Fewer quits and historically low layoffs & discharges mean fewer job openings, and less hiring to fill them. The massive pandemic churn slowed. But that’s only part of it.

By Wolf Richter for WOLF STREET.

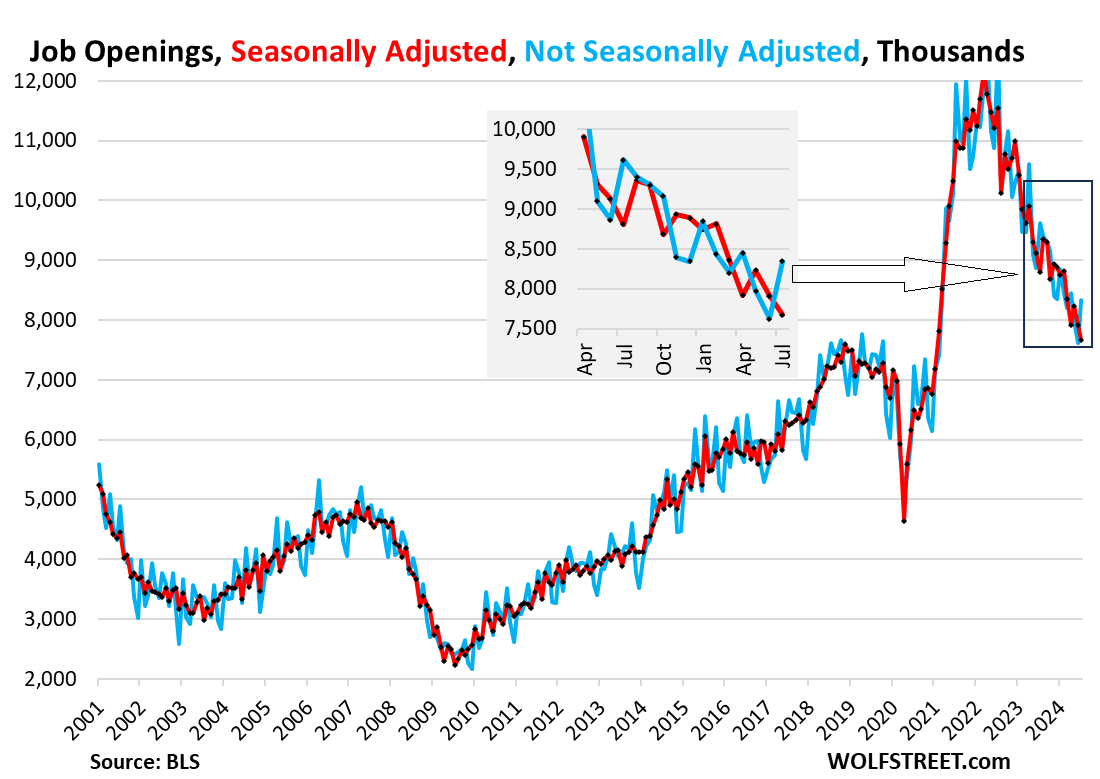

Not seasonally adjusted, the number of job openings in July jumped by 720,000 to 8.34 million, according to data released today by the Bureau of Labor Statistics. Job openings typically jump in July: Last year, they jumped by 750,000; in July 2019, they jumped by only 250,000; in July 2018, they jumped by only 414,000. So the July jump this year was fairly hefty compared to the last two prepandemic years (blue line in the chart below).

But seasonal adjustments that attempt to iron out this seasonality slashed the seasonally adjusted job openings by 668,000 to 7.67 million (red). The insert shows the details back to April 2023.

Beyond the month-to-month seasonality, we can see the trend: Job openings have come down from the crazy period of the labor shortages but remain well above the prepandemic levels in the data going back to 2001. So are job openings now normalizing? What even is normal? We’ll look at those questions in a moment.

This data is based on surveys of about 21,000 work sites, released today by the BLS as part of its Job Openings and Labor Turnover Survey (JOLTS).

What is normal?

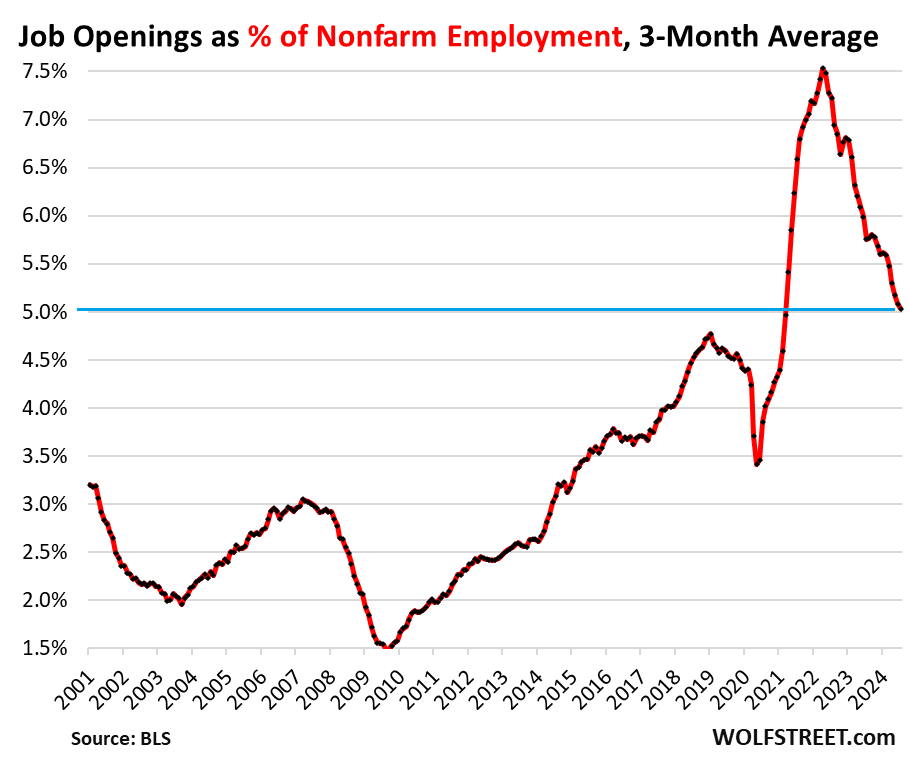

The ratio of job openings to nonfarm employment takes into account the growth of employment over the years. As the population, the labor force, and employment grow over the years, job openings should also grow with them. The ratio of job openings to nonfarm employment shows this relationship.

On a seasonally adjusted basis, job openings as a percentage of nonfarm employment dipped to 4.9%, which still higher than the highest point during the strong labor market in late 2018, and far higher than any period beyond that going back to 2001.

The three-month average, which irons out some of the month-to-month squiggles, dipped to 5.0%, well above all prepandemic levels. This perspective shows that the labor shortages are mostly gone, but that the labor market remains relatively tight compared to prepandemic normal:

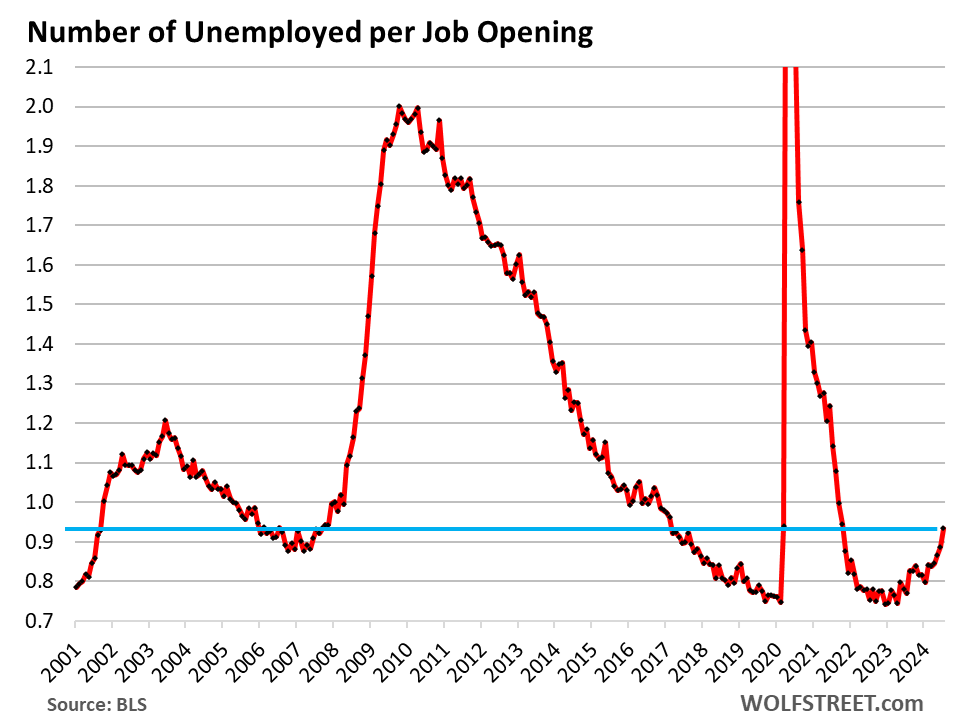

The number of unemployed persons per job opening is a ratio that Powell mentions a lot in his press conferences as one of the indicators of labor market tightness, meaning the supply of labor in relationship to jobs.

The number of unemployed persons includes the portion of the well over 6 million immigrants that came to the US in 2022 through 2024 (Congressional Budget Office data) that are looking for work but haven’t found work yet, and therefore count as unemployed.

This massive influx of immigrants has caused the number of unemployed to increase though layoffs and discharges remain historically low, as we’ll see in a moment.

In the jobs report for July, there were 7.16 million unemployed looking for work, while in today’s JOLTS data, there were 7.67 million job openings in July (both seasonally adjusted), so 0.93 unemployed persons looking for a job for each job opening.

From this perspective, which includes the large number of immigrants still looking for work, the labor market is looser (bigger supply of labor) than it had been during the relatively tight labor market in 2018 and 2019:

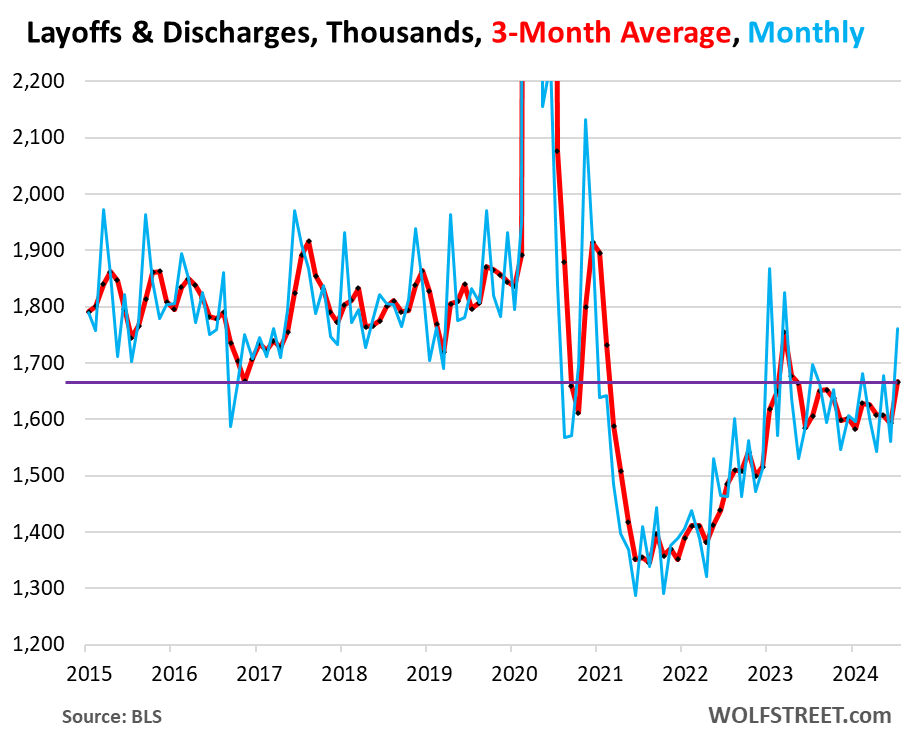

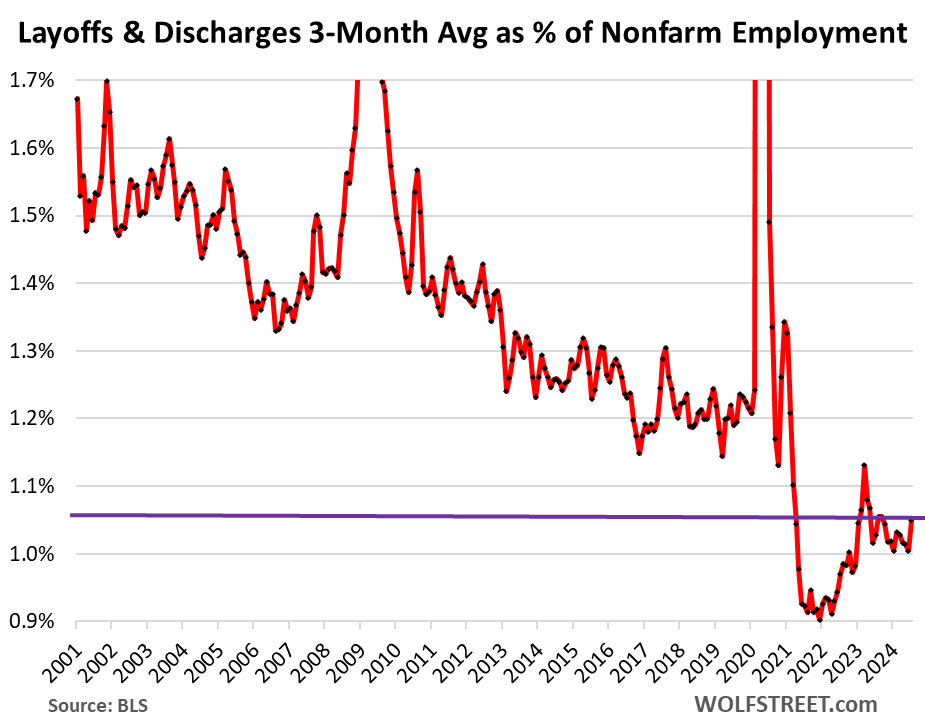

Layoffs and discharges jumped to 1.76 million in July after having dropped sharply in June. This is very volatile data with big month-to-month squiggles. The three-month average irons out some of the squiggles. It rose to 1.67 million, still in the same range it has been in since early 2023, and below the low points of the prepandemic years.

The initial unemployment insurance claims reported by the Labor Department have shown a similar situation: Despite some breathless headlines about layoff announcements globally, there have been fewer layoffs and discharges than during the Good Times before the pandemic.

Layoffs and discharges in relationship to nonfarm employment is a ratio that accounts for growing employment over the years.

From that perspective, layoffs and discharges are still far below normal (to iron out some of the big month-to-month squiggles, we use the three-month average of layoffs and discharges).

This is a sign that employers are hanging on to their workers. Some economists have speculated that employers are “hoarding” workers because they got burned with the labor shortages after their mass-layoffs during the pandemic when they couldn’t rehire the people that they’d let go. If true, that would be a good thing. Maybe employers learned something.

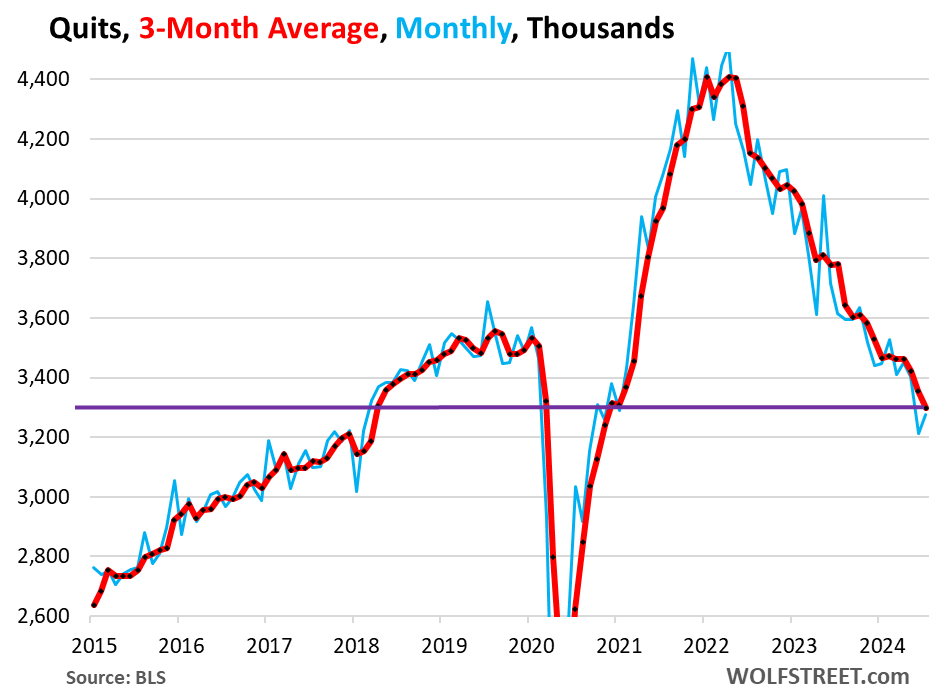

And workers quit quitting. Voluntary quits ticked up to 3.28 million in July. The three-month average dipped to 3.30 million, well below the levels of 2018 and 2019.

After the huge churn during the pandemic, when workers jumped jobs and industries to improve their pay and working conditions, it seems they have settled in.

Fewer voluntary quits and historically low layoffs and discharges mean fewer job openings to fill, which means less hiring, and less competition for labor. The massive churn during the pandemic is over, that’s for sure.

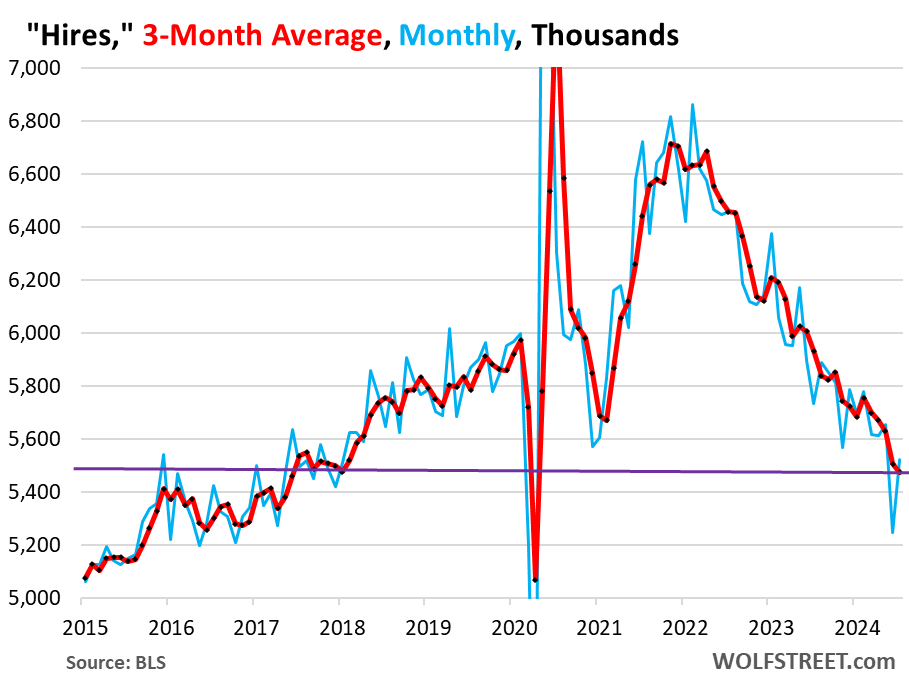

Hires jumped to 5.52 million in July, seasonally adjusted, after the drop in June. The three-month average inched down to 5.47 million.

So let’s repeat: Fewer voluntary quits and historically low layoffs and discharges – as employers cling to their workers – mean fewer job openings to fill, which means less hiring. And that’s part of what we’re seeing here.

The other part we’re seeing here is that the economy now creates jobs at a slower rate than in heady days of 2022 and 2023, and there are fewer new jobs to fill.

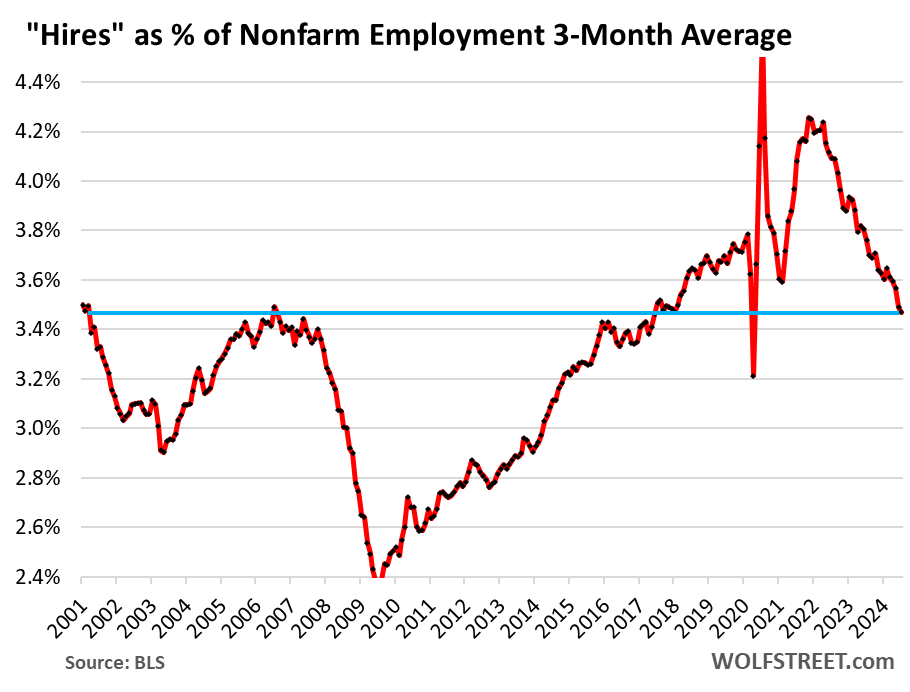

Hires in relationship to nonfarm payrolls has declined below 2018-2019 levels, which were considered tight labor market conditions, but remain well above nearly all months in the prior period going back to 2001. Is this level of hiring in relationship to payrolls historically “normal?” Maybe.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Speaking of normalizing, apparently the 2/10 yield curve de-inverted..as it usually does when recession actually starts. I guess the consensus was “this time it’s different for the last few years” but I guess we’ll see.

It inverted and uninverted in 2019 and there was no recession. Here is my explanation why the yield curve in the era of QE and QT by the Fed and now of bond-buybacks by the Treasury Dept. has become meaningless:

https://wolfstreet.com/2024/08/26/the-data-mess-markets-interest-rates-risks-of-financialization-overleverage/

Only the 2-year 10-year spread uninverted by 1 basis point — again. It also happened a few days ago. And in 2019. All the other spreads are still massively inverted.

Here’s the 3-month 10-year spread, still inverted with a spread of -141 basis points. Note the inversion in March 2019 and the uninversion in Aug 2019, and nothing happened. This was the first time that the yield curve failed as a recession predictor.

I have long said that the yield curve cannot predict recessions during the era of QE and QT because the bond market no longer reacts to the economy; it reacts to the Fed and the Fed’s gigantic balance sheet and to what it thinks the Fed might do. And now there are Treasury buybacks to muck up the bond market’s predictive spirit.

Nice point. I even doubt whether the markets care about the balance sheet. May be they only care about the possible rate cuts.

Apart from that, I think there will be no recession ever. Markets learned that money is not a finite resource – CBs can print as much money as needed to dodge any recession. But the assets are finite. There can be stagflation, but that’s a very low probability.

The short end of the curve reacts to Fed rates. During rate hikes, the short end of the curve shoots higher. With rate cuts in the future, the short end drops. So that’s determined by the Fed’s rate cuts/hikes, and not the economy.

The long end reacts to a mix of inflation expectations, rate cut expectations, fear, supply, demand, exuberance, etc. The Fed plays a big role in rate cut expectations, supply (QT when markets have to absorb the bonds), and demand (QE when the Fed buys).

So you get this dynamic where the Fed hikes rates and pushes up short-term yields a lot (to 5.5%), while long-term yields dance to different dynamics and don’t rise as much, so the yield curve inverts.

Then, the Fed talks about cuts and actually cuts, and short-term yields plunge, while long-term yields move down more slowly. And the yield curve uninverts.

All this happened in 2019, and there was no recession. Just the mechanics of the new era.

“CBs can print as much money as needed to dodge any recession. But the assets are finite. There can be stagflation, but that’s a very low probability.”

Sure, the Fed has discovered the MMT infinite free lunch during 25 years of pretty damn crappy total payroll growth (compare it to prior 25 year periods) and a widely pissed off populace is just imagining things in terms of overall economic deterioration.

At least you beat the MMT’ers in terms of pointing out that printing money doesn’t magically create real assets (instead, rather, immediately creating inflation as the ratio of money-to-real-assets zooms up).

*Maybe* that government-led inflation lashes increased economic activity (and payrolls? significantly?) into existence – *because that inflation operates as a *taking* of every private dollar saver’s prior savings level – ie, money printing equals savings dilution.

The G, as unbacked master printer makes out.

*Some* reckless speculators (gambling on how ZIRP/inflation will distort the asset markets) make out.

(See floating rate newbie apartment landlord speculators (Applesway) who blew themselves up…but not before evicting tenants who actually couldn’t afford 25% rent hikes…)

But the dollar holders/savers?

They get incrementally expropriated in the name of giving the G yet another shot at fixing its policy errors (which led to the *prior* stagflations).

You just pointed out how we have financed debt in America. Like 1929, it took time to reveal the depression. The 3 month vs 10 year is more manipulated than the 2s and 10s.

Wolf-

You said “And now there are Treasury buybacks to muck up the bond market’s predictive spirit.”

Apologies if I’m asking a repetitive question, but what’s the expectation for how long the duration-swap Treasury maneuver (Operation Twist 3.0) will continue?

Has Treasury stated intention as to timespans, quantities, or policy goals?

Or is this another reactive credit market “experiment,” with no fixed plan to conclude? (…in which case, “Mr. Bond Market – RIP”)

Thanks in advance.

They buying back those bonds (issued during the low-interest era) at discounts, and they’re replacing the discounted buyback value with new bonds (with higher yields), which lowers the outstanding balance of the debt. They can keep doing this until they run out of bonds to buy at a discount, which depends on where yields are going, but at the current pace of buybacks of $2-4 billion a week, it could go on for quite a while.

True that during the Era of QE/QT many of the normal indicators and relationships have not been reliable. But the question becomes – did the Fed “solve” the economy and business cycle and banish recessions forever? Is it finally different this time? Or will the price to pay just be that much steeper when the Laws of Economics assert themselves again. Maybe there is a free lunch and our wonderous central bank will be serving the sandwiches in perpetuity as long as we all believe.

Rate cuts are coming? Great that means things are going perfectly and the stock market will soar to all time highs. Or as QT has progressed that’s also great and the stock market has soared to all time highs. If the Fed decides to restart QE that will also be great and the stock market should soar to all time highs. I can’t think of any scenario where the market is expected to do anything but soar to all time highs.

The Fed did not “fix” the business cycle, and there will always be recessions, though the Fed thinks that it should try to prevent recessions unless inflation surges (the dual mandate).

A recession is not the end of the world. Run of the mill recessions last a couple of quarters during which GDP declines a little, companies shed jobs, employment drops a little, unemployment rises, and lots of debt blows up at investor expense (but investors got paid to take those risks). And after the debt-blowup, companies are less burdened by debt and can expand again, and growth starts all over again. That’s how it should work. But the Fed is supposed to prevent that from happening, which is part of the problem because the debt isn’t then allowed to blow up and keeps bogging down those businesses and the economy.

A big part of the asset price inflation we have seen since 2009 was the result of QE, and those results linger as QT has removed only part of it. the Fed should have never done QE. That had nothing to do with the business cycle.

The repo market says hi.

Nothing happened, well the memory hole certainly has a scar.

The repo market blowout was triggered by other issues that are now fairly well understood.

The yield curve as an indicator is long dead, unless you actually believe that CONgress is going to be fiscally responsible and balance the budget.

Interesting times.

Ancient Chinese curse: “May you live in interesting times”.

All these interesting data points right before the decision in two weeks. So far, from everything I gathered, nothing points to a good, strong reason for a rate cut. These unemployment numbers are still looking good, the market is still wild, and home prices are still out of control. Do we really need more fuel to add to the fire? It seems like the fire is burning quite well on its own, and we’re still not at the 2% target yet, let alone holding it at the 2% inflation target for a while.

Oh well, junkies need their next fix real soon, those temper tantrums is getting louder and louder..

If thing are normalizing, then I guess it depends on what your view is of the true neutral interest rate. Interest rates should probably trend towards neutral if all, or most, of the data indicate normalization.

Agreed. In other words, this economy and this job market is what most countries would love to experience….inflation is the problem, especially for young families…

Inflation was running what it is now back in the 80’s and 90’s (3%ish range). I headed a young family at the time and we were fine because my income grew at a bit higher rate. I think we all became spoiled in the early 2000’s when the US began massive imports from low-cost China and inflation collapsed. That kind of change may be a one off. I don’t know if any other country can be a low-cost producer with the discipline of China.

During rate hikes, Wall st and some FOMC doves used to say Financial conditions have already tightened, why to raise further. They used to give 10 yr yield as reference. Even Mary Daly once said 25 BP up move in 10 yr yield is like 50 BP hike in Federal Funds Rate. Well Reverse must be true then. 100 BP point downward move in 10 yr yield is like 200 BP rate cut in Federal Funds Rate. So why to cut rate at all in Sep?

4.3% is still historically low unemployment rate. This number is exaggerated because of 6 Million immigrants. Economy is doing fine. Labor Market is fine. Inflation is down but still higher than target. They have enough levers to pull if they had to do it. But as of now they should be patient and dont cut at all. Wait for inflation to go really down.

FED showed patience in 2008-2018 time-frame for inflation to go above 2%. They didnt say we are close enough and we are not going to wait till we actually cross 2%.

It feels like FOMC Doves have taken over again at FED.

Not for nothing, but the bookkeeping is that every deficit dollar adds a dollar into the non-government sector. It’s an “identity,” it’s always true by definition. The concept that every deficit dollar removes a dollar from the non-government sector is incorrect. Tax hikes remove dollars. Fed rate hikes transfer wealth from labor and small businesses up to the super-rich, who buy a lot of that debt. That’s called the “allocative effect.”

You left out the other side of borrowing: Government debt is money borrowed from investors (who want to earn the interest), so yes the funds do come out of the private sector, but from investors wishing to earn interest with the certainty that they will get their money back.

And then as the government spends the borrowed funds, it transfers them into the economy, but not all of it since part of the debt issuance is used to pay interest on the old debt which goes back to investors. So when the debt increases, it’s in essence a money flow from investors to the economy, but it creates this huge interest cost in the future, where more and more borrowing is needed just to pay the interest.

I agree 100%!

However with most control systems involving large inertia, you can’t continue full-throttle and expect not to overshoot and oscillate drastically.

You need to ease off the throttle slowly as you approach the desired point.

Ie, if you launch a satellite to a stable orbit, you don’t continue full-throttle up to the desired point. If you do, inertia will take you far beyond where you want to go and then you have to reverse throttle and oscillate. ie maybe overshoot enough for a recession/deflation.

Maybe the Fed supercomputers have some control system theory embedded. The previous once a month 3 martini lunches didn’t provide the best control.

After some thought, I guess the best analogy is the soft landing of a jetliner. You don’t go into a power dive and ease off when you reach the ground. You need to ease off well before the ground in order not to end up 6 feet under.

@Wolf says:

“So are job openings now normalizing? What even is normal? We’ll look at those questions in a moment.”

When I look at the first figure where the number of job openings spiked by around 5 million jobs from 2021 to 2022, I wonder how suddenly we ended up with such a spike in job-opening numbers. That many people died or quite the country or the free money and the resulting surge in stock prices lead to that spike? Interesting.

“The other part we’re seeing here is that the economy now creates jobs at a slower rate than in heady days of 2022 and 2023, and there are fewer new jobs to fill.” — 2022 to 2023 a magic?

I remember 2021 and 2022 were fairly lucrative years for remodeling, but never thought about there being 5 million more job openings those years. I remember reading about how there were layoffs, and the stimulus money was better than going back to work, so maybe that explains it.

All I know is there are not enough construction workers!

They were having openings in anticipation of forever business growth. It’s just an opening, doesn’t mean it had to be filled or had to make sense. When openings increased more than labor available, people saw an opportunity and moved around for big big pay hikes. Some of that excess was trimmed as the outlook normalized. Businesses don’t want to layoff more than necessary and people with 2021-22 packages are riding it out because of lack of opportunity for another 20-100% jump in salary.

Look at LinkedIn, tech workers are complaining about bad labor market and here Wolf is scratching his head, things are better than 2019, which was almost the best in past two decades.

At the current rate, 2025 – 2026 a fair number of employees with stock based compensation will see their wages fall, after their typical 4 year RSUs vest and companies are not aggressively competing for talent.

Of course, there are many assumptions about status quo continuing as is.

But my point is, people are not taking risks because they have inflated salaries.

@themsicles

Dead on. I’m one of the people you’re talking about, dipped my toe in the labor market this year and had a shockingly bad time, compared to any previous year other than 2009. Decided to keep quiet and hold very still at my current role as long as the good times keep rolling.

Hope to be gone by 2026 if the hammer drops.

We need to weed out the over leveraged not bail them out with lowered rates in order to right the ship.

Don’t the markets efficiently take care of matters such as that?

hahahahahaha…almost cost me a keyboard. thanks for the smile on my face.

So, the labor market is balanced, but on a very tight balance, and this tight balance was achieved during July, which most probably will be the coolest month of this year, in terms of labor market. The question is: What happens if the economy gets a liquidity boost? Will the companies increase their hiring in the face of increased consumer demand as consequence of cheaper credit (due to the decrease in yields), and the spike in equities as consequence of the increased liquidity in the market? Also, in such situation, how long will take before the employees notice that the labor market is hitting again, and start looking for better opportunity? If that happens, then what will be the impact of all of that on wage inflation and super core service CPI and PCE?

From anectodal evidence around me, I can see a strong demand for labor. I see and hear layoffs in north-east area, but the employees who are laid off find new jobs usually quickly.

Around me, strong demand for labor and blue collar workers and weeks at the lower spectrum of wage spectrum.

This is opposite for workers at higher spectrum of wages.

Around me, it seems like there is still steady demand for lower paying jobs, but less on the white collar side. I see hiring signs and ads, but not as many as 2 years ago.

On the flip side, we do have a open IT job on my team and haven’t gotten a single qualified resumes during the first two weeks of the position being posted.

I don’t know what to make of this data, but the doom & gloom rate-cut crowd are sure pushing their narrative with it.

Anecdotally, I have more work than I can handle at both my regular jobs right now.

When an 80 year old long retired guy get’s hit on to go back to work, IMO that indicates how desperate trying to find help has become.

When I ask, being on the daily walk my (4 legged) GF takes me on around the hood, why it’s taking so long to build the ”infill” houses under construction, the general superintendents start whining about how backed up all the subs are because they can’t find enough help.

When I ask how much the workers are getting paid, the answers are always a LOT more than even a couple years ago.

When a ”handyman” finally showed up to install a couple replacement doors recently, he was charging 3 times what we paid a couple of years ago, but was a bit better carpenter to be honest.

A decent sub in MN takes home $500 – $1500/day. Of course, that’s before taxes and equipment depreciation, but the general provides materials and consumables.

The thing is: inflation has come down a lot and all inflation metrics are well below the Fed’s policy rates. So the Fed has room to cut as long as its policy rates stay above the inflation rates.

If inflation rates head up again, it can hike rates some to keep up. Rate cuts are not final. Back in the day, before QE, there were rate cuts followed by rate hikes, no problem. An 8-year period with no rate hikes (2008-2016) has never occurred before in the data I can see going back to 1955. It was an anomaly, stuck at 0%.

Listening to the procession of doomers on YT interviews bloviate about recent layoffs you’d be convinced we’re in some kind of employment depression.

But the graph above showing layoffs as a percent of the workforce certainly paints a completely different picture than what you hear from a lot of self-proclaimed “experts” on this topic.

Is that a thing? I guess it depends on how you bend your antenna. My search algo’s feed me nonstop and econo-halcyon: all signs pointing up up up with bottomless punch bowls abounding.

It doesn’t hurt to have $2.5 trillion deficits spiking the punch bowl yearly. A balanced budget would now be the ruin of the economy, it can’t happen. Enjoy.

1.5 trillion fiscal year 2024

Max,

I think it depends what you do. If you are HR or Marketing in a large company, the good times have stopped rolling.

Sales, engineering, and skilled labor(plumbers, electricians, etc) seem to be short people who can do the work so the demand is there as long as the drunken sailors keep buying.

In my area of expertise, engineering, the engineers must do the tech work and the marketing along with their regular job. They have to learn to solder and make great PPT presentations. Much longer work hours to replace the jobs of the laid off people. Again, the drunken sailors keep buying so the work is more and not less.

It’s reasonable to posit, just like trillions in stimulus by the Fed & Congress contributed massively to inflation and broke many models of what comes next, that 12.5M new residents is massively distorting the labor market.

Everything is out of whack, which means when a recession arrives, we should expect it to get pretty ugly and for there to be a GONZO reaction on the part of Congress & the Fed.

Nobody has any real clue of what’s going on, including the Fed.

What is normal for the labor market is whatever prevents the worker from getting any real wage gains; it has been that way for centuries.

Innovation and technology prevents the individual worker from real wage gains. The owners of the land/capital and society and benefit though, generally speaking.

And (illegal) imigration.

If JPow pulls off a soft landing I’ll be beyond impressed. Even if things are normalizing – the slope of the lines coming from the Covid economy are steep. One move too soon or too late and I think we can overshoot by quite a bit.

Lot of turbulence at lower altitudes.

Lower altitudes? All the metrics I see are still at nosebleed levels…

So where do retirements fit into the picture? About 4 million people turn 65 every year. Some are already retired, and some are not yet ready to retire, but we still must be losing at least 300,000 workers a month. Just replacing them requires 300,000 new entrants, never mind growing the workforce.

It is not surprising that unemployment has stayed very low.

Up until now I was against any rate cut in September. Now, I can see that a 0.25% cut would be reasonable. Current interest rates are finally leading to weakening in the economy, despite strong job growth and huge government debt growth/spending. Considering that the bond markets (and presumably financial institutions to some degree) have already priced in a rate cut, it should not have too much of an impact, but may slow down or halt the current slight weakness. As Wolf has said, if inflation rears back up, the Fed can always raise back up when appropriate. That said, I can also see not cutting rates in September, but waiting until the following meeting to get another month’s data on inflation.

At this point, I’m not sure a 0.25% cut will make a huge difference, but I sure hope they don’t do a 0.50% cut — in my view the data don’t support a cut that large. Slow going is the best going for now.

The data supports a rate hike of at least 0.50% by the Federal Reserve just to address the massive and increasing inflation issue.

I think we should hike 1% ( ͡° ͜ʖ ͡° )

There is no appreciable weakening of the economy. Everyone wants the excessiveness of the past four years to continue indefinitely, and if it doesn’t continue at that frenzied pace, they yell recession. Last thing we need is a rate cut which will reignite inflation. The Fed needs to hold tight for awhile (I’m for them going away actually). They should not be cutting with inflation still above their target, especially services.

Agreed. Economy is doing just fine. Current Atlanta GDP Now estimate for Q3 is 2.1% and we’re approaching the holiday spending season. This time in 2025 will be the most telling on where we stand but as of right now, everything is just par for keeping things steady with no cuts.

Another anecdote: post Labor day commuter traffic in Boston is even worse than in prior years. I’ve been doing this commute since 2021.

The local commuter transit lot I drive by was completly full by 10am yesterday & today, including the overflow on-street parking. I you drove there to catch a train you would not have been able to park.

ShortTLT,

Anecdotally, I, personally, never had to worry about parking at the local train station.

I could either take a local bus or my wife would drive me to the station.

Anon,

That works if you’re already in the city (or suburbs with public transit).

This particular parking lot is at the northern teminus of a subway line, ergo a lot of folks commuting in from outside the reach of trains will park there to minimize how much driving into the city they need to do.

I made the comment because I’ve been driving by this parking lot for the last 3+ years to get to my day job. Although it was occasionally full by late morning/early afternoon in years past, this is the first time I’ve seen this level of demand at the facility.

No recession anywhere in sight here.

Verizon is buying Frontier for $20 billion in a proposed merger which will be concluded in 18 months.

I need to look up what Frontier does.

7 years ago, they managed my 80 year old mother’s wired landline. That seemed to be a dying business.

I guess Verizon doesn’t have enough wires. The copper must be worth a fortune.