People are waiting for rates and prices to drop, while supply keeps rising.

By Wolf Richter for WOLF STREET.

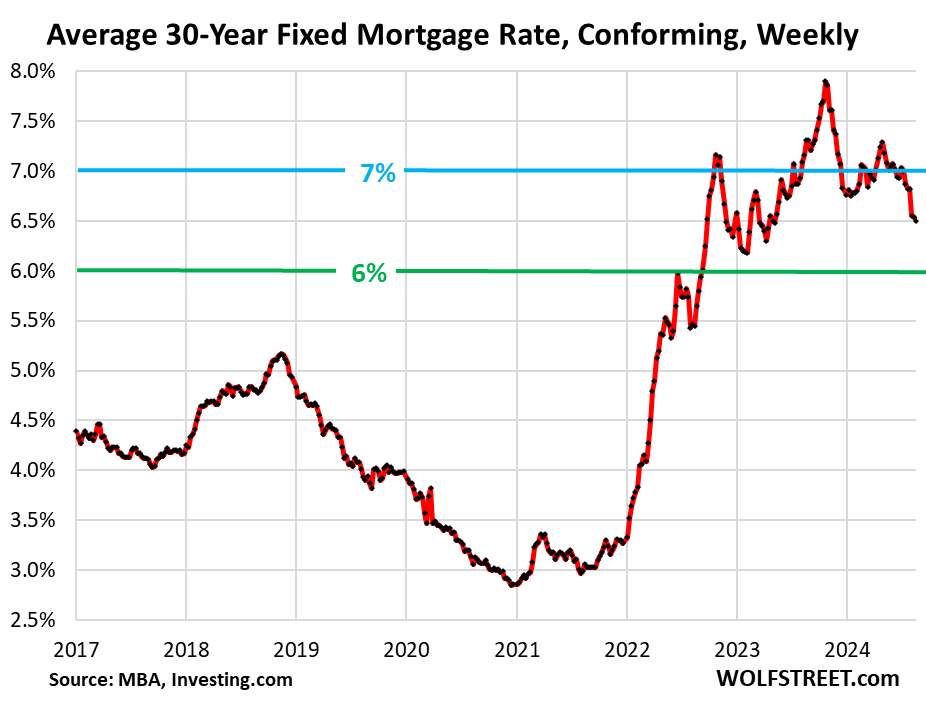

Mortgage rates dropped to 6.50%, the lowest since May 2023, according to the Mortgage Bankers Association today. But instead of re-igniting demand for homes from buyers who need mortgages, these dropping rates have caused potential buyers to wait for mortgage rates to drop further, and to wait for home prices to drop, as prices are way too high, and so demand has dropped further, with applications for mortgages to purchase a home dropping toward their historic lows.

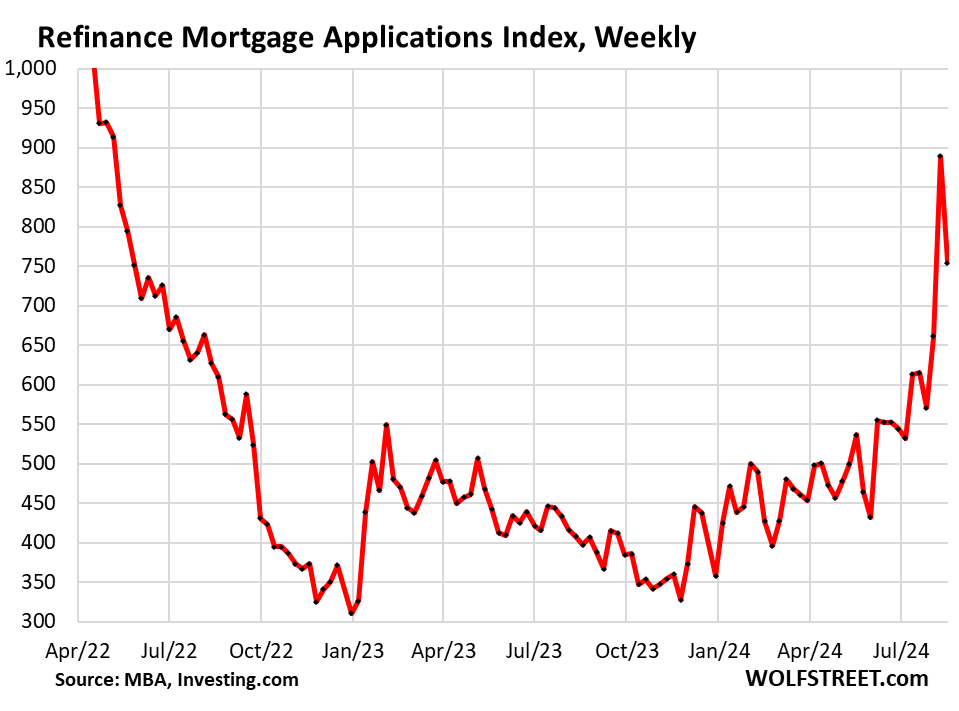

But the lower mortgage rates have re-ignited applications to refinance existing mortgages, and refi mortgage applications have jumped in recent weeks and have doubled from the historically low levels last fall. This surge for refi applications does nothing for the housing market, but it does speed up the pace of the Fed’s QT because it causes the mortgage-backed securities (MBS) to come off the Fed’s balance sheet faster, and we’re seeing the first signs of that.

The average conforming 30-year fixed mortgage rate during the latest reporting week dipped another 4 basis points, to 6.50%, the lowest since May 2023, according to the Mortgage Bankers Association today. This measure of mortgage rates has been above 6% since September 2022.

People are on Buyers’ Strike, waiting for lower rates and lower prices.

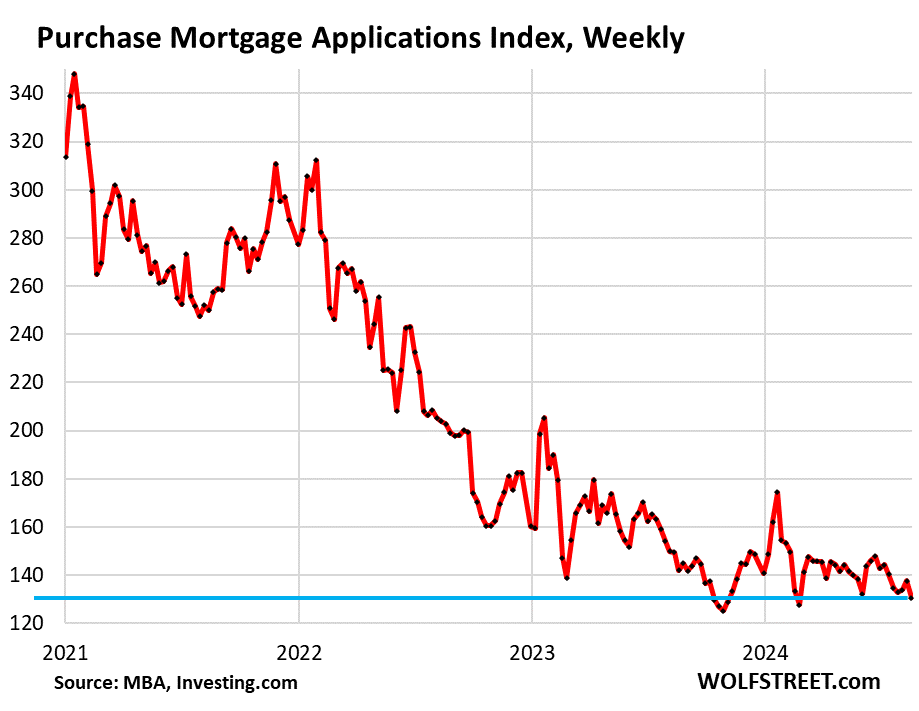

Home prices are too high even for cash buyers and institutional investors, purchases of existing homes have plunged, as supply has surged, and applications for mortgages to purchase a home have collapsed by nearly half from their pre-pandemic levels in 2019, and in the latest reporting week fell further.

The Purchase Mortgage Applications Index is now just a hair above November 2023 when they’d dropped to the lowest levels in the data going back to 1995 after mortgage rates had spiked to 7.8%.

Mortgage applications are an early indication of demand and home sales volume:

Mortgage refi applications spike will speed up the Fed’s QT.

But mortgage applications to refinance a home have been rising in their zigzag manner since early 2024, from very low levels. And in early July, as mortgage rates dropped, refi applications started spiking.

Last week, the index spiked to the highest activity level since April 2022, the beginning of the rate-hike cycle. In the current week, mortgage applications backed off from that spike but were still the highest since May 2022. Since last fall, refi applications have more than doubled. Surging mortgage refis accelerate the pace of the Fed’s QT.

In terms of the Fed’s QT, mortgage-backed securities (MBS) come off the Fed’s balance sheet when the underlying mortgages are paid down via regular mortgage payments, or are paid off when the mortgaged home is sold, or when the mortgage is refinanced, and these principal payments are passed through to the MBS holders, such as the Fed.

The Fed’s monthly MBS runoff had moved along at a crawl from the beginning because mortgage rates had soared before the Fed even started QT, home purchase volume had plunged, and refi volume had collapsed. By early 2024, the pace of the MBS runoff had been running at about $14 billion a month as a result of the historic collapse in mortgage payoffs.

But these refis in August are the highest since the Fed started QT in the summer of 2022. The QT pace for MBS is approaching $20 billion a month, reflecting the higher refi volume this spring. The jump in refi applications since early July will speed up the pace of the Fed’s QT when the passthrough principal payments from the paid-off old mortgages actually reach the Fed.

A future increase in home sales volume, and therefore higher mortgage payoffs, will further speed up the Fed’s QT.

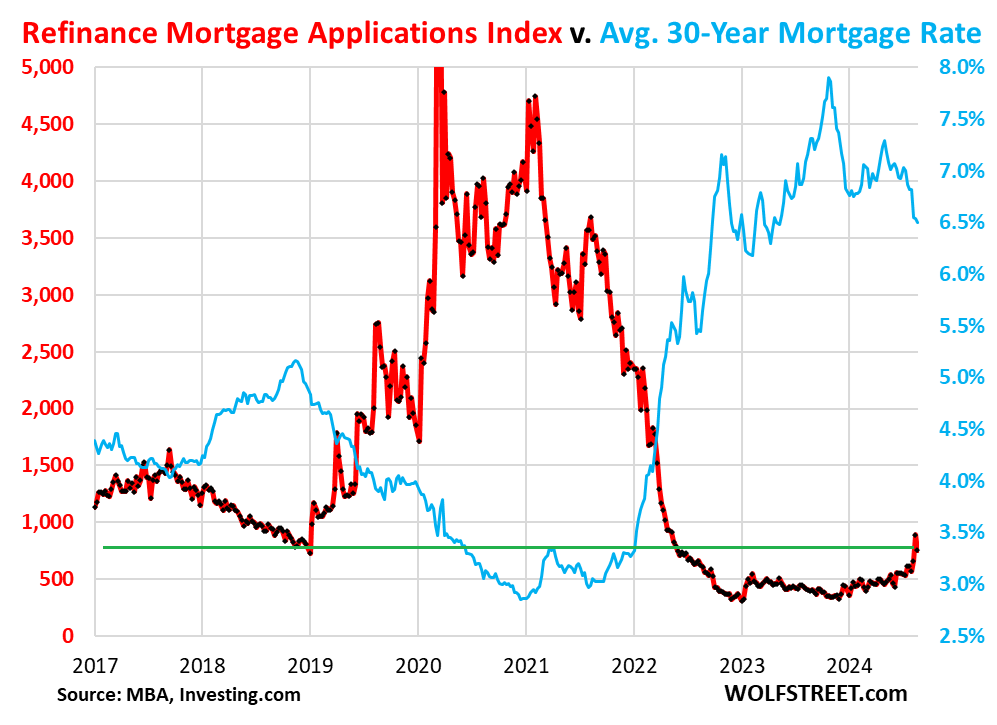

On this longer-view chart, which includes the historic spike in refi applications during the 3%-mortgage era, we can see how refi applications (red) have nearly doubled from the lows last November, as mortgage rates (blue) have fallen.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hard to see how in most markets that a decline in interest rates would bring down home prices since sellers would expect lower interest rates means more qualified buyers. Buyers are hopefully just evaluating the total cost to them but the flip side is that buyers might jump in expecting house prices to go up and they can simply do a refi in 18 months or so expecting some decent rate cuts.

Buyers set the transaction prices, not sellers.

Sellers only set the asking prices. If asking prices are too high, buyers say, forget it, and the home doesn’t sell, and there’s no transaction, and no transaction price, which is the case now a lot, hence the plunge in transactions.

Here are the asking prices (listing prices) that sellers set:

Funny.

Jerome Powell sets the price.

He sets the price of short-term money. That price is now still over 5%.

Mr. Valentine has set the price.

The affect of higher interest rates and the Buyers’ Strike has been the bulk median price – ignoring seasonal variation – staying the same over the last couple of years. The same can be said for Canada. I suspect this trend will continue until economic conditions change. If economy deteriorates for some reason leading to job losses house prices will fall, vice-versa. Which way will it go? Too many variables to guess.

Home prices were slowly going up ever since the bottom of the great recession, but I swear it was the trump tax breaks in 2017 that started the lift off in real estate prices. It was then that prices were flying away from me. Something in that tax code compelled investors to mop up properties like crazy.

“Hard to see how in most markets that a decline in interest rates would bring down home prices”

If you believe the Fed is about to cut rates and home prices are falling, it makes sense to wait a few months in order to get a better deal. I don’t think you can refi that quickly after the initial purchase mortgage.

While depends on the specific loan conditions, most have no waiting period or very small. Obviously anecdotal but in my neighborhood houses only fell from their high by a little and houses don’t sit on the market long. My guess is at some point things will heat up quickly and will be interesting which direction things will trend. My inconsequential guess is my house might get back above the highs from before interest rates started going up. My house was 405k when purchased in 2016 and everyone thought way too high. Similar houses shot up to as high as 750K and have been selling for 660k in recent months. I’m hanging so purely a curiosity thing for me. I like my house, my neighborhood and 100% telework. Could do with less summer heat but who wouldn’t!

Tons of people have been priced out on the sidelines. I’d guess there’s a large population of would-be buyers whose incomes are close but not quite there to secure a starter home mortgage. With rates falling as much as they have, these buyers can now get pre-approved, begin shopping, and compete against each other to purchase. This demand will increase home prices.

I understand that some people may wait longer hoping for further rate decreases. And I understand WR’s data above suggests the opposite of my suspicions- buyers are still waiting despite a major rate decrease, at least for now. But I’m suspicious that trend won’t continue when we see the next few home sales data points, should mortgage rates stay around this level or below. We know the demand is out there, and we know that buyers lack critical thought and restraint.

I hope I’m wrong, but I wouldn’t be shocked to see sales up (seasonally!) and prices up over the coming months.

Be careful of what you wish for. Looking at the history of bouts of inflation, the Fed (Burns, Volcker…) when they thought they had vanquished inflation, it reared back up when the Fed initially cut rates. Too early. So they had to hike the rates even further. Maybe Powell is luckier, but I’d say that it’s now still too early to cut (Sept.).

I think there’s many more shrewd & sober would-be buyers who are sitting it out and watching their savings grow and thinking…nah. What’s the hurry when you can rent the same thing or better, keep your down and pay 1/3 the monthly?

Lots of much funner pits into which one can hurl their hard-earnings.

@HowNow

To be clear, i want homes more affordable due to price decreases. I’d be happy with mortgage rates at 10%+.

@bullfinch

Agreed that’s the correct outlook, let’s hope that’s the case. But the insane bidding wars building this bubble are barely in the rearview mirror. Maybe i’m just jaded and it’ll be different this time.

What virtually no mortgage brokers and realtors, not to mention homebuyers and sellers, seem to understand is that the 7 and 10 year treasuries drive mortgage rates, and 7-10 year yields are already baking in a boatload of rate cuts starting in September. So it’s entirely possible that rate cuts start and there is no impact to mortgage rates or mortgage rates could even move higher. If the public sees 2-3 cuts by the Fed and mortgage rates do not come down, do you think buyers come back to the market/stop waiting or does the market stay pretty frozen? Practically nothing is transacting in my “luxury” suburb as of about June.

Does the 10 year yield really reflect the appropriate rate needed to compensate for the inflation risk in 10 years or does it just reflect the limited supply – the Treasury opting to fund itself in shorter durations. Shorter terms are still paying 5%.

In the end, the need to sell Government Debt (in the absence of the Fed buying) will set interest rates. I guess there are still lots of old and new tricks that can be used to make sure funding gets done. We just have to wait and see. The Fed can “cut” rates, but there are still trillions of new debt issuance in the pipeline.

Anecdotally, we’ve been on the sidelines for while. I’m guess I’m one of the strikers now since I’m not rushing out to pay $450,000 for a 1,800 sq foot home that’s 50+ years old that may have foundation issues, mold, lead paint, old roof, and on and on.

Seems like more people are agreeing with me. I’ve seen some houses sitting for 2 months now and slashed-pricing everywhere. There is still demand for nice, turn-key places, but those are selling far above the national average anyway

Ha…try over $1m for something much smaller than 1800sqft in SoCal amd most of the time it is a condo with high HOA too

Wolf,

I am quite happy to see MBS coming off the Fed’s balance sheet a bit faster but am skeptical that a pickup in refinancing is the cause. I would imagine the vast majority of mortgages on the Fed’s balance sheet are at rates far lower than 6.5% and would think that it is mainly folks who have bought in the last few years who are refinancing now at slightly lower rates (and given the Fed hasn’t rolled over any mortgages in that time period, seem unlikely to be on the balance sheet). Am I misunderstanding something (perhaps the number of mortgages at higher rates pre-2022?)

Well, that would make sense on an intuitive basis.

But apparently — and this comes from mortgage brokers — there are lots of homeowners with relatively little debt on their house, and they want to get cash out of the house. So they could do a $200k HELOC, but at a 9% or so rate. Or they can do a $200k-cash-out refi at a 6.5% rate. And so they do the math, and whatever works out better for them, they’ll do. Some get a HELOC (and we saw volume rising there too), and others will do a refi.

And that’s part of what’s happening because nearly all refis now are cash-out refis.

Seems kind of crazy to give up a sweet 3-4% mortgage to load up with the same debt (and more) at 6.5% but I guess cash-in-hand gives folks plenty of reasons. Given how prices (and homeowner equity) haven’t increased much the past few years, I imagine folks deciding now is the time to refinance would be fairly small (and with “relatively little debt” perhaps not that much to pay off the Fed’s balance sheet anyway). I don’t suppose there is any way to separate the refinancing from the outright (and principal payments) coming off the balance sheet?

Oh well, so much for all that “equity.” Let’s just make the giant housing black hole even larger.

This is the very reason so many will be underwater if we have even a tiny dip in housing prices that lasts longer than 1 year.

That debt isn’t free money. It’s a credit card that uses your house as collateral.

BrianM,

Here is a different perspective, ours. We closed in June on a house after renting for 12 years. Our landlord priced us out of the rental market. We didn’t buy a house for equity, we bought it to lock in a long term lease. We consider our down payment Key Money to secure the lease, if we ever sell we should get it back.

Many of the refi’s you are seeing now could be people using our logic. Get your Key Money out now while keeping the “rent” payment relatively low for your income/neighborhood.

BTW, we bought the house from a mega landlord who probably priced themselves out of the rental market, like our last landlord. The real estate market is changing rapidly at the moment and it is not just about prices, interest rates, and commissions. The way to look at home ownership has changed.

Petunia,

Sounds like a potentially reasonable reason to purchase and I certainly agree that a home purchase should be about stability in keeping a roof over ones head, and not based on any assumption about equity appreciation. Housing prices can however fall, so it does seem like “key money” is more substantial and less secure than a rental deposit (although with other savings one can still imagine coming out ahead over time)

To my original point, I imagine your purchase might have little effect on the Fed’s balance sheet as it isn’t a refinance for you and it isn’t clear to me if the Fed would have MBS from a “mega landlord” on their balance sheet.

“So they could do a $200k HELOC, but at a 9% or so rate. Or they can do a $200k-cash-out refi at a 6.5% rate.”

From the bank’s point of view, why the 2.5% premium for a HELOC vs. whole-enchilada refi (9% vs. 6.5%)?

Both loans have the same collateral, and the HELOC in almost all probability would have a much lower potential total loss exposure (lower revolving HELOC drawdown than whole-enchilada-of-borrowers-equity refi exposure).

So the banks’ are charging *more* for *less* risk?

Why?

Is this symptomatic of bank lenders just becoming middlemen/bookies who only originate and slightly season mortgages…quickly selling them off into public market MBS – so that ultimate loss exposure matters much less to the originating “lenders” than simple, gross, loan origination volume?

HELOCs are second-lien. The original mortgage is first-lien and has priority. If the borrower defaults, and the home gets sold in foreclosure, the original mortgage gets paid off first. What’s left, if anything, from the proceeds of the sale goes to the HELOC lender. So higher risk = higher rate.

Very nice to see this, although still not seeing any real meaningful impact to lower price in SoCal, time will tell..

The real proof in the pudding will be next spring season, depends on where we are at with mortgage rate at that time and what state of the economy we will be at..

“…these dropping rates have caused potential buyers to wait for mortgage rates to drop further”

“This surge for refi applications does nothing for the housing market, but it does speed up the pace of the Fed’s QT”

Interesting – rate cut predictions are now having the effect of attenuating housing demand and speeding up the Fed’s bal sheet reduction.

Hi all!

What does anyone think about the new realtor commission from buyers’ side? Would think it would lower sale prices.

Hard to say but period of adjustment needing buyer representatives sign stuff up front. My guess in long run it will remain flat in long run where in a buyers market the seller agrees to cover that part and in a seller’s market the opposite or in the middle. Basically concessions like any other in the home buying process that are negotiated.

It’s easy list your house,be your own realtor,hire a title company .SAVE BIG MOnEY.did it many times .

Seen a lot about how buyers will need to sign agreements and be prepared to pay for agent or negotiate reimbursement with seller. But nothing so far about seller’s agents: shouldn’t listing charges for sellers presumably now drop from 5-6 percent to 2-3 percent?

Redfin is at 1 1/2% but if you do both sides of the deal with them, it drops to 1% for the listing. At least that’s what we’re looking at right now. These commissions are too damn high. Listing agents don’t do much of anything.

When the time comes, I’d love to bypass the buyers’ agent. I’ve never had good luck with them. Only when we sold properties are the agents worth it, IMO. How could we look at a property though? Just call up the seller? I wonder if sellers will start offering a work around other than FSBO? I’d love to work directly with a seller.

You maybe the exception buy most buyers will be taken to the cleaners by getting themselves into a bad deal. The majority of buyers and sellers have no idea where to even start the process of buying or selling a home. I’m looking forward to it… clean up the mess the average person will get into going it alone.

I wonder if Redfin, Zillow, etc. have now taken this into account when they post what they think a property is worth. If buyers now have to pay the buyer’s agent, then that price shouldn’t be rolled into the asking price that Redfin and Zillow post, right? I know buyers can negotiate with sellers about this, but since the asking price has historically included both the buyer’s and seller’s agent commissions, doesn’t it seem logical that the asking price reflect this new scenario? I’d like to know what people think.

The slowing purchases may also include people waiting to see how new realtor fee structures are going to shake out.

I’d agree. That kind of structural upheaval in how homes are sold can have a substantial impact on volume as buyers, sellers, and brokers are trying to sort through this.

But the shift started just now, so I’m not sure it can already be reflected in the numbers here — maybe some of it.

Sellers paying the cost of a transaction doesn’t make sense. Maybe it’ll change…

Sellers don’t pay. The buyer has always been the one paying because they are the one giving/spending money. NOT the sellers. The sellers are on the receiving end. What you mean is the cut of revenue the seller receives should be more and not divided so much. The seller already knows what they will get when they sell so they should price accordingly rather than look at the topline number of all fees the buyers amount covers.

Good comment Z6, and clearly SO for the dozens of transactions over the last 5 or 6 decades we have seen and been involved in,,, so far…

Again, I want to encourage ALL folx in ANY RE transaction to RTGDFCFP!!!!

Otherwise, Please do not complain, etc., etc.

1) The boomers frontend approach eighty. Within a few years there will

be less of them. They follow the silent gen : 78% homeownership with a dwindling number. They spend less on restaurants, but more on surgeries, pharma, dentists and home insurance. They have plenty assets as collateral to cover their expenses. They will leave less to their families.

2) Gen alpha (2010/2024) is the smallest in 100 years. They are 30/40 millions short of the boomers. The boomers don’t know how to order

online in MickyD. Old pilots cannot fly F-35. There are not enough gen alpha to replace the boomers.

3) Gen alpha is much more sophisticated than the boomers. They get their knowledge from millennials and zoomers. They will be more productive and efficient workers. Labor shortages, higher productivity

and efficiency ==> higher wages. Highly skilled workers will pull the unskilled workers wages. A good economy lift all workers. Profitable co will be able to pay them.

4) There are not enough workers to increase demand for home prices, even with lower mortgage rates, especially if the gov plan to build 3,000,000 new housing units in the flyover areas and suburbia. The new

immigrant labor will be their downpayment, along with wealthy donors.

I would prefer kiosks you speak to, instead of tablets you have to touch. The fecal matter on those ordering tablets would blow your mind. Men’s Health magazine reported that every single ordering screen they swabbed had traces of fecal matter on it. No thanks. The bonus of a kiosk you can talk to is that you could use the same technology for the drive through.

You should probably just stay home.

Don’t open the door to that restaurant. Don’t touch money. Don’t pick up produce. Don’t push that shopping cart. Don’t use that water fountain. Don’t check out that library book. Don’t open your mailbox. Don’t pump your own gas. What else did I do today…

Or, wash your hands once in awhile and rely on your immune system. Your choice.

Well said! My daughter used to eat dirt as a toddler…has the immune system of an ox now!

The Boomer generation is already fading… 1/3 already gone and accelerating

73,000,000 x 0.66 = 48,180,000

Still over 48 million of us left.

I wonder how the decision in issuing lots of short term notes versus more longer term notes has impacted the Fed? It certainly makes sense for the government to do this to ensure limited high yield long term treasuries but also seems like it could work against reducing inflation. Seems like perhaps immaterial if rates move towards target and employment stays strong.

I certain don’t know for sure, but I would suspect that long term rates will either remain where they are as the yield curve eventually uninverts, or get higher. I would also guess that the FED’s current bias towards short term is as much related to their future QE 2.0 scheme.

Feels like the choice was either let inflation run a while with a tepid housing market or let the layoffs from a recession help drive the price down to something that passes the mortgage apps.

Looking like plan B might be the way we’re going?

Anyways I think we missed our window for anything orderly although 80s still on the table maybe.

John Hope Bryant, former Obama advisor is being reported as advocating a 40 year mortgage as the new standard. However, the 1970s negative amortization mortgage is still the greatest miracle of the “creative finance” of pre Volcker regimes.

Interest-only mortgages have been around a long time, and they’re a standard mortgage in CRE. A 40-year mortgage is a step closer than a 30-year mortgage to an interest-only mortgage. A 100-year mortgage is just about an interest-only mortgage.

So basically leasing a house from a bank?

Not really, because you carry all the costs of the house (tax, insurance, maintenance, etc.), and if the price goes up, you can sell the house, pay off the loan, and call it a good deal. If the price doesn’t go up, you can just make the payments until you die, and then let someone else worry about it.

Not to quibble, but that’s exactly how I would describe my recent experience leasing a car. In fact, I traded my lease in early because the trade in value was higher than the cost of the remaining lease. Probably not a typical case, but the result was the same for me.

I guess it is all semantics, but I find the recent trend of younger generations not caring about property ownership concerning. Private property rights are foundational to our country.

People are renting blue jeans for crying out loud

I would love a 100 year mortgage, lowest possible payment and would still get to enjoy tons of home appreciation because of all the additional people that would qualify for this mortgage and buy homes. Come to think of it, it would be the closest thing to a time machine that takes you back to when mortgages were first offered, and we all know how that went $$$!

ChS – …perhaps a recent popularity of one’s ‘breadth of experiences’ has been outrunning that of ‘pride of ownership’…

may we all find a better day.

When I run my mortgage through a 40 yr calculator I get a mortgage only about 8% cheaper per month. So in an efficient market, basically overnight, property values go up ~8% (but time to payoff goes up by 33%). Isn’t that the opposite of what the 40 yr mortgage people want? Prices going up? Creating more inflation? Really shouldn’t they be asking to begin stepping down from 30 years to say 25 over a 10 year time span or something?!? A 40 year mortgage to me only looks good for investors and those that bought immediately when the 40 yr became available.

First time homebuyers should wait to see what goodies Harris will throw at them.

Lol 🤣😂

You forgot the /s!

Those last two charts illustrate perfectly how to form any kind of narrative in the media. I looked at the first one showing refi index the last two years and thought “how can 6.5% drive that kind of spike?”

Then I saw the long term view in the second chart and discovered it didn’t, just a blip off a generational low.

Pick whichever you want to fit your story. Thankfully Wolf gave us both.

Home buyer’s strike? We want houses. We’re just broke.

Mortgage rates, both new & refi, are influenced by, but not determined by, the 10-Year. At the end of the day, mortgage bankers are selling vegetables, and they must sell vegetables to survive. Mortgage bankers price their produce at rates that sell enough to survive at acceptable levels. God bless America. TFS

Mortgage bankers don’t have to survive…

All RE is local, but it costs much more to own and there seems no end in site.

Insurance is up for me 100 plus per month, new ac 16k. House is 12 years old and all updates and fixes will cost more.

Unless you are in one of the right areas, rent is not going up much. Perhaps people are getting smarter and see the american dream can be a nightmare and prison!

When you can work from anywhere, you have options and your money can earn real returns and not hopes.

Good friend who has much more money than most ducided to rent in a tiny town near me and drives an average car. Not everyone needs to show off like the wannabies. In his early thirties and smarter than most. He can walk down his street at 2 am and is safe! Can you do that in any of the good urban areas?

Perhaps many of the younger ones have watched the struggles of their parents and want no part of that prison.

A persons home is their castle. An oasis in a desert. Owning nothing isn’t happiness. Owning control of one’s life and purpose is happiness.

That’s a load of BS if I ever heard of one…or perhaps a gospel preacher for consumerism

either that or you forgot /s in your reply

Why is it BS?

I share Flashman’s sentiment regarding a sense of satisfaction that owning the roof over my head brings.

It helps motivate me to mow the lawn, shovel snow, and do all the other work that sometimes makes me miss renting.

ShortTLT, while i don’t disagree, and i enjoy owning my home, there’s another angle to your story: Renting instead of buying eliminates the need to mow the lawn, shovel snow, and do all the other time-consuming work required by homeowners. Those efforts can instead be put towards fulfilling things that bring people happiness and satisfaction, such as travel, hobbies, and spending time with family. Always 2 sides to the coin.

I own too many cats to ever rent…

Doesn’t seem like BS to me. I agree. It’s an oasis in an otherwise inhospitable desert of consumerism that’s trying to eat you alive. As you get older and have dependants for most of us you will want to control your costs of living the best you can. Renting and moving all the time is a bad trade off for having to mow the lawn.

Though maybe I just prefer death by a thousand grass-blade-cuts to the swift falling axe since it gives some semblance of control over my life in the meantime, oh and also something might change for the better while I’m being cut…

Robert

“As you get older and have dependants for most of us you will want to control your costs of living the best you can. Renting and moving all the time is a bad trade off for having to mow the lawn.”

This makes sense if you believe that the value of a house only goes up. If you buy a house during a bubble, it loses 50% of it’s value, and you lose your job, that’s not controlling your costs nor having control over your life. That is not a risk with renting.

Old Chinese saying,”toad in puddle knows not the ocean”. Toad goes back to puddle, doesn’t like ocean.

I do know some people who have taken a “cash-out refi” on their business properties to perform upgrades that they hope will increase foot traffic. That is a reasonable risk that I can understand (more competitive, more business, more income etc.), but why in the hell would any sane person with a < 3.0% mortgage give that up on any property? That's just stupid IMO.

Maybe they’re using the cash to buy more NVDA.

Been upgraded by analysts to $145! Woooo

They believe they can earn more than the 4% difference in the yields with the removed capital? They didn’t want a reverse mortgage for their last few years of life? They see the true value in a currency not being inflated by the feds and politicians?!?

Buyers strike waiting for Kamala fee money palooza

Speaking of lower prices on new builds and (partially) on fixer uppers – I wonder where that break even point is.

When I planned some renovation back in 2021, I was estimating flooring to be around 2-3k for the area I needed. In the end of 2022 I could not find anything less than 10-12k. Similar increase in most of the other stuff at Home Depot and Lowe’s.

With house prices poised to go down and prices for most construction materials still flying sky high, won’t it create a situation of razor thin margins for new house builders? I believe I heard 10-20% as a margin most builders operate at, and with Lennar already recently admitting they currently spend up to $40k per house in various perks, that sounds like we are quite close to the point where new construction may stop ot slow down if construction materials don’t go down in price? Am I looking at it wrong?

The Refin impact on the Fed’s MBS retirement and related QT is immaterial, isn’t it?

It’s immaterial to the price of cheese in Holland. It’s not immaterial to the Fed’s balance sheet or financial markets.

Yarg, I just camembert it, edamit..

…Gouda mean that?

may we all find a better day.

The ZIRP policy since GFC and the “transitory” delusion during the Pandemic has killed the American dream and turned it into the American nightmare so severe that the middle class is moving under a bridge, into a van in the wilderness, or killing themselves with fentanyl. Mr. JP and his counterparts lack the creativity (possibly the gonads) to bring the financial economy in alignment with the real economy. He would rather repeat the insanity of “can-kicking” that has only blown the problem to the current gargantuan proportions, while pretending to do something meaningful. The real answer is obvious: systemic, controlled deflation. Here’s how:

1). Keep the interest rate “higher for longer,” maybe crank it up even higher for a while to speed things up, so banks will start to fail.

2). In case of bank failure, re-initialize an “enhanced BTFP”: FED goes in with 6 months of “support” but manages the operations jointly (give it a nice sounding name such as “guidance” so they can maintain the illusion of independence, I don’t care, but enforce the tough measures).

3). Analyze and segregate the accounts in the spirit of the Glass-Steagle. Build a firewall and extend protection ONLY to the accounts transacting in the “real economy.” The ordinary Joe’s account. Let the gamblers and leveraged accounts fend for themselves. In fact, put the networth of the gamblers on the line in case of defaults.

4). Banks will undoubtedly blow up, but there won’t be any bank runs because the ordinary Joe will know that JP has got his back. Wall Street will panic and implode, but who cares if a few (or many) fake billionaires and the 15% that own WS go down. Just put their net worth to good use. Most of the 15% don’t even own much on WS anyway, so only the 5-10% (fake billionaires) will be the real casualty. And any fake wealth is actually leverage and illusion or delusion!

5). For the housing market: BTFP or the FED manages (gives guidance on) the mortgages of the failing banks (after the networth of the fake billionaires has been accounted for) to cause a fairly rapid, then transitioning into a gradual tapering deflation over the next 3-5 years, aligning housing costs (including rents) with incomes. The “enhanced BTFP” should have a provision of offering special one time low interest rate mortgage to verified owner-occupier buyers (=mortgage rate buy down). This would restore an important pillar of the American dream to the vast majority of the citizens and even boost household formation/aggregate demand. The “enhanced BTFP” program should ONLY protect existing owner-occupiers’ (ie. primary residences) if their home value is in the red from the deflation (no protection for AirBnB empires or Institutional empires devouring the American dream and the middle class). Their existing mortgages would be refinanced (maybe yearly) to the new market valuation as the deflation progresses so their monthly payments would come in line with and eventually stabilize when the devaluation is completed and we reach real market equilibrium. At that point the BTFP program stops, the FED denounces Alan Greenspan and promises NEVER to engage in interest rate repression again.

But who are we kidding. JP would rather shuffle the chairs on the titanic, and instead of restoring capitalism and democracy.

Would be very curious to understand the plumbing of the conflicting forces at play here – specifically, if lower rates speed up QT by way of MBS rolling off, and we know that the Fed taking on MBS artificially tamped down rates, how does a cut and continued QT on the MBS side actually impact rates? Is there a world where we see rate cuts but 10 year yield goes UP!?

The plan is to get rid of MBS from the balance sheet entirely. After the Fed ends QT, MBS will continue to roll off until they’re gone, but will be replaced by Treasury securities. So now, it’s just a question of how long this process takes. If mortgage rates drop a lot further, such as below 5% and stay there, those MBS will roll off at a fairly good pace, not only because of refis, but also because home sales volume will pick up again, meaning that homes with existing mortgages are sold and those mortgages are paid off, and the principal is passed through to the Fed (if its MBS had those mortgages in the pool).

This means that the Fed is withdrawing direct support for mortgage rates. It will just try to influence Treasury yields.