I would bet against the long term success of the state of IL all day long, I’m shocked that anyone still lives there.

As always, hard to tell where this admin will go. But yes, it’s pretty clear that absent us heading into a recession (doesn’t seem like it right now), radical rate cuts into rising service and goods inflation would be a bad thing for the 10 year, which actually might throttle the economy more than short term rates are doing.

But with a captive Fed, one has to wonder what happens if they undertake yield curve control? Nobody, even the bond market, can fight the Fed. You might be tempted to say “they learned their lesson, they wouldn’t do that!” and you’d probably be right, but in this environment who wants to get bashed by POTUS over fulfilling your lawful mandate?

Tough time as a prospective first-time homebuyer. There are discounts happening on properties I’m interested in, but my market isn’t in Wolf’s big list [yet]. Some would say so goes the Fed, so goes the economy, but tough to straddle a macro future that ranges from inflationary YCC fever dream to [garden variety] recession with an extremely overpriced RE market.

One thing I rarely see discussed when talking about the new home prices is the decline in square footage. Builders are buildering smaller, and have been for years.

Q2 2025 homes are 15.6% smaller than Q1 2015.

Q2 2025 homes are 8.8% smaller than Q4 2021. (See FRED stats for HOUSTSFLAA1FQ).

When looking at price per square foot, specifically of these 2 datasets (Median Sales Price for New Houses Sold in the United States/New Privately Owned Housing Starts in the United States, Average Square Feet of Floor Area for One-Family Units), you see that the price per square foot has been roughly flat since 2022.

The peak price per square foot was Q1 2024, at $182.57. Q2 2025 is $175.41, or a decline of 4% from the peak.

So yes, the price of new homes are clearly falling. But part of that is simply homes are being built smaller than they were in the past.

So 2015 was peak McMansion at about 2,467 sf. Everyone complained about it and made fun of it. It was ridiculous.

By comparison, in 1982, the median size was a more reasonable 1,500 sf.

Then in 2016, the size began inching back down.

But in 2024, the size bottomed out, but still huge 2,146 sf.

In 2025, the median size rose again.

Yeah, there is always some goofball the whines about the affordability crisis and then complains that homes are 300 sf smaller than they were at peak McMansion though they’re still nearly 1,000 sf larger than they were for people like me when we started buying homes.

Lots they sit on always shrink.