The “real” policy rate is massively negative, with the new policy rate of 0.25% far below Core CPI of 2.6%.

By Wolf Richter for WOLF STREET.

At its meeting today, the Bank of Japan raised its policy rate, the “uncollateralized overnight call rate,” by about 25 basis points, to “around 0.25%” from the range of around 0% at the March meeting. Before the March meeting, the rate had been negative (-0.1%).

The policy rate is far below the inflation rate in Japan. Annual core CPI accelerated to 2.6% in June. The BOJ’s target for core CPI is 2%. And the “real” policy rate (policy rate minus core CPI) remains massively negative at -2.35%.

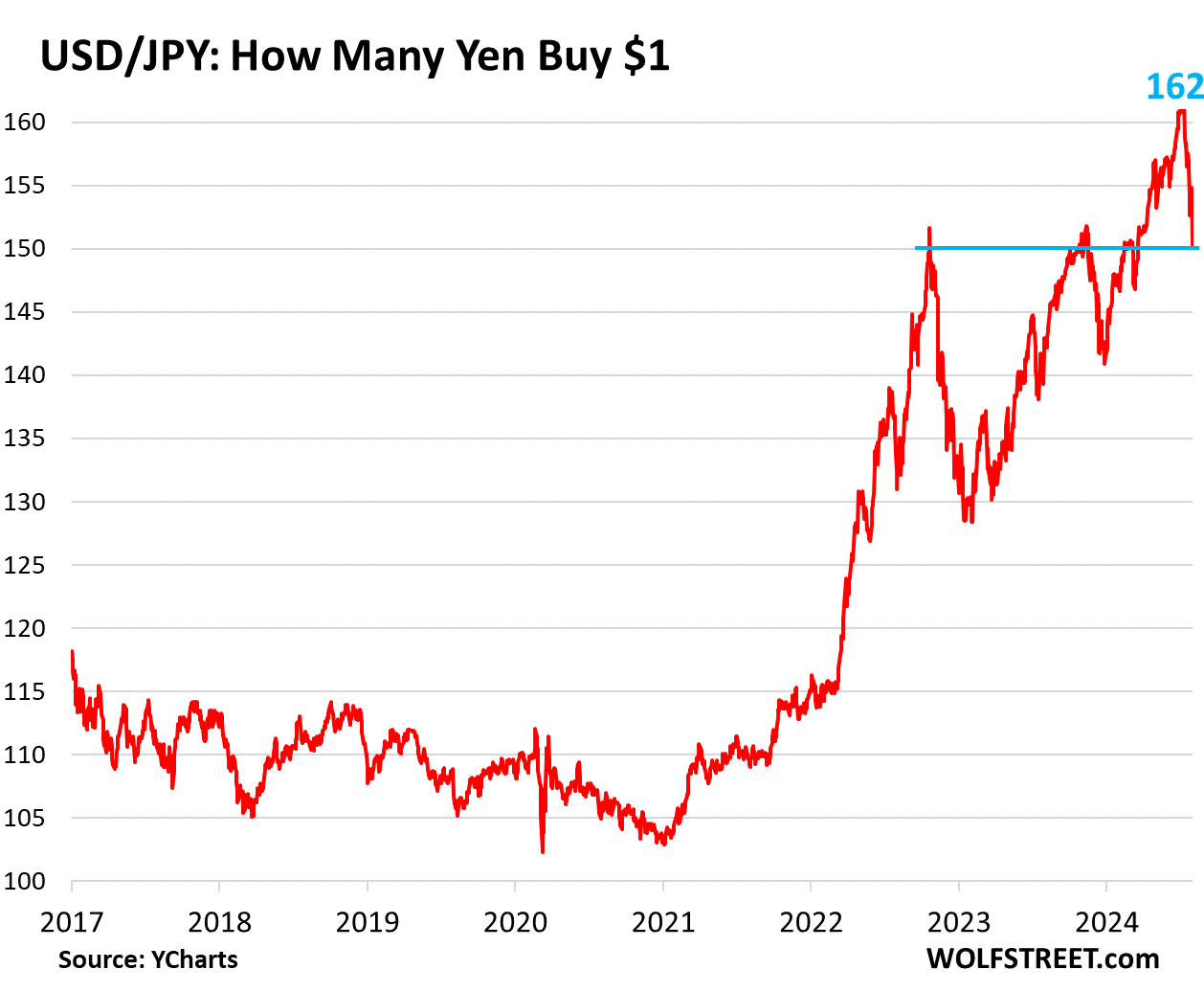

So the BOJ is very late and very slow in raising its policy rates, and the yen has plunged over the past two years as a result of it. It’s the plunge in the yen – and its effect on prices of imported goods, including energy commodities – that has forced the BOJ to get off its crazed interest rate and QE policies.

At the press conference, when asked about another rate hike in 2024, BOJ governor Kazuo Ueda opened the door for more: “If data shows economic conditions are on track, and if such data accumulates, we would of course take the next step,” he said.

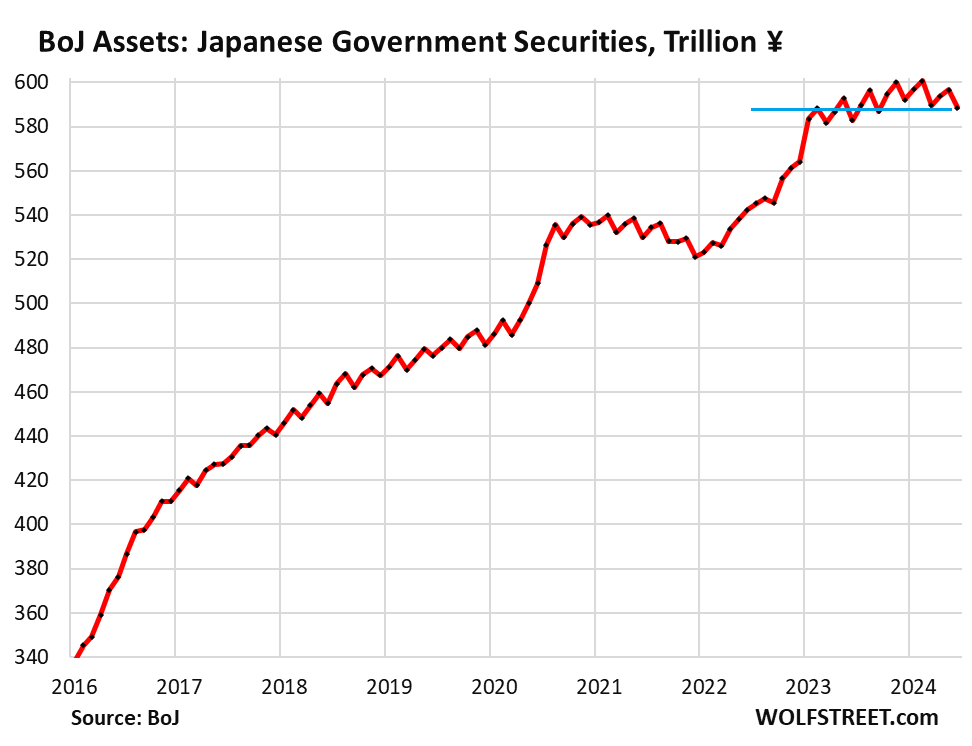

Initial QT starts now: The BOJ announced that it would start running off its holdings of Japanese Government Bonds (JGBs), at a rate that increases every quarter, until the monthly runoff reaches its full speed of about ¥3 trillion per month ($19 billion per month at today’s exchange rate) in January-March 2026. And it would then continue at that pace.

About ¥6 trillion in JGBs on its balance sheet are maturing every month. The BOJ has been replacing most of them in recent months, so that its holdings of JGBs have declined very gradually from the peak in February 2024.

This decline will accelerate until the decline rate hits about ¥3 trillion per month in early 2026. After this long ramp-up period, its JGB holding would continue to decline at about that rate.

The BOJ’s holdings of government securities through June:

That the BOJ would shift to QT was announced at the last meeting. What was new today were the amounts. The BOJ provided this schedule of the decline of its JGB purchases to increase QT:

- July 2024: actually purchased ¥5.7 trillion ($38 billion).

- Aug-Sep, 2024: to purchase ¥5.3 trillion, for QT of ¥700 billion per month.

- Oct-Dec 2024: to purchase ¥4.9 trillion, for QT of ¥1.1 trillion per month.

- Jan-Mar 2025: to purchase ¥4.5 trillion, for QT of ¥1.5 trillion per month.

- etc.

- Jan-Mar 2026: to purchase ¥2.9 trillion, for QT of about ¥3 trillion per month

- Going forward until further notice: to purchase ¥2.9 trillion, for QT of about ¥3 trillion per month.

How big is this QT? When QT reaches about ¥3 trillion per month in 2026, it would represent a reduction of its JGB holdings of about 0.5% per month. How much is that relative to the Fed’s Treasury QT?

By comparison, the Fed, which at peak held $5.8 trillion in Treasury securities, rolled them off at a pace of $65 billion a month, after the three-month ramp-up period. It maintained that pace through May 2024. So when QT entered full speed in September 2022, the Fed rolled off about 1.1% of its Treasury holdings per month. The Fed has now rolled off $1.33 trillion of its Treasury holdings.

So the BOJ is very slow in ramping up QT – instead of three months, as the Fed had done to ramp up QT, it takes its goodly time through 2025. And when it finally gets to full speed in early 2026, it will be at half the relative pace of the Fed’s Treasury roll-off.

To prop up the plunging yen. The BOJ is doing minuscule rate hikes, way too late, and is very slowly accelerating QT to a pace that will ultimately be half the Fed’s full pace. But it is moving in the right direction, and that has given initial support to the yen to keep it from collapsing further.

The prior announcement that the BOJ would shift to QT (while leaving the decision on the amounts to this meeting), and the anticipation of further rate hikes, based on what BOJ governments had mentioned in their speeches, accompanied by large-scale and very costly currency interventions over the past few months, finally started to support the yen in July. Today, the yen traded up at ¥150 to the USD. Back on July 4, it had hit the low point of ¥162 to the USD.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is not about the BoJ move but related I think. The Fed has not announced yet I believe, but the market is reacting as though it is going to cut rates. Is the market just overly optimistic or has there been a decision to cut and it has leaked before the announcement ?

The market has been in and out of rate-cut mania all year.

I’m hoping Powell puts a damper on it, but I am far from optimistic.

The Fed could very well signal a cut for September. At some point, rate-cut expectations are going to be correct.

But if it pushes back against the September rate-cut expectations, it’s going to get very interesting.

Small consolation price for a country that’s so far behind playing catch up. Only backhanded compliment you can give them is, at least they are not doing what Canada or the Swiss did..

Canada agree, but the perennial problem for the Swiss is the currency being too high. At times of US$ weakness folks hide in gold and the Swiss franc. Switzerland has a very robust manufacturing / exports sector which is hurt by this.

They tried pegging it but it gets expensive. If pegged to dollar they have to buy US$ and sell Swiss.

Funny thing: their guy in charge of this was thinking about ending the peg and, just talking about work, mentioned it to his bed partner. She goes out and speculates accordingly.

He resigned.

At the end of 2023 the Swiss Debt to GDP ratio was a bit over 17%. Nothing like us basket cases.

Anecdote: if cutting metal with electric ‘jig’, or reciprocating saw, don’t bother with any but Swiss blade. It’s red.

Nick,

Quite right, brains, energy, discipline and self belief are an unbeatable combo, largely lost by 1st world society. Travel by train from France through Switzerland to Germany and it is interesting to see the factories and industrial buildings start and stop on the borders of Switzerland, unusually so. A good currency investment but not so good for equities, which have to be bought out, S&P 500 of course.

In the end, it’s all about manipulating interest rates. I’m reading “The tapering pace may change, the BOJ said, adding that it will carry out buying “flexibly” to prevent a surge in bond yields.”.

Way I see it, QT and negative real interest rates (interest rate – inflation rate) won’t coexist for long, unless fiscal policy stops running deficits. A regular investor won’t want to buy a bond with a negative real yield if there are better options.

I think the jury is out on whether any of these QE economies can permanently exit QE. I hope they can.

“Kazuo Ueda opened the door for more: “If data shows economic conditions are on track, and if such data accumulates, we would of course take the next step,”

If this guy was an airplane pilot he would say he was flying nicely until the ground came up and hit him.

If there are any Japanese nationals (or people who have lived there extensively)– how high would inflation need to get to where there would be political consequences for the ruling party/coalition for not taking it seriously?

The government approval rating has been in the 2X% range for a long time, but every time, they get re-elected still. How much lower does it need to go for them to get kicked out?

It’s a de facto one party system here. A bit similar to Singapore, with the difference is that in Singapore they actually have capable people running the country, unlike here in Japan.

Higher for longer… BOJ front running Jay?

He’s back-running Jay by over two years, LOL

Two years? I think you mean two decades.

Well, the FED is running out of days for there so called high probability rate cuts? LOL

On another note. I am getting daily texts, or calls, or post cards for my flyover rental properties. A guy from Phoenix called me yesterday. Said he is not doing flips in Phoenix anymore and is looking to the midwest were houses are cheap.

Maybe before the last Japanese person dies and the race goes extinct they’ll have an interest rate above inflation, but not a second before.

At least their cties arent crime infested hell holes, so they got that going for themselves unlike in the US.

But they are, the Yakuza had their fingers in everything. Another hidden tax on productivity. The 1990s bubble is still rippling and echoing. We should take heed and not repeat their policies. But alas, BoC and all the west are addicted to debt at the cost to society.

All empires collapse from within. Lets see what happened the next 2 years .

You are just showing that you get your information from sources that are looking to take advantage of your ignorance and fear.

Crime in most cities is way down.

Get better sources of information and you will appear to be much more intelligent.

> Get better sources of information

How about CNN and MSNBC? Are they on your approved list of information sources?

I think you are projecting your biases on to everyone else.

Point is, using better information sources leads to be a better informed person. If the information sources you use keeps leading you to be misinformed (like the poster above about crime) why do you continue to use them?

I have a theory that some people do not care about being informed but instead are looking to have their biases confirmed. That seems dumb to me, as I prefer information to ignorance, but everyone’s milage may vary.

“accompanied by large-scale and very costly currency interventions over the past few months,“

I don’t trade/ know forex BUT I couldn’t help but notice that Thursday July 25 was a very high volume day for the USDJPY and EURUSD pairs (probably others?).

I have also hear people saying that the Japanese central bank was propping up the Yen, but didn’t say anything publicly, to not be labeled a “currency manipulator.”

Isn’t that the stated job and expectation of central banks?!?

When all you have is a hammer?

Everything’s a screw.

Looks like my wife and I will continue increasing our stockpile of JPY. Both for a potential real estate purchase and for our next trip to visit her family.

Thank you for you updates on the BOJ even if it’s not your most popular subject!

Unfortunately when looking at the Japanese economy, most people look at it like it is the U.S. economy and unfairly criticize it based off of that false comparison. Japan is not the U.S. There are very distinct differences, from savings rate to consumer and labor behavior. Different economy and different culture. Their economy is highly dependent upon exports which is different than the U.S.

So I am hesitant to pile on the Japanese Central Bank because I think many of its critics are looking at it through a U.S. lense which is wrong.

All of that said, the Japanese Central Bank is way too late and tightening way to little. They need to be better.

Hi Wolf. can you please share your views on Yen carry trade? Is it something that investors need to worry about at this stage? Or may be at what level of interest rate in Japan or interest rate differential between US and Japan? Thanks

The carry leveraged trades are being unwound as we speak for last 4 weeks.

NON-COMMERCIAL FUTURES ONLY POSITIONS (CONTRACTS OF JPY 12,500,000) dropped ~22.4% from maximum of 220973 SHORT Contracts to current 171498 SHORT Contracts.

The half speed of BOJ is negative news for JPY though. I see the following scenario to unfold.

Inflation in US will drop in autumn, FED will manage to cut 2-3 times 0.75bp (max 1bp) before inflation will start increasing in 2025 and FED will be forced to re-hike again.

-At current US interest rates at 5.5, FED will not be able to cut under 4.5.

-At current JP interest rates at 0.25, BOJ at half speed will be able to increase rates by max of 0.5bp to 0.75bp

– 4.5-0.75=3.75 approximate differential in rates at the start of 2025 is still strong case for carry trades to continue [3.75% for free, leverage 1:2 7.5% for free, etc.]

-Think about it, it will take BOJ 2 years to increase rates to 4.5 at current speed, liquidity around world is increasing, central banks cutting rates and slowing down QTs, governments spending at all time high

-As inflation will start increasing at the end of 2024 again and/or if momentum in JPY will starts loosing strength, NON-COMMERCIAL speculators like hedge-funds, etc. will start repositioning and jumping back on carry trades again.

-We will see new lows in JPY again! It’s not over yet.

Certainly they were costly interventions, but they were also profitable interventions because the BOJ is unwinding dollar yen purchases with a much weaker yen.

Inflation is now in the public Japanese conversation and there may well be pressure on the government because the benefits for the average citizen are very hard to see.

I’ve just come back and the prices haven’t burst yet, i mean the price increases are noticeable but not in your face. In the UK over our recent bout with inflation I was noticing prices changing three times in the year.

Not like that with Japan. I think also for Japan shrinkflation is not a flier, because they had deflation for years they are already on tiny portions or maybe thats just my view.

I would be very interested in Wolf’s view on the repatriation trade because certainly as time goes on we are getting closer to either the yen dramatically strengthening from the repatriation trade, or simply that it does not.