The surge of the “nontraditional reserve currencies.”

By Wolf Richter for WOLF STREET.

The status of the US dollar as the dominant global reserve currency has helped the US fund its twin deficits, and thereby has enabled them: the huge fiscal deficit every year and the massive trade deficit every year. The reserve currency status comes from other central banks (not the Fed) having purchased trillions of USD-denominated assets such as Treasury securities, other government securities, corporate bonds, and even stocks. The dollar status as the dominant reserve currency has been crucial for the US, and as that dominance declines ever so slowly, risks pile up ever so slowly.

The US dollar lost further ground as top global reserve currency in 2024, according to the IMF’s COFER data released today. Total holdings of USD-denominated securities by other central banks (not the Fed) fell by $59 billion to $6.63 trillion at the end of 2024, from $6.69 trillion at the end of 2023.

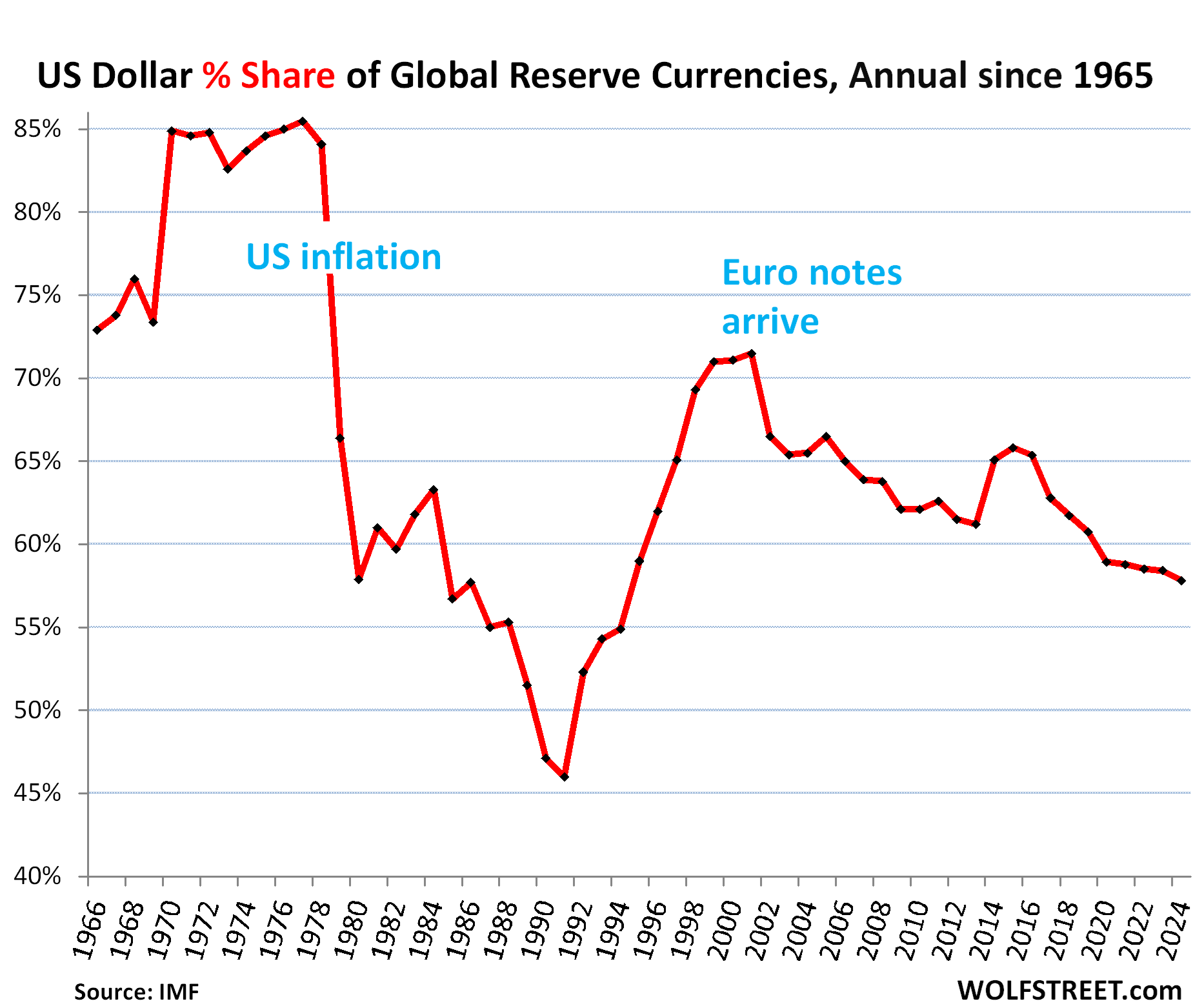

And the dollar’s share declined to 57.8% of total allocated exchange reserves at the end of 2024, the lowest since 1994, down by 7.3 percentage points in 10 years, as central banks have been diversifying their holdings for years to assets denominated in currencies other than the dollar, and into gold.

The dollar had already experienced a huge loss of global confidence before: Its share plunged from 85% in 1977 to a share of 46% in 1991, after inflation had exploded in the US in the 1970s and early 1980s. But by the 1990s, as inflation had been brought down and mostly stayed down, central banks loaded up on USD-assets again, and the dollar regained share as a reserve currency until the euro became a full-fledged currency.

USD-denominated foreign exchange reserves include US Treasury securities, US agency securities, US MBS, US corporate bonds, US stocks, and other USD-denominated assets held by central banks other than the Fed.

The major reserve currencies.

Central banks holdings of foreign exchange reserves denominated in all currencies, including in USD, edged up in 2024 to $12.36 trillion (from $12.35 trillion at the end of 2023).

Excluded from the total are any central bank’s assets denominated in its own currency, such as the Fed’s holdings of Treasury securities and MBS, the ECB’s holdings of euro-denominated bonds, and the Bank of Japan’s holdings of yen-denominated assets.

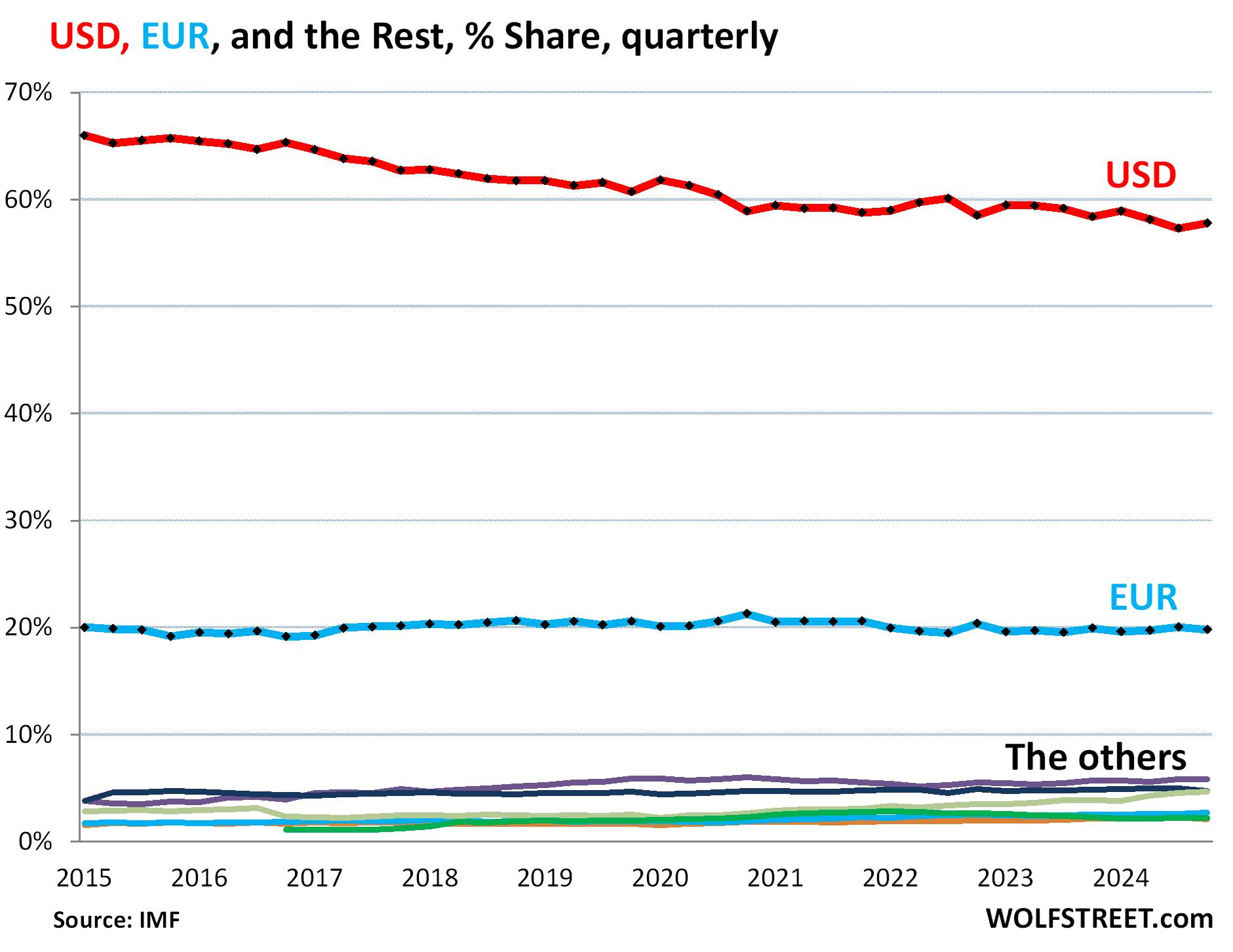

The USD is not losing share to the euro. The euro has been the #2 global reserve currency, with holdings at $2.27 trillion at the end of 2024. Its share has been around 20% for years, with a low of 19.1% in 2016 and a high of 21.3% in 2020. In Q4, the euro’s share was 19.8% (blue in the chart below).

So over the years, the USD has not lost share to the euro; it lost share to other reserve currencies, including “nontraditional reserve currencies,” as the IMF calls them. The colorful tangle at the bottom of the chart represents the largest of these other reserve currencies. More on those in a moment.

The surge of the “nontraditional reserve currencies.”

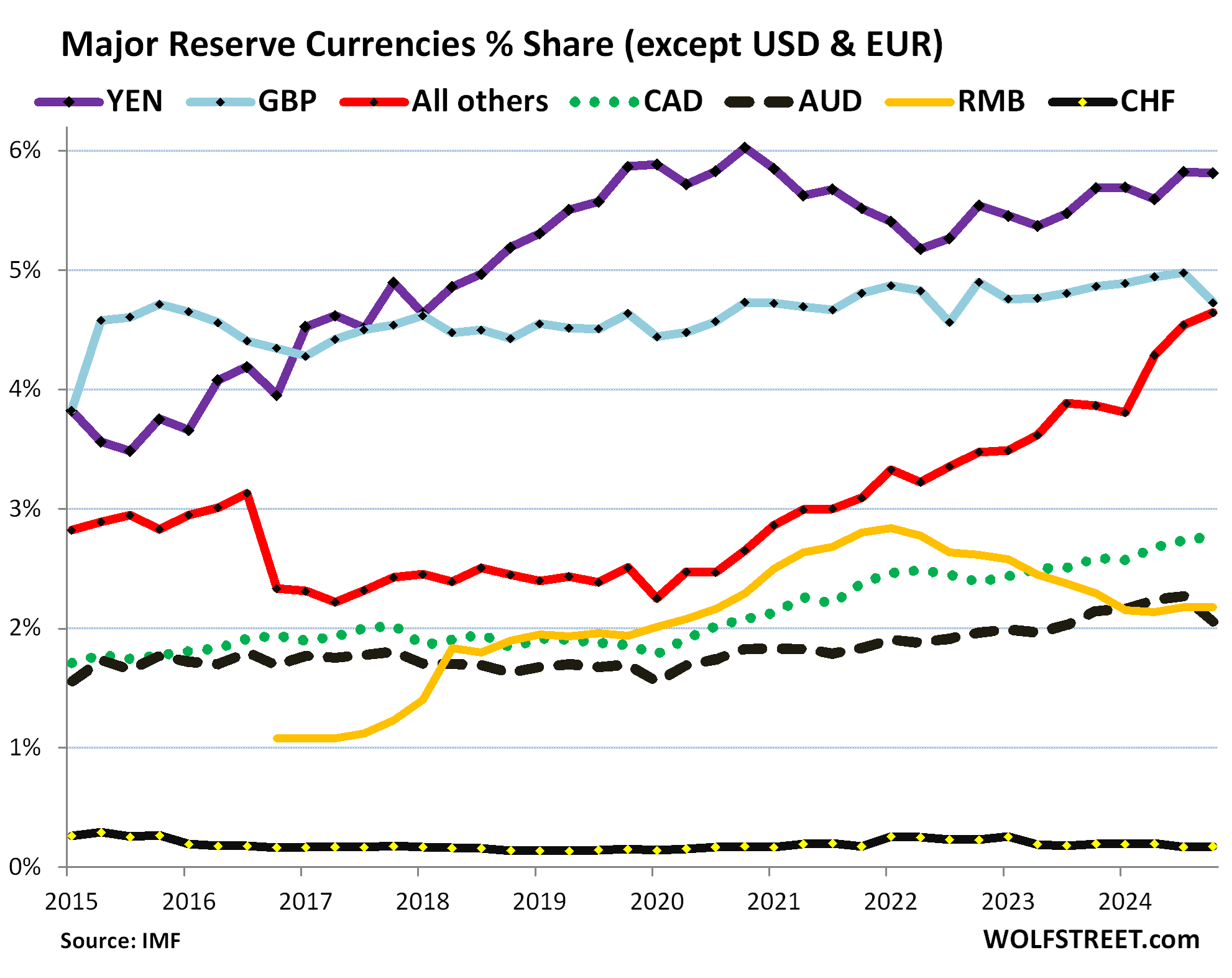

Some of these other reserve currencies have been gaining share at the expense of the dollar, especially the currencies in the basket of the “nontraditional reserve currencies,” that the IMF combines into “All others,” whose combined share has been surging since 2020 (red in the chart below).

But the Chinese renminbi has lost share. China is the second largest economy in the world, but its currency, the renminbi, plays only a small role as a reserve currency. And it has lost ground against the USD and other currencies since 2022. Central banks have not been enamored with RMB-denominated assets due to China’s capital controls, the RMB’s convertibility issues, and other complexities (yellow line).

Note the surge of the nontraditional reserve currencies combined in the “all other currencies” group (red).

- Japanese yen, 5.8% (YEN, purple).

- British pound, 4.7% (GBP, light blue).

- “All other currencies,” 4.6% (red).

- Canadian dollar, 2.8% (dotted green).

- Chinese renminbi, 2.2% (yellow).

- Australian dollar, 2.1% (black dotted).

- Swiss franc, 0.2% (black).

The other diversification: gold.

Gold bullion is not a “foreign exchange reserve” asset of central banks and is not included in the data above. Gold is a “reserve asset” not involving foreign exchange.

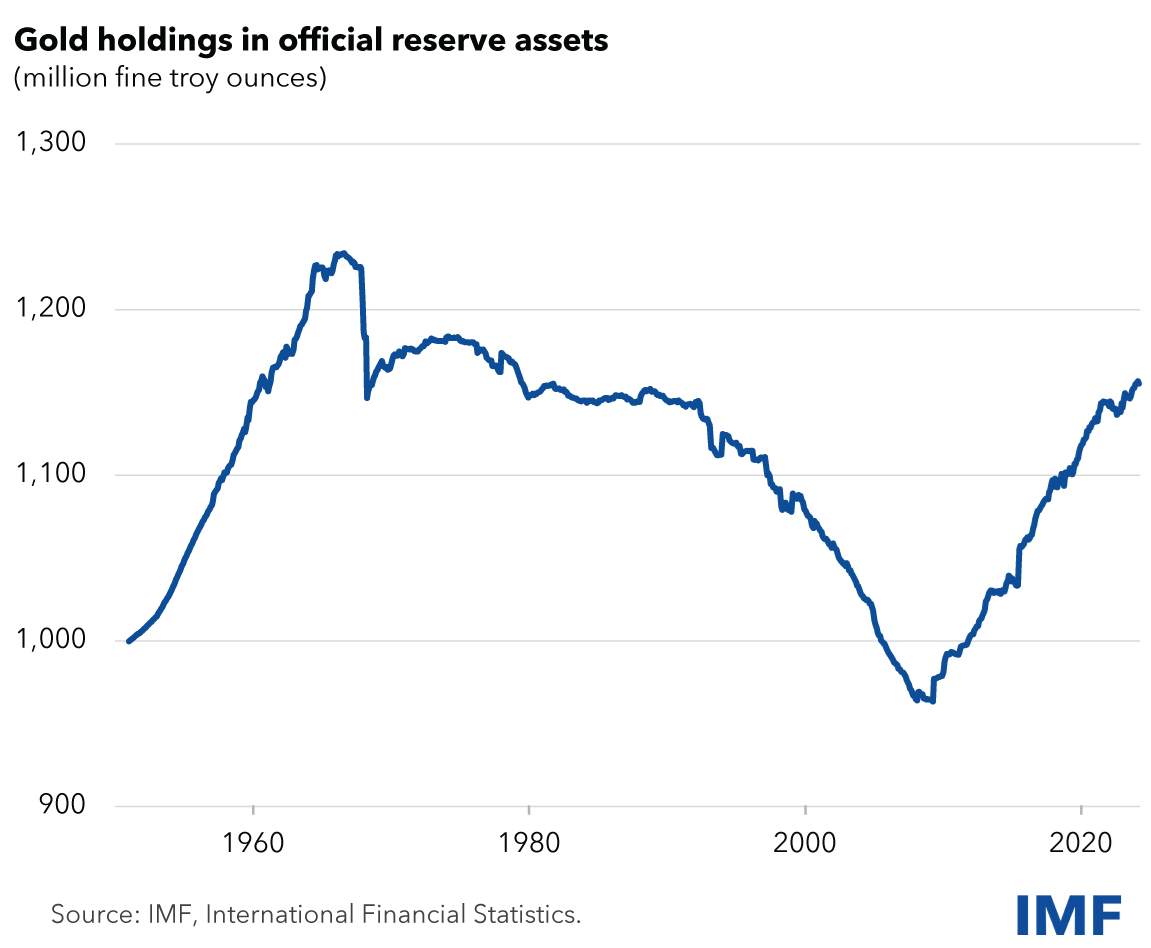

After four decades of unloading their gold holdings, central banks started re-adding gold about 20 years ago.

The top four holders have not changed their gold holdings in at least 20 years (based on IMF data released by the World Gold Council):

- US: 8,133 tonnes

- Germany: 3,352 tonnes

- Italy: 2,452 tonnes

- France: 2,437

But there has been a lot of movement below the top four, especially with Russia and China, which are now the #5 and #6 largest holders. And they did move the needle:

- Russia: 2,333 tonnes, little changed since Q2 2022. But between 2005 and 2022, Russia, one of the largest gold producers, had added nearly 2,000 tonnes.

- China: 2,280 tonnes. In 2024, it added 44 tonnes. It started piling on gold in 2009 and by 2015 had tripled its holdings

Since 2005, Russia and China combined have added 3,626 tonnes to their holdings.

Smaller holders have added large amounts of gold in 2024, such as Poland, India, Kyrgyzstan, Uzbekistan.

According to the IMF figures not updated for 2024, central banks’ gold holdings have surged by roughly 200 million troy ounces (6,221 tonnes) from 2006 to 1.16 billion troy ounces, driven largely by China and Russia. The increases in China and Russia alone represent nearly 60% of the total increase since 2006.

In dollar terms, these gold holdings at today’s price amount to $3.65 trillion. The IMF’s chart has not been updated for 2024, but it shows the historic moves:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Your first sentence says it all. The reserve currency status ENABLES the massive deficits. Like a drug addict or drinker or overeater who weighs 600 pounds, someone out there is probably enabling this destruction.

The pain of sobering up and going on a diet is going to be significant. Some say it’s too late and we can’t do it and the system as it is just has to play out until…? What? Death and liquidation of the US?

The Treasury should issue a new type of bond, an interest-only perpetuity bond that only foreign governments can buy. Basically, if they have massive surpluses with the US they can gather all that dollar currency from their domestic businesses and buy 2% “forever bonds” from the US. Or we can have tariffs. Whichever they prefer.

Well, it’s also true that you have to run a deficit in order for other central banks to accumulate your currency as reserves — every ledger has two sides and there are accounting identities in play here.

“Buy these shit bonds or we’ll beat you up.”

That’s… Sad.

Hmmm. That’s not really what I said. The US absolutely should have reciprocal tariffs equal to what other countries impose. Maybe that will help reduce the net trade deficit to zero. For instance 10% on European autos just like they have on US cars. That’s not “bullying”, that’s just fair trade. Trump is imposing 25% as a shock to the system but I’m sure over time if everyone agreed on 10% or 5% or 0% we’d get there. Would the Europeans agree to this? Or are they always going to want more protection and barriers for their markets than what the US has? Somehow a lot of people (yourself?) think it’s perfectly fair for things to be this way. Read all about it:

https://www.bbc.com/news/articles/cq8kn5v37wxo

The article you linked is stupid unadulterated BS. It alleges that American vehicles don’t sell in Europe because they’re too large. Which is idiotic ignorant bullshit. BMW, MB, Audi, Porsche, etc. sell the same cars in the US that they sell in the EU. Those SUVs, sedans, and sports cars are no smaller than US SUVs, sedans, and sports cars. Mid-size pickups are popular in Europe, and there are many mid-size pickups of the same mid-size in the US, such as the Ford Ranger, Chevy Colorado, Jeep Gladiator, Honda Ridgeline, Toyota’s Tacoma, Nissan Frontier… many of them made in the US. Tesla sells the same cars and SUVs in Europe that it sells in the US. Most are made in Germany, some are made in China, some are made in the US.

This bullshit that US vehicles are too large for Europe and therefore don’t sell is just idiotic bullshit. This is why outlets such as the BBC have such a shitty reputation. I’m glad that US funding of BBC via USAID has been stopped.

Wolf, I agree. It’s all BS. I just wanted to show the the 10%/2.5% disparity was real. Just happened to be a BBC link.

The issue is accumulation of huge debt petro dollar ponzi scheme for the past 50 yrs. So, the deep state which enforced it through Republicans know that it is not sustainable anymore since the interest payments for debt surpassed military spending. The DS chose democrats/liberals (for dedollarization) who have been preparing the groundwork since 2008 financial crisis (first nail in the coffin of fiat dollar). BRICS just playing along by doing trade in local currencies. Obviously, they don’t want another unipolar currency which also means end of the USD based globalization There has been no demand for treasury bonds since 2022. So, party is over for the west.

“There has been no demand for treasury bonds since 2022.”

🤣❤️ The 10-year yield today is at 4.2%, which is ridiculously low. It should be well over 5%. But a low yield means a high price, and a high price is a result of LOTS of demand for this stuff.

Until us either gives it’s debt holders a haircut and gets the budget in order or goes through hyperinflation and the USD dies to be replaced with the new dollar or whatever

Good afternoon.

One question:

Do China and Russia report their domestic production of gold that never leaves their shores?

I believe not. Thus I personally believe they have equaled or surpassed the #2-4 at the very least.

Just a thought.

Thank you.

Note that the topic here is central bank “reserve assets,” and NOT “gold production.”

Thank you!

This is gold held by central banks as “reserve assets.” It has ZERO to do with gold production. Same with Treasury securities: there are $36 trillion out there, only a portion is held by the Fed and other central banks. The rest is in the wild. The part that is in the wild is irrelevant for this article.

Yes, all gold production is fully reported from all global sources to the World Gold Council as well as all holdings in Central Bank reserves.

I would point out that currency risk is not a part of the normal American person’s day.

Gold is a category of asset that is currently indicating that the currency is being systematically devalued.

A rise in long term treasury rates would confirm gold’s rampage.

Hi Dang,

To one degree or another FX risk whether recognized or not influences everyone’s day, doesn’t it?

Ignorance is bliss of course, at least until it bites you.

Only another financial crisis could hurt the USD, I think. Luckily, I have lots of gold I bought mostly in 2005, when I feared a financial crisis that came only a few years later. I sold half my gold last year, when it was about 14% lower than today (in Euros). My fear now is that it may fall in a coming bear market. All this is really hard to guess, but I have done well so far.

Nice you enjoy rabid speculation!

Nice that you have been wrong about the gold price since it was around $2000.

Care to share your latest price prediction?

Check out Wolf’s imploded stocks section for more enjoyment; also IPOs and cryptos recommended by respected analysts until they clear their book.

The nice word is ‘distribution’.

Great job living through 2005 til today in the EU. EU has had some real challenges for sure . Especially energy though Nuclear Power is a great option .

In the short to intermediate term the price of AU will be determined by Fed policy. If the Fed turns seriously hawkish (i.e. Volker), I suspect the AU price to soften.

However, should political pressure be used to lower interest rates AU will go higher.

If the dollar collapses due to the demise of the Constitution and the rule of law (increasing probability in my estimation) AU would be the only store of value.

In the long-term who knows.

If the world goes to cr*p and somebody offers you a big fat gold bar for half of your food, medicine, ammo and firearms, do you take it? I certainly don’t. Is it really a store a value then?

…makes one seriously consider what maintains the reach and import of that nebulous term: “full faith and credit” when describing a nation’s currency…

may we all find a better day.

It will always be there, unlike digital assets that can go POOF in the night.

I worry about the USD being scheduled to depreciate somewhere between 20% and 40% every decade. We know 20% depreciation per decade is the floor under current Federal Reserve policy.

I have a 5% allocation to gold. Done very well on that lately.

Better stock up on glass jars, buttons, and fish hooks….

If the world goes to crap no “asset” will have any value so every time I see comments like this one it tells me that the person/people making them is not serious or hasn’t thought through the real reasons people hold gold.

So far the world has never gone to crap either

People hold gold for numerous reasons one of which is to protect themselves from currency depreciation.

Wolf, can you help me understand why a trade deficit is necessarily bad? I have a massive trade deficit with Safeway. I buy a lot of their stuff but they never buy anything from me. Is that bad for the “Ross” economy? As long as the buying isn’t funded by (consumer) debt, I don’t understand why it’s bad to buy more from someone than you sell to them.

Yes, the law of comparative advantage. Leave the groceries up to them. No need for you to start a farm. The US exports technology platforms to the world, let them manufacture our stuff.

To no longer have a real “base economy” or a true export economy and instead go all in on knowledge workers and exporting consultancy services will just delay a very unhappy ending to the world’s number one economy.

Ross,

Your analogy is total BS. Try to use your brain?

So maybe the the US should outsource most of its rate earth needs to other countries by to mine and process as they have a comparative advantage.

And might as well outsource pharmaceuticals as well.

No reason in the world for the US to have items such as these products to be sourced in country.

Nothing bad could ever happen to the US if those products were for some reason cut off…..gotta let that law of comparative advantage hold…..

“Is that bad for the “Ross” economy?”

It is if you don’t have sufficient income. If you ran perpetual deficits in your own economy, you will go bankrupt.

I’ll add this circa the early 70’s trade deficits were settled with gold until Nixon closed the gold window due to hemorrhaging of our gold holdings from about 25,000 tons after WWl to present about 8300 tons, if it’s still all there in Fort Knox.

Remember what Donald Rumsfeld said in the 2000’s “ deficits don’t matter”.

Wasn’t that Dick Cheney?

“Wasn’t that Dick Cheney?”

…Something something Germans, something something Pearl Harbor.

I stand corrected, it was Dick Cheney, I have trouble keeping the Neocons straight in my head.

Let’s give Rummy his fair due – he brought the concept of “unknown unknowns” to zeitgeist.

I bet he didn’t give a sh*t about deficits either

Actually, British Economist David Ricardo said that. He was noting that high government spending was a problem no matter whether it was financed through higher taxes or deficits. Many modern economists disagree.

>Remember what Donald Rumsfeld said in the 2000’s “ deficits don’t matter”.

Not only Cheney, but I think all US politicians say that when their party is in power. At least they act that way.

The 8,133 metric tonnes of gold owned by the US Treasury was never at any point in time ‘all there’ at the US Mint facility in Fort Knox, KY but rather distributed around various US Mint facilities with much of it stored at the West Point, NY facility.

But you would only run a trade deficit with Safeway if you didn’t pay your bill with cash once you check out. If you put it on a credit card then you are running a deficit but once you hit your credit limit, unlike the US which continues to increase its debt ceiling, you will grow hungry. The difference is the accumulated debt. If the US could balance its books like you or I have to then there would be no deficits.

Ross, Safeway has a deficit with the labor market and vendor market. It buys a lot of labor and stuff from vendors but doesn’t supply labor or products to vendors.

Deficit should be aggregated at some logical level not at any random level.

For historic reference see the Roman Empire. It was all fun and games as long as they were able to keep conquering and thus the money flowing to pay for all the silk, dyes, ivory, precious gems, incense and other luxuries from the East. But over the centuries they kept debasing the Roman currency which was not sustainable after a while.

Hi Ross,

Your ‘trade’ deficit with Safeway is offset by your ‘trade’ surplus (infome) from other sources. Try running that Safeway deficit without the offsetting revenue and see how that works out for you.

Correct information. I would only add that everyone should have seen this coming with the announcement of Basel III and the demotion of government debt and the promotion of gold back to a “tier I” reserve asset. Wolf can correct me if I am wrong but I believe the deadline to be compliant with Basel III is this July.

Interesting times.

The total amount of gold in the world of which 70% is in the form of jewelry widely dispersed around the world is worth less than 1% of current global assets and has no monetary relevance whatsoever in today’s world where other assets far outshine gold and render it irrelevant.

So you keep saying as the price keeps going up and central banks keep buying.

Just released DB 1st quarter assets performance report just released and guess which asset came out on top?

Yep, gold.

The important thing to monitor is the volume of short-term securities held by foreigners. That’s an indication of a move out of the U.S. $

I discussed this here:

https://wolfstreet.com/2025/03/18/who-holds-the-ballooning-us-government-debt-even-as-the-fed-and-foreign-holders-unloaded-treasury-securities-in-q4/

Foreign entities held in total:

$7.31 trillion in long-term securities

$1.2 trillion (14.1%) in T-bills.

That ratio of T-bills to total foreign holdings has been between 12.1% and 14.6% since mid-2020. Before the pandemic, it was in the 10% range.

It’s also a function of T-bills having had higher yields during the time of the inverted yield curve, without the duration risk of longer maturities. T-bills became relatively more attractive during that time.

I’ve been absent from comments for a year or more. In the advance of gold from $2000 to over $3000 we might be in a seminal moment. I’ve been a metals guy since circa 1973 and a part time coin dealer since 1978 and followed and invested in this market.

I remember gold at sub $300, Platinum at plus $2000 when gold was $400, and palladium at plus $1000 when gold was $490. Also silver at $50 in 1980 and 2011.

While I don’t have liquidity now to invest more, I might trade gold for silver or platinum which I see potential gains in the future.

For anyone with no solid assets, land or metals, I see a potential especially for platinum. Platinum is ten times rarer the gold and originates from unsure sources, mainly Russia and South Africa.

At this point in time platinum looks yummy, and might have a great future with fuel cells and hydrogen development.

Gold has an inherent or intrinsic value of no more than $20 per ounce and it is increasing becoming nothing but a speculative commodity of little to no relevance exactly like BitCON.

Why $20? Jewelry is way more expensive!

Because you need to buy it at the speculative asset (“physical Bitcoin”) price to use it for jewelry. Otherwise it’s uses are industrial where its high electrical conductivity and/or high corrosion resistance have value. But those uses can be satisfied by a micro-thin plating.

Oh, it also makes a great coating for brass instrument mouthpieces. Better “feel” than silver on the lips.

If it were not made so prohibitively expensive by speculation, there might be more uses other than the above and jewelry, so its value might settle above $20/oz.

If this forum was an Economy class you would get an F. Yes you failed, stop commenting BS here , nobody cares what you write. Go back and repeat the class.

Everything is speculative in this market including RE and S&P 500. It all trades on the ability of central banks and governments to artificially stimulate well into the future. Yet, we know that may not be wise or achievable.

I certainly do not advocate the recent excessive federal deficits. But some economists say that running some degree of deficit, or at least trade deficit & a negative net international investment position, is the price you pay to be the world’s reserve currency.

It’s the other way around, as I said in paragraph #1: Having the world’s dominant reserve currency helps you fund the twin deficits, at least for a while until the gig is up. Having the dominant reserve currency ENABLES you to have the twin deficits.

The problem arises when you no longer have the dominant reserve currency, when foreign central banks no longer buy your financial assets. How are you then going to fund those twin deficits, and the accumulated pile of debt? That’s not a trick question. It ends up in a mess.

Bingo Wolf.

Exactly.

Yes. Precisely why certain types of assets, collateral, and reserve assets (i.e. gold) are being pursued and purchased. Sorry Ben, but yes, the deficits suddenly matter.

Yep, we are exporting inflation

It’s a circular argument because while we do pay a price for being the world’s reserve currency as we sink further into debt we become a less welcome reserve host. Some would argue we have paid too steep a price for dollar dominance and all it has done is enable the elected criminals who spend our money and grow our deficits with impunity.

eight-to-ten-year cycles of boom and bust are the normal fluctuations of the capitalist economy. Wild speculation and overproduction are followed by collapse and panic. The post-Soviet period has been no different. However, as real growth possibilities declined, speculation and credit became the principal manner by which the U.S. sought to prop up its entire order. The aftermath of the 2008 “Great Recession” exposed this clearly. Facing a possible depression, the U.S. coordinated a historically unprecedented credit and monetary expansion. This created anemic real growth but a gigantic growth in asset prices. Even to most bourgeois economists, it is obvious that this simply meant setting the conditions for an even greater collapse down the road. For over ten years, the playbook has been the same at each sign of faltering growth: kick the can down the road by increasing credit. During the Covid-19 pandemic, this was pushed once more, to all-time highs. To solve the consequences of shutting down huge swaths of the economy, the capitalists simply printed money. This was too much, and finally the possibilities of this approach have reached their limit with the inevitable “return of inflation.”

The drastic increase in interest rates and the end of QE in the United States is sucking vast quantities of liquidity out of the world economic system. As Warren Buffett famously said, “A rising tide floats all boats…. Only when the tide goes out do you discover who’s been swimming naked.” After a decade and a half of easy money, gigantic segments of the economy are bound to have been “swimming naked.” When the buck stops, the results are bound to be catastrophic. Since the U.S. is at the top of the capitalist food chain and essentially controls international credit conditions, even if it turns out to be the epicenter of the crisis it will be able to use its dominant position to make the rest of the world pay for the consequences. This will be particularly devastating for countries of the developing world, many of which are already in deep crisis, such as Sri Lanka, Pakistan and Lebanon. But the consequences will be global and will necessarily lead to further blows to the world order, including from powers the U.S. today considers allies.

A significant part of the economic establishment is either lying or willfully blind to the prospects of the world economy. Certain parts of the social-democratic left have argued that high government debt levels are of no great concern and that working people would benefit more from low interest rates and more debt than from the current policy of higher interest rates. This is an echo of those in the bourgeoisie who wish to kick the can one more time, hopefully past the next election. The truth is that all policy alternatives—whether high debt, high inflation or deflation—will be used to attack the living standards of the working class. The fundamental underlying problem is the huge imbalance between the capital that exists on paper and the actual productive capacities of the world economy. No financial wizardry can solve this problem. The only way out is for the working class to take control of the political and economic reins and reorganize the economy in a rational way.

Yes, we are perhaps in an inflection period based on our printing of money/credit since 2008. Or perhaps not: the dollar came back from the 1991 post-inflation low, in its world reserve proportion.

On the other hand, the Renminbi’s outcast status in this regard stands as a stark cautionary example of why we should be very careful with meddling in central bank independence.

How can there be a positive or neutral trade balance when there’s also demand for dollars from abroad to act as reserve currency?

We cannot have at the same time the US dollar as the main reserve currency and a positive or neutral US trade balance.

Your assertion is nonsense. See the euro: huge trade surplus with the rest of the world outside the Euro Area and #2 reserve currency.

It’s the other way around, as I said in paragraph #1: Having the world’s dominant reserve currency helps you fund the twin deficits, at least for a while until the gig is up. Having the dominant reserve currency ENABLES you to have the twin deficits.

The problem arises when you no longer have the dominant reserve currency, when foreign central banks no longer buy your financial assets. How are you then going to fund those twin deficits, and the accumulated pile of debt? That’s not a trick question. It ends up in a mess.

How do you explain the period from 1945 to 1970 when the US had both the main reserve currency and a positive of neutral trade balance?

In 1945 everyone else was bombed to bits. We flooded the world with quality inexpensive goods after transitioning from wartime to postwar production. US manufacturing was unparalleled during WWII, and for many years after.

I was asking Perco this question, because Perco said a country can’t have both the main reserve currency and a positive or neutral trade balance. History says that’s incorrect. What you’re saying is correct in the immediate aftermath of WWII. A chart from the St. Louis Fed shows the positive US trade balance spiked to 4% of US GDP immediately after WWII. However, it subsided by 1950 and remained roughly between 0 and 1% for the next 20 years. The point being that it is entirely possible to run a goods trade surplus and still be the main reserve currency.

See “Historical U.S. Trade Deficits” from the St. Louis Fed.

The Korean War, which began in June, 1950, initiated the chronic balance of payments deficits that persist to this time and which will probably continue as long as foreigners are willing to increase their net investments in this country.

The U.S. has had a net liquidity deficit in every year since 1950 (with the exception of 1957). Up to 1976 (when the private sector contributed its first trade deficit ) these deficits were entirely the consequence of excessive U.S. government unilateral transfers to foreigners (re: foreign policy – solely our far flung military bases and personnel).

During all this time the private sector was running a surplus in all accounts: merchandise, services and financial. The Vietnam Ten-year War administered the coup d’etat to our gold bullion standard.

By 1968, in an effort to keep the dollar at the $35 par, we had exhausted nearly two thirds of our monetary gold stocks, or approximately 700 million ounces to about 260 million ounces.

“2. British pound, 4.7% (GBP, light blue).”

“Sound as a pound” is sarcasm nowadays. Most of that big spurt occurred in first quarter 2015. The pound is not something I would rely on for anything. The UK economy is a mess.

The yen is actually below its third quarter 2021 print.

Wolf typo: “Note the surge of the nontraditional reserve currencies combined in the “all other currencies” group (yellow).”

The (yellow) should be (red) unless I am brain-damaged.

Speaking of which, as Wolf points out, all the action since 2020 has been in “all other currencies”. I wonder what countries those are.

Wolf, how does this relate to a weaker dollar? I keep reading that a goal of the mar-a-lago accord is to weaken the dollar, would losing ground as the reserve currency weaken the dollar in comparison to other currencies?

Well, if they’re going to scare the world out of USD investments, then the value of the dollar against other currencies might drop, which would be a “weaker dollar.” But the “strong dollar” has contributed to the cooling of inflation from mid-2022 through mid-2024. If the dollars weakens a lot, and make imports more expensive, people are going to scream that this is inflationary?

MW: Nvidia’s stock hasn’t had a month this bad since the last big crypto crash

Its valuation, like that of Tesla’s, had long ceased to bear any resemblance to economic reality.

The BIS classified gold as a Tier 1 asset and is now comparable to US Treasury securities.

That has numerous implications. For one it means gold can be counted by banks as part of their capital base and be held with zero capital requirements.

Many central banks consider gold to be a foreign exchange equivalent as well. The holding of gold as a foreign exchange equivalent also has the benefit of zero counterparty risk.

Other foreign exchange assets held by central banks all have counterparty risk as Russia has found out.

And of course gold hit another milestone today as well with silver being smacked down again.

Look for more fireworks as the 1 July COMEX Basel III deadline approaches.

The BIS should have given the same status to silver as it did to gold.

All gold ever mined is worth less than 1% of all global assets.

Beach Dude: Gold does not need to be this or that % value of all the other assets in the world—nothing does, it’s irrelevant. All gold is asked to do is to preserve its purchasing Power for its owner in relation to those other assets—something it has done quite well over time. All fiat currencies have failed miserably at holding purchasing power over much shorter time frames including our mighty dollar.

You do not understand what a “currency” is what and an “asset” is. They’re NOT the same thing.

“Central banks holdings of foreign exchange reserves denominated in all currencies, including in USD, edged up in 2024 to $12.36 trillion”

“In dollar terms, these gold holdings at today’s price amount to $3.65 trillion”

Looking at how price of gold (expressed in USD) behaves (goldprice dot org), it is possible, and even likely, that in 10 year value of gold held by central banks will exceed value of all fiat moneys taken together in all exchange reserves of all cental banks.

Once again, the aggregate value of all gold ever mined is less than 1% of all global asset even at today’s price of gold making it not financially relevant at all to anything.

You have made the same comment three times. Do you think that continually repeating the same nonsense will buttress your argument? Maybe you should try all caps?

What I stated is 100% correct. It appears that some of you folks just don’t comprehend the actual facts at all. Once again, all of the gold ever mined – 70% of which is widely dispersed around the world in the form of jewelry – is worth less than 1% of current global assets.

Good point. LOL

Sounds like someone does not have any gold. You are missing the point! Ever if it is only one percent at todays prices, all that means is the other 99 percent is fiet currency!

If it even went to 2 or 3 percent it would make some very well off. It is about diversification.

Bear Hunter,

You do not understand the difference between “currency” and “asset.”

Why has the GBP such a high weighting? I would rather have a resource rich G7 as a reserve currency – Canada/Australia? Post BREXIT UK did nothing that they could have ; No US/China trade deal, no tax cuts, no reversal of insane EU rules/regulations, zero progress on AI or energy policies.

Yes, people thought that the GBP share would plunge after the Brexit vote. But its share only declined a little for a year and a half and then rose again. The UK is a global powerhouse in financial services, London is a huge trading hub and financial center. It runs a fairly liquid bond market and a global stock market. So there are reason…

I wonder why the A$ is even held at all.

The economy is small compared to others and the population is small as well.

It has a huge and growing government debt with deficits now projected for the next ten years.

It has hitched it’s future to China and the only things that has kept its economy afloat has been selling stuff to China and importing people.

It depends on what your “base” currency is. If you’re an American with expenses, retirement, etc. all denominated in dollars, I wouldn’t see any reason to hold GBP.

To a European or Japanese, the pound looks pretty good as a carry trade. UK 10 year is ~50bp above US 10 Year and 200bp over German debt. Plus, if you live in a place like Greece or Italy and the Euro falls apart one day in 10 or 20 years, you aren’t going to want to have your whole savings parked in your Greek or Italian savings account or your country’s debt.

Given the geopolitical upheavals at the moment, there’s a good case for non-Americans (aka the rest of the world) to not put all their eggs in the dollar basket.

AUD or CAD are resource rich, but commodities can be pretty volatile. CAD was above parity with the USD in 2011, but by 2016 the USD was worth 1.40 CAD when WTI went bust down to $35.

The UK actually secured a pretty good Brexit deal for The City (finance lingo for London). The British countryside is phucked, but they retained all of their overseas territories used for money laundering, tax evasion and all of their consultants and finance bros remain important globally.

Also – many continental-European are listed on the London Stock Exchange in GBP as capitalism is just sooooo much simpler in the UK compared to the EU. Some EU leaders suggested creating a common stock exchange with lower costs and a more IPO-friendly network for small-caps to compete with London, but nobody is really wiling to give up their national stock exchanges.

*continental-European firms – that word was missing for full clarity.

The EU requires IFRS accounting principles, while in Britain the UK GAAP is the standard – which is a dealbreaker for many fresh IPOs.

The UK couldn’t do any of those in reality. US trade deal would have let chlorinated chicken into EU via NI of there was no physical border so was specifically ruled out by withdrawal agreement.

Proposed tax cuts collapsed MaY’s government when the markets panicked at the implementation.

Reversal of EU regulations was mostly abandoned because the UK market is too small to have it’s own regs so manufactures would just be manufacturing to eu standards anyway, adding more would have been comolexand there would have to be two standards one for ni and one for GB and the people were up in arms at losing EU rights and there is a fair competition clause in the withdrawal agreement to stop that,it was the price the UK paid to get the benefit of the withdrawal agreement.

So gold is actually the second most popular reserve medium, after USD and before EUR.

Gold is a “reserve asset” but not “foreign exchange reserves,” such dollar-denominated investments because gold is independent of currency. So it’s not even listed at all among foreign exchange reserves. I added it as a “reserve asset” because that’s what central banks are also diversifying into.

So gold “competes” with foreign exchange reserves to be a “reserve asset?”

I assume that the basis for the rediscovered competitiveness of gold on CB balance sheets around the world lies in the very fact that that it IS “independent of currency, “ and due to production/supply realities, less manipulable.

Add to that the fact that physical gold has no counter-party risk. In a world where counter-parties resort to money manufacturing, a reserve asset with no counter-party becomes king (at least for a while.)

Does the Fed actually “own” the gold on the Fed’s balance sheet, or is the gold owned in some sort of a “gold certificate” form backed by bullion holdings at U.S. Treasury?

The Federal Reserve has practically no gold on its balance sheet and its only real activity related to gold is to rent out its vault in NYC for storage of gold. By contrast the US Treasury owns around 8,133 metric tonnes of gold much of which is stored at the US Mint facility in West Point, NY.

Wolf – when adding gold reserves data from 2024, is there an acceleration or a continuation of the same pace since ’05 ?

Isn’t this merely semantics? The effects of gold holdings are what counts, aren’t they?

Ya-hoo!!! Inflation, tariffs, soaring insurance costs, home prices in the stratosphere and now the U.S. dollar to become the reserve toilet paper of the planet. 🌎. Look out, Charmin!

Didn’t Prince have a song ‘Party Like it’s 1999’?

India’s private gold stash( by the public multi generational wealth passed on by mother to daughters) estimated at 25,000 tonnes, exceeds the combined gold reserves of the world’s top 10 central banks—including the US, Germany, China, and even the Reserve Bank of India. Possible because out of the 1.4 billion people hardly 5% file/pay tax. balck parallel economy is huge. Gold jewellery and bar are “to go”the stash for un reported incomes

DXY up again.

“as that dominance declines ever so slowly, risks pile up ever so slowly”

Another famous quote…

“How did you go bankrupt?”

“Slowly, then all at once.”

Wolf, thank you for providing some clarity to the general public. Even in the academic Economics profession understanding of these issues has been an opaque area for decades.

These comments above are illuminating the lack of understanding of how this international trade system has supported America, and allowed ordinary Americans to benefit from the ability to buy anything, anytime, at the world’s lowest prices.

The problem with the current dollar system is the unsustainable level of debt here in America. The Federal Reserve beginning to finally understand that it can raise rates to combat inflation and slow down the domestic economy. However, the effects on the Treasury debt interest costs are beginning to swamp the ability to raise taxes to even cover the interest payment at the current rates. An increase will start forcing a debt spiral, which will just print more, etc.

Further, pulling back on international trade will cause tremendous international problems. Nobody has seen the distortions of such large tariffs in our lifetimes, and the economic disruptions to large exporters and importers does not have much of a track record.

Further, without an obvious new currency, the flailing about we see for stores of value by everyone on the world stage is the result of this sea change in the American post Nixon system. Change is here, there is no way to obscure it now, and as long as we don’t try to go back the decade of relative stability, we will all figure out our next actions in reaction to the markets.

This presupposes the outcome of world war is avoided, which was the result of both world trade reorganizations of the early 20th Century.

I find it funny that research I did 30 years ago that was denigrated as “contrarian” and “unpublishable” has finally found a relative time. The depression in agriculture that is upon us as a result of these policy choices is already baked in the cake. We are just going to be eating it soon.

Yes, lower prices for companies (therefore higher profit margins), not necessarily lower prices for consumers, as you know if you ever bought a new car.

And it comes at the cost of dismantling US manufacturing, US manufacturing expertise and engineering, US manufacturing infrastructure, US manufacturing research, US manufacturing supply chains (robotics), in favor of becoming totally dependent on foreign manufacturing. We cannot even build ships anymore in the US. The big new tower of the San Francisco Bay Bridge couldn’t even be built in the US anymore. It had to be built in China, LOL. This is also part of the US wage repression system.

The ONLY beneficiaries of dismantling manufacturing in the US are corporate profit margins, executive bonuses, and stock prices. Fuck them. What matters is the US economy, and manufacturing is hugely important in it.

I cannot believe the stupid bullshit people post about abandoning manufacturing in the US to other countries… that this is somehow good for the US. Are you on Xi’s payroll???

Australia no longer has any domestic automobile production as a result of high costs, labor union problems, and a small market.

It has lost almost all the expertise in those fields as well as all the associated infrastructure.

All cars are now imported, but strangely enough the tariffs put on cars to protect domestic products still remain.

As the market is small some companies are planning to reduce models supplied to the market such as Honda.

Mitsubishi didn’t even bother to upgrade its ASX model to comply with new braking systems and new ASX’s can no longer be sold in Australia

Other Mitsubishi models were also affected as well as other companies’ products.

Bravo! Bravo! Bravo!

Well, Xi would not want to hear what I have to say, so not paid by ccp. The more specific target I am referring to is the American export agricultural sector. They will just feel massive pain. Ironically, the consumer is going to be the big winner, because food will become even cheaper over the next decade. Huge quantities of wheat and corn are exported, and those are going to be the most vulnerable to the retaliatory nature of tariffs.

The manufacturing onshore will eventually have all those benefits you cite. What I am talking about is the pain.

“The ONLY beneficiaries of dismantling manufacturing in the US are corporate profit margins, executive bonuses, and stock prices. Fuck them. What matters is the US economy, and manufacturing is hugely important in it.”

Put that (in your unique way of summarizing the world) on a mug and we’ll make it worth your effort. Promise. Damn, I’m impressed.

What can we learn from the last time the US $ share of global reserve currency collapsed in the 1970s and 80s? Wolf mentions some of the causes, what were the effects on the Global economy at the time ? What currencies gained dominance in the period of US decline in the 1980s? Also other than the stabilization of inflation what other factors allowed the US to regain its dominant position as top reserve currency?