“A sales recovery did not occur in midsummer”: NAR. Because prices are way too high, doesn’t take a genius to figure that out.

By Wolf Richter for WOLF STREET.

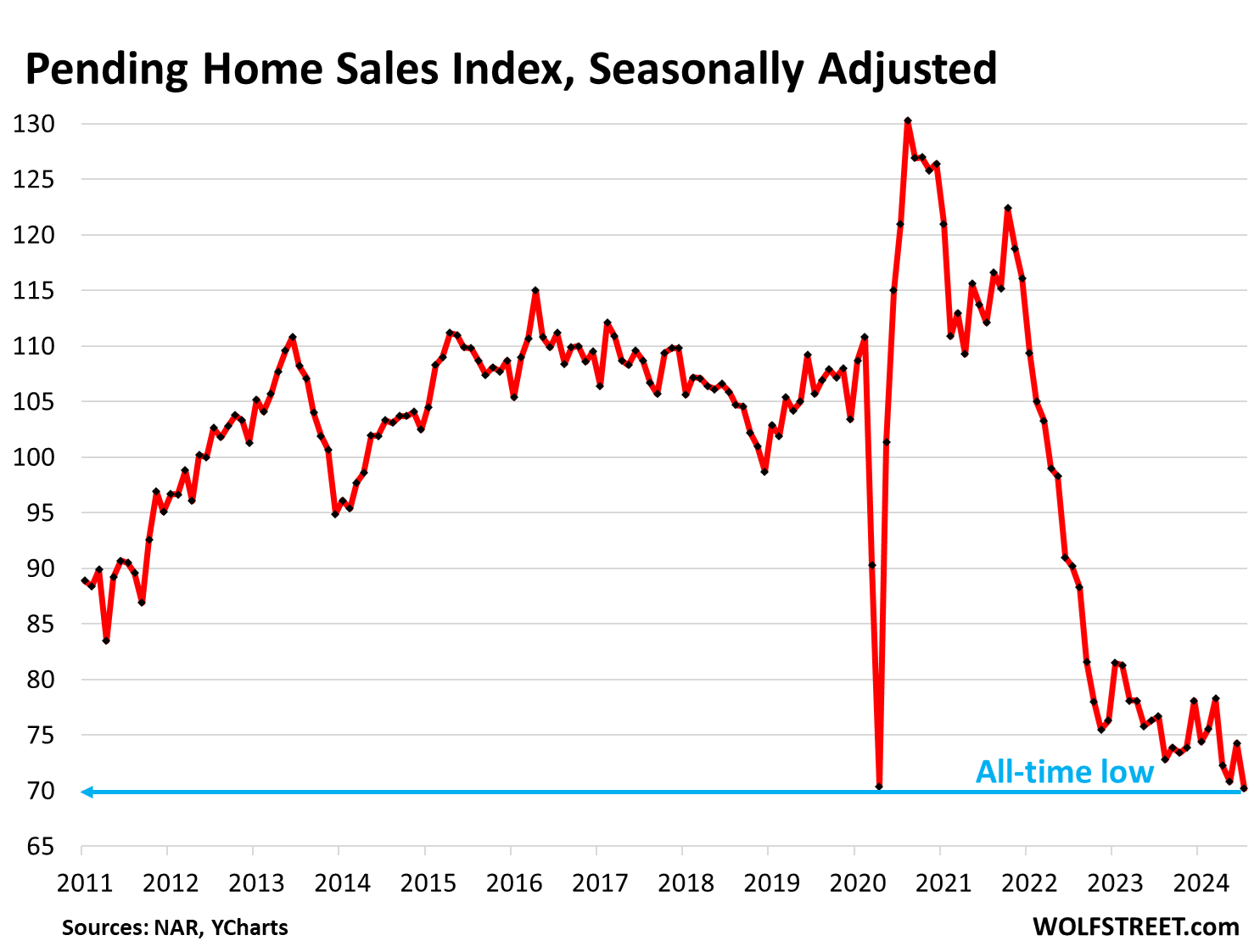

Pending home sales – a forward-looking indicator of “closed sales” over the next couple of months – dropped by 5.5% in July from June, and by 8.5% from a year ago, to an index value of 70.2 (seasonally adjusted), the lowest in the history of the index going back to 2001, when the index value was set at 100, according to the National Association of Realtors today (historic data in the chart via YCharts).

Pending sales are based on contract signings and track deals that haven’t closed yet and could still fall apart or get canceled.

So compared to the Julys in prior years:

- July 2023: -8.5%

- July 2022: -22%

- July 2021: -37%

- July 2020: -42%

- July 2019: -34%.

What NAR said about this situation:

Predictions of rising sales during the summer amid much lower mortgage rates turned into the opposite:

- “A sales recovery did not occur in midsummer.”

Prices are way too high, plus wait-and-see:

- “The positive impact of job growth and higher inventory could not overcome

- “affordability challenges

- “and some degree of wait-and-see related to the upcoming U.S. presidential election.”

Lower mortgage rates will drive up sales, the same thing NAR has said for months, the opposite of which has been happening:

- “Current lower, falling mortgage rages will no doubt bring buyers into the market.”

Mortgage rates have already priced in massive rate cuts.

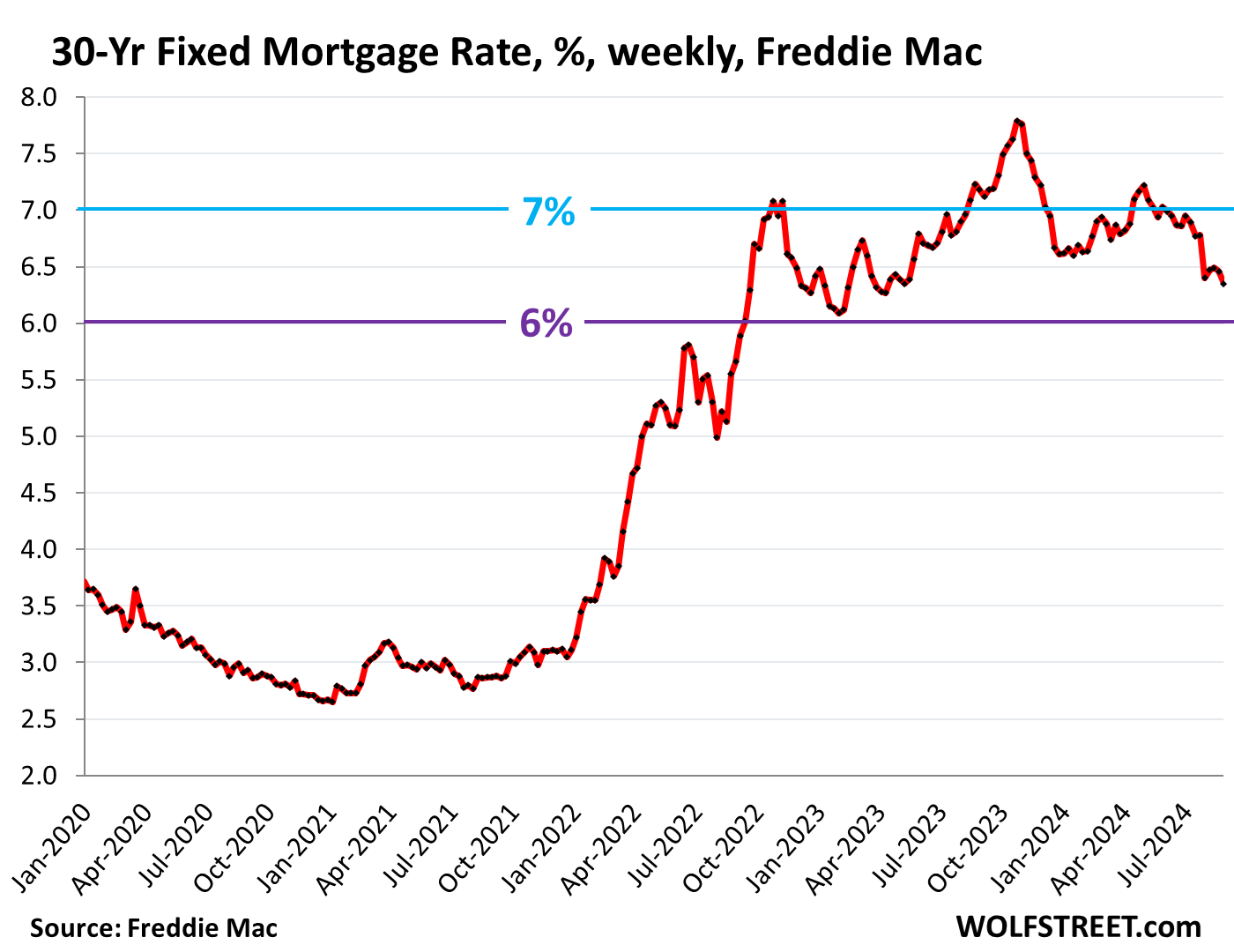

The average 30-year fixed mortgage rate dropped to 6.35% in the latest reporting week, according to Freddie Mac today. This rate is nearly 1.5 percentage points lower than it was in October 2023.

Mortgage rates, which roughly parallel the 10-year Treasury yield but at higher levels, have already priced in a long series of rate cuts. They’re now just 88 basis points above the one-month T-bill yield (5.47%).

Even if the Fed cuts a bunch of times, mortgage rates might not move much further since those cuts are already fully priced in. And if the Fed doesn’t cut that many times, or more slowly, then, well, we’ll see.

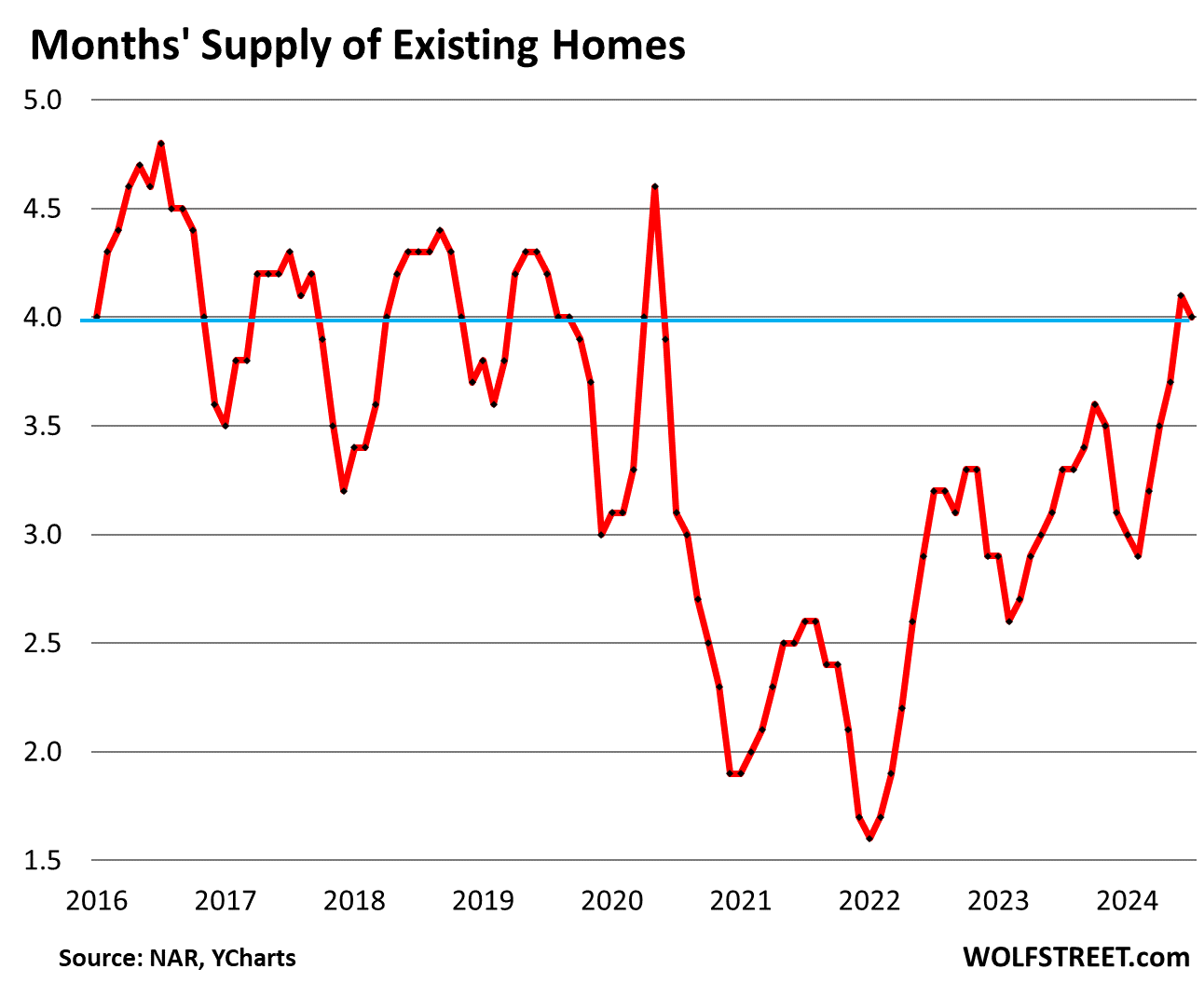

While supply is piling up.

This sustained plunge in demand despite much lower mortgage rates is occurring even as supply in June and July jumped to around 4 months, both the highest since May 2020, according to NAR last week:

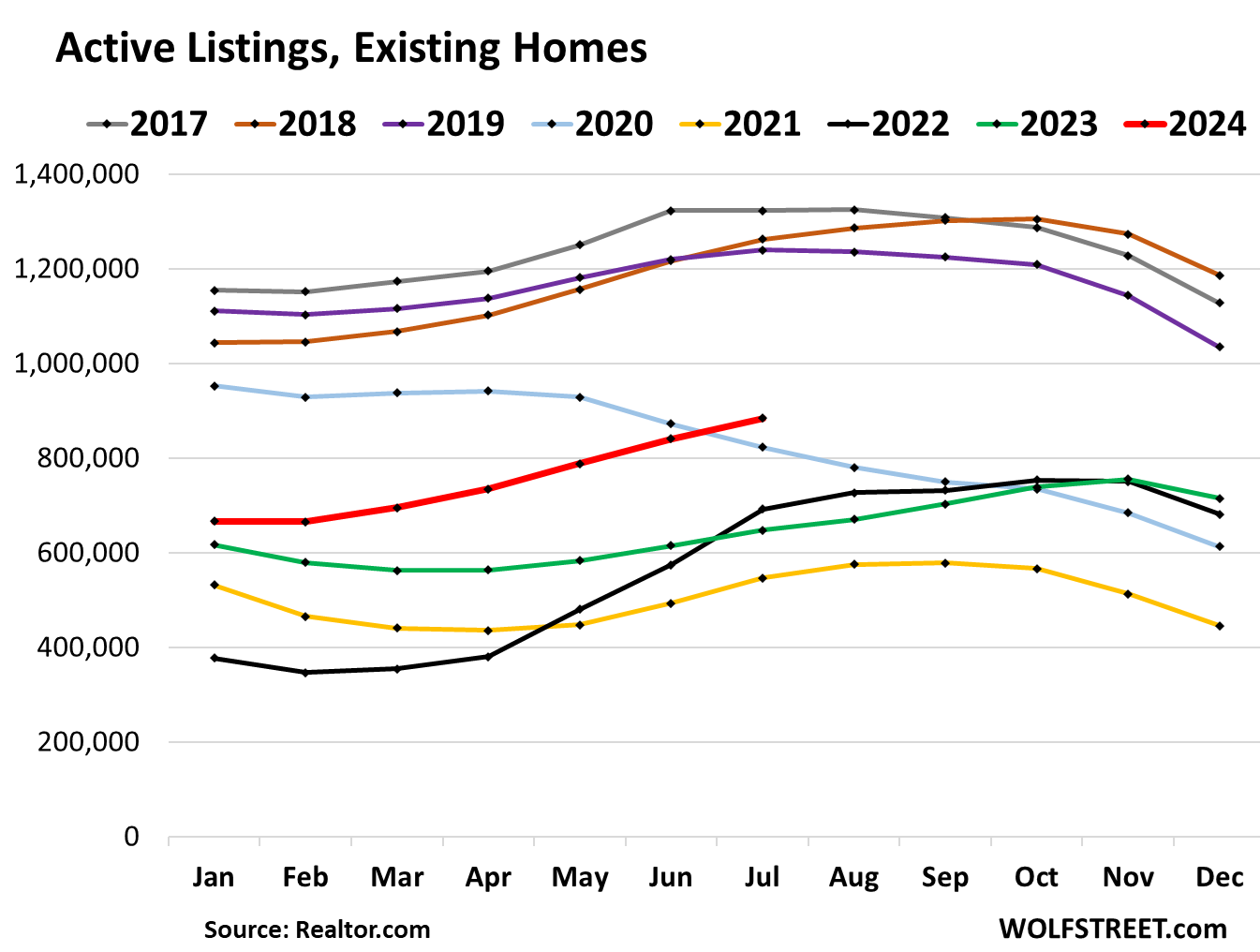

And active listings in July jumped by 36.6% year-over-year to the highest since May 2020, according to data from Realtor.com.

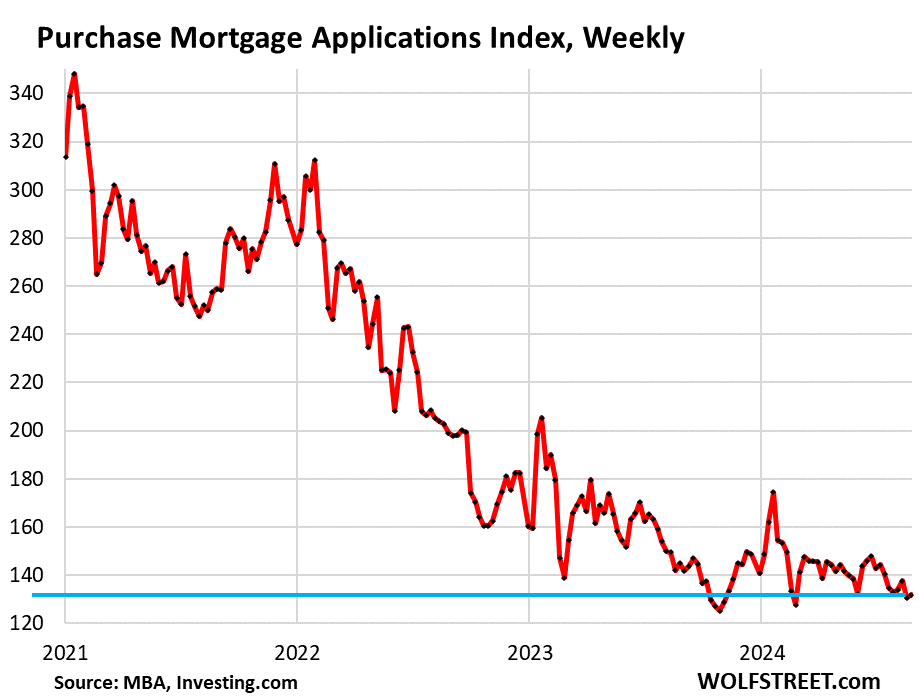

And in August, the Buyers’ Strike Continued.

Applications for mortgages to purchase a home in August have dropped back to the near record lows in November 2023, when they’d dropped to the lowest levels in the data going back to 1995, according to the latest weekly data from the Mortgage Bankers Association.

Mortgage applications are an early indication of pending home sales for August (to be released a month from now), and closed sales further down the road. And those indicators are still going to heck despite much lower mortgage rates and surging supply — because prices are way too high, doesn’t take a genius to figure that out:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

what really will be the kicker here is whether the 30 year mortgage rate drops when the fed funds rate is cut, or whether that has already been priced in. if rates bottom at 6%, i see prices tanking.

gap’s great earnings report and dollar general’s awful one shows that we have a tale of two economies now. one for asset holders and one for everyone else.

“we have a tale of two economies now. one for asset holders and one for everyone else.”

You’re basing a generic comment about the economy on your silly interpretation two specific retailers, which always leads to hilarious results.

Gap isn’t for “asset holders” 🤣 Rolexes are. Rolex prices are falling, have fallen for the 9th quarter in a row, and supply is rising. Sales prices of used luxury watches have plunged. So that’s for asset holders.

Walmart, which isn’t for asset holders either, had a blow-out quarter.

you’re right, i shouldn’t have generalized. but that is a sense i get from talking to many groups of people, is that the percentage of people who feel the economy isn’t working for them is higher than it was in the past. as you’ve written, the bottom 10-20% has always felt that way. it seems higher today, but of course, it’s just anecdotal.

Same thing that happened to Subway and McDonalds. They increased their prices at a faster pace than slightly higher quality merchants so the people that go there just hopped to the next category. Dollar shoppers went to Walmart. McDonald’s consumers went to Cava. That the bottom quintile of earners have seen the highest wage gains doesn’t hurt that process any. See also Best Buy seeing increased sales.

Dollar General was a harbinger of wide spread poverty after 08. It’s collapse means what?

@Feanz G I don’t know how old you are but your experience “percentage of people who feel the economy isn’t working for them” will change depending on 1. The overall economy and 2. Who you hang out with. @Wolf when I was in High School I bought a used Rolex bubbleback for $250 and sold it in college (for $400) to buy a used Rolex Submariner for $800. One night in the 90’s I was at the “Good Guys” (a long gone Bay Area chain that sold TVs and Car Stereos) and all the sales guys were wearing fake quartz movement “Rolexes”. I sold the Submariner and replaced it with a Seamaster (and I have not owned a Rolex since then). As a guy that buys and sells watches I keep track of the Rolex world and I’m betting thaturchases in the last few years had WAY more “flippers” and “fake it till you make it” guys than “asset holders”…

I’ve always said that Rolex caters to the Dumb Percent. False scarcity is the only reason prices are high, not mechanical superiority. They make about a million watches a year, but according to their salesmen, if they are lucky enough to get one, they will hold it to the side, but “just for top customers, such as yourself”. That said, there will definitely be a wait.

+10000 on this. Real watch people that don’t need to flex and actually have money to appreciate haute horology tend to stay away from Rolex. They go for brands that general public don’t know like MB&F, De Bethune, H Moser, Grubel Forsey..etc. The price of some of these will blow their mind..

On the other end, if you’re douche and want to really flex, there’s always Richard Mille..

Rolexes are ugly baubles for the monied idiot. Find an old Sherpa skindivers watch. Not prohibitively expensive, reliable and miles more handsome.

Lol, watch people. I have a casio g shock that has been in three different oceans, 12k feet on a mountain, in -50 weather, left in a car in the summertime, been knocked around and beaten for over a decade.

Never even so much as a battery. 100 bucks. It isnt some gigantic baseball hanging off my arm like most luxury watches and it tells me the altitude, temp, moon cycle, and time.

To quote the internet denizens, why havent you taken the casio pill yet wolf street commentators? Sure beats dropping 30k dollars on some hublot that youre afraid of showering with.

Wolf, you keep saying “Prices are too high.” What should home prices be? 10% lower? 20% lower? Where? East coast? West coast? Mid-west? It seems to me that, without distortions, a free market will set the price. Isn’t that what we have now? Sure, things might change if interest rates go up or down, but if interest rates go down that will make house more affordable and that will drive either price stability or price appreciation. Baring a recession or some other shock to the job market.

What do you think?

People mostly say “prices are too high” when they happened to first care a lot about the price of something. That anchors it in their mind forever, regardless of the years of inflation, demographics changes, and supply/demand gurstions that occur in subsequent years and decades.

Ya, ya, we get it … the trolley was a nickel, steak was 4 bits, and you could buy a house from the sears catalogue for $2000 back when wearing a turnip on your belt was the fashion.

I use a regression line to determine what I (imho) believe to be a fair price for a home/property – basically take the increase seen before covid, ignore the bubble and calc what the price would be if the price increase remained linear.

Other factors I use are: when the property last sold and at what price. If the seller expects to get double what they payed for the property and has held it for less than 10 years, I will not consider making an offer (because it would be look on as a low-ball). If the seller bought the property in 2022 or 2023, I pretty much dismiss those too (the seller likely paid too much and is looking at a painful loss.

Just what I do, does not imply success

It begs the question, is Walmart eating Dollar General’s lunch? What’a happening to them? Has inflation just eroded their margins so much? DG talks about a struggling lower end consumer – are they just going to Walmart now for their $5 product offerngs and 7,000 price rolled back items?

Cracker Barrel has several different $5 meals to take home.

Reality check local Hawaii grass feed beef hamburger and pot roast are $6/ pound and steaks $15/ pound.

We do all our shopping at Amish market Easton, MD or Farmers markets on Big Island Hawaii. Use cash to buy $100 of meat in Hawaii and vendor gives 10% off. Make Cash Great Again.

That sounds about right. I lived for 20 years in Waikoloa; still have family out there and go back all the time. It’s flabbergasting to me though how Hawaii, in the middle of the Pacific Ocean can get the price of gasoline cheaper than California. Shoots brah. Aloha.

The fashion influencers I follow, who mostly push luxury items, are all featuring Walmart fashions in their videos. Some of the influencers are designing fashion lines for Walmart as well. These influencers have the clout to push merchandise and I think that is what is bringing higher earning customers to Walmart.

(wish I got this in earlier)

No, DG is in trouble because their prices are outrageous – to feed the EBT (food stamp) crowd. Has anyone here ever been inside one? I visited once and that was it. Walmart/Winco are committed to low prices and generally can’t be beat. Another reason I think Walmart is doing so well is due to their “Online order pick up”. Now higher end consumers can hide outside the store in their Range Rovers and Mercedes’, with “No touch” (held over from Covid) anonymous service. I see it all the time.

I live in the sticks of Appalachia. Sometimes DG stores aren’t even open because they have no workers. When they are open, unpacked boxes sit around. It’s a depressing experience. It makes Walmart seem upscale. Then there are the prices, awful.

I saw the Dollar General drop and bought some of the stock because I personally like the store and think it offers value and convenience, unlike other store retailers like Kohls, Target, Walgreens, etc. that don’t seem to have a viable offering.

People will argue on Target. I’m not sure why it is doing well. The clothing is very low quality and the grocery selection and pricing is unattractive. I don’t like it.

>>People will argue on Target. I’m not sure why it is doing well

Same here, Bobber. I honestly tried to look at it at different angles, but absolutely don’t see any appeal in shopping at Target in-store.

Sadly for me, it is opening a huge new store in my town, less than 5 miles from their other store, and many locals seem ecstatic about it on social media. I just shrug my shoulders. I say “sadly” as I would much rather prefer some good major east coast grocery chain like Wegman’s come to my town, but it doesn’t seem to be happening.

You are not the target market for Target. Go to the store and look who is there. Now go to Walmart. They serve completely different demographics. “Target” people don’t want to be caught dead in Walmart. Namely, 15-45 YO attractive females. This is why target has one small isle of tools and Walmart has isle upon isle.

Target has a moat with that demographic. The question is, is that demographic large enough to sustain Target’s margins? Time will tell.

Nemi5150, man you just gave me hope that I won’t stay single forever! That’s where I’ll try to strike a conversation with ladies (especially attractive!) and maybe I’ll eventually get lucky!

I think I’ll start shopping Target and drink Frappucino Pumpkin Latter every morning, thanks!

You are not the target market for Target’s target market either.

I personally am not targeting Target’s target market. Way too wholesome and mindful. She’ll drain my bank account and I’d end up with Live Laugh Love pillows all over the house.

We don’t have any Walmarts on the SF Peninsula, but I’ll often go into a Walmart when I am outside the Bay Area (since they are often next door to a Home Depot) to get something. As Nemi5150 says “attractive females” don’t shop at Walmart (and 99% of the females over 14 in Walmart typically weigh more than me a 6’2″ athletic guy, and I’ll almost always see at least a couple women that weigh more than twice as much as me)…

Nemi5150, as I read through the comments, yours was the first one that I thought to myself, yeah, this guy gets it. My daughter is 39, a former actress and model. We spend a lot of time in Target.

Yep, here in washington, Target is filled to the absolute brim with 20-something flat belly white girls wearing expensive clothes and trendy makeup/hair.

Walmart is a bunch of methed out zombies and old people arguing with the on staff off duty cops that are there 24/7.

We dont have dollar general here but in places that ive lived that did have them, the DG is the welfare shack. Single mothers with 5 kids, meth heads, and trailer trash or hood rats. Had a guy pull a knife on me at a DG once in some tiny backwoods hole years ago. I refuse to shop at them.

Im almost to that point with walmart. Too risky to go there during busy daylight hours. Tempers are red hot with people that have nothing to lose or are mentally unstable. Maybe a few local dollar generals would clean up the walmart?

Anecdotally, I think The People of Walmart are starting to shop at Target. Not sure if Target is going downhill or if the general populace is just getting fatter and more tattooed, but Target in my town ain’t what it used to be.

…ah, yes. My stepdaughters and their friends have referred to it (tongue-not-so-in-cheek) as ‘Tar-zhay’ for some years, now. Trucker, if you were around NE WA back in the ’90’s, you’ll recall the advent of Wally-World in Metaline Falls taking out most of its Main Street small businesses (Willows in NorCal, and doubtless other locations a similar story). Modern, corporatized/financialized life rolls on…

may we all find a better day.

Target is carrying makeup brands that are more upscale than before. I noticed that a couple of weeks ago when I breezed through the store, which I rarely go into.

I agree with you on Target somewhat; it has a lot of competition; people seem split on the Target brand vs. some of the other things. I am curious about DG but I am a shareholder of target from the low 100’s. I can tell you with Target it wasn’t so much about the grocery and other offerings there (Walmart has them beat there) but their margins were suffering because of theft and the covid over-inventory that many retailers went through. So the play on Target was that they were going to be able to get some margin recovery that filtered down to the bottom line eps growth.

Target is closer for me so I do shop there vs. Walmart. Go to the dollar store all the time for little arts/crafts that are great for the kids.

Dollar General overbuilt. There is one on every corner where I live in TN. No one works there. Boxes just stacked in the isles. Junk convenient stores only for a quick single purchase. I have been to their stores twice since living here. Once to buy some jerky on the way to an Army field exercise and once when the restaurant I was at ran out of sweet tea and DG was next door…

Basically a play of the Chinese Yuan.

“one for asset holders and one for everyone else.”

Hmm…*leveraged* “asset” holders (thankfully you didn’t say *owners*).

Borrowers using leverage (sometimes absurd amounts of leverage) to buy (overpriced) assets frequently don’t appreciate that they are first off the gang plank when a) interest rates rise and/or b) the economy blows up (for not entirely unrelated reasons).

But *lenders* have been staging these goat rodeos for a long, long (loonnng) time – their lending is almost always tied to loan *terms* that guarantee the leveraged borrowers are first against the wall when the revolution comes – those borrowers are going to lose *all* their “gains”/equity/collateral before the lenders lose a dime.

And the lenders end up with the asset.

An excellent example of leveraged newbies getting annihilated (with massive, er, collateral damage for renters) is the Applesway syndicated apartment loan fiascoes in Houston.

The incredibly stupid leverage games that 20 years of Fed-birthed ZIRP empowered are essentially infinite.

Driving borrowing costs to near zero created an entire universe of every mal-investment imaginable – far beyond any hope of “regulation”.

And that is the seam-popping, pressurized environment we exist in today.

Am I crazy or did the RE market in the US just hit a new ATH?

Houses are sitting and sitting. Price cut after price cut. Historic low home sales but a new ATH in price? Welcome to insanity.

Very well said. We are living in the

Real Estate Twilight Zone, where the laws of gravity and economics do NOT apply. I saw a little home In Colorado on zill ow…actually, it’s a glorified outhouse…was listed for $425K, price is now at $285K, after SEVEN price reductions. I’ve heard that referred to previously as chasing the market downward. Greed on steroids. Anyway, I believe we are being fed horse dung on the housing market. I believe the housing market is on life support in the ICU. Death may be near. It may become difficult to give homes away.

The straw that will likely break the camel’s back is when the large investment firms become desperate to offload their inventory to mitigate losses from buying during the peak. They have been trying to very slowly unwind their position this year, but if they can’t sell them it will get ugly.

https://www.zillow.com/homedetails/350-Francis-St-Longmont-CO-80501/13203068_zpid/

Not sure about what earning reports mean, but I fully agree with the tale of two economies. Fed’s reckless money printing and govt’s irresponsible spending caused the asset holders thrive and savers suffer since 2020.

There are haves and have-nots? I now understand that this time is truly different.

Well depending on how things pan out, many of us if we have to sell are about to add on an extra $25,000 to the listing price and in California, an extra $150,000 for first time home buyers. I’m gonna call it a “processing fee.” LOL

You forgot to add the leverage. These are not cash buyers. That is a downpayment for a loan. It’s going to push the price up multiples of $25,000. The overwhelming majority of people don’t understand money, and buy payments, not prices.

Meanwhile, actual condo prices in Oakland are down about 20% from peak already…

According to pew research, 68% of the new immigrants are Christians, also 68% of Americans identify as Christians.

So….what does that have to do with the price of a house or this 25 grand discount? Probably nothing, I was just thinking about it.

I read that about 15% of homes under contract were cancelled in June. Maybe they are hoping for lower rates? I wonder if this trend will continue.

Could potential buyers be seeing a Harris administration and with it, a $25,000 subsidy for new home buyers? And why stop there?

We’d be watching the housing market collapse entirely while buyers are waiting for this miracle.

Lots of concellations too. Oh but the government says consumer confidence is up. What a laugh. They will say anything to get their candidate elected.

“Oh but the government says consumer confidence is up. What a laugh. They will say anything to get their candidate elected.”

Ignorant BS. That was a private sector survey by the “Conference Board” a private-sector nonprofit thinktank funded by its member businesses.

I get really really tired of this stupid political bullshit people drag into here. Do that on X. That’s what X is for.

“Even if the Fed cuts a bunch of times, mortgage rates might not move much further since those cuts are already fully priced in. And if the Fed doesn’t cut that many times, or more slowly, then, well, we’ll see”

This might be true but going back to your previous article about Treasury buying back notes/bonds and suppressing LT yield, if it continues and the 10-year yield is down again, you think mortgage rates will go even lower? I fear that at least in SoCal, a million dollar is less of a concern if somehow the folks can squeeze into that monthly mortgage and 30yr at less than 6, maybe it will bring back some demand in certain insane markets like SoCal

Either way, it’s quite depressing to see flipper special in not so special neighborhood in Long beach asking $1.6M for a 1600 sqft home, and looking at the price history it was bought for $1.3M just 2 years ago, guess people are expecting Nvidia style return on everything…

PI, you do realize that those prices are insane… I just cannot believe that those home prices can be sustained.

Yeah it’s pure insanity. So far even with volume down, there’s still people buying at these prices. Either there are still quite a few who have more money than brain cells and not bark at prices vs what you get or these folks are the smartest and they still think they are getting in at the right time and in a year or two they can refinance at lower rates plus seeing their house head to $2M….

Either case, this level is absurdity would be really funny if it didn’t F over many other people who just want a damn place to live and can call your own without love leveraging to no end..

“So far even with volume down, there’s still people buying at these prices”

True, but volumes *are* down by about 33% over 29 months of unZIRP – and volume declines are the predicate for price declines.

And, as Wolf points out, normality is slowly (oh so slowly) returning in terms of “for sale” inventory.

That said, you,me, and almost certainly the Fed are shocked by how slowly home/stock prices have declined in the face of unZIRP.

In a better world, it would chasten DC/the Fed but it won’t.

In the end, the currency/economy will be damaged over and over again if it means that DC’s agenda-of-the-moment takes priority and needs to be funded.

In other words, DC has mutated an “economy” with a bias towards itself and auto-destruct (it can’t survive for long without ZIRP).

Northern, TN real life example: Bought a 960 sq ft home in 2018 for 70K and renovated it for another 5k. 3 tiny bedrooms, single bath, no garage, and gravel driveway. Located one street over from low income section 8 housing. Literally one of the 3 worst areas in the city. Now worth $220k and the area is being gentrified as it is the most affordable in town. Nearly quarter million gets you a happy meal shitbox in an area you would not want to live and a school district you would never allow your children to visit. Rent has gone from $795 to $1300 in same time period. Absolutely insane….but here we are.

Astute buyers as the bottom is in.

As wolfs “most splendid housing bubble” charts show home price don’t seem to be budging much, if at all. The citizen has money the citizen has a job…life is good for the home selling citizen. If no one wants to pay for his crapola house then wait a month and raise the price. The “house rich” citizen has the luxury of being patient.

But wait….Wolfs new and improved ( up to date) housing charts are soon to arrive, possibly bringing hope to the hungry hopeful homeowner.

“The “house rich” citizen has the luxury of being patient.

Not infinitely so, not historically.

Even in this warped age, for sale inventories are rising.

This will eventually shake out to the downside, IMO. It’s generally easier to hold out as a buyer than it is as a seller.

However, beware once the damn breaks or starts to overflow and prices head south. There’s a thing called the “wealth effect” which we haven’t seen in action to the downside for many years.

If folks feel poorer, they spend less on EVERYTHING. If they spend less, we may finally get that recession everyone has been predicting for the last 5 years.

Sure feels like this damn breaks is becoming a mythical thing that will never come or finding the next Big foot

The government has been juicing the economy. The COVID stimulus took a few years to be spent and not all of it is spent. My state is still trying to spend some of the money allocated to it. Multiply that by 50.

Just as the COVID money is slowing down, Congress passed the 1.5 Trillion Inflation Reduction Act which will most likely cost over $2 billion. This money will take another year or two to be spent.

The question will be will there be any other big government spending programs next year and the year after to keep the economy purring along.

Without the IRA act. I wonder what the economy would look like right now?

…an interesting thought/auto-whatever thought question (the physical, downstream-disaster effects of a ‘dam break’ contrasted with a collapse (“…damn!”-break) of will in maintaining an individual’s price resistance/buyer’s strike of purchasing whatever…

may we all find a better day.

PI-

Are rents in that area that high that those prices can be supported by the market? That is just mind-boggling but then I don’t live in CA. I’ve always considered most things out there as insane. You would get 4 – 5000 square ft of river-front / lake-front mcmansions for that price where I live. Different worlds.

Rent is high but still cheaper compare to price of buying by a pretty wide margin. Just Google houses around Cal state Long Beach near 7th street and you’ll see what insanity I am referring to

Long Beach is the cheap city, BTW.

For those outside CA they can go to Zillow and see how crazy things are on the SF Peninsula. My wife recently mentioned a “nothing special” ~3,000sf home up the hill from us that is for sale for $5mm down the street from one of her friends). The Zillow rent estimate is ~$8K/month and the PITI (with a $1.25mm down payment) is ~$30K/month…

Looking at Zillow, you can still find plenty of homes in the Bay Area between 0.6M and 1M in Oakland. That is easily affordable for two high income earners. Not that I want to live in Oakland or anywhere near there. It isn’t cheap, but affordable for two high income earners.

Cali and major metros in Canada have a lot in common, rents are increasing fast but do not cover mortgage payments if you buy at current prices. The reason people do it anyway is because they hope 5-10+yrs down the line prices will be even higher and they retire on that , move to a cheaper area, or buy a Ferrari or something. Many years of watching prices explode to the upside has conditioned people to accept ever more risk, they feel RE is “safe” while offering huge leverage on their money. Many RE agents in Metro Van and Greater Toronto play the game and own multiple properties themselves, would be surprised if it was any different in California.

I’m not saying any of that is smart, just how people are behaving. I wish there was a way to measure overall leverage in an economy, I imagine the “everything bubble” as people call it is interconnected, people buying inflated assets by borrowing against other assets which themselves are inflated, one of them goes and their collateral is toast and then dominoes.. that’s my complete guess as an amateur, but so far it seems central banks are sticking the landing and I’m wrong 🤷🏻♂️

Rents are not increasing fast. In fact they have come down. And renting vs buying isn’t funny anymore. Buy and pay 12k in PITI or rent for 5k.

A little different in Canada. The newcomers somehow get a mortgage with at least few names on the deed and then 20 to 30 people live in each house. It’s the same thing they do in their country of origin. This puts a floor in the housing market and prevents prices from falling.

Pretty much the definition of a “Mexican standoff”. Either the sellers who have to sell drop the price or the buyers who have to buy pay more. Houses don’t change hands when neither of those is actually true. Like overpriced collector cars. “I really do need to sell it”. Ok sure, lower your price.

I do think inflation and population growth driven demand are going to cause housing prices to more or less level off for a while, maybe -5, -10% here and there but not the 40% nation wide drops some seem to hope for. We all know if it approaches even half of that the Fed buys MBS again and mortgages go to 2%.

Except only for a very small percentage is buying even an option because how far out prices are. What can’t happen won’t happen and it will take time for people to realize they’re throwing money away. It’s less of a “Mexican standoff” and more of waiting for sellers to buckle because houses have huge, and growing, carrying costs.

“population growth”

Except domestic population growth is flatlining…not least of which due to insane housing costs (can’t afford a house, can’t afford kids).

cas127,

“Except domestic population growth is flatlining”

You mean “natural population growth” (births minus deaths).

But total population growth, including from immigration, has shot up by over 6 million people in 2022 and 2023, according to the Congressional Budget Office.

I’d seen charts from FRED which show the number of housing units per household, and per person, are as high as they were during Housing Bubble I. However, I do wonder about if those numbers capture immigration, illegal especially, and how would the per capita housing situation look if immigration was taken into account.

I keep hearing about how the problem is lack of housing units. I’d thought it was really about the distribution of housing units, which is certainly a factor (i.e. a much larger number of entities who own two or more housing units) but perhaps per capita housing units are actually down IF immigration is undercounted in the FRED data. Be interesting to see some data.

I guess mass immigration is one way to keep housing elevated? Millions of immigrants who need a roof. Hard to see how that benefits citizens who dream of buying a house one day….

Wolf- a very minor statistical (and likely unanswerable, other than case-by-case) query-ignoring the dirt, is there any kind of average/median ‘mortality’ metric for different types/ages of structures in terms of affecting the overall size of real estate market supplies?

may we all find a better day.

Supply of existing homes doesn’t really seam to be “piling up”. Perhaps normalizing?

Well, it did pile up over the past two years, look at the chart! Whether the current supply — which has more than doubled since 2022! — is normal or abnormal or paranormal, or whatever, or normal compared to what, is a judgement that can be made looking at the chart.

and the inventory buildup is very regional, the South leading the pack

Inventory has doubled. In our street houses USED to sell like hot cakes. Nothing would sit. NOW we have one sitting since a looong time. Multiple price reductions. True story.

LOL, it just looked normal compared to the pretty blue line that I can’t seem to get out of my mind. Also noticed the supply slightly decreased recently. We’ll see I guess

In many of the states where there isn’t a lot of new home building, such as in the midwest, great lakes regions, northeast, new england…not only are the prices much higher than pre-pandemic. But the inventory on the market needs tens if not hundreds of thousands of repairs, upgrades, and ongoing maintenence. Lots of the housing stock is 50-70-150+ yrs old. That is IF you can find a contractor to do the work. Not sure first time homebuyers have the resources to do all this repair, even if they get in to the home in the first place. And the property taxes, insurance, utilities, etc… are all HIGH.

Costs of living are not cheap pretty much anywhere anymore.

Where I live, Mohave county Arizona (bullhead city) cost of living is very inexpensive….dirt cheap, low gas prices, low property taxes, nice houses close to the Colorado River, casinos, shows, music, events and many golf courses. For under 300.000. you can get a nice desert dwelling (brand new) with palm trees and a few lizards. Smaller towns have their own offerings. Zillow about and see what to your wondering eyes appears.

All True. But I have never met anyone who said, I really wanna live in Bullhead city one day.

The lack of demand from buyers seems logical based on current home unaffordability. I see demand continuing to drop as the economy cools off. The low supply is a huge anomoly at prices this high. I suspect it’s attributable to price momentum and greed on the part of sellers, and that rarely ends well in any market (stocks, bonds, or RE).

The problem is the Fed always seems to encourage asset price speculation by stimulating every time there is just a slim threat if deflation. The Fed’s policies of the past 20 years have been a huge anomoly as well, and that won’t end well either.

“The low supply is a huge anomoly at prices this high.”

The qualifying income needed to get a mortgage at current prices and interest rates is the resource bottleneck. In other words, not a large enough pool of potential buyers, no matter how bad people may want to buy. You are not going to build (or list) for something that has almost no potential buyers.

Is it fair to assume then, that the real reason behind what we’ve been seeing between 2020 and 2023 was pure FOMO, and nothing else?

I still see LOTS of people moving to our state, however it feels like nobody is running like crazy after new builds anymore, nobody lines up at 6am for every open house and nobody is engaging in multiple bidding wars with all contingencies waived. People seem to be totally fine with renting for a while and figuring things out later.

Higher inventory indeed seems to be a huge factor, but it definitely feels like everyone is way more relaxed now. I guess the overall buyers’ mood seems to be “it’s unlikely to become worse (rates, prices), so longer we wait – the better”

Don’t underestimate both the stupidity of the “average” person (ample supply) and the pull of social conformity (fomo demand), or you could reverse that and call one demand and the other supply. Bottom line: people are baboons in sheep’s clothing – have no concept of the difference between “price” and “value”.

IN – …always consider that the promoting of ‘FOMO’ is the major, if not the PRIME, directive of our advertising ‘industry’…

may we all find a better day.

…which, in turn, fuels, and seems to direct much of our news-reporting apparatus…

may we all find a better day.

When consensus is ‘I wish I hadn’t bought’ or ‘glad I didn’t buy’ – you’re beyond any lower rate dramatic fix. Larger factors than rates are in play.

And, NAR’s Yun is consistently worthless. TFS

So when do we start to see price drops?

Wolf didn’t quote Lawrence Yun. Not sure if I can believe an article with the NAR and not know what ol’ Lawrence thinks.

“It’s a great time to buy a house”- Lawrence Yun.

For example:

That’s a joke, right?

Definition of “home”: Random House Webster’s Unabridged Dictionary:

1. a house, apartment, or other shelter that is the usual residence of a person, family, or household.

2. the place in which one’s domestic affections are centered.

3. an institution for the homeless, sick, etc.: a nursing home.

4. the dwelling place or retreat of an animal.

5. the place or region where something is native or most common.

6. any place of residence or refuge: a heavenly home.

7. a person’s native place or own country.

8. (in games) the destination or goal.

9. a principal base of operations or activities: The new stadium will be the home of the local football team.

10. Baseball. See home plate.

11. Lacrosse. one of three attack positions nearest the opposing goal.

It kind looks like the market is showing the middle finger on this chart.

🤣 true

Haha good one. Is that an ominous for the seller or is the middle finger to future potential buyers?

As Wolf always says: the cure for high prices is high prices.

Or, as the old “Wargames” quote goes: “The only winning move is not to play.”

We’re in the same boat: our house is paid off, and while we’d like to move to a more exurban/rural (read: peaceful) setting, and technically, we could afford it, I flat out refuse to make the move at most of the prices I see right now (and this is the Great Lakes region, to boot!).

If the market stays irrational and we lose out, so be it – we’re not in a position where we *need* to move.

(applause!)

Same with us here in the saintly part of the TPA bay area.

Even the bare land I have been looking at in more rural areas north of here seems overpriced, and if one takes the time to research recent sales, grossly over price.

And with all the tax benefits of our cap and homestead and elderly, etc., selling out for even 3 times what we paid for does not really pencil out.

The challenge of course is to sell out at or near the top, wait a while and buy back in when prices decline, which they always have to some extent, over 50% last time…

”If wishes were horses, every beggar would ride.”

@hreardon,

Your house is paid off and you consider moving. If you decide to sell your house, aren’t you selling for the highest price you can possibly get? Rhetorical question.

Or are you planning to rent out your house and buy another one.

Exactly my thought.

“I refuse to buy a new house until prices drop a lot” sounds a lot like

“I refuse to sell my existing house until prices drop a lot”

MW: The dumb money poured into Nvidia ahead of its results. It could’ve gone worse.

NVDA -6.31%

That’s only Day 1. NVDA could pull an Intel-style plunge soon, you never know…

The owner sold 3/4 of his shares about 3 weeks before the earnings came out. I told everyone after he sold them.

The US Golden Age in Capitalism was propagated by 2/3 velocity, i.e., by putting savings back to work (George Bailey’s It’s a Wonderful Life). Today’s economy is propagated by primarily new money (the money supply hit all-time highs during Nov. 2020). Thus, housing prices have appreciated >50 percent during C-19. Inflation is the most destructive force that capitalism encounters.

It will take long-term monetary stringency to turn the economy around.

Home affordability is all that matters. I’m personally no longer looking to “move up” out of my starter home of 20 years, since the current predicament is terribly out of favor for anyone trying to buy a larger/newer home. While I was close to taking the plunge a few years ago, I’m just going to pay off what I’ve got and “age in place” as we all know, you never chase. 😌

My in-laws dreamed of moving up for a long time. They have given up on that dream. They have lived in their starter home since too many decades. It’s paid off now and they don’t want to start over with a mortgage. Interest rates and sky high prices prevent them from moving. Yeah, they could move to a low(er) cost state and be far away from their kids and grandchildren. Not what they had in mind for their life’s as retirees. Sad story but at least they have a paid off house (old shack with many issues and repair needs).

That is pretty common actually. Historically just over one-third of homeowners nationwide own their homes free and clear. By necessity that will be either rich people who can pay cash for their mansions… or poor people who can pay peanuts for their shacks… and it skews towards poor people.

That is why the two states with the highest percentage of mortgage-free homeowners are West Virginia and Mississippi with over 50% having no mortgage. The next state down the list is Louisiana with 35%.

https://www.fastcompany.com/91139348/housing-market-economy-supported-by-record-number-mortgage-free-homeowners

Howdy Prisoners. Told Ya a long time ago they ZIRPed folks to stupidity.

So, have the Lone Wolf charts shown their final housing peak??? Are we finally hissing our way back down??? What great give aways are coming after Nov??? Taxpayer Cash for clunkers, or cash for buying a house??? How about anyone that buys a house gets a check too???? You just have to live long enough to be amazed again and again.

Let’s get those graphs to the level they would have been at for Salt Lake City in the movie: “Damnation Alley.”

Condos are doing very well all of a sudden here in the Swamp. It may be because that’s the only form of housing first time buyers can afford.

I keep hearing from a realtor friend, now is the time to buy. Get in now because things are going to skyrocket again next spring with the rate cuts….

Live in Denver Metro suburb, inventory is up, houses are sitting, lots of houses selling for at or just under asking. There’s some price cuts but not really drops they were just overpriced even for the current market. No real price depreciation yet though. Also from what I hear airbnb’s are struggling a bit.

But hard to know if she’s right? Will people continue to sit on the side lines for the foreseeable future? I got quoted a rate below 6% on a 30yr mortgage from my lender this afternoon and rates haven’t even been cute yet.

I see inventory increases coming from the following:

1) investor airbnb properties that aren’t making as much money as 2021 with a die down in covid yolo travel and a potentially slowing economy

2) people who chose to rent out or airbnb their home when they moved instead of sell in hopes of further gains. They have to live in their house 2 of the last 5 tax years in order to get the capital gains exclusion. A lot of people will be coming up on the end of that window and will need to decide if they want to be long term landlords and give up their capital gains exclusions

3) return to pre-covid living patterns: return to office/hybrid work, younger people choosing to have roommates vs live alone (to avoid covid), out migration from covid hot spots to more affordable areas

Will enough buyers come off the sidelines with rates at 6% or lower to absorb the supply or will we possibly finally start seeing some significant price decline outside of the few places like Austin and San Francisco?

The Fed cutting doesn’t impact mortgage rates

Mortgage rates are closely correlated to the 10y bond yields. However, the FED and monetary policy have an impact. The bond market is pricing in rate cuts and mortgage rates subsequently came down a little bit. In other words, it’s unlikely to see multiple rate cuts in the FFS and no change to treasury yields and mortgage rates. The expectation is lower mortgage rates. What will actually happen is anyone’s guess.

Disagree, if the Fed cut rates to zero today I’d imagine yields would actually go up.

The markets prices rates.

The Fed throws darts

You expect higher inflation?

If investors believe inflation will rise despite the Fed cutting rates, they may demand higher yields on long-term bonds, which can push mortgage rates up. Happened in the late 1970s & early 1980s. During this period, the Fed reduced the FFS to combat a recession, but mortgage rates remained high or even increased due to persistent inflation concerns and economic instability.

If the growth rate of inflation is decreasing I don’t see how mortgage rates can remain elevated if the FFS is being reduced.

Fed rate cuts often signal economic concerns, prompting investors to seek safer assets like bonds, which drives bond prices up and yields down, further reducing mortgage rates. If the market expects the Fed to continue cutting rates, mortgage rates might drop in anticipation. You already see this happening rn.

haha even though that’s a “friend” would you expect RE agent to tell you any different? Unless they truly don’t drink the Kool-Aid and have your best interest at heart, otherwise that friend probably wants to be your agent and get some sweet commission.

There are also a lot of them who are also truly into this gospel and latch onto everything Barbara Corcoran said as “advice” so go figure

In central California, Nipomo, a master planned 1,370 residential community is nearing final approval with 30 percent designated for very low, low, and moderate-income affordability as part of the state’s Regional Housing Needs Allocation. We’ll see how it goes.

Those are NEW houses sold by builders. That’s a different product. And you made my point that I addressed in the article linked below.

Here we’re talking about pending sales of existing homes sold by homeowners.

The link below shows the data for NEW houses sold by builders. They cut prices, bought down mortgage rates, and piled on incentives, and they’re selling, unlike homeowners sitting on their overpriced homes:

https://wolfstreet.com/2024/08/23/inventory-of-new-completed-houses-surges-to-highest-since-2009-triple-from-2-years-ago-exactly-whats-needed-to-bring-down-prices-across-the-housing-market/

Yes, I agree my post would have made more sense under your new house article on August 23, 2024. But this project was not approved until August 28. 2024, by the Community Services District Board, a key step in the ultimate approval process. Nevertheless, it is an interesting data point demonstrating the effort by California legislators to provide more houses. It will probably be years before a house is actually sold on this project in the best case scenario, but with existing homes in California selling for over $600,000, an even more extreme amount than the $400,000+ national price of existing homes, the California housing market is a more out of balance situation than your article described nationally. According to Redfin, 82.4% of homeowners with a mortgage have a mortgage rate below 5% and 62% have a rate below 4% so this situation is going to take many years to play out. Thanks for all you do.

Dollar General : what used to be $1 is now $3. Higher prices shrinking sizes.

In Manhattan the price of renovating an apt is $400/sqft. 600 for a townhouse. Add the land. Add the building. Add all the fees. Add the headaches, the scams…… Far chaper to rent these days. If you qualify .

For ApartmentInvestor way up thread:

Walmart

600 Showers Dr.

Mountain View CA

Just off Camino near San Antonio.

3 miles from Google

Pretty much the center of the SF Peninsula

Why do people keep saying housing is expensive?

Put the current cost of a home in an inflation calculator, check to see what that value was in say 2000. Compare the price.

I see no change in the suburbs of Chicago. I was waiting for too long to purchase a home, believing the hype. Started to read here for a differing opinion, Wolf lays it bare, changed my views over the last 6 months, sometimes begrudgingly on my part.

Houses are not the issue, they are keeping up with inflation. Granted the inflation is higher than comfortable.

Paychecks/annual earning are the issue I currently see (until Wolf corrects this viewpoint), they are not keeping up for the non asset class.

I was exploring this inflation using candy bar costs to my children. They were .40 when I was young, it’s now 2.29 for the same looking bar (size/shape). So, should I wait for candy bar prices to fall before getting another Skor bar?

Not a lot of people complain about house prices in the CITY of Chicago. They complain about property taxes there.

Even vast metropolitan area of Chicago belongs to the metros where housing didn’t shoot up until 2020. But then it shot up by 50% in a few years.

In the CITY of Chicago, it’s different. Condos for example have been about flat for years, and are flat with 2006.

So there are areas in the Chicago metro, but outside the City, where home prices shot up a lot.

Here is the house price index for the metropolitan area of Chicago, and it doesn’t qualify anywhere near for inclusion into my list of housing bubbles, but it did have a HUGE run since 2020.

https://wolfstreet.com/2024/08/27/the-most-splendid-housing-bubbles-in-america-aug-2024-update-prices-decelerate-below-2022-peak-san-francisco-phoenix-seattle-portland-denver-dallas-las-vegas/

Because it is? You can torture just about any stats or datasets until they confess. Some things are just readily perceptible.

You shouldn’t eat candy bars, period.

Thank you for properly discussing mortgage rates in context to the Fed rate discussions. Truly, encouraging that someone cares to get the details correct.

With regard to the path future mortgage rates, it seems that is now highly economic data dependent. Should unemployment spike, or GDP come in flat /negative, that may significantly impact the rate curve. Lets suppose the 10yr treasury fell 1% further. One might extrapolate that mortgage rates should fall 1:1, so we might see mortgage rates around 5.25%. Except, we can’t forget there is also a credit risk spread above the 10yr treasury for mortgage rates. So it is possible during recessionary fears, the spreads could widen, perhaps we only see 5.5-5.75% mortgage rates under such a scenario.

Or perhaps a different scenario, no recession materializes and strong economic growth continues, and the 10yr treasury rises 1%, Fed stops cutting short term rates early, but mortgage rate spreads over the 10yr might tighten as creditors no longer fear a spike in unemployment. So perhaps mortgage rates only move up to 6.75-7% in this scenario.

I just wanted to point out the complexity of the rates issue, and why we can’t assume anything going forward until we have more economic data confirming or denying recession fears.

Wow! That first chart is just brutal. It is obvious why the 2020 numbers tanked (COVID) but for willing buyers and sellers to not be able to get deals done right now is incredible.