Housing CPI re-surged in July from the June outlier.

By Wolf Richter for WOLF STREET.

On a month-to-month basis, the Consumer Price Index (CPI) and Core CPI accelerated in July. Inflation in core services, which accounts for 65% of total CPI, bounced back from the outlier and re-accelerated sharply; food prices ticked up; energy prices stopped dropping; and durable goods prices slowed their historic plunge, according to the Bureau of Labor Statistics today.

It’s the historic plunge in durable goods prices that has done the heavy lifting in bringing inflation down this year. But durable goods prices aren’t going to plunge forever from the pandemic spike. Services inflation, though it has come down from the red-hot zone, remains high.

On a month-to-month basis:

- Core Services CPI: +0.31% (+3.8% annualized), acceleration from +0.13% in June.

- Durable goods CPI: -0.30% (-3.6% annualized), a slower drop than in June.

- Core CPI: +0.17% (+2.0% annualized), biggest rise since April.

- Food at home CPI: +0.13%, same increase as in June.

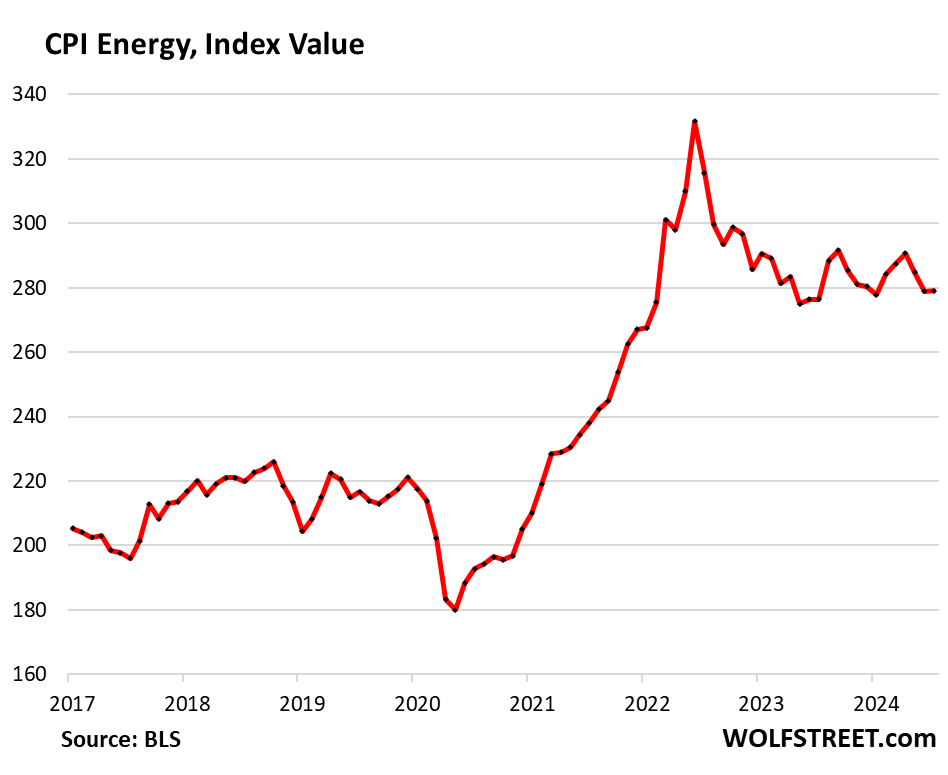

- Energy: unchanged, after the drops in prior months.

- Overall CPI: +0.15% (+1.9% annualized), highest since April.

On a year-over-year basis, in summary:

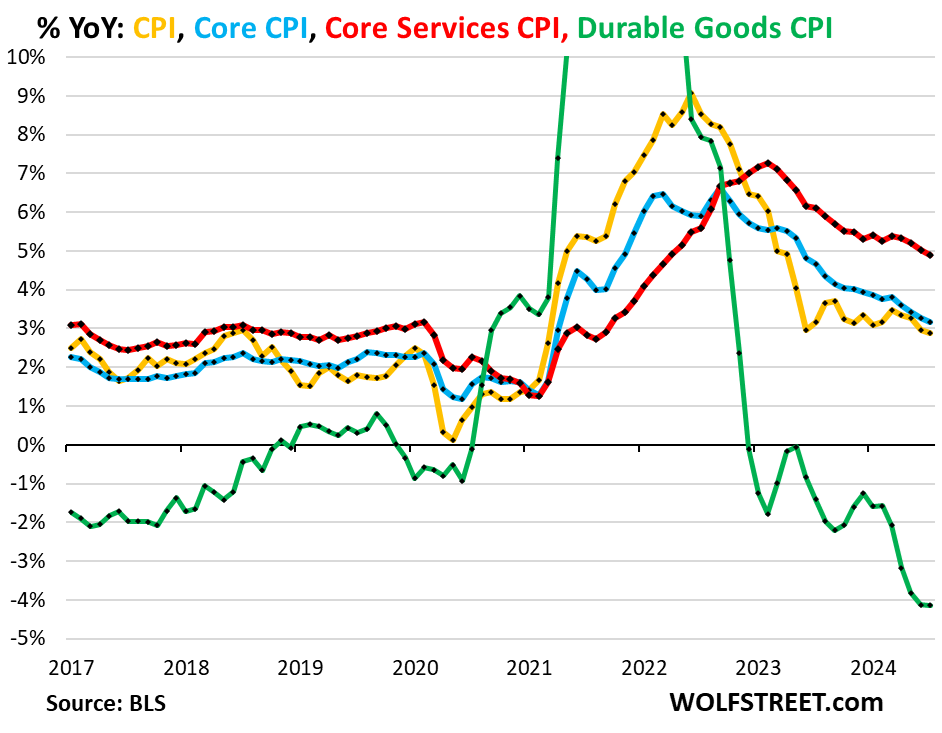

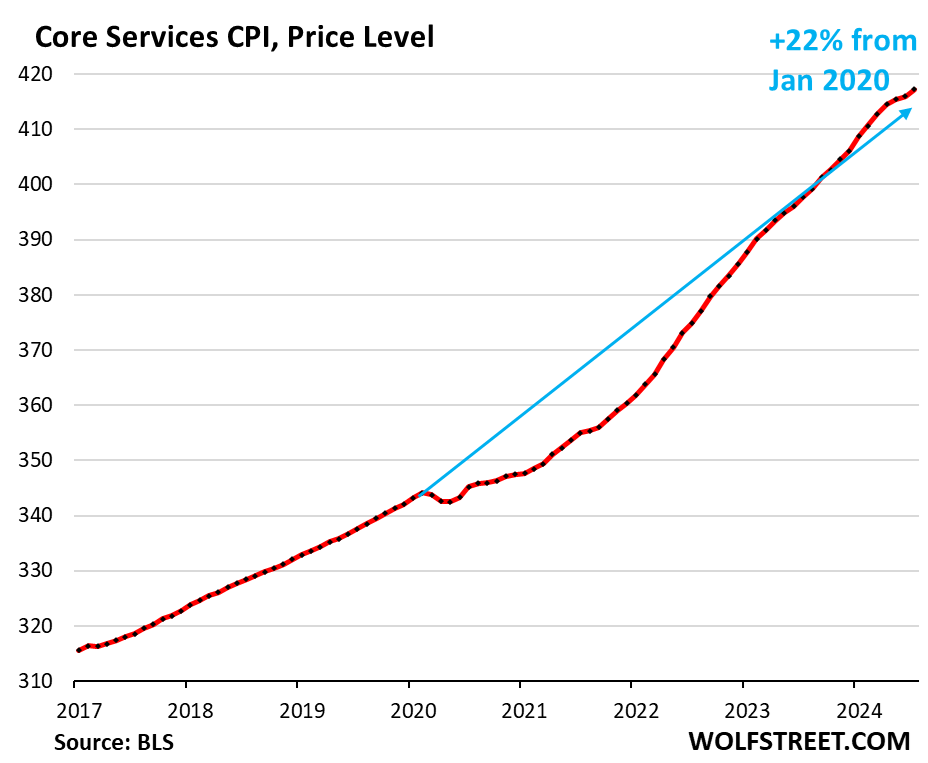

Core services CPI (red line in the chart below) rose by 4.9% year-over-year in July. It has been near the 5% line since December 2023. It includes all services except energy services.

Durable goods CPI (green) has been falling since mid-2022 to unwind the massive spike during the pandemic, led by plunging used-vehicle prices. In July, durable goods CPI fell by 4.1% year-over-year, same drop as in June, and the biggest drops since 2003.

Core CPI (blue), which excludes food and energy, rose by 3.2% year-over-year, continuing a slow deceleration, driven by the historic plunge in durable goods prices, while services inflation remains high.

Overall CPI (yellow) rose by 2.9% year-over-year, a slow deceleration from June. It has been in the same narrow range since June 2023.

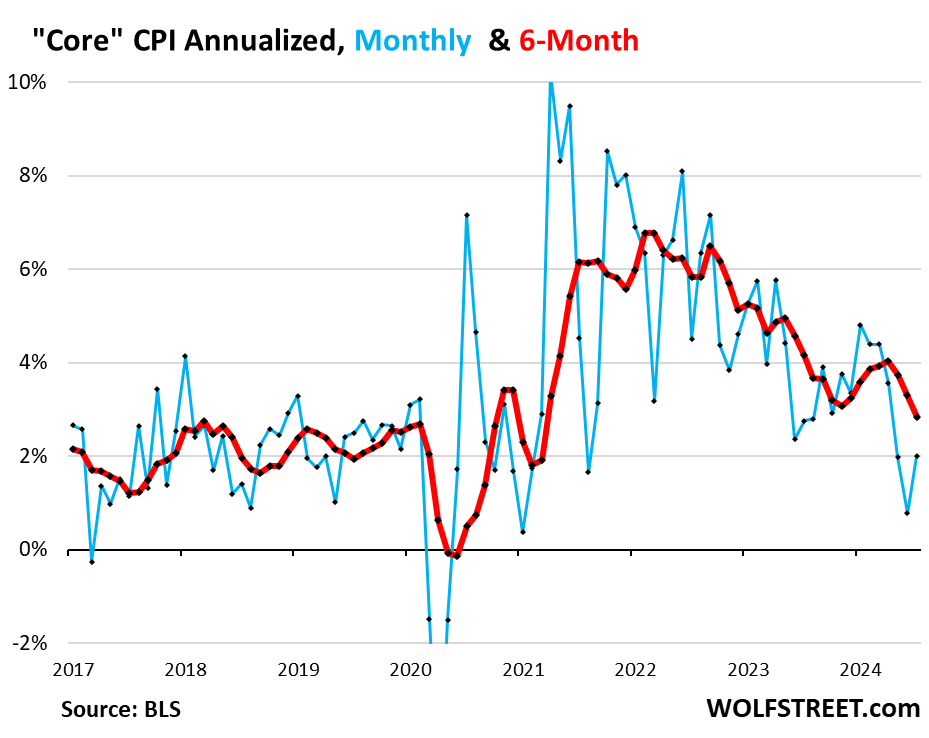

“Core” CPI, month-to-month.

Core CPI rose by 0.17% in July from June, or +2.0% annualized, the biggest increase since April, and an acceleration from June (+0.06%), which had been an outlier in the month-to-month squiggles (blue line in the chart below).

The increase in month-to-month Core CPI was driven by the re-acceleration in core services CPI. The durable goods CPI plunged, but at a somewhat slower rate than in prior months, pushing down core CPI somewhat less forcefully.

The six-month core CPI, which irons out some of the month-to-month squiggles, rose by 2.8% annualized, the third deceleration in a row.

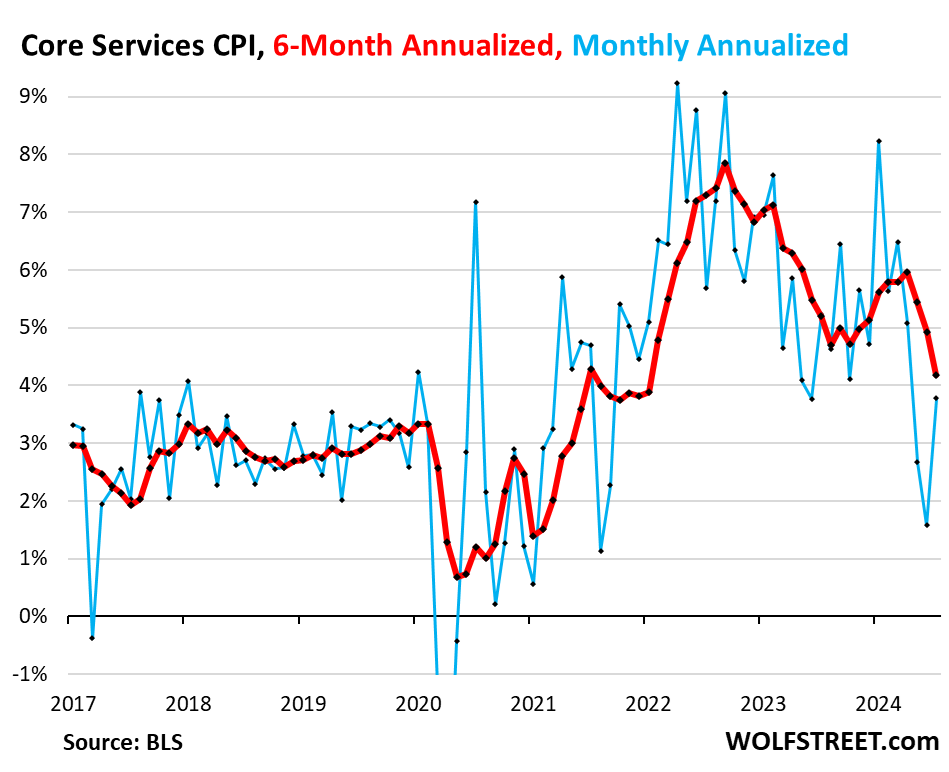

“Core services” CPI bounced back from the outliers in June & May.

Core services CPI increased by 3.8% annualized in July from June (+0.31% not annualized), a big bounce-back from the outlier in June and the highest since April (blue line).

The six-month core services CPI decelerated to 4.2% annualized, the smallest increase since January 2022, as the high outlier in January (+8.3%) fell out of the six-month period (red).

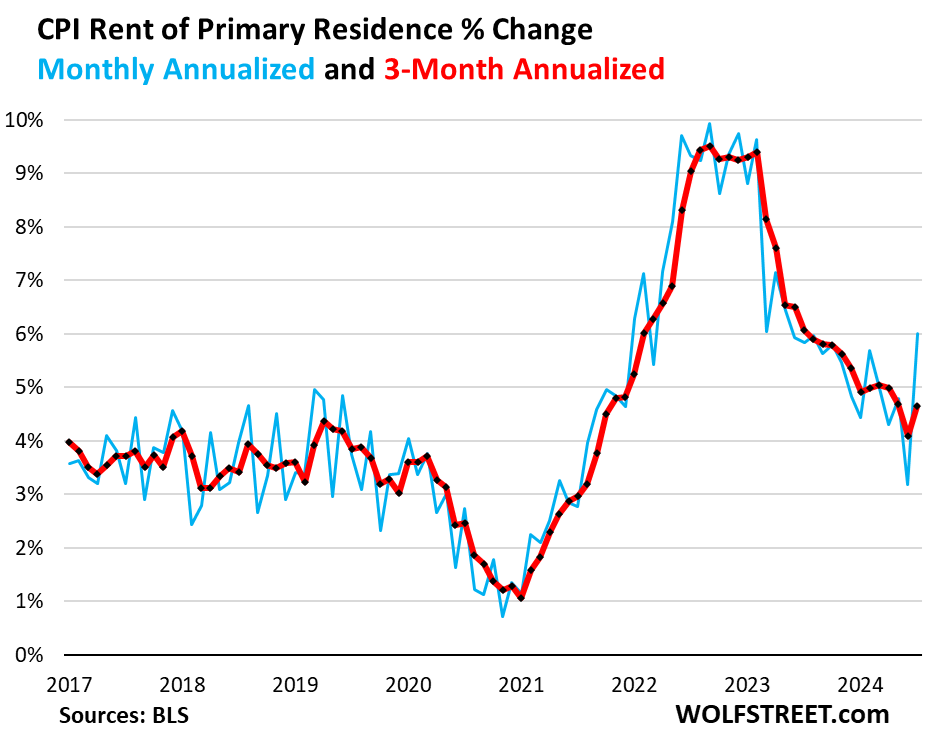

The housing components of core services CPI.

Rent of Primary Residence CPI bounced back from the outlier in June, and jumped by 6.0% annualized in July from June, the fastest increase since May 2023 (blue).

The three-month rate rose by 4.7%, an acceleration from June and back to the same rate as in May. In January, the three-month reading was 4.9%, so rent inflation really hasn’t cooled meaningfully this year.

The Rent CPI accounts for 7.6% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants, who come and go, actually paid in these units.

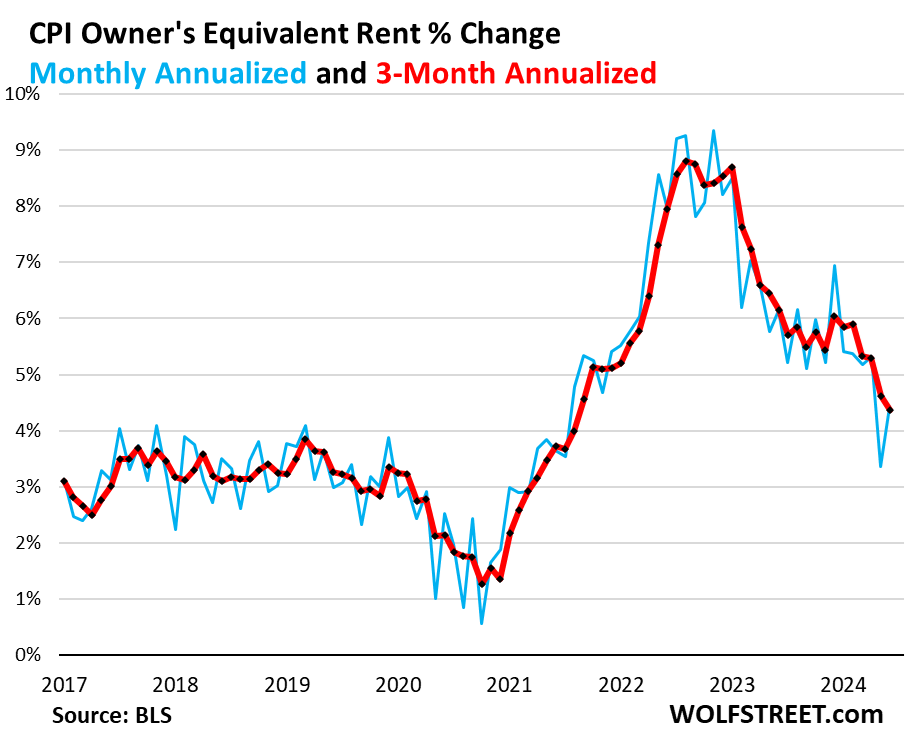

The Owners’ Equivalent of Rent CPI bounced back from the outlier in June and rose by 4.4% annualized month to month.

The three-month OER CPI also rose by 4.4% annualized, a further deceleration (red).

The OER index accounts for 26.8% of overall CPI. It estimates inflation of “shelter” as a service for homeowners – as a stand-in for the services that homeowners pay for, such as interest, homeowner’s insurance, HOA fees, maintenance, and property taxes. As an approximation, it is based on what a large group of homeowners estimates their home would rent for, the assumption being that a homeowner would want to recoup their cost increases by raising the rent.

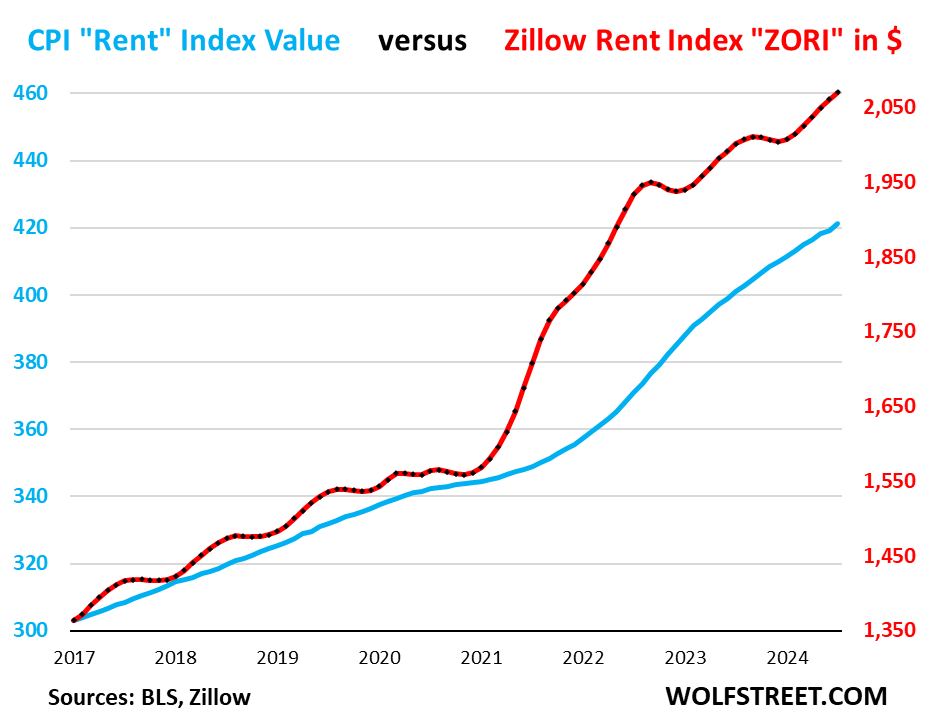

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. Because rentals don’t turn over that much, the ZORI’s spike in 2021 through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those asking rents.

For July, the ZORI jumped by 0.44% month-to-month, seasonally adjusted, and by 3.4% year-over-year.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 55% from January 2017. The ZORI was up by 50% from January 2017, and the CPI Rent was up by 38% over the same period.

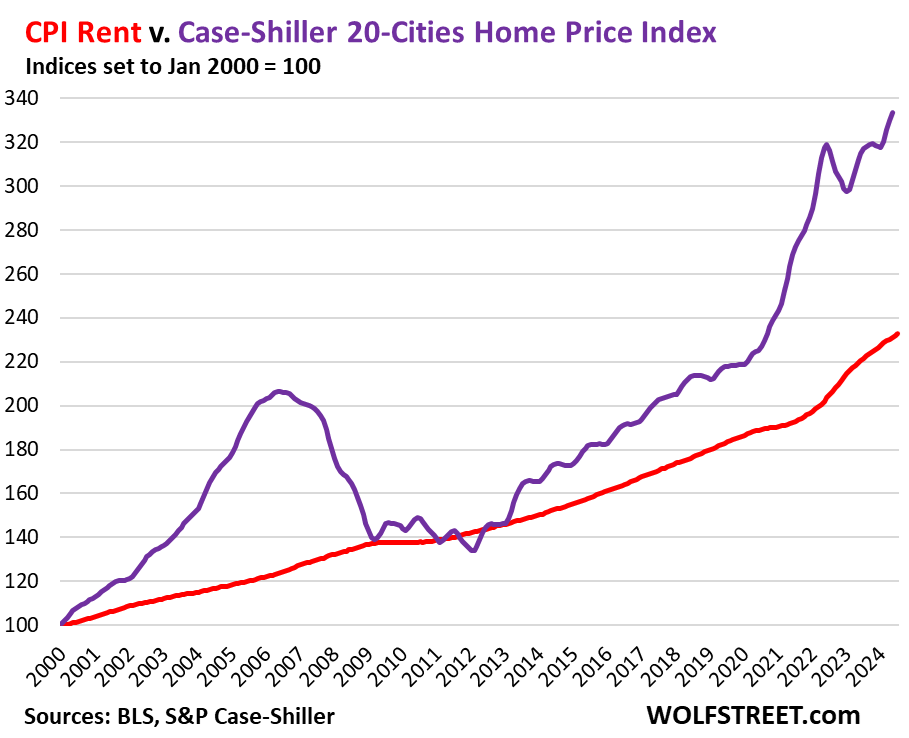

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence as index value. The purple line represents the Case-Shiller 20-Cities Home Price Index (which we use for our series, “The Most Splendid Housing Bubbles in America”). Both indexes are set to 100 for January 2000:

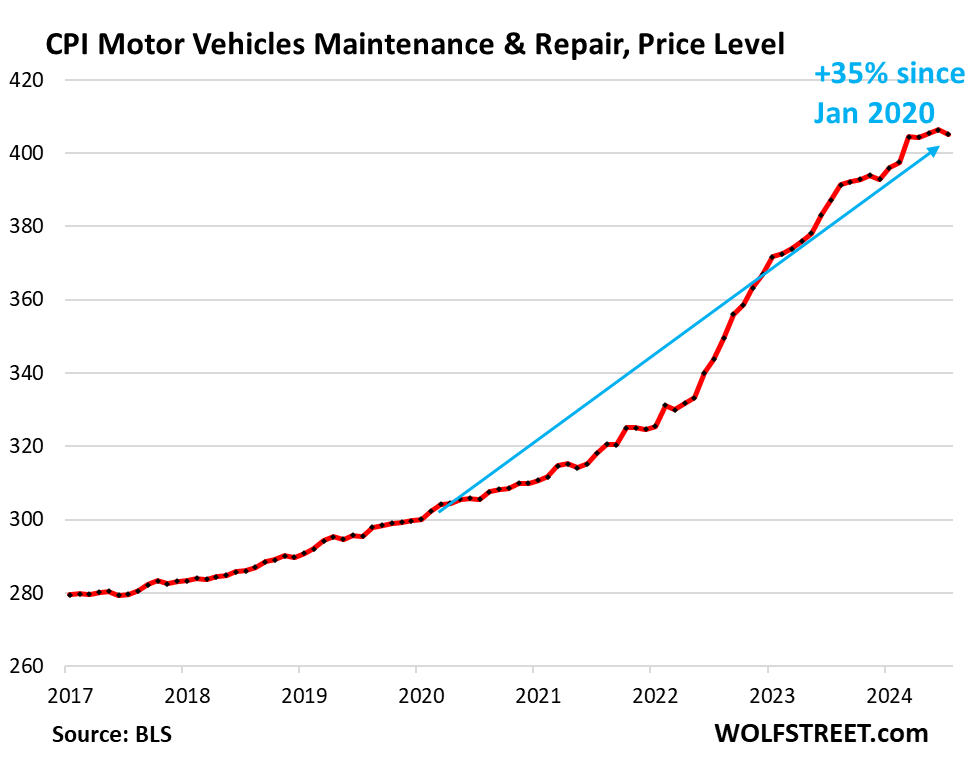

Motor-vehicle maintenance & repair inflation has cooled in recent months, after surging 35% since January 2020 because wages of auto-repair technicians had surged, and because prices of replacement parts had surged.

- In July from June annualized: -3.5%

- Year-over-year: +4.6%

- Since January 2020: +35%.

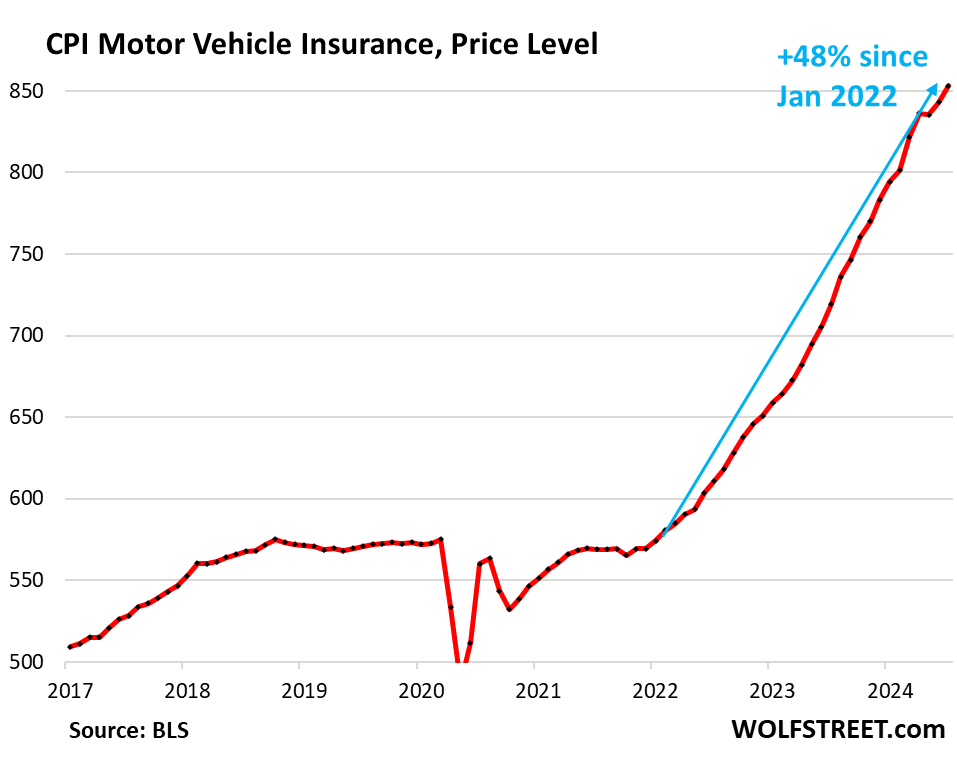

Motor vehicle insurance inflation continues to explode; it exploded in 2022 and 2023 because motor vehicle repair costs surged, and because used vehicle prices (replacement values) had exploded in 2021 and 2022, and because auto insurers wanted to fatten up their profit margins.

For example, Buffett’s Berkshire Hathaway reported for Q2 that operating income from the companies it owns rose by 15% to $11.6 billion, with almost half of that profit coming from its insurance empire. At GEICO, massive increases in premiums and reduced claims caused underwriting profits to more than triple!

And unlike motor-vehicle repair costs which have stopped rising over the past few months, and unlike used vehicle prices which have continued to plunge, inflation of auto insurance continues to explode:

- In July from June: +15.2 annualized

- Year-over-year: +18.6%

- Since January 2022: + 48%

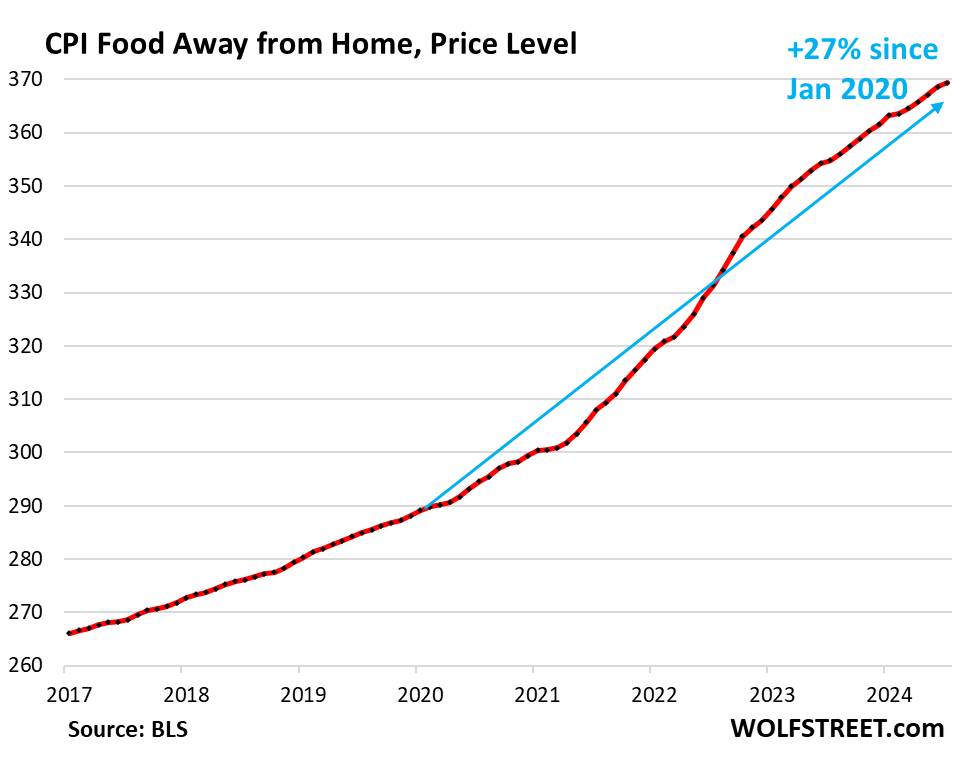

Food away from Home CPI – often called food services – includes full-service and limited-service meals and snacks served away from home, food at cafeterias in schools and work sites, food served at stalls, etc.

- In July from June annualized: +2.5%, a deceleration

- Year-over-year: +4.1%, same increase as in June

- Since January 2020: +27%.

Core services price level. Since January 2020, the core services CPI has surge by 22%. And it’s not just driven by housing, but very broadly: “Super core” services CPI, which excludes rent and OER, increased by 20% since January 2020.

| Major Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Core Services | 64% | 0.3% | 4.9% |

| Owner’s equivalent of rent | 26.8% | 0.4% | 5.3% |

| Rent of primary residence | 7.6% | 0.5% | 5.1% |

| Medical care services & insurance | 6.5% | -0.3% | 3.3% |

| Food services (food away from home) | 5.4% | 0.2% | 4.1% |

| Education and communication services | 5.0% | 0.2% | 2.2% |

| Motor vehicle insurance | 2.9% | 1.2% | 18.6% |

| Admission, movies, concerts, sports events, club memberships | 1.8% | 0.4% | 3.4% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 0.3% | 5.1% |

| Lodging away from home, incl Hotels, motels | 1.3% | 0.2% | -2.8% |

| Motor vehicle maintenance & repair | 1.2% | -0.3% | 4.6% |

| Public transportation (airline fares, etc.) | 1.2% | -1.2% | -2.2% |

| Water, sewer, trash collection services | 1.1% | 0.5% | 4.5% |

| Video and audio services, cable, streaming | 0.9% | 0.6% | 2.5% |

| Pet services, including veterinary | 0.4% | 0.3% | 4.9% |

| Tenants’ & Household insurance | 0.4% | 0.0% | 3.1% |

| Car and truck rental | 0.1% | 0.3% | -6.2% |

| Postage & delivery services | 0.1% | 0.7% | 5.1% |

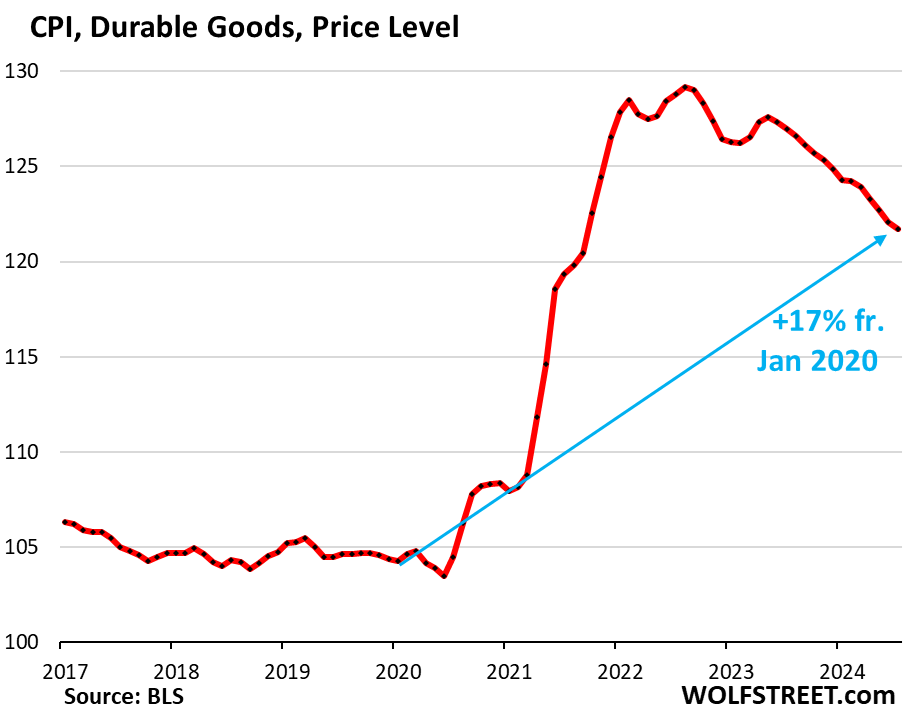

Durable goods CPI.

The durable goods CPI fell by 3.6% annualized (-0.30% not annualized) in July from June, and by 4.1% year-over-year, same drop as in June, and both were the biggest drops since 2003.

New and used vehicles dominate this index. Other goods included are information technology products (computers, smartphones, home network equipment, etc.), appliances, furniture, fixtures, etc. All categories have been experiencing price declines starting in late 2022, following the ridiculous price spike during the pandemic.

From January 2020 to the peak in August 2022, durable goods prices spiked by 24%. Since then, they have dropped by 7.1%, having unwound nearly one-third of the pandemic spike. Compared to January 2020, the index is still up 17%.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | -0.3% | -4.1% |

| New vehicles | -0.2% | -1.0% |

| Used vehicles | -2.3% | -10.9% |

| Information technology (computers, smartphones, etc.) | 0.6% | -6.7% |

| Sporting goods (bicycles, equipment, etc.) | -0.8% | -1.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.1% | -2.3% |

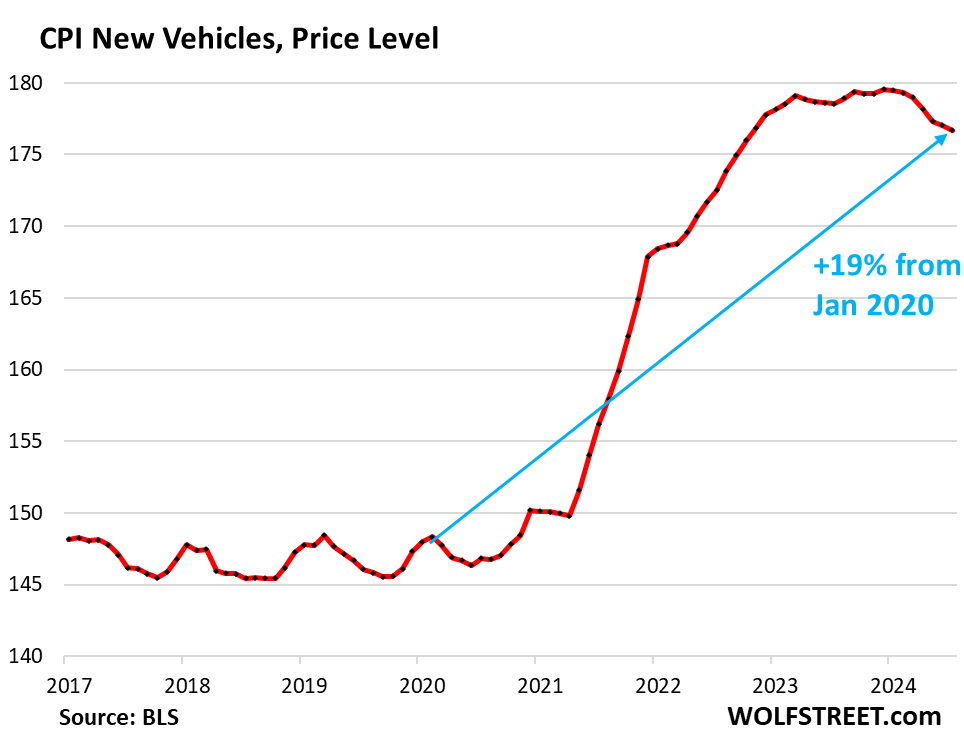

New vehicles CPI fell 2.3% annualized in July from June (-0.19% not annualized), the seventh month-to-month decline in a row. Year-over-year, the index fell by 1.0%.

After the blistering spike from early 2021 into early 2023, and then a long plateau, prices are now finally declining, amid a glut of new vehicles on the lots of many dealers that calls for big incentives and discounts to move the vehicles. The index is still up 19% from January 2020:

In the years before the pandemic, the new vehicle CPI zigzagged along a flat line, though vehicles were getting more expensive. This is the effect of “hedonic quality adjustments” applied to the CPIs for new and used vehicles and some other products (see our explanation of hedonic quality adjustments in the CPI).

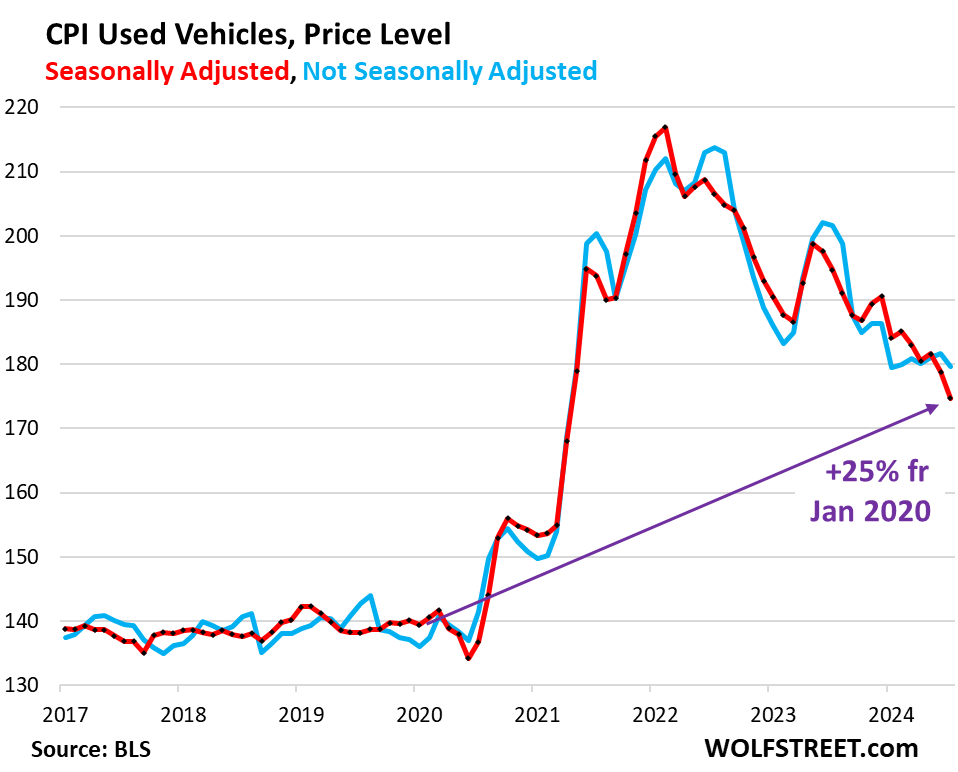

Used vehicle CPI, seasonally adjusted, plunged in June from May by 24.4% annualized (-2.3% not annualized), and by 10.9% year-over-year (red).

Not seasonally adjusted, used vehicle prices fell 1.1% annualized in July from June, after rising in the prior month, and have been roughly flat all year. It’s just that seasonally, used vehicle prices normally rise during the first part of the year into the summer, and this year, they didn’t rise (blue).

But now, which is concerning on the inflation front, the private-sector data on wholesale prices from Manheim, the largest auto auction in the US, already showed big price increases in July, as used-vehicle inventories have tightened and dealers tried to restock at auctions, and these wholesale price increases will filter into retail prices over the next few months.

Used vehicle CPI has now given up over half (55%) of the spike from January 2020 through January 2022, but is still 25% higher than in January 2020.

Food Inflation.

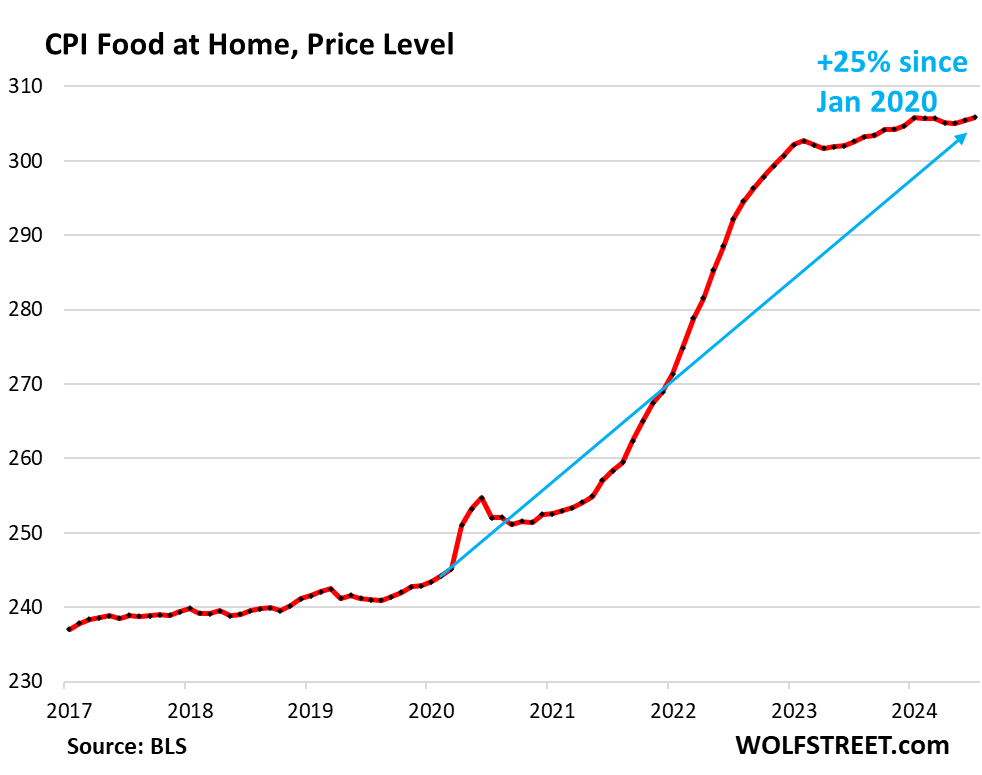

Inflation of “Food at home” – food purchased at stores and markets and eaten off premises – has cooled over the past year from the red-hot pace from 2020 into early 2023.

In July, it ticked up by 0.1% from June, and was up 1.1% year-over-year.

| MoM | YoY | |

| Food at home | 0.1% | 1.1% |

| Cereals, breads, bakery products | -0.5% | 0.0% |

| Beef and veal | 1.2% | 4.5% |

| Pork | -0.2% | 3.6% |

| Poultry | 0.2% | 0.9% |

| Fish and seafood | -0.5% | -1.6% |

| Eggs | 5.5% | 19.1% |

| Dairy and related products | -0.2% | -0.2% |

| Fresh fruits | 1.1% | -1.2% |

| Fresh vegetables | 0.9% | 0.4% |

| Juices and nonalcoholic drinks | 0.2% | 2.5% |

| Coffee, tea, etc. | 0.7% | 0.4% |

| Fats and oils | -0.6% | 3.6% |

| Baby food & formula | -0.3% | 4.6% |

| Alcoholic beverages at home | 0.2% | 2.0% |

The CPI for food at home is up 25% from January 2020, and prices, though not rising fast anymore, remain at very high levels.

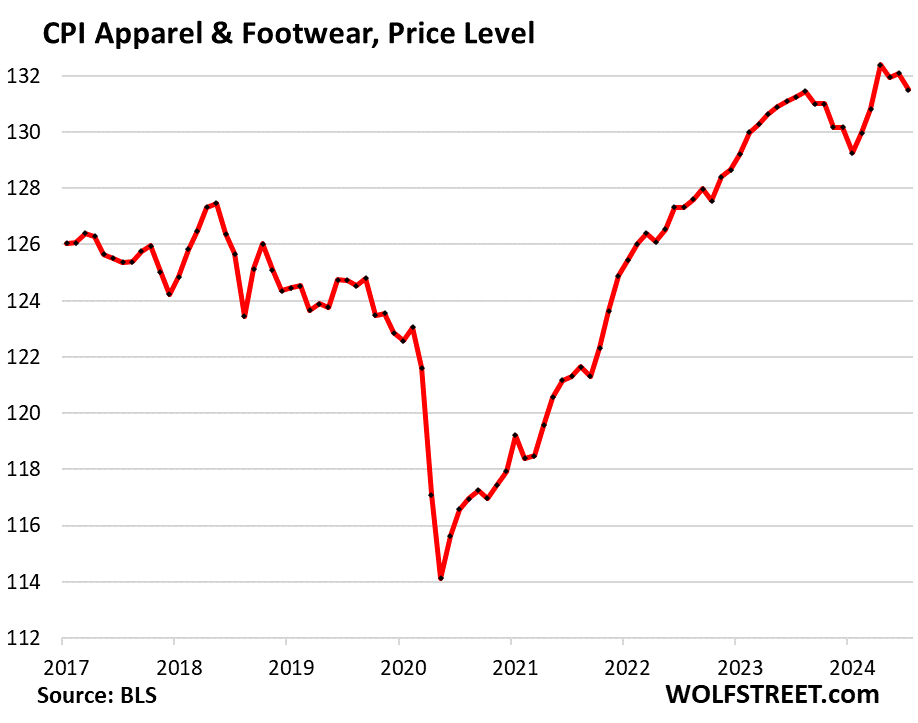

Apparel and footwear CPI.

Apparel and footwear are in the basket of nondurable goods, along with food, energy products, household supplies, and other stuff.

Month-to-month, prices ticked up 0.19% but were down 0.5% year-over-year. Prices had fallen during the early months of the pandemic as many stores were closed, then rose from that dip. Note that prices trended lower in the years before the pandemic.

For the past 12 months, prices ended up roughly flat, despite a drop and a bounce in the middle. In July, the index was 5.6% above July 2019:

Energy.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 0.0% | 1.1% |

| Gasoline | 0.0% | -2.2% |

| Electricity service | 0.1% | 4.9% |

| Utility natural gas to home | -0.7% | 1.5% |

| Heating oil, propane, kerosene, firewood | 1.0% | 1.9% |

The CPI for energy covers energy products and services that consumers buy and pay for directly:

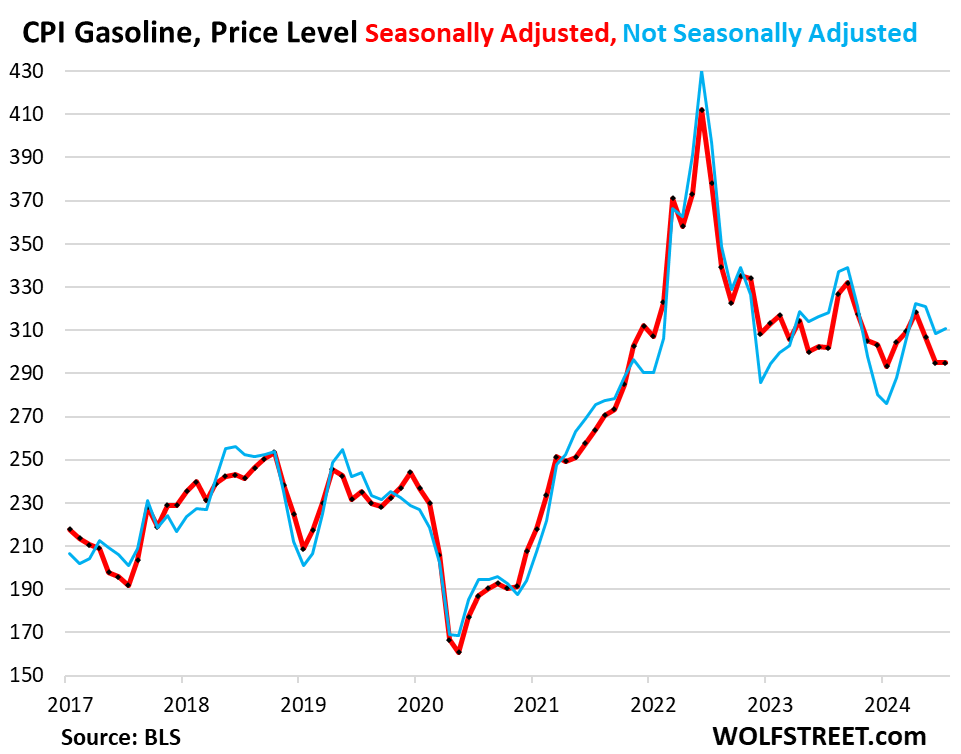

Gasoline prices, which account for about half of the energy price index, are very seasonal, with the lowest prices in December or January and the highest prices during driving-season which starts in June. In July, prices not seasonally adjusted ticked up from June, but in June, they’d dropped, instead of rising.

So seasonally adjusted, gasoline prices were essentially unchanged in July from June, after the plunge in June from May (red).

Since the top of the spike in June 2022, gasoline prices have dropped 28%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Does anyone have a good theory why Vehicle insurance costs have gone up so much since the start of the pandemic?

1. Are cars on average 48% more expensive than now?

2. Do we have more claims?

3. Are repair costs much higher now due to services inflation?

Or is the big component just pricing power of insurance companies?

Thanks in advance.

🤣 RTGFA

Your answer is in the article, which says verbatim quoted from the article:

Motor vehicle insurance inflation continues to explode; it exploded in 2022 and 2023 because motor vehicle repair costs surged, and because used vehicle prices (replacement values) had exploded in 2021 and 2022, and because auto insurers wanted to fatten up their profit margins.

For example, Buffett’s Berkshire Hathaway reported for Q2 that operating income from the companies it owns rose by 15% to $11.6 billion, with almost half of that profit coming from its insurance empire. At GEICO, massive increases in premiums and reduced claims caused underwriting profits to more than triple!

And unlike motor-vehicle repair costs which have stopped rising over the past few months, and unlike used vehicle prices which have continued to plunge, inflation of auto insurance continues to explode:

Maybe I should just post the entire article in the comments so that people who only read the comments will read it?

Take it a step further – post the article *only* in the comments.

This might work. ;-)

Per recent Fitch ratings report (I paraphrase), the recent highly improved auto insurance profitability could lead to flattening of price increases going forward, and improved profits will eventually lead to competitive pressure and resistance from policyholders and regulators for further price increases.

> Maybe I should just post the entire article in the comments so that people who only read the comments will read it?

With the article just a simple RTGFC?

Haha

So Mr. Buffett is fleecing insurance customers…although indirectly.

Pretty directly, Buffet also owns General Reinsurance Corporation.

This old man is anything but kindly. He is a cancer upon society and should be stripped of his entire fortune. He IS the disease which is destroying the very fabric of the US.

I encourage anyone who doesn’t know what “Reinsurance” is to Wiki it and LEARN. The “business web” is a complex one.

The comments have value. Don’t forget who “curates/or tolerates” the commenters”.

Then thank Warren.

i read the other day that the norwegian sovereign wealth fund (try saying that outloud 3 times fast), has hit over a trillion doelars in value and owns 1.5% of every publicly listed company in the world!

forget buffet’s 200 billion plus dry powder, forget blackrock, norwegians own the entire publicly listed world! if there is a company listed in dubai, they own 1.5%of it, a company listed in hong kong, nyse, south korea, paris, you name it, if its publicly listed, they own it.

i dont mind, until norway bought svalbard from denmark and then found oil and gas, it was like….finland or worse even…so good for them!

drill baby drill! anyway, i lost my original point;

point is: all i know is gas is up, rents are up 35 months in a row avging .4%, all prices up for more that 4 years, or 50 consecutive months….thats all i know,

the rest is the telescreen telling me how many shoes the government made last month…as nobody has any shoes.

One of a million examples of how a flat tax simplification of the taxing policy in the US would implode and eliminate a vast web of “business” in the states. You could replace business in the in the former statemnet with “excess fat”, “corruption, or “exploitation and net the stame meaning.

Harding, not that sick evil old man.

everybody wants to fatten profit margins, but over time, shouldn’t competition in the space lessen those margins?

nature abhors a vacuum. if the insurance companies keep raising premiums and profits, someone will jump in to be more competitive.

You’d think. But during an inflationary environment, with only a few big players in each market, that’s not yet the case apparently.

Obviously, they cannot raise by too much forever, but they can raise by a lot for a long time.

The one thing about auto insurance that makes it more monopoly ish I feel like, is we are required to have it. If I own my home, I don’t have to insure it. Can’t say that for my car. So Geico wins . To avoid getting scammed I just have to hope competition comes to keep pricing down, but if they are all a big cartel who work together, they can maintain high pricing because people can’t opt out.

Frank G,

This is one of the great lies of capitalism. Those with more capital squeeze the others out and the laughable expectation that government, who is in their pocket and owned by them, is also believed. Diapers are another example of this. Might look like tons of options but two companies, Kimberly Clarke and Procter and Gamble, control it all. The disease is the system as the system by design works this way and people are forced to participate to stay alive. When I was at Intel, before it became a mess of a company, it liked that AMD has miniscule market share because it was all that was needed to charge ridiculous prices for highly processed silicon.

To Franz G and Glen, The problem is not capitalism. It’s neoliberalism, that narrowly distributes power and prosperity to a tiny minority. It’s an extreme cut-throat form of capitalism that has produced many ruinous outcomes for America and the world. Other forms of capitalism exist where a more regulated form of capitalism that widely distributes power and prosperity. Some call it social democracy (Acemoglu & Robinson, 2012, 2019) and others call it Progressive Capitalism (Stiglitz, 2024).

Blake of course you need insurance. If you are stupid the state doesn’t want to have to recompense victims.

Also insurance could cover a lot in the event of stupidness and not deduct from your paycheck forever.

It’s a pretty cheap shield tbh.

I recall from my ancient Econ101 class of the late ’70’s the term: ‘Oligopoly’…(in context of a business segment’s number of competitors declining to a point that renders opportunities for capital entry providing new competition generally unattractive, which keeps the existing players clear of the ‘monopoly’ tag, or being classified as a ‘public utility’…having your revenue origins reinforced/’regulated’ via public mandate puts questions to this definition, though…).

may we all find a better day.

I apologize. I did read the full article.

What I really wanted to ask was whether someone had actual data on what % of that 48% is attributable to cost increases (vehicle, repair etc.) and what is just plain corporate greed. Increasing prices because they can due to industry consolidation.

For example the cost of paint has increased nearly 2x+. But the input cost for producers likely hasn’t.

The input prices have now actually dropped too

OK, I gave you the charts and data for repair costs and for used-vehicle prices (replacement costs if vehicle it totaled). So you can see how they surged. So you have those two. I also gave you an indication of what GEICO, a giant in auto insurance, is doing in terms of margins. Repair costs flattened out (see chart), replacement costs have plunged (see chart), but auto insurer margins have now shot up because their costs went down while they kept raising their premiums (see chart). It’s all there in the article.

If the repair techs at the shop need a 50% raise in order to not quit, does that count as an input cost rising?

Last year, our brand new car got destroyed in a storm one month after we purchased it. Geico estimated the repairs at $6K, it actually cost $16k. They still owe us a part for the car.

That storm damaged almost every house in my neighborhood. Almost every roof got replaced, including the one on our rental which had been replaced two years before.

During those months the restaurants in my area were full all the time. The money was visibly flowing. Not so much now.

> “what is just plain corporate greed.”

In econ terms, competition would be driving prices down. If it is not, for a sustained time, there is some kind of effective combination or conspiracy in restraint of trade (this is the law’s language from about 1900, not a conspiracy meme). In event of such a market failure, the remaining umpire (government, law, enforcement) is supposed to be policing it. It is called antitrust law. Our recent wild charts may suggest this market failure (i.e., just greed and not being held accountable this way) is not the cause, but by now it might be. Both parties are arguably on the take, but one is completely dedicated to zero antitrust enforcement.

Canada’s transition to electric vehicles (EVs) will cause insurance rates to rise, according to Morningstar DBRS.

In a commentary released this week, the credit rating agency cited the country’s new Electric Vehicle Availability Standard and how it is likely to impact auto insurance rates.

Morningstar DBRS noted that rate increases are to be expected due to EVs’ higher price tag and repair costs.

https://www.insurancebusinessmag.com/ca/news/auto-motor/transition-to-electric-vehicles-will-cause-insurance-rates-to-rise–morningstar-dbrs-476861.aspx

EVs are now cheaper than ICE vehicles of the same category. Tesla Model 3 competes directly with with BMW 3-series (near luxury performance rear-wheel drive or AWD sedans).

Only morons would compare the price of a Model 3 and the price of Corolla.

It’s ICE vehicles that have gotten more expensive, a LOT more expensive, while EVs have gotten less expensive. $100k pickup trucks are now fairly common! There are very few $100k EVs out there.

You see, the anti-EV bullshit never ends.

Wolf,

TBF, profits at GIECO had been hammered and were greatly reduced the previous few quarters from what historical norms were, so a tripling of profits from a reduced level isn’t as dramatic as it seems.

Auto insurance costs are just a delayed reflection of a combination of auto replacement costs and labor. As you know auto replacement costs have been on quite the roller coaster ride the past 5 years and labor has been getting really expensive so auto insurance costs are going to reflect those roller coaster rides as well. Like many markets, COVID brought huge dramatic swings to the market for cars, and that is still being reflected in the auto insurance markets as the insurance companies adapt to those big swings.

In reality, auto insurance is generally one of the most competitive markets in the world, so outsized profits over a long period of time isn’t really possible.

Funny thing, I just realized that I’ve never read a comment complaining about GEICO’s under writing losses? Or any other insurance company for that matter.

But I am curious, what is the proper profit margin for an auto insurer……………….and who gets to decide?

Found the guy who works at GIECO LOL

Kile, in most of the US, the state government gets to decide and cap rates. Insanity.

Kile.

The market decides. Auto insurance markets are fairly competitive. A handful of big players nationwide (Gieco, Progressive, State Farm, Allstate) and a bunch of regional players.

Also, you are making an argument of ignorance (I have never heard so therefore it must not exist). That is not a very good form of argument.

Mr Harding,

Some people can learn and become a better person. Some can choose to remain ignorant and make snarky comments.

I see you have made your choice. Too bad.

I also see blame placed on the higher-tech nature of cars, but don’t know how true that is. You hit a bumper … instead of replacing just the bumper, you now replace bumper + lots of sensors, electronics, etc.

I’m in insurance and no one ever peels back the hood on how f**cked everything is.

These companies make long term investments in financial instruments over long periods of time. Money was basically at 0% so they were hiding money everywhere. Alot of profit taking, but also trying to sweep those unrealized losses under the rug.

But that has been going on for decades. It didn’t just start in early 2022, when insurance premiums began to explode.

The Swamp is contributing to the explosion in insurance premiums. I have a lawsuit against Geico, the most crooked insurance company in the USA. They are corporate scum. They are the insurance company for a hit & run driver who nearly took us out last November. Still paying the medical bills from the accident. I told my junkyard dog attorney not to accept one dime below $100K, and to go to court if necessary.

My theory is that insurers are taking huge losses on real estate investments, and the money has to come from somewhere to shore things up. The Fed Financial Stability reports have (incomplete) data on lots of interesting dark corners.

JeffD,

You’re talking about life insurers and reinsurers, etc., that sit on huge amounts of capital. We’re talking about auto insurers. They don’t have those kinds of capital requirements. Specifically, we’re talking about GEICO, which gives all its available capital to Buffett to invest in stocks, T-bills, and companies.

Big part of that was they were raking in cash during the pandemic. With everyone locked down they were competing on price, swimming in money(low claims). Then reopening and everyone went out playing bumper cars. With less free money sloshing around private equity starts looking for tidy margins. They buying up third party nuclear verdict lawsuits for some serious moola.

Add in the deceptive and careless nature of our degenerate culture along with severe climate weather events….

Yicky

Anecdotally, even basic stuff like transmission, differential, and power steering fluids for my 2011 have gone up – and I change those myself.

Not sure how long I’ll be able to get 10 QT of 5W-30 for $39.99 at Costco but I’m glad I shopped around – the local Autozone charges 50% more!

Short TLT, you ever tried replacing the lithium in an EV?

It’s shocking how hard that process is.

⚡️ 🥁

Hah nice pun

sufferin’ – …there needs to be a better rimshot emoji (but appreciate it all the same…).

may we all find a better day.

Not my experience. I backed into a pole denting my fender and gate on my RAV4. $500 or so for parts and $7500 for labor. Removing, painting and replacing is expensive and manual effort. It does seem like car design and such could make this of a Lego exercise but not my field.

Is that a typo and you meant 750? Because 7500 is insane unless you were going 75mph while backing up.

Or they know you’re dumb and are charging you accordingly.

$7500? Is that a Ferrari RAV4? For that much, probably total loss the car unless your RAV4 is brand new…even then $7500 labor, let’s say at $120hr rate, they need 60 hours to fix a dent? just wow

That was about 100 hours of labor at $75hr. I paid $500 deductible. Go back into a pole and try it so we have some solid comparisons. This was California so other states would be less but the point is cars are mostly built with automation and efficient processes. Repairs are none of that.

So 2.5 weeks of labor and $500 in parts, yeah I’d say they saw you coming from a mile away. If there was as much damage as the amount of labor implies, I would expect a much higher cost of parts.

Is your last name Close? ;)

Unclear on your need to make this a personal attack. I paid $500 total and given my tailgate wouldn’t open that is necessary. If I didn’t have insurance I certainly would have shopped around and perhaps it would have been 4k. Almost everything is a scam of a sort where insurance is involved. When I needed an MRI my insurance would have been billed $2,500 but my deductible was 8K so I lied and said didn’t have any got the cash price of $500. Same deal for blood tests.

Cmon we all know how expensive body work is.

Glen, I’ve had much the same experience with insurance and medical. A switch in plans when I left my employer, left me without a Primary care physician. What a blessing. I have fallen through the cracks in the medical/insurance system. Without the primary care physician, I don’t qualify and keep getting everything at a huge discount. The medical system in the area keeps scheduling me an initial appointment to get a primary physican, but months out. I keep missing it and raking in the savings.

Sports entertainment which all professional leagues are classified legally allows the scripting of all games akin to WWE with paid actors with no recourse to the losing bettor on said scripted outcome…sound like walled street…

ohhh come on, the chiefs really are that good! :’)

lol

The simple answer is because the PSC’s that govern their rate hikes are letting them get away with it. Absent a recession, they’ll continue to get away with big rate hikes. In GA, Allstate raised rates 25% simply because there was a loophole in the state law that let them get away with such a HUGE rate hike. I have no idea if the GA legislature closed the loophole. It’s as much oversight as it is anything else.

Part of it is that cars have more electronics which are a big part of the increase in repair costs. Second has been the epidemic of stolen cars. In the small city where I work, Buffalo (4 months a year, I don’t have. car there) in a city of 240,000 there were 1,650 cars stolen last year. 5X that had windows smashed in.

Post George Floyd riots have not resulted in a drop in car crimes. They have been persistent and costly. Criminals have ben emboldened because they know they won’t be prosecuted.

Over at my fave insurance industry site, companies have been pleading losses for several years running now. Hence their pulling our of some markets where regulators won’t let them hike rates enough.

I’m sure the C Suite execs in these companies that are bleeding dollars are taking lower salaries and eliminating bonuses, correct?

Because it is a forced service, it’s a no brainer that the inflation train is easy to direct when it’s locked on rails. There’s money everywhere and therefore it’s worth next to nothing so collect it thru various insurance scams, ‘natural’ disaster, health disaster, negligent or uneducated ‘homeowners’ and renters, large concentrations of immigrants in high density areas running into whoever gets in the way of their way because they can’t read the signs. Plus we now have municipal dumping millions dollar budget per mile of road on cameras because cameras make the roads safer while car size potholes and various basic maintenance or design goes neglected while car after car get destroyed or cause a pile-up. This is all clown world 101 stuff or more specifically clown car stuff.

YML – …again a redux of The Firesign Theater’s observation that: “…we’re all bozos on this bus…”.

ma we all find a better day.

The cost of repairing and refinishing a vehicle has skyrocketed. The major coatings companies that sell paint to the body shops were already having 7% annual price increases before 2020. (PPG brags every year volume is down but they made it with price increases.)

Then they started having 10 and 12% price increases. A gallon of Torch Red basecoat in the best tier of coatings a company makes can cost $1500 at full retail. The best clearcoats these companies make (not that the body shops use the best) are $750 for a 6-quart setup.

Now, look at vehicles. Every corporate and personal vehicle I own has lane departure, parking sensors and cameras, radar cruise, and some type of LED headlight that automatically adjusts and moves as I drive and turn. A minor deer hit to one of my vehicles would take out 2 $1200-1400 headlights, god only knows what kind of sensors in the bumper, plus the bumper, grill and hood. That’s before labor and paint.

And State Farm still insures these vehicles for $900-1100 a year. I wouldn’t insure these vehicles for that. I live in a very low crime area, don’t have tickets, and haven’t filed claims.

I have been following car insurance and I think there are some clues.

1) New cars are much more expensive than they were 10 years ago.

2) Repairing newer vehicles is much more expensive, both parts and labor.

3) People, for whatever reason, are in a greater hurry and more reckless on the road – this raises the prices for everybody.

4) Insurance companies regularly run complex computer models with sophisticated algorithms to determine risk and adjust premiums.

Insurance companies are in the business to make money and not lose money. I live in Florida and I can tell you first hand about people getting dropped for car insurance, home insurance and other insurances. Climate change data is finally being entered into those sophisticated computer models. Cheers.

Climate hasn’t changed much in Florida. Just more people living in the path of possible hurricanes and flooding. The population there has exploded the last 40-50 years.

Not the eggs again!

Eggs rule, great for you and tin foil, actually it’s aluminum foil these days has numerous applications besides wearing on one’s head looking at all the cooked numbers via 1984

Tin catches those signals best. Filters out the noise.

So inflation’s trend is still higher and higher but the Federal Reserve is still hell bent on cutting interest rates. I guess we will see much high inflation, interest rates in the end of 2025, beginning of 2026.

These moron finance reporters *think* the Fed is hell bent on cutting rates… but I don’t think the Fed actually thinks that.

WS must have forgot or gaslighting themselves into thinking this isn’t really the positive news for their Sept rate cut narrative, seems like they are jovial at this point no matter why. Best winning strike over the last 4 days…nah, we still need another emergency rate cut please….

Gaslighting and empires are peas and carrots…choose your poison carefully as all is the entertainment field with a fraternity of actors in high places…I wonder if the English have paid off their 1.6 billion pounds in debt from the napelonic wars?…don’t drink the tea, stay natural and fear Greeks bearing gifts…all is upside down…

well i have this to say… “I AM NOT ENTERTAINED!!”

1:04 PM 8/14/2024

Dow 40,008.39 242.75 0.61%

S&P 500 5,455.21 20.78 0.38%

Nasdaq 17,192.60 4.99 0.03%

VIX 16.31 -1.81 -9.99%

Gold 2,484.50 -23.30 -0.93%

Oil 77.15 -1.20 -1.53%

US National Debt: Over $35.15 trillion

Interest on debt: over 1 trillion (3rd largest expenditure)

This is what has taken to drive up the stock market. How long do you think it is sustainable?

Not much longer IMO.

Between inflation spikes and that debt rates are going up long term.

That’ll cause a debt spiral I’d think

Suez crisis 1950’s — the Brits got their financial and geopolitical wake-up call after decades of trying to ignore the signals. What are they now? Bulgaria with financial casinos and nuclear weapons. Not even as many pubs, anymore. They drink at home.

The narrative about debt being unsustainable is now about 40 years old. Not suggesting it is sustainable but predicting the point at which it isn’t is missing the damage it does all along the way.

Maybe so but the interest on 35 trillion is a bit bigger burden then the interest on 500 billion… So unsustainable nearing a tipping point… Within ten years I’d say is more then reasonable to assume the damage done is felt by the ones doing the damage🤞

American Dream,

I think you need to define unsustainable in real terms. My unscientific term is declining quality of life and purchasing power for Americans since clearly we can always pay our bills. The disappearing of the middle class is a vague notion but it fits in with either increasing taxes, fewer services or inflation and so on. I’m honestly rooting for it because things have to get worse before people get off the sidelines and demand real change. By that point however the hole is super deep. MLK probably said it best.

“because motor vehicle repair costs surged”

THIS. Yours truly is good at turning a wrench so I am interested in this topic. Know quite a few folks who have traded their BMW and Benz vehicles since they could not afford the maintenance anymore. Germans make great cars but many models break down lot. For example, someone had to spend 18k in two years just to maintain a Mercedes GL 550 (engine timing chain, transmission, tires, air suspension, electronics, etc.). Same thing with Volvos and VW cost of ownership.

Newer cars are very hard to work on and it take hours just to replace simple things like an alternator. Once the warranty is over it is really over. I recently saved 3k in labor just by replacing the struts and some power steering components myself.

I truly hope Jay Powell’s car breaks down and he has to take it to the mechanic himself.

he bike rides to the office daily. I’m certain they have a family car…likely leased if I had to bet.

i was with you on everything until that final sentence..

do you really believe that guy actually drives anywhere himself?? id expect the fed chair to be fully motorcaded/escorted at all times, given the potential risks to their person.,

that said, it is highly doubtful the guy will ever see a repair bill.. and if he ever did, there is no chance it would have any epiphany inducing effect, as you suggest/hope for. ‘concerns for thee, but not for me…’ to put a spin on the saying, i believe sums it up nicely..

come on man!

Good comment John. Happy motoring can be summarised in 2 words: Toyota and Honda. I suffered painfully with my Audi and M. Benz, BMW just as bad. BMW take huge profits back to Germany from their very expensive spares to subsidise lower new car prices and the others are probably the same. My Honda motorbike dealer also sold Renault cars, when asked why he wants to sell rubbish like that he said they make most of their money from their workshop. A new engine needed under warranty after 3 months? Fantastic for them, the more the merrier.

“Happy motoring can be summarised in 2 words: Toyota and Honda.”

Yup, the Japanese do it best.

Not sure about anywhere else, but in New England, 90% of the old (15+ y/o) cars on the road are one of six models: Civic, Accord, CR-V, Camry, Corolla, or RAV4.

I think it vile what the car manufacturers did: force-marched us to overbuilt and over-engineered products, smartphones on wheels. In concert with tech enablers. Worst antitrust violation ever. Money extraction units. Talk about gutting a (captive, former) middle class.

phleep – methinks you may be underestimating the knock-on effects of smart-phone/rideshare culture on the old auto-culture paradigm (don’t care for it, personally, but phone ‘enthusiasts’ now vastly-outnumber motorheads IME…best.).

may we all find a better day.

“On a month-to-month basis, the Consumer Price Index (CPI) and Core CPI accelerated in July.”

Headlines everywhere: Dow Rises As Inflation Cools

People see what they want to see, as always.

See no inflation

Hear no inflation

Speak no inflation

WS sees lowest since 2021. You see acceleration. Pick your narrative. Truth is probably somewhere between permabulls and permabears.

“Truth is probably somewhere between…”

Nonsense. there are 2 common ways to express the data, and 3rd less commonly cited:

1. month-to-month which accelerated quite a bit;

2. year-over-year, which adds up the last 12 month-to-month changes, and which decelerated a little.

3. 3-month or 6-month rates (the Fed uses them, as do many others) which iron out some of the month-to-month squiggles without getting totally lost in the 12 months of changes.

The article here uses and charts ALL of them.

RTGDFA

You just made my point. Thank you.

LOL, your point is comical, perhaps RTGDFT instead. Did Wolf scare monger that everything is accelerating? what a joke

“Beneath the Skin of CPI Inflation: Broad Month-to-Month Acceleration, Services CPI Bounces Back from Outlier, Plunge in Durable Goods Prices Slows “

The 2s and 10s are showing steepening again. The 3 month and 10 year dont look good either. The euphoria of cheap money has destroyed the working class. The working class does not have access to capital like a business, however; Basic lodging, a consumer competes with a hedge fund etal.

Here we are seeing a boom in insurance costs, yet regulators are more interested in price appreciation in food. Insurance should be investigated.

A cut in rates will be a mistake.

Somewhere in the middle here.

The CPI not so good, but a tiny bit better than the Expected.

It kind of accelerated but to some extent effect of the previous month outlier.

One more perspective from common Joe from real life:

The high prices have really created problems for lot of working people. High prices need to come down.

They sure do, but the people who make the decisions (who, coincidentally, are all members of the asset-owning classes) will be perfectly happy to see those prices in aggregate continue to go *up* at just over two percent annually.

So many people are happily clipping coupons in this political economy. Those people also have more influence per capita.

I asked the AI app Perplexity whether anyone at the Federal Reserve reads Wolf Street. It responded:

“It’s difficult to say with certainty whether anyone at the Federal Reserve reads Wolf Street, as that information is not publicly available. However, given Wolf Street’s reputation for insightful economic analysis and commentary, particularly on topics related to monetary policy and financial markets, it’s certainly possible that some Fed staff or officials may be aware of or occasionally read the site.

“Wolf Street, run by Wolf Richter, is known for its detailed coverage of Federal Reserve policies, including quantitative tightening (QT), interest rate decisions, and balance sheet changes[1][2][3]. The site often provides critical analysis of Fed actions and statements, which could potentially be of interest to those working at or closely following the Federal Reserve.

“That said, Fed officials and staff likely rely primarily on official economic data, academic research, and internal analyses to inform their policy decisions rather than commentary from financial blogs or news sites. While they may be aware of various perspectives in the financial media, including those expressed on Wolf Street, it’s unlikely to directly influence their decision-making process.”

Marc Epstein…

Gobbledygook, thank you for your thoughtful contribution…

I think it was interesting. The AI App could have added “Wolf Richter is also known for reviewing all comments and shaming anyone who comes up with stupid conspiracy stories and stupid theories”.

This kind of bland bot talk is what, the still-active business folks at my job (business school) are saying businesses all want as skills in graduates. (I ran a business, but just teach lately.) ironically, it is Wolf’s crafted, incisive, artisanal product that is so much more valuable for anyone with a real noggin on their shoulders. But welcome to bland world, where bots chat all day with other bots.

Sure seems like this is looking for a dark cloud amongst the silver lining.

I think the trend in housing costs pretty much ensures that we won’t hit the 2% average inflation target anytime soon, but easing rates in September will help shore up employment which, unfortunately, is typically forgotten as part of the FED’s dual mandate.

I’m very pro people having jobs.

No one should have their talents wasted. But creating employment via unsustainable debt growth will likely cause much more unemployment in the future.

The government has created a lot of employment in the last two years. This can continue but at what costs?

The Fed says “we would do anything it takes” can be interpreted as this goal is the only goal we care about no matter what the consequences are. Do we really not want to know what the consequences are?

What good is a job that doesn’t even cover rent? Prices need correction.

Bingo. It now takes 3+ incomes in many locales just to afford shelter. They broke shit, and they refuse to fix it. They should raise rates 75 basis points in September. It’s time to start financially crippling the billionaires and all of their buddies.

The billionaires have more influence over public policy than the common run-of-the-mill electorate. They fund the political campaigns of the elected officials, so they WILL be heard … and unlike Warren Buffett, most of them don’t want adverse conditions to touch their delicate heads … might shake loose some old-guy dandruff.

Really? What country do you think you are living in? The billionaires control everything in this country including all the political offices which matter. So no crippling is going to occur – in fact quite the opposite.

“So no crippling is going to occur – in fact quite the opposite.”

Oh, really… How’d that work out for Marie Antoinette?

DC,

i am with you in general sentiment, and have been for some time..

but lets be real.. you write about ‘they’ and what ‘they should’ do.

imagine you are ‘them’.. why would you do as you suggest here? there is simply no imperative for it, from ‘that side’ of the table.. and there is not anybody who will make them either.

the system as it exists now simply cannot be rectified from within. there are just too many feedback loops which directly contribute to it staying ‘broken’ for the regular people and ‘working as designed’ for the elites..

so there are really only two choices: deal with it as best you can, or completely decouple from it.. which is nearly impossible at this point in history, because very few have the skill set to do so.

n0b0dy-

I am under no illusions that the FED and the PTB will EVER do anything to improve the staggering wealth gap they’ve created, other than bigger it as an “improvement” for themselves and their wealthy buddies. I am simply stating what they should do were they to actually work in the interests of the public and country as a whole.

n0b0dy — consider what you wrote but imagine you were discussing the American landscape prior to the 13th amendment instead of wealth disparity.

i agree with everyone here. the problems won’t be fixed from within. it’ll require a cataclysmic event and a much lower standard of living before the average person has enough.

people grumble, but no one really does anything, because people are still generally comfortable.

when that ends, look out below.

Depth,

Did it ever occur to you that it isn’t the FED that created the ever increasing wealth gap that you mention? It is the politicians that YOU regularly vote for. The pass laws that make the field undeveloped and tilted.

Only one politician in the past 30 years passed legislation (it is named for him) that even slowed the increase in the GINI coefficient. Yet I bet you hate that politician because your political masters told you to hate him.

Someday you will realize that you are the problem. Not the FED.

Mr. Richter’s articles are all data that he publishes regularly, if you go back in the series you’ll see that the methodology doesn’t change to go “looking” for anything, it just is what it is.

The Phillips Curve was debunked long ago.

Wolf has addressed employment here. It isn’t really a bad picture. The supply of labor has increased, via our borders. Jobs are not really in short supply.

Paul:

I listened to David Lin’s interview with Thomas Hoenig. He was very articulate and insightful.

He was fairly adamant that the Fed must remain focused on the inflation side of the mandate, as other commenters here have pointed out: Pumping job gains is just inflation fuel.

4.3-4.5% unemployment is not high but rather historically low.

The consumer spending number today has rates reversed (again, that blasted recession from last weekend has blown over)… and the “recession watch” here at WS continues: nothing in sight.

Since the pandemic, my family doesn’t really grocery shop “by hand.” Rather it’s ordered online and picked up.

I used to be able to pay attention to what prices, generally. I did hear my wife say yesterday “butter, for $9?” I assume it’s an ordinary brand, and a pound. That seems like a lot?!?

Of course it is in the numbers somewhere, but there still seems to be a “whack-a-mole” nature to these price increases. The big lump was swallowed, now there’s just little bumps around.

Another inflationary force is “additional fees.” I read about a (unique to Colorado) PIF: property improvement fee added by a Target store on the front range (Denver/ Co. Spgs areas). It was a 2.5% fee, and is subject to sales tax (another 10%). A product of Colorado’s TABOR no doubt: cant add a tax, without a vote. Fees are fine.

In my neighborhood it’s things like “kitchen love” which is basically a 5% fee, because the menu has already increased, so we hit them after it’s already eaten.

Finally: of COURSE a legally required item is seen as a way to expand profit margins! The insurance industry is a government sponsored entity. Having corrupted the auto industry, it is now a drug pushing conglomerate in the healthcare sector.

“Butter for $9?”

Or a single half inch galvanized hex head bolt for $4.60. That doesn’t include the washers and nut. Or a single stick of 2×6 redwood which was $60 at one point. Or 7.5 ounces of Kettle Chips (which used to be 8.5 ounces) for $4.99, or coffee, or tires, or anything else. They broke the economy by handing obscene wealth to the already obscenely wealthy.

You keep saying this over and over like it’s a bad thing. The economy is not broken. It functions to serve the interests of the wealthy and it is doing an excellent job of it.

In case you hadn’t heard, Hell is on a hiring freeze; they’re all full up on advocates down there.

Great stuff, Wolf! Love comment section but always read the article first!

With rampant inflation, rampant deficits at all levels of gvt, with mountains of unpayable debt in the hundreds of trillions I see no soft landing and the proverbial can being kicked down the road hiitting a hard brick wall at the end. So, I predict a 70% drop in the stock market in 2025 and a 2008 2.0 economy with inflation soaring as the US$ crashes!

Thanks for the inflation breakdown, Wolf!

I’ve been so confused lately, is 4.3% unemployment something to panic over? That still sounds low to me. The economy would probably be fine without a rate cut a bit longer, yes it’s slowing but that is the point. If it hadn’t slowed we’d have even more inflation.

Also since the numbers are so skewed by illegal immigration, is the unemployment rate really even 4.3%. Are we comparing apples to apples when we compare it to historical unemployment rates?

Lastly, has the fed ever raised or cut right before an election? I have a feeling the evidence might have to be pretty strong in one direction or the other for them to do anything other than hold until the November (post election) meeting.

What is telling is the growth in Zillow Observed Rent Index dramatically exceeding the growth in the CPI Rent Index Value. To me it says CPI inflation understates “street inflation”. Of course not surprising ! You also made sure that both sides of the graph increased by the same percentage to make the index to dollars comparison accurate. Great job Wolf !

“it says CPI inflation understates “street inflation”.

I get so tired of this BS.

1. Year-over-year, the Rent CPI rose by 5.1%, a whole bunch faster than the ZORI (+3.4%)

2. Zillow’s ZORI tracks what landlords want for their VACANT units. No one is paying rent in those units or else they wouldn’t be vacant. Those wish-list rents shot up during the pandemic, but not many people actually ended up renting at those asking rents, and so ACTUAL rents never spiked like the ZORI did.

3. Rent CPI tracks ACTUAL rents paid by tenants in a large group of the same rental houses and apartments, and whoever happens to rent them puts in their rent amount, and the changes of those rents of the same houses and apartments are tracked over time. This is THE best rent inflation data that we have.

4. Looking at asking rents (such as ZORI) as “rent inflation” is braindead bullshit since NO ONE is paying those asking rents or else those units wouldn’t be on the market for rent.

Good point! First time in years, end of July saw 3 rentals become vacant in our immediate hood.

Another has one been vacant for many months and neighbor next to that one said they raised asking rent to $2600, first, last and security of same, so $7800 to move in and ”proof of $7800/income,,, and so it sits…

Generally, rents in this hood have gone from about $700 to about $2,000 in last six years, with one good guy still at the lower rate and his current folks just buying a fixer on the block for about $200K versus $70-90K six years ago.

I have seen the exact same thing here with rental units. They want a pie in the sky rent so the unit sits vacant month after month. They don’t seem to understand that the rent from the vacant months is money they are NEVER going to get back. They would be better off just lowering it to a level where they can get a tenant.

I remember when an old landlord tried to raise rent too much. I told him he was pricing himself out of the market and we wouldn’t resign, but he did anyways. We moved to another place six houses down on the same street (lol) that was nicer and cost less.

The old place sat for a few months before I saw any lights on.

Short-the term ‘entitlement’ wears many, many faces…

may we all find a better day.

From Zillow….

Zillow Observed Rent Index (ZORI): A smoothed measure of the typical observed market rate rent across a given region. ZORI is a repeat-rent index that is weighted to the rental housing stock to ensure representativeness across the entire market, not just those homes currently listed for-rent. The index is dollar-denominated by computing the mean of listed rents that fall into the 35th to 65th percentile range for all homes and apartments in a given region, which is weighted to reflect the rental housing stock.

ZORI IS A REPEAT-RENT INDEX. From the beginning of 2021 ZORI is up 30% while the Rent CPI is up 22%. So if its due to timing; Rent CPI must catch up and close the gap between ZORI & Rent CPI. If it doesn’t then I still say CPI rent understates real world rent.

read your own comment:

“…the mean of listed rents…”

“listed rents” = ASKING RENTS. That’s all it does. It scoops up the asking rents of vacant units listed for rent.

Your last part is bullshit constructed on the foundation of your failed reading of your own first paragraph.

So is it really urgent to load up on bonds now to lock in these high rates?

We’ve been through this rate-cut drama over and over again since last November.

Yes, like that groundhog day movie…

I am not loading up on Treasury notes or bonds (which have maturities of two years or more). I am sticking with Treasury bills (which have maturities of one year or less). In fact, as my 8-week and 13-week Treasury bills mature, I am pushing the cash into 4-week Treasury bills. As of today the 4-week bills (at 5.49%) are yielding 0.17% more than the 13-week bills (at 5.32%). More to the point, the 4-week bills are yielding 1.07% more than 1-year bills (at 4.42%) and 1.66% more than 10-year notes (at 3.83%). If you think that the hype about fast and furious rate cuts is either overblown, or simply impossible given the amount of the government debt that the Fed needs to finance, then you go ultra short on Treasury Bills. That’s where I am.

Alternative insights welcome… I don’t need to be the smartest boy in the class, just an informed investor.

Where are you getting 5.49% on the 4 week bills? Max yield for the past couple weeks has been 5.38 per the Fed releases of auction results.

LogicalNumbers – In response to your post below, today’s 4-week yield of 5.49% comes from the Treasury’s web site. To access:

1) Go to this URL: https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics?data=yield

2) Then select “Daily Treasury Par Yield Curve Rates”

With respect to yield… Perhaps you are confusing the “Discount Rate” with the “Yield”. They are not the same thing. In my experience, the Yield is higher than the Discount Rate.

For the finance geeks (I’m one):

Issue Price = {Par} x (1-[{Discount Rate} x ({# days to maturity}/{360 days}])

Yield = ({Par}/{Issue Price})^[365/({Issue Date}-{Maturity Date})]-1

So why not just invest in a fed money market fund?

Same thing

sufferinsucatash – Federal money market funds are not the same thing as buying Treasury bills. The most important differences for me come down to *risk*.

1) No FDIC coverage – This is a direct quote from Vanguard’s description of its Federal Money Market Fund: “An investment in the Fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.”

2) Even if a money market fund did somehow offer FDIC insurance, at any one financial institution that coverage would be limited to $250,000 for individuals or $500,000 for couples.

In short, when you buy Treasury securities you are buying directly from the U.S. Treasury and have zero default risk. In contrast, when you buy federal money market funds from Vanguard or Fidelity or the broker in town you are buying from a middleman, and that comes with non-zero default risk.

I’m seeing about 5.29% for 4-6 week tbills on schwab this morning

@Doubting Thomas, most of the good funds, such as FDLXX, are not FDIC covered, but SIPC applies, so unless you expend the equity valuation to drift, they are only very slightly more risky than t-bills, with slightly worse returns (fund costs, typically) but with the added liquidity of being able to exercise “whenever”. If it’s just money you’re saving, t-bills direct are a great way to go, but if it’s a downpayment or something and a month+ delay on access is problematic, the funds can be good options with minimal increased risk.

You just have to be really careful about the specific funds, because some aren’t primarily treasuries, but a mix of other things. As always, make sure to read the fine print on the funds and due your own DD, I am not a broker nor an investment expert.

David – Yes, there are scenarios where the need for short-term liquidity (specifically, needing access to your cash less than four weeks from now) would push you to a high quality federal money market over buying a 4-week Treasury bill. No argument there.

I think only one money market fund ever “broke the Buck” as they say. And a fed agency was going to step in to fix it.

There’s no way the Gov. would let a federal funds money market fail.

There’s prob Trillions in them.

Sufferinsucatash – Assuming you don’t need to access your cash in the next four weeks… If zero default risk and higher rates of return don’t convince you that buying Treasury bills directly from the U.S. Treasury is better than putting your cash in a federal money market fund, then I don’t think I have much more to say other than: I am willing to learn new things, are you?

By the way, Sylvester the Cat says, “Sufferin’ Succotash”. Note the spelling.

You can always compromise and do a mix of both.

That’s what I do, sort of: 75% actual T-bills in a ladder, and 25% in SGOV for more immediate liquidity needs (and/or if I need increments <$1000).

@Doubting Thomas,

“zero default risk and higher rates of return”

My favorite feature of Treasury Direct is that four week bills can’t be sold prematurely, making them hacker proof.

Just FY (and everyone’s) I

Fidelity is offering a money market / checking account with the ability to write checks, use a debit card and use bill pay. All backed by a Gov. Money Market account @4.96%. If you choose the FDIC insured option then you can get it @2.75%.

I mean if Fidelity is doing this, it has to be really solid right? 😉

I don’t think the end of times is coming so soon.

With the market surging like it has in the past week, and no recession on the horizon, I don’t see any rate cut in September. In fact, if inflation picks up, there is more justification for a rate increase. I wouldn’t try to lock in any rates now with all this uncertainty. I’m getting 5% on 1 year CDs with my credit union and sleeping well at night.

Services will continue to climb, and I remain convinced that the second wave of inflation hasn’t even come ashore yet. More DIY projects in my future I guess…

From the article; “insurers wanted to fatten up their profit margins”

Interesting, well I hope these fuckers taste like chicken then…

Interesting times for sure.

We went to an Italian place that we’ve frequented a lot less since the original owner sold 10+ years ago. Now recently now on the 3rd owner. $23 for a plate of shells w/sauce, some nice spices and a smattering of Italian sausage. Last 3 years jumped from $13 to $23, now lower quality, no white wine sauce selection, comes with no bread. Met the new owner. He’s very nice. Can’t get workers. Complained pizza boxes were up a dollar each.

Me: “You mean a pizza box costs a dollar!”

Him: “No. Boxes are UP a dollar!”

Positive note. He’s really a brewer and bought the restaurant to try and expand his brewing business. He also bought a pizza joint on Kauai in Princeville. His Hilo Bay Lager was excellent. I have tried a crap load of small brewers over the years and this stuff was exceptional. So smooth I could not believe it. The other local breweries beer is crap, IMO, but they sell a ton of it. Or should I say gallons? First time I’ve had a beer in years and I craved another right away. Not that there’s anything wrong with that…

I made an organic rotini casserole, feeds 4, $8. At home

Can’t beat $2 a serving baby!

Shells are fun too, a little legwork but you have meals for all week. I’d say for $3 a meal.

Saw Zandi on CNBC state if you remove shelter from CPI Calc. it would be mission accomplished. I think these morons think everyone owns their residence outright. US economy still outpacing world caused by huge deficit spending, they should be raising rates, but other central bankers cutting is going to force JPow hand.

other than that little mishap, how did you enjoy the play, mrs. lincoln?

If you remove durable goods from it, inflation would be red hot.

I feel like everyone is eating crazy pills when I read wolf sensible analysis and intuitive graphs I feel like inflation is going up up up…. then I go read WSJ… or anything else and they are all getting off on how inflation is fine? NUTZ. Wolf do you know many other people on this damn interweb that publish similar analysis? You are like a light in the dark… and the light can’t go out because it makes too much damn sense. The rest of the internet is a pile of hallucinating lies…

when the ‘hallucination’ BECOMES reality, is it really a hallucination anymore?

if i pretend and you pretend, and that is multiplied across society.. then reality BECOMES the illusion, does it not?

what was it the soviets used to joke?

“we pretend to work and they pretend to pay us…”

i think on some level nearly everybody realizes this.. but what else is there to do except to continue the charade, because thats just what life has become now?

If my aunt had them, she would be my uncle.

An honest reporter would have replied “a cherry-picking greedhead says what?”

Concerning automobile hedonic quality adjustment, while four of the thirty features on a car improve my driving experience, the other twenty-six unused/unwanted features that make the car “better” are not adding any quality. In fact, if each independent feature has a 2% chance of breaking each year, those 26 features add up to a wopping 40% probability of time in the shop and repair costs, each and every year. No thanks.

PS The math: if each feature independently has a 2% chance of breaking (quality of parts is getting worse, not better), then that is a 98% chance of not breaking. Spelled out, there is a 98% chance feature 1 doesn’t break *and* 98% chance feature 2 doesen’t break *and* … In mathematics, the word “and” is a multiplication, so the probability that none of the 26 features I don’t want will not break is 0.98^26 = .59. This means the chance that one of the 26 unwanted features will break in the year is .41, or 41%. I’ve got my money on that stupid navigation tablet being the first thing to go, which on a Tesla model 3 (wbich I don’t own) is about $1500.

Strike either the word “none” or “not” in the third sentence. I turned my attempted emphasis on the negative into utter confusion with the extra word.

… third sentence of the postscript. Sigh.

JeffD – to reprise (again) the old engineering joke: “…if something works really well, it doesn’t have enough ‘features’, yet”…”. (…makes me wonder in our modern age, about the real-time population ratio of those who effectively-adapt to the contemporary flood of tech ‘features’ to those who are left behind, won’t ‘adapt’, or worse…).

may we all find a better day.

My exact thoughts.

That’s why I’m driving my 2011 till the day I die.

On a similar note, refrigerators used to be durable for 12 to 18 years. There are many stories out there about LG refrigerators breaking within the first three years. Where’s the hedonic adjustment for that? Or for the fact that electric car batteries degrade over time?

You don’t hear about the refrigerators that last a long time because everyone takes that for granted. We’ve had ours for 17 years, still doing fine, and I never mentioned it (until now). But if we buy one that breaks down after two years, you can be sure the world will know about it, LOL.

There is an inherent bias in what is posted on the internet.

JeffD

It took me a while to find a car without all that crap you described above, but I found one, a Mitzibushi Mirage. Got a 2020 like new one for $11,500.

Thanks for the tip. On the other hand, once my car conks out, I’m seriously considering an electric bike (for short trips), rental car (for long trips), and ridesharing services (for everything else). I don’t commute, so it makes a lot of sense for me. There are too many add on costs/hassles for ownership nowadays. Plus, I can have fun driving different rentals.

PS Given the paltry number of miles I drive each year (I already use rental cars for long trips), under no scenario does the $70,000 car purchase plus yearly tax/insurance/gas/servicing amortize out as as a good value.

Marc Epstein,

Maybe next time give a Magic 8-Ball a try.

Don’t forget, these are rates of change, so there is a compounding effect. In other words, just because an unaffordable rent is no longer increasing, it still isn’t affordable.

What working Americans need is deflation…

Banks and Wall Street, not so much, I’ll let you decide which group actually owns CONgress.

stocks are surging today because retail sales were good. the algos actually believe we’re going to get a goldilocks landing and rate cuts in the fall

s&p now up 7% from last monday’s crash which needed a 75 bps rate cut. lol.

Indeed, would be great to see a 25-75 bps hike!

Let’s see how the bond auctions go today.

anyone who buys 10 year treasuries at 4% is an idiot.

“anyone who buys 10 year treasuries at 4% is an idiot.”

You mean like banks and retirement funds…

Yes, I don’t know any individual buying any government debt with a duration longer than 8 weeks…

With all the world’s central banks on the same page since ~2008, global hyperinflation is “baked in”, it’s only the timing that is in question. IMO, only a world war would change that at this point.

no one is forcing them to buy those.

they’re gambling that they can front run cuts and get price appreciation.

“no one is forcing them to buy those.”

That’s false. Many retirement funds must allocate a certain percentage of their portfolio to government debt by law.

Banks, yes, they are gambling because they can always pull a “Hank Paulson” and hold a gun to the head of the taxpayer via their bought-and-paid-for representation in CONgress.

Home prices are too high for meaningful rent declines to be plausible. Rents have consistently gone in only one direction in the last 3 years: up.

The gap between the two lines in the OER vs CS home price isn’t getting any smaller…

Well, the data and charts looks like everthing is decelerating compared to the past 2 years. So, indications are a “soft landing” for the economy. However the labor market, the yield curve and the 10 year Treasury bond seem to saying “alert, alert, alert….fasten your seatbelts”. Wolf, perhaps you can address those indicators.

I was a stupid, clueless teenager in the 70s. I remember inflation back then even though I didn’t understand it. I remember gas at the pump for 19 cents a gallon and we got free gifts. My dad paid 2700.00 for his brand new Dodge Dart, 4-dr sedan. I was there at the dealer and saw the numbers on the bank check that he endorsed over to the finance guy at Fairfax Dodge in Virginia.

I am 66 and I got my MBA 20 years ago. I think these boneheads at the Fed and the US Treasury are clueless. They are using antiquated economic models from 50 years ago. I am anxious about 2025. I have a daughter in her mid-20s who is just starting out in life. I worry for her future and those in her age cohort.

“Tell me lies, sweet little lies…” Fleetwood Mac.

God Bless America.

“Soft landing?” There is no landing. There is a re-acceleration. Just look at all asset prices. They are all charging towards new all-time highs.

“They are all charging towards new all-time highs.”

Priced in FRNs, yes. I don’t see that trend reversing anytime soon, especially if the Fed cuts in September. Place your bets…

(because this sure as hell isn’t “investing” anymore)

the fed hasn’t even cut or printed yet. it’s all based on the market believing they will. that’s why 5.5% has done nothing to rein in speculation.

but i’m glad you noticed that it’s only at all time highs priced in dollars. that’s what people mean when they say that things aren’t worth more, the dollar is worth less.

we’re not more productive than we were 5 years ago.

If the Fed cuts before anyone experiences real pain, inflation will skyrocket. And no, 4.3% unemployment and 3.6% yoy wage growth is not pain, but the very opposite of pain. Cutting now would be the equivalent of a Fed put on maintaining (elevated) lifestyle, which once unleashed, can’t be taken back, politically.

Asset prices do not contribute to inflation.

I have a question for the group that I desperately want to get feedback on:

Is the whole “if stocks go down for more than 3 days it is the end of the world and we just need to print money to make them go up” mindset firmly entrenched in all developed countries?

I am coming to the conclusion that the existing power structures would happily sacrifice their own currencies (and the wellbeing of most of the citizens in those countries) to maintain the above mindset.

What are people seeing/hearing/thinking?

The billionaire scum have control of the entire globe, and have turned central banks and their respective currencies into their own personal piggy banks. When the kid is in charge of the cookie jar it is soon empty, and he has chocolate all over his face. The pigmen have filthy faces.

The problem we run into as market participants is that we have to deal with what is in front of us, regardless of our personal feelings about how fucked up the situation is.

Have we passed the point of no return, where the political/economic concentration of power is such that existing power structures would rather sacrifice the purchasing power of the majority of their citizens to stop stocks from having anything other than a very short term correction?

Correct, you ask the right questions. Looking at what is in front of us in this in, I’d say the legacy power structures and supply lines are still intact, so barring an immediate disruption in either, global devaluation of fiat currencies will continue. So long as goods and services continue to cross borders we should be fine.

The answer is yes in my opinion.

I believe we are at that point where asset prices have been artificially supported too long. Any drop in general asset prices exceeding 10% is a threat to employment that must be reversed quickly, or recession would result.

This Fed will likely continue supporting markets until people realize such policies will keep actual inflation much higher than 2% over time. That realization may take a while.

@Bobber,

And what’s so bad about recession? People talk about it like the end of the world (looking at you), but it actually makes the economy healthier. Recession is just like a wildfire, let it happen and the ecosystem will thrive. Never let it happen, and *guarantee* conflagration down the road.

JeffD,

Recessions WERE a good idea when debt levels and asset prices were within normal ranges, but after 20 years of the Fed’s short-sighted boneheaded policies, the economy can’t take a cleansing recession. With massive debt levels and nosebleed asset prices, a recession must immediately be met by massive fiscal and monetary stimulus. Otherwise, a downward cascade would be triggered.

We haven’t had a serious recession since 2009 because the Fed won’t allow it.

At some point, the Fed will be overwhelmed by market forces and its tools will be useless. Poor policies, when applied for long periods, have severe consequences.

bobber it seems what you’re saying is that the u.s. will continue on printing and deficit spending at every hint of a recession until it loses the reserve currency status and the economy completely fails.

Counter-argument:

The Fed can let stocks and housing do an orderly decline without threatening the stability of the system. A crash is less preferable for PR reasons.

The bond market – specifically Treasuries – is what really matters. The Fed’s true mandate is to ensure there continue to be buyers for USG debt. As long as demand remains, the system is stable.

Every time I see a post of yours I think about Michael Moore asking the rhetorical question, “If it’s just about markets and profit, why doesn’t GM sell crack cocaine?”

Answer: because it’s illegal, because crack cocaine destroys communities, just like closing a profitable factory and moving it to Mexico destroys communities.

The icing on the cake was the answer to the question from a guy in the audience:

“Because the C.I.A. has the market cornered!”

Couldn’t disagree more. Depth Charge is on the right track, just slightly overzealous. Doing nothing or overstimulating (as you seem to be suggesting) will create more problems than it solves. Look around you. Would you say the US is cleaner, more vibrant, and more economically healthy than in 1980? Personally, my answer is no way. I’ve never in my lifetime seen such homelessness and in-your-face crime *everywhere* coupled with lack of civic duty and moral character as there is today.

On second read, it looks like you might have been applauding Depth Charge rather than disparaging. If you were applauding, I obviously agree.

that mindset is certainly firmly entrenched in the minds of investors in those developed countries. the banks don’t even have to print, because people will believe they will.