There are exceptions: Parts of commercial real estate are in a depression, and the housing resale market has frozen.

By Wolf Richter for WOLF STREET.

At the Fed’s post-meeting press conference on Wednesday, Powell will likely re-point out for the nth time that policy rates are mildly or moderately “restrictive,” with the midpoint of the Fed’s policy rates (4.33%) still being substantially higher than inflation rates. Overall CPI inflation accelerated to 2.7%, and core CPI to 2.9% in June, driven by reaccelerating inflation in services, especially non-housing services, and services matter because they’re two-thirds of consumer spending.

The Fed’s policy rates being substantially higher than any of the inflation rates in theory means that these policy rates turn financial conditions “restrictive,” which would then filter via the financial markets, especially via the credit markets, into the economy and restrict demand in the economy, which would allow inflation to cool.

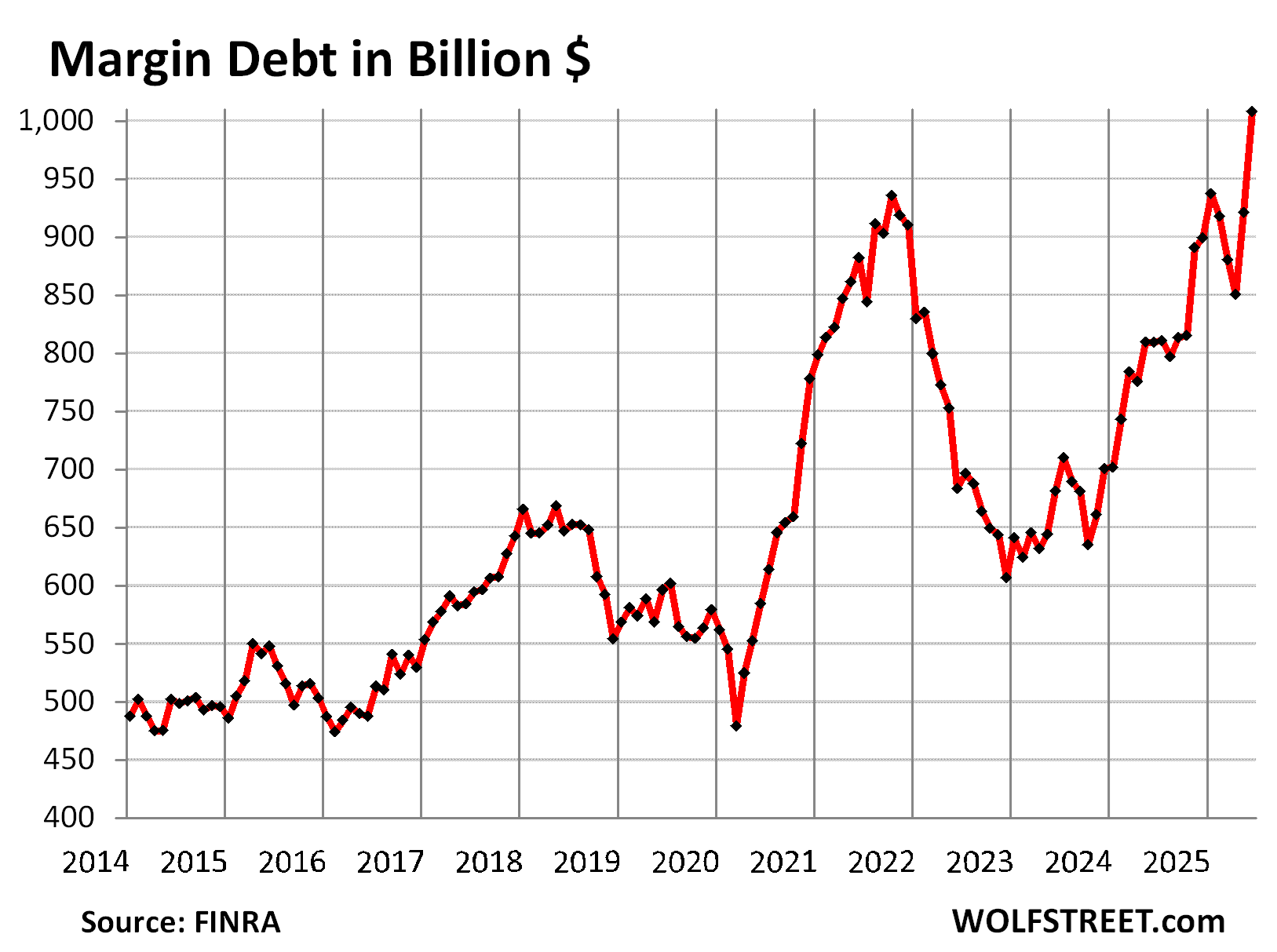

But financial markets have blown this theory beautifully out of the water, they’re practically ridiculing it: Stocks have risen from record to record and are immensely expensive by just about every measure. The meme-stock mania has massively flared up again, where people gang up in the social media with leveraged bets on the most shorted stocks – GoPro, Kohl’s, Opendoor, Krispy Kreme, etc. – causing these stocks to briefly spike by silly percentages. There are signs everywhere that people are taking huge risks with a this-is-so-much-fun attitude, including with cryptos where another mania is in full swing. And margin debt blew out by a record amount, to a record, and is Exhibit A of loosey-goosey financial conditions.

Amid manias left and right, Goldman Sachs reported a 36% year-over-year spike in equities trading volume in Q2, Charles Schwab reported a 38% year-over-year spike, Morgan Stanley a jump of 23%.

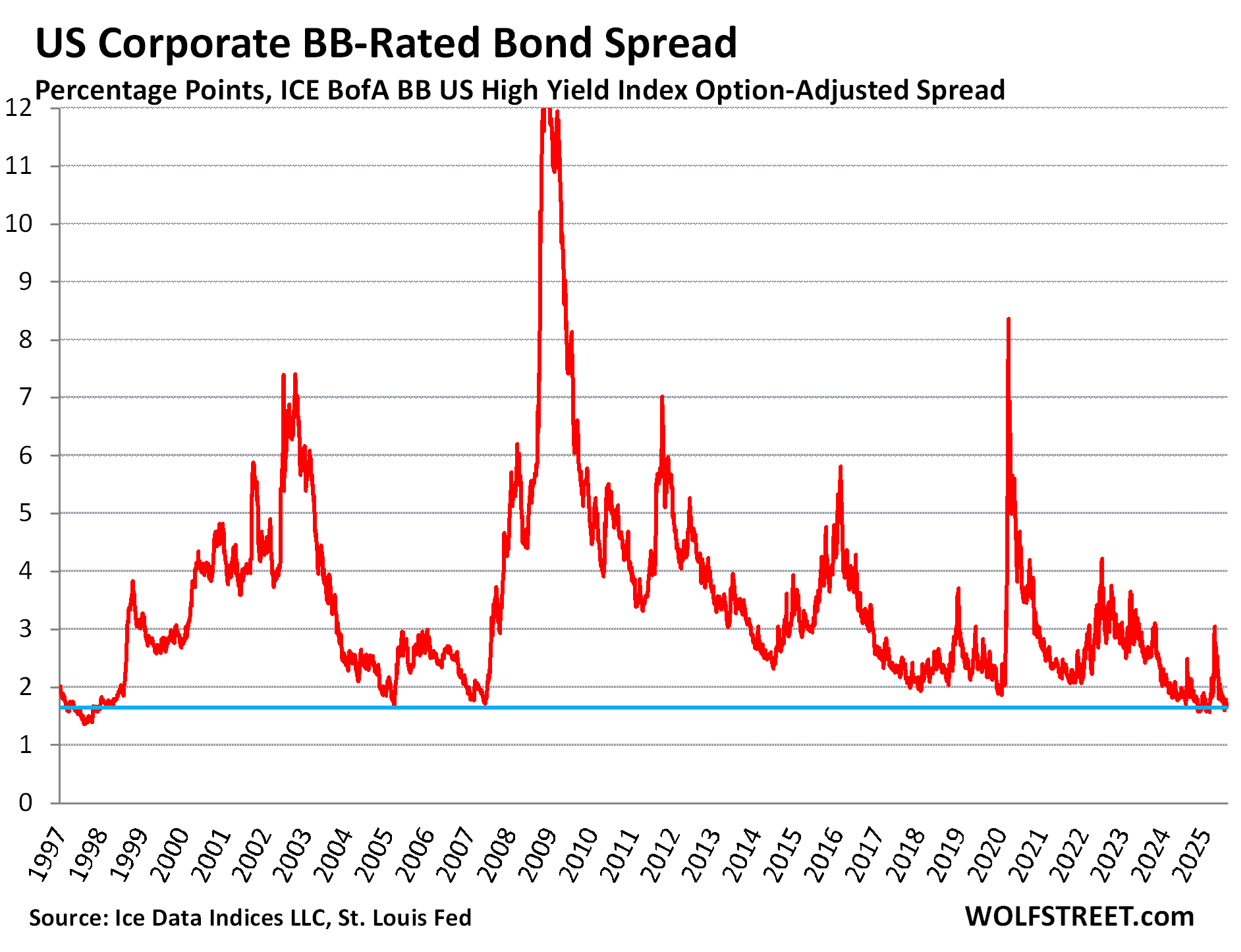

And in the credit markets, spreads between high-risk junk bonds and Treasury securities are historically narrow – and that’s Exhibit B of loosey-goosey financial conditions.

Sure, there are some exceptions. Powell cited real estate as an example where financial conditions are restrictive. He cited both commercial real estate, segments of which are in a depression, such as the office sector with record default rates, and residential real estate, where the resale market has frozen largely as a result of home prices having spiked by 50% and more in a two-year period through mid-2022, from already very lofty levels, and those prices don’t make any economic sense. But that hasn’t impacted the overall economy enough to make a dent.

Exhibit A of loosey-goosey financial conditions: Margin debt blew out, spiking by 8.3% in May from April, and by 9.4% in June from May, to a record $1.01 trillion. In dollar-terms, June was the biggest month-to-month spike ever (+$87 billion). Combine margin debt with meme stocks, and it’s magic.

In percentage terms, there were bigger spikes, such as in November and December 1999, just before the Dotcom Bubble imploded – less than three years later, the Nasdaq Composite was down by 78% – and in May 2007 just before the simmering Financial Crisis broke out into the open for all to see.

Exhibit B of loosey-goosey financial conditions: Junk bonds are completely in la-la-land. The spread between BB-rated junk bonds and Treasury securities has narrowed to 1.64 percentage points, according to the Option-Adjusted Spread of the ICE BofA US Corporate BB Index. These BB-rated junk bonds yield only 5.64% on average (the WOLF STREET cheat sheet of corporate bond credit ratings by ratings agency).

A narrow spread between BB-rated junk bonds and Treasury securities means that investors are bidding up prices of these bonds despite their substantial risk of default, and thereby investors are not getting paid to take those risks, and investors just don’t care. They’re eager to take big risks to get a little more yield.

There were a few other times with an even narrower spread after the Dotcom Bubble:

On Mar 9, 2005, spreads narrowed to 1.65 percentage points. And in June 2007, just before nearly everything blew up, they narrowed to 1.71 percentage points.

And then from November 2024 off-and-on through February 2025, the spread was as narrow or slightly narrower than now, despite the supposedly restrictive financial conditions. During the lead-up to, and for a few days after, the Liberation-Day parade of horribles, the BB-spread widened sharply and peaked on April 7 at 3.06 percentage points. But that has now also gone away, and by July 25, the spread was back to 1.64 percentage points.

All of this clearly shows that the Fed’s policy interest rates are not restrictive – however Powell wants to phrase this. Financial conditions in the financial markets are amid the loosest ever. There is no tight liquidity anywhere. Markets are still awash in liquidity. Nothing is restrictive.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Market expects inflation is headed down over the medium to longer term?

so the $26 lb ribeye is going to moderate

excellent

$50 steaks it is then

and $6 lb hamburger

week ago instead of going to restaurant for burgers

we bought chuck steak and had meat market grind it

2 lbs in freezer

large mushroom swiss burgers

$20

From AI IT WILL GET WORSE

Yes, Brazil is a major supplier, supplying over 210,000 t of beef to the U.S. in early 2025.

• Yes, Brazilian beef is (or will be) tariffed at about 50%, but that applies in addition to the existing 26.4% tariff beyond the quota, reaching a combined rate of roughly 76%, which severely limits its economic viability.

⸻

🔍 Broader context

• Domestic cattle inventories in the U.S. are at a 70‑year low, prompting increased reliance on Brazilian lean beef, particularly for ground beef production.

Nonsense.

1. The US produced 13.5 million tons of beef in 2024. So the 210,000 tons imported from Brazil is just a small percentage.

2. the US EXPORTED 1.5 million tons of beef in 2024, or about 11% of its production. If the US didn’t export this beef, it would more than make up for the imports from Brazil.

3. The US imported 2.3 million tons of beef in 2024.

4. So the US had a trade deficit of beef of only 800,000 tons, or less than 6% of its production.

5. The US is an importer of beef from Australia, so buy Australian beef. For example, Trader Joe’s sells grass-fed Australian beef. There are other countries the US imports beef from, such as Canada, Mexico, Argentina, and Uruguay.

6. So there is zero reason to buy beef from Brazil — and imports from Brazil will come to a halt unless Brazilian producers are willing to eat all the tariffs, suggest medium rare.

7. That’s why tariffs are dynamic, and people like you keep getting tangled up in your own underwear over them.

8. You can also buy US pork (it’s delicious), and demand for beef will collapse and prices come down.

The reporting of the “inflationary and disastrous” impact of tariffs is everywhere in the media. Just today, on DC news radio, I heard their primary money commentator, Jill Schlesinger, state that tariffs were showing up in car prices, computers, electronics, furniture. Being DC metro, this is what executives, policy makers, congressional staffers hear and internalize.

The media wants to create interesting stories because that’s how you get paid – by advertisers who want audience. They want to create these stories as quickly and easily as possible as that is human nature, so they accept plausible pre-written copy from corporate contacts.

Politics is about shaping public opinion, because that’s how you get votes, and facts (and complex facts especially) are largely secondary.

Inflation is continuing to accelerate; however, restrictive interest rates are those higher than the rate of inflation. The only way for the current inflation increase to occur is if inflation is not measured correctly and the control of interest rate being above inflation has a too low rate.

Any engineering control theory course teaches the need for negative feedback to stabilize a system; therefore, this economy needs higher interest rates. What will then occur is the amount of interest over an improperly measured inflation rate will demonstrate a bias requiring a correction factor.

don’t forget the big beautiful debt bill

as MAGA supporter I was NOT IN FAVOR OF UNIPARTY/RINO bill

IMHO this debt is being issued fraudulently

ie never intended on being repaid

Yes, the federal budget deficit is 6%+ of GDP. How much inflation does that cause by itself? There is no way interest rates are restrictive.

Yes, but engineering is a true science and economics is really just made up math to make it look like science. Social science, sure, but nothing more.

The average monthly Federal Funds Rate from July 1 1954 to June 1 2025 was 4.61% (source FRED). Lots of ups and downs. But based on this history, the current rate of 4.33% is a little loose, not restrictive. Curiously, the median over the same time period was 4.33% which is exactly the same as the current rate.

The FOMC ought to step up ST rates by 100 bp easily over next 12 months. The market signals have been there all along. Corollary: the general indices of price inflation are intentionally suppressed by the govt.

I agree with all of this and have been proven wrong as the S and P shot to 6300 from 5,000 in a matter of months. What’s the counter narrative here?

Counter narrative is valuation alone is not enough to blow up the stock market. Need a recession, etc to blow it up.

Thank you for stating the obvious in clear terms Wolf.

And No Thanks to the Academics at the Fed that bury their heads in their Models and Theories without regard to reality.

The idea that they should ignore financial markets in their policy settings is frankly ridiculous and the Financial Journalists should call them out on it.

Every meeting.

This is one of the most important articles available to understand financials conditions…would love if this could be published monthly similar to the housing updates. Thanks, Wolf!

chase won’t allow CD’S in IRA’s

Merrill does, but bills pay more and are more liquid.

TBills that is, AI auto correct working well.

Vanguard man!

You own the company!

What’s better than that?

Warren Buffet “Jack Bogle has done more for the American Investor than anyone else, Thanks Jack!”

There is some truth to this but the Fed absolutely CANNOT “go with their gut” when guiding the USA’s monetary policy. Computers and The Internet changed the game and it will take time for science to understand and predict well under the new way of things, the producing better predictive models.

They can use existing models, be somewhat wrong, examine everything, and improve for the future. It’s not perfect but it works.

But if they make policy based on those new theories without the backing of history then policy will fly all over the place (because there are many such theories) and they’ll get lambasted for any mistakes because they’ll have no justification but “it felt right”.

It’s easy in hindsight to point out some theory that clearly predicted the past forgetting that, in the past, it was only one of a dozen contrasting theories of which none was obviously correct or widely accepted.

I didn’t say the Fed should be “going with their gut”.

My point is that they NEED to value and emphasize market conditions in their monetary policy decisions, especially when they are so clearly making a statement about the looseness of financial conditions.

Market pricing is a reflection of millions of decision makers, betting their own and others money and thus a valuable input.

Current dogma in economics is that the economy can be quantified and modeled which will yield a control board whose knobs can be tuned to produce desired results. I’m guessing this whole idea is false.

Many financial markets have become global and tightly integrated. Now massive carry trade like quantitative programs operate extracting pennies and depending on low volatility.

But when “everyone” is using the same models and trading based on the models doesnt that have the tendency to make the models the market. I suspect that is why all the traditional metrics seem to tell us that the market is behaving oddly.

Is it because the markets are no longer a reflection of an actual economy of production and consumption. The markets are now a reflection of the models and not the economy

Uh yeah I don’t think the last 400 years of economic research and economic technology agrees with you.

From a very old article by Peter Warburton

“ The loss of a stable numeraire

In the physical world, there are constants that serve as dependable benchmarks against which to observe natural phenomena. Examples are the velocity of a falling object, the freezing point of water and the time taken for one rotation of the earth on its axis. In the economic and financial world, this degree of precision is lacking. Instead, we content ourselves with approximations, indices and averages. We pride ourselves in knowing the difference between an inflation rate of 2% per annum and 2.5% per annum. Small deviations of outcomes from expectations can trigger dramatic trading in financial instruments and result in the transfers of billions of dollars between investments. Yet, in the financial realm, can we really be sure of the value of anything?”

Brian

“the Fed absolutely CANNOT “go with their gut” when guiding the USA’s monetary policy.”

“We will be data dependent” J Powell

“We will see through the data when appropriate” J Powell

ie, the Fed will do whatever they feel like doing. And that is why we need the Taylor Rule or something “hard rail” similar.

I find it amazing what “science” can do with incredibly fast and billions of simple on and off switches….totally amazing!

Especially vastly improving on our ability to predict the future….time for us is becoming just a small bump in mankind’s historical road…….we will likely eliminate it completely and VERY soon…

……..and to think we started by going with our gut.

BTW: Provocative article…..well done.

Also, being a (likely senile) old Luddite……it just seems to me that most everyone who is able to, is just kiting the maximum checks they can….to use an old and out of date term.

And there really are MANY who can, thanks to inadequate, much less enforced rules, lots of corruption (even LEGAL bribes), and ESPECIALLY the lack of ANY boundaries to this weird immoral and hypocritical game of ours….which has resulted in extreme wealth inequality……and the many check kiters.

There are no Academics at the Fed. That department was eliminated.

It’s not “frankly ridiculous”, it’s the law, which spells out the Fed’s responsibilities, which do not include being a welfare program for stock investors.

I think all of this demonstrates that while QE is sufficient for loose financial conditions, it’s not necessary. 3 years of QT hasn’t really affected financial conditions, even as the money has been withdrawn, as the psychology of investors hasn’t changed.

People are investing like this because they think they can’t lose. Only a prolonged bear market will shatter that ingrained belief.

People are investing because they believe the fed will step in and intervene.

Look at the markets pre SVB bailout and then after. The market doesn’t believe that a bear market can ever take place.

That seems true for now. A non ‘too big to fail’ was deemed ‘too connected’ to fail and saved out of compassion for the little guy. Oh wait….

Investors in SVB got wiped out. Uninsured depositors got bailed out…. meaning people and companies with over $250,000 on deposit at SVB. Deposits of less than $250,000 were insured anyway. Turns out, deposits of billionaires’ startups and rich Silicon Valley people’s own deposits were bailed out. So not exactly the “little people.” The little people had deposit insurance and would have been fine. The big people exceeded deposit insurance and would have gotten a haircut of maybe 20% on their deposits. Not the end of the world. The banking regulations and FDIC rules should have been allowed to work and do their jobs.

Wolf little people shouldn’t get Christmas bonuses.

But Clark Griswold’s cousin Eddie threw a Hail Mary one Christmas in chicago.

Record

“…they believe the fed will step in and intervene.”

Indeed.

The Fed has decided they will iron out all business cycles. That is there new self defined mission….from lender of last resort to the fairy of perpetual up markets.

Correct.

If you think your investment is risk-free, or at worst, you’ll have a downturn that lasts 6 months, you don’t care about valuations at all.

Unfortunately, this is correct.

People have this idea that asset/equity prices can go up forever and ever without end or pause. It’s creating a lot of bubbles – see real estate. I still see idiots/scammers around who say that stocks or real estate or crypto will never go down so you should get in now.

To break this mentality, prices for assets and equity can’t merely go down (and they will, a lot) – they have to stay down for a long time, preferably at least a decade if not two. Long enough that people quit thinking that owning financial assets is a guaranteed route to endless riches. Only then will sanity be restored.

I agree with you, but I want to add to it. It needs to go down, and Congress and the Fed have to ignore the caterwauling from the mainstream media, that represents the rich and powerful, to “do something.”

“do something.”

Exactly.

A big (perhaps, huge) part of the unprecedently aggressive “investor” mindset on valuations is the (far from unfounded) sense that any significant asset price decline (no matter how justified) will be met by a DC “printer’s put” in order to “fix things”.

And the resultant chaos from the resultant inflation?

These people don’t think that far ahead (or use it to justify taking/selling financial meth to “win” inflation’s Red Queen’s Race).

I’ve been an investor for decades primarily in the securities markets primarily. While not a “Bogle-head” I keep investing simple: a few select stocks, a few ETF/Mutuals in the broad market (think S&P500) and a preponderance of Treasury securities. I agree that there is a real danger that individuals woefully underestimate the risk involved in owning securities, real estate, or even Treasury securities. I absolutely cringe when I hear Dave Ramsey (who is extremely popular among the broad populace) throw out comments like “the market goes up 12% per year” or “4% inflation adjusted withdraw rate in retirement is stupid-you can do 8% or more”.

A 50% decline in year 1 followed by a 100% increase in year 2 is an average annual return of 25% but an actual return of 0.

But breaking the mentality, as you suggest is required, will utterly wipe out everyone except the very, very rich (like the top 0.1% and above). Retirements, homes, and jobs wiped out. Followed by wide-spread destitution and most probably a deflationary depression. Of course the Blackrock’s of the world will be overjoyed – assets on the cheap (just like 2008).

Yes, there needs to be less froth in the securities markets. Housing needs to come down (probably back to 2015-18 pricing plus inflation). Wages need to increase. And inflation needs to come down.

But the long term destruction of asset prices will destroy the country. Be careful what you wish for.

Exact opposite. It’ll wipe out the very, very rich. Everyone else will be okay, as they don’t have enough in stocks to make up for the inflation caused by the asset froth.

I’m going to take the other side of this. I listen to a lot of Gen Z’ers in my workplace and there’s a common theme that they feel like they can’t get ahead when it comes to home ownership, plagued by student loan debt, persistent inflation, and have difficulty saving. Their thoughts on the stock market is a lotto ticket to them getting ahead. I don’t necessarily agree with all of this, I’m just telling you what they’re saying.

Student loans are a personal decision.

My granddaughter went through college applying for grants and scholarships and came out debt free. It’s really not that hard to do this or even just come out with very minimal debt. also, she had a part time job while in college. .

And a very smart money man said never go into debt your first 2 years of college. Go to a junior college if you have to and then transfer for the diploma.

Makes sense. They have heard from their parents’, and experts of similar age, that you should just “buy and hold” either “high quality companies” or “well diversified index funds,” and “you’ll be rewarded in the long term.”

The main difference is that the economy used to grow, and stock growth was a reflection of that. Now, while the economy still grows, most stock growth is multiple expansion.

They have to hope that what worked from 1981 on will continue to work. Which means that valuations never start mattering, if they want stocks to continue to appreciate, or at best, that they flatten out for years while valuations catch up.

It looks like Trump is betting that the U.S. economy can continue to grow by bringing manufacturing back home. To some extent, that seems reasonable—but it may not lead to sustained long-term growth.

Regardless, even if there is no growth, investing in stocks could still offer some protection wrt interest rates.

If history is any judge gen Z will wind up being richer than any generation before. Not to mention the beneficiaries of tech benefits never before seen by humanity.

But now there is pain.

Agree, it’s less about current policy and more about the expectation for dovish future policy. The equities owning public, top 50%, has seen how dovish the Fed and congress will get in the face of any slight hiccup, and are placing bets accordingly.

coming great reset is getting boost from

big beautiful bill

issued fraudulently with no intent on repaying

QE was so huge that the small amount of QT has only put a dent in the amount of money QE injected.

I mean, that’s not true. About half of the COVID QE is gone. It’s not enough, but it’s not “small.”

Maybe they should have kept the QT rate higher for longer.

Perhaps another example of these trends is mainstream banks finding ways to lend into private credit deals, extending credit to firms they would traditionally refuse or charge more in interest to. This reminds me of banks rushing to make foreign loans (many times over centuries), preceding big financial system stresses. It could be a mispricing of risk, driven by competitive pressures (keep dancing as long as the music plays, right?), and the feckless current regulators have no eyes or handle on it. (I was pleasantly amazed in the COVID crisis that Trump’s appointees such as Mnuchin and in that moment anyway, Powell, had some ability.)

There are so many institutions and relationships exposed suddenly to potential volatility due to the political change in climate, with such complex crossovers and mixtures (private credit plus stablecoins, loosened regulatory oversight, political Fed pressures, etc.), with plenty of opacity in all the possible mixups and mashups, I think one thing that could cool these markets is something unforeseen breaking across new fault lines, inducing losses in unexpected places.

I got 4% seller carryback

only put down 70%

The current interest rates should be mildly restrictive, but are having no effect on the handful the tech stocks that dominate the stock indexes. The big techs are fueling the impression that interest rates don’t matter. Nvidea doesn’t care about another 100 basis points. The uphoria about the overall SP500 index price is raising all the boats in the water. How else can you explain 200x pe ratios for companies like Tesla?

Higher interest rates make about as much sense as lower interest rates in this fairy tale land.

However the music will eventually stop, and many boats will crash in the rocks. Interest rates will once again matter.

And my guess is a majority of the record margin is in the mag 7 stocks. So look out below if they all head for the exit at the same time. Margin calls and a bloodbath.

Fed should be accelerating QT instead of slowing it.

I expect they would prefer that. The risk is that they go too fast, something breaks, and they have to do another bout of QE thus undoing much or all of the work done so far.

If no speed limit is posted but you know you’ll get your car impounded if caught speeding, how fast would you drive?

They’re playing it safe. We’re going in the right direction, according to the Fed mandate which does not include the stock market. I generally agree with them.

Brian, fantastic analogy.

While I would also like to see the Fed increase the rate of QT, I acknowledge that breaking things would put the whole institution at risk thanks to one particular pushy, button mashing politician. A slow fat burn doesn’t overwhelm the system as much as a 1,000 calorie diet paired with daily half marathon runs.

The Fed is caught between a rock and a hard plate. It they lower short term interest rates now, the ones they control, the long term rates will go up like they did last fall, including the 10 year Treasuries, 30 year notes, and further hurt the housing financing market, CMBS refinancing, etc. If they stay pat they will be get pounded by the current administration like there is no tomorrow. They are is a LOSE LOSE situation. I predict they will stay pat and let the markets determine long term interest rates which given the strong economy cited above will go up anyway and lead to a money crunch for those industries which rely on long term debt refinancing.

Getting “pounded” by the president is part of the Fed chair’s job. The president can push for low interest and then blame Powell for not delivering. This is why the law makes it “illegal ” for the president to fire the Fed chairman despite the constitutional provision that executive power is vested in the president. Good cop bad cop.

Even if Trump doesn’t understand that, I suspect his advisors do.

I think what he’s doing is lambasting Powell so that if and when something breaks, he can say “See! I told him he should have lowered rates!” But on the same token, he doesn’t actually want the long-term yields blowing out and further damaging the economy.

The rock and hard place is their foray into the Long End which gave them a one Trillion paper loss

They always finds the rock and the hard place when they try to make water run uphill

Isn’t creating money out of nothing…balance sheet gimmicks a form of magic? Is not the pen mightier than the sword? With the flick of a pen new reserve money is created on the books ..he who controls the books, controls the world …we have too many rackets…money being king. TC.

Rule 1. The spice must flow.

Rule 2. Rule 1 is sacrosanct

Perhaps the Fed is more worried about the leverage in the markets than inflation ? It would seem a little more regulation

would have sim plied the Fed’s position

in the long run.

We should start evaluating whether the spread is narrowing less because investors are underplaying risk on credit and more because they perceive Treasury securities as having greater risk relative to corporates. Of course Treasury securities are “risk-free” in an important credit sense, but the last 15 years, especially the last 5 years, has shown an appetite for political wrangling that threatens the stability of the Treasury bond market. Debt ceiling negotiations have regularly threatened technical defaults, and there has been open talk of restructuring by altering maturity terms of existing Treasury securities. There has been talk of applying default or restructuring selectively based on the holder.

I am not suggesting I am certain of this effect. I am just saying we need to start evaluating a model where there is a hypothetical no-credit interest rate and a “political risk” spread on Treasury securities. Under this model, it may be that it’s not the credit spread for corporates narrowing. Instead, it’s a stable credit spread but widening political risk spread for Treasuries.

To put it differently, who would you rather lend to? Microsoft or Congress? There is a point at which political dysfunction will make you more confident in Microsoft.

“To put it differently, who would you rather lend to? Microsoft or Congress?”

1. Here we’re talking about BB-rated junk bonds, not AAA-rated Microsoft bonds (one of just a few US companies with a AAA-rating).

2. Microsoft can go bankrupt, like so many formerly big unbeatable iconic AAA-rated companies have (remember Kodak?).

3. But Congress cannot go bankrupt, though it’s morally already bankrupt.

as long as Microsoft (and Apple) have their monopoly, I’d rather lend to them.

Yes, with the current lack of antitrust policy, they can practically print money for themselves by twisting the arms of others.

Howdy Folks. Bubba says its time for Greenspan. Maestro would lower, lower, raise, lower, lower, lower, lower, raise, maybe lower, maybe raise, raise, raise. Believe it or not??????

Wolf,

Do you think there is a fed rate at which your examples become restrictive that isn’ so high it crashes the economy? While I agree the current rates aren’t “acting” restrictive for either Exhibit A or Exhibit B I think it’s more an example of the phycology of the investor than the restrictiveness of the current rates. I get the feeling that the general age/maturity of current investors tends to slant more to the lower end of the spectrum (my opinion, its more a feeling though I’d be curious if there is actually any historical charting of investor experience levels) so they really haven’t lived through a time when “everything” was going bad, so they don’t have the kind of ingrained fear more experienced investors have. Between that and the advent of Robin Hood, et al which makes the process easier – is this just a case of the guy at the slot machine betting his rent on an “investment” that in his short time has “always” paid off? I would think that type of person isn’t even factoring in the margin rate because if everything is a sure bet any margin rate will just take a bit off the top of their winnings. And I’d assume (maybe incorrectly) that similar to 2008 the people on the other side of those margin rates (Robin Hood, Schwab, etc.) are so giddy with the money it’s bringing in that they are being a bit looser with credit than they ought to be.

Wolf, you added a third building.

Brilliant

Margin debt dropped 30% twice on the chart. Markets dropped too but obviously recovered and did fine. Not sure margin debt is a great indicator of anything other than margin debt.

The November and December 1999 reference of margin debt in the article is not shown in the chart. The Nasdaq dropped 78% from its high in March 2000 and took 15 years and lots of QE and 0% to get back to its old high. The S&P 500 dropped 50% and took 13 years and lots of QE and 0% to go past its March 2000 high.

But those are the index values. If you owned individual stocks, and not the incices: Thousands of stocks were either zeroed out and became worthless or were bought for a few cents to a couple of bucks and then vanished.

Many investors who were margined were completely wiped out, with essentially nothing left in their accounts.

But yes, no one invested in a market like this takes any warnings about a market like this seriously. That’s why these kinds of markets can exist – until they can’t.

Investors in 1999 and 2000 didn’t have the guaranteed store of wealth that they do today: crypto.

A permanently high plateau of a permanently high plateau.

/sarc

Traditional measures of liquidity and Fed-type mechanics seem impossibly disconnected from reality, probably because society is not what it used to be.

Quantifying the behavior of the casino crowd at this stage is an exercise in futility — more so, with a casino-brained president.

Obviously lots of shocks within the last 10 years or more have accumulated into a new form of group thinking, and a new attitude towards risk and future value. The generational refinement of investing behavior has been highly modified by pandemic YOLO and FOMO, which is amplified by 0dte and Ai — which have changed global behaviors.

The Fed or any organization that uses 100 year old models to measure these new dynamics won’t capture the current level of insanity.

Nonetheless, I just looked at a chart, comparing GameStop to the UST 3m, out of curiosity — and surprisingly, GME stopped rocketing as soon as the Fed started hiking in 2022.

According to chart, from October 22 to now, GME performance is negative 7% — and apparently 3mT up 32%.

In a way, that almost represents the reality of short term speculation and meme spikes, versus longer term outcomes, after the fun.

In the bigger picture markets, maybe that’s similar too, in that these deceptive restrictive rates, which don’t seem useful — or delayed, are dynamics that unfold over longer time horizons.

I keep beating the drum, suggesting tariff impacts are currently delayed, and we’re nor gonna see reality until Christmas — in any case, shorter term euphoria often looks different a year or two later, for almost everything.

Buy a 6% BB-rated bond that’s been trading stable for the last year on good economic data or buy a 4.4% treasury that’s going to lose value as soon as the debt limit is raised? The narrow spread is not surprising. It’s a fiscal problem, not a monetary one.

That makes absolutely no sense. If the 4.4% treasury loses value (that is, prices drop and yields go up) for whatever reason, the 6% BB bond will almost definitely lose value too, for the same reason.

Correct. So it seems worth repeating here that there are two primary risks with bonds:

1. credit risk (probability of default)

2. interest rate risk (probability market yields will rise)

Treasuries have essentially zero credit risk; junk bonds have a substantial credit risk. That’s their main difference, which is what the spread is supposed to compensate investors for.

Both have essentially the same interest rate risk.

So…

The risk you take on with Treasury securities is interest rate risk.

The risks you take on with junk bonds is interest rate risk PLUS credit risk.

“Depth Charge

Feb 8, 2023 at 3:03 am

“If I were Powell, I’d be getting the willies just about now.”

Yet when I was calling for the FED to continue with their 75 basis point rate hikes until they reach the rate of CPI I’m accused of “just wanting to burn it all down.” Now look, they’re falling behind.

The fact is that the FED blew it by quickly ratcheting back to 25 basis point hikes, especially given what’s transpired since September. All of the signs were there, they just ignored them. There is absolutely no good reason why they didn’t do 50 basis points last meeting. Just an abysmal failure of a job.

I contend that the FED is playing a role of fake tough guy on inflation, with the actual goal of hyperinflating the price of all assets permanently. There’s no way they’re as incompetent as they’re acting. They know that the longer they string out this inflation, the higher prices will be in the end.”

I called all of this years ago. They are intentionally blowing the biggest asset hyperbubble in history, and trying to make it stick.

When they first “paused,” I immediately stated that asset prices would be setting new highs, yet was told that there was no way that could happen because their rates were “restrictive.” Nope. This whole outcome was so obvious that Ray Charles saw it coming.

Your Ray Charles joke ruins what might otherwise be a post with arguments worth considering. The joke implies you have poor judgment and instead just want to be provocative.

Pfffft. Cry harder.

“with their 75 basis point rate hikes until they reach the rate of CPI”

They blew threw the rate of CPI with their rate hike in May 2023 to 5.0%-5.25%, while CPI had dropped to 4.9%. And CPI continued to drop, eventually reaching a low of 2.3% in April.

Depth

Yep. Too slow to raise. And didnt raise enough.

How can Trump and clowns like Jim Cramer call ….SCREAM for rate cuts when Gold, Stocks, and nearly everything else at all time highs?

Greedy…….and apparently fully invested.

Exactly. Selfish, rapacious greed with zero regard for the future of the country and the young.

Some finance writers say margin debt doesn’t matter as much as option notional values these days. Is that true? (Or does option notional still end up reflecting in margin debt somehow… e.g. the market makers hedge their options exposure with futures that increase their margin debt?)

Just read that Jim Cramer had a bit of a meltdown about rates on TV again – the last time back in ’08 I think he was onto something in terms of his WS buddies opening their office windows. Maybe without a constant promise of cheaper and cheaper money even at ATH the whole bubble is about to explode. These guys want permanent ZIRP so that everything doubles in price every three or four years. Even +10% a year is no longer enough to keep the plates spinning.

Powell has cut QT to nearly ZERO. A $50B shot of liquidity into the economy that should be absorbed.

Obscene

The 20s are roaring, baby.

‘including with cryptos where another mania is in full swing.’

Juiced by the executive branch of govt that is beyond crypto friendly to the point of being a participant.

Fossil fuels, crypto, and law enforcement are the main winners in this admin so far.

Great article. Thank you. Little to none of this info. in the financial MSM, or elsewhere. I agree that financial conditions are “loose.” Your Exhibit A and B are clear examples of this, as are ATH stonk market valuations, by most all metrics (Buffet indiator, CAPE, etc.). Stonk market only goes up since the 2008-2009 GFC. 16 years. Stonk market = the economy. Must not crash. Hence, fiscal dominance (high deficit fiscal spending), else, recession. Must prevent recessions now. No “creative destruction” allowed. Central planning rules, comrade! We’re all Socialists (Communists) now. So much for Adam Smith’s “invisible hand”… However, asset bubbles always burst (J. Grantham). The Everything Bubble in search of a pin.

Gambling (“investing”) is near all time highs. That does not reflect the real economy. Those zombie companies would never be able to refinance at those junk bond rates. Rates for small commercial loans are also much higher, same with personal loans, mortgage rates, credit card rates. It looks like the speculators are less betting on Fed cuts, but more on another round of QE.

Or, they’re betting on everyone else thinking there will be another round of QE, and therefore, prices will never fall. A sort of positive feedback loop, caused by QE hopium and greater fools investing.

👍

I am hoping that Congressman Marjorie Taylor Greene’s proposal to make the sale of a primary residence exempt from capital gains taxes becomes law. It would free up housing in high cost metro areas around the country. I have been in my place since before Prop. 13 passed in 1978. Several homes in my neighborhood sit empty while families wait for heir older relatives to die and pass the property to them without capital gains taxes.

The solution to that isn’t to eliminate the capital gains tax on primary residences. The solution is to eliminate the “basis step up” upon death. That never made any logical sense to begin with.

That would be a recipe for disaster. Housing would become way more unaffordable, because all the gamblers would then flood the market and buy up even more houses in hope of tax free gains. It would be more helpful to tax houses sitting empty in areas with high demand. That certainly would speed up turnover.

If they are going to give away more tax benefits, it should go towards builders who can permanently increase supply. A gain exclusion to sellers would only temporarily increase inventory, while increasing wealth concentration. Remember, in order to benefit you’d have to be sitting on a $500k housing gain. Why do such people deserve to be subsidized by people who are not fortunate enough to have such gains?

In 1997, the Taxpayer Relief Act changed the capital gains tax treatment of houses, to allow 500K to be excluded from taxing for joint filers (250K for other filers). That appears to me to be the point where the first housing bubble started, the Case Shiller slope changed (FRED has the Case Shiller chart going back to the 90s). The 90s was period was one of muted house price gains and the tech bubble was gaining steam.

Today, the context is different – the prior period had elements of a housing mania (e.g. “offers due by 5pm Friday”) with low interest rates, as one significant difference.

I suspect an elimination of housing capital gains taxes could well give housing another leg up, based on that experience, but perhaps not as explosive as the first housing bubble.

If the current stock bubble implodes and they start pushing interest rates down, I think that could again stoke home prices. But the context again is different now so the only question IMO would be not that it would accelerate the housing market (it would) in terms of sales and prices but by how much.

I’ve taken the article’s position for years now. The current interest rate might be restrictive over a 20 year period, but it’s not restrictive enough to calm asset and CPI inflation over a period that is reasonable to most people. If you want to tackle the beast, you need rates restrictive enough to remove a few degrees of speculation from markets. And yes, that means considering asset prices levels as part of interest rate policy.

The Fed totally ignored asset price inflation for decades, and that’s why we are in this mess.

The best course from here is to let market forces take some corrective action, and if that means a higher rate of unemployment until asset prices settle at a lower level, so be it.

Sp 500 priced in yen closed at its triple top. Yen carry trade is a world wide phenomenon, the world borrowed yen and invested a big chunk of that carry in US equities. The yen fell hard today and we hit triple top resistance price. It’s crazy town as wolf pointed out. Maybe Yen bounce would force the carry trade crowd to sell at or near the high water mark priced in yen for SP 500, professionals egos love to profit at the peak before a downturn. Or everything can keep going higher LOL, crazy town. No clue what will happen :) it’s liberating feeling being free from the delusional rational mind. If yen keeps dropping historically that would be bullish. But who knows what will happen next except maybe the master Algo or whoever programmed it.

You admit this much – “ Parts of commercial real estate are in a depression, and the housing resale market has frozen.” Wow. I’m surprised. If parts of commercial real estate are IN a depression, LOTS OF PEOPLE are going to lose a LOT of money! It’s also a sign that many businesses have either closed, scaled back or laid off workers. All bad signs, and bad signs that will eventually be reflected in the massively overvalued real estate markets. Yes, many housing markets have corrected some, but much more punishment is coming. This upcoming event may end up making the Great Depression seem like a walk through Central Park.

“You admit this much – “ Parts of commercial real estate are in a depression, and the housing resale market has frozen.” Wow. I’m surprised. If parts of commercial real estate are IN a depression…”

🤣❤️ Did you EVER read anything here??? Or first-time reader here? I’ve been writing about it for three years, article after article: spiking default rates, spiking vacancy rates, foreclosure sales, huge losses for lenders, wipeouts of landlords, office towers selling for 30 cents on the dollar, everything, right here in this category:

https://wolfstreet.com/category/all/commercial-property/

And NOTHING has happened to the broader US economy, LOL