Whiplash-causing month-to-month services PPI fell in July after hot readings in prior months. Core goods PPI is well-behaved.

By Wolf Richter for WOLF STREET.

The sharp deceleration on a year-over-year basis of the core Producer Price Index and the services PPI in July was a one-time shot, caused by the services PPI of July 2023 (+9.9%), the highest month-to-month reading in over two years, to fall out of the 12-month figure and be replaced by July 2024 (-1.9%), lowest month-to-month reading since March 2023.

It won’t repeat the rest of the year because all the remaining month-to-month figures that will fall out of the average over the next five months were low to negative. And the base effect that was such a tailwind in July will flip to a headwind in August and going forward.

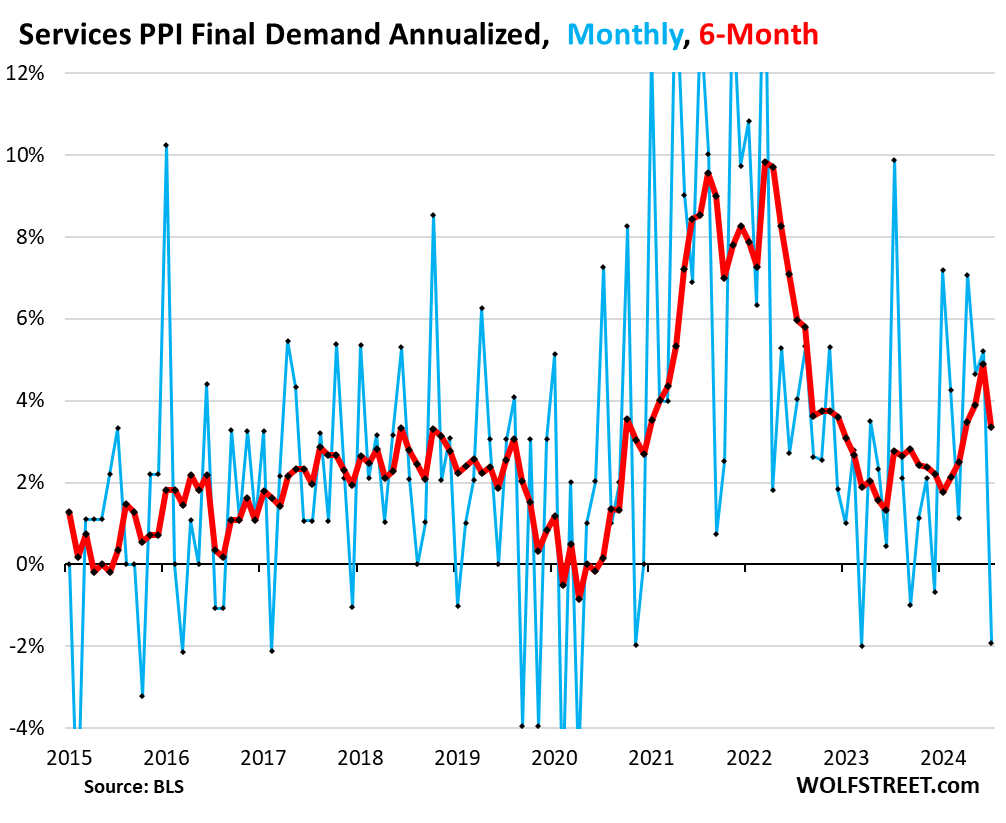

And in terms of the month-to-month figures (the blue lines in the charts below), well they’re whiplash volatile.

On a month-to-month basis, the Producer Price Index for final demand, which tracks inflation in the goods and services that companies buy and ultimately try to pass on to their customers, decelerated in July from June, on a plunge into the negative by the services PPI, after the hot readings in prior months. The PPI for finished core goods, which exclude food and energy products, accelerated month to month but remains well-behaved.

Services PPI fell by 1.9% annualized in July from June, seasonally adjusted, after the jumps of 5.2% in June, 4.7% in May, and 7.1% in April, according to data by the Bureau of Labor Statistics today (blue in the chart below).

The 6-month average decelerated to 3.4% annualized in July, after having risen at a red-hot pace of 4.9% in June, the highest since August 2022 (red). The six-month rate irons out some of the whiplash volatility of the month-to-month readings and includes all revisions. It decelerated so sharply because the 7.1% January reading fell out of the average and was replaced by the negative 1.9% July reading.

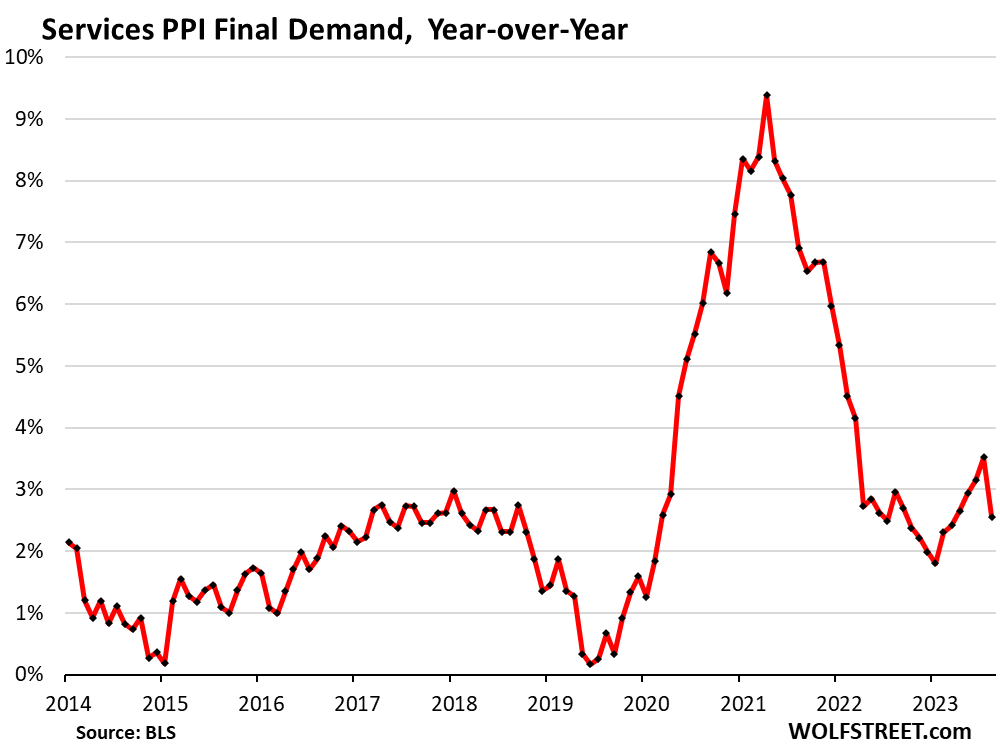

Year-over-year, the services PPI rose by 2.6% in July, a sharp deceleration from the 3.5% increase in June.

The extreme base effect: The year-over-year reading fell so sharply because the freak month-to-month spike of +9.9% annualized in July 2023 (the highest in over two years) was replaced by the drop of -1.9% annualized in July 2024 (the lowest since March 2023). Going forward, the low-to-negative month-to-month readings last year in August through December will come out of the 12-month base and be replaced by the readings going forward, and the tailwind of the base effect in July will flip to a headwind starting in August.

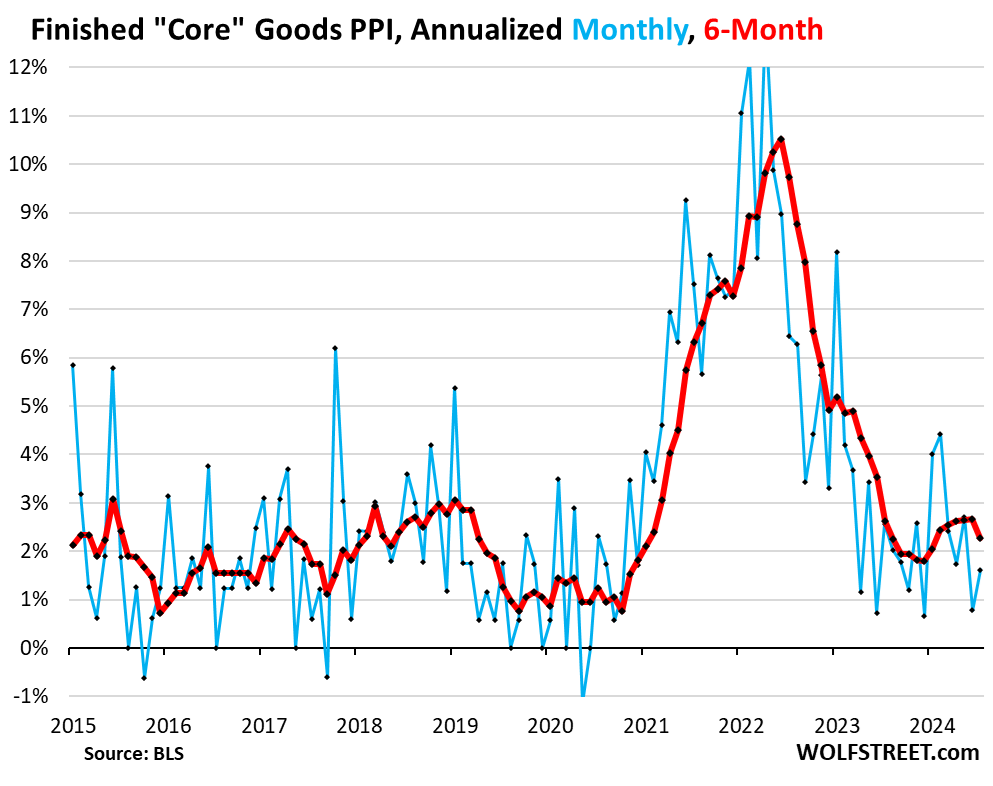

“Finished core goods” PPI is still well-behaved but accelerated in July from June, rising by 1.6% annualized, up from 0.8% in June. As we have seen all around, there have been no major inflation pressures building up in core goods in over a year. Inflation has been largely wrung out of core goods.

The six-month rate decelerated to 2.3% annualized from 2.7%, as the month-to-month 4.0% jump in January fell out of the average and was replaced by the 1.6% increase in July.

The PPI for “finished core goods” includes finished goods that companies buy except foods and energy. Prices have continued to rise, but a pace that’s in the normal pre-pandemic range.

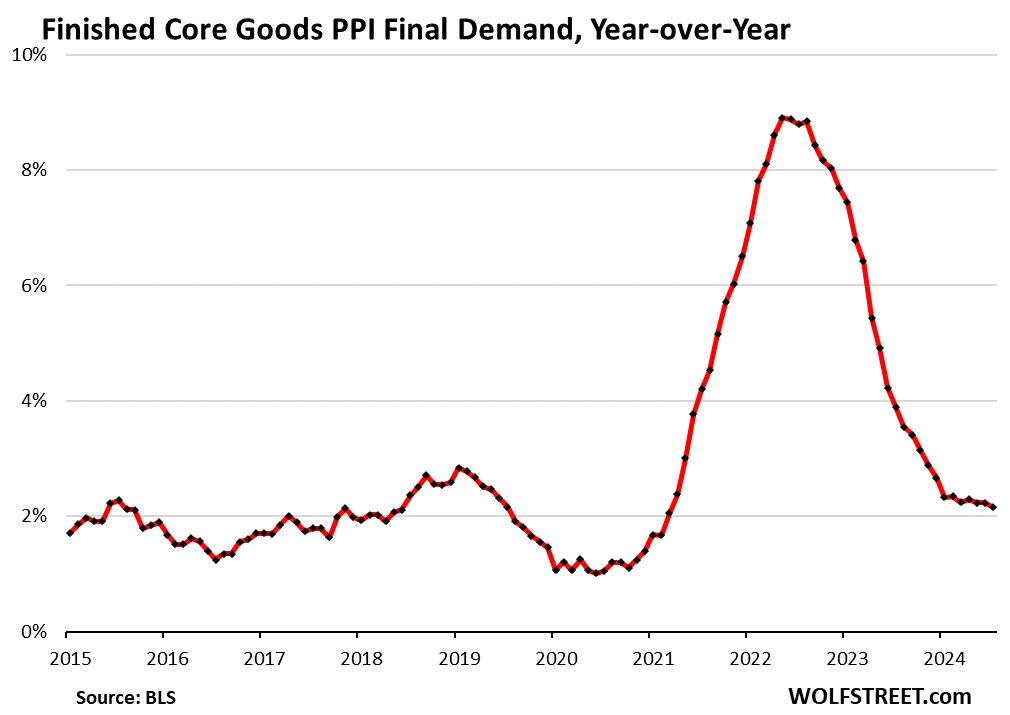

Year-over-year, the finished core goods PPI has been around 2.2% all year with a minuscule down-trend that gets lost in rounding – all of them the lowest since March 2021. In July, finished core goods PPI rose by 2.16%:

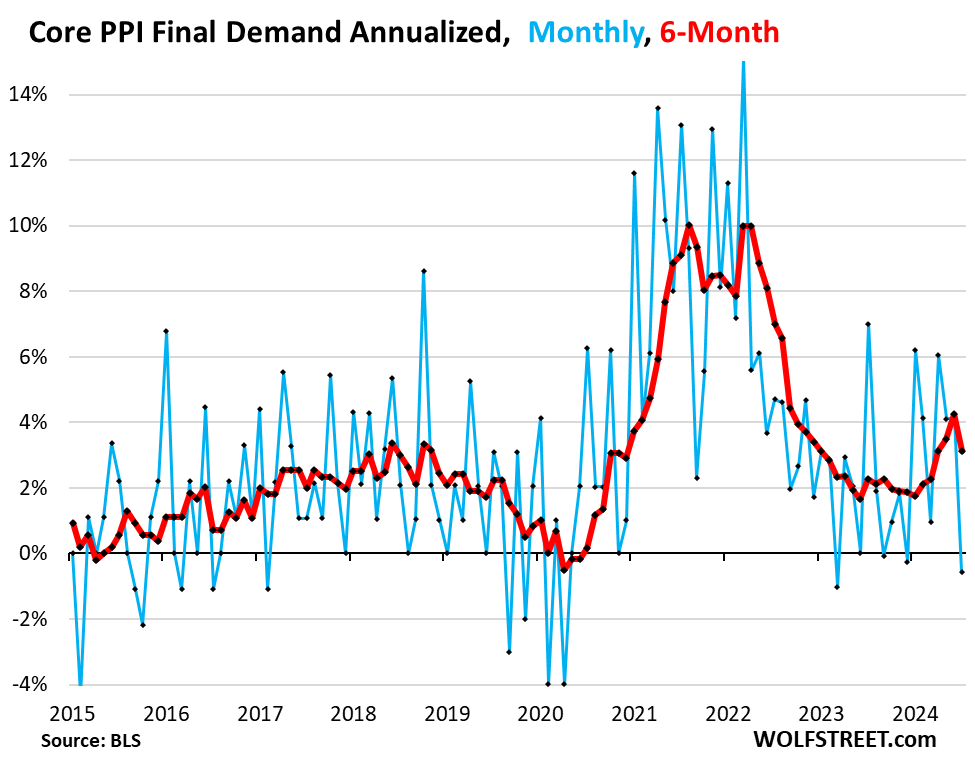

“Core” PPI fell by 0.6% annualized in July from June, seasonally adjusted (blue in the chart below), driven by the drop in services (-1.9%), which dominate core PPI, and muffled somewhat by the acceleration in finished core goods (+1.6%). The -0.6% annualized reading in July comes after the 4.1% increases in June and May, and the 6.1% increase in April.

The 6-month rate decelerated to 3.1% in July, from 4.2% in June, which had been the highest since September 2022. After being well-behaved much of 2023 near 2%, the 6-month rate re-took off in February (red).

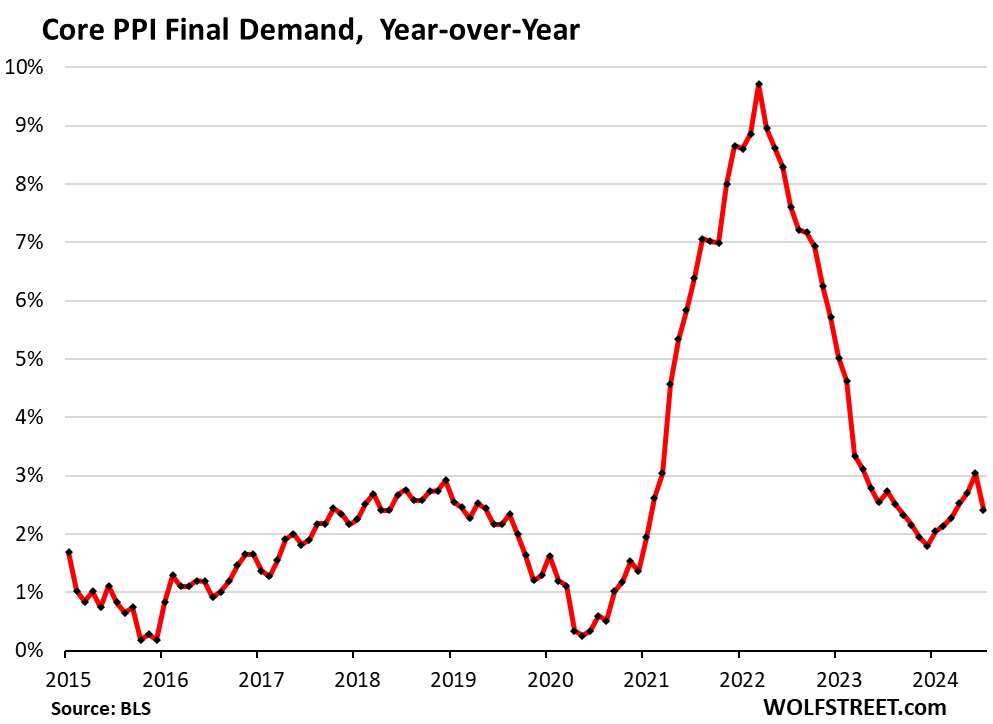

Year-over-year, core PPI rose by 2.6% annualized in July, a sharp deceleration from June, driven by the base effect in services, as we noted above. June (+3.0%) had been the worst reading since April 2023.

For the rest of the year, the readings this year will replaced the low to negative month-to-month readings from August through December 2023, and the tailwind of the big base effect in July becomes a headwind starting in August.

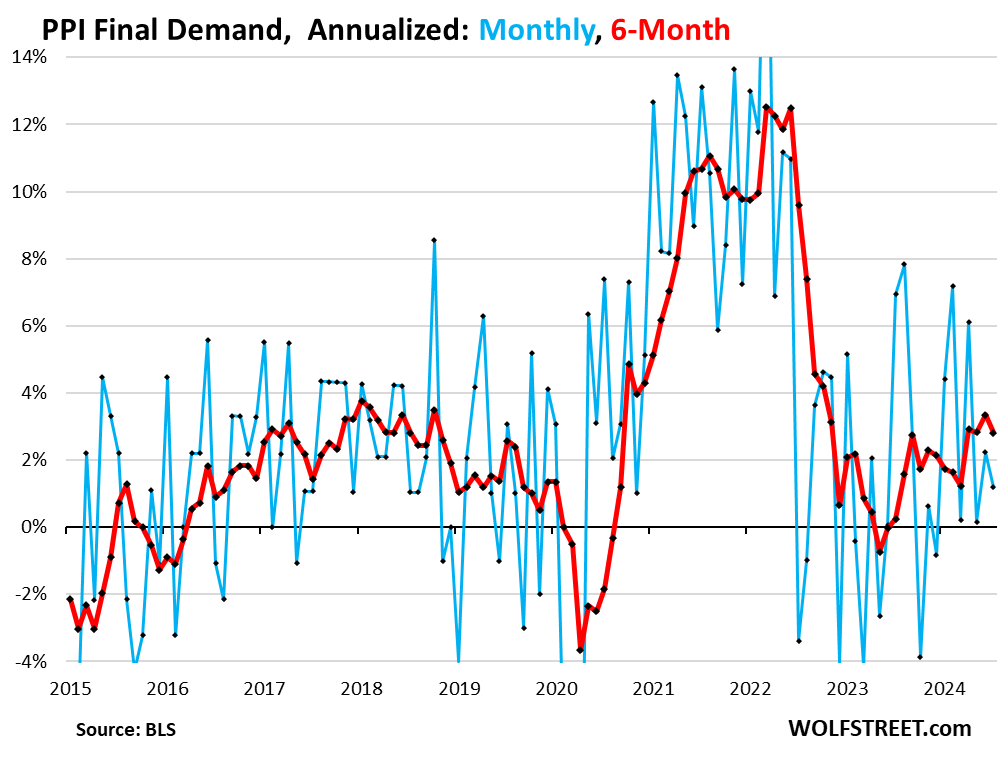

The overall PPI for final demand rose by 1.2% annualized in July from June, a deceleration from June (2.2%). The 6-month rate rose by 2.8% annualized, a deceleration from the 3.3% in June, which had been the highest since October 2022.

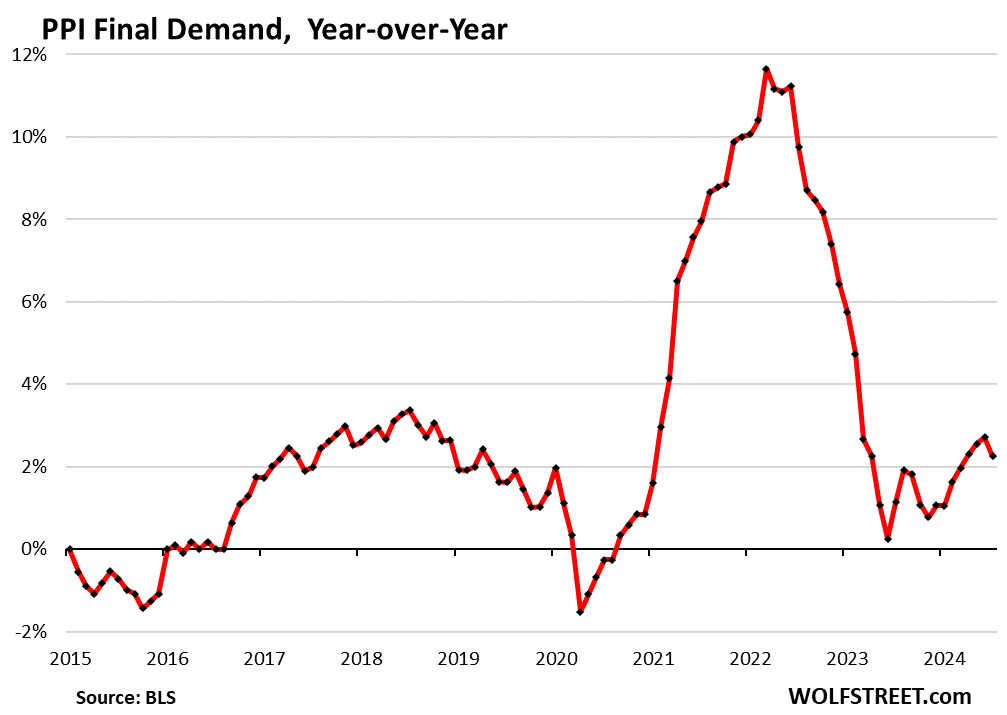

Year-over-year, overall PPI rose by 2.2%, a deceleration from 2.7% in June, which had been the highest since February 2023:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

That’s pretty good news. AAPL, NVDA plowing along. Is the panic over?

The headlines are always good news, come hell or high water, even if they’re not good news. And that’s the only thing folks and algos out there are reading right now, and how they’re reading it.

The economy/market never gives 100% of good news, even if so, plenty of people (bonds, t-bills holders, gold, crypto, Rolex?) say that in the future there be “end of the world as we know it”.

But markets do go up and up over long time, often not in straight line. And my strategy is to harvest it. Just enjoying live and let it work by itself.

Plenty of bonds, bills holders on this forum. Note, if bad news you are getting lots of comments. If things are not bad way less.

Depends on your definition of bad news. It wasn’t good news. Read the article again slowly. Headline looked better due to base effect from last year’s hot reading. It was propagandized by the entities you covet as being positive for the casino due to rate cut mania. And you fall into that category of spinning it as a positive, or maybe you plain just don’t get it. Your extreme obsession with the casino, at the expense of main street, is not a positive.

@DR

This is positive news to me. I’m actually caring the most about the actual data. Not both sides trying to spin here both ways.

Have you seen this? What is bad to you?

Actual data:

PPI-FD – M/M last 0.2% expected 0.2% today: 0.1%

Ex-Food & Energy – M/M last 0.4% expected 0.2% today 0.0%

Biker,

This one monthly data point is arguably good news. But one data point doesn’t make a trend, and the next one is likely to not be good news – I think that’s Desert Rat’s point.

@ ShortTLT

The purpose of today’s PPI reports was MM aka PPI for the last month. The rest, YY, is just result of MMs over months. Simple. Period.

And this article was talking about the PPI report. So my response was as it was aka some good news.

The rest of discussion is irrelevant to me since does not bring anything new materially, just some insides to the human psychology.

YY is elementary school. I think I get it, maybe not? :)

If I understood how “YY” and “MM” were being used in the above discussion, would it help my understanding of the discussion?

Not asking for an explanation…..just rhetorical, by anyone at my LOW econ understanding level…I could barely get through the article, but I know it’s an index the Fed USES, and roughly how, and what it may portend….maybe even how soon?….something becoming more critical to someone of my modest means (NOT COVETING!!!!!….that’s Lake of Fire stuff for sure and I’m old)

But I do have a feeling some good points were made.

There is no “lake of fire” stuff here.

It’s just inflation — the loss of purchasing power of the money you earn from your job. There is always some inflation. But there was a lot of inflation in 2021 through mid-2023, and that’s a problem, and now there is less inflation, but still quite a bit, a lot more than there used to be. Too much inflation can be a problem for the economy. If wages don’t keep up with inflation, it causes even bigger problems. So it’s important to bring inflation down.

As you can see in the charts, inflation is not spread equally across all product categories. Some categories have big deflation (declining prices), others have big inflation (rising prices). This article exists to show you what inflation is doing where.

Thanks. And I DO derive some satisfaction from seeing the costs of many things in that CPI “basket” that I spend ZERO or to next to nothing money on, as I am fixed income.

Was kidding about my “Lake of Fire fears”, but maybe 50% or even more of my fellow citizens are NOT….and that kind of “thinking” is VERY scary to me, as I have said before.

I also have never meet a “biker” (I usually preferred to be called a RIDER…..I guess they are even more interchangeable terms now……although am EX-BOTH, now) with that kind of apparent knowledge, either…both observations can’t help my understand of that dialogue much.

Side note: Every time I see “Flo” I think “Biker” image is changing…..those advertising creeps will do anything to sell insurance”…….or ANYTHING

Even the specialized motorcycle ambulance chasers with “colors” but on Honda 750s.

No wonder I’m confused…or senile.

NBay – the ‘Hell’s Accountants’ segment of the moto-cruiser market has been a thriving one for decades (…the ratio of preferred moto, and the importance/distance/destination of its actual riding mileage to its one of a personal pose-platform is HIGHLY variable, as you know-ALL simple-minded advertising memes aside…). Best.

may we all find a better day.

Wobble wobble……so east to spot….especially at 35 mph top gear with full throttle….making the loud blap blaps….while trying to see if anyone is looking. And EVIL handling.

Funny!

Guess some pay a second even bigger price, though.

Later.

PS; “Hell’s Accountants” was GOOD!

Skull with dollar sign(s) and the above rockers HAHA!

Knowing that FED rate adjustments take 12-18 months to fully take effect, what metric are you looking for to ensure the momentum is heading in the right direction that would support a rate cut?

Any hypothetical rate cut would be heavily dependent on the inflation situation — which remains volatile. The U.S. central bank leads the other central banks in its rate manipulations, so what it decides to do will be aped mindlessly by Canada et al. where I live. Only the soul of the grifter is encouraged by this news.

Why does it feel like markets will always win regardless of headlines being right or completely wrong? Today’s news’ rise will be higher than next month’s plunge. At least until there is a recession.

Because they will as long as the option of a bailout is on the table. That is what a bailout is. Look at our current society, after the bailouts of 2008, are you surprised we now celebrate failure? A bailout also makes sure that nobody knows the price of anything. The only people come to this site is because they hope to get some kernel for when the bailouts won’t work anymore. Soon, very soon.

Correct. At the heart of all of society’s problems is the fact that the system has been rewarding bad behavior for some 40+ years. Especially in finance, and at all levels. One example; AIG, Goldman Sachs, etc., all those fuckers should gone bankrupt and had their assets liquidated. Instead, we made Goldman a primary dealer bank and raped savers for 15+ years. I predict that we will see even larger price distortions, in real estate in particular, especially if the Fed actually cuts in September. I don’t see CONgress or either political party becoming responsible financial stewards. Hedge accordingly.

Think they call that a lack of moral hazards. WS has been conditioned and rightfully so to think they can do no wrong and FED will always bail them out and come to the rescue and for the most part, they have been right in the last decade or two since 2008, 2018. Will they be right forver? Tough to say but that line of thinking is still strong or the general consensus

“Will they be right forver?”

No

In fact what you saw in 2020 might have been practice to how they will react when they can no longer kick the can. I think they can’t kick it anymore. Why else raise rates now, why not anytime from 2008 thru 2019? Heck 2.5% almost derailed the entire thing in 2019. Only reason they raised to 5% now is the deflation was so large we only got “10%” inflation after all the money printing they did in 2020. I think that funny money is running out of umph, and they need another excuse to print, the question is what do they choose this time? I’m leaning on war.

Jaime the wait always feels longer. I can tell you from experience that the dot com bubble felt like 30 year long.

But often in investing and finance, patience is rewarded. It works out well…but it doesn’t feel that much great along the way.

The mind plays tricks :)

It might also feel like a longer than normal wait this time, because they’ve been able to keep rates inverted without a recession for the longest time in history.

The [10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity (T10Y2Y)] on the FRED website shows how long the market has been laughing in the face of the Fed and its higher for longer position.

The bubble felt like 30 yr or its deflation? The Nasdaq did not recover its bubble high for 15 years.

We all are waiting for dear recession for last 2 plus years :-).

Home Depot call today:

“Consumers are in deferred buying mode”

meaning they are waiting for the interest rate cuts to spend $ at Home Depot on projects.

How much money would a lower rate free up for a stretched homeowner? I mean yeah if rates get cut in half, but that will take years. IF Powell even lowers to 3-4%, which is doubtful with 3-4 years of “taking the temp” for 6 months at a time.

Recessions have been removed from the business cycle.

I think we have enough evidence that the neutral rate isn’t much below five. Maybe 4

How funny, looks like we’re back to good news is good news and bad news is good news again when it comes to WS. Guess the bad news is bad news vibe lasted about one week or so before we flipped back to hopium rate cut soft landing narrative again couple with a sprinkling of emergency rate cuts now from our favor pundits…

The news regardless is a trading positive for the last several months of PPI and CPI almost a traceable event if one is not risk adverse. I think the big market moves are a result of the volatility dropping with the actual news out vs the anticipation

Ever onward and upward!

I just got a 5.15% brokered Bank CD called (8/30) in my Schwab Account. And the latest round of for sale brokered CD’s on Schwab are in the 4’s, percentage wise.

I just had some 5.98% agency bonds called in my Schwab account. I’m waiting for rates to bounce back before adding more fixed income.

And I get 5% at Robinhood without any commitment, so I just moved all my cash from my checking account to sit there instead of at Chase. I don’t know why I just did it now when I could have done it a year ago. 🙄

Is Robin hood trustworthy? I’ve heard mixed reviews.

I hope it’s insured somehow

It doesn’t get much shadier than Robinhood. I hope they get destroyed by that antitrust lawsuit.

This happened years ago – right after rates went up. Banks lost a lot of idle deposit cash from checking and savings accounts. 5% on cash is nice!

No mention of the base effect in any of the other PPI articles I’ve read… these financial pundits think inflation will just magically disappear.

Bloomberg economic calendar suggests MoM (3 bulls) is more important to the market than YoY (1 bull)

1:04 PM 8/13/2024

Dow 39,765.64 408.63 1.04%

S&P 500 5,434.43 90.04 1.68%

Nasdaq 17,187.61 407.00 2.43%

VIX 18.01 -2.70 -13.04%

Gold 2,506.60 2.60 0.10%

Oil 78.51 -1.55 -1.94%

Gold didn’t hang onto 2500, but interesting to see it poke above that level briefly.

Gold remains above $2,500 on my screen. No surprise really. Deficit spending in a bankrupt world continues, I’d say $2,500 is the new floor. Silver is the mystery to me, especially considering current industrial demand.

Gold spot never reached $2500.

December contract is most widely traded currently (not sure which one is cited above or on the “finance screens”).

Yes, it reflects the inflationary/ money printing environment. Yes, it also reflects the “real rate” environment. Both of which is variable worldwide. ALSO the gold price will likely be affected by the unwinding of the Yen carry trade.

WB: I honestly expect a backtest of the $2070 level, a 10-20% drawdown in gold price will (to me) signal that the “recession has arrived.” After which the price will go “to the moon.”

Ratio charts are a good indicator of money flows. The Dow:Gold ratio has broken down some, but the gold:S&P will have to rise above 0.5 to be the “watershed moment” of the PM bull market (of tomorrow).

Silver is more correlated with small caps and (somehow?) sugar from what I have seen. Also (debatable) I have heard that silver should lead the secular PM Bull (I have also heard it should be gold or SMH the miners).

I see Dr. Copper is looking ill; what industrial demand?!?

Thanks for the insight.

Plenty of demand for copper in my neck of the woods, between the multi-family construction and EV/solar manufacturing. The latter is tied to global manufacturing and like it or not, the real owners are forcing this on us, globally. Biotech is a fucking mess right now, at least according to all my old contacts that stayed in that game. I left the bay area just before the collapse of the first bubble…

MW: Starbucks shares rally on turnaround prospects under former Chipotle CEO

SBUX 24.51% CMG -7.47%

Chipotle’s stock is the S&P 500’s worst performer as CEO’s exit triggers ‘rock star’ jitters

I really dislike chipotle and how they are run.

Did you hear that they were intentionally short changing the customer ,when it comes to portion size?

Now the same underhand practices come to Starbucks. Yipee. 🤨

Americans could do with smaller portions.

Bro we’re building dem big Mascles, Like Arhnald!

Get to Tha choppa!

💪 🚁

And we’re not addicted to smoking like a lot of other countries. Cure your populations lung disease and call me in the morning. Thanks

Larger portions mean a doggie bag and the next meal is heated up from the bag. Two for the price of one!

Us old, fixed income retirees like that, and the cat has his food to himself (for a while longer).

Regardless of facts, there’s always narrative. Fed. Governor Bowman delivered a speech to a room full of bankers, with a fairly clear and objective view of the economy.

She acknowledged the base effect, that inflation is still high and the labor market is a bit of a tough read. I browsed the transcript and it seemed prudent (she’s been known for hawkishness, even mentioning rate hikes until recently).

I saw a headline saying she’d “green lighted” a 25bps September cut. SMH

Geopolitical pressure almost ensures a continued pressure on inflation IMO (also referenced by Bowman)

Regarding market dynamics: S&P clearly broke down below the rising support channel/line. Has risen nearly to a backtest of this line. Weekly and monthly closing prices are always key to watch!

Bloomberg economic calendar suggests MoM (3 bulls) is more important to the market than YoY (1 bull)

If we have a decent CPI report tomorrow at 08:30EDT,the Markets will be off the charts…

And by ‘decent CPI’ you must mean ‘headline number that’s still above the Fed’s target but below mkt expectations’

Down or up?

Howdy Old paperboy 2024 CPI 3.1 3.2 3.5 3.4 3.3 3.0

Anything below 3.1 tomorrow should have the stock boys and girls going wild……

But maybe an excellent CPI report is priced in by now, and anything less than excellent is going to rattle some nerves?

You can “price in” the same thing multiple times these days. You can gin up fantasies, you can do anything. Lie, cheat and steal is the name of the game. Fake internet coins with market caps in the billions? They printed way too f**king much….

excellent point!

Core CPI is still 3.7% yoy and Services ex. energy still 4.9% yoy. Shelter inflation re-accelerated from June.

Not exactly what I’d call decent.

Three things are going to cause inflation to firm up. Deglobalization, tight labor market, and credit impairment.

Howdy. THANKS Lone Wolf. Looking forward to CPI Tomorrow… “Articles of Truth “.

If MM goes down, would that be a good news? Sorry, couldn’t helped myself 😀

so whats the the prediction for CPI read on Wednesday?

Based on this article, I guess cpi would be lower and stock market should be higher.

the stock bubble will last until people would rather have cash or other assets than stonks with p/es of 50.

Lots of people already do, including Buffett:

https://wolfstreet.com/2024/08/04/berkshire-dumps-nearly-half-its-apple-shares-plus-other-stocks-into-the-final-rally-proceeds-went-into-t-bills-cash-is-king/

“Lots of people already do, including Buffett:”

Perhaps he also thinks the next bailout will not have the expected effect.

It’s a peculiar behavior.

Most want stonks when P/E is 50.

Most want cash when P/E is 15.

Because GREED. It’s the reason everybody wanted a house at peak pricing during the last housing bubble, but nobody wanted them when they were dirt cheap. They only want the appreciation. When there’s no expectation of delicious returns, they scatter like ‘roaches.

Yes indeed, this is why I think the current housing environment is the greatest bubble of all time, and high prices are only partially due to inflation.

“Price go up” has been far more valuable than “roof over head” since about 2016 and went into hyperdrive in 2021.

There is no housing shortage, but there are very few houses available because every single extra house is bought as an “investment property” when appreciation is perceived as guaranteed. If the appreciation expectation is gone, only then do we see housing’s true value.

Some like to use the construction cost metric as a “floor” for pricing, but that is also directly inflated by the speculative bubble when there is a mad dash to create new magical wood appreciation boxes.

Carlos, I do think that there’s a way to value a house (any human occupied real estate). The intrinsic value is what the house (or income property) can be rented for. The traditional measure is gross income x 7 or 8 = value of the property. Right now, where I live, that multiple is closer to 20 times annual rental income.

So, if you borrowed 80%, at even a 6% rate, included extras like taxes and insurance (not even a reserve for maintenance), you’d be in a deep hole financially every month. The ONLY way you could come out ahead with that investment is if you could sell it in the future at a higher price, high enough to recoup your monthly losses plus some measure of profit. In other words, a greater fool.

Housing is in a bubble. The cost of the building, from scratch, is not really a major factor for valuation, in spite of appraising the parts. If you have a factory/shopping center/triplex with a million $ as a sunk cost, but it’s obsolete, can’t be rented, and needs to be razed, the value of the bricks, doors, etc. is irrelevant.

@HowNow,

The problem is that there is now cartel pricing, with software like RealPage setting a floor that every landlord adheres to, with a maximized algorithmic ratchet-up over time from that floor. They are boiling frogs, and the government does *nothing*, except inflate shelter cost through policy (in)actions..

I moved everything into CDs before Buffet did. He’s behind the curve. The Swamp is ahead of Buffet. I’m glad he’s finally has seen the light. Now , we need to get J Powell to see the light and start increasing interest rates, like I have been recommending on this site for the past 6 months.

Rate cutes are coming in September. Only question is would it be 25 or 50 bps.

Why not 100 basis points, while we’re at it?

Makes sense, SC. Crash all assets, except CDs and Treasuries, so you can go shopping.

Good luck with that. Buffet moving into CD s is obviously an indicator of slowing economy.

It’s an indicator that he cannot find any value in the stock market at these prices. Nothing to do with the economy, but with out-the-wazoo market prices.

Well no matter if stocks are inflated or if people are willing to have more expensive stocks, all the while the true bottom rises. ⬆️

Bottoms are based on earnings. At least, they used to be.

Thank you for the wonderful information. I have struggled this year with the market in many ways. I watch the data being presented on CNBC painting a picture that the economy is nothing but sunshine and rainbows. I then read about the same information and it is the opposite. This is the hardest environment to invest in that I have experienced. For example I go to Costco each week and all meat products have increased for the last 2 months. Uber comes out and beats top and bottom numbers but the day before a driver tells me he had to take a 2nd job because business is off.

The 3rd is at Saratoga food truck sales are down and tips are down 40 percent. It’s just hard to believe the economy is great

Everybody I know is at least outwardly doing well. I have a few elderly friends and family grousing about the economy, but its tough to be 100% dependent on Social Security. Maybe I live in a goldilocks area (E. Central Florida), not sure, but it seems to be the best economy of my lifetime. Yes, inflation was high, but it seems under control now and easily adjusted to by adjusting spending.

People are (re)learning to substitute goods and services.

yes best economy if you have lots of assets and a house with a low mortgage.

not so great for everyone else.

Not hard to invest at all. Short term treasuries or brokered CDs are still around 5%, as are money market funds but those have a risk of a run on the fund so I’d favor the first choices. Also I bonds and TIPS are safe with pretty good yields. Plenty of healthy foods are still very affordable, some really cheap like dry beans and rice, potatoes, onion, carrots, radishes, tomatoes, jalps, cabbage, etc. I’m not too knowledgeable of meat prices but rotisserie chicken low priced.

Newsrooms; ‘If it bleeds it leads’

WS; ‘If it’s green, it’s seen’

Makes it increasingly difficult to model the thought process leading to a prediction of no cut in Sept. Not whether there should be a cut but whether there will be.

One can make the argument that only a severe recession can wring out the excesses created by the previous artificially low rates. That a huge dose of pain for a year or two would be long- term beneficial. And a lot of seriously overweight folks could benefit from a period of near famine. But they aren’t going to sign up for it.

The next FOMC meeting is Sept 17. The data on hand now is most likely the data they’ll have then.

If someone is steering a large ship, like a tanker, and is trying to hit course 120, they have to begin correcting long before 120. The bigger the ship, the more its momentum will tend to swing it past the desired course.

The ‘perfect’ is the enemy of the good, or let’s say the ‘not bad’. The Fed is close enough to its course of the world’s largest ‘ship’ to begin slowing the pace of correction.

“The next FOMC meeting is Sept 17. The data on hand now is most likely the data they’ll have then.”

So Second GDP reading, August PCE data, JOLTs, Sep Jobs report, CPI, PPI (all will come before Sept 17) don’t matter?

Interesting….

Your analogy of Big ship is nice/creative way of asking Rate cuts..

Agree. If there is an abrupt change in the next 32days there could be a change of course..

Especially since the ship is steming across open ocean at the moment. You may need to reach port tomorrow, but that still leaves plent of time, so no hair-on-fire decision making required right this nanosecond.

“One can make the argument that only a severe recession can wring out the excesses created by the previous artificially low rates. That a huge dose of pain for a year or two would be long- term beneficial. And a lot of seriously overweight folks could benefit from a period of near famine.” Yes. But the person proposing that argument is into S & M. Maybe they need a good spanking or a beating to enjoy sex. A few who comment here feel that “wringing out” the excesses, or “cleansing the system” is somehow virtuous. No rationale, really, just some Calvinistic notion that suffering and persecution is good for the soul.

In my experience, some folks are natural pessimists and others are natural optimists. The pessimists have been running for the hills since before the Great Recession and have completely missed out on the greatest bull market in history. Like everyone, they want to be right. Nobody wants to be wrong especially when realizing the amount of wealth that they’ve lost. I was a pessimist for a long time and missed out on a lot. I know. It sucks. I was fortunate to have a friend, an optimist, ask me if I had been right or wrong in my predictions, I responded with “wrong”. He then asked me “how long do you plan on being wrong?” I began dipping my toe into optimism and have been handsomely rewarded.

HowNow: Not just S&M enthusiasts, but basic rules of nature acknowledge:

Stress and Rest is a healthy cycle. Daily we wake, experience activity and sleep.

If we seek greater strength and fitness, we will increase the daytime intensity of activity, only to take some time off… to rest and recover.

If one wants to “juice” their gains, supplements, then steroids and more are possible… but cancer may lie ahead.

Conversely, if I add calories and stay on the couch, I will also see gains, in excess weight. I will actually lose capability and functional capacity, even though I gain in one metric (weight). Again, systemic dysfunction is likely to creep in (diabetes).

The economy has grown mightily! I don’t believe most people want things to crash and burn. The problem with the MMT juice is that it’s created an unequal measure.

Depreciating currency, favoring corporates with bailouts and other policy changes to tax codes and financial systems creates un-equal opportunity. The masses can’t keep up and the insiders gain advantage.

We here on WS are doing the due diligence to (struggle? to) keep up. Once I catch the pack, it’s likely there will be another set of rules/ objectives (not talking rate cuts; more like a CBDC, new trade agreements or billionaire entitlement program).

Don’t worry, I still make my bi-weekly contributions to the Street. Even put this year’s raise completely into the “politicians retirement plan.”

Seems to me like the current powers that be are saying future generations can suffer for what they *think is their benefit now and pilling up huge debt and leaving it for someone else’s problem is what’s going to really bring pain on oneself.

No, you are wrong. The data they have now is not the data they will have then (Sept FOMC).

Between now and the Sept FOMC (September 18-19) we will get today’s CPI, one more PCE, one more CPI and one more PPI plus a jobs report and JOLTS.

Oh I didn’t mean there won’t be a halt to the weekly, even hourly stream of data. but I can see it could be read that way. It just seems unlikely that 30 days will radically alter the PPI direction described in the WS piece above.

Re: the huge gyrations in our markets and the wilder ones in the Japanese market: second biggest one day drop in the Nikkei, followed by largest ever rally. Isn’t that ‘net no change’ and therefore no cause for concern? No. the system is going unstable and chaotic.

Moving from control of ships to airplanes: the most feared event in a plane, apart from fire, is a stall. If anyone has seen video of the recent crash of the turbo- prop twin in South America: that is a super stall. Fell over 7000 feet in less than a minute. There is no sign of damage, no bits falling off, it has just stopped flying and drops like a brick.

A much valued characteristic in a plane type is early warning of a stall. The plane may droop one wing, or it may shake. This is the time to quickly put the nose down and gain airspeed. Because once a stall occurs it can be impossible to correct.

The result is a landing you don’t walk away from.

In the GFC the financial world hit a super stall. Banks wouldn’t lend to each other. Maybe the Fed, BoE, ECB, overreacted but at least the GFC wasn’t followed by a decade of depression.

LOL. Can we stop calling it the CFC, and call it what it really was, the Great Financial Fraud (GFF). MBS were a violation of 150+ years of contract law. Greatest financial fraud in the history of the world. Remind us, who went to prison? There wasn’t a depression, but there will be consequences.

Hedge accordingly.

Head line briefly on CNBC just a few minutes ago: ‘Rate cut hopes dwindle as inflation slows’

It’s gone now. Maybe someone said ‘huh?’

Near famine? I think people have lost sight of what a recession means in realistic terms. Wallstreet has fearmongered people into equating recession with apocalypse. Nothing could be further from the truth. The reality of the situation is this: a few percent of the population, most of which are likely just misfitted to their job, get fired. Most of those people then take a job that is a better fit to their skills and abilities, making the economy more efficient and productive. Somehow that doesn’t sound like near famine to me.

JeffD – …what was formerly termed a ‘recession’ appears to have been semantically-inflated to equivalence with the horrors of a true ‘depression’ (causes of the last one we, of course, permanently-‘fixed’ so it could NEVER reoccur, right? (Right?)).

may we all find a better day.

unfortunately the high base effect will continue to august and sept reading as the 2023 reading come to 0.7% and 0.4% respectively

Unfortunately, that’s total bullshit.

All you have to do is look at the blue line of the chart. And you’ll see what will fall out of the 12-month reading next month and every month for the rest of the year:

Services PPI, month-to-month not annualized. In bold what will fall out of the 12-month reading the rest of this year. In red what fell out in July (0.79%, the highest reading in over two years); what will fall out in August (0.17%) and in September (-0.08%), etc.

7-24: -0.16%

6-24: 0.42%

5-24: 0.38%

4-24: 0.57%

3-24: 0.09%

2-24: 0.35%

1-24: 0.58%

12-23: -0.06% = will fall out in Dec

11-23: 0.17% = will fall out in Nov

10-23: 0.09% = will fall out in Oct

09-23: -0.08% = will fall out in Sep

08:23: 0.17% = will fall out in Aug

07:23:0.79% = fell out of current 12-month period

@wolf, do you foresee similar base effect impacts to the upcoming:

CPI (today)

PCE (August 30)

Or are those not subject to the same situation (i.e. high readings falling off)?

No major base effect today in the yoy CPI today.

The financial news media has already declared that Powell will cut rates in September even before Powell takes the stage.

Yes, because it’s obvious.

No. That is not ‘obvious’ at all and price gouging continues all over the US economy including with gasoline and many things and services as we head into September.

I bought a boatload of TLT at $90 to hedge against current monetary leadership, which always seems to error on the side of interest rate dovishness. That trade has done very well lately.

This is no recommendation. I will be ditching TLT if it moves up much more. I think it’s a terrible long-term holding.

You inadvertently hedged against short-term rate cut hopium – not a bad trade.

I haven’t actually been short TLT in a couple months – took profit on those positions but planning to re-enter if duration keeps going up in price. No way this rally is sustainable with short rates >100bps higher.