Sales of new houses jumped, fueled by lower prices, big incentives, and mortgage-rate buydowns. Homebuilders are taking share from homeowners.

By Wolf Richter for WOLF STREET.

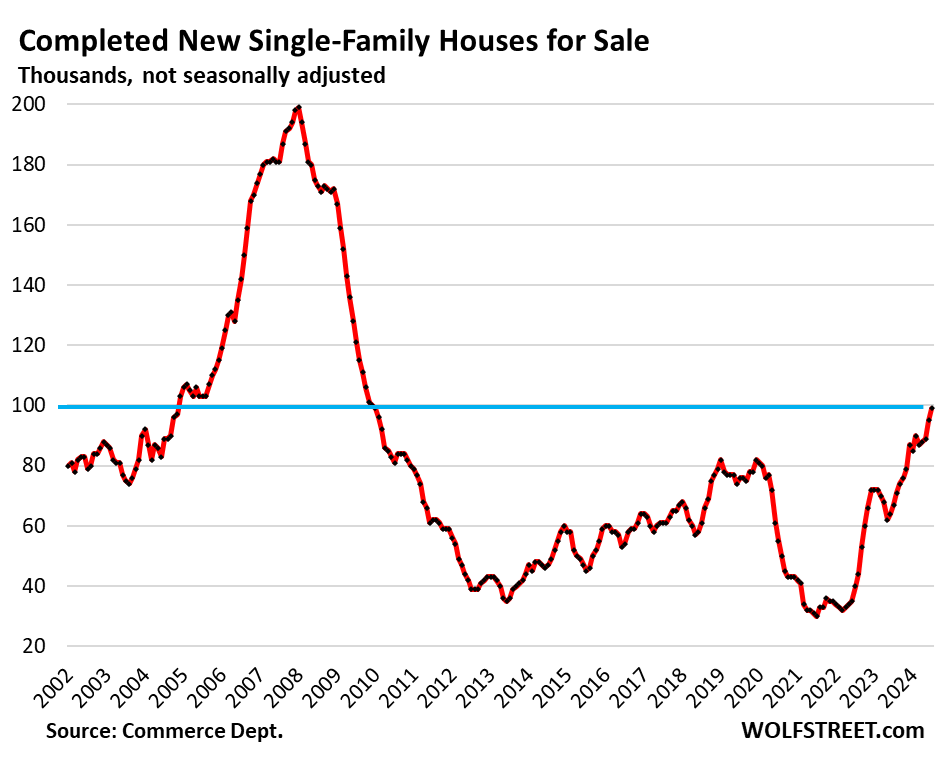

Inventory of new completed houses jumped to 99,000 houses in July, the highest since 2009, and about triple the inventory during the price-spike era of March 2021 through June 2022, according to Census Bureau data today.

Sales of completed houses jumped by 27% year-over-year to 28,000 houses. At this brisk rate of sales, the unsold inventory of completed houses translates into a healthy 3.5 months of supply.

These speculative houses are essentially move-in ready, they have to be sold quickly, builders have tied up lots of capital in them, and that inventory is encouraging builders to throw more incentives and mortgage-rate buydowns into the mix. This buildup of spec houses is exactly what the entire housing market needs the most to tamp down on prices.

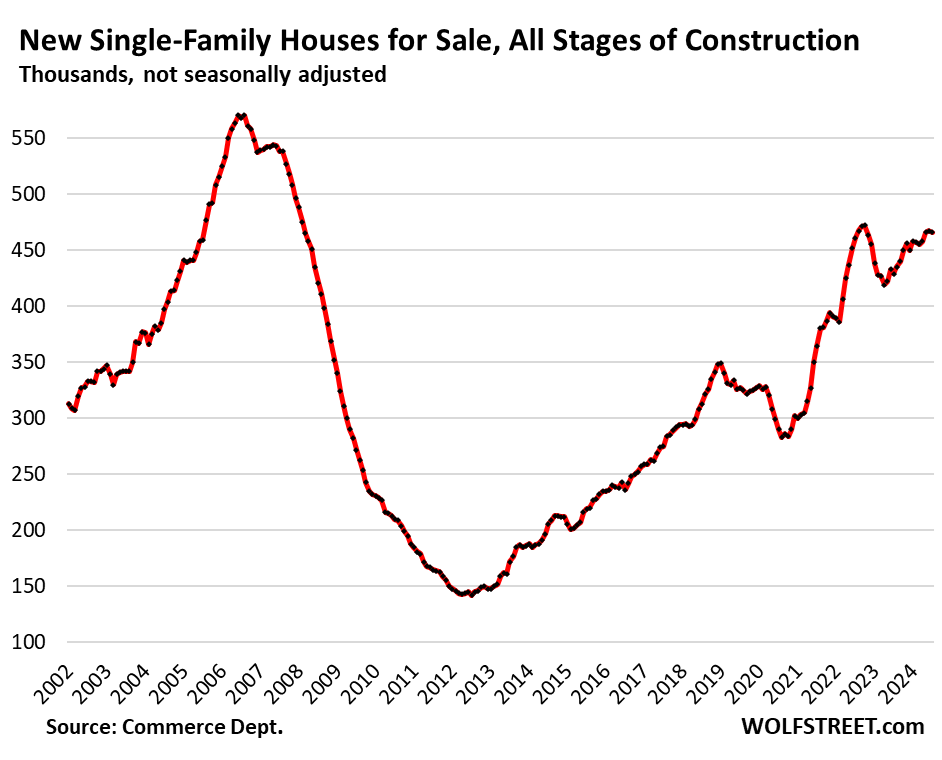

Inventories of houses in all stages of construction – from not yet started to completed – remained at about 466,000 houses for the third month in a row, along with August-October 2022 the highest since 2008. Supply, given the jump in sales in July, fell to 7.3 months.

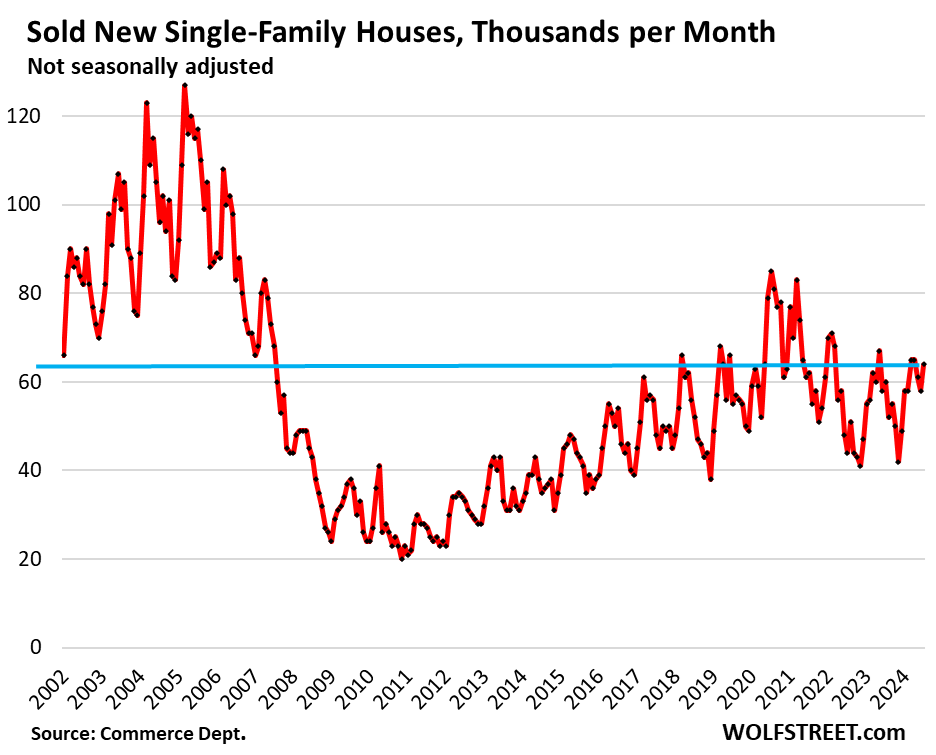

Homebuilders sold about 64,000 houses in July, not seasonally adjusted, up by 6.7% year-over-year and by 12% from July 2019, according to Census Bureau data today.

They’re the pros in the housing market, and they’re taking advantage of homeowners’ refusal to adjust their price expectations to reality, and so sales of new single-family houses have held up well, even as sales of existing houses have plunged to the lowest levels since the depth of the Housing Bust (in July -27% from the same period in 2018 and 2019).

The seasonally adjusted annual rate of new house sales jumped by 10.6% in July from June, and by 5.5% year-over-year, to a rate of 739,000 sales, the highest since May 2023.

The big publicly traded homebuilders have figured out how to deal with this market. Unlike homeowners sitting on vacant houses, they cannot outwait this market (though a small builder might try that). Big builders have to build and sell houses to keep their revenues flowing, and they’re doing it.

They’re selling at a good clip, and they’re building at an even better clip, with unsold completed houses on the market now piling up, which is exactly what this market needs, though it’s a risky calculation for homebuilders.

Homebuyers who are frustrated with trying to buy an existing house, can go out and make a deal for a move-in ready new house, at a lower-than-market mortgage rate that the homebuilder bought down, and come out with lower payments.

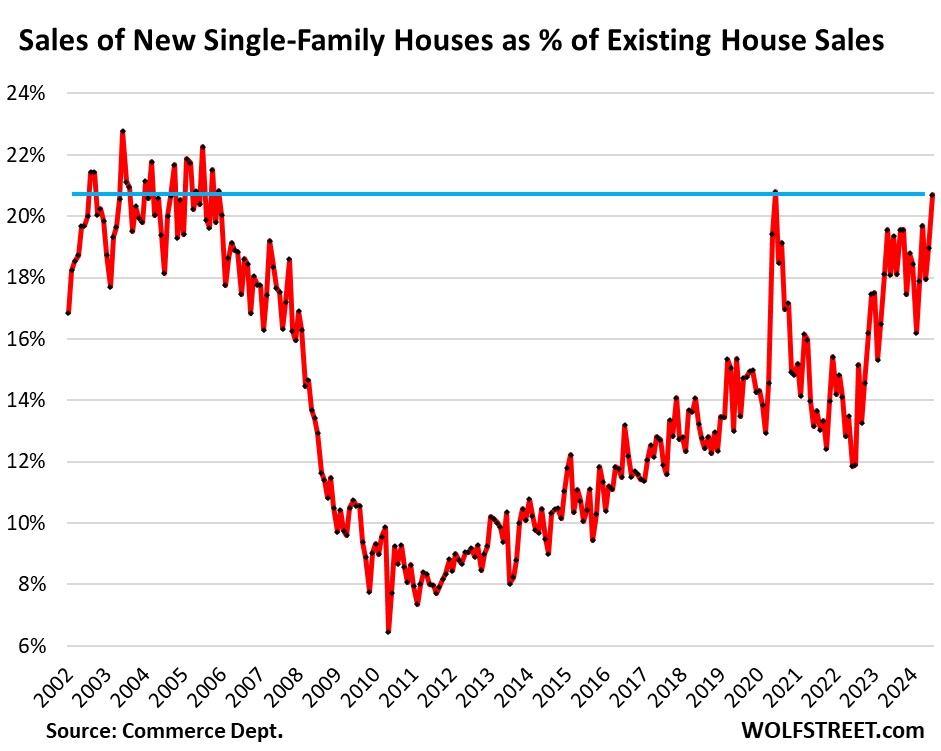

Homebuilders’ sales take an ever-larger share from homeowners.

Sales of new houses as a percentage of existing house sales in July jumped to 20.7%, the highest since 2005 (except for the lockdown spike in June 2020), as some buyers have shifted from existing houses to new houses.

This aggressiveness by homebuilders will help tamp down prices as it adds supply to the overall housing market, even as demand for existing houses has plunged.

Prices of new houses have dropped and are competitive with existing house prices.

Prices of new single-family houses sold at all stages of construction have been wobbling lower since the peak in late 2022, as builders are offering houses at lower price points – smaller, less fancy houses, and less fancy appliances and finishes – and they’re throwing in big incentives, including mortgage-rate buydowns, which are costly for builders. For example, Lennar disclosed that mortgage-rate buydowns cost $47,100 per house on average.

But the prices here a contract prices, as written into sales contracts, and the costs of mortgage-rate buydowns are not included here.

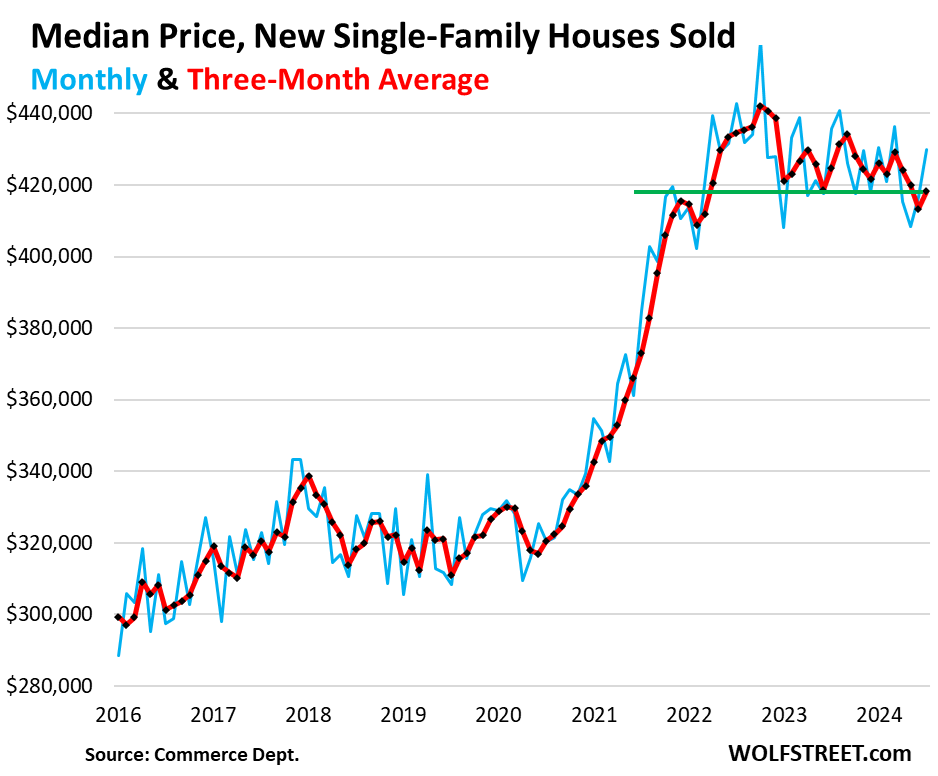

The median price of new houses (based on contract prices) is subject to large monthly up-and-down squiggles that are often heavily revised, so we focus on the three-month moving average of the median price, which includes all prior revisions, and irons out some of the monthly squiggles.

This three-month average of the median price of sales contracts ticked up to $418,300 in July, down by 1.6% from July 2023, and down by 3.8% from July 2022, and down by 5.4% from the peak in October 2022:

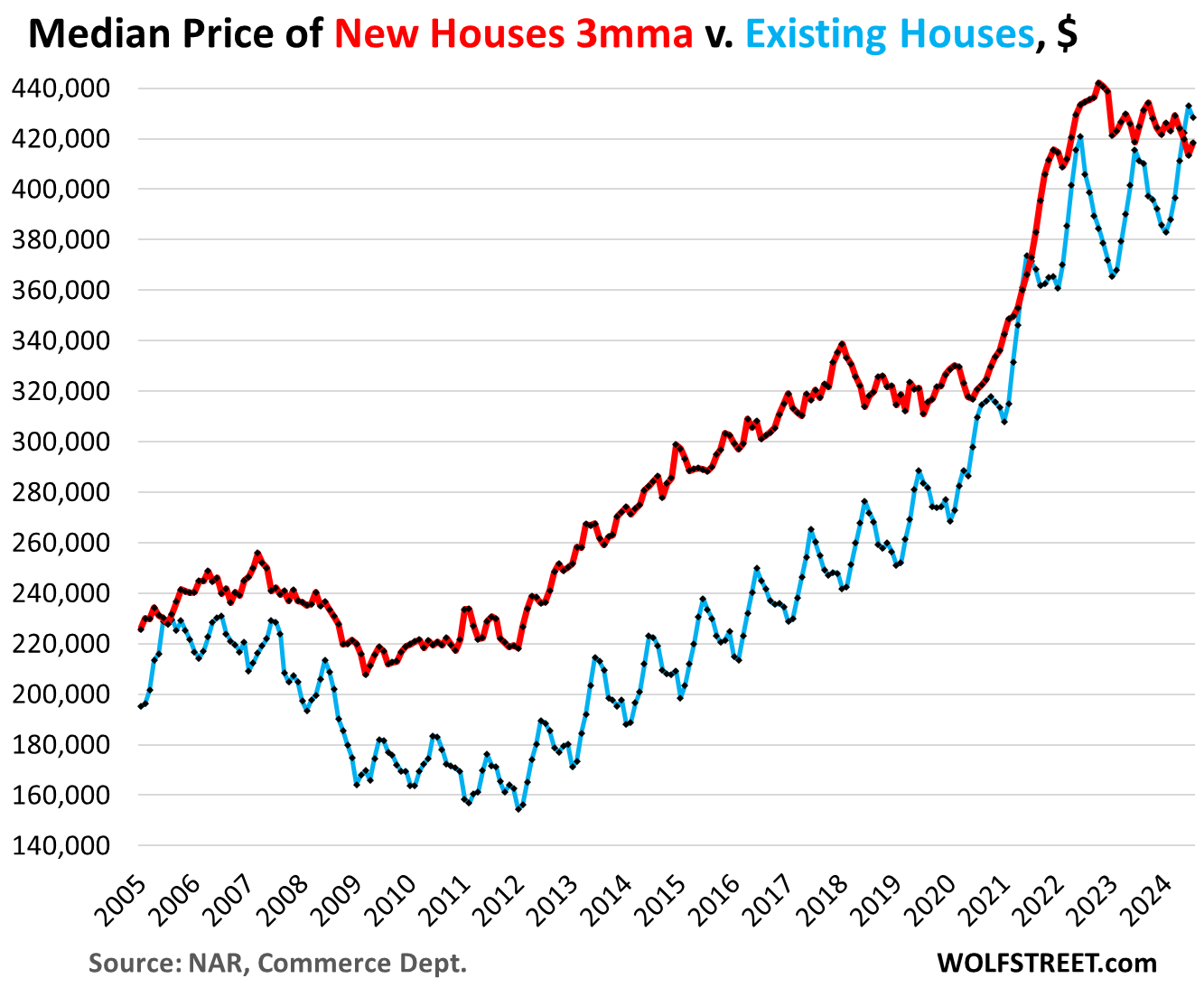

By comparison, the three-month-average median price of new houses (red in the chart below) is roughly $10,000 lower than the median price of existing single-family houses. For seasonal reasons, the median price of existing houses will drop for the rest of the year (blue):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This will definitely help move the pricing needle in the right direction for areas with lots of new build, not so much for NorCal and SoCal…

Noooo…we want a President who kicked us in the teeth by asking his buddies in Congress to kill a bipartisan immigration bill.

Because we love two-faced politicians who will rail against immigrants yet not do anything about it. If he were serious about it, he should have done something during in his four years in office.

Exactly. People in some states may benefit from more inventory. Those in other areas, where inventory is low, prices are high, and new construction costs are expensive, will not. Looking at national averages doesn’t tell the whole story.

BTW, I just read that tariffs on Canadian lumber have increased and I expect supply may be disrupted due to rail strikes.

part of the Harris Inflation Production Act

taking lumber tariffs from 8% to 14%

with friends like us, who needs enemies

A few of the US objectors to tariffs are US Home Builders Association and US Bed Framers. Latter was blunt:

“We don’t want no gnarly boards sawed from piney wood pecker poles”

Or something like that. But it is fact that the US is not self- sufficient in high quality construction grade lumber from slow growing conifers like spruce.

The federal govt. has put a floor under all asset prices. They created TARP during financial crisis, backstopped ALL deposits when SVP imploded, etc. Apparently asset price protection is part of governments objectives. In this quasi-freemarket we live in it’s best to load up on debt/assets because there is no risk. Well anyway I refuse to leverage my 6 figure income for a shack in El Cajon, just my opinion but govt. should not have its hands in so many things.

People put a floor under asset prices. They’re heavily incentivized to do so by debt and fear of losses. The government spent many years making those burdens easier, but aren’t doing that so much now.

Yes this is the system!

Howdy Folks. Will there be new housing peaks???? FED is gonna start lowering rates…. Looks like history is gonna repeat to me. Leisure Suit, check, lava lamp, check, ……

Lowering rates at the apex of the biggest everything mania in the history of the world, with inflation still way beyond the FED’s “target” of 2% (which should be illegal in and of itself), will be the most reckless move in FED history, all things considered. It will reignite inflation and the speculative orgy which has finally started to wobble.

Howdy Depth. YEP, the 70s 80s were something to behold….. Pretty sure the smart folks are headin US back to the future…….

Don’t forget the crazy high level of fiscal spending above tax revenue!

Put another way, the crazy low federal tax rates relative to federal expenditures, the vast majority of which is NON-discretionary. Contrary to the talking points of our wealthy/corporate overlords (and their lackey politicians), the United States has among the lowest taxes as a percentage of GDP among developed nations. Our budget deficits are at least as much of a revenue issue as they are a spending issue. Generally, the boomer generation has underinvested in our nation’s future and passed on the bill for what very little investment was made on to future generations through budget deficits.

Tax receipts in the US are at record highs…

The bubble (#3) permits higher spending, and the associated wealth effect increases tax revenues. It’s going to be difficult when the wealth effect evaporates.

You lower the administered rates and drain reserves simultaneously. I.e., continue with QT. Interest is the price of credit. The price of money is the reciprocal of the price level.

After the dotcom bubble, with its 99% collapses and bankruptcies, I thought the market had learned its lesson. Then I read an article around 2002-2003, called “Double Bubble.” I thought, ” No, impossible! The market has learned not to overvalue assets….” Then 2007-09 happened. Bubble #2, and it was brutal. Once again, I thought the lesson had been learned!

Here we are now in the “everything bubble,” arguably history’s greatest ever overvaluation of assets. Some are still arguing that the valuations can be justified.

The collapse of bubble #3 will surely be epic, and will cut ✂ across all asset classes except probably commodities, which have largely been too cheap and affordable for too long. Be careful out there. The bubble is popping now, as I write.

Let’s not have a bubble #4!

Bubba: for those of us who were just being born in the 80s, could you please elaborate how history is repeating itself?

Home prices at all time high. Food prices at all time high. 3 stocks are 10 Trillion dollars. Quickly, cut the rates!!

Not just any rate cut, we need emergency .75 rate cut now..we can let Nvidia fall below 3T market cap..

WS and MSM are now back on the 4 rate cuts narrative after Pow Pow speech…go figure…rinse and repeat…hopium is like McClain…diehard

Just saw this article in Bloomberg: Major Central Banks Now Aligned as Powell Signals Fed Cuts Ahead

But wait for it….there is actually a line that reads:

“marking the beginning of the end for an era of high borrowing costs”.

OMFG. They are trying to say, if their belief about cuts turns out to be true, that 2 years constitutes and era.

And that these rate hikes are “high borrowing costs” in the grand scheme of things. It’s a total lace of perspective and a quite a bit of gaslighting.

An era was the DECADES of QE for gamblers.

Powell thinks he is Taylor Swift…

Correct.

The FED is completely transparent. They are hell-bent on keeping asset prices high. They will destroy the US dollar to do it. The wealthy will not be taking haircuts, even if it means starving the young and the poor. It’s time to start protesting outside the Eccles Building with an iron maiden with Jerome Powell’s name on it.

“FED is completely transparent.”

The Fed is a crime syndicate. BTW, I seeing old people (70s, 80s) in dire straights as well, those who retired years ago. Many lucky enough to have a paid off home (nothing extravagant), are taking out reverse mortgages. Others with no assets are SOL. It’s disgusting.

You’re a riot DC!

The idea that inflation somehow benefits the wealthy is wrong. Inflation only benefits government bureaucrats and politicians.

Tell that to all the Billionaires QE created.

Who are wealthy by all measures vs their constituents. It’s a cooked game, democracy has sold out to the highest bidder all under the guise of freedom and security (which are oxymoronic notions).

Silly. The politicians and bureaucrats who benefit are upper middle class college graduates who lack the skills to become billionaires.

Money printing does inflate asset prices, but it’s unsustainable, so I think you are right, unless the wealthy are smart and sell off their inflated assets (like Mr Buffett). Most of the wealthy will be hurt by the popping of bubble #3, as everything they invest in will be or already is deflating. Even Berkshire will take a major haircut.

I agree.. the fed manipulates markets to remove the boom bust.. no more bust opportunities for citizens who work hard and save to get ahead!

It would happen if the news media would not be owned by the overlords.

I don’t think the Government needs any help from the Fed in destroying the dollar. The Gov is doing a fine job on their own.

“Quickly, cut the rates!!”

That’s what you’d do – if you’re a private banking cartel that exists purely to service the rich.

Over and over and ………

Service the rich Fed style

Where I live a new detached house is like 3 million dollars and on a stamp sized lot of something like 40 x 80 feet.

If prices drop I’ll buy at the bottom. I’m waiting. That 4 bedroom next door finally sold after being on the market a while, and yes, the owners are a family as predicted ( walking distance to school). The block over has a flipper just sitting on their property. They claim it will be on the market soon. We’ll see how long it sits.

“The block over has a flipper just sitting on their property. They claim it will be on the market soon. We’ll see how long it sits.”

This is exactly why there is not a housing “shortage.” Instead, we have hordes of speculators, from Blackrock all the way down to the green-eyed mom and pop, buying up nearly every house that hits the market as an “investment property,” fully expecting that the combination of inflation + the appetites of greater fools + FOMO exceeds the building’s carrying cost and natural depreciation.

Since 2013, they’ve been right, hence why this unending mania is now “normal” and ingrained deeply into the culture. If this market ever drops on a nominal basis (big IF) for an extended period, and sentiment finally turns, there’s going to be an avalanche of houses that no one wants to pay for.

Haters gonna hate. Hordes gonna hoard. Homes gonna home less.

Smilers will smile.

Many smiles on many faces, people have money. 65% of Americans owning their own homes. Smiling faces also because of market gains and treasury gains.

Could be, a lot of smiles will be lost up ahead by the slaughter house.

I am one of those Mom and Pop landlords that bought seven properties between 2008 and 2013, and I couldn’t be happier. All of them are now paid off so I don’t have to really work anymore.

Uh-huh, riiiiiiiight……everybody’s independently wealthy on the internet.

DC, exactly. He who protests too much lol. I’m wading in it now.

You might want to sell and put money in t bills

That’s funny the cost guru clark Howard got into being a landlord the last recession and he hated it so much he swore it off!

Now if the cost guru hates it, you know it’s bad. And he takes calls from poor people all day long!

lol rofl 🤣

Sure thing bro

I bought my house in 2010. Your strategy will work. Give it time, there will be false starts on the recovery side.

That was quite an expensive time if I remember correctly.

Houses near me were asking 100’s of thousands over what they eventually fell to for a couple years. Then they slowly ratched back up. And on the way Congress knew to get rid of almost all tax deductions for homeowners. Quite a coincidence

I’m not sure I agree this will help. Builders have been deeply discounting and using rate buy downs for 2 years. The discounts not show up when the sale is reported. The rate buy downs do not show up either. So a 50@k house with a 50k discount and a 4% rate gets reported as a 500k sale. And the mortgage rate discount further brings down the payment. But none of that helps in bringing down the median or average price in a geography from a reporting perspective.

Sellers need to see prices falling to encourage them to list and/or reduce price. Buyers need to see prices falling to get them interested.

Nothing in this moves those needles.

Actual unemployment/underemployment and honesty from the BLS would help more than this. Let’s see what happens when unemployment hits 5% and then 6%. You’ll see prices start to fall.

What the article says is that what builders are doing — lower prices, incentives, rate buydowns while building massive supply — will help bring down prices of EXISTING homes because homeowners have to compete with builders.

Hi Wolf,

Are you able to see the new house inventory by state? Which areas are more affected by the increased inventory and which are affected the least? Also, New homes inventory includes condos?

The whole article is about new single-family houses, and existing single-family houses. So no, they do not include condos.

By-state data is not available.

Reventure has data by state/county. It’s a subscription service.

Kamala is promising $25,000 down payment assistance for first time homebuyers, and she’s including anyone who didn’t purchase a home within the last 3 years.

All those Kamala buyers will flood the market and quickly buy up all that inventory. So don’t worry about homebuilders, the election is in a few months.

Regarding inflation, today I bought a gallon of bleach at Walmart for $7.98. I don’t buy much bleach, but the last one I bought was $2.29. inflation is clearly out of control.

But the FED cares more about employment than anything else, and they’ll prove it again if they cut rates anytime soon.

Price fixing of anything is always completely stupid and futile. The capital markets are much better equipped than any group of bureaucrats. But common sense and reality are in short supply in DC and amongst the government class the world over. We’re just asking for the ride.

It’s a campaign promise. How many of those get fulfilled?

Not to mention, new houses come with a long-term warranty priced in. Who doesn’t like a new house!

The discounts show up in the earnings calls. If you look up on Zillow a town called Surf City in North Carolina, you will see roughly 80% of the recently sold homes are from a DR Horton subdivision. New builds are taking demand from existing homes.

Until we get a 30% cut in the markets and higher interest rates, housing prices are staying where they are or are headed up again…and inflation is about to take off again too…but don’t worry, its transitory.

If history is a judge (last bubble), we have 5 years until the bottom. 15% is what inflation will eat the dollar in that time. So the bottom may meet your falling house prices and party on to new highs.

Powell has lived this chapter before.

Yep, I was in my new development sales office today to say hi to the salesman that sold me my new house a year ago. Sales are up in August! This phase is closing out by year end and two new phases are starting construction nearby. These are starter homes selling at about $175/sq.ft.

Builder is offering a buy down in mortgage rates over 5 years to come out at 6%. They bought a “block of mortgage money” he said.

Life is good! He bought a NEW LEXUS SUV!

He did mention that if the FED lowers rates and mortgages fall further, they will start moving new build prices up accordingly.

They moved prices down to stimulate demand. But the big thing they did was buying down mortgage rates. That will go away if mortgage rates drop far enough. That’s the thing they will drop, no more buydowns. They will still offer other incentives and price their pile of inventory to move it. They’re sitting on big inventories and raising prices in this environment is only something that a salesman would say.

I am just like many others waiting for the prices to be more friendly and don’t listen to BS about $15,000 downpayment assistant for FTHBs and similar excuses that can help us to buy it, no, I fist do care about the price and then rate of mortgage!

Wolf ,its first time seeing you that you are so sure and firmly predicting that price reductions will be here soon! 🔜??? Confirm please, otherwise its not going to be good!

lol if only the purchase of a Lexus suv was the barometer of a healthy minded and economically sound individual!

In this case it is by a salesman of sticks and land.

therefore it is as a suit is to a businessman. Necessary attire and projection.

🎣 he gotcha. Want a dollar? Hehe (State Farm commercial)

Lexus is a quality car. You can get 20 years out of it if serviced regularly.

Cmon, it’s really just a Toyota that costs almost twice as much.

Any mechanic knows.

🎣 Toyota reeled in another!

lol I’m kidding.

“block of mortgage money”

Anyone know what this means?

Still way too expensive. Price per square foot is ridiculously high. High HOA fees. High Insurance. Property taxes. I guess I’ll be staying in my apartment. Fine with me.

Builder down the street is furiously putting up 6 homes on a lot and prepping the much bigger lot across the street. 2 of the 6 were framed and have plywood roofing in less than 3 weeks. I suspect prices when finished will still be 3-4x my rent.

I forgot to mention maintenance and repairs.

Yearly expenses range from 1%-4% for homeowners.

So for a home valued at $200,000 you would need between $2000-$8000 for annual upkeep.

Buying a new home when prices are near record highs is not something I would even consider, and there is something VERY WRONG with the Fed lowering interest rates with record high asset valuations, home prices, stocks, etc., and inflation still nowhere near 2%. Usually they are hiking rates under such circumstances.

The insurance premium increases are getting annoying tbh.

Remind me to buy their company stocks so I can ebb their flow.

Pay me then I’ll pay you. $

Where I live you can’t find anything for less than about $1,000 a square foot. Resale studio condos start at $1,000 a square foot.

Now….those are bubble prices for sure.

What I remember back in the housing crisis of the 80s is that when new home inventories got too large, “bulk buyers” (the term used by builders) showed up from overseas to firm up the sales with cash. The prices need to be controlled to stop sales from crashing the mortgage book of the banks and lenders (comparables).

Everything will be done to save the comparables.

“… stop sales from crashing the mortgage book of the banks and lenders (comparables).”

LOL, didn’t get the memo? Most of the mortgages on these new houses are sold to government entities and turned into Agency MBS. The banks are not on the hook. No one cares if the taxpayer loses money on these mortgages. No one will do anything to stop the taxpayer from losing money.

Is there a limit to how much in losses the taxpayers is on the hook for

100%

100% of losses or 100% of the capital the feds have invested in Fannie and Freddie?

It would be interesting to see how the impact of new homes competing with existing homes plays out market by market. Lots of metro areas are largely built out, with new homes going up on the fringes, not competitive with existing homes because of drive time, but smaller markets or retirement markets this is probably less important.

My thoughts as well. The builders competing with homeowners debate could be reframed as suburban homes (existing) vs exurban homes (new construction). If you work from home, new construction makes sense. The prospect of commuting 50 minutes each way might nudge a buyer to purchase an existing home.

Now share active inventory of new and existing homes going back to 2006.

My charts here in this article of new home inventories go back to 2002. Why do you want me to shorten the time line to 2006?

Because they’re overleveraged and need housing to keep going up so they want to try to disprove every metric as “meaningless.”

Because Abum didn’t RTGDFA!!!!

In many urban areas there are very few new homes available for sale. This is true in the Swamp and neighboring close in suburbs. Many new homes being built are located far out from the jobs in the Central City, and involve long commutes. This is never mentioned in the comments on Wolf’s articles on this subject. People don’t like long commutes. So all the arguments in these posts about the advantages of purchasing new homes and getting a great deal with buydowns etc from builders falls on deaf ears as far as I am concerned. For example, new homes built in the urban areas and nearby suburbs (via teardowns) in the area where I live close to the jobs and public transportation to get you to the jobs are snapped up at full price, and show no sign of slowing down the pace of sales. Realtors are glad to point this out in the many solicitations they send you in the mail. For once they are correct. Inflation in housing is alive and well and getting worse.

If you want to buy something new in a city core, you buy a condo in a new big building. If you want a new house with a yard, you’re likely going to look further away from the core and commute, or maybe work from home. That’s how it is – a tradeoff.

Let me add, we appraised a well built recently renovated brick rambler in Silver Spring MD, just over the DC line that was convenient to public transportation, with a metro subway station within walking distance. The price per square foot was calculated at $1,300/sq foot. That’s some serious housing inflation. The Veteran that bought the house was doing a high five when the appraisal came in at the contract price.

Single family home new construction in my neck of the woods are all over 1 million, some north of 2 million, while existing homes are generally in the 600k-1.5 million range. All new construction is focused on high end luxury mcmansions (luring the endless pool of wealthy MA buyers). Inventory has now risen high enough for 2 whole pages on realtor.com (in a town of 25k people). The new construction boom is highly geographically dependant, and for sure will put strong downward pressure on home prices in markets with high volumes of new builds. I suspect this will be less an issue in New England and moreso a feature of the boom towns in the South and West (FL, TX, CO, UT, ID, etc). Some of the price declines we’re already seeing in these markets will likely continue to gain momentum.

Exactly.

Most of the undeveloped land here is protected forest and conservation land. You’re never going to see an entire new subdivision of new builds those in the midwest and south, except for those new luxury builds.

Kamala Harris plans to build 3,000,000 housing units. If materialized in construction of all stages will exceed the 2006 peak. Until then home builders will be cautious. The banks will force them to liquidated inventory and cut cost. Completed and available for sale will decline. This industry will be on hold waiting for Kamala.

Name the last election promise that ever came to be? Elections promised are about getting elected then back to business as normal. I know those that break promises point to the other side or within the party but a study of several large initiatives disproves that. Ruling classes and their large patrons are very happy with status quo.

I’ve been in a deep dive in RE for years and I look at RE prices all over the nation. And then I compare the want ads to see what jobs are available and what wages are being paid to fuel these insane prices.

And I can say with 100% certainty that everywhere I look RE is completely out of whack. It’s not jobs and incomes that are driving home prices.

bought a condo at the beginning of 2022. lost 20% value on it due to rate increases. but… the bank is holding the portfolio loan turd. I want to see through the mortgage and make the bank pay.

we bought another condo all cash that has depreciated 36% from 2019 prices.. thank you high rates. this was new construction that went live in feb’2020. lol

the timing couldn’t have been more awful for the builder. we tried to first jump on the first wave of price adjustments in 2022 with lower mortgage rates. then the double whammy of pandemic and higher interest rates just squeezed the life out of the prices.

I can’t believe my fortune I live in a brand new home that has depreciated 36% from 2019!!

May be I lose more value. don’t care, living the life I wanted and that was not possible before.

So yeah, builders will work with you more. And I’m happy to be free of my stocks. That tax bill hurt somewhat next year. But the treasury can use it to pay for Wolfs T-bills. ;) ;)

Wolf,

Here is what I read in the Bulgarian press.

I know this article is not about the Fed but when will your article come out about the speech of Powell?

“Federal Reserve Chairman Jerome Powell said the time has come for the central bank to cut its key interest rate, Bloomberg reported.

So Powell reiterated expectations that central bankers would begin lowering borrowing costs next month and made clear he intended to prevent further cooling in the labor market.

“The time has come to adjust policy,” Powell said Friday in a speech at the Fed’s annual conference in Jackson Hole, Wyoming. “The direction of travel is clear, and the timing and pace of interest rate cuts will depend on incoming data, the evolving outlook and the balance of risks.”

The cut coincides with base effects. It will give the market false signals.

it’s clear to me that the fed won’t tolerate any recession. that’s why it’s lowering rates even when unemployment is only a small problem.

Pass legislation to prevent ownership of more than X homes in Y area and you would break the monopoly pricing power that industrial homeowners have as well as force the ibuyers to be in and out of markets if they want to continue operating in a desired area. I suspect this would fix our fake “supply” problem overnight. Anti-monopoly laws are there for consumers, but there has been no enforcement in the housing market. Monopoly pricing is rampant all over the place. There’s definitely no supply problem, people just can’t afford what’s available for sale.

You are proposing a draconian solution to an imaginary problem. I defy you to demonstrate the existence of the monopoly pricing power that you pretend exists.

they speak of all the airbnb properties

I’m still waiting

Lots to learn. Glad to see inventory pick up. But if you look at the Case Shiller home price index – in Jan 2020 it was 212.4 and in May 2024 it was 323.48. That’s a 52% gain in a short time. Building is going to have to accelerate to make any kind of a dent.

It’s almost like the fed’s massively increased balance sheet forced up prices of all risk assets since 2020, funneling wealth from the bottom to the top at a furious rate, when none of that was called for. Amazing how few people (outside of these circles) realize that.

Never underestimate the number of mouthbreathers out there.

I consider having a home is a place to live. Not as an investment. I wish everyone doing the same.

Hear, hear!

Owning a home can also be a money pit…

Buyers are the ones who are still buying and keeping the prices high. Realtors and MSM are gaslighting those Buyers.

“Rates are coming down now. Buy now before Prices go up further. You can always refinance. etc etc”

Last 3-4 weeks, my city (SF Peninsula) had Existing home inventory built up. Not many NEW homes. In last 3 days all of them went into Pending. I went to Open house yesterday and Listing Agent had same BS. How Price can only go up from here.

Well, personally I will stay out of this crazy Market and I know one city doesn’t represent broader picture. It is just one city.

But point is as long as there are Idiots out there who can afford to put down Payment and Buy house at those Crazy prices, we wont see any much correction in Housing Market. Stocks and Crypto has given FALSE confidence to Many, Markets go up and up only. Why shouldn’t they? Govts and FED come to rescue many times…