QE was a huge gravy train for taxpayers. But then came the hangover.

By Wolf Richter for WOLF STREET.

The Fed released its financial report for the third quarter on Friday afternoon. The two items we pay attention to in the era of the money-losing Fed are its operating losses and its “unrealized” losses.

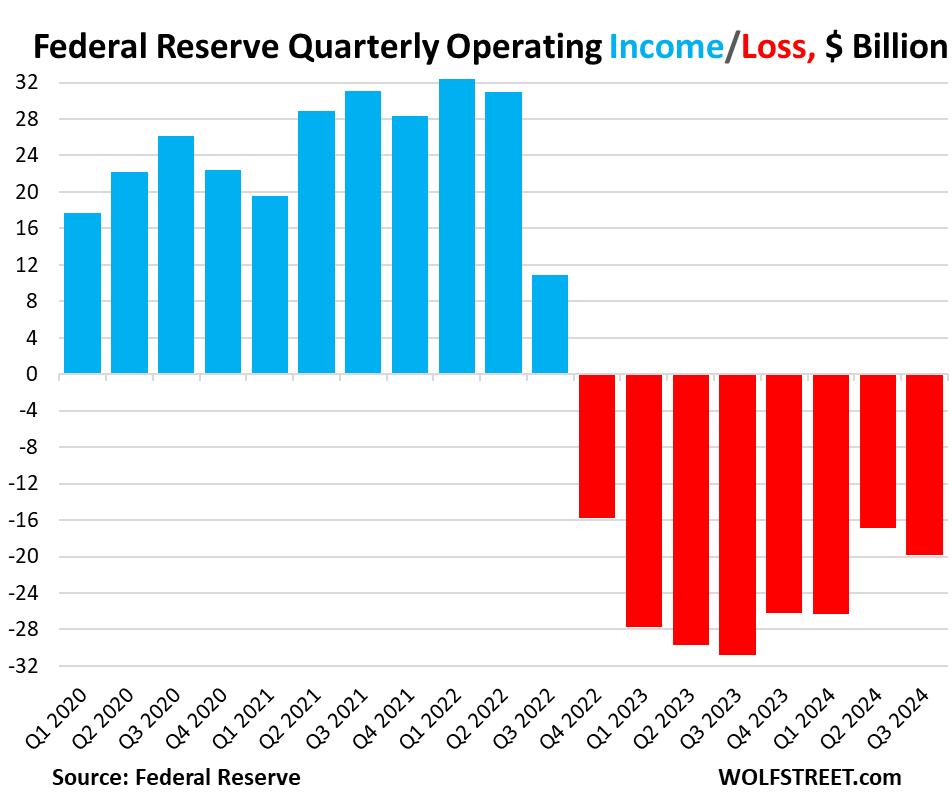

Operating losses.

The Fed incurred $19.9 billion in operating losses in the quarter, down from $30.8 billion in Q3 a year ago, but up a little sequentially from Q2. Those losses are largely the difference between the interest income it earns on its huge but shrinking portfolio of Treasury securities and MBS, and the interest it pays to banks and money market funds on the shrinking amounts of cash they keep at the Fed.

The expenses of operating the Federal Reserve System – the Board of Governors of the Federal Reserve and the 12 Regional Federal Reserve Banks – are also included.

When the Fed started hiking its policy rates in early 2022, the interest rates it paid to banks (Interest on Reserve Balances, IORB) and the interest it paid money market funds (overnight reverse repos, ON RRPs) rose in tandem because they’re two of the Fed’s five policy rates. And so the interest expense shot up with higher rates, even as the combined balances began to decline due to QT.

But the interest income was capped as the Fed held an $8-plus trillion portfolio of longer-term securities whose interest rates didn’t go up. And then, as QT reduced those holdings, interest income from them also declined. As of the last balance sheet on Thursday, the Fed’s QT has reduced its total assets by $2 trillion, to $6.92 trillion.

So the interest income was capped and then started declining under QT, but the interest expense shot up with the higher policy rates, and by September 2022, the Fed started losing money.

On a quarterly basis, Q4 2022 was the first quarter when it was in the red. Losses worsened as the Fed hiked. Then as QT reduced liquidity in the financial system, the combined balance of reserves and ON RRPs began to decline, and the interest expense began to decline, and a year ago, the losses began to decline for the first time.

For the first three quarters of 2024 (YTD), the Fed’s operating loss declined to $63.1 billion, from $88.1 billion in the same period last year.

| Federal Reserve System, quarterly, in billion $ | |||||

| Q3 2024 | Q2 2024 | YTD 2024 | YTD 2023 | YTD Change | |

| Total Interest income | 38.0 | 44.7 | 121.5 | 132.7 | -11.2 |

| Interest Expense | |||||

| ON RRPs | 10.2 | 10.9 | 33.1 | 86.6 | -53.4 |

| Reserves | 46.9 | 48.3 | 145.7 | 128.0 | 17.7 |

| Total Interest Expense | 57.2 | 59.1 | 178.8 | 214.5 | -35.7 |

| Other income | 1.6 | 0.0 | 1.3 | 0.2 | 1.0 |

| Operating expenses | 2.3 | 2.4 | 7.1 | 6.6 | 0.5 |

| Net operating loss | -19.9 | -16.9 | -63.1 | -88.1 | -24.9 |

For the full year 2024, the operating loss will likely fall below $85 billion. For the year 2023, the Fed reported an operating loss of $114 billion. Depending on its future interest rate policies and the pace of QT, it will take several more years before the Fed stops generating operating losses.

“Unrealized losses.”

The Fed’s cumulative “unrealized losses” declined to $818 billion on September 30, from $1.075 trillion at the end of Q2, and down from $1.302 trillion at the peak, which was the end of Q3 2023. They declined mostly because longer-term yields continued to fall through Q3.

But that decline in yields ended in late September. Since then, yields on longer-term Treasuries and MBS have risen sharply. We have discussed this, and what it did to the yield curve, a lot, most recently here. So if this continues through December, the Fed’s cumulative unrealized losses might be back near the $1 trillion mark.

These cumulative unrealized losses are the difference between the securities’ amortized cost (which will be equal to face value by the time the security matures) and their market value at the end of the quarter:

- Securities, amortized cost: $6.88 trillion

- Market value on Sept. 30: $6.06 trillion

- Cumulative unrealized loss: $818 billion

The Fed bought most of these securities years ago when yields were far lower than now. As market yields rose over the past three years, market values declined. As securities get closer to their maturity date, the unrealized losses diminish and vanish entirely at maturity date when the holder gets paid face value.

In terms of MBS, they’re paid back mostly through a stream of passthrough principal payments as the underlying mortgages are paid off when the home is sold or refinanced, and as regular principal payments are made. When the pool of underlying mortgages shrinks enough, the MBS is “called,” the holder gets paid face value for the remaining balance, and the remaining mortgages are repacked into a new MBS. It’s unlikely that any of the MBS will still exist by their maturity date. The Fed will get its money back much sooner.

If the Fed never sells these securities, but just takes the cash when they mature or when passthrough principal payments are made, it will not have any actual (“realized”) losses. Securities in the Fed’s portfolio mature all the time, but many of them won’t mature for years, and some for decades.

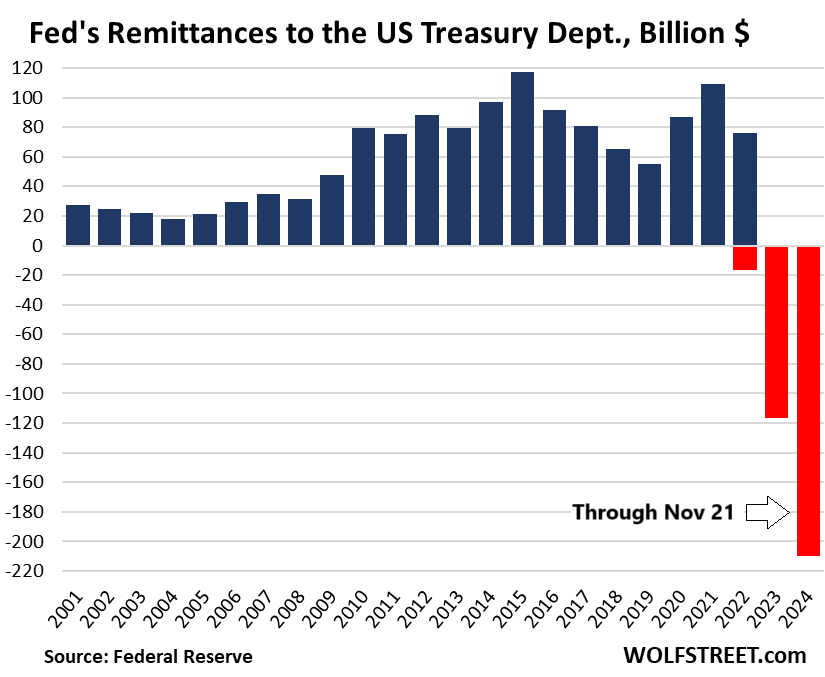

Losses don’t matter to the Fed but matter to the Treasury Department.

Since the Fed creates its own money, it cannot become insolvent. So in essence, losses don’t matter to the Fed.

However, losses matter to the Treasury Department. The Fed has to remit nearly all of its operating income to the Treasury Department (like a 100% income tax). Those remittances stopped when the Fed stopped generating operating income. The losses pile up on the liability side of its balance sheet as a negative amount due the Treasury Department.

As of the last balance sheet on Thursday, that negative amount reached -$210 billion (last red column in the chart below), representing the total cumulative operating losses from September 2022 through Wednesday.

The Fed will continue to have declining operating losses for a while, and the cumulative negative amount will grow though more slowly (red columns). When the Fed finally generates operating income again, it will go against that negative amount and whittle it down over time, and remittances to the Treasury won’t restart until the negative balance has been reduced to zero, and then turns positive. This will take many years.

QE was a huge gravy train for taxpayers, generating remittances of $1.1 trillion from 2008 through Q3 2022. But then came the hangover.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you for the analysis. I feel like this time there is a lot of “so whats” left unanswered for the reader or average audience not in the ins and outs of these processes.

With the right attitude, everything can be “so what.” Modern version of Zen?

The Fed prints money and loans it out at interest.

Only a government agency could lose money with a racket like that

Actually, the Fed (like all central banks) sends paper money (in the Fed’s case, Federal Reserve Notes, the paper dollars in your pocket) to banks on demand, in exchange for assets such as Treasury securities. There are currently $2.35 trillion in paper dollars out there (“currency in circulation”) for which the Fed got $2.35 trillion in collateral that is earning the Fed interest. That right of “Seigniorage” is how the Fed (and all other modern central banks) was funded before 2008 (before QE). It didn’t have losses back then because nearly all its Treasury securities were T-bills, and there are no significant unrealized losses with T-bills. And it didn’t pay interest on reserves and ON RRPs. And it remitted its profits to the Treasury Department. That has been the classic setup of the Fed from its beginning through 2008.

If I understand you correctly, I agree.

The mechanics of Fed operations (and profit/loss) can be convoluted and counter-intuitive (for those who can’t print unbacked money in the service of a central bank/perpetually deficited State).

But the One Most Important Thing to Understand is simply this…that when the Fed creates unbacked money out of thin air (to finance all those convoluted operations and Treasury salvation) the ratio between “money” and real assets definitionally *rises* (aka price inflation).

At the instant of creation of that new Fed money no real assets are equivalently summoned into existence…result – inflation.

Now, defenders of the Fed and Treasury deficits will tell you that all this money printing/deficit spending will result in *incentives* that will create *more* real assets than if inflation were not summoned forth from the outer darkness.

I’ll leave it to the audience to judge whether or not the history of the last 50-70 years justifies such faith.

I can’t wait for Trump to send the Fed back to the states as well.

Ha! Maybe we’ll also have 50 different currencies in a few years.

We used to have more than 50 different currencies. Somehow the country survived and prospered.

It is kinda amazing how America somehow managed much greater GDP growth rates from 1800-1900 relative to those of, say 1970-date, despite all the massive interventions of “The Very Smartest People”.

How did economies ever manage to achieve The Industrial Revolution without Keynesianism?

Not saying there weren’t periodic Depressions…but the long term growth rates put present day ones to shame.

How would he do that?

What are are the benfits to the country and the states?

So: Fed creates the positive and negative results. Fed has immunity to losses. Treasury only wins only if the Fed’s outcome is positive. Treasury pays for Fed losses. While member banks earn dividends regardless of the Fed’s outcome. Fed is largely unaudited. Yet Government/Treasury legislated the existence of the Fed and these rules.

Correct?

The Federal Reserve is completely and thoroughly audited each year by one of the big four accounting firms and those reports running around 500 pages each are made public on the Federal Reserve website as well as being presented to the US Congress.

Yep. The Fed’s own public gov account has a whole webpage dedicated to the audit system laying out in detail the different levels and financial statements that get audited. That’s one thing at least they are reasonable transparent about.

It was obvious to me that he meant operational audits, not a financial audit.

“Treasury pays for Fed losses.”

The Treasury also got $1.1 trillion of the Fed’s gains since 2008.

“Fed is largely unaudited.”

The Fed’s financial statements are audited every year, just like any company. There are no other audits that companies have to undergo.

Insurance agencies and companies are absolutely subject to procedural audits, though not on an annual basis. Procedural audits are normally done for a length of time after a certain amount of errors and ommissions claims are reported. I have had the pleasure of overseeing the internal audit review for an agency which was then reviewed by a third party who reports to the state insurance department.

Tom-

Not sure if this addresses your question, but your comment brought these thoughts to mind:

Players involved:

– Policymakers (Lawmakers and Agencies who survive on -salaries and power)

– Bankers (who survive on a combo of profits and/or subsidy)

– Producers (who survive on a combo of profits and/or subsidy)

– Taxpayers (who ultimately fund the US Treasury)

– Consumers (who ultimately pony up for inflation)

By it’s originary and evolving documents, the Fed’s role has been to “stabilize” the economy in terms of employment levels, dollar purchasing power, and interest rates. Judging by the last 110 years — including the Roaring 20’s, the Great Depression, the high inflation ‘60’s and ‘70’s, the volatile ‘80’s and 90’s, the tech-wreck and Great Recession — the FRS has failed at stabilization of the economy.

Medium to long interest rates between 1914 and 2024 (highs in the mid teens and lows at or near the zero bound) have been demonstrably more volatile than the rate volatility experienced during the 19th century. Add in the excessive debt enabled by years of rate manipulation, and the central banking “stabilization” era appears to have been a flop.

Apologies if this was not the direction you intended to go…

Interesting comment on rates vs 19th century. How much of this long-term historical analysis of rates is US-specific? The US didn’t really become a global economic player until around 1870 and it seems from my cursory read that Europe was constantly having debt crises around John Law-type figures before copying our institutionalized FRS.

William McDonald-

For perspective on interest rates covering more than 1870 to present and more than just the US markets, pick up a copy of Sydney Homer and Richard Sylla’s History of Interest Rates early editions are worthwhile, and there are newer revisions. It’s very readable.

Sample:

“The greatest of all secular bear markets, which began in April of 1946, and probably ended in September 1981, carried prime long American corporate bond yield from their lowest recorded yields to their highest. The yield index rose from 2.46% to 15.49% for seasoned prime issues and up to 16.5% (industrials) and 18.0% (utilities) for high quality new issues. This was a yield increase of 1303 basis points on seasoned issues, and 1981 peak yields were more than six times greater than 1946 low yields. The great bear market lasted some thirty-five years, by far the longest duration for a bear bond market in U.S. history. If a constant maturity thirty-year 2 1/2% bond had been available throughout this second bear market of the century, its price would have declined from 101 in 1946 to 17 in 1981, or 83%. In contrast , in the first bear bond market of the century, 1899 to 1920, the same bond would have declined 35% in price. The recent bear bond market seemed to have much more social and economic significance than that of all earlier bear bond markets. In all the others, bond yields stayed within the traditional band that had prevailed for centuries. This time they broke decisively out of that band.”

—Sydney Homer and Richard Sylla, A History of Interest Rates

Also, the US copied the European central banking pattern. (Check out Paul Warburg articles and promotional campaigns for a US central bank in the early years of the 20th century. Much is available on Fraser system at St. Louis Fed site.). Sweden, UK, France, Germany and others acted as patterns for the US FRS. The US lagged in central banking, before it led them all.

It is fun to look at government bond rates throughout history. Not too surprisingly they are pretty much all around the 4% to 5% range, which I would guess would be about average, with some higher and lower of course depending on whatever crisis was occurring and how long the crisis lasted. Current US Treasury rates are around 4.5%.

If we assume the Fed is full of great people trying their best to serve their role, then we have to consider the monumental weight the Federal government has add to their shoulders. The federal government has been running counter to the purpose of the Fed since its creation. If we then assume the Federal government is full of equally stalwart people, then we have to consider the monumental weight of the citizens expectations of the government in solving all their problems.

Thankfully, neither is filled with such outstanding people and that means its not OUR fault. :)

Why would a taxpayer worry about a measly trillion dollar loss at the Fed? I read this somewhere how big is a trillion: If you had a job paying $1 per second is $3600 per hour. That amounts to $86,400 per day or about $32,000,000 per year. It would take you 31.5 years to earn a billion dollars and it would take 31,688 years to earn a trillion dollars. Congress will spend 6.75 trillion in 2024. How many trillion dollars are spent in excess of revenue via the printing press? Like Alfred E Neuman said, “what me worry?

Yes, but the US is not just one person. It’s over 330,000,000 people.

Can’t wait for DOGE to pull back the curtain.

GuessWhat – assuming these DOGE people are actually able to follow through with their wet dreams of slashing entire departments in the federal government, any savings will be immediately offset by more incoming tax cuts and fiscal insanity. The national debt will continue its march to the moon. I think these incoming “disruptors” are about to find out how incredibly difficult it’s going to be to make the government more efficient. Firing half of Twitter is a much different animal than reforming Washington. I don’t think they have it in them. I imagine their efforts will end up looking like a partially built symbolic wall on the Mexican border – a campaign slogan. Just don’t want you to be disappointed. I’m happy to be pleasantly surprised but I’m not holding my breath.

Your the one they had stand in the corner.

36 trillion in debt is good but 50 trillion is a much better number.

36 trillion was far to easy.

I feel like Musk just threw out that $2 trillion figure based on nothing at all and for two weeks now everyone and their dog has been trying to figure out what exactly they’re going to cut.

The left wing and mainstream media seems to be interpreting it as what can they cut without hurting entitlements their base depends on and/or blowing up the economy, and they aren’t finding a lot of options.

The right wing is just going like, cut absolutely everything. Food stamps, Medicaid, pensions, schools, foreign aid, public transit, renewables, EV subsidies, HUD, community development grants, etc, are some of the things I’m seeing on right wing websites. Oh and now we have MTG going on TV and threatening to cut all Federal funding to states that don’t go along with the deportations.

Whether any of that happens is highly questionable but personally I liked it better back when “the politicians don’t do anything they say they’re going to do” just meant they aren’t going to follow through on the GOOD things they promised. It did not mean “don’t worry they aren’t crazy enough to actually destroy the Federal government” like people keep assuring me.

On DOGE or Dogecoin? Elon is behind both.

A doge was the most important government official in an Italian city-state, for example Venice and Genoa, back to the Middle Ages. I recall visiting Venice where there was much history about the doge. I was surprised when I first heard the term “doge” used by the media within the context of some new department headed by Musk and Ramaswamy.

so to even pay more for cunsultants as the government looses even more inhouse expertise? Sound like a good scam.

“… government looses even more inhouse expertise”

One man’s expertise is another man’s “dead wood.”

Shiela Baer, in a recent interview with David Lin, posits that the government (or at least the FDIC) is staffed with mainly smart, capable and properly motivated managers and employees. While I’m guessing that is true, it doesn’t mean that here isn’t also a layer of dead wood that could and should be addressed.

Food for though: would it endanger the work output of the Federal Reserve to lay off the 501st least productive PHD?

Vector matters when it comes to bureaucracies and deficits, IMHO.

Us humans are highly incapable, we work slow and think slow. Were a cross between a cow and a turtle.

If I may be allowed a slice of personal sentiment, I believe my lovely AI robots will some day rule the world and move on to other planets leaving the humans here on earth to ponder their miserable fate.

Project 2025 sounds a lot like the Shock Doctrine that caused so much pain in both South and Central America.

Nice, banks really raking in the reserve interest payments?

The lower the interest rate, higher the remittance to the US Treasury, eh?

High interest rates look like they’re here to stay for a while. All this talk about tariffs and encouraging corporate job growth, and expanding US oil production which increases global market share…Economists say that lower oil prices are good for US consumers.

This article really is the deep, I’m a shallow water creature so I don’t comprend.

….I figured out how the broken fridge works all that told me is I need a new fridge.

A fall into a pit makes you wiser…so….

We are all in the gutter, but some of us are looking at the stars.

And some of us think that because the stars appear small, a microscope is the best way to view them…

“A fall into a pit makes you wiser…“

…and yet we keep “wabbling back to the fire.” John Law’s art and science live on, toward the same temporary ending.

Keep up your keen comments, Mr. Toad!

DM: Trump’s new Treasury Sec billionaire Scott Bessent is close friend of King Charles and Queen Camilla

Billionaire Scott Bessent has been a long-time supporter of the King’s charities, while Camilla stayed at his sprawling home in the Hamptons, New York, in 1999 during her first solo trip to the US.

I’m not sure that’s any worse than Janet Yellen. Who would be your pick?

The husband of Paris Hilton’s sister.

That Bessent guy has donated millions to Trump. I hope he isnt for QE, or bailing out gambling hedge funds with debt on the American people. And the wrestling lady Linda McMahon, who Trump picked for Education secretary also gave millions to Trump.

Are you complaining because our Great Leader is rewarding those who contributed to his victory? I guess you thought it was all about principles and high minded thinking. Dude, this is now a Third World country. When you take power, you loot the country.

Actually Powell is not so bad imo, our incompetent Bailey and the “committee”, despite loud howls for his dismissal, has led to cumulative UK losses estimated at around 7.5% GDP !

Plus no holding to maturity. Just get the losses immediately made up with a prompt transfer from government (taxpayer).

Powell claimed that inflation was transitory. One of his 2 jobs is price stability.

Economist Milton Friedman said it best: “Inflation is always and everywhere a monetary phenomenon.”

And who controls the money supply? Federal Reserve.

A couple of hundred billion dollars loss is nothing compared to the cost of inflation to the American consumer.

The Federal Reserve is not our friend.

Friedman made a simplistic statement that has been proven wrong by many years of crazy monetary expansion in many countries that generated little inflation. But that suddenly ended in 2021. Why that sudden end in 2021 of this phenomenon of little inflation despite crazy monetary expansion? Inflation is much more complex. A big factor is mass-psychology, what I call the “inflationary mindset” when consumers and businesses are willing to pay whatever, which they suddenly did in 2021 and 2022.

That statement you cited should be thrown into the junkpile of simplistic idiocies and never be cited again.

I’ve long thought that even simpler human traits can have a role in influencing consumer behavior and consumption.

From the linguistic side, the progression from “dime store” to “dollar store” was simple enough, but we don’t have a nice progression for “two dollars” and “fin” has gone away. The “anchor” value of a dollar or “a buck” for many daily consumer goods was useful for busy folks, but having to use alliteration to devise “five dollar foot long” will be difficult across categories.

Likewise, as the numbers grow quickly exponentially larger, it simply becomes more difficult to do the math on inflation, discounts, etc. and to ever display and discuss prices–Japan struggles with this. I’m curious if we will go their way of keeping the same unit of account as it value depreciates to below a penny or devise a “new” dollar.

Most consumers and businesses can’t pay whatever unless money is cheap/abundant.

You didn’t get the point: Money was cheap and abundant in the US and Europe from 2008 through 2020, and there was little inflation. Money was cheap and abundant in Japan for the two decades before 2021, and there was little inflation. And then SUDEENLY it kicks off, including in services where there were no supply chain issues.

PPP loans and stimulus checks. The gov’t literally handed over hundreds of thousands or millions to business owners. I personally know at least five who took enormous loans and bought real estate with the money. Then the gov’t forgave the loans and they were basically given free money for no reason at all.

Sure, money was cheap from 2008 to 2020 but the government wasn’t handing over large sums of it to people who didn’t need it who then turned around and invested it in assets.

That might be PPP fraud.

@grimp,

It’s not fraud if you used the PPP money for the required expenditures and used the money you were going to use for something else.

Wolf, with due respect to your excellent blog and formidable analysis, Friedman said essentially that inflation doesn’t exist without monetary expansion, not that monetary expansion doesn’t exist without inflation, those are very different statements. There isn’t a single significant modern peacetime inflationary episode that wasn’t accompanied by massive monetary expansion.

How much pre inflation money supply was placed in investments and 2nd homes? Then suddenly those investments are no longer good ideas, people suddenly have extra money. I don’t see how the money supply isn’t king, sure inflation can be delayed and psychology matters, international absorption of money matters too. But it will equalize.

Yep. $3 eggs no longer seem so expensive to me. Even though I remember paying under a buck for them for a long time.

It is interesting that the Fed operates as though it is an actual bank (twelve banks, in fact). It maintains this pretense by means of double entry accounting. But a bank that can incur any amount of losses is not a bank at all. It is what Keynes called a “Monetary Authority.”

Applying normal accounting to the Fed produces some puzzling anomalies. Federal reserve notes – the legal tender currency – are liabilities of the Fed. They are matched on the asset side of the Fed’s balance sheet by U. S. Treasury securities and MBS, which are promises to pay federal reserve notes. Wonderfully circular, isn’t it?

The Fed, like all central banks, uses “central bank accounting” which is different from regular accounting because central banks don’t have a “cash” account, but create and destroy money on a daily basis instead. There is even a 202-page manual for it, latest version:

https://www.federalreserve.gov/aboutthefed/files/bstfinaccountingmanual.pdf

^^^^THIS

Yes, circular and UNPRODUCTIVE, as in, we would get by just fine without the Fed.

I cannot imagine a world without the Federal Reserve. Their primary job is to clean up the messes other entities make. they are further constrained by two seemingly different mandates so by law they cannot always do what needs to be done.

Lest we forget. Much of the recent difficulties in our economy were brought about by a pandemic and most, not all of us, came through it pretty well. IMHO.

What? The Fed has been the greatest enabler of bad behavior the planet has ever seen! Or perhaps you have forgotten about those bullshit fraudulent financial “products” called mortgage backed securities?

If, in fact, the Fed was “cleaning up messes” they would have forced CONgress to prosecute the perps who created that shit, and allowed all those financial firms to fuck off and die. Let the bad actors go bankrupt for fucks sake. That’s capitalism you dumb schmuck. Instead, the Fed gobbled up all the toxic shit making these criminals whole again.

There is nothing even slightly ‘fraudulent’ about MBS (Mortgage Backed Security) instruments. They are simply a collection of mortgages bundled as a collateral pool and sold to investors and are a very safe financial instrument.

You forgot the /sarc tag. I laughed out loud reading this. I guess you never saw “The Big Short”. It was frigging fraud on a grand scale. Those “very safe financial” instruments were packages of Liar Loans!!

I also am thinking you missed theCon.TV which makes the ‘Big Short’ look like “See Spot Run!”

The swinging door between the Fed and Wall St is nothing less than the greatest swindle in history. As for “audits”….the big 4? …the Same ones caught giving 5 Stars to the toxic MBS in the 2000’s….and zero prosecutions for outright fraud.

“If we didn’t rubber stamp those then they wouldn’t give us the business!”

Waiono,

So why don’t you ask for an operational audit of Nvidia??? That company needs it more than anything. And it’s half the size of the Fed’s balance sheet already.

Why don’t you pooh-pooh the financial audit Nvidia’s annual reports get? … “If we didn’t rubber stamp those then they wouldn’t give us the business!” No?

are you high? the fed didn’t clean up any mess. all they did was print money and essentially confiscate 25% of the value of all dollars held throughout the world. anyone can do that, it doesn’t require any brilliance.

The Federal Reserve most certainly did not ‘confiscate any value’ from anyone at any time.

they certainly did. by definition, when you print money, you dilute the value of all existing dollars out there, effectively confiscating them.

it’s not difficult.

Disagree, if the Fed wants to stop messes, it shouldnt have and never should again print trillions to artificially push down interest rates, then rates would rightfully have spiked naturally, forcing govt to quit overspending.

The audit the Fed crowd still doesn’t understand they are victims of a long running goldbug meme. The Fed was supposed to regulate gold prices as well, instead of the evil wall street manipulators that operated in plain sight, along with every other commodity firm.

Whatever. Want some real fireworks, watch what happens when the national debt starts dropping after higher tariffs start biting. So much of the debt is simply someone else’s asset. And as such, they want more of it, not less. There isn’t really much more social security long term holdings, as the boomer crest hits at the assets. The social security trust fund was only really designed to allow the system to get through peak boomer (roughly 1956+77=2033). Gen X retirement is a bagatelle in comparison. Thanks to Greenspan committee. Just have to get more workers into the system and fix medicare.

I haze zero faith in the next administration to do anything long term rational unless confronted by a big crisis.

The Fed is a committee dedicated the status quo, and somehow preserving it, so it will always be behind the curve going up and down.

I just wish that a significant portion of America would actually learn what our money *really* is, and not argue something out of William Jennings Bryant. Fiat lux, baby. And if you don’t like it, buy glod or silber at your local coin shop. Just watch out for the inevitable chinese fakes.

Further, until exorbitant privilege in endanger, we are the laundry, not just the cleanest dirty shirt.

As for housing, tell me what the deportation is really going to be, plus foreign ownership of housing by nonresidents.

And that will be the margin question for the next four years.

And cheap interest rates? Dead, Jim. Get used to having a real i in your hurdle rate equations.

If you actually think that the National Debt will start dropping EVER, I have a bridge in Brooklyn you might be interested in buying.

A 20% minimum across the board cut would be a good start and easy to do with all government spending of any kind.

Could the crises be a trade war? Sen. Rand Paul is anti-tariff and said international trade has made every American $7000 dollars richer, A YEAR.

Rand Paul should stick to his knitting and not stand in the way of the Great Leader bringing prosperity to all. Or at least to his campaign contributors.

You forgot the incredible destruction of the value of the money JH.

Even by ”official” GUVMINT statistics as per the BLS inflation calculator, the current US$ is worth approximately 1/33 of what it was worth in 1913.

That’s why you make a return on your investment to out-earn inflation. If a company loses money, obviously inflation makes it worse in real terms, any company, and there are always lots of companies that lose money, and we’ve covered a bunch of them here, nothing special about the Fed in that regard. And if stocks go down, inflation makes that worse too. Everyone knows that.

As a line item in the Fed budget, like operating expenses, how has the statutory 6% dividends paid to the shareholders of the bank been calculated over this period of feast and famine? Have the shareholders been bailed in?

“The stock has a par value of $100, is of one class, cannot be transferred, and pays a fixed cumulative dividend of 6%..”

The dividends are “statutory,” which means by law, which means by Congress.

Explanation from the Fed:

Stockholder Dividends.

https://www.federalreserve.gov/aboutthefed/section7.htm

How do I become a stockholder of the bank? 6 percent is a nice return. I realize I have to be careful and be sure I do not exceed $10,000,000,000 in assets.

You can become an indirect stockholder by holding the stocks of the financial institutions that hold the shares of the regional FRBs. For example, if you want to be a stockholder of the New York Fed, you can hold shares of JPM and GS and many others.

Wolf,

Are all the losses listed here remitted to the Treasury, or just the unrealized losses?

The unrealized losses are not at all remitted to the Treasury. They will go to zero on their own as these securities get closer to their maturity date, no matter what yields do. And at maturity date, they’re paid off at face value, at no loss to the Fed.

The operating losses are “remitted” to the Treasury in the future, when the Fed starts making profits again, via the mechanism I described in the article.

so the 10 year treasury is down by 14 bps on the theory that Bessent is going to fix all problems.

the amount of confidence the “markets” have in the next administration making happy days here again is staggering.

there are major structural problems out there that transcend politics.

Bessent is quite bright and friends with King Chuckie and his wife as well as the esteemed businessman George Soros and his son Alex.

What!? He is friends with George Soros? Isn’t Soros responsible for everything wrong in this country today? I thought I voted for our Great Leader to defeat Soros and his ilk?