Metros with YoY price drops double to 14: Austin, Tampa, San Antonio, Phoenix, Dallas, Orlando, Atlanta, Miami, Denver, Raleigh, Houston, Birmingham, Charlotte. YoY gains narrow sharply in San Diego, Los Angeles, Boston, Chicago, New York, Philadelphia, Columbus… 20 below 2022 peaks.

By Wolf Richter for WOLF STREET.

March is the time of the year – the spring selling season – when home prices in many markets rise sharply after declining during the winter, and they did so a year ago.

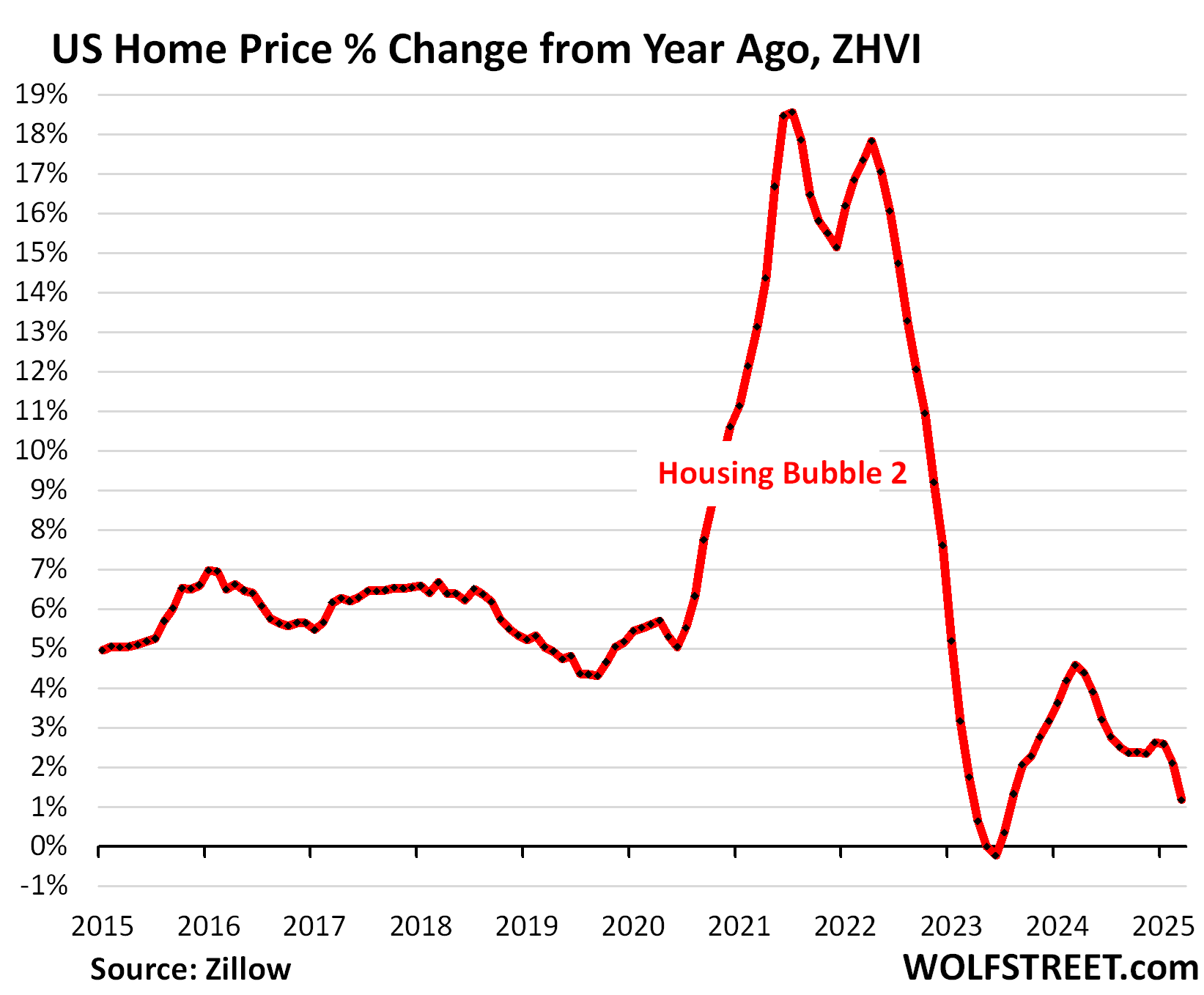

But this March, prices of single-family houses, condos, and co-ops across the US rose only 0.2% from February. A year ago, they’d jumped by 1.1% in March from February.

This small month-to-month price increase in March caused the year-over-year price gain for homes that sold in March to get whittled down to 1.1% overall, from 2.1% in February. A year ago, the YoY price gains were in 4.5% range. During the peak of Housing Bubble 2 in mid-2021, YoY gains exceeded 18%.

Similar scenarios played out in all of the 33 metros here: Month-to-month gains in March – if any… Miami and others had declines – were a lot smaller than a year earlier.

Those markets with YoY price declines in February saw these YoY declines widen in March. Seven of those that still had YoY gains in February flipped to YoY declines in March. And others saw their YoY gains narrow, in some cases to near-nothing, such as San Diego.

All data here is from the “raw” mid-tier Zillow Home Value Index (ZHVI). The ZHVI is based on millions of data points in Zillow’s “Database of All Homes,” including from public records (tax data), MLS, brokerages, local Realtor Associations, real-estate agents, and households across the US. It includes pricing data for off-market deals and for-sale-by-owner deals. Zillow’s Database of All Homes also has sales-pairs data. The index is not seasonally adjusted.

The 33 Most Splendid Housing Bubbles.

Here we track the prices of single-family houses, condos, and co-ops in 33 large Metropolitan Statistical Areas (MSAs). To qualify for this list, the MSA must be one of the largest by population, and must have had a ZHVI of at least $300,000 somewhere along the line.

The metros of New Orleans, Oklahoma City, Tulsa, Cincinnati, Pittsburgh, etc. don’t qualify for this list because their ZHVI has never reached $300,000, despite the massive surge of home prices in recent years, but from low levels.

Down year-over-year: The group of the 33 metros here whose prices declined year-over-year keeps growing. In March, 14 of these 33 metros had year-over-year declines, up from 7 metros in February.

The 14 metros with year-over-year price declines:

- Austin: -4.6%

- Tampa: -4.5%

- San Antonio: -2.7%

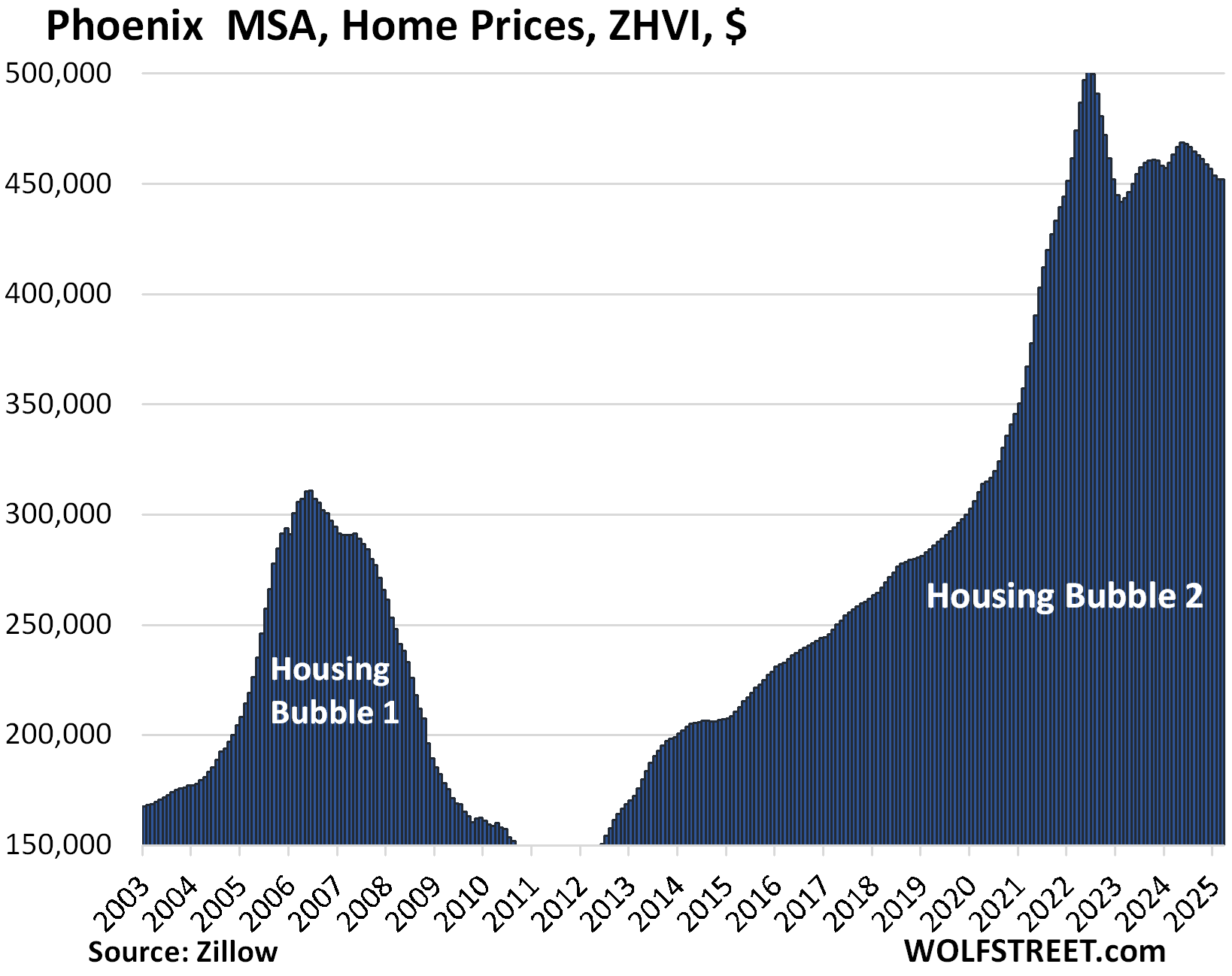

- Phoenix: -2.5%

- Dallas: -2.4%

- Orlando: -2.2%

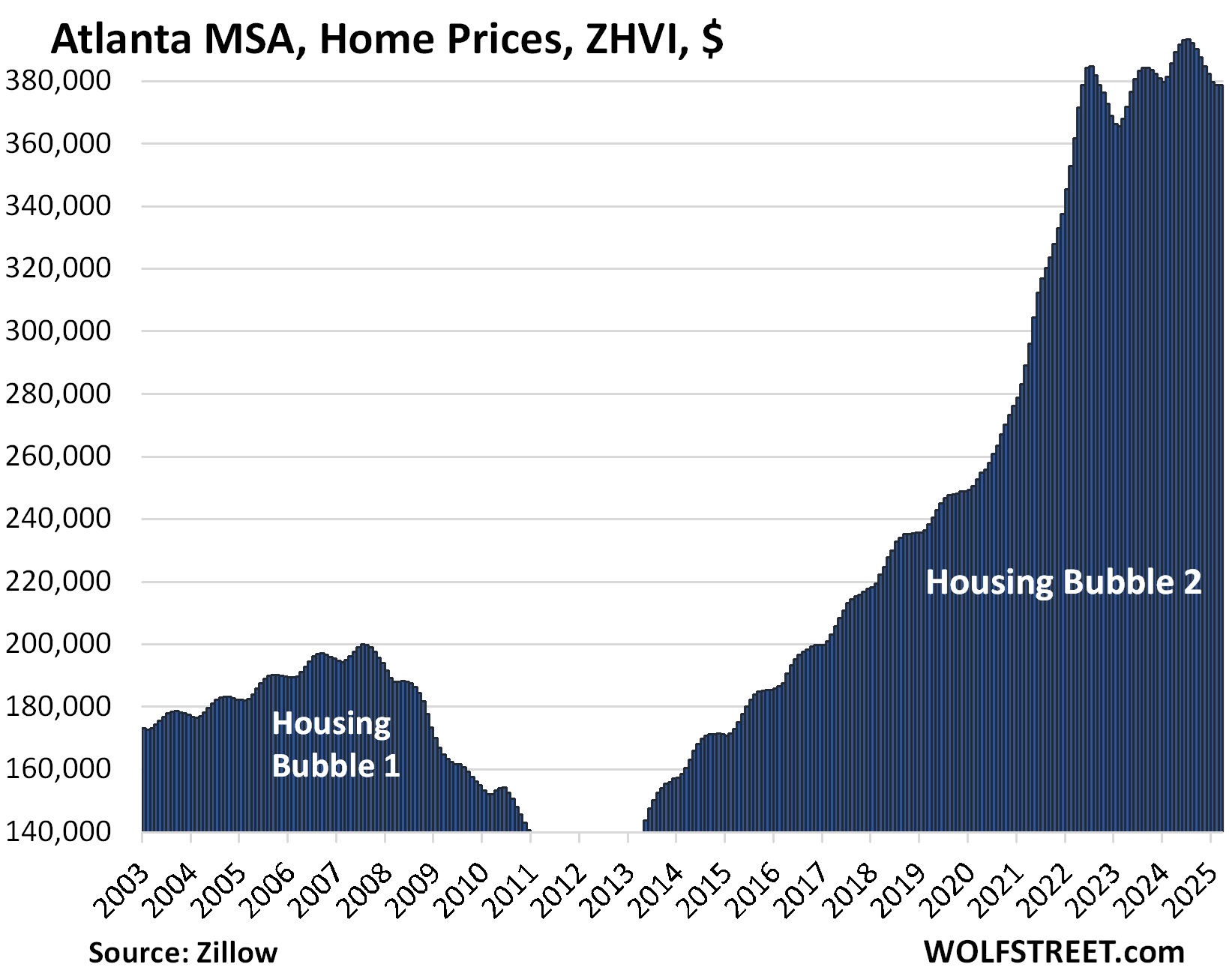

- Atlanta: -1.8%

- Miami: -1.5%

- Denver: -1.1%

- Raleigh: -1.0%

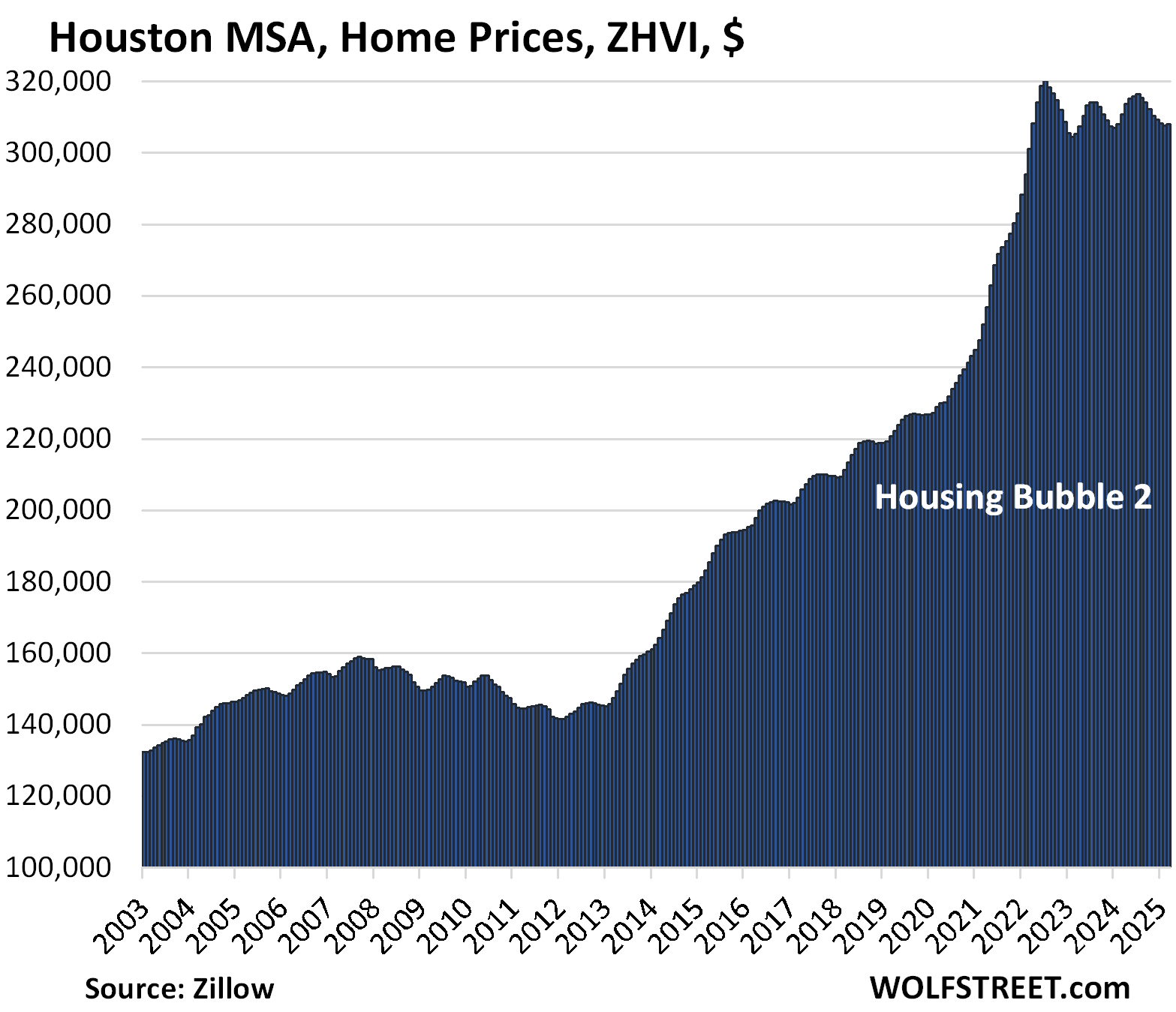

- Houston: -0.9%

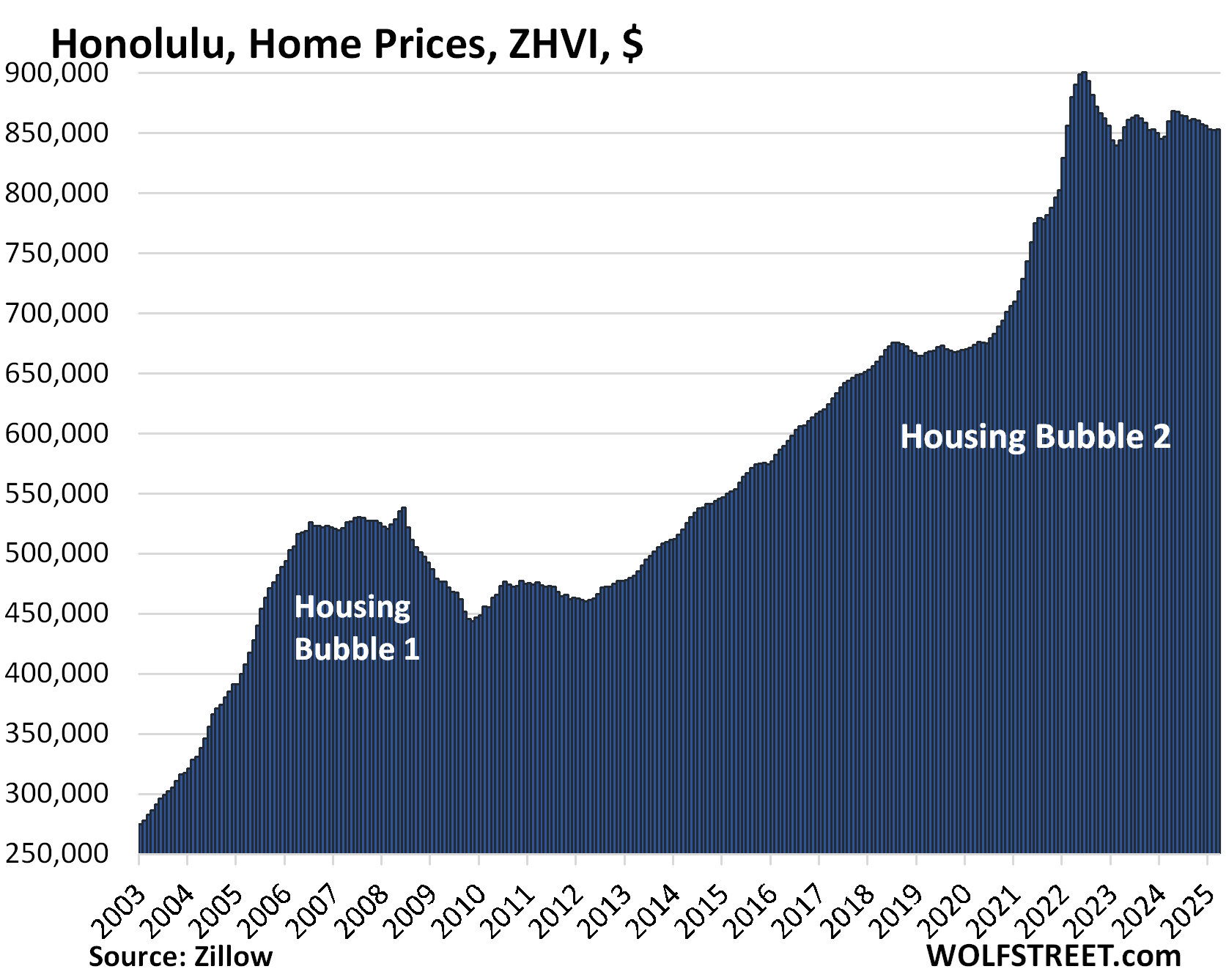

- Honolulu: -0.8%

- Birmingham: -0.3%

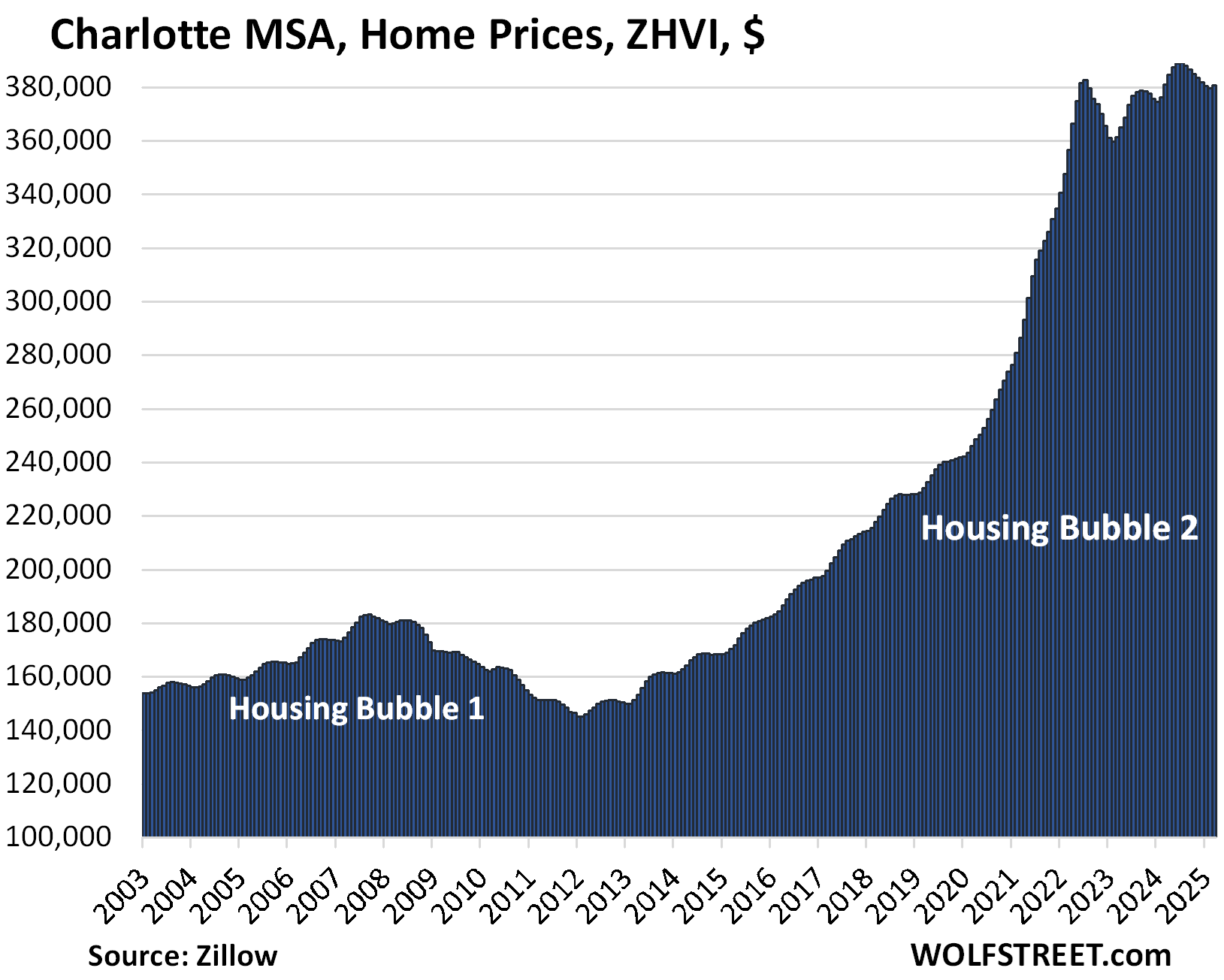

- Charlotte: -0.1%

Down from the 2022 peaks: Prices in 20 metros of our 33 metros are down from their 2022 peaks, led by the metros of:

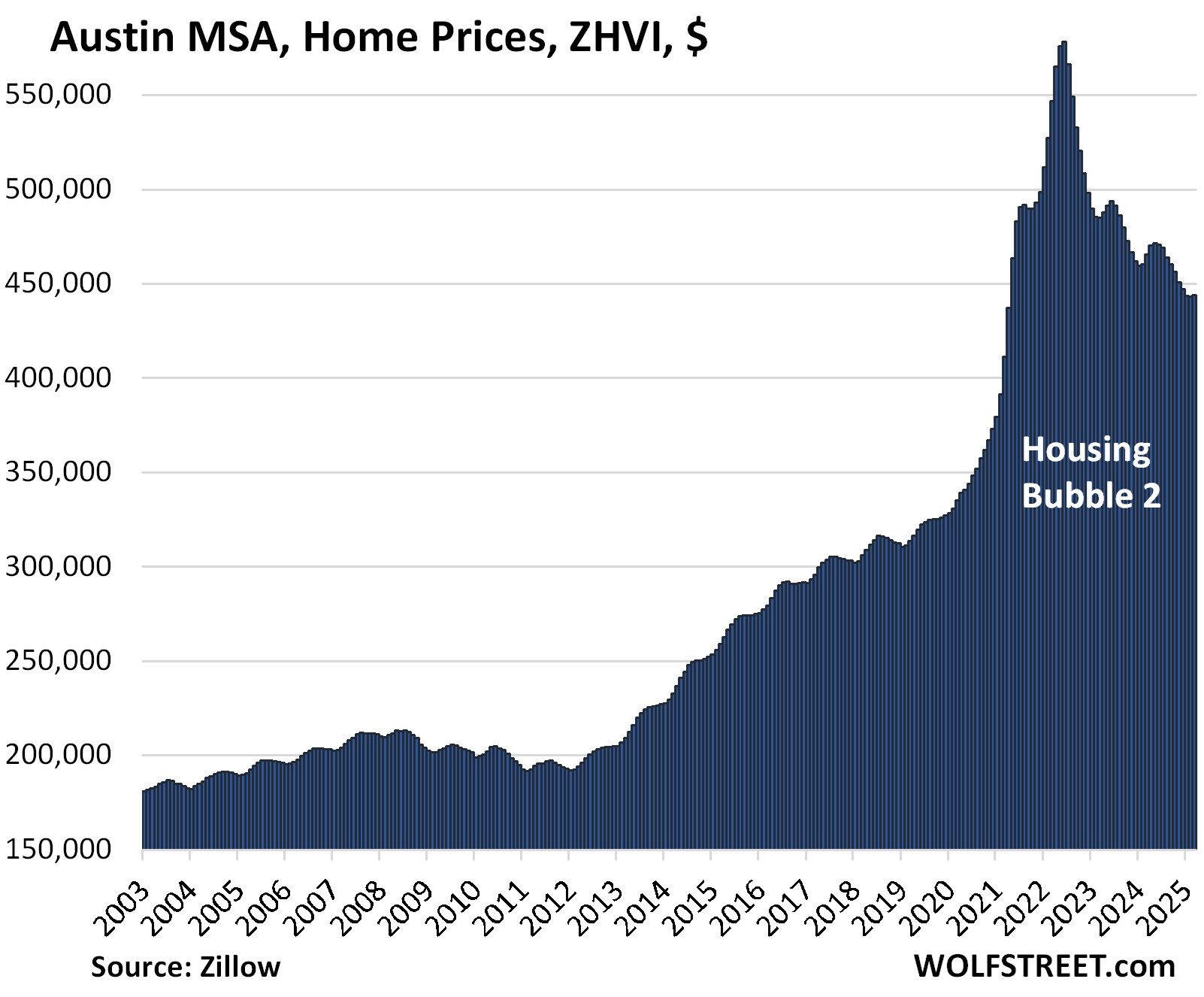

- Austin: -23.2%

- Phoenix: -10.2%

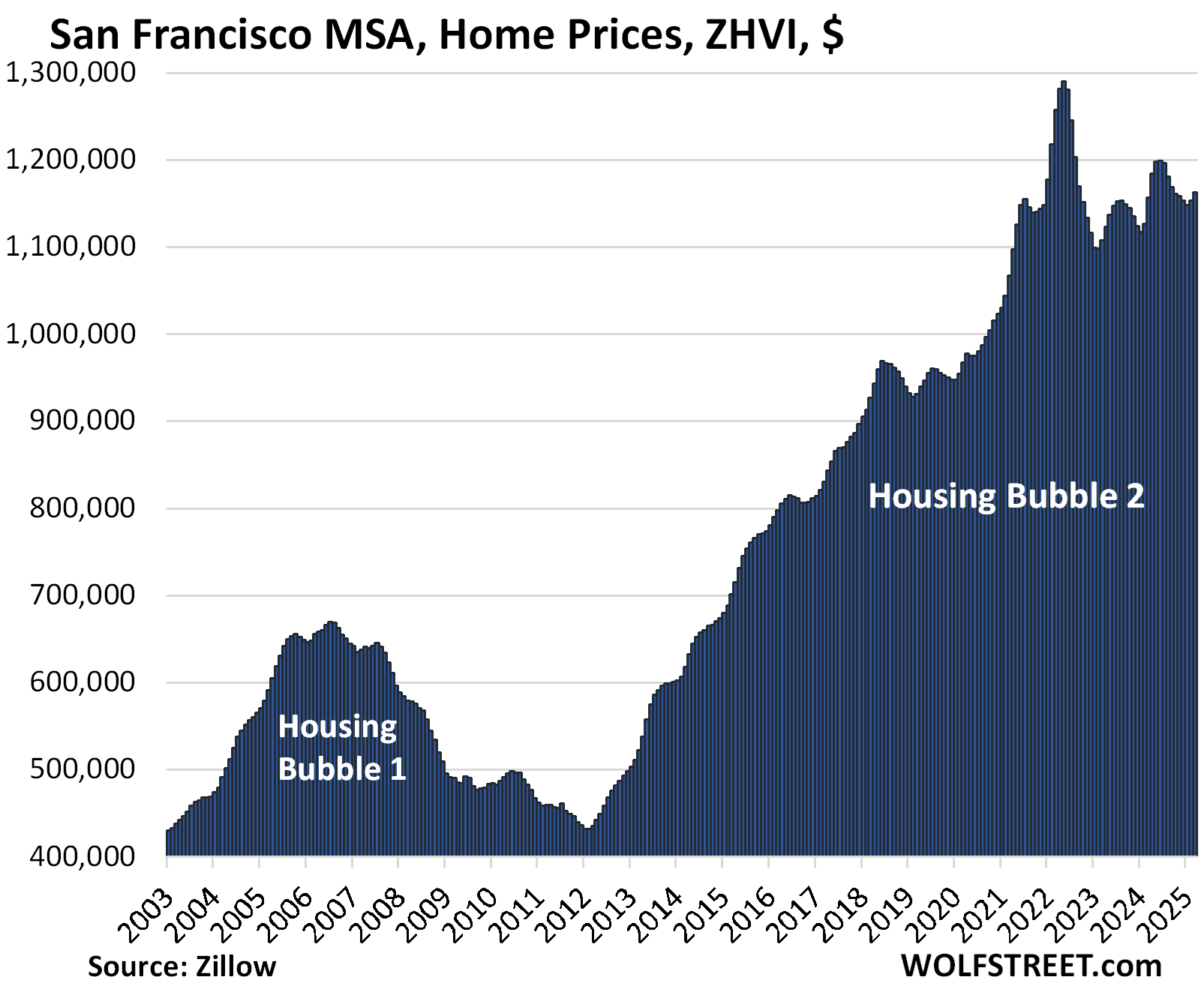

- San Francisco: -10.8%

- San Antonio: -9.4%

- Denver: -7.9%.

Home prices exploded through mid-2022, fueled by the Fed’s interest rate repression and QE, resulting in below-3% mortgages. But the Fed hiked rates starting in 2022 and has shed $2.2 trillion in assets through QT. Mortgage rates have been above 6% since September 2022 and over 7% for some of that time. Prices are now simply too high after spiking like this, and demand has plunged.

The 20 metros that are below their highs of mid-2022.

| Austin MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -23.2% | 0.2% | -4.6% | 154% |

The YoY decline worsened from -3.8% in February. Prices are back where they’d been in April 2021.

The Austin MSA includes the counties of Travis (Austin-Round Rock), Williamson, Hays, Caldwell, and Bastrop.

| Phoenix MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -10.2% | 0.0% | -2.5% | 216% |

The YoY decline worsened from -1.6% in February. Prices are back where they’d first been in January 2022:

| San Francisco MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -9.8% | 0.9% | 0.5% | 293% |

In February, the YoY increase was still +2.4%.

The MSA includes San Francisco, Oakland, much of the East Bay, much of the North Bay, and goes south on the Peninsula into Silicon Valley through San Mateo County.

Prices are roughly where they’d first been in June 2021.

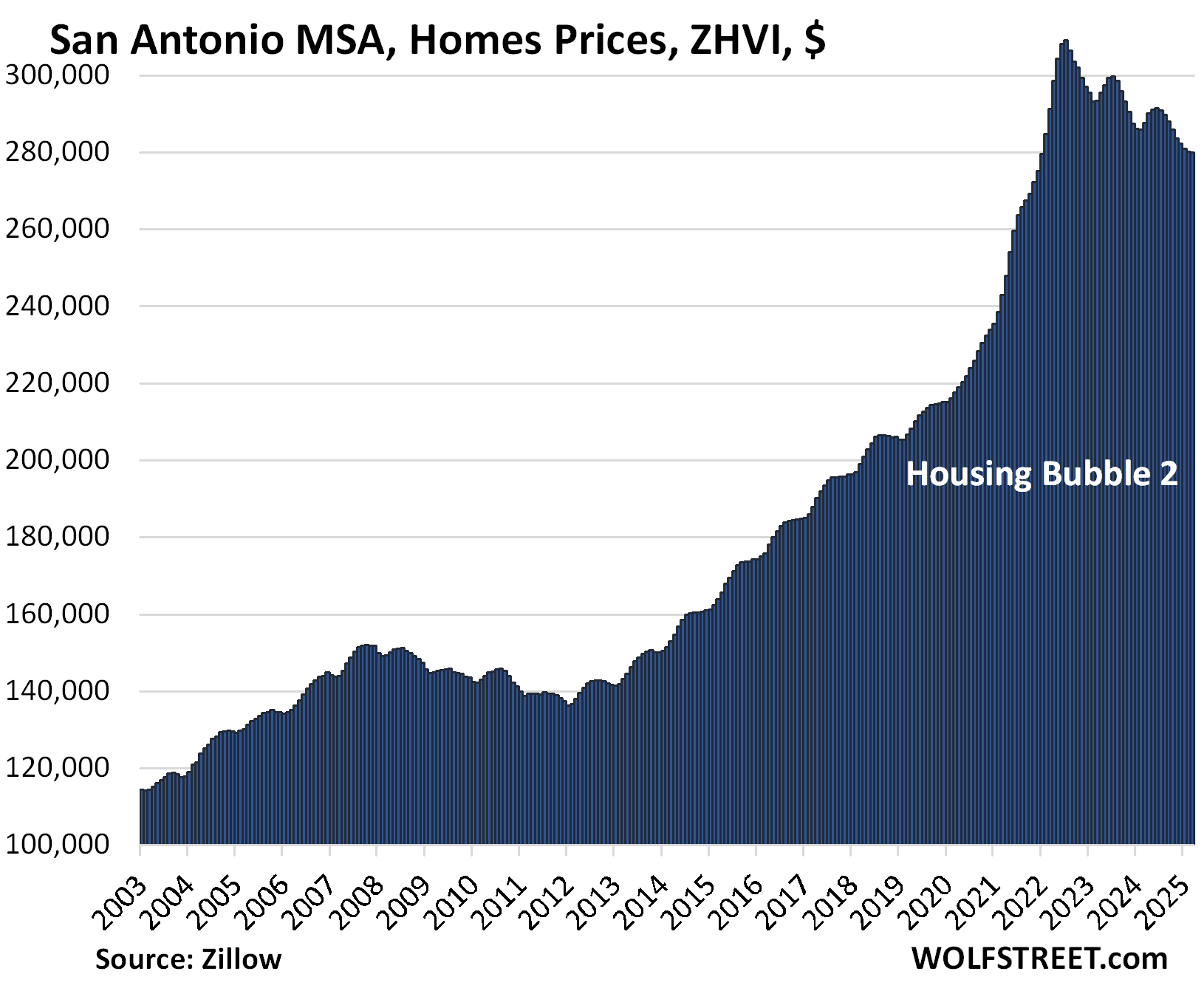

| San Antonio MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -9.4% | -0.1% | -2.7% | 145.4% |

The YoY decline worsened from -2.0% in February. Prices have dropped to the lowest level since January 2022.

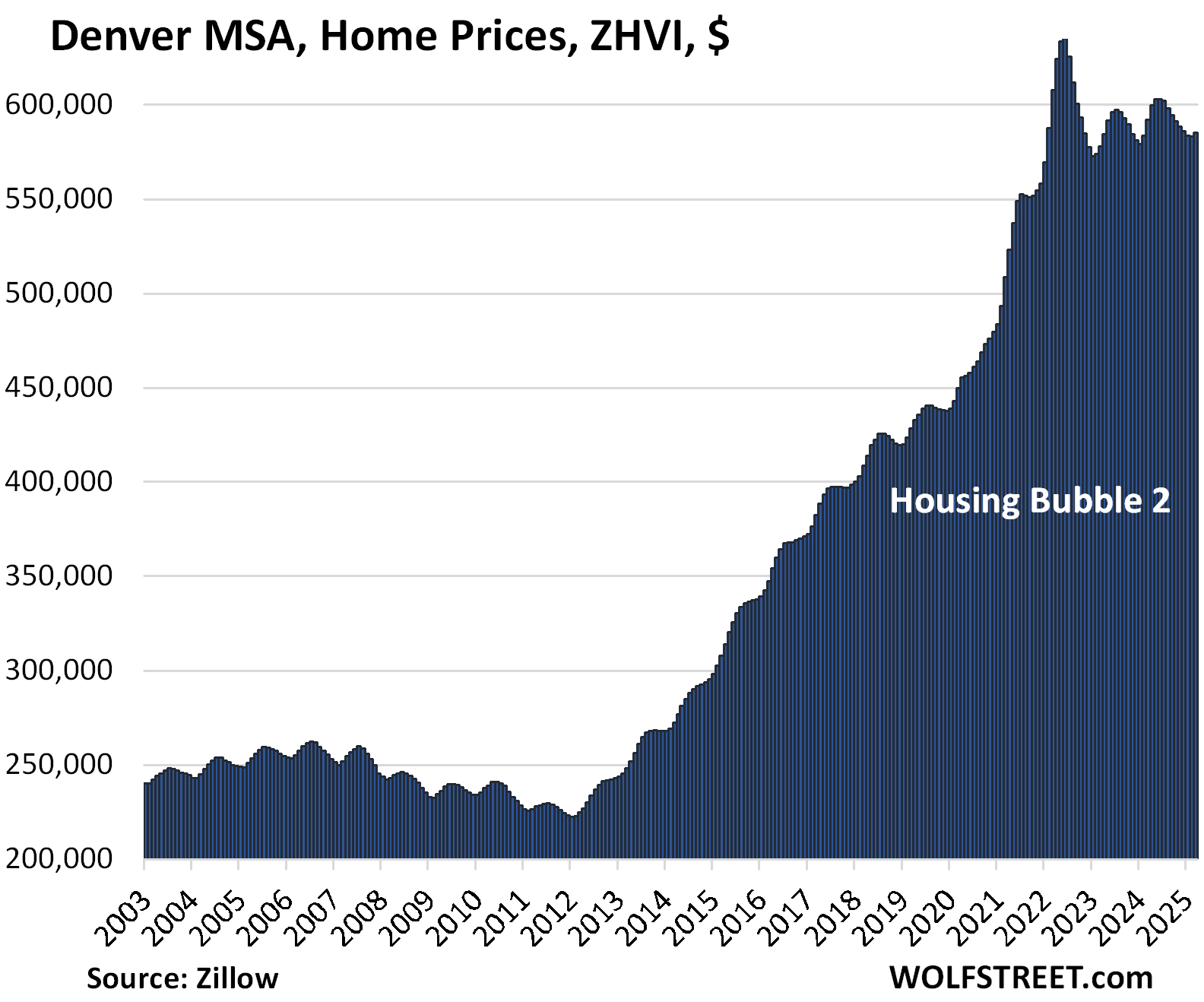

| Denver MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -7.9% | 0.4% | -1.1% | 211% |

The YoY decline worsened from 0% in February. Prices are back where they’d first been in February 2022.

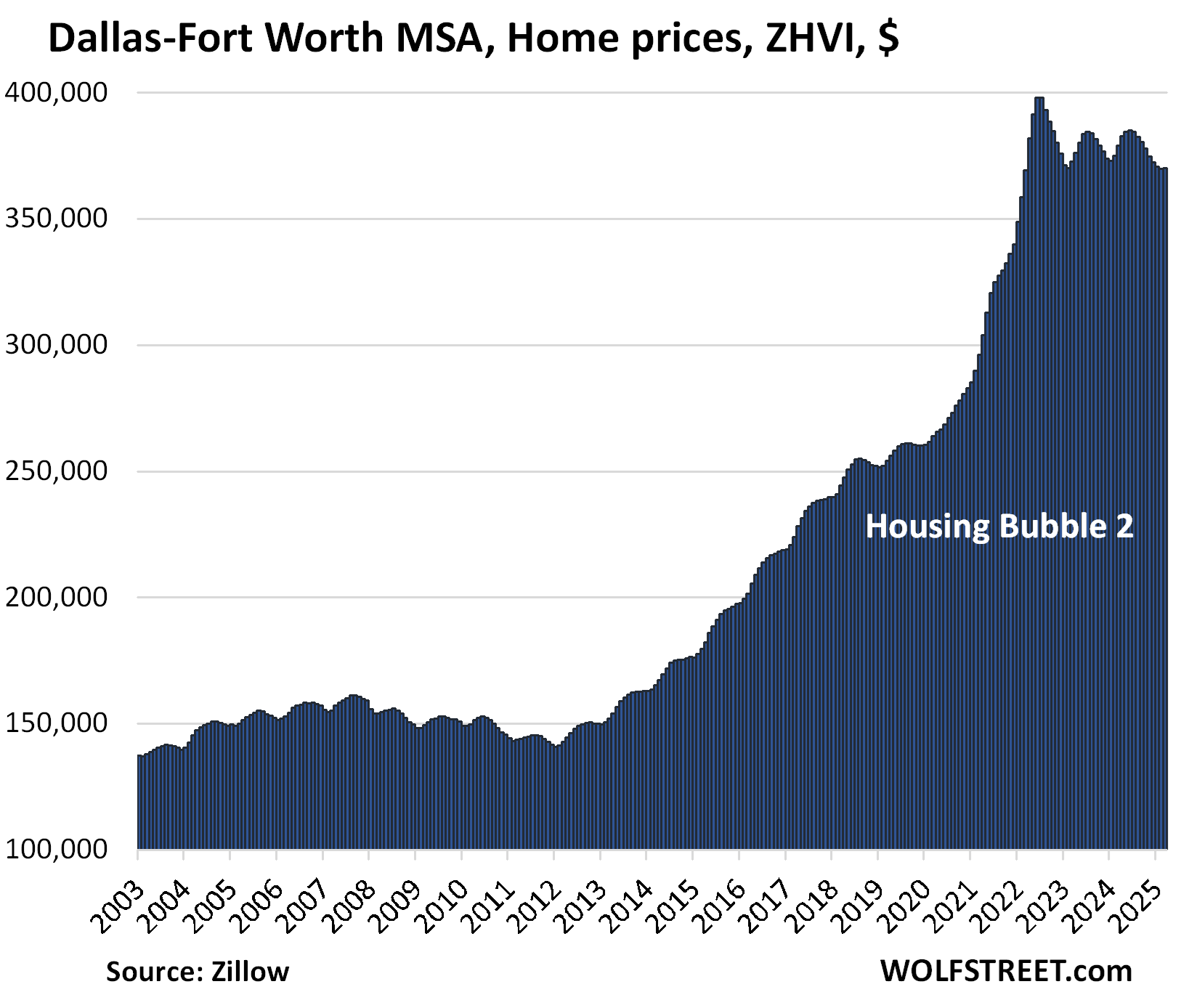

| Dallas-Fort Worth MSA, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -7.0% | 0.1% | -2.4% | 190% |

The YoY drop worsened from -1.4% in February.

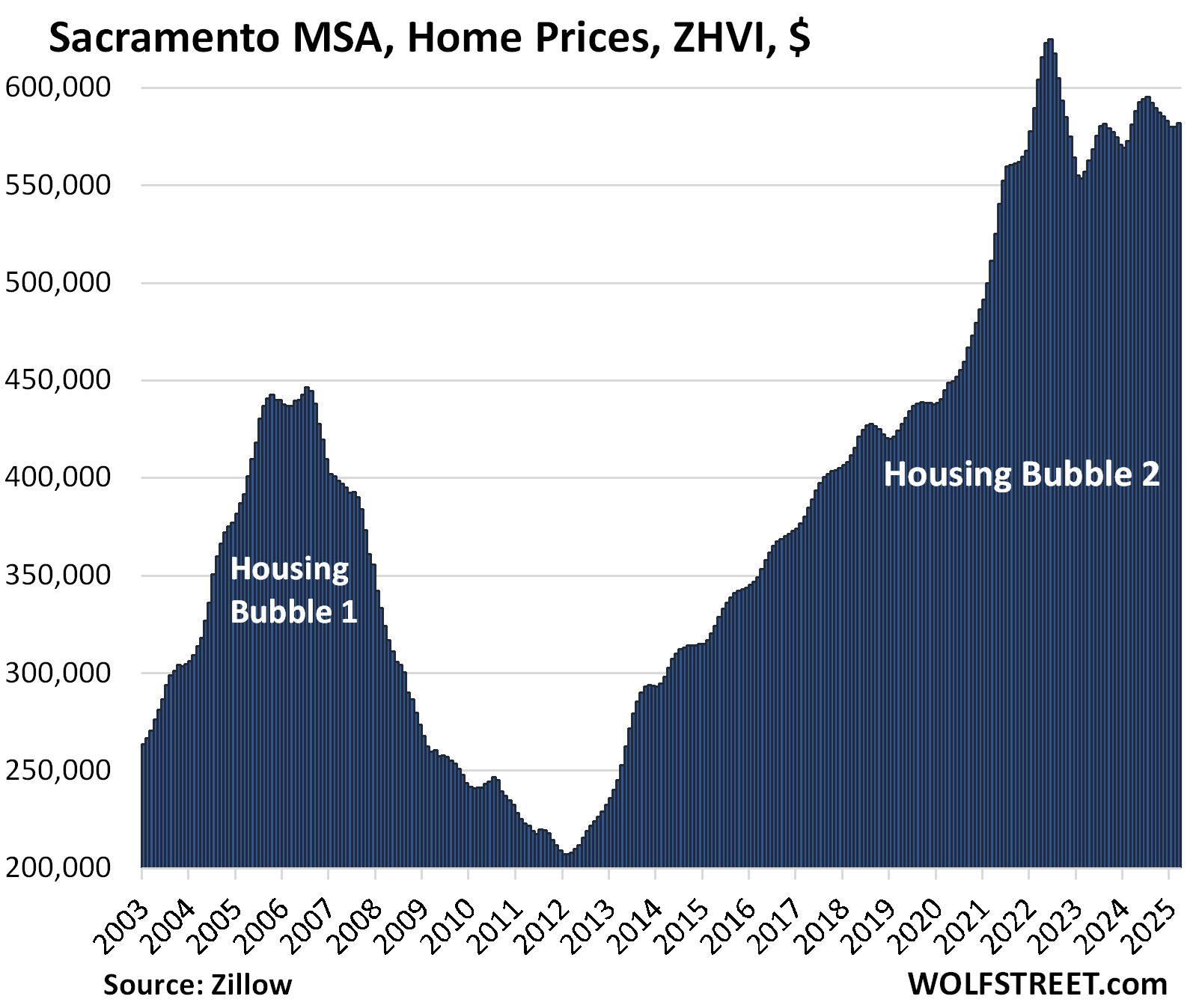

| Sacramento MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -6.9% | 0.3% | 0.1% | 244.0% |

February’s YoY gain of 1.3% nearly vanished in March.

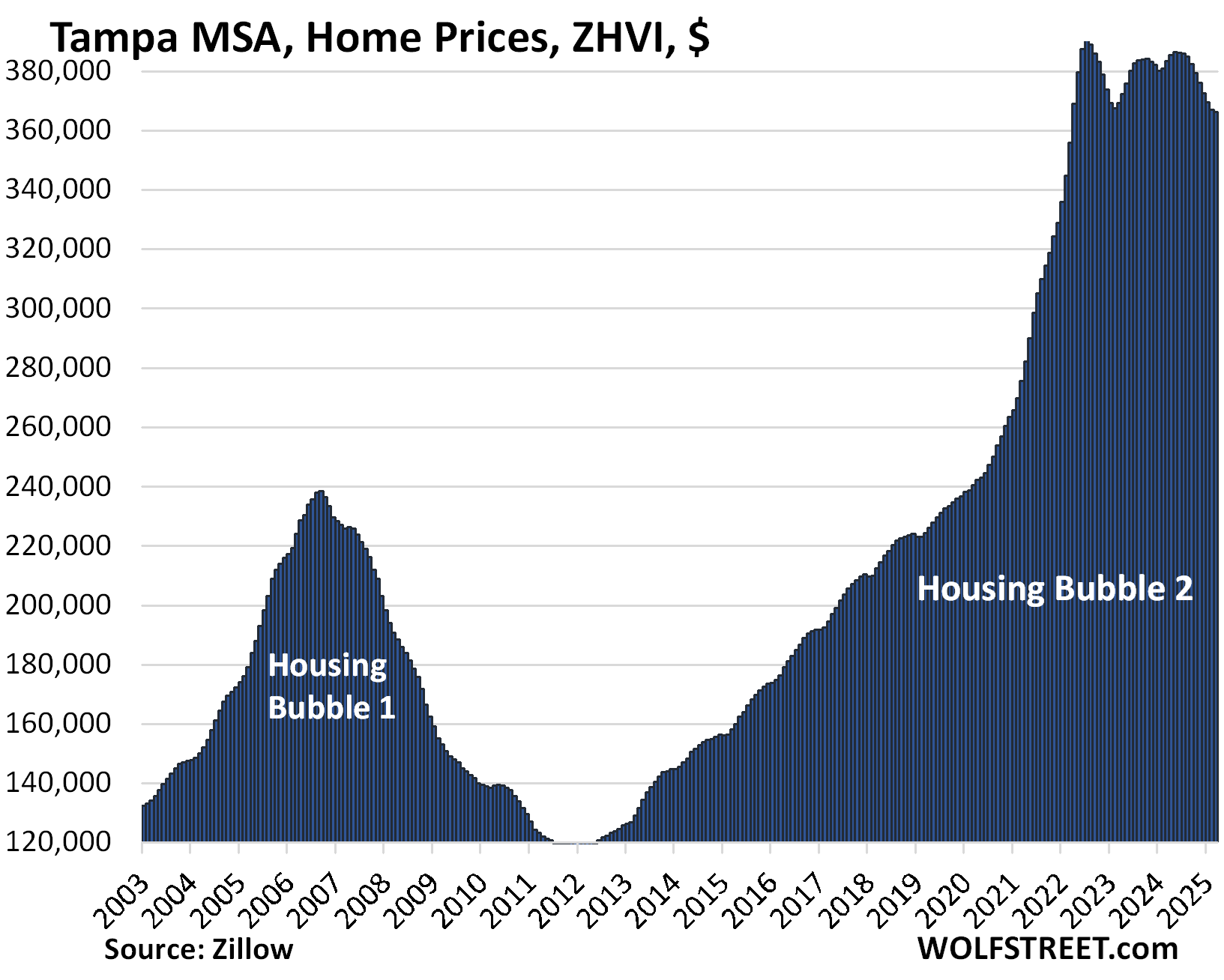

| Tampa MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -6.2% | -0.3% | -4.5% | 261% |

The YoY drop worsened from -3.6% in February.

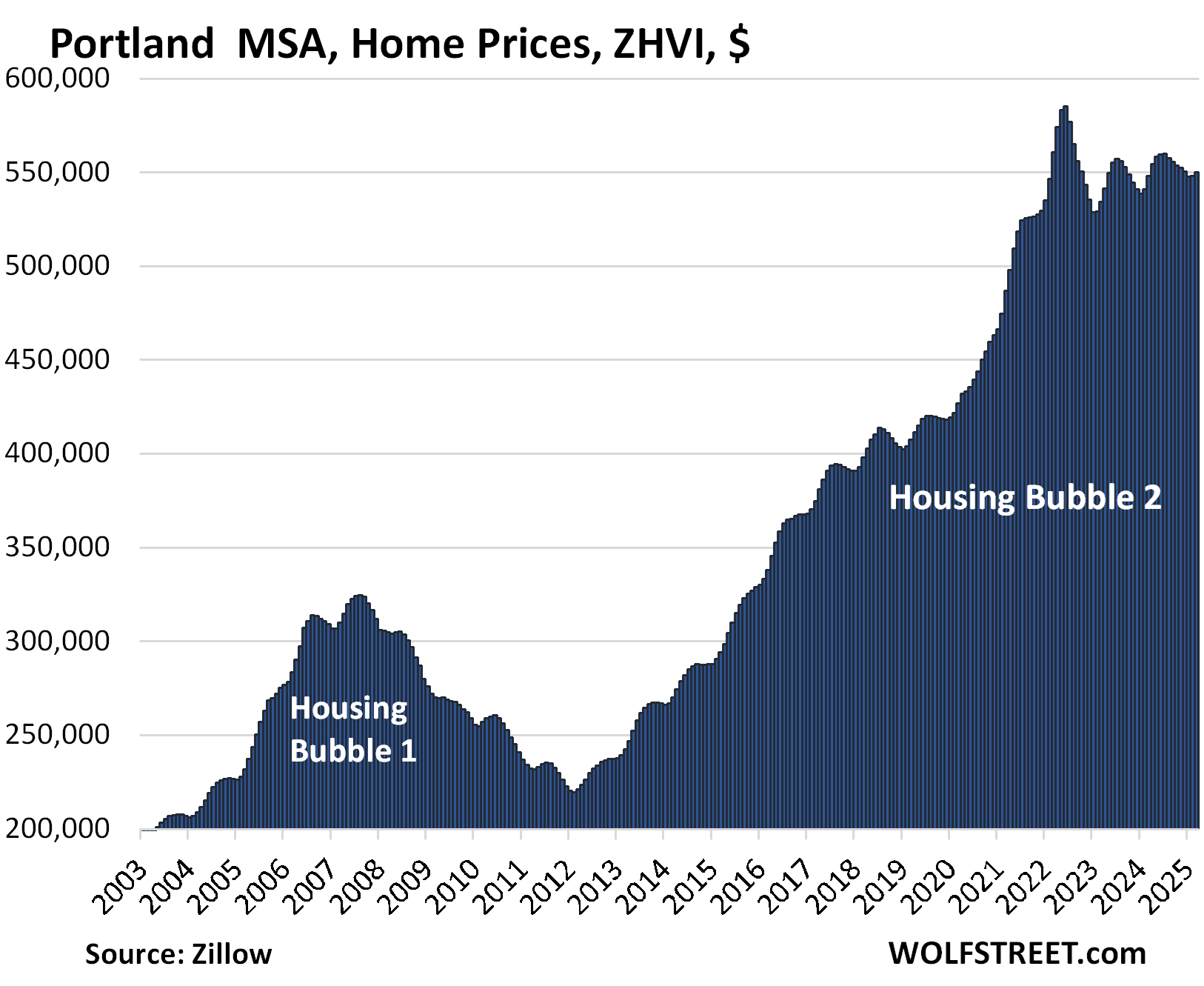

| Portland MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -6.0% | 0.3% | 0.3% | 217% |

In February, the YoY gain was +1.3%. Prices are back where they’d first been in January 2022.

| Honolulu, Home Prices | |||

| From Jun 2022 peak | MoM | YoY | Since 2000 |

| -5.3% | 0.0% | -0.8% | 278% |

The YoY gain in February of +0.6% flipped to a YoY loss in March.

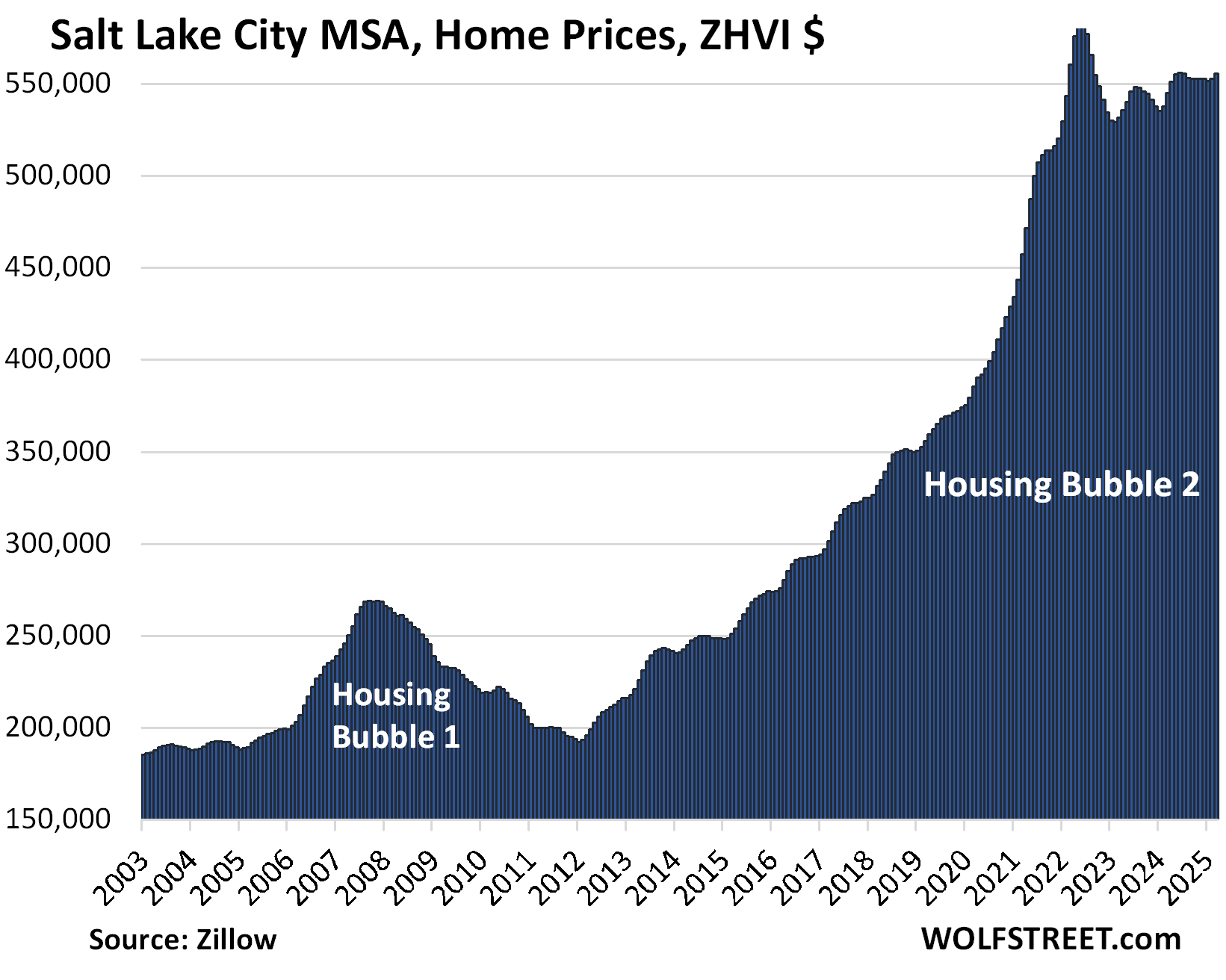

| Salt Lake City MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -5.2% | 0.6% | 2.0% | 216% |

In February, the YoY gain was +2.7%. Prices are back where they’d first been in March 2022.

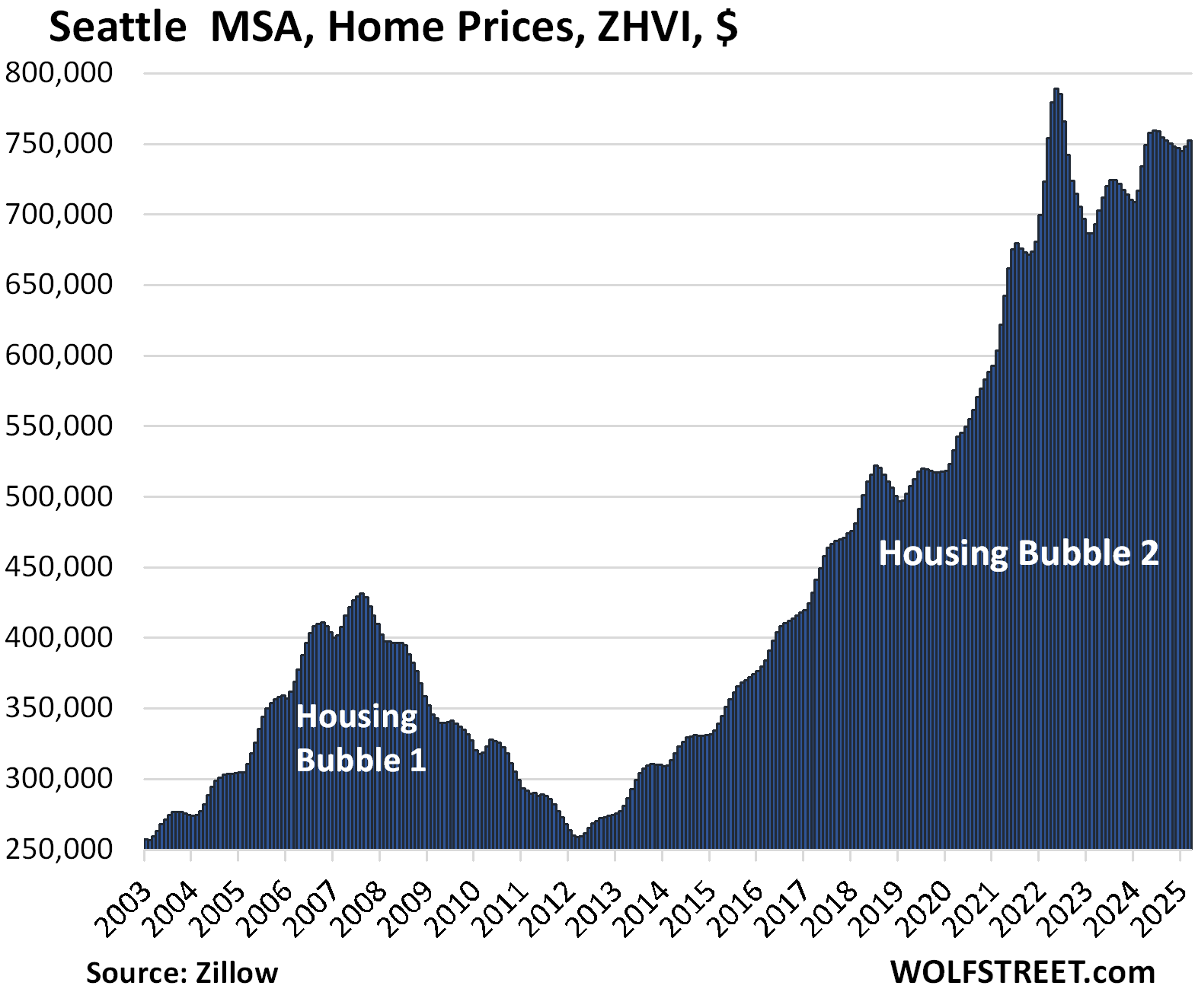

| Seattle MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -4.7% | 0.6% | 2.4% | 240% |

The YoY gain in February was +4.3%.

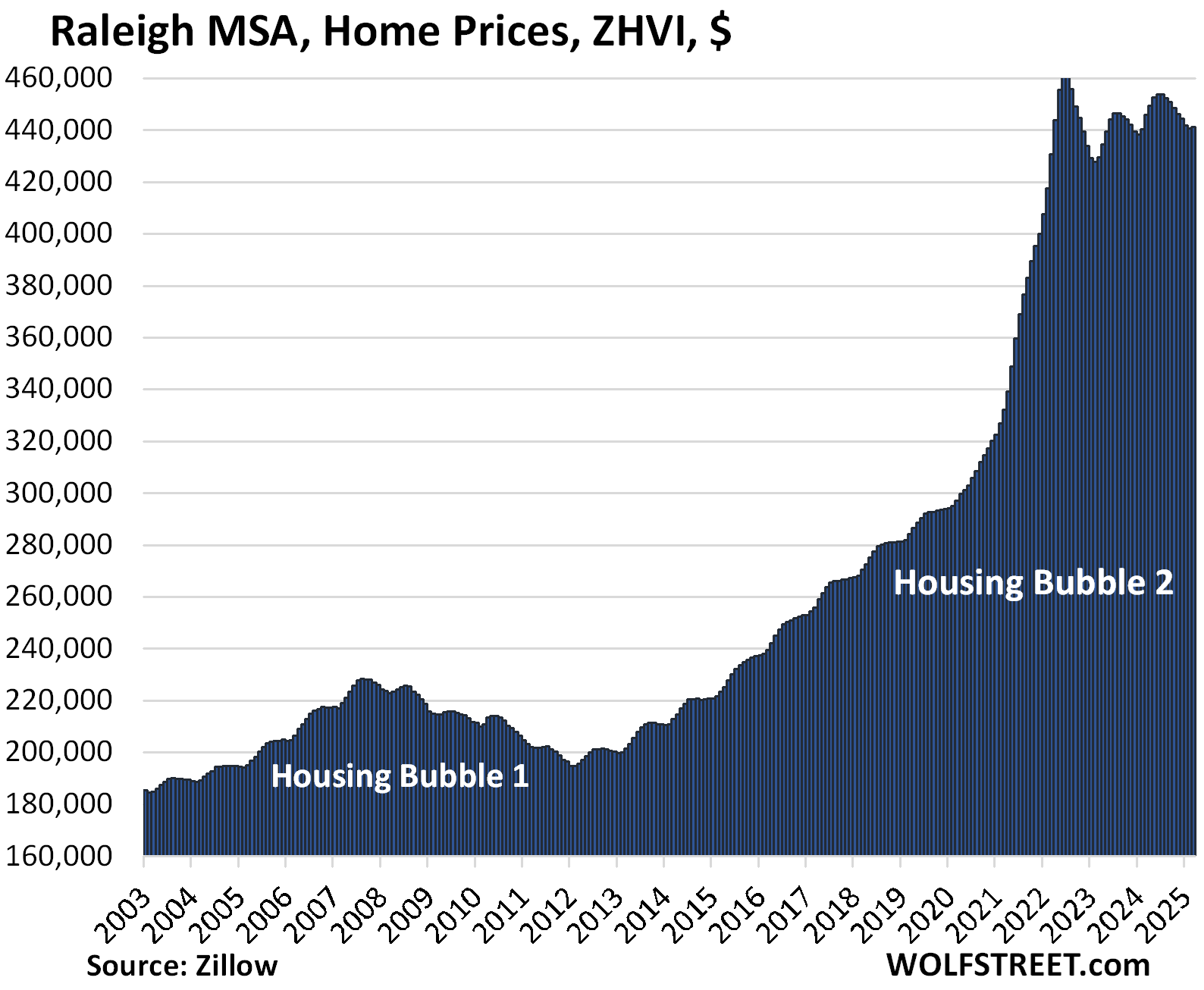

| Raleigh MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -4.5% | 0.2% | -1.0% | 156% |

A deterioration from February’s YoY 0%.

| Houston MSA, Home Prices | |||

| From Jul 2022 peak | MoM | YoY | Since 2000 |

| -3.8% | 0.1% | -0.9% | 149% |

The YoY decline worsened from -0.2% in February. The index is where it had first been in April 2022.

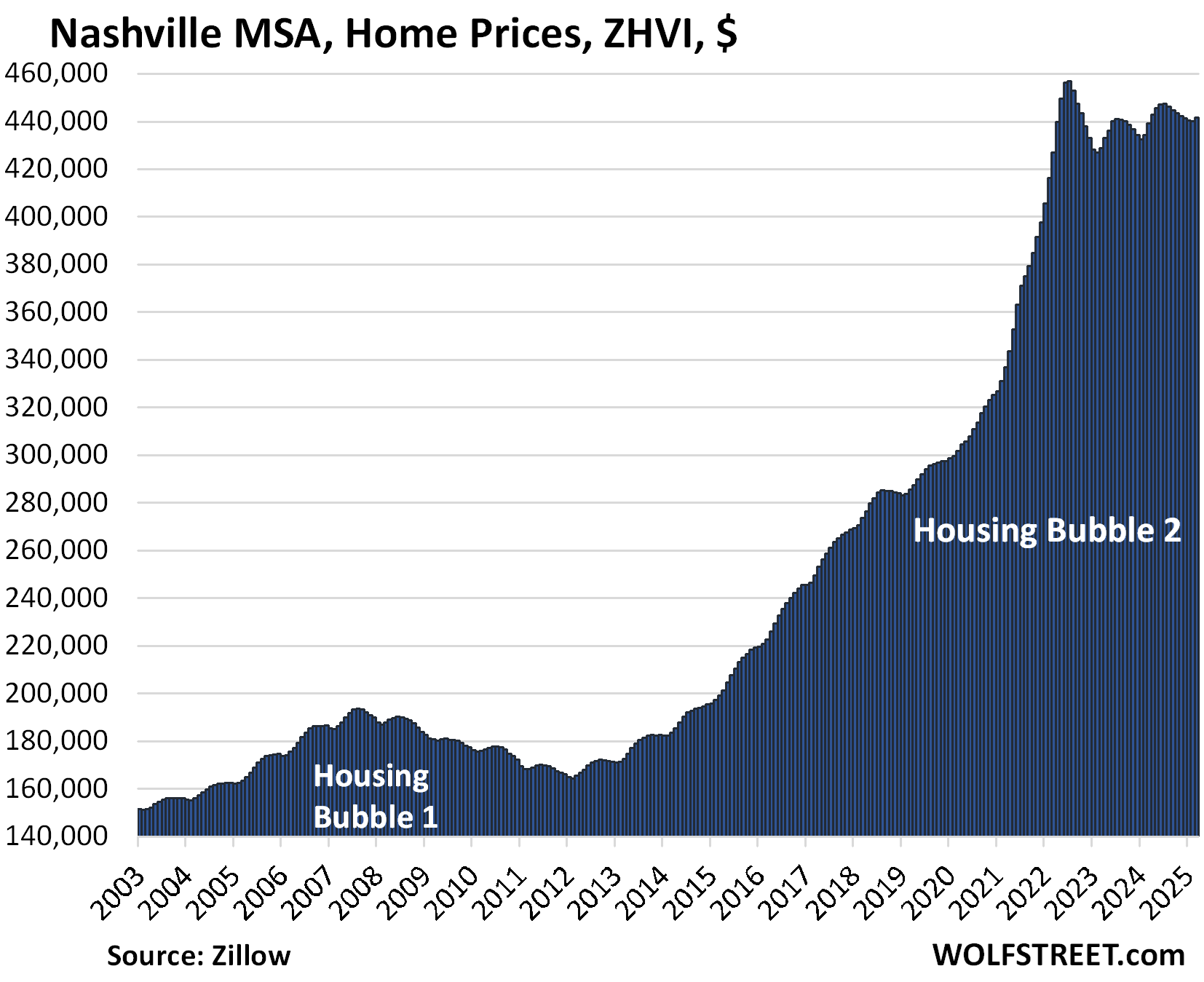

| Nashville MSA, Home Prices | |||

| From July 2022 peak | MoM | YoY | Since 2000 |

| -3.3% | 0.4% | 0.5% | 217% |

In February, the YoY gain was +1.3%. The index is where it had been in April 2022.

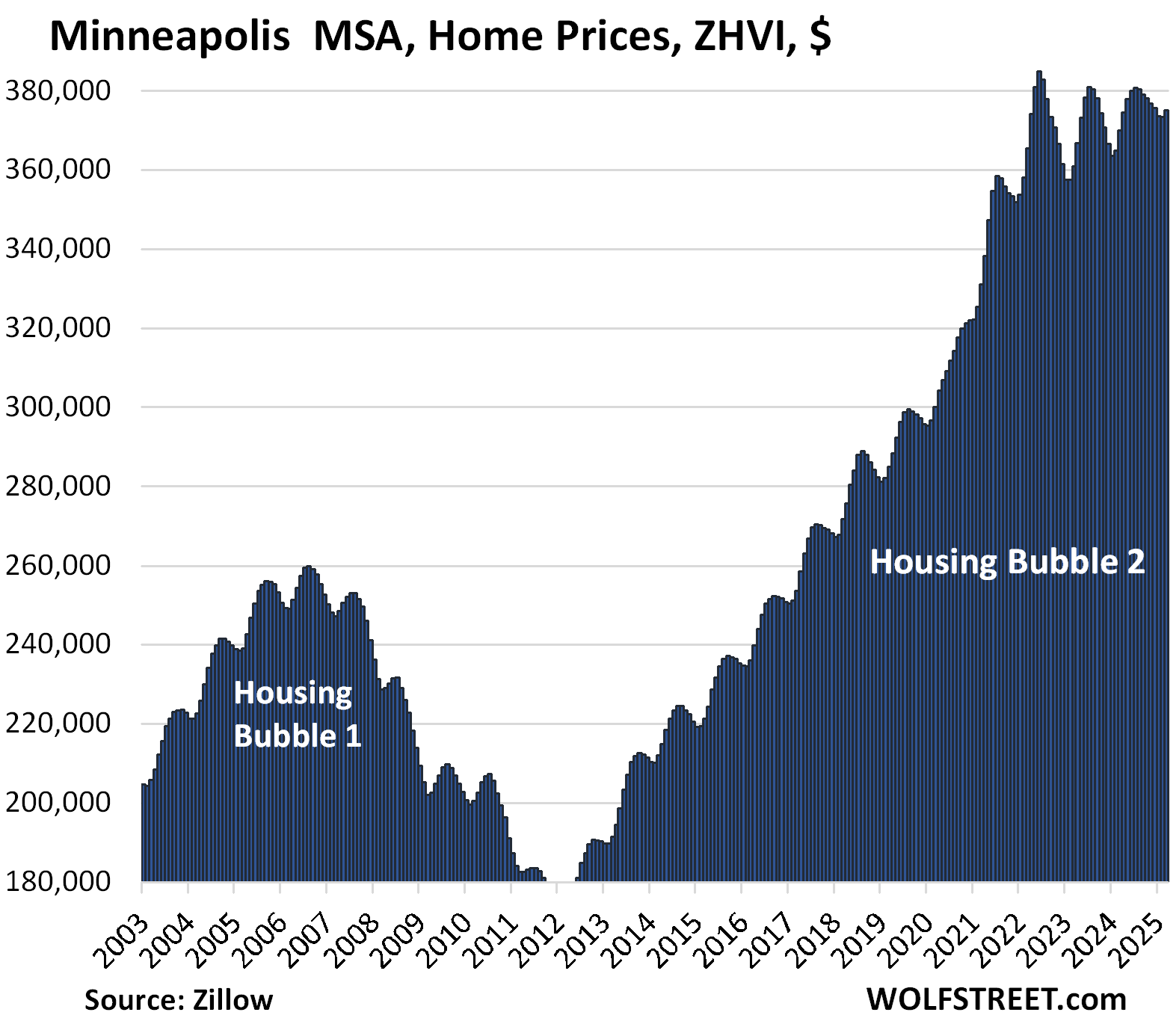

| Minneapolis MSA, Home Prices | |||

| From May 2022 peak | MoM | YoY | Since 2000 |

| -2.5% | 0.4% | 1.3% | 156% |

The YoY gain in February was +2.4%.

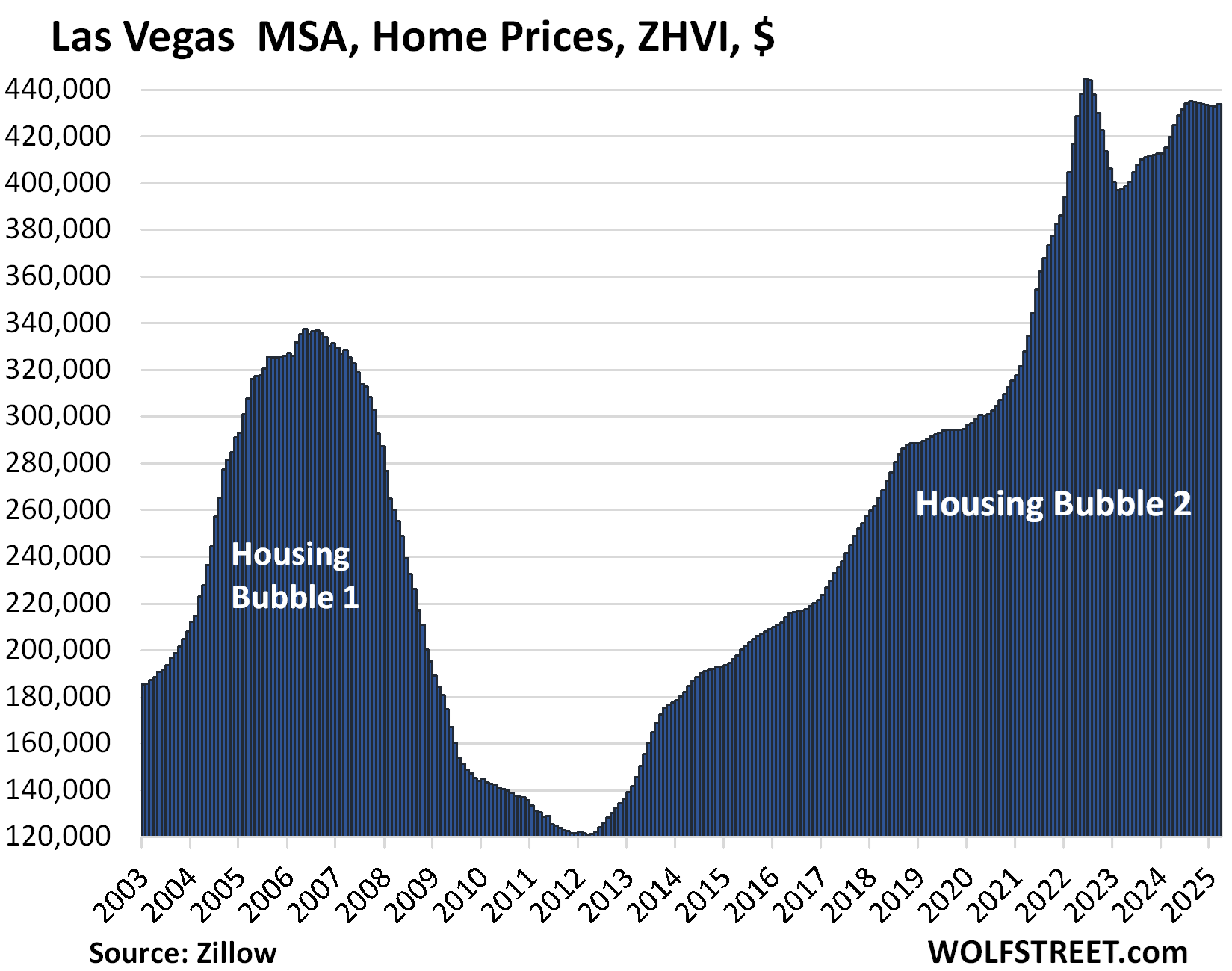

| Las Vegas MSA, Home Prices | |||

| From June 2022 peak | MoM | YoY | Since 2000 |

| -2.5% | 0.2% | 3.3% | 179% |

In February, the YoY gain was +4.2%.

| Atlanta MSA, Home Prices | |||

| From July 2022 | MoM | YoY | Since 2000 |

| -1.5% | 0.0% | -1.8% | 158% |

In February, the YoY decline was -0.7%.

| Charlotte MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -0.5% | 0.3% | -0.1% | 168% |

The index flipped from a YoY gain in February (+0.9%) to a YoY decline in March (-0.1%).

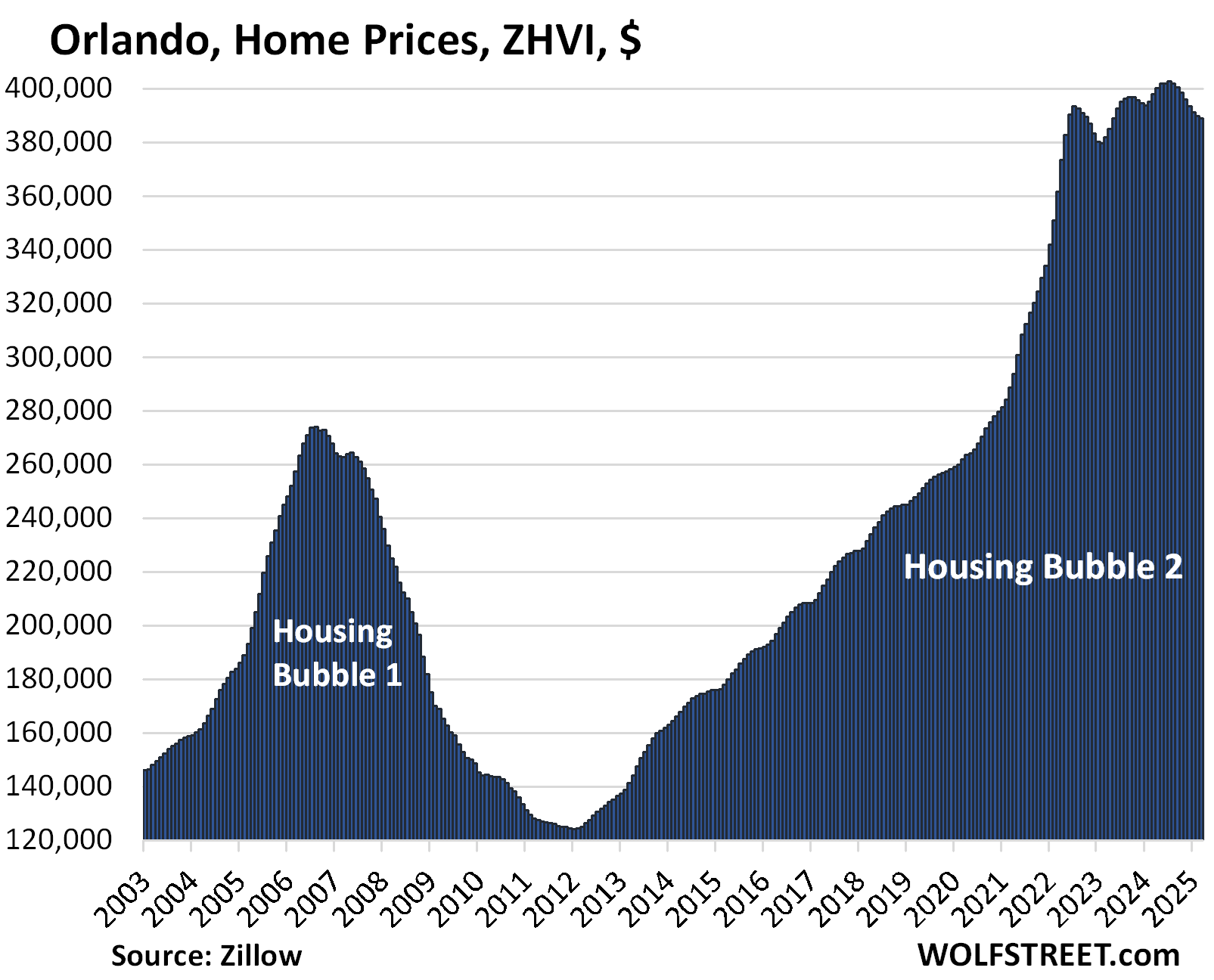

| Orlando MSA, Home Prices | |||

| From June 2022 | MoM | YoY | Since 2000 |

| -1.1% | -0.2% | -2.2% | 231% |

YoY decline worsened from -1.4% in February.

The 13 markets are higher than in mid-2022:

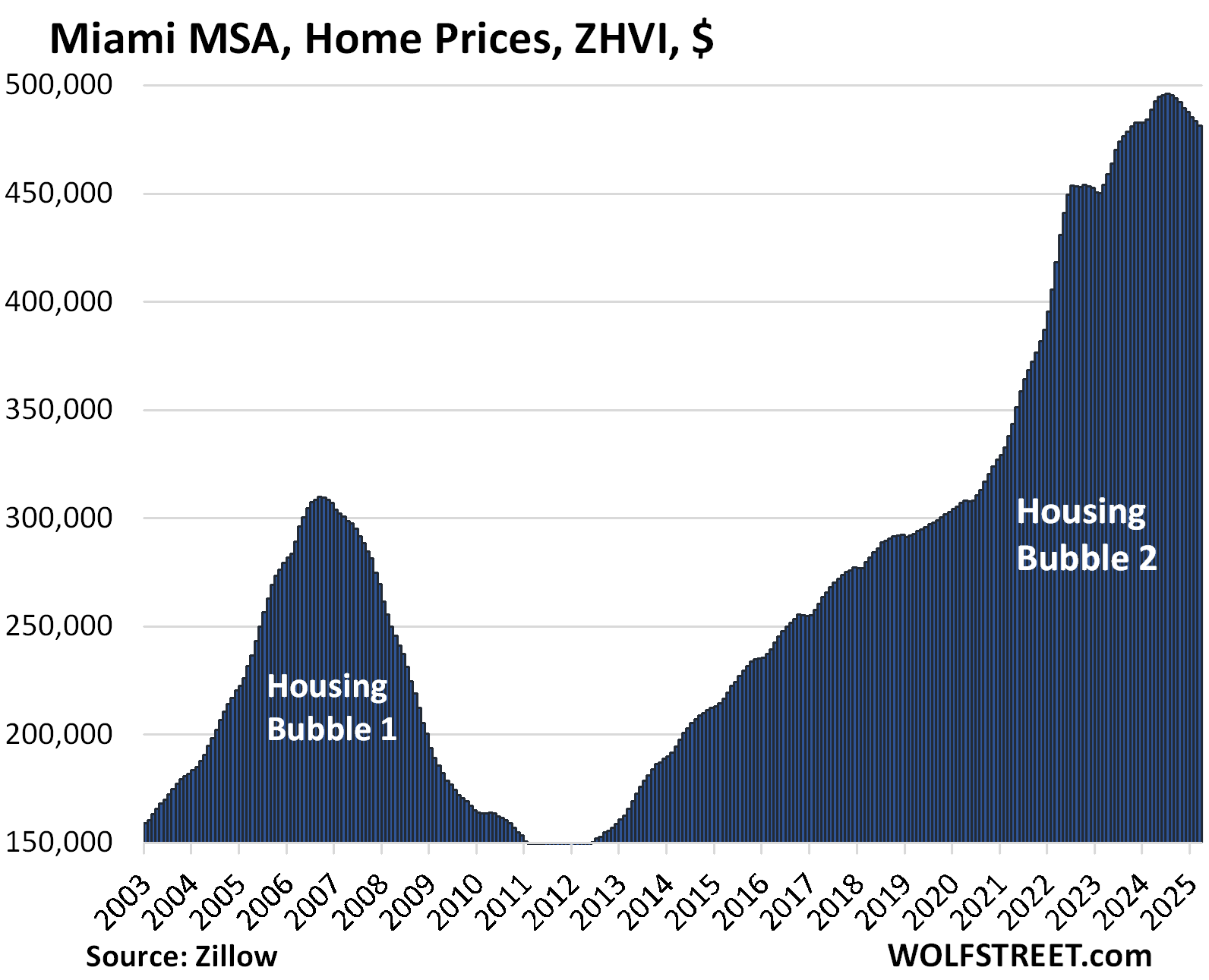

| Miami MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| -0.4% | -1.5% | 324% |

Miami’s market is turning south:

- The YoY decline worsened from -0.2% in February.

- In March 2024, prices jumped by 1.0% from February. In March 2025, prices fell by 0.4% from February.

- Since the high in July, the index has dropped by 3.0%.

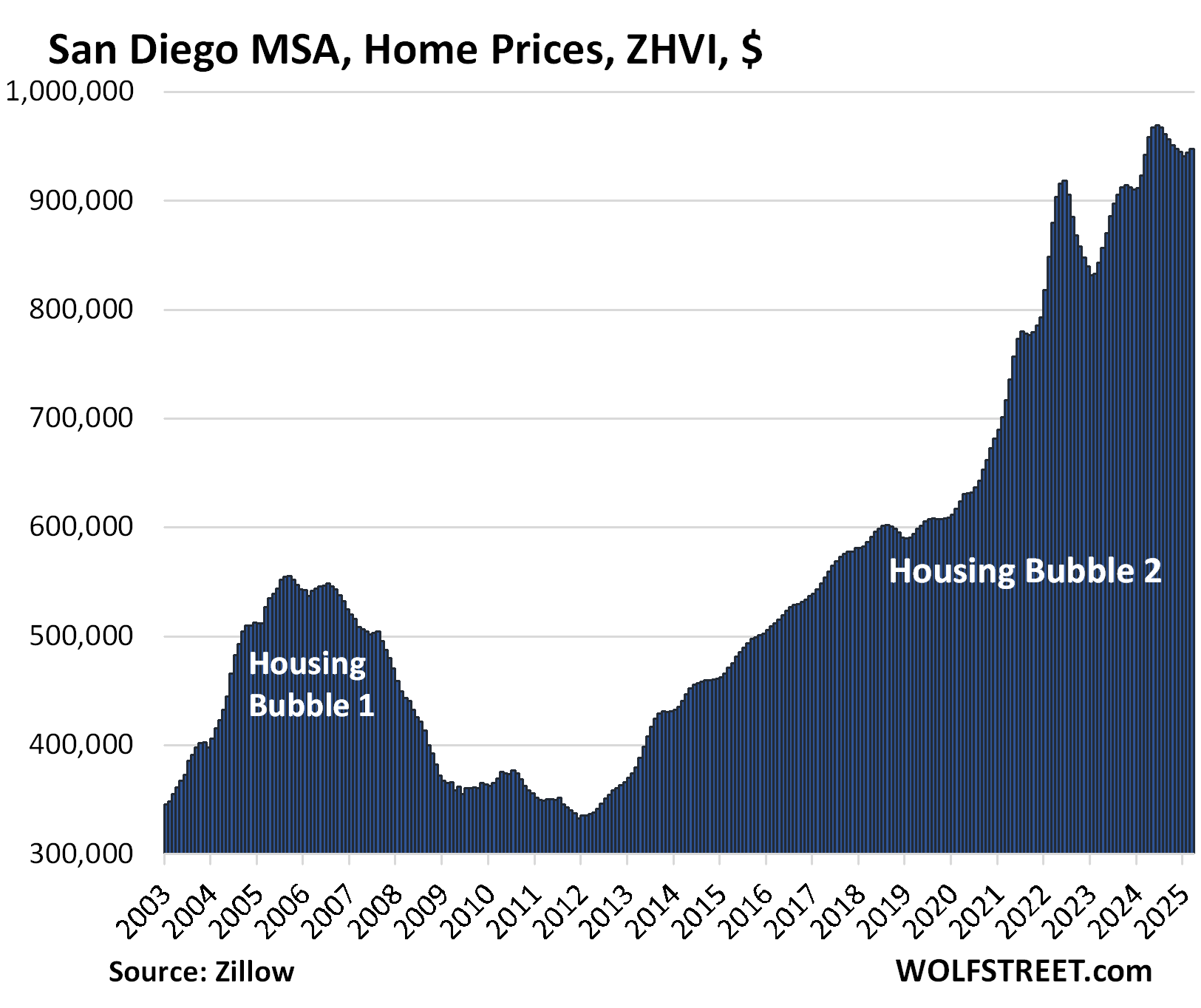

| San Diego MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.4% | 0.5% | 334% |

In February, the YoY gain was +2.3%.

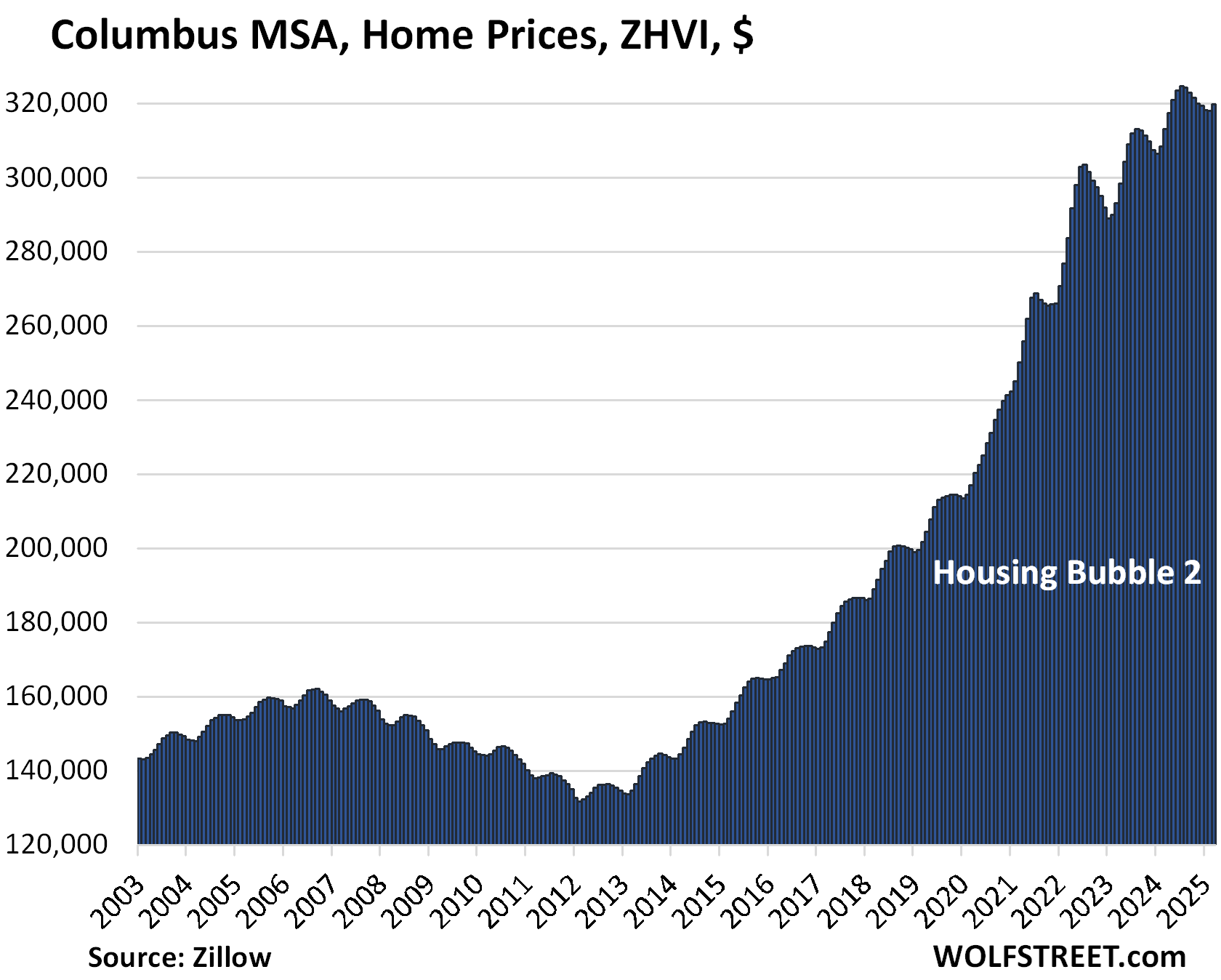

| Columbus MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.6% | 2.1% | 153% |

In February, the YoY gain was +3.1%.

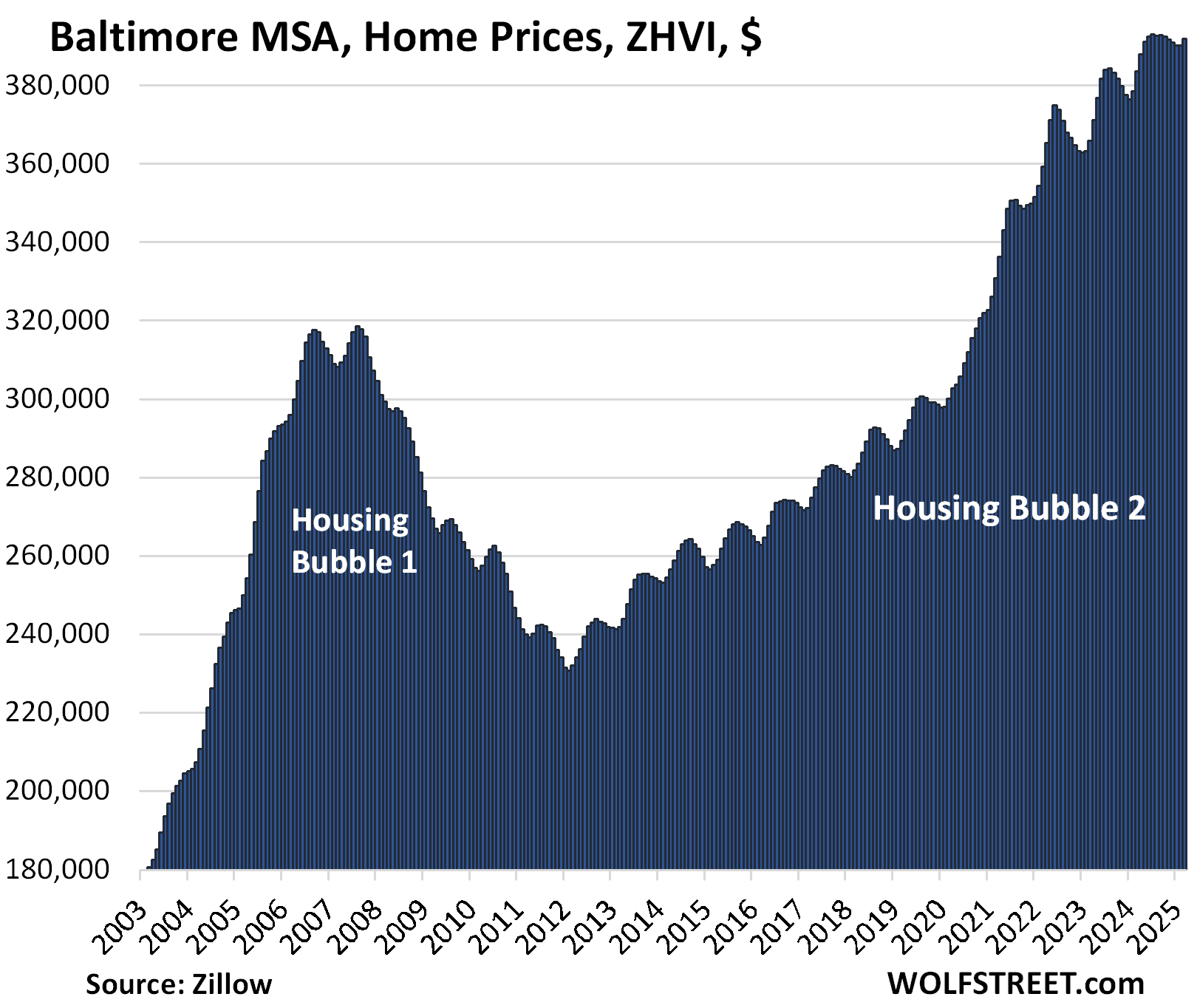

| Baltimore MSA, Home Prices | |||

| MoM | YoY | Since 2000 | |

| 0.4% | 2.2% | 174% | |

In February, the YoY gain was +3.1%.

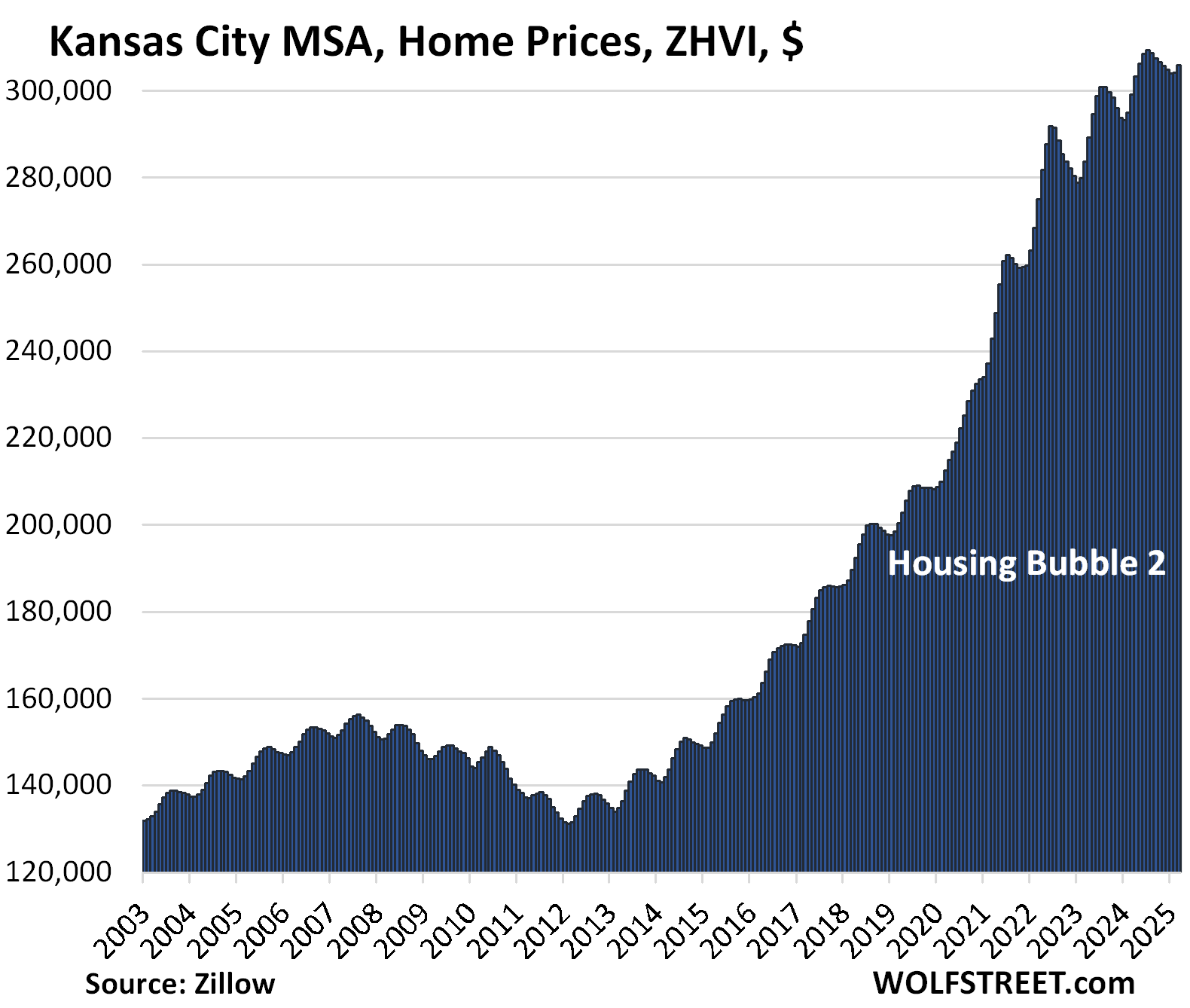

| Kansas City MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.6% | 2.2% | 176% |

In February, the YoY gain was +3.1%.

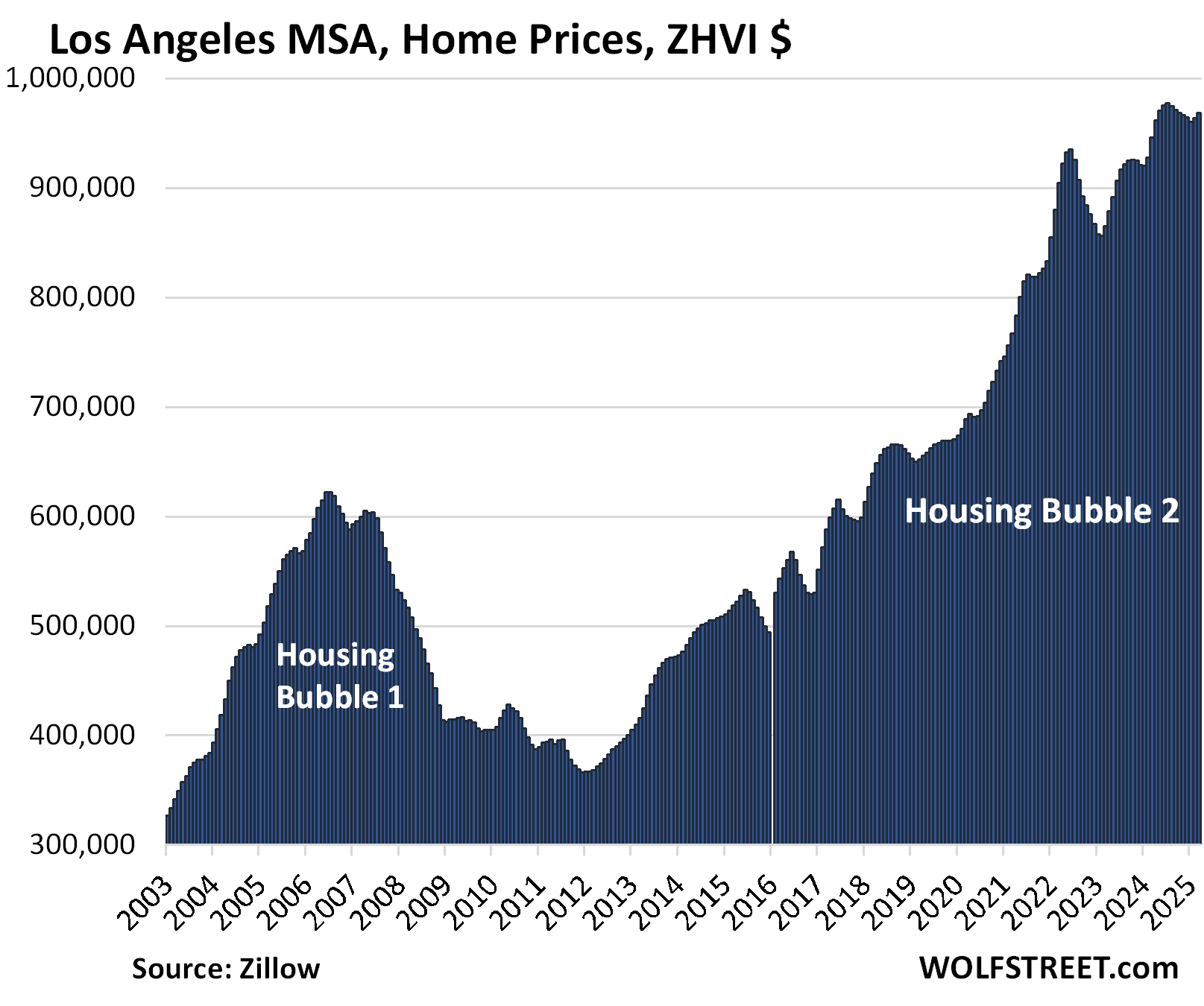

| Los Angeles MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.5% | 2.4% | 331% |

In February, the YoY gain was +3.9%.

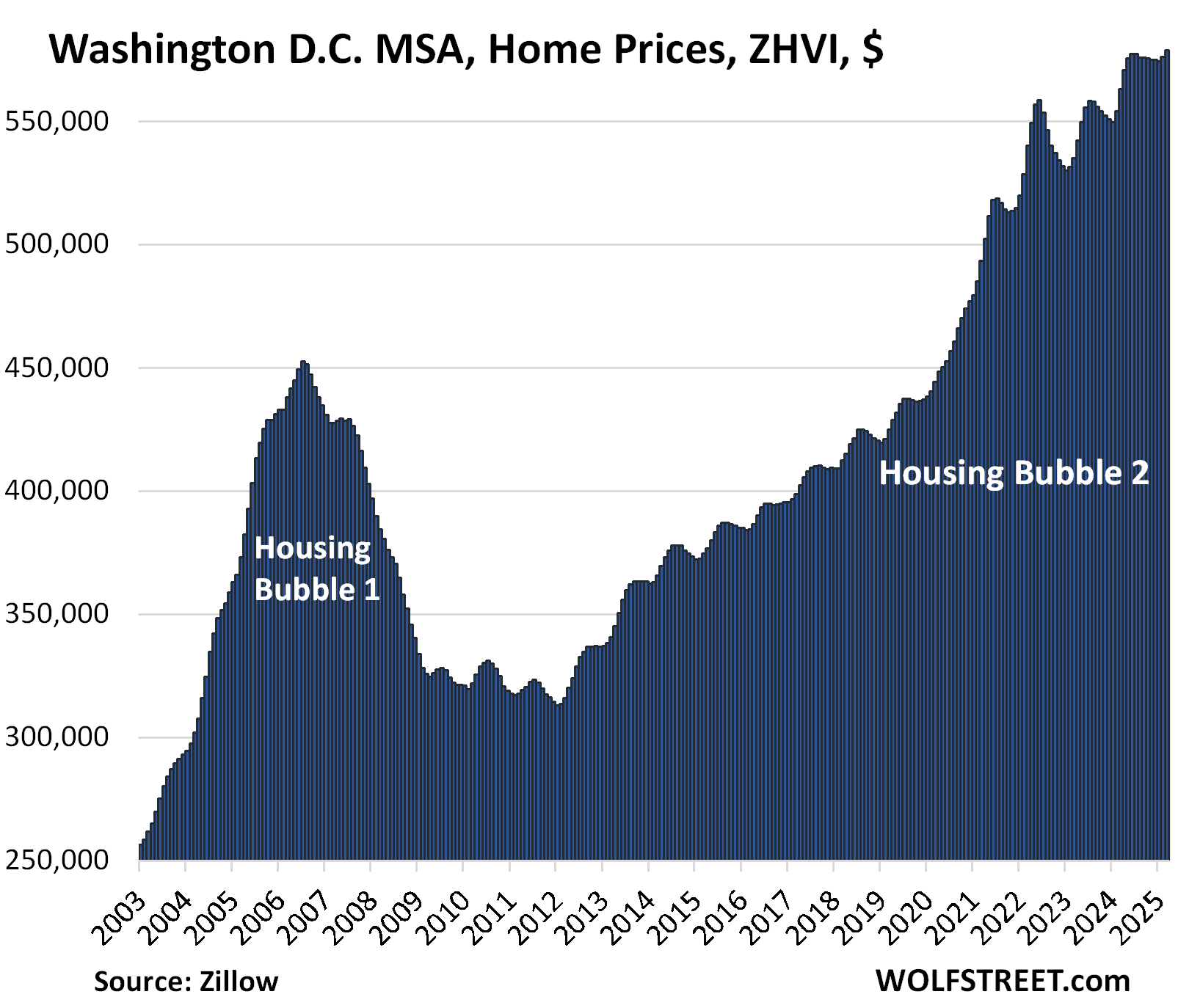

| Washington D.C. MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.5% | 2.8% | 217% |

In February, the YoY gain was +4.0%. The index is roughly unchanged from June 2024.

The vast and diverse metro includes Washington D.C. and parts of Maryland, Virginia, and West Virginia.

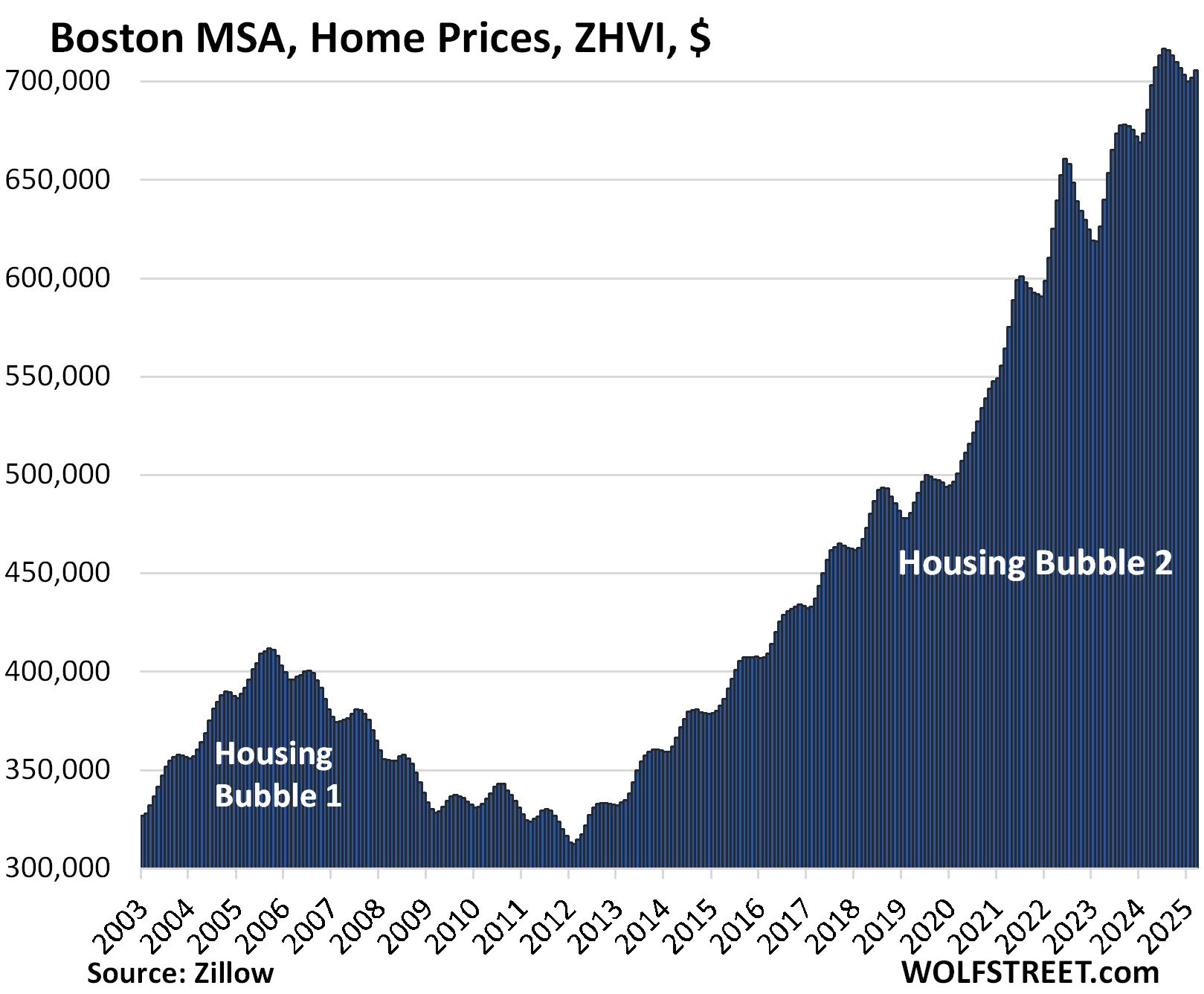

| Boston MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.6% | 2.9% | 225% |

In February, the YoY gain was +4.2%.

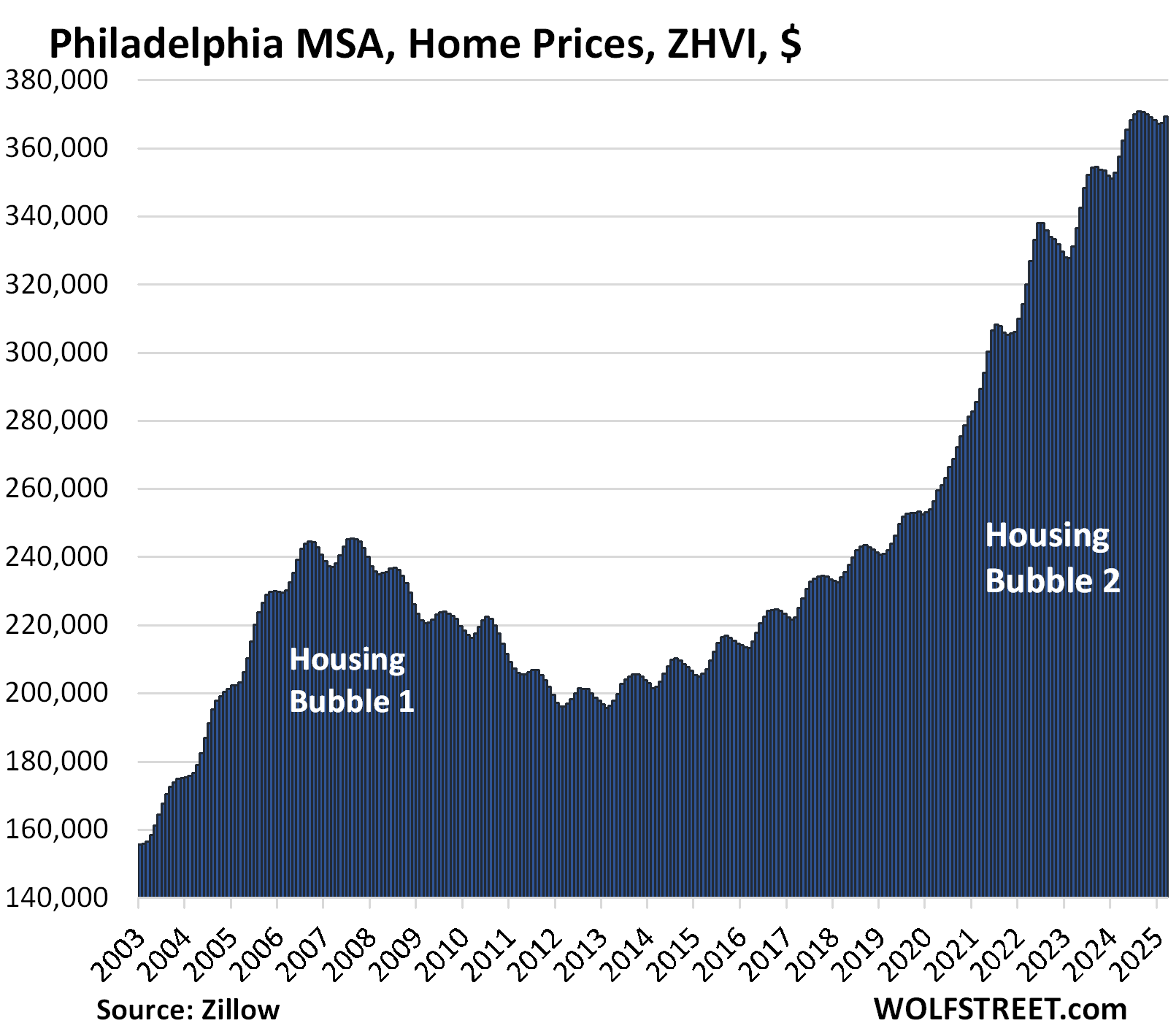

| Philadelphia MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.5% | 3.3% | 201% |

In February, the YoY gain was +4.1%.

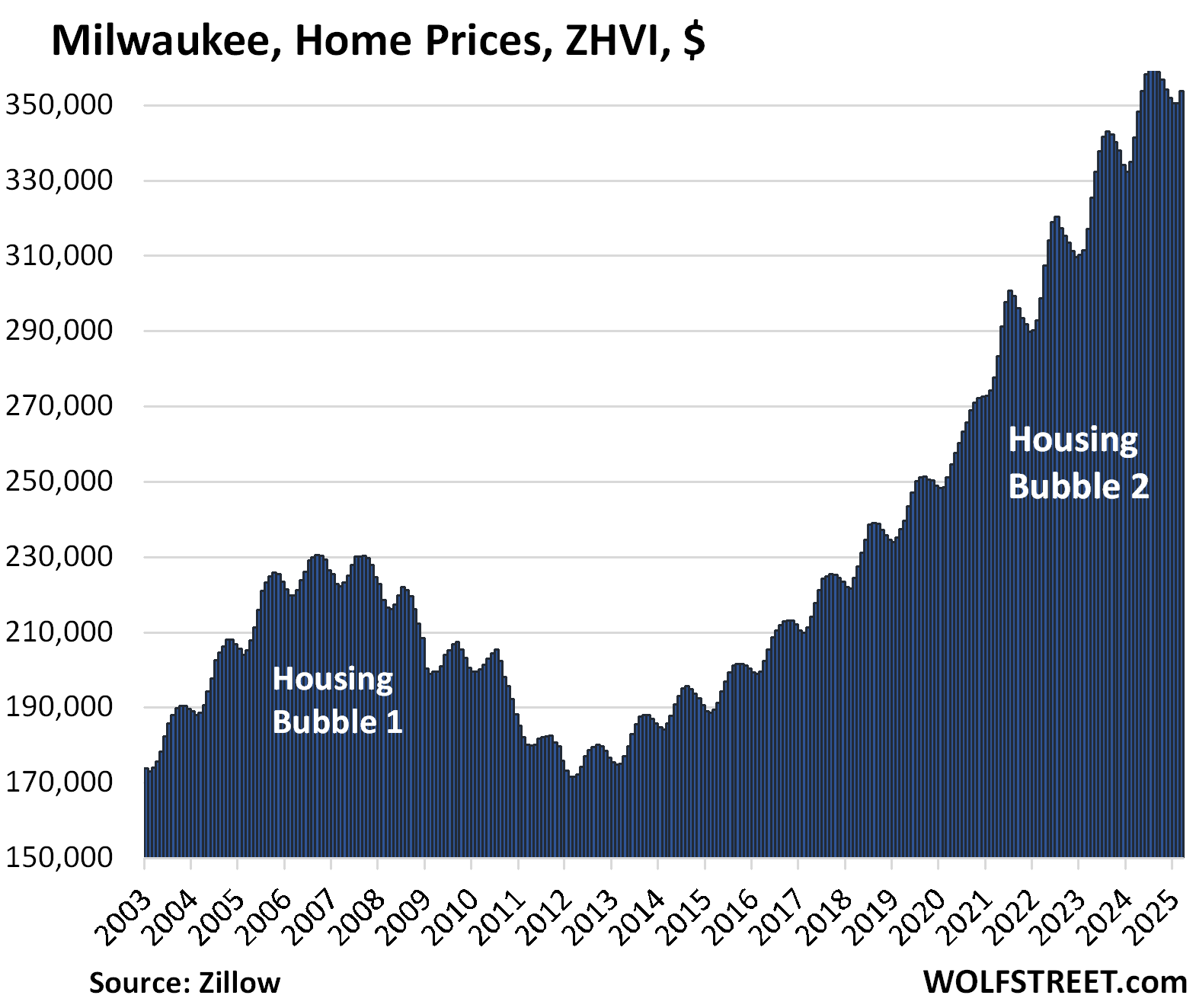

| Milwaukee MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.9% | 3.6% | 143.5% |

Though the month-to-month price gain in March looks big, it was a lot smaller than in March 2024, causing the YoY gain to narrow from +4.7% in February.

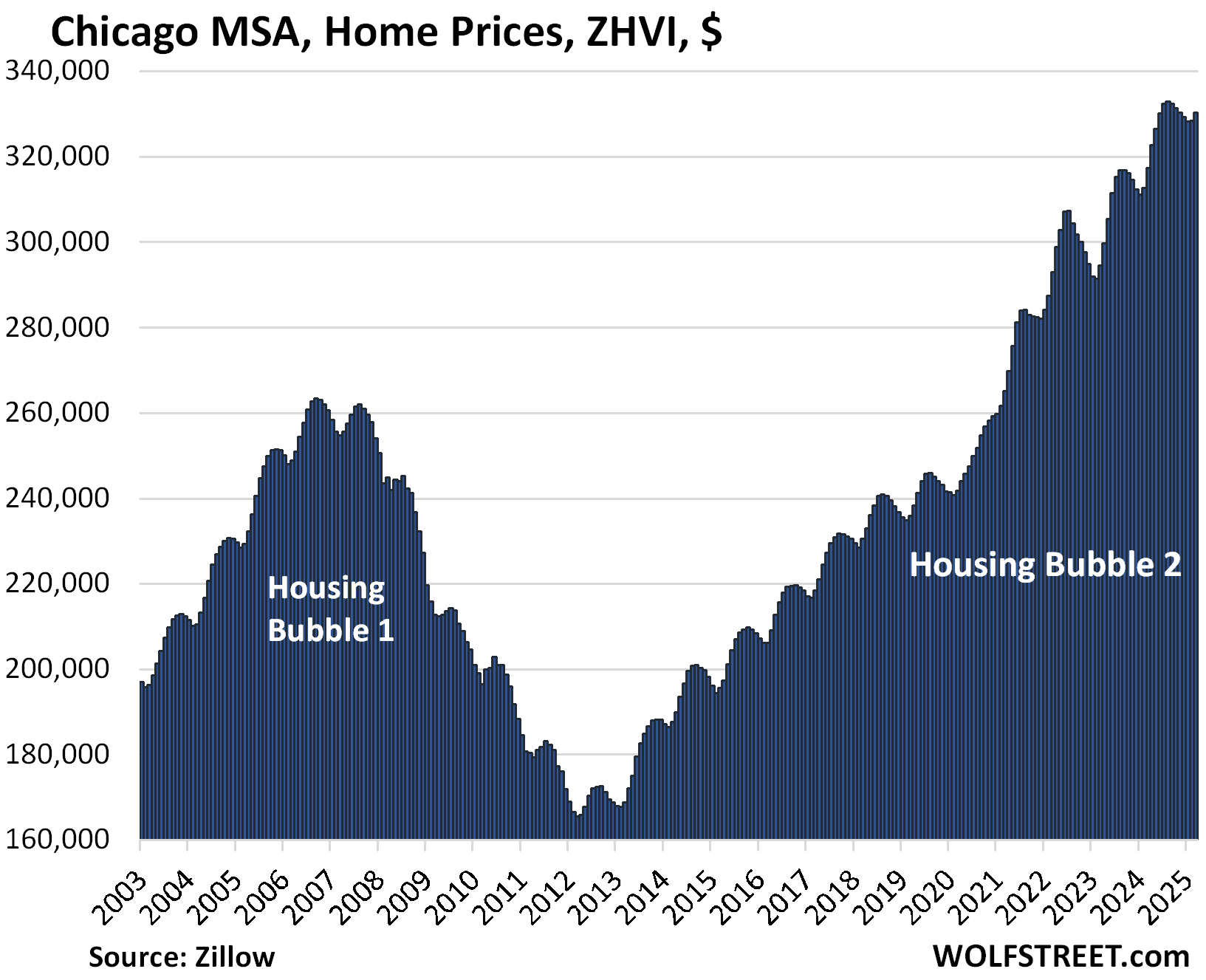

| Chicago MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.6% | 4.1% | 112% |

In February, the YoY gain was +5.1%.

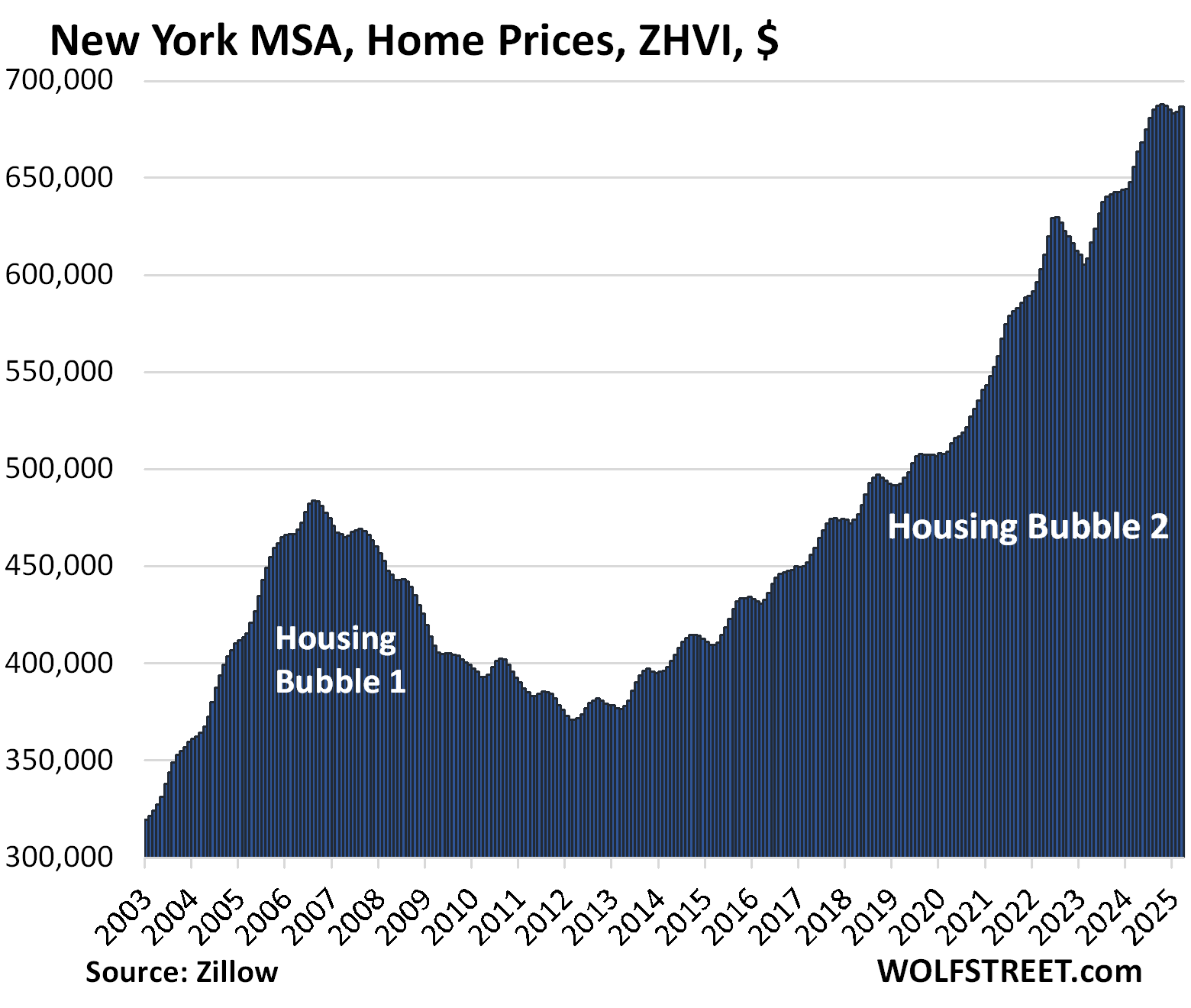

| New York MSA, Home Prices | ||

| MoM | YoY | Since 2000 |

| 0.4% | 4.8% | 212% |

In February, the YoY gain was +5.6%.

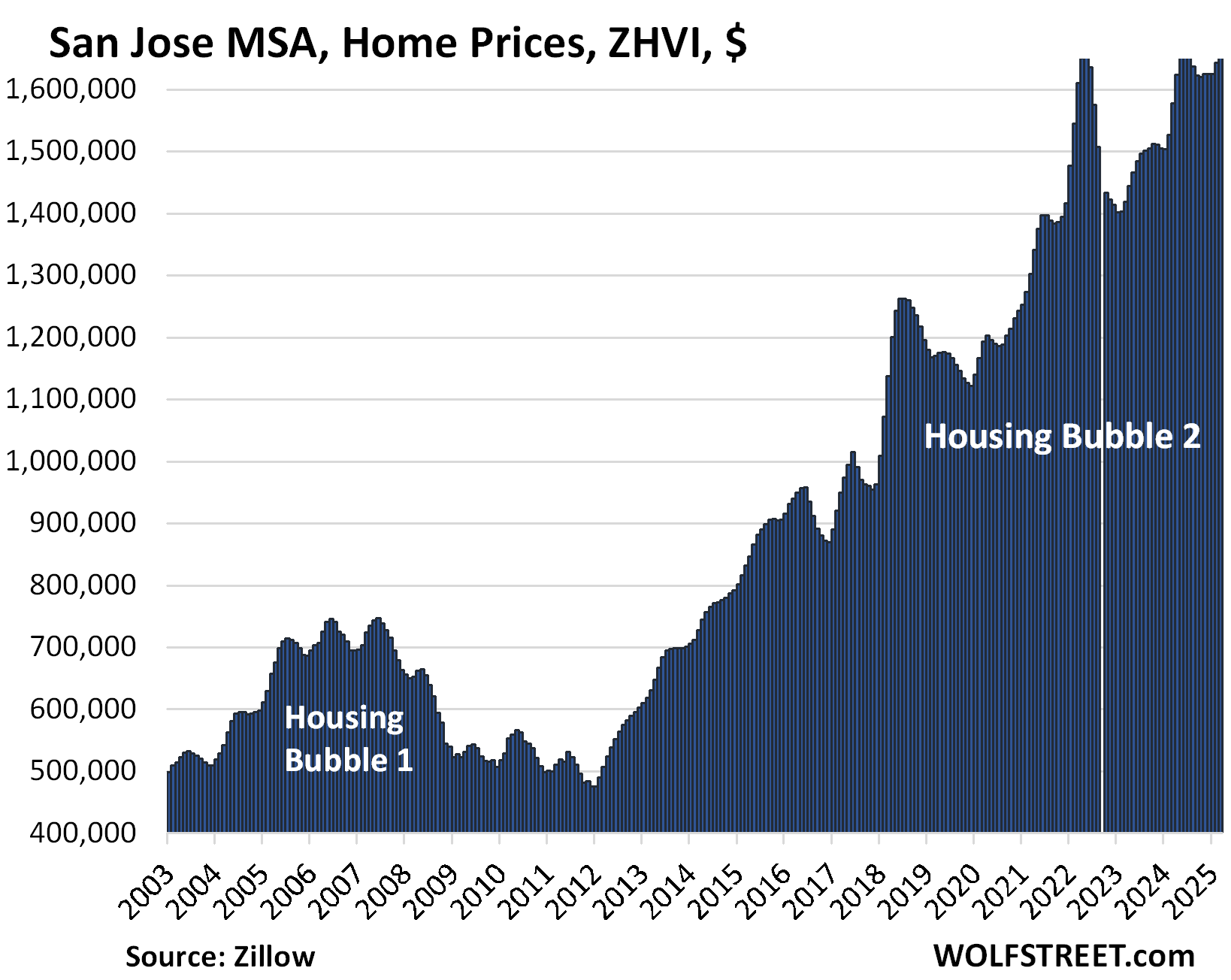

| San Jose MSA, Home Prices | |||

| MoM | YoY | Since 2000 | |

| 1.3% | 5.5% | 348% | |

In February, the YoY gain was +7.6%. The index is roughly level where it had first been in May 2022. Some crazy action:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Still watching that paint to dry and still feel like it’s not drying anytime soon….yeah yeah I know it’s a slowwww moving ship…etc. Think the express line is in Texas and Florida, SoCal is taking the turtle line..

On the other hand, if it’s isolated to just OC markets, I have a feeling it might be even better numbers than what’s shown for LA and SD..

Los Angeles MSA, Home Prices

MoM YoY Since 2000

0.5% 2.4% 331%

San Diego MSA, Home Prices

MoM YoY Since 2000

0.4% 0.5% 334%

Markets in every city will probably start ripping again once Hulk Hogan is appointed as Fed Chair.

or perhaps less funnier and more dangerous…they might have Bill Hwang in minds to replace Pow Pow…I mean what can go wrong with that…

This is within the context that since 2000 cumulative US inflation has been 68.1%. Median household income over the same timeframe has increased 60.4%.

Wolf – these ‘Mickey Mouse’’ price decreases are a joke. You know it and I know it – THE BIG ONE IS COMING. Things can’t keep going up. Currently, prices are stuck in HIGH, and there are reasons for it. It will end badly. The big one is coming! I wanna read Wolf’s column after the housing meltdown begins. Maybe it will be titled in ‘The Most Horrific Housing Meltdowns in America. 33 Cities with the Most ‘New Homeless’.

RE moves very slowly. Downturns take years, sometimes decades.

@wolf – why does RE move very slowly ?

You can make your own list of reasons. Structural issues are part of it, such as home prices that blew out and no longer make economic sense, or economic changes in the local market.

National home price declines over an extended period are rare. Local and regional housing busts, these are severe housing busts with price declines of 60%-plus, are common, and they can last for a very long time.

The last national Housing Bust was lightning fast, and it took about five years to hit bottom.

Local housing busts can last decades. Tulsa’s housing bust started in the mid-1980s and lasted about 3 decades before home prices began to rise again in a substantial way.

Wolf, what do you think about the Homer Hoyt Cycle?

“In 1933, American economist Homer Hoyt analyzed data on real estate prices from the late 19th and early 20th centuries. Hoyt concluded that the real estate market follows an 18-year cycle consisting of four main phases: growth, peak, decline, and bottom.”

Nothing.

Fast money is a fools game. Flips were made to become entertaining and exposed what sweat equity rewards are. Not just buy a foreclosure and get lucky. Slow and measured home appreciations were also put on the back burner mainly due to the slack of housing starts of affordable starter houses which created overzealous flip results, instead of practical rehabs. If you put lipstick on pigs you only end up with painted, fancy pigs.

“There are decades where nothing happens and weeks where decades happen”. Certainly not the latter with housing but perhaps with random tariff and political decisions.

Meanwhile, Admin is ball-kicking Powell again, asking for rate cuts, soon asking to resume QE.

“And prices will rise!” (Think Elaine’s old boss on Seinfeld when he had ink under his nose. Good imagery for this comment)

I’m in Phoenix Metro. Glad to see a little progress behind made. I remember thinking in 2019 that prices were high and due for a correction. I’m not sure if we will ever get back there!

I live in Laveeen. Micro data tells more of a story. Mesa, Chandler, Scottsdale, Gilbert, and Queen Creek are with huge declines. Buckeye, Laveen, and Phoenix continue building with a more modest price point.

We will NEVER get back to 2019 when prices were 280k in the Phoenix area. Debasement of currency and inflation are the reasons.

I actually live in Scottsdale. I have been seeing price drops on listings I watch, but would hardly qualify them as huge. Prices in my parents neighborhood keep seeing increases to all time highs. My co-worker is looking in Mesa/Chandler and has been seeing more significant price drops. Its location, location, location. Scottsdale/PV/Arcadia are the place to be. The rest is urban sprawl.

I’d say: Never say Never.

I have been gullible enough to say that ” this can never happen” and then after due time I see the same thing happening.

Look at the general directions and macro pics, you may get an idea.

I have friends in Austin, sitting/owning on multiple homes. They never thought Austin would see such a decline because in their mind, Austin is next Silicon Valley and everyone wants to move here including top big companies.

Gong by your logic of inflation and currency devaluation, Austin should not have experienced this decline at all as people living in Austin experience the same inflation and currency devaluation like all of USA.

Spent the winter in Phoenix, heading home next weekend.

This city is booming. I can see housing being flat for a few years, definitely down from the 2022 peak, but don’t ever fool yourself that it’s going back to 2019 or 2013 levels. I can’t tell you how many west coasters I’ve met who come over here and think $600-900k is an insane bargain on a nice house. The LA and Seattle money fleeing those locales will keep Phoenix metro strong for a long time.

This narrative is comical at this point. People like you either completely ignored Housing Bust 1, or are willfully ignorant.

People like you forgot how much our government debased currency units to pay its bills. People like you forgot the fed chairman told people in the 2000s to get 5/1 ARMS when rates were dropped. What person would ever get one of those… 2008 was 17 years ago.

How much is (not)having to live through a Phoenix summer worth?

Not having to live through a Phoenix summer is worth something. So is not having to live through a Seattle rainy season. But the value of each is not infinite, and Phoenix is still far cheaper than California.

Everybody says that, yet everybody keeps coming here.

They say weather in Phoenix can be “warm”, “hot”, “very hot”, “extremely hot” and “stupid hot”. Popular joke around here.

Yet, after a few years living here, I barely noticed it anymore. As they say “you don’t have to shovel sunshine”. Another popular joke.

Sure, Arizona heat isn’t for everyone. But I have a friend in Rhode Island, and he’s spending on average $700 a month for heating oil, and then cooling in the summer.

My average in 2000sqft house (2019 construction to be fair, but most housing here is newer), is $150 a month in an all-electric house, heating, cooling, cooking, hot water etc.

I think Arizona heat is a shock for sure at first, but by far most people will easily acclimate. Goes the other way too: I could never go live in a place where it snows again, though I was born and grew up in one. Even places with eternal rain, like Portland or Seattle, are off my list.

All that said, the real reason why Phoenix home prices won’t come down is the economy here. Many companies have moved and are moving here, manufacturing, tech and finance alike. Just look at TSMC and other chip companies. This is “Silicone Valley 2” for real now.

Here in Gilbert, there’s so many new Mercedes SUV (and such) driving around, while 15 years ago when I arrived, it was basically Fords and Chevys.

Not to say I wouldn’t wanna live in the Bay Area, or Orange County CA, I really would, but their prices are insane. 2 bedroom condo in Irvine is now to close to $1M. Insane. Super Hot weather 3 months a year is a small price for getting a nice house in a nice area here for half the price.

The home prices have under paced M2 money growth. M2 money is over 4x what it was in 2000, yet house prices are 3x give or take a little depending upon the region. Median household income was $40,551 in 2000, and $80,020 in 2024, about 2x over that period. Wage growth generally lags M2 growth, so it is likely wage growth will catch up to M2. Given that houses have under paced M2 growth, M2 will have to decrease for a housing to contraction. It is more likely that the excess M2 will continue to flow into wages driving them even higher, and push house prices even higher than current levels.

Is money supply directly linked to housing prices as you suggest? What happened to M2 during 2006-2012? A quick “back of the envelope” calculation tells me that M2 increased 45% from January 2006 to January 2012. What happened to housing prices during that time?

My house in one of the major markets listed above would sell today for 120 ounces of gold, but in 2000 would have sold for 429 ounces of gold. So its price in gold is 30% of what it was in 2000, though the gold boullion supply has not contracted threefold and has in fact increased.

M2 is mud pie. An increase in time / savings deposits reduces GDP. This was demonstrated again, and again after the DIDMCA of March 31st was enacted.

Housing took off after unlimited transaction deposit insurance was removed. This unleased monetary savings.

“unlimited transaction deposit insurance” – I’m not sure what this means, can you define it – is it like insurance on a purchase earnest money deposit ?

Dimartino Booth, in her book, gets backwards: “Fed Up”, pg. 218

“Before the financial crisis, accounts were insured up to the first $100,000 by the FDIC. That limit kept enormous sums *in the shadow banking system* (which was a good thing)

After Dec. 31st, 2012, funds flowed back through the nonbanks from the banks, activating monetary savings. But since the NBFIs are the DFI’s customers, no funds leave the commercial banking system.

This will somehow be blamed on Trump even though we need housing prices to come down bigly

Can’t read an article without some MAGAT crying about their cult leader. It’s pathetic how uterrably incapable you people are of prying your lips from his behind in order to practice critical thinking and develop your own INFORMED opinion.

Lol hahah I got one!

Probably because every single thing is blamed on him. I do have my own informed opinion but thanks.

Nice to know that you guys result to personal attacks because you have no ideas.

Is that you Eric Trump?

Someday perhaps, but unlikely, Americans will wake up to that it isn’t Biden or Trump or whoever is in power but systemic issues. Making life better for all citizens should be the goal of elected government and you simply need to look at the numbers to realize that isn’t true. It isn’t really rocket science what needs to change, but no way either side is going to make the necessary changes. Continue to enjoy your blame game.

Powell has been adamant about US fiscal policy. Telling both sides to meet with each other and figure it out.

He is 100% right but our politicians suck. Atlas Intel poll just released has Trump at -6 but then you look at approval for congressional Rs, congressional Ds, and other D/R leaders and it is lower. When questioned about economic policy Trump is negative again but so are all of the groups mentioned above.

There is no true leadership or plan from either side of the aisle. Both parties got us here and neither wants to get us out.

And money ensures that there is no alternative of course and they are happy to switch back and forth and not make any significant changes. Sure, you can have alfredo versus marinara but same noodles.

When the sleepy guy was “in”, everything was getting blamed on him too! It comes with the job!

His approval numbers were down for sure but he was also covered positively by the media

He was, generally (but certainly not entirely). And that’s largely because most of what he did do, and tried to do, were positive things, steps to create a better world.

Trump, on the other hand, focuses much more on negative things, tearing things down, retribution, settling scores, dividing, and of course, grossly exaggerating his positives and his “enemies'” negatives. You can argue that those things, too, are steps to create a better country, and that may or may not be true. But along the way, it’s definitely a negatively-focused and spiteful process which of course receives far more criticism.

Do you think Trump would be where he is without non stop media coverage? Please stop the bias meme it’s ridiculous.

Scratched and scrimped to buy an old 1958. House on the Calif Central coast in 2008….

Fixed it up for 17 years…I did my job, and it did its job.

Turns out it was the best investment I ever made. 50 percent hard work and 50 percent un adultered luck. Sold for 3 times what I paid. If I would have known, I would have done all I could to buy 2.

Anyone that says they knew that this would happen like this is full of it.

Did similar, but bought in San Diego in 96 and sold in 04, got 3.5x for what I paid. When I sold people thought I was insane but I actually sold a few months after the peak in my neighborhood. When prices make all time highs people get dollar signs in their eyes and project never ending gains. They do it with RE, they do it with stocks like nvidia, they do it with bitcoin and they’re doing it now with gold. It’s a very strange herding mentality. And no amount of facts will sway most.

By end of 2026 some of those cities like Austin should be at precovid levels. I also think places like sac and Phoenix might waterfall down, they seem to be places that aren’t particularly nice but people nonetheless talk themselves into thinking they’re desirable.

I live in Sac and agree it will be interesting. Besides ZIRP, the prices dramatically increased because telework via Bay Area transplants. Paying 700K for a 20 year old house with 2500 sqft in a nice neighborhood was a deal. I don’t gauge it against the high but I paid a little over 400K in 2016 but don’t think it will drop below 600. Still a large government work force here and some of cheapest electricity in the state. Tahoe and Bay Area 90 minutes away as many other places and heat relative to Phoenix not bad😃. I sometimes go to Fort Bragg in the summer to escape for a bit, but basically 4 months of heat but rarely doesn’t cool down considerably overnight. And SF in September and October ideal and Wolf likes the tourism.

This is a classic example of “ownership bias” => “but I paid a little over 400K in 2016 but don’t think it will drop below 600. “.

Why do you think it can’t go below 600K ?I have been incorrect many times, but 600K home is SAC is pretty expensive.

jon,

For example, during the Housing Bust, home prices dropped by 55% in Sacramento from peak to trough. If that reoccurs, and if someone paid $700k at the very tippy-top in 2022, a 55% drop in prices would bring the price down to $345k.

I have seen bigger price drops in Tulsa in the 1980s when I bought my condo there from a bank (foreclosure), and I bought at less than half the outstanding mortgage balance, and then the bank collapsed, and the FDIC got the other condos, and my neighbor bought his from the FDIC for another 20% less than what I had paid. His total was close to 70% below the bank’s mortgage value. Both condos were 1,800 square foot beautifully redone condos, each composed of two 2-BR units combined into one, walls taken out — on the 23rd floor with huge views and balconies.

jon,

Perhaps but I was speaking about my specific house and neighborhood which didn’t get hit nearly as hard. Of course it could happen but right now I don’t think anyone is predicting residential housing meltdown like before but of course anything is possible. If you are a family with both people working for the government you can easily be making 200-250K a year combined. In my case the house is paid for so not something I am banking on. I view the house as a place to live so if it dropped not ideal but not counting on valuations either.

Oh god, if I get a dollar everytime I hear the logic of because I pay this much, it will never go below X amount in SoCal…In better part of LA and OC (especially South OC) this is like freaking gospel among the demographies of wannabe buyers and current existing owners…it’s quite tiresome to hear and even tragic to see they have been right so far sans 2008 which everyone already forgot by this point..

Why did you give it up? Where are you living now? In a tent?

I retired and am leaving the state.

Traded a 6,000 square foot lot for 6 acres

Give me a little room to stretch my arms

Wow! 13 markets above 2022 peaks! And trump’s begging them to lower rates!

Of course. When you have 37T in debt and 90T in short term debt to refinance, you too would choose that. Otherwise, that’s a real depression in the making.

As an alien, I imagine one of the reasons for America’s success historically has been the willingness of the workforce to move to where the jobs are. The sky high property prices now make that look dangerous and the property owners who switched to a 3% mortgage are now victims of their own device. What a quandary.

Why choose Earth?

I prefer it to Planet America.

But seriously, I think everywhere that followed the US lead and cut interest rates plus other measures to deal with Covid is in the same boat. Those measures prevented mass unemployment on top of a pandemic, which is good, but the measures stayed in place too long (controversial, discuss). Here in Australia property prices are sky high partly because the government opened the flood gates to immigration after Covid (which is OK in itself), but numerous building companies went bust because of the rising cost of materials and a shortage of skilled labour. In the old country, the UK, there’s a lot of resistance to building on green land, there is old infrastructure and after Brexit, famously, all the Polish plumbers left. Wolf has also documented the Canada experience.

Not wishing to be hurtful, but I think the only thing that can change the situation is mass unemployment. Whenever I read ‘recession’, I automatically substitute the word ‘unemployment’.

Howdy Prisoners. Somebody is trying his best to lower interest rates. Govern ment could rescue you with 3 % Mortgages Soon. Maybe Zero down and even receive a check for cash again. Just sign and walk right in.

unless the fed starts printing again, that ain’t happening. they could lower the fed funds rate to 0 and mortgages still wouldn’t be anywhere near 3%

Howdy Franz. You underestimate Govern ment

The FED doesn’t need to expand credit. The banks are in position to do it with $3.261T of available reserves. Free reserves should be defined as those above the minimum required by the BOG for currency expansion, etc.

Great job America.

Nothing like stealing the future of the young so people can get rich.

QE was a mistake and the actions from 2008 on will have long reaching affects on society.

The young people should be buying so in 20 years they can be part of the same narrative when housing is 2x the current price.

Does anyone think the Global Governments can stop increasing their debt. The Central Banks will do their best to help inflate so Governments can pay back the debt with cheaper dollars in the future?

I think the U.S. debt should be around 65 to 70 trillion in 15 years?

The massive housing bubble is just one of many “corners” US economic policy (if you can call it that) has painted itself into.

It create a “wealth effect” to be sure, as well as an “industry” (everything house and home) but we know it is not sustainable.

The only real question is how it ends. Drip, drip downward or one big crash. The 2008 crisis was met with top federal policy that stopped the banks from unloading properties at firesale and then hired Blackrock to go around and buy of properties back to original price level (under the guise of developing a rental portfolio). I know this to be true as I witnessed it in my neighborhood. This was Tim Geitner’s brainchild; and it worked.

So the Feds would not look away if housing prices started to collapse; however, neither would the rest of the world. The amount of printed money the US created to “solve” the 08/09 crisis is what caught the attention of others in this world economy. And future dollar largess will only reinforce their desire to move away from the entitled dollar.

A bank unloaded a foreclosure to me in 2012.

I’m just gonna say it because I know everyone wants someone to do so: “not in my neighborhood!”

Are you Stephen Curry?

Nationwide, 400,000+ homes are still being blocked from forclosure due to pandemic-era forclosure moratoriums.

More inventory being artificially kept off the market due to gov’t policies propping up housing.

But, would any of those have to be foreclosed upon if not for the moratorium?

Howdy MussSyke. Local Govern ments can prevent a property owners from evictions also.

There’s a lot of BS circulating around about this. Very few of those homes would go through foreclosure anyway because prices have surged by 50%-plus over those years since those homes were bought, and owners can just sell the home, pay off the mortgage with the proceeds, and walk away with enough cash to feel good and use some of it has down payment for another home. So their old home would come on the market, and their new home would be taken off the market, and the effect on the market would be zero (+1 -1 = 0).

See my comment below, I just don’t see a big housing crash.

Interesting. Heard it from Nick Gerli (reventure) who’s analysis of the housing mkt tends to align with yours.

He claimed these were mortgages already in serious delinquency and would be in foreclosure if not for the moratoriums.

If these homes are in metros that have already experienced significant price declines (FL, TX, etc.), these homeowners might be underwater by the time the moratoriums end and they need to sell.

Also, if their current mortgage is in serious delinquency, wouldn’t that affect their ability to take out a new mortgage? Or is it only the foreclosure that nukes your credit score?

What he claims is just nonsense. The markets you list had the biggest price spikes since Covid. Let’s take Austin because it’s the worst-case example of any major market right now because it had the biggest price drop: If someone bought a house in Austin in late 2019 just before Covid and then got into a Covid-era forbearance deal and still is in it, their home price, despite the 23% plunge in Austin since mid-2022, is still 35% higher than it was in late 2019 when they bought. So prices plunged 23% in Austin, the worst of the big markets, and they owner is still up 35% if they bought just before covid. They’re even more if they bought earlier.

So lets use the index price for Austin here: In late 2019, it was $325,000 – so let’s assume that’s the house these people bought at the time. Then the price shot up by 78% to $579,000 at the peak in June 2022. Then the price plunged by 23% from that high to $444,000 today. So they’re still sitting on a gain of $119,000.

So their mortgage payment (4%, nothing down, 30 years) taken out in late 2019 would be $2,025. If they’re 2 years behind, and those 24 mortgage payments were added to the end of their mortgage, and thus became part of the principal, they would owe an additional $49,000.

So how much do they owe now? The original mortgage of $325,000, minus some principal payments early on with the regular mortgage payments, plus the arrearage of 24 mortgage payments of $49,000 = $374,000. So now they sell the house for $444,000 and pay off the mortgage of $374,000 and walk away with $70,000 in cash, which may be more cash than they’d ever seen in their bank accounts, and which they can use as down-payment for their next home and use the rest to pay off their credit cards.

And Austin is the worst-case example. In other markets, price drops have been much smaller, and these people would walk away with a lot more cash. And if they bought earlier than late 2019, they’d walk away with even more cash.

Only the relatively small number of people who bought near the peak are under water now, and not by much. And they likely weren’t even included in these covid programs, which ended.

Howdy Lone Wolf. Don t forget about 2nd and 3rd leans on properties…..

The number of second-lien loans is minuscule and their balances are small, and third-lien loans are so minuscule they’re near zero. We’ve discussed this with HELOCs (2nd lien), they’re just 3% of total mortgage balances.

You would think so, but in my very small market here, I watch many units be foreclosed on, go thru the whole bank thing, then put back on the market (usually an auction) and sell for more than what the original mortgage was (I have no way to know if they refi’d in there and pulled money out). I’ve also seen two personally where the people just refused to deal with it (the foreclosure process) and just closed their eyes and went nyah nyah nyah instead of selling the house, paying off the loan and probably walking away with money. I think that happens much more often than financial experts think.

Also i have noticed a good sized increase in banks putting them up for auction over last year (where they would usually sit on them for a while or clean them up, now they just want them gone and off their books).

Just one data point among many.

Finally seeing some meaningful YoY declines. License to lowball here in FL.

I see recession brewing and what happens after this is history just like the gfc then unemployment etc etc

San Diego market is propped up by large estates being sold and trader among the wealthy.

The normal homes are stagnant and not selling. There’s three in my neighborhood for sale right now that have been on the market for 8 weeks. 3 years ago they’d be gone in one day.

Who knows what will happen next. But I can tell you that the majority of people my age (under 40) who don’t own homes have gone on strike and can’t/won’t buy.

It would be interesting to see the number of homes sold vs price to see how much lower the transactions are compared to a normal market.

The prices here are “mid-tier” — meaning homes with values in the middle third of home values. So that excludes the high end whereof you speak, and the low end.

IN San Diego, in my neighborhood, I see 4 homes , ( ~$1.4 mil asking price, multiple small price reductions though still aspirational asking price ) sitting for last few months. These homes are typical middle class homes, nothing fancy about the home or location .

This housing bubble is weird because it isn’t a bubble like 2006/2007. That was rampant oversupply and questionable mortgages, and I’m using the word questionable to be nice lol

This one is a price bubble but supply (from what I understand) still hasn’t really caught up with demand in many markets.

Think of it this way, Atlanta prices are at 380k, 80% of that is 304k meaning prices would be at 2021 levels. Hardly a disaster but a good reset for many prospective buyers and many sellers would still make money on their homes, depending on when they bought of course.

I don’t see a huge downturn in home prices, like a crash, but who knows what events will take place.

Some markets have already crashed. See TX and FL.

Please define “crash”

We keep on using words to describe situations that don’t exist. 2008 was a crash, like 50% of the value was wiped out.

Words have meanings and we keep on using hyperbole to describe situations.

I just read a great article on the Hill telling economists to stop saying tariffs would cause a depression but the author also criticized the tariffs in a balanced way. His point being , if you keep on using end of the world language then it undercuts your argument when the world doesn’t end. It is better to be sober minded and talk about the true effects of something.

A 20% haircut, on an asset that “never goes down” would be a crash, in my book.

The prices have gone down in some of the hottest market by more than 20%. and more price decline is in progress. We don’t know how much itd have down when it is all said and done.

Meanwhile, we still need people to catch the falling knife to enable price discovery.

Nice comment Eric. Speaking generally, it could very well be that prices remain in/around current levels for a few years. Like Wolf said, real estate moves slow. It makes me wonder, if a house is $350,000 now and that is considered a high price for many buyers, would that same house (and price) be considered too high 24 months from now?

Thank Alan.

Housing prices being flat or rising less than wages would be a great off ramp for just about everyone involved. Buyers will need to be patient but it is at least achievable.

We really need to get the mortgage payment as a percentage of income back down

That’s the hard part. There’s a built-in willingness to pay for homes that will be hard to shake. Just look at the anxiousness for some on this site to buy. That enthusiasm needs to die off on a large scale, to where enough people just refuse to pay this much of their earnings.

This is not to be confused with changes in the ability to pay. If that declines, sure, prices fall, but homes will still require the same proportion of income as now (or close enough).

So it needs to be Wolf’s buyer’s strike scenario, not an economic decline, etc.

But the prices have fallen a lot in many of hot markets as shown by WR and in remaining markets, prices are barely rising.

I guess the direction of prices are quite obvious.

The supply is increasing every day, the mortgage rates are high for the high price.

When and if the recession hits, which is part of normal biz cycle, then all bets are off.

Even with no recession, I see home prices going down albeit slowly.

For example, just look at what is happening to once hottest housing markets: Austin, SFO, Phoenix etc. despite no recession.

I remember 3 years back, People used to say that these cities would never see any downturn because everyone wants to move here.

Rent prices show the real demand that housing prices don’t. So, next time, could you throw the rental price index in alongside housing prices for comparison?

You just don’t read my articles, that’s your problem. The chart below is from my CPI article a week ago:

https://wolfstreet.com/2025/04/10/beneath-the-skin-of-cpi-inflation-surging-prices-of-food-housing-medical-care-meet-plunging-prices-of-gasoline-travel-services/

Gattopardo I can’t reply but that is an insane take. “Oh Biden was unpopular but he was trying to do positive things!”

GTFO out of here with that nonsense.

FYI, I’m a conservative, to put this in bias context.

Do you not see the difference between say the chips act and the various Trump acts?

Take a look at the reason Biden’s approval ratings were low. He didn’t get enough of his agenda done, and it wasn’t — gasp — left enough for the 20% of the country that is well left of him. Of course he would never get any GOP approval no matter what he did, same as DJT won’t get jack from the other 50%.

Do the math. Tough to get above 35-40% in that scenario. Trump is north of that now only because he’s feeding that far right chunk. Alienate them, and his numbers match.

Don’t confuse positive/negative efforts with approval ratings one way or the other.

Again can’t reply directly for some reason but

“Cory R

Apr 18, 2025 at 1:07 pm

A 20% haircut, on an asset that “never goes down” would be a crash, in my book.”

This is insane too. A 20% pullback is nowhere near a crash after home values have risen so sharply since COVID.

Eric,

If there is no reply button (4th comment in), then go up the thread and click on the first reply button you come to, which puts your comment in roughly the right spot, better than what you did here.

Ahhh. Got it. Thanks!

Wolf….

Mostly all antidotal….

But I just purchased a house in Mississippi, after selling my house central coast california

After watching houses for 6 months in Mississippi and Louisiana….

Prices in the South/East are dropping, and then after the price drop the houses are selling fairly fast.

Prices on central coast calif seem to be pretty solid, for now at least

Stock market bubble, housing bubble: These small up and down gyrations we have seen over the past few years are nothing compared to a real crash. The stock market and home prices are still very close to their tops, relative to their troughs around 2008.

Funny how Trump wants Powell to lower rates. The Fed only has power over short term rates. The markets determine long term rates (which I think is what Trump is talking about). Last year when the Fed used wrong data and cut 50 basis points in one day, long term rates shot up, worried about increasing risk of inflation accelerating. Long term rates will only decline if traders expect a recession and resulting lower inflation. Does Trump want a recession so he can get his lower long term rates? Sounds like it.

Bessent needs to have a talk with Trump about the difference between what determines short-term rates (the Fed), and long term rates (markets). Maybe Bessent is afraid of Trump. BTW, the current Fed Funds Rate is about average when you look at it since 1970. Not too high, not too low.

I highly, highly doubt Bessent is afraid of Trump. Likely he is in DJT’s ear already, has talked him off of various ledges. Trump will continue bashing Powell as a scapegoat, so he has an out if things go bad.

Agreed, this isn’t even CLOSE to a crash. The media headlines are hilarious.

“Denver metro’s housing market faces ‘price stagnation’ with almost 10,000 homes for sale

Homes are sitting on the market for far longer, but prices aren’t dropping yet.” I just love the way they print these articles screaming Shock and Awe like we should be outraged. Denver Mayor announced city will be spending $500 million on increase police and security downtown. $Trillions already spent on the homeless and migrants crisis. Politicians are starting to look like the biggest criminals on planet earth. Donating money or taxes to any organization these days should be vetted. To think 3 years ago folks were buying properties sight unseen, like Tom Cruise in Days of Thunder “ Just get me into high gear or the Damn race is Over for Us.”

Denver price has fallen 7% from pandemic height of 2022. If your house is not 8-10 out of 10 then you are bag holding if you bought 2022.

I live an hour north of Denver in fort Collins. I can’t stand Denver. It is such a crap hole

All you need to know is the following:

“As of 2024, New York City is home to approximately 349,500 millionaires, making it the city with the highest number of millionaires globally. This figure represents about 4.19% of the city’s population, or roughly one in every 24 residents”

That number of millionaires shrinks quickly when markets sag.

Only 4.19% in NYC? That’s it???? That sounds way low. I would guess that to be the proportion in most urban areas across the country.

You do know a mil ain’t what it used to be, right? That’s like only $300k in 1990!

Here’s the report from the midwest (Kansas City). We are trying to buy a house right now and couldn’t even look at one last weekend, because ALL four that we were hoping to see went under contract in 24 hours or less, some with multiple offers. We saw their listings on Thursday and were going to go see them on Friday, but they were already gone by the time we tried to book showings on Thursday afternoon.

I had an offer on another house the weekend before and was competing with two other offers, one of which was willing to go higher than I was.

Supply is limited and there seems to be ample demand in our local metro.

Let Trump layoff a few more federal workers in KC.

Not being personal but do you realize you bidding is the one of the reasons of ample demand.

Looks like you are hell bent on buying a house right now and I truly wish you the best on this.

Not houses, but the number of condos in Waikiki for sale has exploded compared to recent years.

The one site I regularly follow now has 770 condos listed for sale with a 116 of those under contract.

The usual number for sale at one time over the recent past was around the 500 area.

I’ll have to do more research, but a long with increased interest rates it may have to do with recent changes in rules and regulations regarding rental periods for condos as well as the availability of insurance.

Monthly maintenance fees for condos in Hawaii( especially in Waikiki) has also increased by huge amounts over the past few years as well increasing the carrying costs. $1000 a month seems to be the cheapest monthly cost.