New Highs: Boston, New York, Miami, Tampa, Los Angeles, San Diego, Washington DC, and Chicago.

By Wolf Richter for WOLF STREET.

The S&P CoreLogic Case-Shiller Home Price Indices, released today for “May,” are three-month moving averages of home prices in 20 metropolitan areas whose sales were entered into public records in March, April, and May. So that’s the time frame.

Over this period, home prices in all 20 metros increased from the prior month, in most of them at a slower pace than in the prior two months, as home sales have plunged and active listings are now surging.

Prices were still below their 2022 highs in 7 of the Most Splendid Housing Bubbles (month of peak):

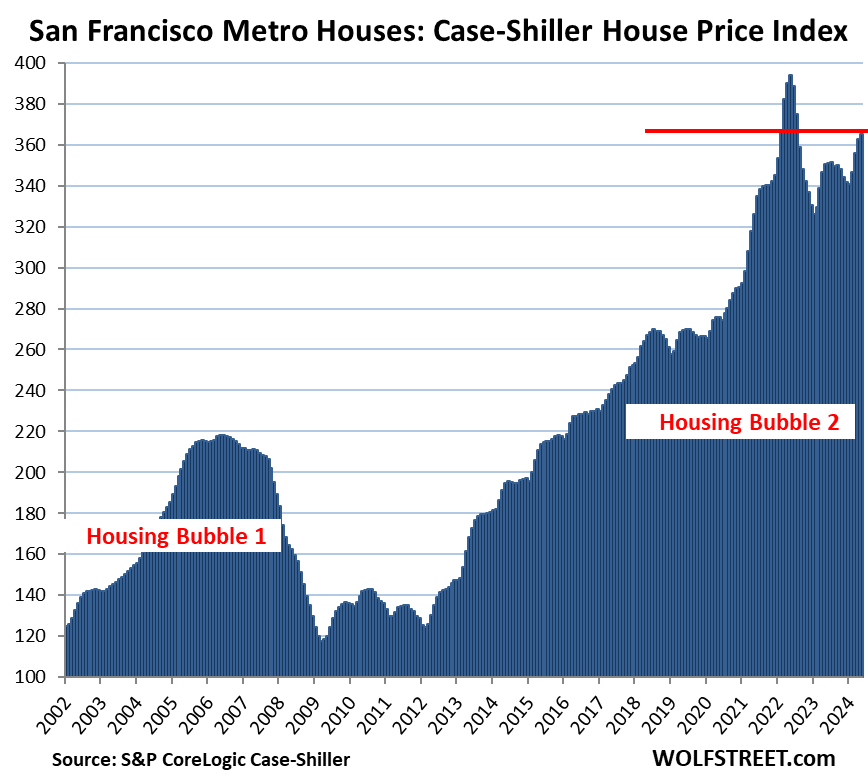

- San Francisco Bay Area: -7.3% (May 2022)

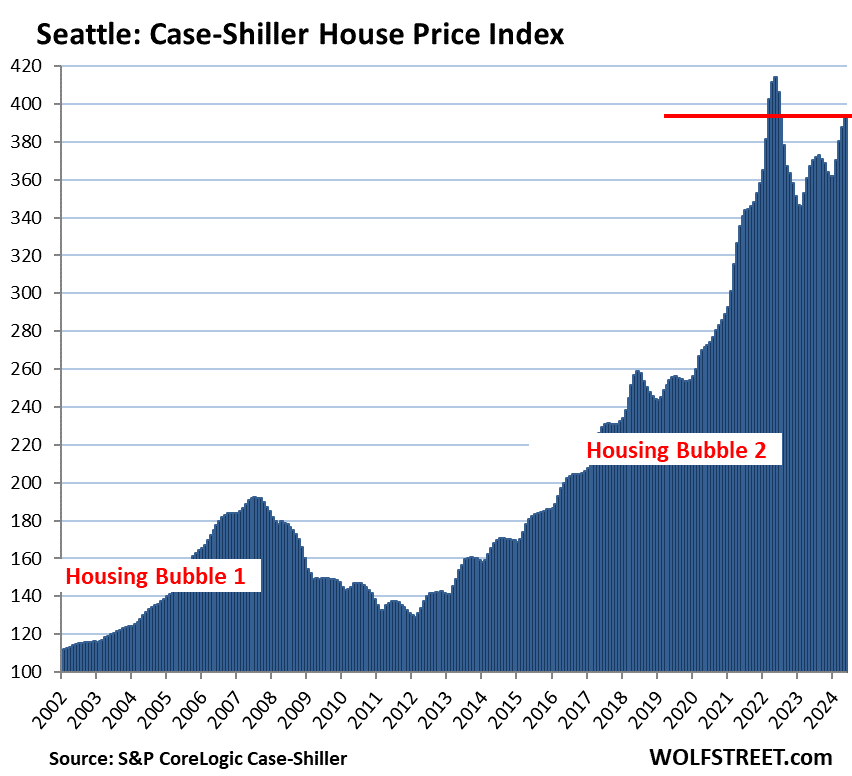

- Seattle: -4.9% (May 2022)

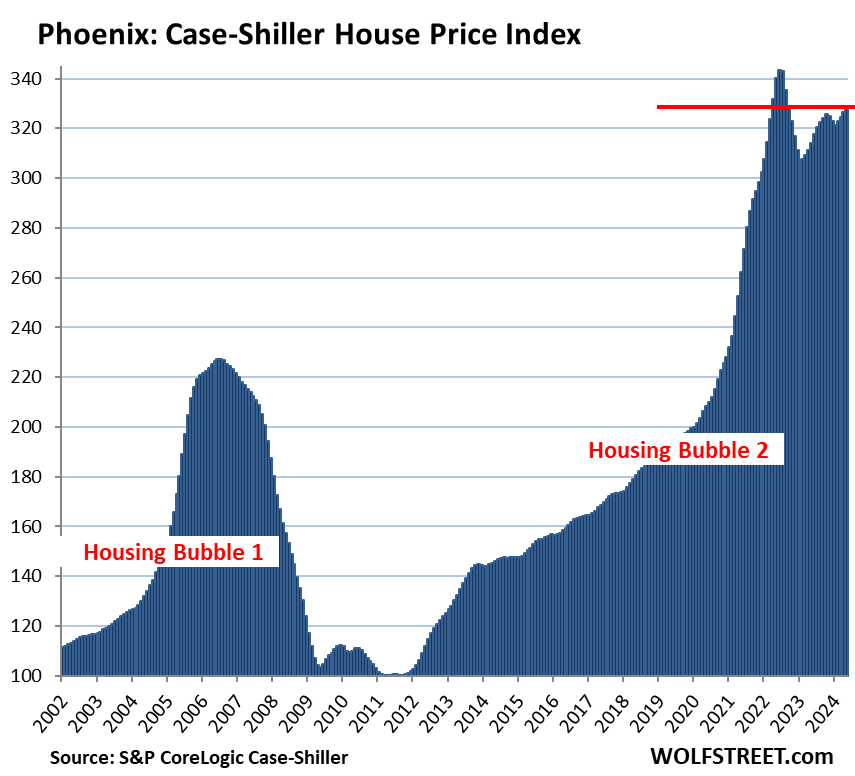

- Phoenix: -4.6% (June 2022)

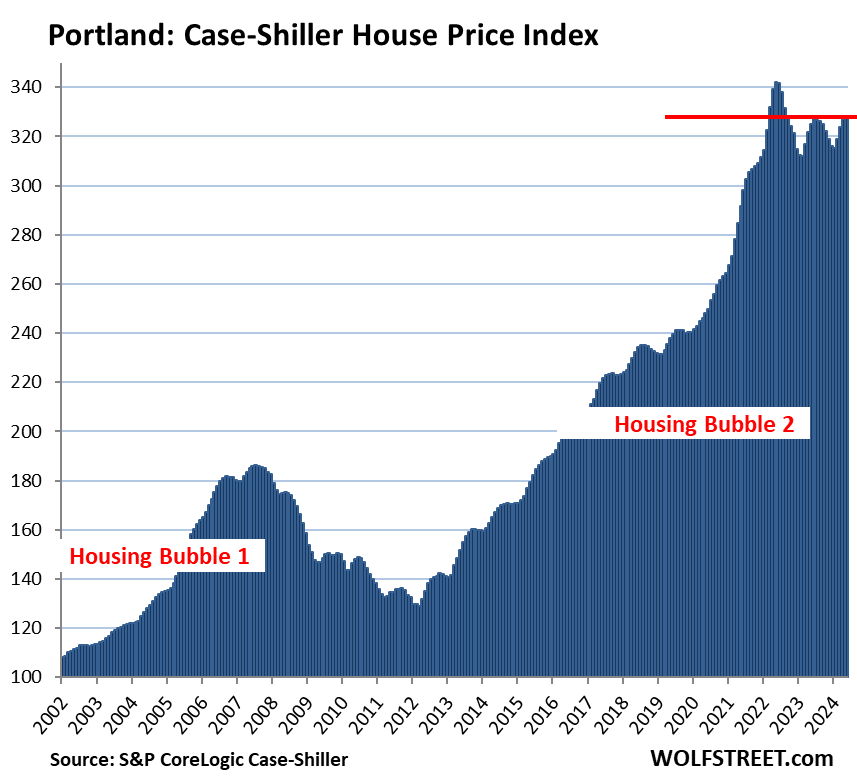

- Portland: -4.1% (May 2022)

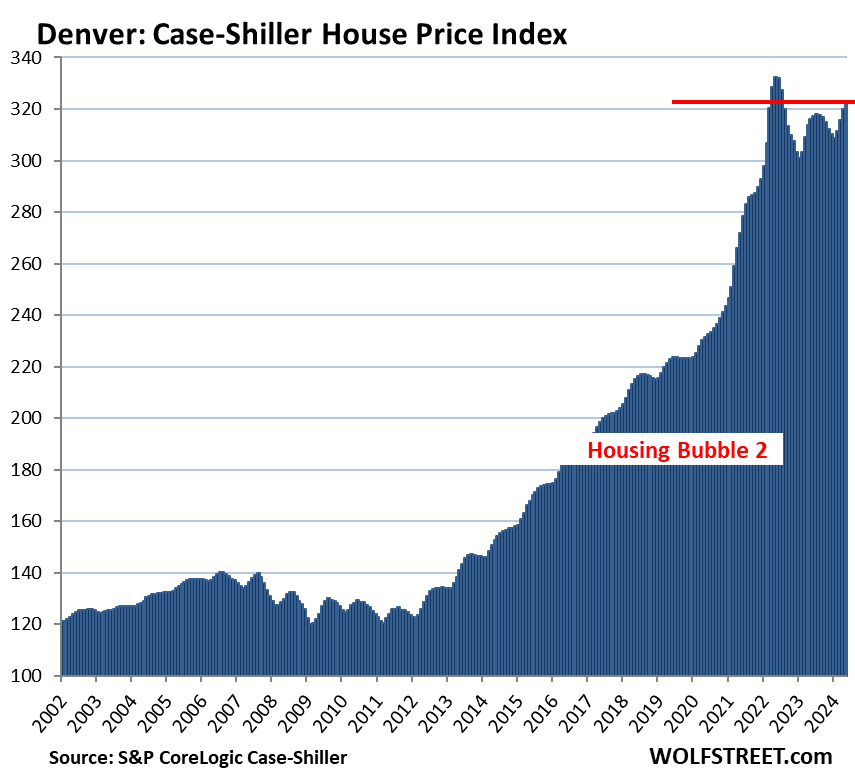

- Denver: -2.9% (May 2022)

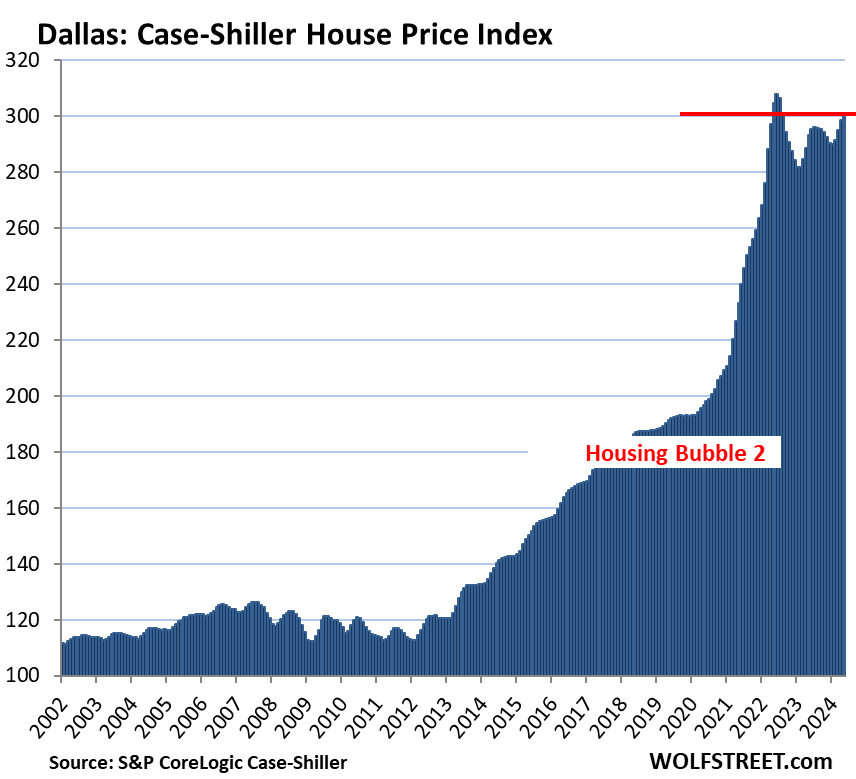

- Dallas: -2.3% (June 2022)

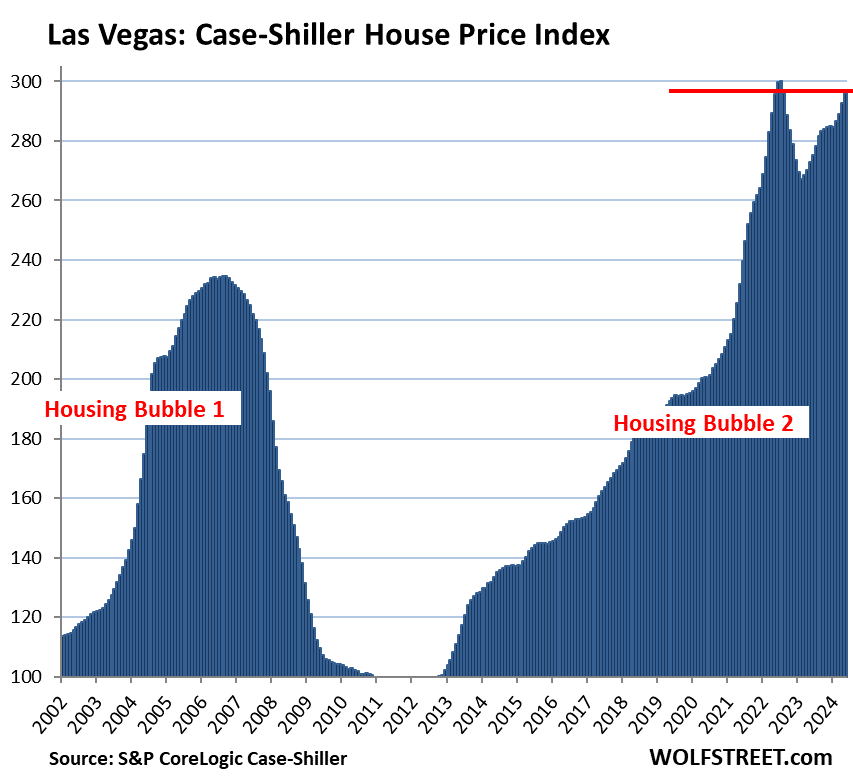

- Las Vegas: -1.3% (July 2022)

Prices set new highs in 8 of the Most Splendid Housing Bubbles, in some cases just a hair above their May/June 2022 highs. In terms of this 2-year time span among the 8 metros, gains ranged from 1.2% in Tampa to 11.6% in the New York metro.

The most splendid housing bubbles by metropolitan area.

San Francisco Bay Area single family houses: the San Francisco metro in the Case-Shiller Index covers a five-county portion of the nine-county Bay Area.

- Month to month: +0.7%

- Year over year: +4.3%.

- From the peak in May 2022: -7.3%.

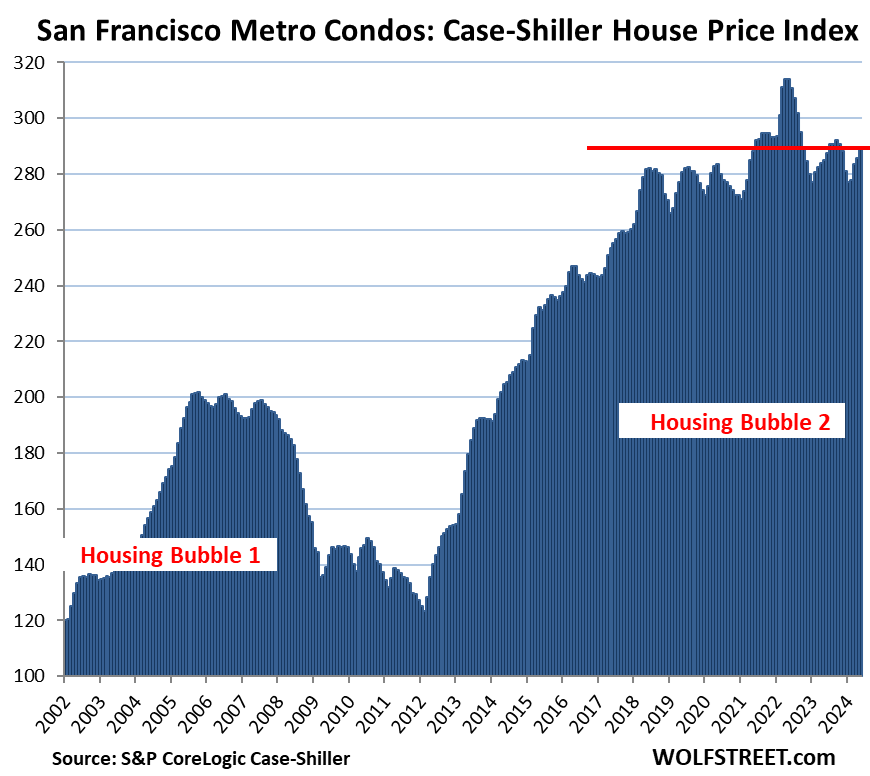

San Francisco Bay Area condos: Condos are a big part of the market in the Bay Area, particularly in San Francisco itself.

- Month to month: +1.2%.

- Year over year: +1.5%.

- From the peak in May 2022: -7.9%.

- Just a tad above May-August 2018.

Seattle metro:

- Month to month: +1.4%.

- Year over year: +7.1%.

- From the peak in May 2022: -4.9%.

Phoenix metro:

- Month to month: +0.4%.

- Year over year: +4.4%.

- From the peak in June 2022: -4.6%.

Portland metro:

- Month to month: +0.3%.

- Year over year: +1.0%.

- From the peak in May 2022: -4.1%.

Denver metro:

- Month to month: +0.9%.

- Year over year: +2.1%.

- From the peak in May 2022: -2.7%.

Dallas metro:

- Month to month: +0.7%.

- Year over year: +2.6%.

- From the peak in June 2022: -2.3%.

Las Vegas metro:

- Month to month: +1.2%.

- Year over year: +8.6%.

- From the peak in July 2022: -1.3%.

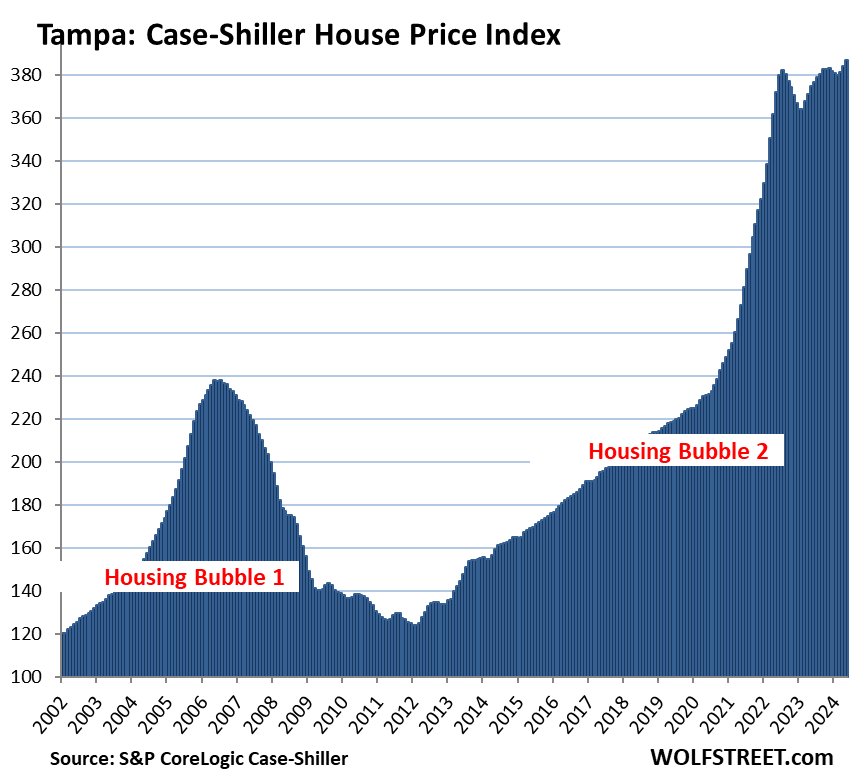

Tampa metro:

- Month to month: +0.8%.

- Year over year: +3.3%.

- New high, +1.3% from July 2022 high.

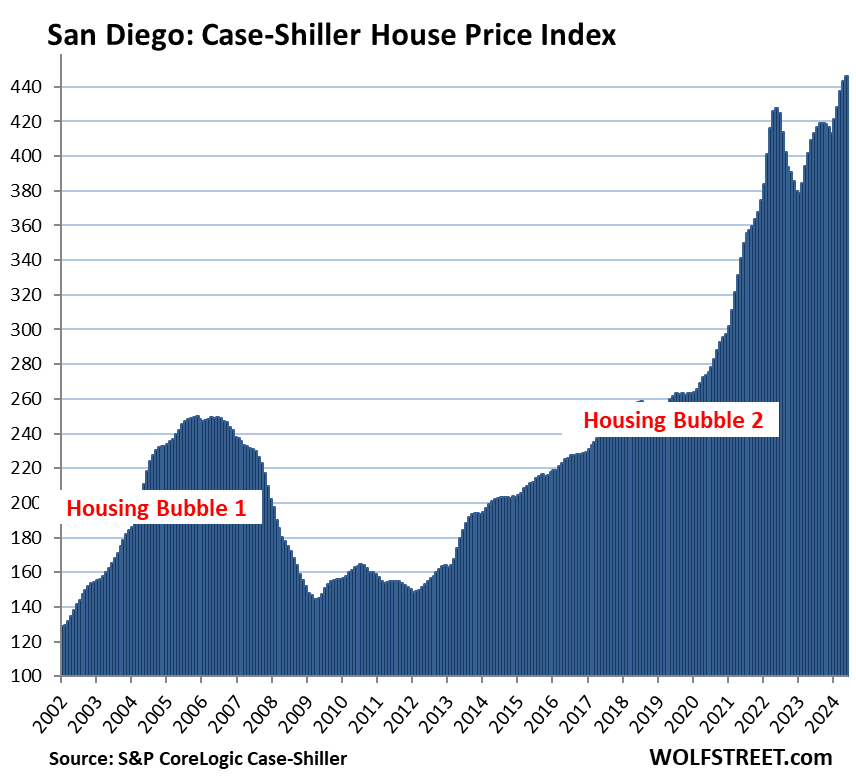

San Diego metro:

- Month to month: +0.7%.

- Year over year: +9.1%.

- New high, +4.0% from May 2022 high.

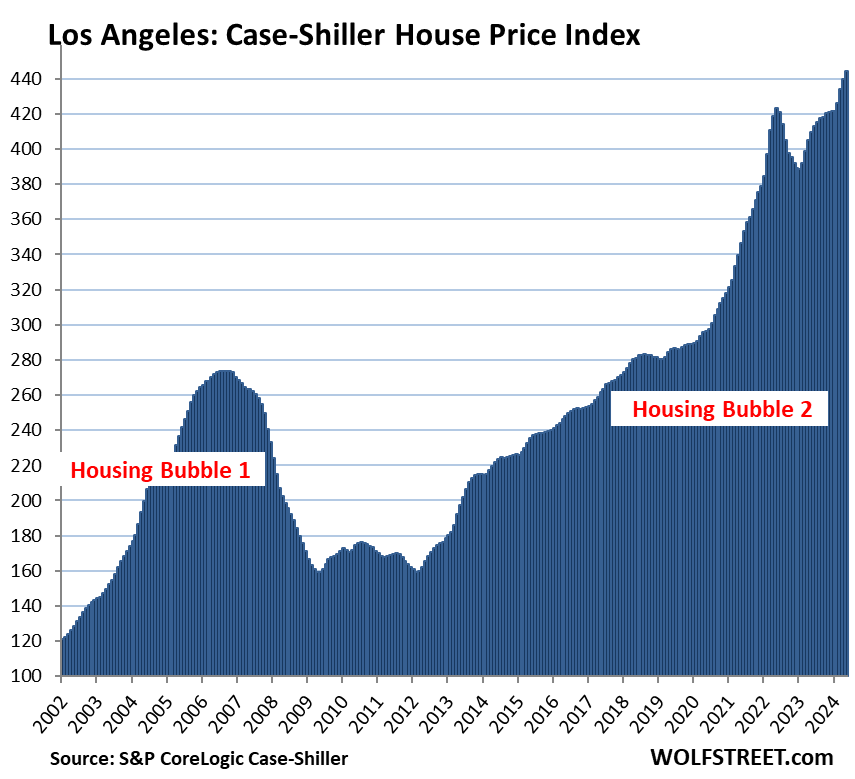

Los Angeles metro

- Month to month: +1.0%.

- Year over year: +8.4%.

- New high, +5.0% from May 2022 high.

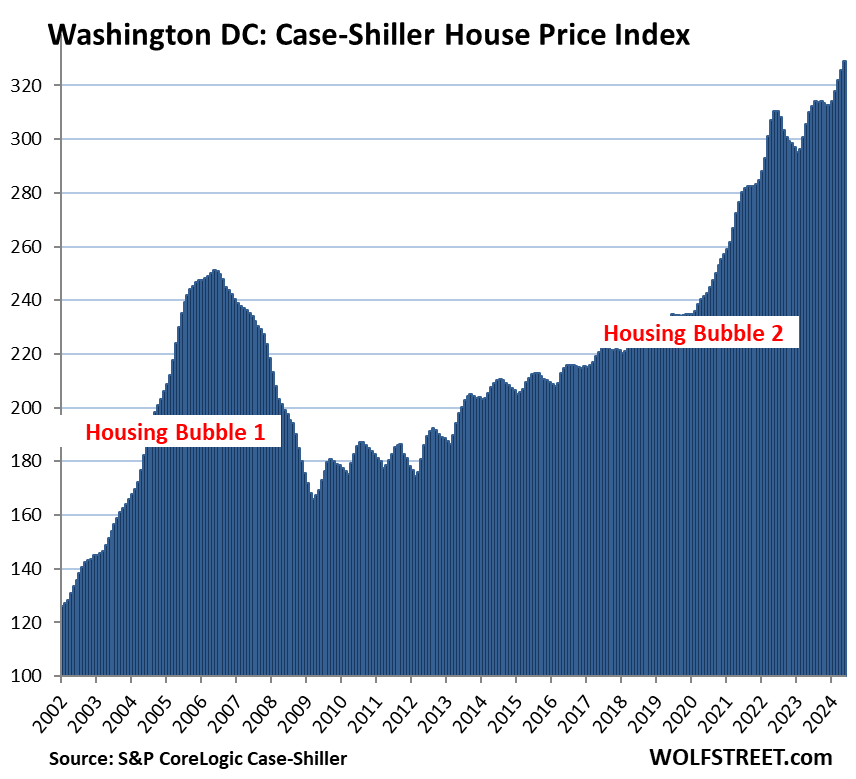

Washington D.C. metro:

- Month to month: +1.1%.

- Year over year: +6.1%.

- New high, +6.0% from June 2022 high.

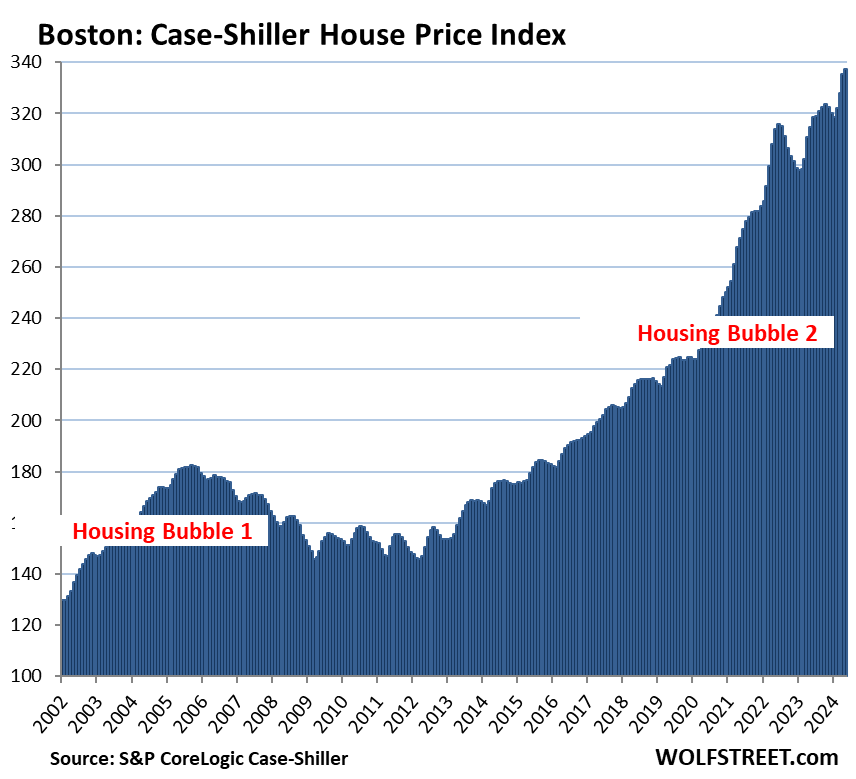

Boston metro:

- Month to month: +0.5%.

- Year over year: +7.2%.

- New high, +6.8% from June high 2022.

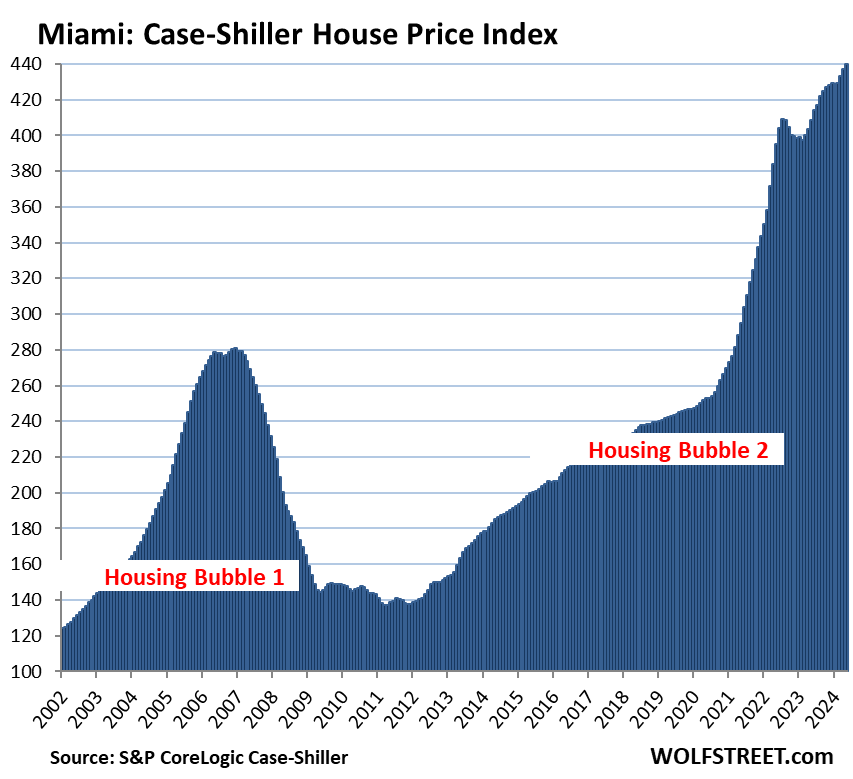

Miami metro:

- Month to month: +0.7%.

- Year over year: +7.6%.

- New high, +7.4% from July 2022 high.

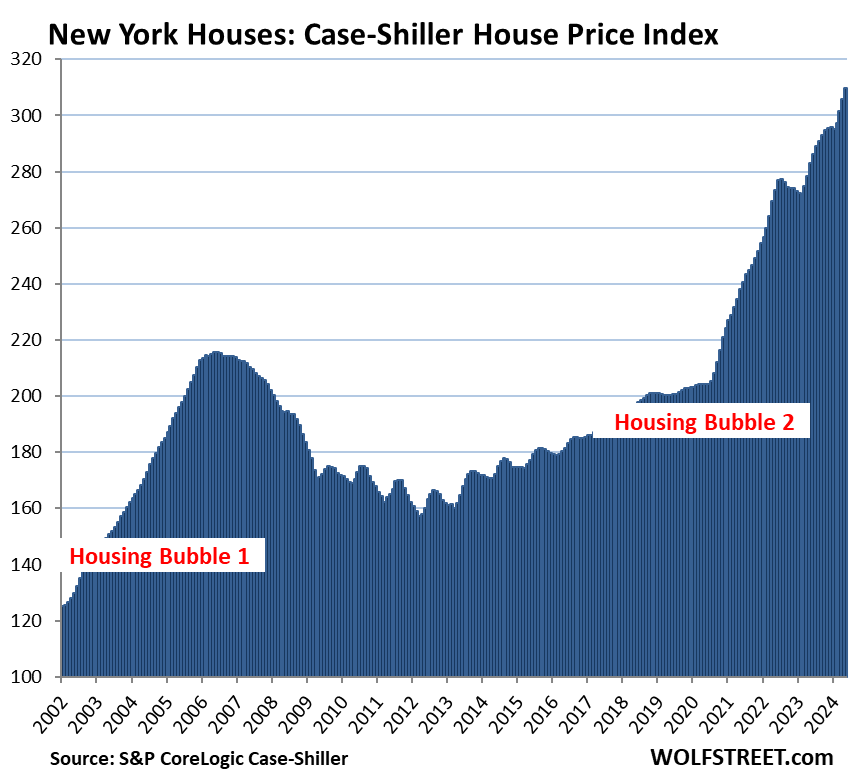

New York metro:

- Month to month: +1.3%.

- Year over year: +9.4%.

- New high, +13.2% from June 2022 high.

To qualify for the Most Splendid Housing Bubbles, the metro must have experienced home-price inflation since 2000 of 200% or more at the peak. The indices were set at 100 for the year 2000. Today’s index value for San Diego of 446 is up 346% since 2000, making San Diego the most splendid housing bubble on this list, ahead of Los Angeles (444) and Miami (440).

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses were sold previously. Price changes are weighted based on how long ago the prior sale occurred. Adjustments are made for home improvements and other factors (37-page methodology).

It’s home price inflation. By measuring how many dollars it takes to buy the same house over time, the Case-Shiller index is a measure of home-price inflation. San Diego had 346% home price inflation since 2000. Over the same period, consumer price inflation, as measured by CPI, amounted to 86%.

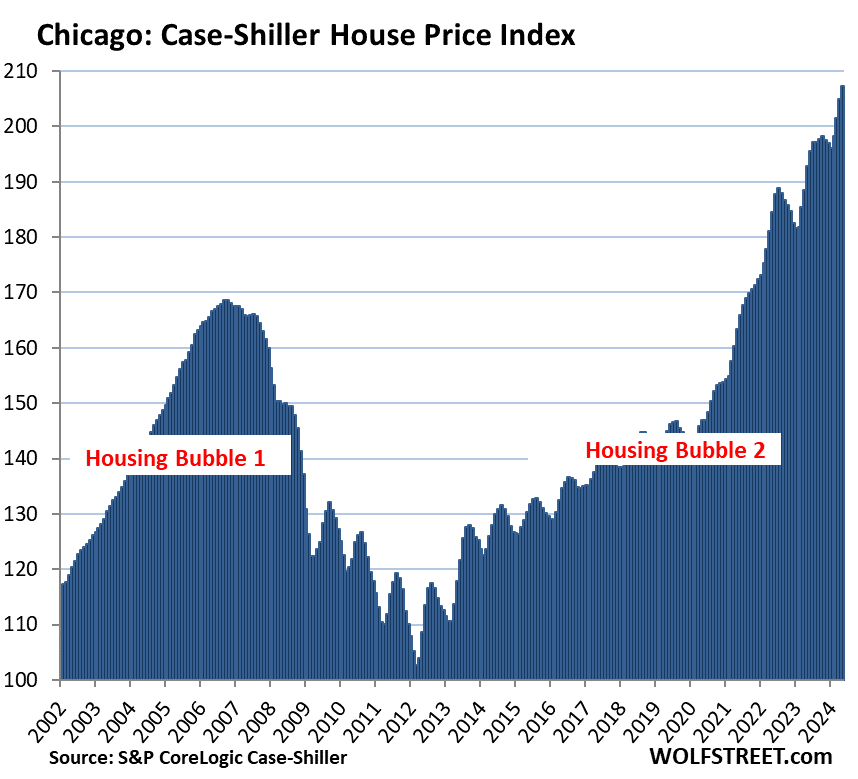

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had less home-price inflation since 2000 despite the price spikes in recent years, and don’t qualify for this list.

Chicago metro – includes 8 counties: Cook, DeKalb, Du Page, Grundy, Kane, Kendal, McHenry, and Will – has an index value of 207 and is up by 107% from the year 2000, and is therefore far from qualifying for this list. But the 46% price spike since the Fed started its money-printing binge in March 2020 has been sufficiently splendid, and it’s such a huge metro, so here it is anyway:

- Month to month: +1.1%

- Year over year: +7.5%.

- New high, +9.7% from July 2022 high.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Sigh,seems I will still be on strike as a cash buyer.

I am looking into unincorporated land that could build what I want without building to the insanity of the building codes(am a licensed builder).I realize no cops/fire but as I want rural by the time either arrive the issue has ended,I will have a built in fire suppression system and as for cops,well,shovel and a shotgun.I also realize will not be able to get insurance but since built my way(safe and solid)will not cost a arm and leg if I had to replace.

Oh,and no property taxes.

Sadly you and I, the volunteer strike buyers seems to be the very minority out of the equation. Majority are likely buyers on strike because they can’t qualified, if as a whole home buyers are more selective about going on strike when fundamentals are not there, we probably would never withness what happened with all the bidding wars, over asking…etc

On the other hand, playing with mortgage calculator, I still have a hard time wrapping my brain around paying for a down payment of $600K, to buy a normal looking place at what’s consider normal now at $1.1M in SoCal, you still have to pay $4600 a month or more for 30 years…that math is just insane to me. Perhaps plenty of people have $600k or more laying around for downpayment or maybe paying even more than that for a downpayment just so they can pay even higher monthly expense than renting something similar…mind blown…

Throwing some lofty numbers around there…

But yes — there was a motherlode of wealth created out of thin air the past many years. Putting pallets of cash in front of a wind machine would’ve been more subtle. This had the effect of pushing the envelope of price discovery and perception to a point of total distortion. Mix that with FOMO and you get what we’ve been seeing: New normal! Get your boots on before the next new normal!

Here’s an experiment: try to think of the scurviest most low-lived scuttlebums you knew 10-15 years ago and everyone in-between them and yourself. Are any of them not doing miles better than they were back then? I bet most of them are — be it from learning some whiz-bang-y technical vocation, to inheriting well, to flipping a hovel or two & sitting, or hell — maybe just starting a business or creating an Only Fans channel.

And I bet what you’re seeing now is a kind of protracted last gasp, where all that new money/winnings sitting on the sides is capitulating and getting back in. What’s overpaying by a $100-300K when you have that in free cash? And then just look at your portfolio and the steam coming off that. What’s to fear? People have more anxiety over what color to paint their toenails than whether to overpay or over-extend themselves on a house purchase.

It’ll take years for that fat to boil off. A decade? I feel for anyone without rich parents who has organically grown their wealth, saving a downpayment over the years through being abstemious & disciplined — brown bagging it, driving a beater, waiting on family formation…hell, even a pet.

I know several such couples, and my sense is that they’ve just moved on. Housing has even become a subject so depressing as to be verboten in conversation; “oh, god — let’s talk about something else…”

Phoenix_Ikki,

“Sadly you and I, the volunteer strike buyers seems to be the very minority out of the equation.”

No you’re not. We have documenting for a long time how demand from people who need mortgages has collapsed; and how demand from cash buyers is also down. And total demand has plunged — even as inventory and supply have surged.

Here is the latest on the collapse of the demand:

https://wolfstreet.com/2024/07/23/here-comes-the-inventory-of-vacant-homes-with-buyers-on-strike-despite-lower-mortgage-rates-supply-spikes-to-highest-in-4-years-sales-drop-except-at-high-end/

Are sales down because people are going on a buyer’s strike. Or are sale down because people who would like to buy a home cannot because of other reasons ?. For example, maybe banks have become more stringent on loans (higher standards, pre-qualified) since the free money era went out the window and the era of expensive money is upon us. Banks are no longer to loan to whoever anymore since money is expensive now.

With the evidence present with this recent article. I think it’s safe to say that those people who are buying are not buying for a “lesser rate.”

The buyer’s strike doesn’t exist in reality if cities keep reaching all-time highs.

By hiking rates, the Fed is forcing people to go on buyers’ strike because they didn’t want to go on buyers’ strike voluntarily on their own and instead kept pumping up prices by being idiots. That’s not a secret. It’s the purpose of rate hikes — and not just concerning people buying houses, but concerning people and businesses buying anything.

My credit union basically laughed me out of their office last year.

Yearly gross income: ~87,000

Debt: 0

Credit score: 780+

Down payment: 25,000-35,000

Eligible for FHA.

Was looking at a budget of 250-300k. They said it likely wouldn’t pass underwriting if I could find something in that price range. Then even if I could, everything at that price wouldn’t pass a home inspection or be allowed to lend on. (E.g. crappy mobile home, no power to property, mineral rights?)

Thanks Wolf, seen that data many times and do understand mortgage application is down. I do wonder how many of these are truly due to protest from buyers (that can afford the down payment and monthly) but decide not to even bother because of insane price to value or how many are on strike because they crunch the numbers and just can’t make it work so not bother to even apply. Hopefully it’s the former if there’s any hope of this market to correct in a meaningful way.

I’ll just repeat this here: By hiking rates, the Fed is forcing people to go on buyers’ strike because they didn’t want to go on buyers’ strike voluntarily on their own and instead kept pumping up prices by being idiots. That’s not a secret. It’s the purpose of rate hikes — and not just concerning people buying houses, but concerning people and businesses buying anything.

Replying to folks below:

I am in Southern Calif and I can tell you, home sales are down because people are not able to afford the monthly payments.

A inland city, where median income is $50K, home prices are ~$10K/month which is inclusive of all things one can think of.

Normal Joe are not on strike on their own will. They are not buying because they can’t afford monthly payment. Things can’t be simpler than this.

New home sales have been much better due to builders offering to buy down mortgage rates. This shows the demand is there, people simply cannot afford it at these rates. Once mortgage rates start falling substantially we’ll return to a 2019 style market, no crash necessary.

Cash buyers are down because there’s better places to invest your money. I’m a RE investor and I’ve been selling off my residential investments and buy heavily depressed bond CEFs and good quality CRE. Rents are down and prices are up in the single family space which has been driving cap rates into the dirt.

James,

Property taxes on vacant land still needs to be payed. Sounds like lots of trees where you plan on building, fire zone?

40 acres, no building code rural Arizona (no utilities for miles) Put in septic system, 2,000 gal water tank, potable water delivered, solar on roof, propane gas.

9 miles down a bumpy dirt road, closest neighbor 2 miles away. Built 40 x 50 ranch style house (have hammer and brains).

Snow bird there for 25 years. Got tired of living way out (sold it) now living way in. Got lucky and found a good fixer-upper with lots of good neighbors here.

The rattlers, mountain lions, deer, Coyotes, javelinas and the creepy crawlers usually didn’t spook the new comers, it’s the solitude that drives them away.

Plenty of cheap vacant land without a building code in Arizona, prices are up some but not much… Whoop-de-do.

Cool toad,glad to hear you found the right place,good news has been lacking lately!

Unincorporated has no town taxes/hence no services excepting what the locals willing to pay for.

A example is plowing and dirt road grading,a friend did unincorporated and those were his costs,his share was very reasonable and the guy who had grader lived there also so had a lot of incentive to do a good job.

My search continues but feel for the time a lost cause.

Sorry but that 2nd chart of S.F. condos looks like a hand flipping the bird. :)

A lot of these condos were bought by investors for price appreciation (who may try to cover their carrying costs by trying to rent them out long-term or as vacation rentals). And those investors, having hoped for massive price appreciation, may feel they’re being shown what you so elegantly explain.

Cash flow negative investments are often an intentionally made decision. It’s so common there’s a term in finance—a negative carry trade. These are used to speculate on the trade value of a price, ignoring the actual revenue of the asset. They’re taking a gamble strictly on being able to sell the asset to someone for a higher price in the future. This method of investing is better known as Greater Fool theory, since there’s usually a fool that will pay more. The speculators just hope they aren’t the greater fool—the final in the chain that’s stuck with a losing asset.

Just like the parlor game of musical chairs!

SF residential investments has been cashflow negative for a long time, and in foreign markets like Canada, Switzerland, Australia, cashflow negative is the rule.

It’s as much speculation as buying US equities. It’s an investment based on the theory that SF economy will continue to do well and the city will continue to be NIMBY central.

However, the price drop has nothing to do with speculator, it’s a very local issue due to tech layoffs, WFH, and the homeless epidemic. Look at SFH prices in the greater SF region overall, it’s up. Look at NYC condo prices, it’s up.

Thank you again! (and again!) Wolf!

My son had been looking and talking about buying a house in Denver in 2022. All of his many friends were also looking. Prices for cr*ppy flips were very high. We insisted that he get an independent inspection and the results in some cases were horrifying. Leaking pipes in the walls and illegal electrical. People were trying to shoddily turn houses for a massive profit in 2022.

My son hasn’t mentioned looking for a house in the last year. His friends have also stopped. They are helping stop the irrational exuberance.

As long as his rent is still half the amount he would pay for a mortgage, he is happy to rent.

Rents will eventually go up and house prices will flatten or go down and when the costs meet, it is time to buy.

He continues to pay rent that is half of what he would have paid if he purchased and he waits.

IMHO, 2022 was driven by a psychology of the masses. We need a little fear in the housing market. Just a little.

I always have an additional anecdote.

My oldest daughter purchased a house in 2015 in Raleigh that was 15% less that the original owner purchased it new in 2006.

The PITA was less than what it would have cost for her to rent a similar house.

Those were the days when buying a house was a no-brainer.

We are still far away from that point today.

Extremely far apart. Wife and I sold our house in Michigan and moved to the Raleigh metro area (Apex) two years ago. Currently renting a 4 br/3 ba home on 1/4 of an acre. The equivalent mortgage — even putting $100-$200K down — is easily $1,000-$1,500 more than the rent I’m currently paying. Factor in no maintenance or improvement costs and it’s more like $2,500-$4,000 per month saved vs. buying a house.

I hate we’re no longer owners and that I can’t have my own place the way I want it, but at these prices and interest rates, I’m joining the ranks of rent forever until things change. We COULD buy tomorrow, but it doesn’t make any financial sense, plus I don’t want to potentially be the one catching the falling knife.

Also, the benefit of having owned a house before and doing capital improvements educated me and opened my eyes to how much time, effort, and (especially) cost there is in doing that work. A lot of these buyers who bought over the last three years and are maxed out have NO IDEA what’s coming when then need to replace a roof, or windows, or siding, or a deck, or… or…

I can never tell if the Millennials that bought the tiny townhomes in the questionable parts of town for a half mil just don’t have any class or if they have those sheets hanging in the windows because they’re out of money.

Lack of money is no excuse for the weeds in the 25 square foot of front yard flower bed, though. That’s just lazy.

Generally, I think people paying high prices for homes should bring up a neighborhood, but I’m not sure how it works anymore.

True. I didn’t include maintenance.

My daughter purchased a 9 year old house in 2015. My experience is that appliances, furnaces, AC, water heaters have a 7-10 year lifespan.

She is having to come up with some of these expenses on top of the PITA.

Roof, window, and siding expenses come up after 15-20 years.

Be prepared or buy a used house with most of this replaced.

I don’t know what home buyers who have PITA twice rent are doing? Maybe they have great wages or invested in AI. :-)

I’m waiting too.

With QT going on for the 3rd year, you would think m2 would go down…it’s not

A little? Try a lot, look to our stock market as reference when you try to inject just a little fear…doesn’t work….BTFD and FOMO comes right back the next day. You can’t un-entrench 20 year+ plus hot hand fallacy in people’s mind with tepid slap on the hand fear IMHO.

I’m waiting too.

With QT going on for the 3rd year, you would think m2 would go down…it’s not

Also in Denver, finally found some houses in my price range in the location I want that look decent (this is not due to price cuts sadly, just more people trying to sell). Mortgage + property taxes + ins with putting 20% down would be $2000 more per month than my current rent. This would be my own house vs the townhouse I rent now and slightly more square footage, a yard and a garage so it’s not Apple’s to Apple’s to but still feels ridiculous considering the size of the down payment. The uptick in inventory is helping, I think sellers/investors are finally starting to worry. If the buys strike continues a bit longer, hopefully we get a reasonable correction.

I note (from FRED) that since 2010 the M2 money supply has gone up from 8.6T to 21.5T. That’s up by 2.5 times. Maybe that has something to do with it? You think”

M2 money supply is a bad metric (by what it includes and excludes). For causes, look at the Fed’s massive balance sheet and its low interest rates starting in 2008 that persisted to 2022. There is now a huge amount of excess in the system that will take years to burn off.

Perfect head and shoulder set up in most cities.

Fingers crossed. If homes keep going up at the current rate, society will unravel, as young people will never be able to leave their parents home without shouldering a significant downgrade in living conditions.

Once again, extremely disappointing to see…either this Titanic refuse to sink or more like the drunken sailors, this is the new normal. Certainly more ammo for housing cheerleaders to gloat about housing will only go up tagline…

“San Diego metro:

Month to month: +0.7%.

Year over year: +9.1%.

New high, +4.0% from May 2022 high.

Los Angeles metro

Month to month: +1.0%.

Year over year: +8.4%.

New high, +5.0% from May 2022 high

Case-Shiller has the problem of not being timely. Many of these areas now have the problem of rapidly expanding inventory with the lowest volume in decades. It won’t take much of a recession to push it over.

My metro (Boston) is insane too. But this data is from the end of spring selling season and supply has risen a lot since then.

I take solace in the record number of for sale signs I’m seeing all over town.

regarding Tampa :

prices are atleast 15-20% off their 2022 highs at the 400k-1mm price points for sfh. this why using avg sold price is a bad way to guage markets.

don’t believe me, check zillow zestimates pricing history for both sold and currently for sale inventory. trend is undeniabley down.

see, YOU get it. I know cuz Im looking here in tampa to buy in the next 3-4 months, ive been waiting for almost two years now!

Looking at Seattle, real estate tripled in 10 years and is now going back down a little [although not going down in 98053 zip code where we live].

So what? Seems like a pretty good investment to me.

If had a time machine and a stack of money I would go back to 2011-2012 and buy as much quality real estate as I could, as long as it was NOT in the City of Seattle.

LOL

Moved to Seattle in ‘91 when it was still a nice place. Lived in Bellevue, Mercer Island & Bothell. You couldn’t pay me to actually “invest” in Seattle proper.

Have a son (single) renting an apartment on the Eastside @$1600/mo. For him to buy a POS fixer home in that area would cost about $5k/month or more now. Plus repairs. Crazy stuff. And he has a good job, too.

I told him save to invest in a business instead.

well if we have a time machine, im going back to 1973 in Seattle where you could buy HUD owned homes on Capitol Hill for $20,000 if you had cash to pay the back property taxes of a couple of grand–were talking victorians that must be $1,500,000+ today. Hell Wallingford “war boxes were $30,000 max all south of NW 45th to Aurora!

All this time since we finally started some QT, and it seems that rich people are STILL figuring out and giggling about just how rich they are. And now they have enough wealth to keep making wild and speculative bets. A couple hundred over what seems reasonable for a house? Why not? It’s just play money, and it’s worth less every day.

Depth Charge is gonna be pissed…

It might be more constructive to look at a 24 or 36 month trend than just one quarter. San Diego and Seattle were the hotspots for property speculation and bidding wars skyrocketing the prices of homes during the Pandemic. It’s only natural that prices are coming down. Las Vegas seems to have finally lost it’s allure of attracting people to the desert where they are having issues with water – too much development and not enough water.

I live in Florida. I don’t see price declines in this article for the cities named in this article. Although, I am reading in other credible news sources that the the real-estate market in large metropolitan markets in

Florida is plateauing. I live in a small city in SW Florida and per Zillow, which I check several times a week, the prices seem to have come down from their historic highs during the pandemic. I had spreadsheets tracking the prices listed and prices when sold for the past 3 years.

I can tell you that 3 years ago homes were selling at or above asking price. Now, homes are sitting on the market even after multiple drops in the market. My neighbor across the street listed a rental property next to me for 300K. Small, tiny 2br, 1ba bungalow. It was on the market for 10 months and finally sold for 250K. It is owned by a family 1/2 mile away and is being rented out. Of course this is anecdotal evidence, but houses in my area are sitting on the market longer and some are reducing prices, but not drastically.

On the other side of the house lives the son of the previous owner who just sold the tiny bungalow to my right. She owns that property and the son is paying highly-subsidized rent to his mother. He is trying to buy or build his own house, but the pandemic and supply chain issues crashed his dream of building a house – he actually cancelled contract to build a new house. I keep telling him to buy now while you are young. You can refinance if the rates drop drastically, but at least you’ll be in the house you want. He hesitates and I feel he will miss the boat waiting for those sub-four percent rates. Not gonna happen ever again. Cheers.

Until I see the final forensic autopsy on Schrödinger’s Cat, I’ll assume this pandemic bubble era of zombie stupidity is still alive and resilient — apparently immune to death and immortal.

I apologize for being pessimistic and not recognizing that after 4+ years, this time is different.

The only problem now is being way too late in FOMO — that ship is out of sight.

Does calling it “Housing Bubble 2” make it more likely to come true? Or will the millennial’s desire to buy keep pushing prices up the same way that the boomers did from the 1950’s until, maybe 50 years later. There was only one real correction in national prices, and the circumstances aren’t likely to be repeated. Highly unlikely that the mortgage holders will foreclose again like they did, and it was all the foreclosure sales that dumped the prices

1. “Bubble” = prices surge well beyond some more or less reasonable level.

2. “Bust” = prices go down hard.

3. We had:

– “Housing Bubble 1” (2001-2006)

– “Housing Bust 1” (2006-2012)

– And starting some years ago “Housing Bubble 2.”

Whether or not we will get “Housing Bust 2,” or just years of stagnation with ups and downs, while inflation and wage increase make homes more affordable again, or something else… whatever will happen in the future, the series will not change its name, which is, as you can tell, partially tongue-in-cheek, and which it has for its entire existence of 6 or 7 years to visually document the crazy price increases.

Judging from all the commenters here who are renting or have children renting and are waiting until prices/interest rates drop, once they do drop, there’s probably going to be a mad rush by all these folks to buy homes.

Whether that will be enough to push prices higher or not remains to be seen and also depends on other factors like unemployment, recession, home inventory etc.

“renting and are waiting until prices/interest rates drop, once they do drop, there’s probably going to be a mad rush”

I’m not so sure – will 25-50bps of cuts really trigger a wave of buyers to re-enter the market?

I suspect that folks waiting for cuts are waiting for bigger cuts, in which case they’ll be waiting for awhile and the market will remain frozen.

Nobody buys in a falling market. Everyone buys in a bull market. Fact.

CCCB and Julian.

I think you are both correct. There is too much FOMO still in the market. If rates drop a little or housing prices drop a little, people will jump in and buy. As long as the psychology of FOMO dominates, buyers will not be on strike.

The opposite happened from 2008-2012. Buyers initially jumped in and then saw their house values drop 10% per year for 4 years. Many homeowners panicked and tried to dump their underwater houses causing more supply perpetuating the housing price decline.

Wolf’s OER vs Case Schiller chart shows this. Fear of Jumping In dominated this 2008 bear market. Buying a house was cheaper than renting by 2012 but who wants to buy a house and see it depreciate 10-20% in the next couple of years? Most people won’t buy in a bear market.

We aren’t in a bear market and won’t be as long as we have a soft landing. A recession like 2008 would be a hard landing.

The road goes on forever and the party never ends

Looks like housing bubble 2 has a long way to go before it deflates

Correct CCCB, there was some excitement that the dramatic increase to mortgage rates that happened in 2022 was going to drop housing prices just as dramatically and that did not happen. Now that it looks like interest rates may start easing along with inflation, we will see housing prices continue their climb. A housing bubble deflation will happen, but it doesn’t look like it will happen anytime soon.

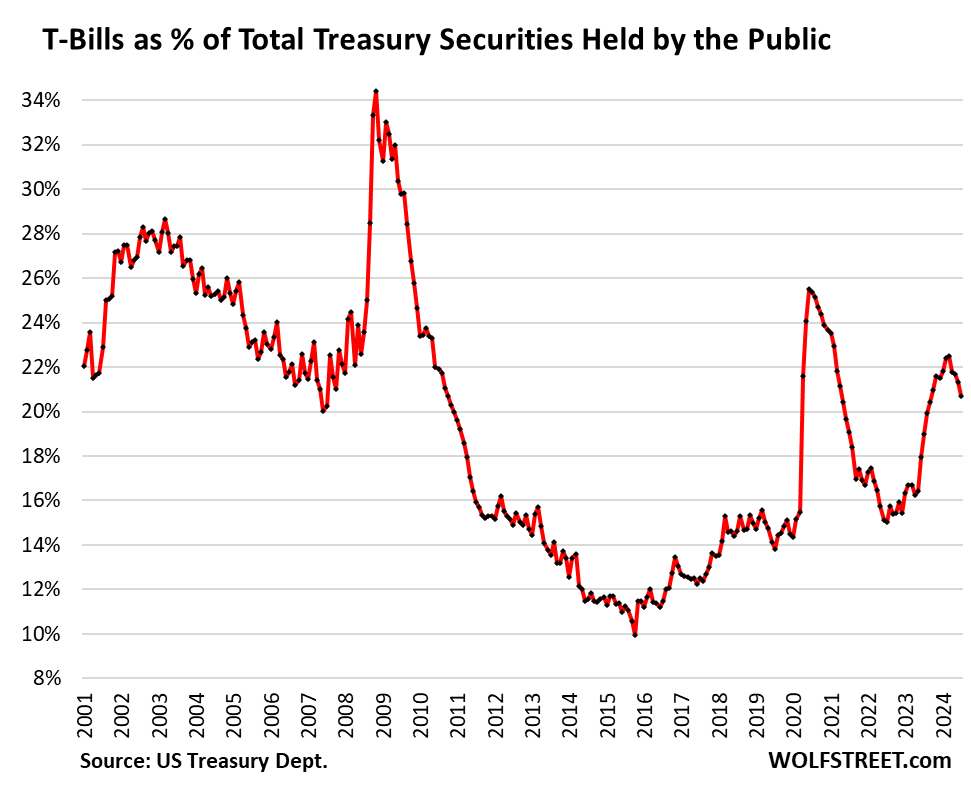

The latest article from Wall Street Journal accuses Janet Yellen of doing back-door QE via short term treasury bill issuance. I wonder what Wolf’s take is on this.

The piece I think you’re referring to was either the paper by Roubini et al, or referencing that paper. So that’s what I’m responding to here. If you’re talking about a different article, let me know.

That paper has already been widely debunked, including by me. It manipulated the data to suit their narrative. The paper alleged that the shift to short-term T-bill issuance was all kinds of things and had the effect of QE. And it came up with huge but fake numbers.

How did they manipulate the data? For example, they stopped with the data through Q1. But starting in April, the data reversed: T-bill issuance backed off and the share of T-bills (T-bills as % of total outstanding public debt) began falling again, and has now fallen four months in a row (through now). And so they conveniently didn’t include April through July because it would have contradicted their point (see my chart below that I posted this weekend).

That said, everyone agrees that Treasury’s shift to T-bills from longer term securities last fall was a result of the 10-year yield spiking to 5% last fall, heading maybe to 6% or 7%, and it scared the bejesus out of everyone, including the Fed. So shifting issuance to T-bills last fall (along with the Fed suddenly talking about rate cuts without ever actually cutting rates) has put a lid on longer-term yields. And that was the goal. Everyone gets nervous when the 10-year yield spikes through 5% like this. But the paper took this to a whole new imaginary level.

And obviously, the paper’s assertion that this had the effect similar to QE is BS. Treasury still borrowed every dime, there was no money being created. It just shifted the yield pressure to the short term, where yields are bracketed by the Fed’s current and expected policy rates and won’t deviate much from them.

Here’s the chart I posted the other day about how T-bill issuance has backed off over the past four months, from 22.5% in March to 20.7% as of Friday:

https://wolfstreet.com/2024/07/27/us-national-debt-hits-35-trillion-debt-to-gdp-ratio-at-scary-levels-dips-a-tad-and-t-bills-share-of-this-debt/

I saw that article and interpreted it as the fat cats on wall street being upset that the little guys is actually getting some risk-free return.

Fuck em.

There sure are a lot of people on Wall Street upset with 5%+ T-bill yields, that’s for sure, including banks that have to compete with their deposit rates.

What’s wrong with the 10 year going above 5%?

Thanks Wolf for the clarification. Thank goodness the government did not sink that low. We were referring to the same article.

15 years ago my son worked in Seattle. I was living in rural central Washington. On one visit to see him, I became so frustrated with traffic that I told him I wouldn’t live there if someone gave me the house (which of course wouldn’t happen). But it was like all large cities that we go to— packed with cars, roadways turned into crawling parking lots.

The past 3 years I’ve traveled to the PanAm games in South America as grandson has wrestled Greco. Large cities Mexico, Santiago, Chili; Lima, Peru are even worse. Most recently Lima—seems the only rule of the road is to get your car squeezed into the space before someone else. A US citizen trying to drive there would be Nuts!

Howdy Folks. Rut Row, more Lone Wolf charts showing more peaks. Inflation is under control at least. HEE HEE

As an additional perspective, was just checking FHA HPI:

“U.S. house price movement was flat in May,” said Dr. Anju Vajja, Deputy Director for FHFA’s Division of Research and Statistics. “The slowdown in U.S. house price appreciation continued in May amid a slight rise in both mortgage rates and housing inventory.”

IMHO, the word slight will be adjusted next month to something less teasing, like extraordinary — or maybe considerable?

Seeing the SF and Seattle prices rise back up at breakneck paces again is unsettling. What happened to JPow’s “homebuyers need a bit of a reset”? It’s like he’s just re-inflating the bubble(s) all over again! JPow and the Bailout Boys at the FOMC are truly the worst.

Howdy Bailout. The Lone Wolf showed me a chart of his, showing inflation rates and the FED fund rate over the last decades. It showed inflation well above the FED fund rate currently. Seems to me, the FED knows exactly what it wants……..

I have seen a couple of articles just lately flashing how the San Fran 9 county bay area prices are up this year because of the recent tech stock market boom? I have not idea if this is correct.

At the very high end ($5 million+ and $10 million+) there was a huge surge in sales through June — the AI and Nvidia millionaires buying. In terms of sales volume at the mid to low end, it has plunged. This move is big enough on both sides that it shifted up the median price.

At a certain point people are going to have to deal with the fact that it’s not a bubble and prices are largely entrenched for good

1. “Bubble” = prices surge well beyond some more or less reasonable level.

2. “Bust” = prices go down hard.

3. We had:

– “Housing Bubble 1” (2001-2006)

– “Housing Bust 1” (2006-2012)

– And starting some years ago “Housing Bubble 2.”

4. Your “entrenched prices” = flat at current levels for good? Many years of wage increases and inflation would make that scenario work.

haha. i heard that at the peak of every bubble. i’m getting old.

Geezus — same here. It’s always different this time in the same exact way it was all the other times.

Wolf,

The symmetry of some of those “housing bubble one” peaks is shocking. Having lived in the Bay Area through the first tech bubble myself, I know that, in many cases, the property values returned to there pre-tech bubble levels. I am not sure if the market could survive that kind of price reduction again. Curious what you think. Charles Hugh Smith posted a blog on the symmetry of market bubbles recently. Curious what your thought were on that as well.

Running into lots of folks in Phx metro who have been dropped by their homeowner’s insurance company for reasons such as too much crap in the backyard, wildfire risk, etc. It seems to be epidemic. I’m staying out of this insanity until we return to the old America. I don’t know how to navigate the new America.

How does that work with a mortgage that presumably requires insurance?

It doesn’t shorTlty:

With similar cancellations and incredible rises of property insurance in FL, and the heat continuing to rise such as 99 temp and 125 Heat Index today here in the Saintly part of the TPA bay area, many folks are considering the present situation the last of the good times for flippers, etc…

OTOH, those folx hereabouts who purchased homes years ago for 10% or less of what the value of their dirt is today probably don’t have a mortgage and from what I hear, many don’t have any insurance beyond liability, if that.

The lender buys insurance for you to cover their loan value at between two and three times what it would cost you to buy it and then raises your monthly payments to fund the escrow account and pay for the insanely priced insurance they just bought.

Owners dropping insurance own their homes free and clear.

By 2026, mortgage rates will be 3.5% again, zirp on in bubble world. This only ends in mass poverty.

Dream on.

How would that work if you don’t do escrow? Just curious.

@CCCB I have seen lender “force place” insurance cost even more than 3x what the last policy cost. Insurance has become a nightmare in CA and companies keep looking for reasons to drop you so my advice to anyone that gets a letter about crap in the backyard or weeds or trip hazzards is to jump on it and correct the problem so they drop another guy and force him to try and get a nep policy at double the cost.

ShortTLT, if you don’t escrow for insurance and/or taxes but have a loan, you have to provide proof of insurance to the lender or they’ll still buy expensive insurance for you.

Upload systems for providing proof can be a nightmare, and some lenders actually expect you to FAX (YES FAX!!) them proof

My home insurance increased from 700 to 4K in last 5 years.

A lot of home insurance companies are not doing new business in Southern CA.

Huge problem in California too. Deals fall through because the buyer cannot get insurance, or cannot get insurance with a premium that’s within reach of the buyer.

What is it about the California State insurance regulations, laws, requirements that make it so unprofitable and difficult for insurance companies to operate there? Businesses like to make money, it would seem that if California was still a good place to do business they would.

The prices in Nashville have softened ever-so-slightly, but with all of the California/New York/etc. transplants moving here and paying top dollar in cash, the upper end of the market remains fairly competitive (as Wolf has alluded to in past analyses).

I have a client closing on a $3.5M house tomorrow, and he didn’t bat an eye at basically paying full price in cash. And this guy is YOUNG, like 35ish.

And my wife thought I was nuts for buying 7 rental properties between 2008 and 2012. Now that I have them all paid off, she is singing a different tune!

if so many people from california and new york were moving to nashville with top dollar, prices would be dropping in those places by an equivalent amount.

that’s not the case. this is pure bubble, not wealth movement within the country.

You know that every year, millions of young people come of age in traditionally crowded, established markets.

These markets all have strict zoning and dont build much housing, or have little space for it.

Those young people, or their elders, need homes. One or the other moves out and someone replaces them in that traditional market.

Understand the dynamics a bit more and you’ll understand why all the hot markets are the first to crash. Look at Boston through “Housing Bust 2”. Not much of a bust.

See my comment below. Lots of new inventory and price reductions right now in the Boston market. Sellers are becoming more motivated.

Per my bi-weekly zillow browse, there are a lot more homes for sale in my zip. Hilariously, a couple were listed last year at higher prices, pulled from the market after a couple months, and re-listed this year for a few % less.

One house was listed last year at 520k, sat for a month, had it’s price cut to 460k, still sat and then the listing pulled. It’s now listed at 449k. Pays to wait!

“Housing Bubble 1” looks like an amazing time to have bought a house.

Sure, not the *best* time, but still great.

If you close your eyes and invest long term, you made a lot. Could you have made more, sure, does it matter that much if you were on the ladder? Not really.

A lot of doom sayers here who will sit on the side lines paying someone else’s mortgage. Some of you will buy in on the next little dip, others will wait for “the big thing” and lose long term as everyone who bought ten years ago refinances and releverages to buy more assets.

Fact is we’ve created an environment (30 year fixed mortgages with little cost available to all reasonably financially stable people) that biases the housing market vs other asset classes.

Sure stocks are great. But can i borrow 80% fixed with no margin calls without being a BigShot? No. But i sure can on my house. And I’ve turned that into two more houses.

It will take a dramatic turn in zoning laws to change the housing market. In the meantime keep labeling your chart “housing bubble 2”. Even a blind squirrel will find a nut if he looks long enough.

That’s five paragraphs invested in some kinda bizarre flex about how it’s actually okay to have overpaid during the last bubble because they blew another bubble which had the effect of eclipsing the former, thereby making some innumerate doofs appear like long-con geniuses. Sure.

Meanwhile, think how much better you’d’ve cleaned up if you’d waited until 2012, when I bought my first home. Hell, waiting 8 months between 2011 and 2012 saved me $250K on the original asking.

I think most would-be buyers today just don’t wanna get stuck over the proverbial barrel. Not unreasonable, I think. And really — wouldn’t it be nice to return to a time when every aspect of one’s all-too-finite life didn’t have to be financialized? Where one could just live their life and not have to fixate on the zestimate of their domicile or obsess over their equity like a pile of melting casino chips?

It sounds damn’d nice.

Welly, I think I see a turd, housing prices circuiing the bowl just before the flush.

The housing market is not functioning anywhere close too what is laughingly referred too, a “free, competitive market place where neither the buyer nor the seller have a competitive advantage and the agreed upon price results in a sale that clears the market.

We have too pretend we don’t know what’s probably going on which way too view the future.

After this short time I have been alive, I can’t believe how much time I wasted.

Consumer price inflation is always an antecedent too asset price inflation.

Whom ever’s putting up the money too support the bubble pricing are reckless in the extreme. Convinced by a demonstratively flawed Ivy League ideology, which in it’s implementation over the past 50 years has done more damage than good.

I fear that it is the treasury who bought the kool aid while financing the CCP labor monopsany.

This is definitely not a bubble at the moment. The 2006 runup was, but this cycle correlates directly with M2 money supply. https://fred.stlouisfed.org/series/M2SL

It’s generally hard for people to think in terms of inflation, but when there’s more money in the system, prices respond accordingly. The housing price behaviors are directly correlated to the M2 at the moment, sure there are regional variances which include population changes, supply/inventory changes, and other factors which affect region to region variances. M2 has performed similar to many of the house price charts above (dropped slightly then slow upward march thereafter) the long-term trend will continue upward as will national house prices.

This is absolutely a bubble – a short term rental speculative bubble. Look at the Airbnb profit chart, it tracks all the charts posted above. Prices have risen in tandem with homes being converted into rentals.

https://helplama.com/airbnb-statistics-revenue-and-usage/

This time truly is different because the fed’s suppression of interest rates allowed everybody to refinance at 30-year fixed rates.

The bubble popped in 2008 largely due to the large swath of two-year variable rate mortgages that were issued in 2006. This is not going to happen now. We will likely be stuck in a frozen housing market for decades

People have to live somewhere. Predictions are that the US population is going to crest somewhere in the ~400 million range in the later 21st century. Housing demand is fundamentally going to hold up for these reasons. Now, we just had a decade’s worth of price increase in three years (2020-22) so anyone who’s expecting big short term profits now is crazy. But buying, holding, living?

If housing stays flat until 2030 and inflation runs 2.5-3.5% a year, prices effectively drop 20%. OR – go on buyer’s strike, rent for six years ($180k total?) then buy later when you’re making 2030 money. Will prices be $180k lower – that’s a wash at best.

I’m not a realtor or have anything to do with housing, but let’s face it – in 2040 every single house in this country is going to be selling for more than it is now. 30% more, 250% more – that depends on location and other factors. Buy in a Sunbelt city and it’s basically guaranteed that in two decades you’ll be more than ok.

Anecdotally, Seattle prices are close to 2022 peak. I sold my house at the peak for $1.5M — an almost identical house down the street just sold for a smidge more than mine last week.

But after two years of high inflation – call it 8% cumulative since 2022 when you sold – that smidge more is actually a lot less. Another five or six years of smidges and inflation and houses just might be priced right again. Prices aren’t going to plummet but they also aren’t going to soar. Think 1980s. If only the Fed can keep its dirty mitts off the MBS market..

Man, so glad my wife and I bought our home in 2015. We’re in Las Vegas. What’s crazy is that our house was a foreclosure. Purchased in 2006 for $386,000. After the Great Recession home prices plummeted so the house went into foreclosure. In 2015 we purchased it for $250,000. I remember thinking you’d have to be crazy to buy this house $380K+.

Now Zillow and Redfin say our house is worth $470K to $510K! That’s insane. Looks like this will be the last home we buy, which is fine. It’s a 4 bed 2 bath home so it’s plenty big. And our mortgage at 2.875% keeps our payments low.

Bought my first house in 1970, 23 years old. 0 down VA. The draft was worth something! Wife and I worked full time, drove old cars, had a garden, $0 from parents, delayed having kids, no CCs, but we saved a little money every month. 1973 gas lines, 1980s sky-high inflation, layoffs, housing boom and bust, it wasn’t a picnic like some claim the Boomers had. Our Depression Era parents taught us to save and and be responsible for ourselves. We were. Now I see in the comments about blaming everyone from the banks, the builders, the government, immigration, farmers, etc.

Young people, look in the mirror if you want to have a good life. It’s up to you. Nobody really cares if you buy a house, rent, or sleep on the street. Watch every penny you spend, save as much as you can, and don’t expect your parents to save you. Good luck.

One of the best honest comment. I can see that no other trolls have any counter comment. This is the best one so far. All you FOMO learn something out of this. BRAVO STAN🤛👏👏👏👏👏

I would be careful with your comment. Wages have not kept up against the cost of schooling and housing as it was in your day. It’s no longer just a matter of being frugal- a hs grad with no parent support can’t just get a minimum wage job and pay for school and a cheap apartment. They’d have to get a great financial aid package and hope to heck there’s more grant than loan – it doesn’t pencil any longer.

The chart that’s missing here is this one from Reuters:

Tracking second mortgages. There was a massive price spike starting in June 2020 as a bunch of workers went remote and investors starting buying up everything they could find in desirable locations to turn them into short term rentals.

As demand for short term rentals has begun to wane, investors are looking for exits and nobody sane wants to buy at the prices they are asking.

We are looking to buy in the next year and can see the price spike from Covid in every RE website estimates. As more cities start banning/restricting Airbnb and the like, this bubble will deflate. The pricing is unsustainable without revenue from rentals, regular people certainly can’t buy. Shut down the short term rentals and watch how fast this bubble corrects.

ALL homes sales have plunged, including second homes.