Pandemic distortions and millions of migrants suddenly entering the labor market, who are hard to track, have wreaked havoc on labor-market data accuracy.

By Wolf Richter for WOLF STREET.

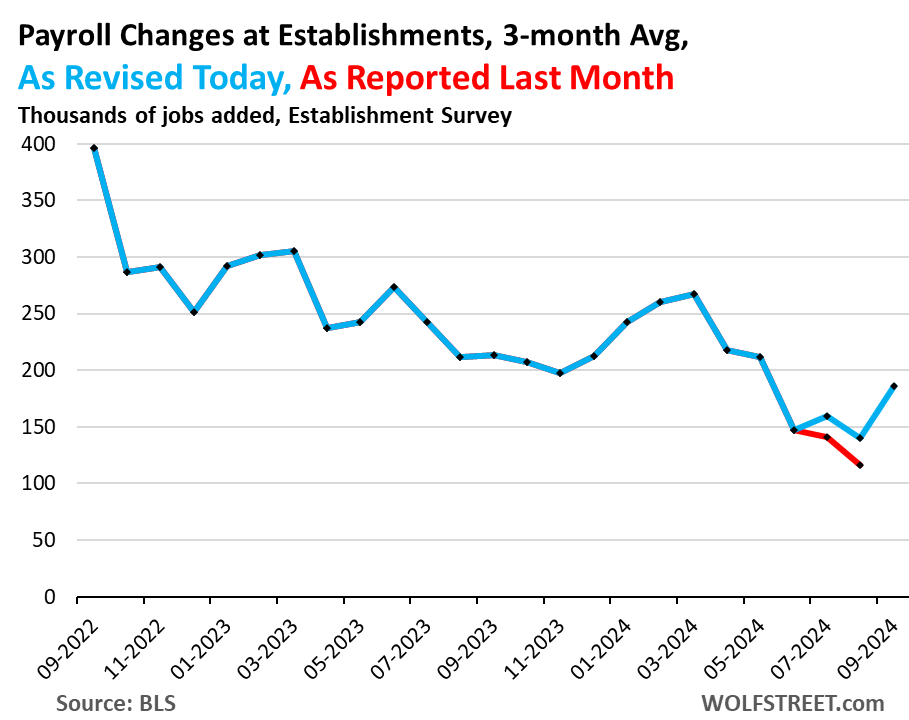

Payrolls at employers rose by 254,000 jobs in September, and the down-revision last month for July was re-revised up a lot, and August was revised higher too, so the three-month average jumped to 186,000 payroll jobs created in September. And the three-month average for August – which had been reported as 116,000 at the time, a scary and sudden deterioration with the revisions that caused so much consternation – was revised up to a half-way decent 140,000.

Turns out, the sudden deterioration of the prior two months were a false alarm. The labor market is just fine, creating a decent but not spectacular number of new jobs, and the unemployment rate dropped for the second month in a row, and wages jumped, and the Fed doesn’t need to cut any further, given the inflation pressures already building up again — though it will likely cut further, though maybe at a slower pace than previously anticipated.

The blue line shows the three-month average of jobs created as reported today. The red segment shows the three-month average as reported a month ago:

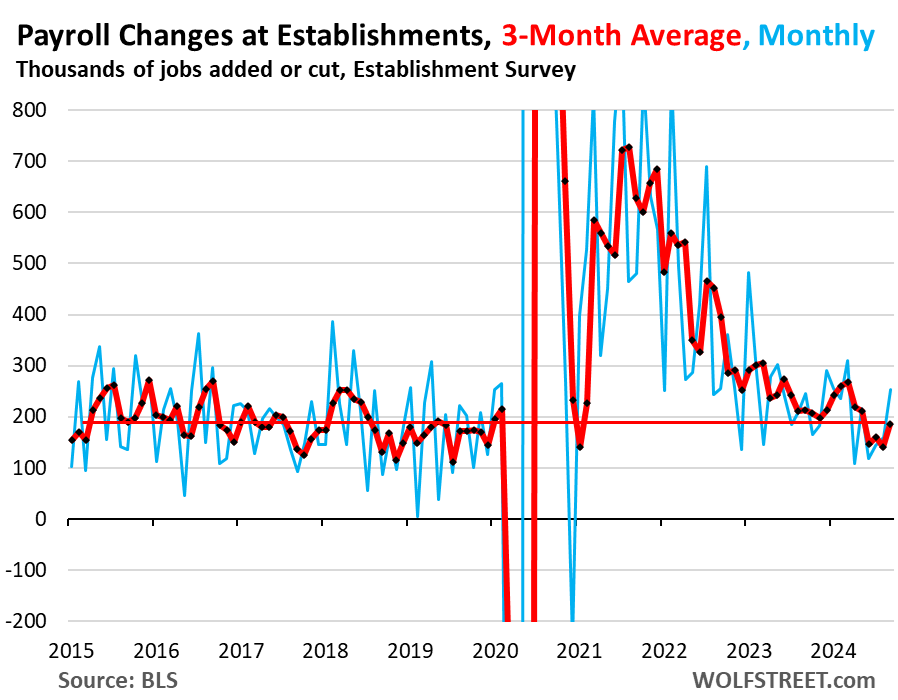

Here is the long view, as revised: The three-month average is right in the sweet-spot of the strong labor market in 2018 and 2019.

Clearly, the frenetic pace of hiring after the pandemic is over, and the labor shortages are over. The pace is back to a healthy strong job growth.

This picture matches other data showing that layoffs and discharges remain very low. Companies in aggregate are creating jobs at a decent pace, and they’re hanging on to the employees they’ve got.

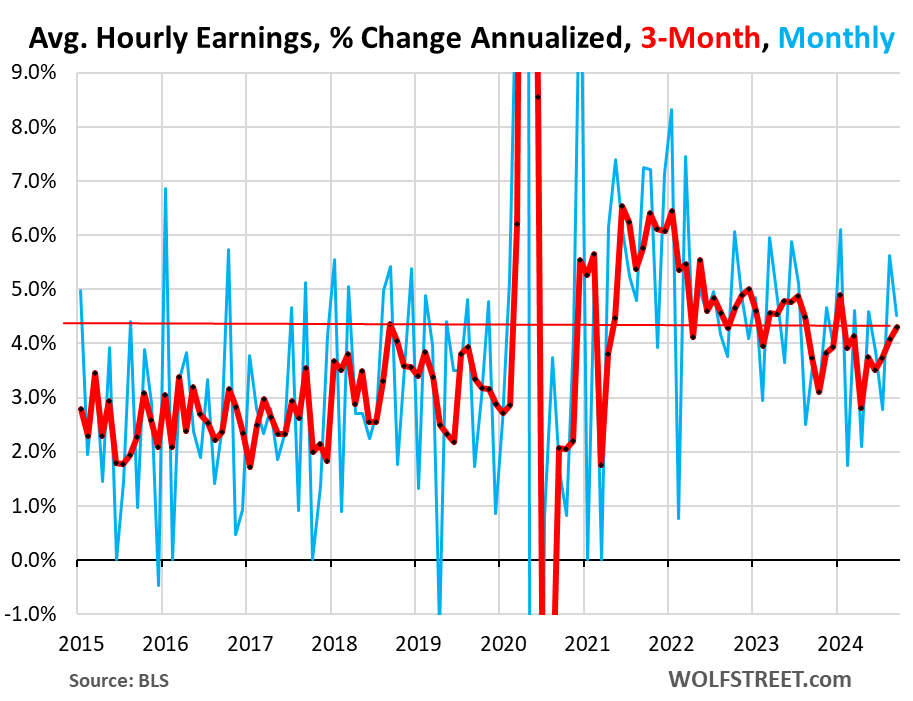

Average hourly earnings were also revised higher for August to a hot 5.6% month-to-month annualized, from 4.9%. And in September, they increased by another 4.5% annualized from the upwardly revised August, which caused the three-month average to increase by 4.3%, the highest since January. The three-month average has been increasing steadily since April (red line). This is based on the survey of establishments.

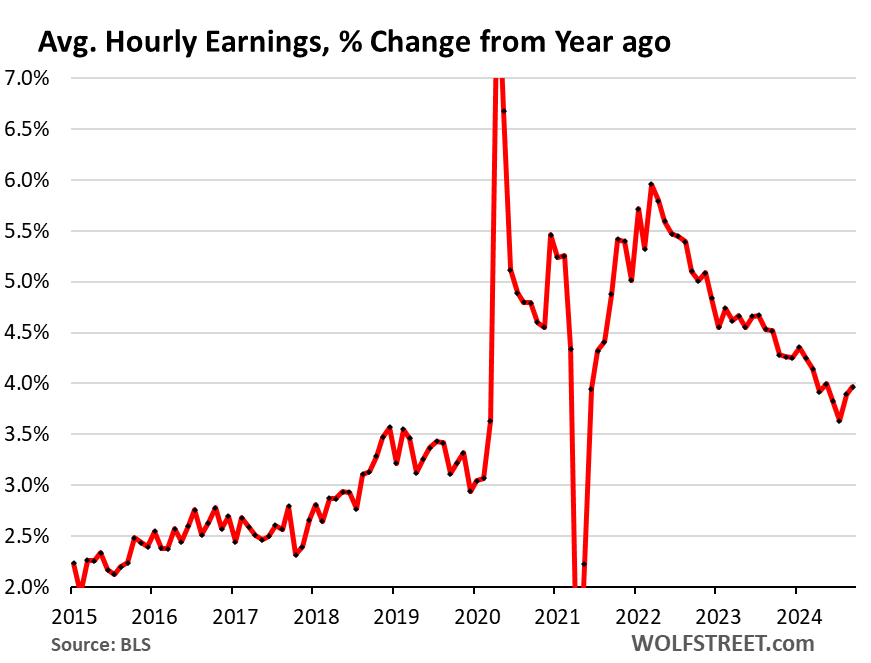

The 12-month increase of average hourly earnings rose to 4.0% in September, and August was revised higher to 3.9% (from 3.8% as reported a month ago). Those two months combined show the fastest acceleration since March 2022, and are well above the peaks of the 2017-2019 period.

So in terms of inflation – and what the Fed has been worrying about – this accelerating wage growth is not going in the right direction anymore.

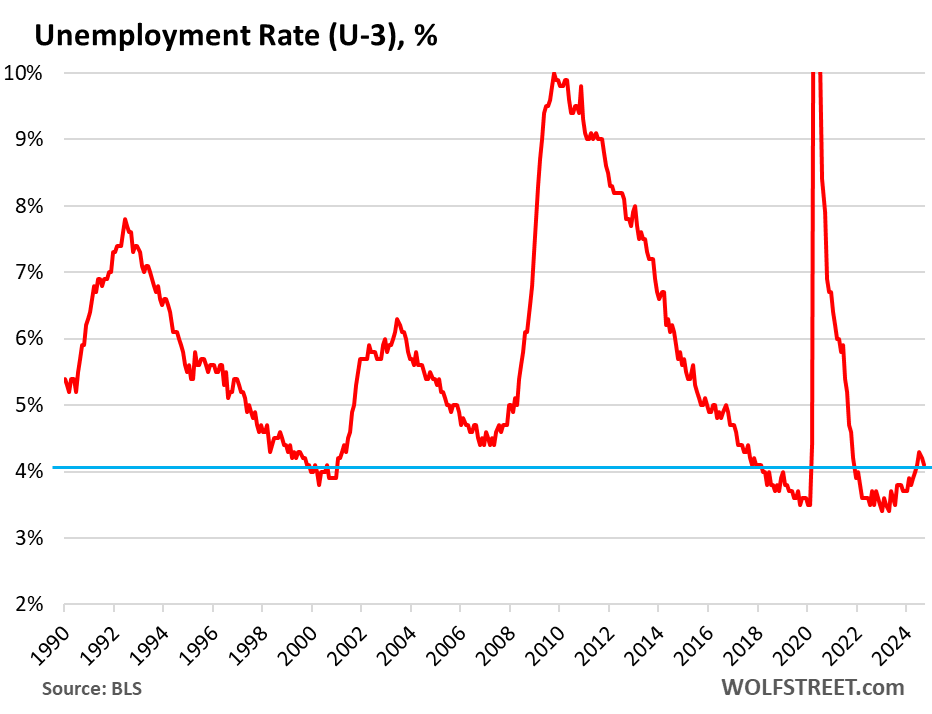

The headline unemployment rate (U-3) dipped to 4.1%, the second month in a row of declines. 4.1% is historically low, but is up from the period of the labor shortages in 2022. This is based on the survey of households.

The unemployment rate is now below the Fed’s 4.4% median projection for the end of 2024 and for the end of 2025, according to the Fed’s Summary of Economic Projections released at the rate-cut meeting.

The weakening of the labor market that the Fed projected in justifying the 50-basis point cut has reversed, been revised away, or failed to happen.

The unemployment rate is also where the massive influx of immigrants over the past two years – estimated at 6 million in 2022 and 2023 by the Congressional Budget Office – shows up: Those that are looking for a job but have not yet found a job count as unemployed. And their influx into the labor force has caused the unemployment rate to rise from the lows last year.

A rise of the unemployment rate caused by a surge in the supply of labor is a different dynamic than a rise of the unemployment rate caused by job cuts and a reduction in demand for labor, as we would see during a recession:

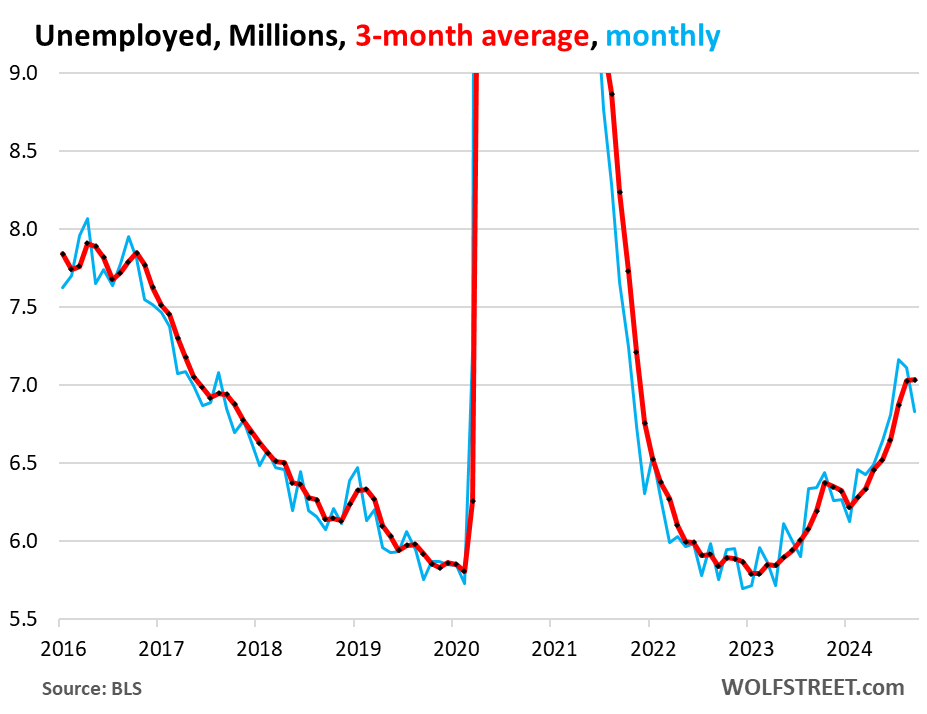

The number of unemployed people looking for a job fell for the second month in a row, to 6.83 million. The three-month average inched up to 7.04 million.

The unemployment rate (chart above) accounts for the large-scale growth of the population and of the labor force over the decades. This metric here of the number of unemployed does not take into account the growth of the population and the labor force, and over the decades, a growing population and labor force entails a growing number of people looking for a job.

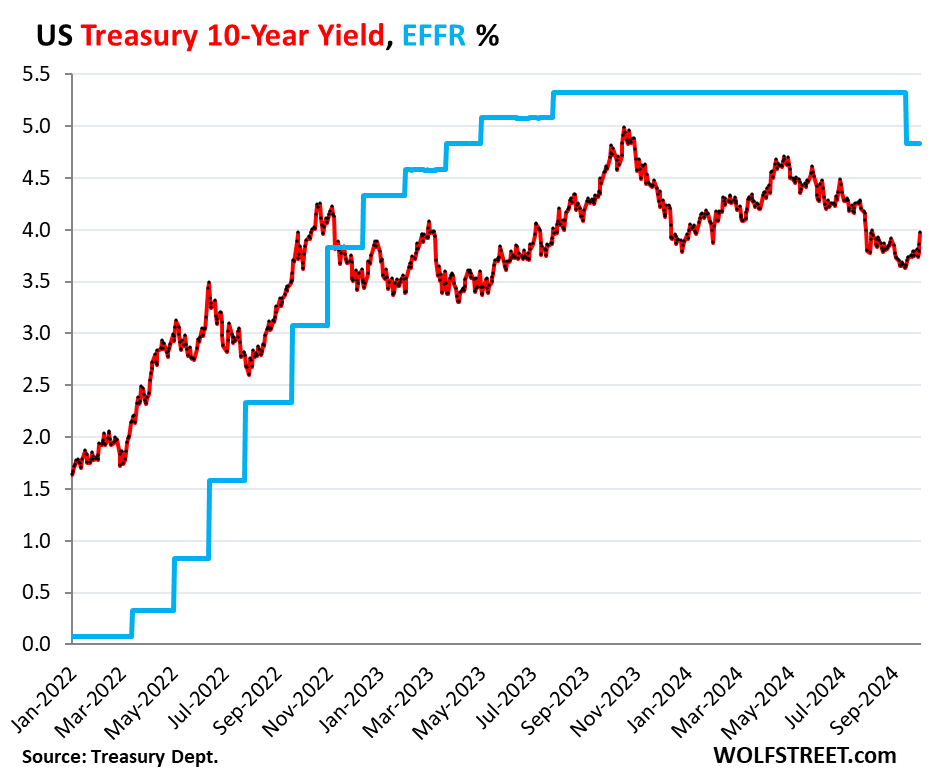

And the bond market woke up.

Upon the news that the labor-market scare last month was a false alarm, and that aggressive rate cuts to save the labor market are not needed, and that wage growth is contributing to general inflation concerns that we have already seen in the Consumer Price Index for August and July, and in what companies have said about raising their prices, and in the pricing power that companies still exert…

Well, upon the news, the bond market woke up, and the 10-year yield jumped by 12 basis points to 3.97% at the moment, the highest since August 8. Since the rate cut, the 10-year Treasury yield has risen by 27 basis points.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yeah, this economy is red hot and for some reason an emergency election-bending, I mean economy-boosting crisis level rate cut just had to happen. Well, it’s nice to see the ten-year head back towards 4% on its way to 5 or 6%.

Red hot – all those kids need to work long hours and demand big raises and pay record highs for housing and stocks and everything else – I’ll be happy with my 1990s style interest earnings again.

The tin foil hat part of me wants to believe the employment numbers were manipulated to justify the unnecessary rate cut, but who knows, incompetence is just as likely.

Today’s up-revisions and big Sept number should tell you that your belief was wrong — because it makes the Fed’s sudden 50 basis point cut look silly.

It was a tongue in cheek comment replying to Ol’B “election-bending” description.

But if that is somehow accurate, I doubt they care about looking silly.

so “IF” they cut in Nov, I guess they are keen on being silly for a while….

Do clowns and silliness go hand in hand?

wolf, respectfully disagree here. there is no good reason to have the yield curve this inverted, for this long. the fed is beyond tight here, well into restrictive territory. furthermore, fed funds rates at elevated levels do not impact long term inflationary pressures. instead, they impact short term speculative behaviors. fed can and will cut further, seeking to get in alignment to a flattish or normalized yield curve.

Central Bankster,

What is different now, compared to the 90s, where these rates are restrictive now, but they were not in that decade?

Wolf, I heard the big SEP number was due to a lot of government hiring. Correct? Can you comment on job composition – PT vs FT, citizen vs foreign born, public vs government.

joe2

Nope. But there is a stupid-ass cottage industry out there that picks two or three month-to-month squiggles out of the hundreds of data points to show that it was all fake, while ignoring all the other data points that show the opposite. EVERY MONTH, year after year, it never ends, by morons for morons.

And then this stupid manipulative clickbait BS shows up here in the comments, invariably. And then I have to waste my time with it.

BTW, “government workers” are mostly state and local government workers, and those are mostly teachers and healthcare workers, just in case you don’t know.

And this twisted ZH bullshit about foreign-born workers (me, my wife, Musk, the CEO of Microsoft, the CEO of Google, etc.) versus native-born is based on a manipulative chart they put together to spread toxic Putin-propaganda. If you’re going to pollute your brain with this ZH shit, fine with me, but don’t let it all hang out here that you polluted your brain with ZH shit. Take it like a man and cry into your pillow.

Birth rates in the US have been low for decades, and have been below replacement rates for years. So the number of native-born workers is going to decline due to declining birthrates, DUH. Every idiot knows this. And immigrants, including me and Musk, have been making up for it. Here are the actual numbers, not ZH’s twisted toxic Putin propaganda.

Nah they want the housing market to unlock, that is why the rate cuts are happening. Their goal of wage suppression was accomplished by rate increases and immigration, so now it’s back to housing market inflation.

What wage suppression? Wages are growing at about 2x a “normal” rate.

@JeffD

The job market is way different now than in 2022. And look at the last five years:

https://fred.stlouisfed.org/series/LES1252881600Q

https://fred.stlouisfed.org/series/MEHOINUSA672N/

The recent consumer income and savings rate revisions have not worked their way through to wage revisions yet. Lawrence Lindsey says that when those revisions are accounted for, wage growth will be pushed up 1.6% to 6% growth, up from 4.4%. That is insanely high in an environment of supposed 2% inflation target. The numbers just don’t jibe.

Cool!

Now I know why one party/group of interests has been flying illegal immigrants, en masse, to targeted cities – it’s all about birth rates! The need must be so great that there is no requirement for “quality control”. Rapes? Murders? Gangs? Drugs? Sex trafficking? Hey, it all nets out. Nothing untoward going on here. Look elsewhere!

I think I love the Chamber of Commerce and other public benefactors. They really, really care.

“Never ascribe to malice that which is adequately explained by incompetence.”

— Napoleon Bonaparte

Socrates takes it even further, I think.

“There is no evil, only misunderstanding.”

It’s getting to be more obvious that the Fed seems to be taking their eyes off the ball, inflation, and starting to peak over at interest expense. $1.1T through the 1st 11 months of FY24 suggests that we may come in around $1.2T for the full year.

$7T is rolling over between now & the end of 2025. That’s a lot of pressure on the Fed to lower rates.

By the end of FY 2029, we’ll be close to $45T in debt. If inflation stays hotter than the Fed expects over that period, the Fed may have very little wiggle room to lower rates. In fact, sometime in the next 3-5 months, the Fed may actually have to raise rates.

“Fed seems to be taking their eyes off the ball, inflation, and starting to peak over at interest expense.”

That sentence is fundamentally a self-contradiction. Longer-term interest rates JUMPED today on renewed inflation fears. The 10-year is nearly back to 4%. Longer-term yields have been rising since the big rate cut on inflation fears. Longer-term bond investors are worried that the Fed is walking away from its efforts to push down inflation.

If the Fed is worried about the interest expense, it would keep short-term rates high, in order to push down inflation, which will push down longer-term interest rates, which will lower interest expense.

By cutting its short-term policy rates, it showed that it’s less serious about inflation, and woosh, longer-term rates took off. For bond investors, inflation is a killer.

>For bond investors, inflation is a killer.

In the short-term, inflation seems to be pretty decent for earnings, leaving stocks as a mighty attractive option vs short term paper. At least the real yield is still positive.

Wolf, can you answer a question for me that has been on my mind? Do you believe the government data pertaining to the economy? I feel that you do, then I feel like you don’t.

I don’t believe the data. I feel most people don’t believe the data. It has truly become politized and is damaging this country.

Thank you.

Thomas Pained,

Do your believing in church. If you want certainty, go to church. Church offers you simple, certain, and permanent answers. It makes life easier, and you don’t have to think.

Data isn’t that way. Data can be and often is exasperating and aggravating, with uncertainties and unknowns all over the place, and it’s mindbogglingly complex the deeper you go. “Data scientists” — thank God I’m not one — try to make sense of data for business decision-making. I think it’s one of the toughest jobs out there. Whatever they’re paid — the BLS says the median pay is $108,000 per year — it’s not enough. They go home with a headache every day.

It was only a matter of time before the market started selling duration in protest…

Tom S, not really. The dividend yield based on the stock price is awful. Stocks are only attractive if you assume the high multiples will continue.

I don’t see how it is. We’re issuing WAY more short-term debt than long term, so the Fed is trying to make sure short-term rates begin moving lower. This will help somewhat with interest expense as the $7T rolls over at lower rates.

“By cutting its short-term policy rates, it showed that it’s less serious about inflation”

That’s exactly what I’m saying, so I’m not so sure why you’re disagreeing with me? I guess you don’t think $1.2T in interest expense is that big of a deal?

As expected, everything is month-to-month at this point. There was this HUGE market expectation that the Fed would cut rates by Sept, so that’s exactly what they did. A very strong argument can be made that the Fed shouldn’t have cut at all or should have only gone 25 BP. The economy is NOT as weak as all of the gurus say it is, at least not yet, which is consistent with your bond investor “woosh” analogy.

GuessWhat,

“We’re issuing WAY more short-term debt than long term”

Wait a minute. That has been wrong since February. T-bills roll over all the time. One-month T-bills have to be refinanced every month, 3-month T-bills every three months, etc., etc. So in general, most of what sells at T-bill auctions are T-bills to replace maturing T-bills, not to add new ones.

But since February, the amount of T-bills outstanding has actually dipped a little, to $6.00 trillion on Sep 30, from $6.01 trillion on February 29. The big boost was from June 2023 through February 2024. See chart below.

So every T-bill sold at auction since February was to replace a maturing T-bill and essentially no new T-bills have been added.

T-bills as percentage of total marketable securities peaked in March at 22.5%. In September it was 21.7%.

All the new debt that was added since February was longer-term notes & bonds.

Thomas…..Wolf is correct vis the complexity of data collection, massaging, “cleaning”, etc., etc. It’s a discipline unto itself. One that can be easily manipulated – we all know this from polling numbers over many decades, for example.

Then one widens the aperture. Putting aside the complexities of “big data”, there is the whole infrastructure/technology set/human capital of statistics, probability, model building, mathematics, feedback loops, processing architecture, deliberate biases, cost functions, and on and on.

At the end of the day, it always boils down to the same thing: it’s not the technology, methodology, etc., it’s whether or not trust can be invested in the people and interests that control the entire colossus. Do you believe in the integrity and impartiality of the keepers of the flame? Do you distinguish between some aggregate of worker bees or the smaller number of people in key gov’t positions who set the agenda, establish the endless regulations that are (as Musk notes) traps to force people into compliance with preferred objectives, etc., etc.

It all winnows down to you.

Describing the economy as “red hot” is nutty. It might be hotter than expected, no doubt. But red hit is silly.

As for election bending. That is nutty, conspiracy territory. Only one president in the past 30 years influenced FED rate policy. That president was the one that most conspiracy nutters suppoert.

Coroprate profits as a share of domestic income is highest since 1929. Is that red hot enough for you?

https://fred.stlouisfed.org/series/W273RE1A156NBEA

Are we having 2000 moment when bubble IPOs with no profit but big promises. Or not. Can’t have both.

And with the annual US Federal deficit running at peacetime (LOL) records, why wouldn’t corporate profits be high?

Is 3.5% GDP not hot? Unemployment in the low 4s?

That’s not the full logic. You are being deliberately evasive.

Fed decisions are inherently political in terms of consequences. The argument is whether this group of private interests, some of whom were forced to resign for insider dealings, align with one set of political objectives or not.

I’m not sure. I do think that there is no clear cut evidence either way. So a positive jobs report correction suddenly appears after a rate cut? Endless and sometimes large corrections period after period? I’m not suggesting post hoc propter hoc. I’m suggesting I don’t believe that the gov’t was clueless about where the data was trending.

Perfectly true perspective. It was definitely a false alarm. There is much much much more than enough money (and will stay so for a very long period of time) in the system that will confidently continue to elevate (or keep elevated) asset prices, wages, inflation and interest rates, while pushing down unemployment and bond prices for years to come. This is the new norm. I think everybody should adapt to it.

Based on market action so far, I think they haven’t quite decided if this is good or bad for the market or fit into good news is bad news type of deal….

No more rate cuts….that’s a nice thought and one hell of a rude awakening for the pumpers, would love to see that…

If the rate cuts were made impossible by legislative fiat, the private sector bankers would get their heads together and figure out another route to getting what they want.

We live in a financial sector world. England has de-industralized and relies solely on the crutch of the City of London’s stock exchange and Lloyd’s of London to maintain its standard of living and import food and goods. America still has some industry (mainly military, it seems), but Wall Street is the economic engine of the 50 states.

The banking elite are listened to very closely by Washington. Hell, whole government departments are led by men from Goldman Sachs. If Washington turned on them, they’d find another way.

I’m rooting for a higher COLA

At this point, every doomer bear is on Prozac and or various narcotic cocktails to help them ignore how perfect this economy is.

The previous period of Vibcession is officially over and anyone who’s still bitching about cumulative inflation impacts, high home prices or anything at all — need to wake up and embrace this moment in the sun — breath in the greasy smell of explosive equities heading to the moon — and embrace the glory of future earnings being revised to roaring twenties excess.

Fabulous doesn’t even partially describe my exuberance!!

Absolutely right. I’m doing the best I’ve ever been. The doom bears just simply cannot fathom things being well. Will they break later? Sure, but right now things are good.

I love free money!!!!

50bps should be off the table and I think this is “good news is good news”

Every news is good news and reason for another rally in the markets.

Looks like the market is agreeing with you as it’s starting to turn up…still couple of hours left, let’s see how it will end

According to Austin Goolsbee, the hot jobs report and solid wage growth do not alter the Fed’s calculus for a bunch more rate cuts.

Is this guy a drunk or just a big fan of inflation?

Eebsloog nitsua.

Sounds Romanian, but it’s the demon Austin Goolsbees name spelled backwards. Who knows what evil lurks in the corridors of power, a ghoul or a fool….

These people are dangerous psychopaths. They want their friends on Wall Street to live like kings while the rest of America is living in pig squalor.

I don’t believe for a NY minute that this whole thing wasn’t orchestrated. They can claim low inflation, high job growth, and they can pump asset prices.

The inflation won’t return until December, so the damage is done.

Perhaps you should read and comprehend his actual words instead of some silly summary that doesn’t accurately reflect his words and instead seek to take advantage of you.

JimL, I’m reading this and other comments on this article. You are free to give these people the benefit of the doubt if you want to.

We aren’t required to.

IMO, doing so requires a level of naivety I am not willing to entertain.

the fed will cut further, because you have misperceptions around what causes the fed to cut or not cut. hence your frustration with anyone who disagrees with your assessment.

hint: FFR is does not impact long term inflationary pressures.

During the course of my life, the current interest rates are actually pretty normal. Not sure why there would be much urgency from the Fed perspective to be lowering them all that fast or at all if the economic situation remains solid. Leaving them be might also help the hanger-onner house sellers come to the realization they need to lower their prices.

Interest rates at this level, and even a quarter or half point lower are still restrictive. Weve got more to go to get to neutral.

Like it or not, expect more cuts in the future unless inflation moves back up.

Yeah, very restrictive. That must be why the economy is booming, the labor market is historically tight, consumers are flush with cash and spending money like it’s going out of style, and stocks and housing and crypto are still well into bubble territory. It’s all that terrible restriction!

The inflation adjusted Fed funds rate is about 2%. It has only been this high for 3 out of 24 years this century. The only time it’s been substantively higher is during the Volker years (with far, far higher inflation), though it used to range between 0 and 2% quite often during the 20th century.

“It has only been this high for 3 out of 24 years this century.”

That’s a very big part of the problem.

Lol! Why? Because long bond prices or 2yr bond prices are low? Maybe they are mispriced. Maybe tbey should be higher? In fact all evidence points in that direction.

Goods prices are expected to have a drop, after a 40% runup in such a short period. Reacting to that normalization in prices like its an actual fall in prices is just goofy. Prices are the one place where the Fed language got it right — transitory.

*Goods* prices are the one place…

The 2-year was sold hard today – up 20bps!

Looking at the consumer spending, asset market price rise, low un employment rates, loosest ever financial conditions etc etc, it does not seem the rates were ever restrictive.

In the course of my life, (60 plus years as an adult), I have to say current rates are below normal. 7-8% was the norm for most of it with the occasional double digit number. Only very recently have they been this low.

The public has only a ten year memory. You can fool them with the same simple tricks over and over. All these economic discussions sound like background noise to me. I can smell peanuts on the breath of the elephant in the room, but he seems to be invisible to all the pundits. 35 trillion in debt and still growing. All these discussions are just people arguing over the bar tab on the Titanic.

And here I thought they were arguing over where the deck chairs should be…….

Learn something new everyday.

US unemployment rate still below long term average, unbelievable fed cut rates to begin with. Have a feeling fed was cutting to take pressure off the other central banks of slowing economies in they cant deficit spend like we can. Housing market was just starting to think about coming down to earth.

I deleted it because it contained a political BS half-liner.

Commenting Guideline #3

“3. When commenting, we check our political views at the door. WOLF STREET is a business, finance, and economics site, not a political site….”

You could have just left that half-liner out, and it would have stuck.

I understand why they need to “estimate” how many unemployed people are looking for work, but I don’t understand why they need to “estimate” how many people are employed. Can’t the government just look and see how many people paid payroll tax last month? If I want to know how many of my apartments are full I look to at a report and I see who paid (I don’t survey some residents and “estimate” how many units have residents paying rent).

1. As you know, companies file payroll tax forms once per quarter, not once a month.

2. That’s only people on W-2s. Does not include contractors that companies also employ.

There are many other complications in trying to count the number of nonfarm payrolls in this vast, complex, decentralized economy. People always want a simple answer, but that just doesn’t work.

@Wolf thanks for the answer, believe it or not I didn’t know that “companies file payroll tax forms once per quarter, not once a month” in my 20 years as a W-2 employee I had taxes deducted from every paycheck twice a month and I assumed that the money was sent of to the government by the payroll firm. I pay my own taxes once a quarter, but I have never had any “employees” (my apartment resident managers are all employees of my third party management firms). Years ago a sucessful apartment investor told me “two things I with I did earlier on after I started buying apartments is 1. not have any employees and 2. not have any reserved parking

The money is sent from the company with each payroll in one big payment to the US Treasury. Form 941 is filed quarterly.

Contractors make quarterly estimated payments, not monthly.

Also Social Security has max limit. so not contributing to Social Security doesn’t mean they are not employed.

Medi-Care yes, but then above 200K collection 1.45% extra so that also not concrete.

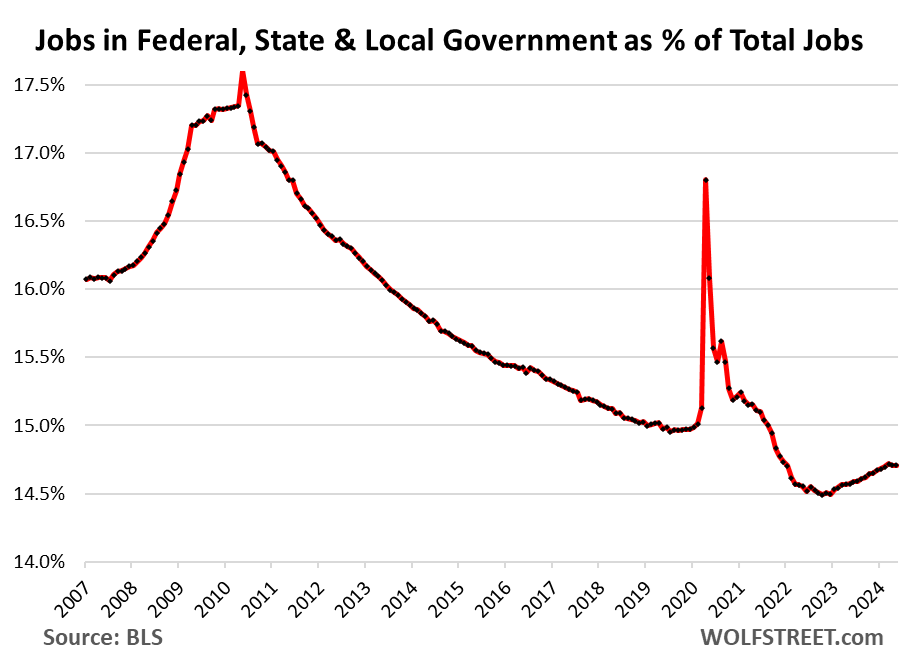

i would like to see Government Employee numbers broken out as a part of the report – are they already in the numbers but hidden?

Vast majority of government employees are local and state — mostly education and healthcare. Federal is pretty small in comparison.

Jobs at federal, state, and local governments: 14.7% of all employees work for governments at all levels:

Federal government: 1.9% of all employees

State governments: 3.4% of all employees (including higher education).

Local governments: 9.4% (much of it in education, such as teachers and school administrators).

https://wolfstreet.com/2024/06/08/longer-term-trends-of-employment-by-industry-category/

The 10-year remains in an uptrend. I still don’t understand how people assess this inflationary environment.

The forward looking market should be looking at some form of 5 year breakeven. Yet still the 10-year breakeven has not been over 3%, and peaked in March 2022 (the 5-year was 3.6% at the peak) per FRED.

Mr. Market is banking on this unseen recession or the UTubers deflationary depression that is “imminent.”

Mr. Hanke says it’s baked in the cake, because “M2” that the Fed doesn’t look at. I’m thinking that pre WWII era is more comparable than post WWII. Possibly a blend, with (now) Middle East economies literally blown out, Europe and China stuck in neutral and the USD milkshake is also the US economic milkshake?

My Hanke has been so wrong for so long with his M2. His take is M2 is going down and we are in recessionary times. WR has said many times M2 does not matter like inverted Yield Curve.

Bottomline: Economy is red hot.

I think a lot of observers are looking in the wrong direction when they focus on monetary policy — the real action is in fiscal policy, and with the US Federal government running record peacetime deficits, that’s a ton of stimulus for the private sector.

Hey kids, can you say “Policy error?”

There’s no policy error through the perspective that everything is transitory…

When someone like Komissar Powell and his Politburo wannabes (FOMC) are wrong more often than they are correct, the smart move is to bet against them. After his most recent decision last month, I was thinking about shifting from 3 month T-bills to long-term CDs, but took my own advice and waited. I will be doing 1 month T-bills henceforth, and look forward to the Komissar’s next decision (if any), so I can adjust my strategy to do the opposite if needed.

If you had shifted to long-term CDs back in the summer, you’d be making higher yields than anyone else right now. Because you stayed out of duration, you’re now chasing yields down.

Don’t fight the Fed.

Long term yields like the ten year have been trending up since the panic cut and are almost back over 4% now. The low in rates and mortgages post-pandemic might have been a couple months ago and with this red-hot employment number they could only be heading higher from here. A good economy like they tell us we’re having should be able to handle 5-6% ten years and 7-8% mortgages.

The daily measure of the 30-year mortgage rate jumped 27 basis points today to 6.53%, up from 6.11% before the rate cut.

@Wolf,

Well, at least *something* smart happened today.

Thurd2 – Putting aside any feelings for or against the Fed, I agree with your strategy of moving to short-term 1-month Treasury bills. Here’s why:

– The Fed doesn’t set all interest rates. The fed sets the Federal Funds Rate, which is the rate banks charge each other for short-term loans to meet their reserve requirements. There are many other interest rates, and they are determined by the market.

– The Fed does influence market interest rates massively via the money supply. An increase in the money supply raises the inflation rate, all other things equal. An increase in inflation raises interest rates because lenders want to be compensated for future inflation when they make a loan.

– The other major influence on market interest rates is real growth. The higher the real growth in the economy, the higher the rate of interest lenders can charge the borrowers who are making that growth happen.

– So, together, the rate of inflation and the rate of real growth are, I believe, the main drivers of interest rates set by “the market” where the market is the vast number of lenders and borrowers coming to agreement on interest rates, one transaction at a time.

– I believe that the inflation rate over the next few years will remain stubbornly higher than the 2% that the Fed claims to target. I also believe that the U.S. economy is packed with outstanding businesses that will continue to deliver outsized real growth.

– Put those two beliefs together, and you conclude that interest rates are too low right now and that the market will push them to higher levels. They will increase due to both inflation and real growth.

– Here’s the punchline: If everything I have said is true, then right now you want to put the cash dollars in your risk-free bucket into the place where returns are best and where you have the most liquidity: 1-month Treasury bills. That way you can reinvest the Treasury bills into higher rates of return each month as the market adjust interest rates upwards.

The usual caveats apply. I’m not an expert, but I do want to invest wisely, so I invite *constructive* criticism.

“I also believe that the U.S. economy is packed with outstanding businesses that will continue to deliver outsized real growth.”

If above is true then better to put money in stock market then in cash.

Unless everyone is lying a few stocks made enormous gains and most of the rest modest gains at best.

Doubting Thomas,

Respectfully, I have to disagree and nitpick a lot of what you wrote:

“The fed sets the Federal Funds Rate, which is the rate banks charge each other for short-term loans to meet their reserve requirements.”

The Fed Funds market is a ghost town these days – banks rarely use it. Banks lend and borrow in repo markets to meet their liquidity needs these days.

“An increase in inflation raises interest rates because lenders want to be compensated for future inflation when they make a loan.”

Unless those “lenders” are bond traders speculating on rate cuts to increase the m2m value of the bond.

“I believe that the inflation rate over the next few years will remain stubbornly higher than the 2% that the Fed claims to target.”

I actually 100% agree with this.

“…you conclude that interest rates are too low right now and that the market will push them to higher levels”

Which rates are too low?

The Fed is lowering short-term rates, while long-term rates (duration) are moving UP in response.

If you go all cash (1-month bill/MMF/etc), then you’re getting progressively lower and lower returns as the Fed lowers short rates, while rates on duration going up mean you don’t want to own that either.

Hmm, how can one make money on rising rates on duration???

Thanks, Jon, Anon and ShortTLT.

Jon – I am moving slowly but surely back into broadly based stock market indexes. Slowly because…

Anon – Yes, I agree stocks are overvalued now, even with the massive opportunity that U.S. businesses have in front of them now. Earnings multiples are crazy high. Too much money sloshing around in the hands of amateur investors who buy the hype.

ShortTLT – Your points seem reasonable to me. I could be wrong, you could be right. Or vice versa. Who knows? But while I still have cash on the sidelines (prior to fully dollar-cost averaging back into an overvalued stock market), I believe that interest rates are too low right now on *both* the short duration bills and long duration bonds. So, that’s why I am holding my cash in the highest yielding, highest liquidity option: 1-month Treasuries.

I appreciate all of your feedback.

Exactly where we’re at at the moment DT!

Had done the higher CD rates months ago, and they still looking good so far.

Are doing the T-Bills and will continue to go with the largest yield, for now.

Totally retired and trying to keep up with grand dad who vowed to live day to day on his SS only, and doing so, so far.

Old folx when I was a kid, always told me to live on the yield, NOT on the capital, so might be a bit of challenge if the inflation stays above the SS Cola, as it seems to have done since 2020…

Interest rates may respond to influences other than inflation rates and inflation expectations, either current or expected (there is a demand side factor (government deficit financing) operating in the loan funds market as well as a supply side factor.

At the same time supply is decreasing, the demand for loan funds is expected to rise as a consequence of the expected massive increases in federal deficits (for savings), the larger the deficit, the greater the demand.

The deficit financing impacts on the supply side (as well as the demand side) will push interest rates up or will retard their fall. With supply decreasing and demand increasing (in the schedule sense), there is only one way for interest rates to go in the long run– up.

Ordinarily an increase in demand for loan-funds coming out of a recession would be highly desirable, being indicative of, and a necessary adjunct to, a business recovery. But the present and future increased demands for credit are the result of the irresponsible fiscal practices of the federal government.

The funds being borrowed do not increase our productive capacity, nor increase the efficiency of the work force. Rather the funds are used largely to finance transfer payments to non-productive recipients and to finance “dead-weight” military hardware. Since the goods and serves being finance by these monstrous deficits are not offered in the marketplace, enormous inflationary pressures will be generated in the economy.

Given these demand side conditions the fed, acting alone, cannot hold long-term interest rates down to levels necessary to foster a healthy economy. The future climb in long-term rates reflects an extremely pessimistic perception of the future. The consensus of investors is that the federal government is expected to move into an era of truly massive deficits.

Spencer – I think we’re on the same page:

Scenario # 1) No money creation: If the U.S. government increases its debt and the Fed *does not* create new money to finance that debt, then the U.S. government will have to pay higher rates of interest to draw scarce cash from lenders. Businesses and consumers will be crowded out by government borrowing and will also have to pay higher rates of interest.

Scenario # 2) Money creation: If the U.S. government increases its debt and the fed *does* create new money to finance that debt, then the U.S. government and all borrowers (businesses and consumers) will have to pay higher rates of interest because lenders need to be compensated for inflation.

Bottom Line: With or without new money supply (and inflation), as U.S. government debt grows rapidly, interest rates will increase for all borrowers.

By the way, I believe that the second scenario will prevail. That is, the Fed will create new money to finance the U.S. government debt. That’s why I am dollar-cost averaging my way out of the U.S. Dollar (and Treasury bills and bonds), whose purchasing power will continue to decline meaningfully in my remaining lifetime. Despite my belief that the stock market is currently overvalued by 10% or so when viewed through the lens of traditional discounted cash flow analysis, I put my faith in investing in businesses (via stock market indexes) who have time and again proven that they can create value, even when facing the headwinds of inflation and high borrowing costs. I’d rather overpay 10% for stock indexes now than hold U.S. Treasury securities long-term and watch my purchasing power plummet every ten years when we encounter a new crisis that the government needs to “fix” with budget blowout spending.

Only Scenario #2 is possible without deep changes at the Fed and at central banks and governments in Washington, London, Brussels, Ottawa, etc. The Fed will print money , inflation will shrink the real value of debts, and governments will settle their obligations with funny money. Meanwhile, Milei has a chance to prove them all wrong.

“The funds being borrowed do not increase our productive capacity, nor increase the efficiency of the work force. Rather the funds are used largely to finance transfer payments to non-productive recipients and to finance “dead-weight” military hardware. Since the goods and serves being finance by these monstrous deficits are not offered in the marketplace, enormous inflationary pressures will be generated in the economy.”

Much wisdom here, spencer.

eg and Spencer,

Spencer’s “The funds being borrowed … are used largely to finance transfer payments to non-productive recipients…” was a manipulative lie, typical internet bullshit getting spread around.

The vast majority of transfer payments are Social Security payments, and they are self-funded. In fact, the Social Security Trust Fund, after 20+ years of surpluses, has been a huge LENDER to the US government, it has lent $2.7 trillion to the US government currently. Disability payments are exactly the same way, they’re self-funded and the system’s Trust Fund is a LENDER. Medicare part A hospital insurance (paid to healthcare providers, not consumers, LOL) are the same way, self-funded and paid out of the Trust Fund. Medicare Part B and Part D are funded by premiums, interest earned on the Medicare Trust Fund, and funds appropriated by Congress. Unemployment insurance is self-funded. Etc. There are only a few types of payments that are not self-funded, including Welfare, which is a minuscule part of the budget.

Abusing my site to spread this kind of malicious lie on my site can get you blocked.

I just didn’t see the original line or else the comment would have have been trashed. Apologies for being in dereliction of my duties.

Doubting Thomas, it has been your scenario #2 ever since the Nixon shock and the end of the Bretton Woods agreement — it’s the only way the US Federal government ever spends money (which it creates). States and municipalities are, on the other hand, always in scenario #1.

This is the case for investing in gold, silver, and even the miners. The gains are already 40-50% from February. That’s incremental for this sector. It takes some getting used to….

Laurence – You have piqued my curiosity. I have never learned enough about gold or silver to invest confidently in either of them. I know that both gold and silver have been valued throughout human history for their beauty and scarcity. I know that silver has important uses in manufacturing settings, so its value goes beyond aesthetics. But, as a born skeptic, I have always scratched my head about the innate value of gold. With due respect (I’m not trying to be a wise guy), can you explain to me how gold is different from crypto? Isn’t gold a kind of retro version of crypto? Both are scarce in their own way, but what value due they have, really, beyond everyone agreeing that they are valuable? Even as I write this, I am chuckling at the naivete of my own question… I could just as easily ask what the innate value is of fiat currencies like the U.S. Dollar. Anyway, please do talk to us about why it makes sense to invest in gold and silver under the current circumstances. Thank you, sincerely.

Should say, “… what value do they have…”

“all other things equal”

Which is, of course, never.

But as it happens, I agree with your observation that there are secular inflationary forces, not the least of which are geopolitical in character, and I also have a lot of short term paper right now (though that’s primarily a function of having two college age kids). I don’t attempt to time equities, since I generally never sell those; most of my equity purchases are programmatic and aimed either at dividend accumulation or the very long term on behalf either of my children or my (not yet born) grandchildren.

If you look at the history, 90% of the time Fed is wrong.

I love internet made up statistics. There are very few funnier posts.

That’s a lot of credit for the Fed. The last time they were really right was Volcker in 1987.

The Fed is never universally “right” or “wrong” — such evaluations are all about whose ox is getting gored.

No more rate cuts needed? No rate cuts were needed.

I had to park some money this week and did a short-term T-bill as I assume rates are not going down further, and maybe even up in the next year, and I assumed I can fine a better deal in a few months instead of locking in. I was never convinced inflation was gone, and thought the Fed should have just sat tight. No matter the election outcome, the fire hose of government spending will not abate, putting pressure on both money supply and and need for government borrowing.

“OK, Forget it, False Alarm, Labor Market Is Fine, Bad Stuff Last Month Was Revised Away, Wages Jumped. No More Rate Cuts Needed?“

Best headline ever. Drop the mic.

Hear, hear!

The 62% ILA wage increase is certainly an eyeopener…for a one day day strike . Unions like longshoreman, police, firemen, other essential workers are always the warning shot for economy wide upward wage pressure.

Maybe it’s not quite in line with the thread guidelines Wolf, but the 50% cut walks, looks and talks like a political move. 25%…perhaps….50%…no way.

Real estate…

I still see no way those 66% home owners move on from sub 5% loans and here in Hawaii folks seem to have adjusted to the new price levels. Higher wages will certainly help them eventually purchase…

and

“The Food and Agriculture Organization of the United Nations’ Food Price Index, which tracks the international prices of a basket of globally traded food, averaged 124.4 in September, up 3% from August and 2.1% higher versus the same month one year ago.”

The yield dip in the 4 week Bill is over

I hope I’m wrong to get a 1972 kind of feeling (as in, political moves, with inflation not solved). Oil shock on the way??

Keep cutting. Arthur Burns Redux

My professor used to read Burn’s correspondence to his money and banking class. He called him ignorant and arrogant.

But I liked his excuse: “Money has a ‘second dimension’’, namely, velocity . . .. ” Arthur F. Burns in Congressional Testimony.

Note the surge in MMMF balances. That increases the transaction’s concept of money velocity, the activation of monetary savings.

MW: Larry Summers says the Fed’s half-point rate cut was a mistake

That’s what DXY is telling you.

The recent 50 basis point rate cut was the most reckless move by the FED in history. Jerome Powell should have been removed long ago. He is a danger to the US.

The Fed cut reminds me of that funny commercial in which the kids running from the psycho look at the shed with chain saws and scythes hanging all over the place place and say: “We’ll be safe there!”

Oh, he’ll get his comeuppance soon enough. Patience. Let’s see how he likes eating a 9% CPI print next year. I suggest he’ll eat his rate cuts, too.

I will literally bet any amount of money up to mid 5 figures that the CPI doesn’t hit 9% in the next 12 months. There are plenty of online sites that will neutrally take our bets. We deposit and enter the parameters and they decide. You can pick one. I just want your action.

You pick the amount and you pick the site. I am in. Put your money where your mouth is. Let’s do this.

If CPI includes assets, as I believe it should, it would have been at over 9% for the last decade every year.

Steve B

“If CPI includes assets, as I believe it should, it would have been at over 9% for the last decade every year.”

You need to use your brain, Steve!

If home prices were included, CPI would have been steeply negative in 2005 through 2012 during the housing bust. CPI might have been -10% for years even as prices of everyday stuff rose. People would have laughed about CPI at -10%.

That’s why asset prices are not a measure of consumer price inflation and shouldn’t be part of it. Asset prices vary for their own reasons, and are measured by separate indices that measure asset price inflation, and we cover them here in our Most Splendid Housing Bubble series.

BTW, housing costs are about 1/3 of the CPI, it’s just expressed differently than home prices. And it’s one of the hottest parts of CPI right now.

Wolf, I hear you, but, is it possible that our leaders would not ignore asset bubbles if the deflation of them would count as CPI deflation?

I’m 27. My friends are I angry that assets are unaffordable, and even more angry that our leaders don’t seem to give a damn. Many of us think both political parties are cut from the same cloth.

Steve,

The solution is higher long-term mortgage interest rates and less speculation. They can be brought about by: Fed’s QT, Fed’s higher short-term rates, dialing back government support for mortgages, abolishing any kind of down-payment aid, throwing people into jail for tax fraud if they don’t pay hotel taxes with their vacation rentals, charging extra taxes on 2nd, 3rd… homes, charging extra taxes on vacant homes, etc. (the US needs tax revenues more than anything).

There are lots of solutions. But no one will do anything because pumping up home prices is sacred. Right now, in that sense, the Fed is the only adult in the room with its ongoing QT and still relatively high short-term rates — which has caused demand for existing homes to collapse.

I agree with all of that. But you can’t deny that people’s belief that the Fed will come to the rescue is what’s causing all assets to trade at bubble prices.

Nobody would be willing to pay 20x income for a house, $65,000 for a Bitcoin, or $600 for a share of Meta if the Fed came out and promised to never do ZIRP or QE ever again, no matter how bad things got. But they won’t do that. Why?

The real solution to almost all the problems is to reward savers, not borrowers, as was the case, more or less, before the 1960s. Let the market set rates, not the central banks. This will fix asset inflation. It will be very painful, but less painful than allowing the central banks to have a printing press.

In a just world, of course Powell (and the rest of the FOMC) should have been removed and replaced with people who have something resembling competence.

But in the real world, if Powell had been removed at any point in his tenure as Fed chair by either of the presidents he served under, the replacements would have been worse, not better.

Your inability to comprehend basic facts does not reflect on Powell’s or any FED bkards competence.

Maybe you might want to review your assumptions. Just saying.

What basic facts, specifically, am I failing to comprehend?

A fool thinks himself to be wise, a wise man knows himself to be a fool.

—-wiliam shakespear

That Powell quote is certainly egregious, but he’s a lawyer, not an economist. My suspicion is that there are underlings within the Fed who know better, much as those at the Bank of England who wrote “Working Paper No. 529: Banks are not intermediaries of loanable funds — and why this matters”

(Zoltan Jakab and Michael Kumhof May 2015)

But it will take a while for the old guard to die off, and it will likely take even longer for the dullards who are your elected representatives and policymakers to catch on …

The 50 point rate cut was ridiculous. If any cut was needed, then 25 would have been adequate. None of the “data” Komissar Powell says he relies on suggested any cut was needed. Therefore one can only conclude the Komissar’s decision was based on other factors. Powell wants to keep his job, and Trump has indicated he will fire him. The Democrats in power said they wanted lower rates. Senator Warren sent the Fed a letter suggesting a 75 point cut. Do the math. I know Wolf does not like politics, but really what was Komissar Powell’s motivation? Keeping ones job in DC includes factors that are both economic and political. Mortgage rates (as Wolf pointed out) and the long bond market suggest Powell was full of you know what. Short-term T-bill rates are creeping back up to nearly 5%.

These people are either going to have to regulate their own behavior and not let their desire for filthy lucre govern that behavior, or it’ll be done for them. In what form that will be, I don’t know, but history does not look kindly on greed.

Tin foil hat talk. Nutty.

When the rate cut happened, there was plenty of data that showed the employment market was softening.

Turn off FOX, educate yourself. Stop letting your political masters take advantage of you.

“plenty of data that showed the employment market was softening”

And also plenty of data that inflation was nowhere near their 2% target.

And now that “plenty of data” about unemployment has been revised away, and inflation is moving back up.

So the question is: will they continue cutting?

NB: I had been defending Powell & the Fed on this site for holding rates at 5.5%, but I think continued cuts will come to be viewed as a policy error.

I hope Powell can see the forest through the trees.

The Federal Reserve works at the pleasure of Congress, not the President. The President has no ability to fire Powell. Congress, at the behest of the leadership of the House and Senate, does. The likelihood the current House and Senate are going to vote to remove Powell is a big, fat zero.

The Fed chair is nominated by the president and confirmed, or not, by the Senate. The House is not involved in any way. Powell’s term ends in May 2026 and will not be renewed if the president does not nominate him. Terms are four years. Trump has indicated he no longer wants Powell as Fed chair, and will not renominate him, which is the same as firing him. But don’t let the facts get in your way,

Your constant reference to Powell as a Russian Party Official makes me wonder how anyone can take you seriously.

It’s not productive, it’s annoying.

Take it to X

Mkst reckless move in history?

Lol. Hilarious. We’re you born yesterday?

The FED has made tone of mistakes. This isn’t even in the top 5.

You’re just triggered all over the place on this thread, aren’t you? Thorazine – it’s what’s for breakfast.

In American Yale Professor Irving Fisher’s truistic “equation of exchange” (a transaction concept, not an income concept), the rate-of-change in short-term money flows (proxy for R-gDp) is headed lower. However, simultaneously, the proxy for long-term money flows is headed higher. This is based on the distributed lag effect of money flows, the volume and velocity of money.

So, we have the classic paradox, a double bind for the Fed (FOMC schizophrenia: Do I stop because inflation is increasing? Or do I go because R-gDp is falling?). If it pursues a rather restrictive monetary policy, e.g., QT, interest rates tend to rise.

This places a damper on the creation of new money but, paradoxically drives existing money (savings) out of circulation into frozen deposits (un-used and un-spent, lost to both consumption and investment). I.e., the percentage of DDs to TDs shrinks. In a twinkling, the economy begins to suffer. 2018 is prima facie evidence.

This is why the correct policy levers are primarily on the fiscal side — but good luck getting any traction with this understanding over all the noisy heat and smoke generated by endless arguments about monetary policy.

I am increasingly suspicious that this widespread misunderstanding is not entirely accidental — many rice bowls depend upon sustaining it …

Welcome to the Twilight zone, Nothing is real, what’s up is really down…

Maybe Uncle Herman really isn’t dead, I’m heading to the graveyard with Aunt Bertha.

Shhh… Little Jeromey might wish us all into the cornyard! Repeat-> “It’s a good thing you did with those fine rate cuts, Jerome. A real good thing!”.

We’re back to Transitory Town? Like a Twilight Zone train that keeps looping?

At what valuation will hedge funds, ETFs, say “Time to take profits and move our money to 4-6% bonds, TBills, foreign markets ?

The big down move won’t come from economic downturn (due to Fed Put) but rather from valuations that cannot be sustained with rosy projections and promises of ever bigger profits.

Would those among us with that downturn calendar date please give me a heads up ?

Well, that will take a while. The 50 bps rate cut has already done its damage.

There is a high probability that stock prices could fail this month (Michael Oliver), which would increase bond buying (and prices) for a few months. The asset price collapse would lower tax revenues. The Fed will print money in response, be assured of that (Luke Gromen). How easily we forget that economic growth is built on saving, not borrowing.

“The headline unemployment rate (U-3) dipped to 4.1%”

U-3 came in at 4.052% – literally 3bps away from being rounded down to an even 4.0%.

The labor market is fine, but inflation supporters will continue to push for lower rates and other inflationary policies.

It would be a hoot if it drops back to 3.9% over the next few months, with wages rising at a 5%+ pace.

Sounds like a .50 rate hike after the election.

lmao!

It would be a hoot indeed.

“Wage-price spiral? What wage-price spiral? My eyes are closed!”

Sounds like a carnival ride.

Just got my six-month auto insurance renewal offer. With no changes to my insured vehicle or my driving record, the six-month increase is 5.8%. Clearly, inflation is vanquished!

Isn’t that the very definition of cherry picking?

No, that would be citing an increase in the price of cherries.

I think Pea Sea’s comment was tongue-in-cheek… CPI for auto insurance has been a lot higher (yoy) per CPI, so it’s exciting to see “only” 5.8% semi-annualized increase.

No. It’s an anecdote. In posting my anecdote, I assume that I’m writing for grown adults who can recognize an anecdote when they see one, and can give it the appropriate amount of weight (and can take it with the requisite grain of salt, as it’s clearly just a blog comment offered with no proof).

In that case you’re lucky your insurance inflation is that low. Mine went up something like 20% last year.

Insurance rates reflect true cost increases. Salaries of insurance & auto repair workers, materials, auto parts, health care costs, injury rewards, legal costs, operational costs of both industries…. It’s more than an anecdote. It’s evidence that official numbers are lowballed, arguably on purpose.

It’s almost a u-turn. Forget all the numbers and revisions of the past two years. Look at these new and improved numbers.

Who has some trust left now it turns out they were wrong all the time. Or have we been fooled? And have we been fooled now or in the past?

What direction do we take, now we discovered that our compasses have been of no value at all?

Hard to deal in facts when the revisionistas are staggering about on the front lawn, revising.

She said she was a stable red head with a sizeable bank account, then after revision she became a poor street walking crack head with crabs, but her hair was red.

You people are a hoot: it’s political when the numbers are revised down, and it’s political when the numbers are revised up, and it’s political when the numbers are not revised at all. This BS never ends.

And all this means what to the growing deficit or inflation!

Perhaps all the numbers will be revised again next week and the Fed will be seen as saviors.

The USS Titanic is full steam ahead and me checking on the lifeboats.

To me, it all comes back to the voters, and the dynamics of our democracy today. For politicians, it is impossible to remain in office while (1) taxing responsibly in relation to spending, or even to suggest that, or (2) lowering spending to an other-than-fantasy level. So here we are. I can rearrange deck chairs a tiny bit in my investing choices.

I see inflation as our actual tax, along with tariffs, because anything called a tax will be howled down.

That was true in some measure since the founding of this country, which was in part a big tax revolt.

A perhaps not-so-new fun feature added on top, intensifying this state of mass unreality, is the savior grift in our politics. Somehow star zillionaires are going to save our species and magically transport us to a fantasy past. But for me, the ultimate villain is us, in the aggregate. All I can do is clip my coupons and keep my leverage low!

I’m still puffing inhalers like a madman, trying to keep up in this game of how to invest for post pandemic and post election.

Last night I was looking at s&p500 valuation and it appears to be in the Goldilocks camp, relaxing with champagne on the soft landing — the current spread between bbb and 10 yr was 1.18%, which apparently gives us the adjusted E/P ratio premium of 4.97% — set against E/P ratio of 4.31% for future s&p earnings estimates.

My hesitation and fear about a recession is disappearing and instead of a downward revision in future earnings, this series of upgrades to GDP and decline in unemployment really screws up my pessimism — however, the hints of increased inflation and currency debasement are floating back to the surface.

However, as we’ve seen with equities over the past four years, inflation and valuation stuff hasn’t mattered a bit — but therein lies the black swan ghost and, maybe this time is different.

Reigniting a rally in stocks as treasury yields slowly drift higher, essentially takes us back to higher for longer instability with inflation weighing on growth.

I think things go sideways with ambiguity while everyone trips over each other in a very volatile, crazy world, where data and news — along with the feds credibility are irrelevant.

The Goldilocks economy and soft landing will continually be under enormous pressure in terms of sustainability — Goldilocks is Schrödingers cat!

The Fed is like a hippo in thinning waters. The food is going, but it keeps devouring everything in sight, sucking loan money from the private markets to fund government largesse in general. Every dollar the Fed arranges for the fedgov to have, is a dollar that private industry could have used to develop, modernize… nice work, guys.

There is no competition for money. Rates are dropping, in fact. Your statement applies to a world that no longer exists — one that went away over a decade ago. There is no barrier to money creation in a low rate environment.

Money is a flow, not a stock.

The future is confusing

Gold stumbles as a strong payrolls report seems likely to lock in 25 bps in November,” said Tai Wong, a New York-based independent metals trader. “Revisions to last month were higher as well, which we haven’t seen in many months, while the unemployment rate ticked lower even as participation stayed flat.”

Even the Yen and Japan are confused — they did a 180 yesterday on rate hikes, because of recession fear — so expect another 180 very soon, ack to inflation fears.

The US Dollar Index shoots through the roof after stellar Nonfarm Payrolls print urges traders to wind down Fed rate cut bets.

upbeat US Jobs Report that saw Nonfarm Payrolls jump to254,000 against the expected 150,000 has triggered an unwind in the sizes of rate cuts expected from the Fed for the coming months. With that, the boost and surge in demand for Oil could be diminished and be less a driver for Oil prices as it was when multiple big rate cuts were still priced in…

Everything confused except greed

So now wage growth rate is almost 3 times higher than the inflation target growth rate, unemployment is at a ridiculously low 4.1%, and the Fed wants to lower rates? Don’t hand them a pistol, because they’re sure to shoot themselves in the foot.

Mr Wolf I love your articles! Always so informative (even thought I need to ask ChatGPT about words I don’t understand)

Have you considered using AI to write your articles? It could free up time for golf….. NVDA to 150!!!!!

Generative AI has been used in publishing for many years. I was approached in 2016 by some outfit that wanted me to try its version. Reuters, Bloomberg, MarketWatch, etc. have all published AI-generated articles for many years, sometimes edited by a human, sometimes not, sometimes disclosed as AI-generated, sometimes not.

Now everyone wants me to use it for a fee, Jetpack (part of WordPress on whose CMS this site runs) wants me to use it to write articles, for a fee. MailChimp, which I use to send the daily emails to subscribers, wants me use its AI (since it got bought by Intuit) to write the headlines for a fee, etc.

Generative AI has already killed many good websites (they’re now bad websites).

Seeking Alpha has an outright prohibition against AI-generated stuff. All contributors have to agree to it.

That said, there is a lot of human-generated BS out there in the media, so AI can replace those humans, no problem, and it’ll cost less and can’t be any worse.

Someday in the near-ish future, I’m going to write an article with this headline:

“If AI Takes Over my Job, I’m Just Going to Walk Out in a Huff.”

I like this fantastic artisanal stuff. But I buy equity in the robot that might devour my job, just in case. Gotta hedge.

Overheard a Walmart order puller (ie most likely not a long term Walmart employee) tell another employee that he had finally got an AI to act reasonable. That got me to thinking that maybe herding AI would replace writing code meme as the way for smart people to get ahead in the job market.

Good stuff. Like you mentioned, there are some highly educated/ respected people who write the crappiest articles full of BS.

AI is the future in many fields. It will be a boon to mankind. I have lots of hope for AI. That said, currently it is overhyped and I think there will be lots of money conned out of people in the near future in the name of AI.

Mr. Richter, I’m curious. Do websites that use Generative AI to create articles also have the ability to use Generative AI to create “comments”?

Bots have been creating “comments” for many years, including on this site for over a decade, and I usually recognize them now and block them. This includes dozens to hundreds of spam comments this site gets every day that are all bot-generated, and I always block them.

It doesn’t require AI. Bot accounts were a huge problem on Twitter for many years. Not sure if it’s still the case on X.

I assume that AI comments are smarter than bot-generated comments. Some posters here have posted AI-generated comments and said so. They weren’t too bad, not good either.

I stumbled into a generated article about how Lam Research was going to the moon, $80 to $800, invest now!

The reality…LRCX started the day at about $800 and ended at about $80, after a 10 for 1 split.

Even the data is ziggin and zaggin. Unreal!

Powell has his zoot suit on and is weaving down the alleys. Saturday night will be fun, but after that ….

There is a claim that most of the job increases are Gov jobs and that the BLS didn’t seasonally adjust enough for teachers coming back from summer vacation.

There is a cottage industry out there that every month cherry-picks a couple of month-to-month items and says it was all fake. Every month. One month, it’s government jobs (teachers); another month, it’s bartenders, another months it’s healthcare workers; the next month it’s whatever. It never fails. There’s always a couple of items that fall out of line. And those get cherry-picked. It’s always the same BS but a different flavor.

That’s why I look at the three-month average (the big fat red lines in the charts). So show me the three-month average.

Seasonal adjustment factors cancel out because they’re negative one month and positive another, and over a 12-month period they add up to zero. If they’re too high in one month, they’re then too low in another. That’s also why I look at the three-month average (big fat red line in the charts).

NOT seasonally adjusted, nonfarm payrolls spiked by 460,000! Seasonal adjustment cut the increase in nearly half (254,000)

Why cut rates at all? The economy is strong, the unemployment rate is low, the stock market is bouyant, and property prices in most cities are still too high for many people to afford. This is a problem in many countries, including where I was born (Australia).

I think the Fed should spend less time trying to predict the future with its forward guidance and focus more on what’s happening now. When asked about the future, the boilerplate response should be we’ll let the data decide what’s the best course of action. No one can predict with confidence what will happen – we’ve seen that time and time again.

Powell’s comments that rates would stay low for a prolonged period and that inflation was transitory fuelled the speculative bubble in 2020 and 2021. Other central bankers made the same mistake, notably Phil Lowe at the RBA who foolishly said rates would stay around 0% for years.

Powell has made some mistakes but he has a tough job and has generally done a good job, especially over the last couple of years. However, his comment that property prices are a supply problem and not an issue for the Fed to take into account is misguided. The supply of good land is fixed and it takes time to build suitable housing. In my opinion, he should also stop painting himself into a corner but trying to predict what’s going to happen. The lessson from 2020 and 2021 still hasn’t been heeded.

And to make matters worse, after the central bankers were wrong about 0% rates in 2021, they doubled down and refused to do anything for over a year. It’s not just Powell, but all of them.

The number 1 Fed mandate is to make sure the banks are protected and grossly profitable.

They’ve been crying uncle in my opinion and pow pow caved.

Yep. That and several other things that all came to a head at once. The Fed has become exasperated and punted on inflation fighting to address a portfolio of other “needs”.

I think maintaining the asset bubble is their number one priority, as too many institutional investors, banks, and other parties needed to maintain wealth effect spending rely on it.

The S&P is now nearly double where it was in May 2020, when the Fed’s balance sheet was the same. That means that the bubble is based on the Fed Put, not economic reality and not liquidity.

The Fed needs to maintain that, for a host of reasons, which are unfortunately bad for the common man.

A common man has 401. A common man could invest every month what they pay for cable TV, not needed truck payments, latte etc and be millionaire in years. Actually it feels like a communism when the main focus is to make an undisciplined common man “rich”.

Yeah, and if the 401K went insane without a corresponding increase in production, it would buy less stuff in retirement.

Asset bubbles are a problem, as they inevitably lead to wealth concentration.

Asset bubbles are part/essence of capitalism. What system would be better. How would you control a buble?

Biker: Look up Mises, and the Mises Society. Mises believed that bubbles are the most destructive economic force, and the Central Banks are mainly interested in sustaining them.

Here is my partly? coherent bubbling.

Economy is not a hard science. There are different “schools”. Too much human’s psychology etc is involved. The schools are creating nice desks, salaries for the involved. Good for them.

Bubbles are part of price discoveries. It is hard to really know if something is in bubble. Can only tell for sure after the burst.

Excessive bubbles are something to avoid obviously, not be the part of it. Attempts of controlling bubbles often could be worse than the bubbles itself.

30+ years ago I was a witness of an economy without bubbles. The prices were set by party/government. No bubbles, but no goods available too.

That literally isn’t true, but you do you. Whatever makes you feel good.

The FED would have never raises rates to 5.5% if what you said was true.

The FED is run by the American Bankers Association. The politics were to accommodate the banking lobbyists which influence the House & Senate Banking Committees (whose “campaign contributions typically exceed all other industry & labor groupings”).

So, the Fed & Congress eliminated Reg Q ceilings, converted all the thrifts into commercial banks, reduced reserve requirements until reserves were no longer “binding”, & allowed financial engineering to undermine funding for all.

see for example:

SEC.gov | SEC Adopts Money Market Fund Reform Rules

There was no legitimate reason to cut rates other than pier pressure

There “was” a legitimate reason. But it went way.

Again the BLS repeats its refrain “What we told you last month is rubbish” – there should be a penalty for wasting Wolf’s time in this way

Way I look at it, the economy is roaring at an annual 3% GDP that is fueled by deficit spending at 6% of GDP? I look at this as a kind of “check engine”, economic indicator. These numbers make no sense to me.

Anyhow, the only interest rate that matters is the “real” rate, that is (interest rate – inflation rate). And, if it is true that inflation has receded, and the interest rate hadn’t, then, the real interest rate would have risen, amounting to a tightening.

The Fed is within their bounds to keep the real interest rate constant so as to not tighten further. So, if they’re keeping the real rate constant, so be it.

(It’s when they want a negative real rate that they have to fire up the printer for QE.)

From a 50bps cut in November to a chance of no cut in just one week.

Alot of those 60/40 portfolios are going be thinking WTF happened to my bonds this week… Better buy more stocks lol

Just to be the contrarian, the cut was perfectly timed as by Spring time the slowdowns will begin and the cuts will have sunk in. The decline in rates will get the housing markets going which will drive spending in the home improvement and other related areas. The first 15 plays are drawn up so time to get them executed.

“The decline in rates will get the housing markets going”

You’re talking about the prior decline in rates, the one BEFORE the rate cut. Because long-term rates, including 30-year mortgage rates, have shot up since the rate cut. They’re higher now than they were months ago. Inflation fears are pushing up long-term rates. The daily measure of 30-year fixed mortgage rates is back at 6.5%, and the 10-year yield is back at nearly 4%.

The Fed’s role is a low vol mandate and liquefier of assets, can’t not think the Fed wasn’t aware and got the 50 pt cut in before this report as it would have been much less palatable after. PPI coming in hot pre cut, guess I just feel dumb shorting high yield.debt and CRE

I don’t believe the govt data on the job market. I see a lot of job losses that lead to lower paying jobs, and that’s for the workers who find a job.

I went to Goodwill today, a box store sized one in my town. The parking lot was 90%+ full. The crowd was mostly young, both men and women. About 10% of the merchandise was new with tags, mostly lower priced merchandise, but a good assortment. There is always new merchandise in this Goodwill, I assume the merchandise is being donated by all the stores that are closing. It is also not a good sign to see young men shopping there on a weekday in the middle of the day. This is the data I believe.

My community college has maybe a quarter of the cars in the parking lot as it did in years past and my neighbor who teaches math there hasn’t had much work. Most of the cars are probably administrative folks and janitorial

Hanging with petunia at goodwill picking up some stuff. Not the worst of news.

Go to the morgue if you think things are bad at goodwill, look at the bodies, many unclaimed. Young men and women who die young from drugs and suicide….so many.

Donations of clothing to Goodwill are tax deductible if you itemize. You can download the normal amounts you can deduct for each piece of clothing. Lots of people get rid of stuff that way, including us, that they no longer want or like, or that doesn’t fit anymore, or never fit, or that they bought in error, etc.

If you go to the Goodwill, you will find people who shop at Goodwill. If you go to a soup kitchen, you will find hungry people. This will be the case regardless of where you are in the economic cycle.

Pea Sea, wonderful comment dear.

This is an inflationary great depression, evidenced by the homelessness epidemic and by observations of young adult poverty, such as yours. We are reliving an inflationary version of the 1930s. The inflationary aspect makes it worse, not better.

Goodwill stores are packed with flippers. Flipper trolls- wait on new carts to hit the floor – I’ve heard they can be quite aggressive. They complain when items are marked too high because it cuts into their margins.

Lots of people won’t search thru thrift stores but will easily check ebay to find what they want. Flippers are great for getting donations into other hands. From Peoria to Atlanta. Or wherever. Too bad so much ends up in landfills. Too bad people buy so much that they just don’t need.

Indeed shows opening for Goodwill District Manager – San Fran – $110,000. That’s a lot of donations.

I don’t get how [6] million migrants get picked up in many official statistics if so many are illegal and lack any papers entitling them to jobs etc. If you were an illegal migrant, would you be answering these surveys? If you were an employer breaking the law, would you be filling in the return fully and honestly to these enquiries?

Also, I get why there is always a percentage of employers willing to hire undocumented migrants, but to believe that they picked up even a majority of these folk in just three years, it seems a stretch.

Go to your local social security office and see the line for getting an appointment for a new social security card. I was there twice at the beginning of this year and was astonished at the number of immigrants. The new border crossers are all asylum seekers and they are technically not undocumented.

Wolf,

It is my opinion that the FED was perfectly justified in cutting rates last meeting. Personally I would have only cut .25 BPS, but I understand the .50 rate cut. The difference wasn’t significant in the bigger picture.

I also think that in light of the latest employment data, the FED will not be cutting rates at all in the near future. It will definitely give them pause.

I don’t think you would disagree with either of these views. Moderate, with an understanding that the economy is in a very grey area.

What i do not understand is why you tolerate the nuttiness here. I can fully respect a contrarian argument that the FED should have held off due to certain data. I might not agree, but I would respect it and certainly take it into consideration regarding my thinking.

However, many posters go beyond that. They assert that the cut was for conspiracy reasons. They do not cite data. They take it as a given. It is true because they want it to be true.

Why do you allow thise type of comments to stay? Don’t get me wrong, I am all for hearing contrarian views. Challenging my thinking only sharpens my views. However, unsupported nuttiness is none of that and actually distracts from valuable interactions.

For most working class people interest rates don’t matter. When we desperately needed a newer car, we bought it at 24% interest. We could afford the payment and our credit was bad. We had no choice but to pay. Our last car was purchased at 6% interest and we are barely affording it because the price were so high.