“The market is at an interesting point with rising inventory and lower demand”: National Association of Realtors

By Wolf Richter for WOLF STREET.

We here in our little corner don’t normally more than glance at the “pending home sales” data by the National Association of Realtors. It’s a forward-looking indicator of “closed home sales” based on contract signings – on deals that haven’t closed yet and could still fall apart. But today’s release of pending sales was interesting for several reasons, including the NARs’ expectation that the collapsed demand along with rising inventories is going to cause home prices to “stabilize” in the second half of the year. So here we go.

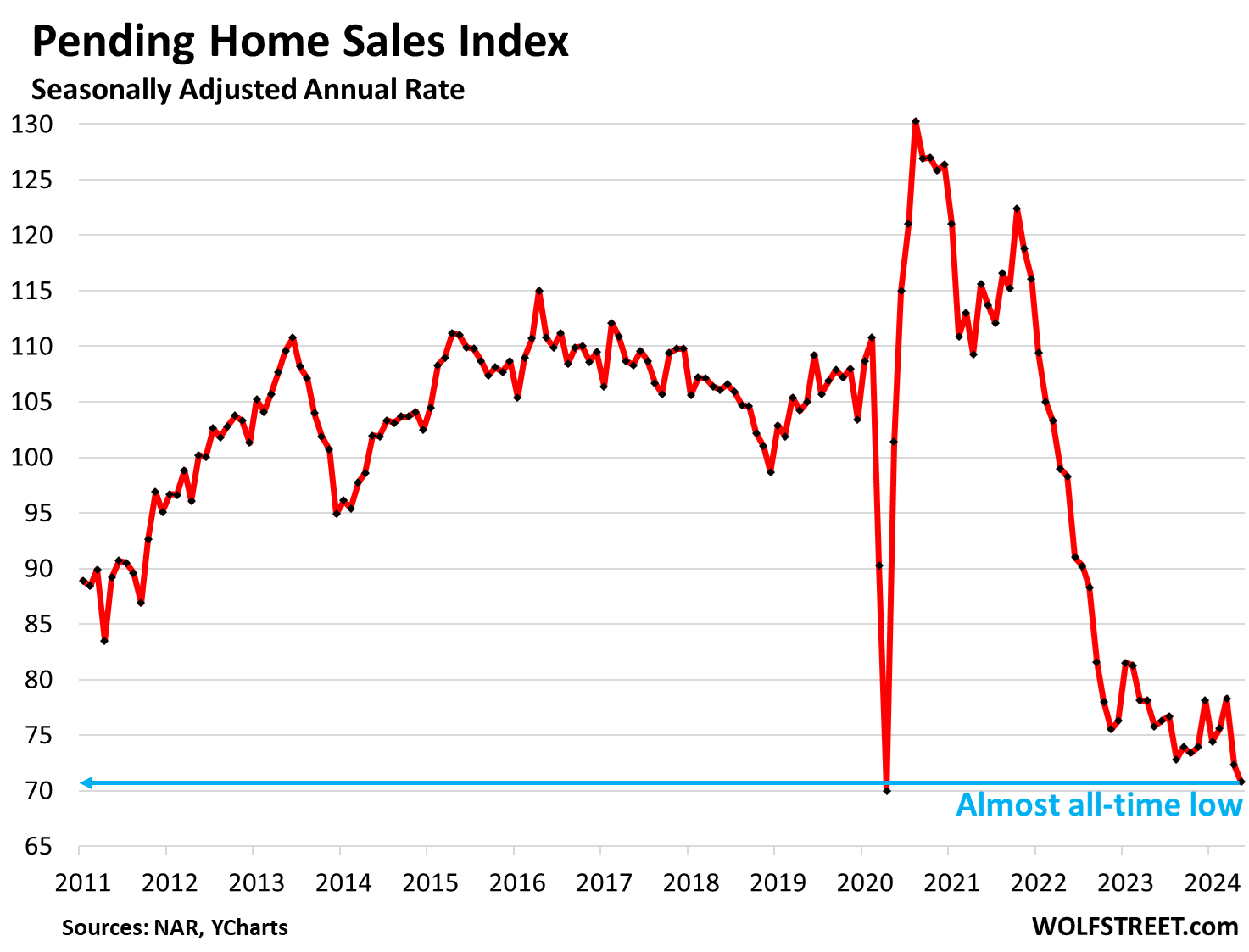

The index value of pending home sales in May dropped by 2.1% from April, and by 6.8% from a year ago, to 70.8 (seasonally adjusted annual rate), what headlines dubbed an “all-time low” or “record low” in the data going back to 2001, and that’s close enough. In the NAR data we have access to via YCharts, today’s reading was still a hair above the prior all-time low of April 2020 (index value of 70). But the idea is the same: demand has collapsed, even as inventories have risen.

The index value was set at 100 for contract signings in 2001. So today’s value of 70.8 is down 29% from the index average in 2001. Compared to the Mays in more recent years:

- May 2022: -28%

- May 2021: -39%

- May 2020: -30%

- May 2019: -33%.

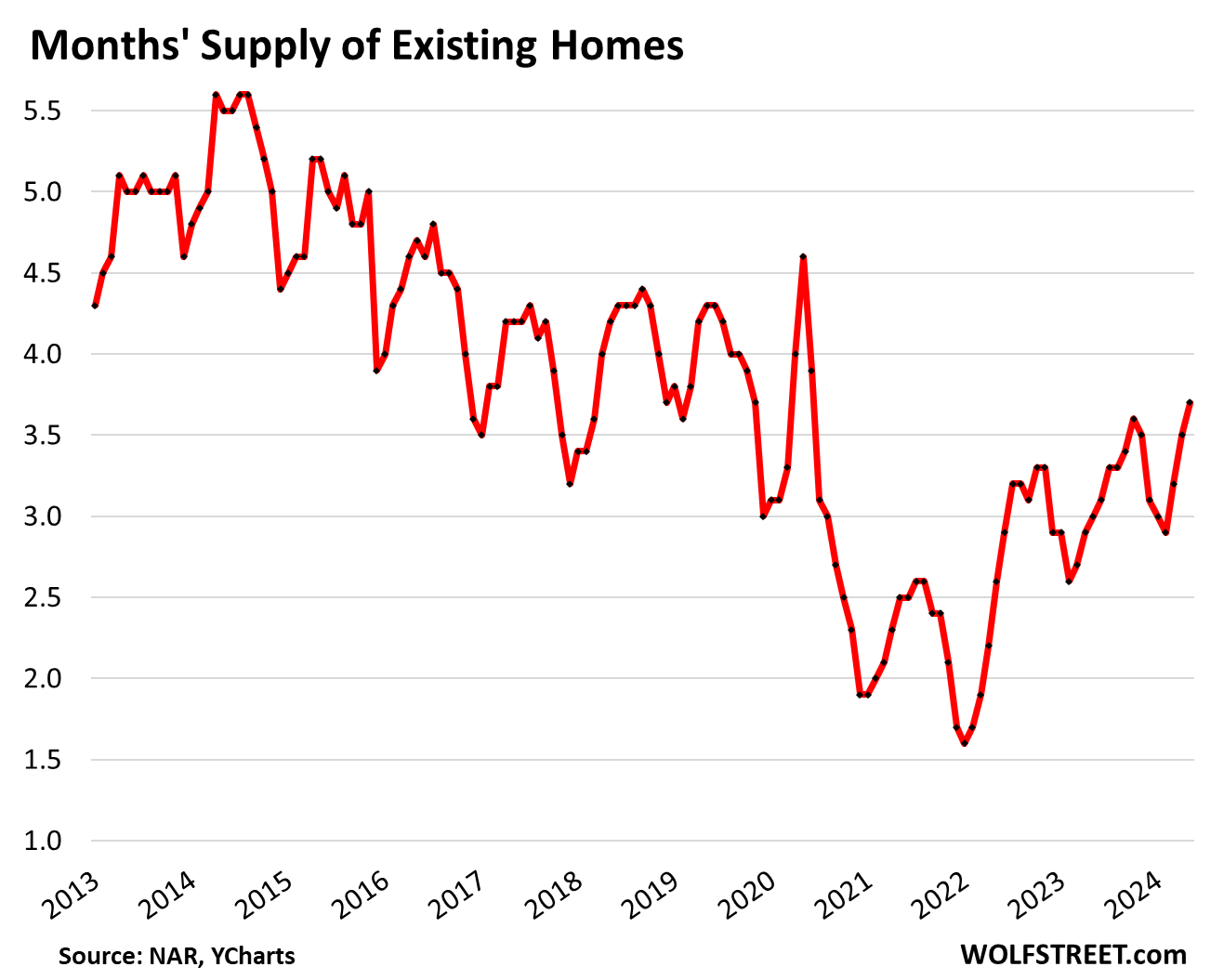

And this sustained plunge in demand is occurring even as supply in May jumped to 3.7 months, the highest since June 2020, and as inventory for sale jumped by 18.5% year-over-year, to 1.28 million homes, according to NAR last week:

So here’s what NAR said about this situation:

- “The market is at an interesting point with rising inventory and lower demand.”

- “Supply and demand movements suggest easing home price appreciation in upcoming months.”

- “In the second half of 2024, look for … stabilizing home prices.”

Oh, and praying for mortgage rates to “descend”:

- “Inevitably, more inventory in a job-creating economy will lead to greater home buying, especially when mortgage rates descend.”

- “In the second half of 2024, look for moderately lower mortgage rates…”

But maybe they won’t descend by a lot or even enough – they’ve been around 7% for months:

- “NAR predicts mortgage rates will remain above 6% in 2024 and 2025, even with the Federal Reserve cuts to the Fed Funds rate.”

What a bummer?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Gentle reminder: people don’t buy “homes”. They buy houses.

Living in the house eventually makes it a home.

The realtors and builders use “home” rather than the correct “house” as a linguistic marketing ploy to appeal to people’s emotions. Don’t adopt their framing, it can be toxic to your wealth!

“Home” has many meanings. According to my trusty Random House Webster’s Unabridged Dictionary (digital version for Windows 98 that still runs on Windows 11), “home” has 31 meanings, as noun and adjective (so maybe they added new meanings since then). but here are the first 4:

1. a house, apartment, or other shelter that is the usual residence of a person, family, or household.

2. the place in which one’s domestic affections are centered.

3. an institution for the homeless, sick, etc.: a nursing home.

4. the dwelling place or retreat of an animal.

In the housing market nomenclature, “home” reflects the #1 meaning, a summary word that includes single-family houses, townhouses, condos, and coops. Home = “dwelling.” A “house” is a specific type of home.

“Random House Webster’s Unabridged Dictionary (digital version for Windows 98 that still runs on Windows 11)”!

How’d they fit THAT on the box??

In IT terms it is considered “backwards compatibility”.

If no one remembers the high of shopping for software at staples or Office Depot or games at say a babbages, then you missed out ;)

But Steam is very fun to peruse as well.

He’s not being literal, he’s being poetic. He’s saying it’s a specific framing by NAR to make people emotionally attached to buying big, expensive properties. He’s implying that somebody can be happier making a “home” in a more modest house.

Does Summer time usually reveal the true nature of real estate? Since most homes are listed and sold in the Summer months, and drops during Christmas, are other bubbles typically bursting the Summer time because in a good market sales go up?

This is seasonally adjusted data, as it says in the article and on the chart.

‘The chill that has taken hold of the Toronto area’s usually red-hot real estate market is leaving a growing number of new homes to languish — with stubbornly high prices and heightened borrowing costs icing out prospective buyers, and new home sales down 71 per cent compared to last year.’

From Toronto Star

In my opinion a 70 % drop is a crash.

Moving on, the future for ‘The One’ the ninety floor half- finished tower in downtown TO is not looking good. It is now for sale by the receiver for 1.5 billion. This would be ambitious even if wasn’t surrounded by other half empty towers.

On June Sixth, the day after the BoC stepped out and cut rates by .25 %, the Globe and Mail kind of embarrassed itself on the front page of the Biz section with a reporter saying that more cuts were ‘widely expected this year and next’

On next page a seasoned contributor’s piece was headed:

‘Hoping for more rate cuts? Be prepared to wait’

So…bipolar. In other pages in the G&M an economist warns that more ‘cuts by Canada alone could tank the C$.’

But the C$ is already tanked, down from eighty three cents US about 5 years ago.

Why is there and always has been such a large difference between interest rates in America verses Europe. Example 10 year US 4.5% , Euro 2.5%?

One part of the difference is that you cite a figure for Germany. Here are a few others, and the difference is smaller:

French: 10-year: 3.2%

Italy 10-year: 4.03%

Spain 10-year: 3.3%

Another part of the difference is that the ECB’s main policy rate is now at 4.25% (after 1 cut), while the Fed is over a full percentage point higher (and no cut): 5.25%-5.5%.

Another difference is that Euro economic growth has slowed a lot; Germany has had around 0% growth for two years, etc. In the US, GDP growth has been between normal and hot.

The US growth is normal/hot because the US is taking on a trillion dollars of new debt every 100 days.

I have unsuccessfully tried to buy puts on the ETF NAIL on and off this past 8 months. Homebuilding 3x ETF.

High interest rates did not slow down home builders. The lockin effect helped out new homebuilders too.

But I am seeing new permits dropping everywhere. You would think this will hurt the homebuilders profit in a quarter or too. Maybe my puts on NAIL will eventually pay off. I am making a little now over the past couple of months.

But I am getting swamped by phone calls to buy my rental properties. I am getting 10 calls a week and 3 to 5 letters a week. This is more than the mania in 2021. They pretty much dried up late last year and until two months ago.

I have no idea what is going on unless some cash buyers are trying to front run rate cuts next year. In my area house prices are steady and increasing a little but they are not hot with bidding wars.

“…unless some cash buyers are trying to front run rate cuts next year…”

This is exactly what’s been going on. And as the prospect of rate cuts dims, their speculative appetite for these already-overpriced homes fades.

@ru82 I am also getting more of the the calls (despite working hard to hide my phone number) and postcards (at the PO Box that is the mailing address for all my LLCs) and the reason is that as the market cools there are less flippers and realtors “actually working on deals” and with sales volume down, WAY more people have time on their hands to mail stuff and make calls “looking for the next deal”. I bet less than one in ten calls and postcards are really from “someone that wants to buy” and the rest are from people looking for a potential listing, a pocket listing or guys “bird dogging” for realtors looking for someone that might want to sell).

I answer some just so I can ask what company they work for and where they are located. Because the caller ID has a local number. I tell you what, a lot have very thick Asian and Indian accents. I live in the midwest and there are not many Asians or Indians in the city I live in.

They are not realtors. I can can smell out a realtor.

Anyway, they are very secretive on who they are (or they just don’t know anything) and they say they are local investors (not) but if I am interested, someone else will call me back in 30 minutes with a cash offer.

Maybe realtors are using call centers now for leads. I think these calls are just lead generators who get paid if someone answers the phone. They all sound like twenty somethings.

Be careful when it comes to Asian or Indian accent individuals looking to give you a cash offer. Someone I know had a sister who was offered a good amount over value of home and when she went to sign paperwork, everything looked legit (had building, office, staff,etc.) and she didn’t read fine print and instead of the 300k (2019 numbers) it said somewhere it was only 200k and they ripped her off for 100k. By the time she tried to report these individuals the building was abandoned, phone lines disconnected and money was never recovered. Just do your due diligence when it comes to anything being offered over the phone.

I had a house listed in Florida last summer. I received a phone message from an organization saying they were interested in buying the house, so I called them. My first question was – how did they get my phone number, since it wasn’t in the listing. The question went unanswered. The guy had an Indian accent and I had the distinct impression he didn’t know what he was doing. I asked what outfit he worked for, and he said they do all kinds of work in the real estate area, without getting specific. He wanted me engage in another conversation with a team of people who wanted to give a proposal. I said sure. A few days later I got a call back from two guys (including the original guy), and it was very clear they knew nothing about the listing or the area. I hung up on the jokers. If they were scammers mining for personal information, they weren’t very good at it. If they were RE people, they need to find a new line of work.

I still don’t know how they got my phone number. Maybe the realtor gave this information out or disclosed it in some filings.

AI: The standing AD in my local paper (which is ALL local politics and RE ads) from a long time producer is:

Looking to sell in 2024?

Definitely looking for work.

ru82: The “local area code” is from auto-dialing software. It’s essentially a VOIP that plugs into a vacant number… in YOUR area code! I get a lot of these.

For a while I was using phone leads, and this was the process: just use a spreadsheet of numbers (sourced from all kinds, public records are great) and the software connects you when (if) a human answers. It felt like (and was) telemarketing, which I did for a shift about 25 years before my recent experience.

Since getting a new phone number after the carrier for many years just stopped my service, I have received NO spam calls, so the offers, still several per week, now come on post cards or actual letters.

The most recent postcard had a cash offer amount almost exactly FIVE times what we paid in ’15…

Crazy hardly describes it, eh?

It’s awfully hard to buy a put on a 3x levered ETF and make money. The spread has to be awful. There’s nothing systemic about homebuilders. They react quite quickly to reducing inventory and cutting costs and surprises are few and far between. Levered ETFs themselves are meant to be traded, not held. Options on them are just a dumb luck thing and you’ll likely lose 99.9% of the time. Why not just take a 3x larger put position on a single name or two in the index? Far more reliable tactic.

Me, too.

They want to buy rentals, and don’t seem very interested in things like condition, location, etc.

Love to see it! Housing market is slow moving so this will probably take some time (another year or two?), but inventory building back up is a good thing. Hopefully these overpriced homes start falling back to more normal price to income levels.

Normal, did you say Normal?

Normal is gone forever, I saw her getting on the bus with a smile on her face.

Forward looking, I see hard times for many, Turmoil everywhere.

Harmony has also left, she was carrying her dog.

But, who just arrived is very interesting, he looked like the zig-zag man, maybe we’re all going to get smoked.

Definitely interesting when the biggest housing bill narrative pump is saying there might be chink in that armor…then again I am sure they are still telling you it’s good time to buy.

Also saw CEO of Refin saying something similar on MSM. Part of me wonders what kind of jedi mind trick or reverse psychology angle they are working on..then again NAR did say price will stabilize so I guess if you buy now, it will just flat line until that juicy interest rate comes around..

Lawrence Yun’s job is to lie for the NAR. In 2008, he was telling people that there was no issue. I am surprised he even says that home appreciation rates may slow.

I am still seeing people putting houses on the market at astronomical prices. Those that need to sell are dropping asking prices. The one I am interested in has dropped three times in six weeks. Luckily, I have more patience than money.

Yun’s a moron. Has the data, why not go back to 1980 and pick up impact of 18% FHA neg-am 245s when President Reagan was shot, 1987 market crash, 1990 RTC drama, then flow into 2000, etc. Easier to just bend the data to support a narrative short term, until another NAR OOPS and revise flawed data. I’ve been paying feeble NAR too much money since 1978. TFS

Howdy Broker. If the NAR goes through with its planned changes, you may no longer need the NAR badge to operate…….

Lawrence Yun’s job is to tell people that is “always” a good time to buy “and” sell a home (since the people that pay him get paid when people buy and sell homes). Mr. Yun’s “advice” on when to buy or sell home will be similar to the “advice” you get when you ask the salesman on the lot of a car dealership if it is a good time to trade in your car and get a new one.

P.S. To DFB, I’m pretty sure that the NAR can’t “force” people to join and pay dues anymore…

Yun is another shill for his employer, what else is new? Would you trust the spokesperson or scientists from big oil or tobacco industry. NAR is no different, protecting their revenue interest at all cost. This is the root of capitalism, morality and truth is little garnishing they like to put on top of the big turd at their core of their interest.

This is the root of human nature, morality and truth is little garnishing they like to put on top of the big turd at their core of their interest.

*Fixed it for you

Isn’t what the NAR just said about supply and demand another way of calling it a crash?

Didn’t the NAR go back and “revise” all their data after the 2000’s housing bubble because they basically lied about it?

The NAR exists to enrich its own members, not provide facts to the house-buying public. I’d treat any numbers and narrative from them with this in mind.

Howdy MCMatt. Brokers enter the info to their local MLS organization. The NAR can easily manipulate averages like anyone else.

It’s going to take a long time for the housing market to smooth out and be healthy again. What’s the “right price” for a house now? Early 2022 prices? 2019? 2024+ at an all time high?

The Fed needs to continue to shed MBS mercilessly and never muck with that market again. And if mortgages stay at 6-8% for years and years prices WILL eventually find their correct level. There will be more people in the US and there will be more money sloshing around so prices will stabilize soon enough.

Have you ever looked into investor activity today and compared it to 2007-2009?

More recent research into the GFC suggests that:

“The investor share of mortgage balances roughly doubled between 2004 and 2007 reaching a peak of approximately 30% and accounted for close to 50% of all foreclosures at the height of the crisis, even though their share in the borrower population peaked at 14%.”

” We show that credit growth between 2001 and 2007 was concentrated in the prime segment, and debt to high risk borrowers was virtually constant for all debt categories during this period. The rise in mortgage defaults during the crisis was concentrated in the middle of the credit score distribution, and mostly attributable to real estate investors.”

A release from Corelogic in April 2024 states, “The share of U.S. home investors hit a new high in December, according to CoreLogic data [1]. In October, November and December, the share of single-family home purchases that were made by investors was 28%, 27.3% and 28.7%, respectively. This eclipsed the previous all-time high of 28.3% in February 2022 and makes the investor share rising above 30% in 2024 a distinct possibility.”

The big investors have pulled away from this market because it’s too expensive, and they have become SELLERS of individual houses they own in disparate places. Instead of buying existing houses, they’re now either building their own developments with rental houses, or they’re buying those build-to-rent developments from homebuilders — hundreds of build-to-rent houses in one development with a leasing and maintenance office and common amenities, such as a pool. This move to build-to-rent is the biggest thing real estate right now. We’ve discussed it for years. In other words, the biggest landlords are funding new supply of rental houses and selling some of the houses that they’d bought cheaply in 2012.

https://wolfstreet.com/2024/04/24/biggest-landlords-pile-into-build-to-rent-single-family-houses-but-are-selling-older-houses-into-this-overpriced-market/

The investors that are still buying existing houses are mom and pop investors, and there are 11 million mom and pop landlords in the US:

https://wolfstreet.com/2024/04/09/the-biggest-landlords-of-single-family-rental-houses-and-multifamily-apartments-in-the-us/

Howdy Lone Wolf. Just imagine if the 3% s had the courage like Ma and Pa had. The sailors membership sure would grow……

Have you ever looked into investor activity today and compared it to 2007-2009?

More recent research into the GFC suggests that:

“The investor share of mortgage balances roughly doubled between 2004 and 2007 reaching a peak of approximately 30% and accounted for close to 50% of all foreclosures at the height of the crisis, even though their share in the borrower population peaked at 14%.”

” We show that credit growth between 2001 and 2007 was concentrated in the prime segment, and debt to high risk borrowers was virtually constant for all debt categories during this period. The rise in mortgage defaults during the crisis was concentrated in the middle of the credit score distribution, and mostly attributable to real estate investors.”

A release from Corelogic in April 2024 states, “The share of U.S. home investors hit a new high in December, according to CoreLogic data [1]. In October, November and December, the share of single-family home purchases that were made by investors was 28%, 27.3% and 28.7%, respectively. This eclipsed the previous all-time high of 28.3% in February 2022 and makes the investor share rising above 30% in 2024 a distinct possibility.”

I just thought it was interesting that investor activity doubled from 2004-2007 and similarly, according to CoreLogic, from 2019-2024 investor activity, as measured by share of monthly single family home purchases, roughly doubled (~15% to ~30%). Most of whom, as you mentioned, are small investors (3-9 properties).

Howdy Max. Bet the investors are buying because of all the 3 % prisoners out there.

Max, if you go back to the Big Short and some of the other context, subprime actually grew a lot earlier on and had a mini-crash in the early 2000s. That’s what made some people like Steve Eisman aware of the problems. So, I suggest that healthier data might have actually looked like a decline in subprime in the mid-2000s.

“The investors that are still buying existing houses are mom and pop investors, and there are 11 million mom and pop landlords in the US”

and if most of these mom and pop landlords get wipe out in the next bust (if there will be one) I have the smallest violin for them. We’re no longer in ZIRP environment, some of them need to stop being so Fing greedy and think they can make a better than 5+ cap rate on their return on rental.

Personally dealing with a landlord now wanting to raise our rent 15-20% because that’s what the market around here is listing for..blah blah, nevermind that comparable been sitting there for a while and often it’s nicer inside. This whole greedy landlord operating on that raise the price Airbnb mentality is going to come back to haunt them soon enough…

1. “and if most of these mom and pop landlords get wipe out in the next bust (if there will be one) I have the smallest violin for them.”

Those that have owned their rentals for many years and didn’t cash-out refinance or pile on big HELOC balances will be just fine during the next bust. Those that bought recently will also be fine if they can keep their rentals filled with tenants who pay their rents. The problem arises when they can’t fill their rental, or can’t get the rents needed to make the mortgage payments and cover other costs. And there will be a crop of them.

There are many mom-and-pop landlords here in the comments. And occasionally some bigger ones too. So we get to hear about some of their issues.

2. “Personally dealing with a landlord now wanting to raise our rent 15-20% because that’s what the market around here is listing for..”

Landlord greed is a disease that afflicts some landlords. And sometimes it knocks out the afflicted landlords when things get tough, and when stable good tenants who pay their rents and stick around are a godsend — the very people that the afflicted landlords ran off with their rent hikes.

Many “Landlords” actually have their properties managed by property management outfits. Most renters I know, hate dealing with those outfits.

The PM has to make their 10% on top of the return the Landlord wants. It’s a very tough low margin business. Like any low margin business, it only works with volume and generally move volume than the PM can actually effectively manage. So renters experience poor, arbitrary and demeaning service.

I’m thinking the Rental business only works these days for those who can operate without debt (or very low debt). Otherwise it’s a big squeeze and with 5% returns on Treasury Direct, it’s an increasing argument internally, if it’s worth it.

Couldn’t agree more Wolf. Sadly, shortsighted landlords that wants to maximize profit above all are more commons that the ones that value a good tenant that take care of their place. Most around here just want to charge as much as they can until one day they get a nightmare tenant, that’s when my schadenfreude really goes to high gear..

Same with my landlord now, even if we renew enjoy that extra income cause next time you fly too close to sun I’ll be laughing my A$$ off when your listing go unrented for a very long time or you try to scramble sell when price is starting to head down

When danf51 wrote: “Many “Landlords” actually have their properties managed by property management outfits. Most renters I know, hate dealing with those outfits. The PM has to make their 10% on top of the return the Landlord wants. It’s a very tough low margin business.” it reminded me to let people know that other than people that are a pain that you “want” to move out few actual “landlords” push rents really hard since they 1. want to keep good renters who pay the rent on time and 2.you get killed with lost rent and turnover costs every time someone moves. Many property management firms get “construction management fees” and “leasing fees” on top of their flat “management fees” so they often make MORE money when a landlord is paying out thousands to renovate and re-lease a unit. P.S. To Phoenix_Ikki the legal owner of real estate is public in all 50 states and you might see if you can track down the actual owner (not the manager) mailing address and mail them a letter asking for a lower rent increase (sometimes Google will find this, but if you don’t have any luck most realtors can bring it up on their phones).

“the legal owner of real estate is public in all 50 states”

Not in CA or TX in my experience.

I live in CA and I can assure you that the legal owner of real estate is public record. I asked Google if they are public public in TX and this is what came up:

“The information about your home purchase and the terms and conditions of your mortgage loan is recorded among the land records in the jurisdiction where the property is located. These documents are public.”

MM: As AI mentioned, it is public record.

Public record does NOT mean easy to find (as salaries and other data for the public sector are also on record).

Regarding RE ownership, the county assessor’s office is generally responsible for the data.

Much of it is probably online (and government websites are a nightmare to navigate), and some is probably safe, in the file, in the office (especially in smaller/ rural communities).

The county data is also the likely home of tax lien information (maybe at the courthouse, next door to the assessor), a major source of Kiyosaki’s wealth (Rich dad fame)

Yep, most of the appraisals were are doing now in the Swamp are mom & pop landlords. We’re seeing prices and supply stabilizing but not much movement either way. Lots of condos and two units.

Does a forward looking indicator for housing appreciation exist ?

The NAR might have price data on pending sales but doesn’t disclose it. Maybe that’s where their caution about prices in the second half is coming from.

Realtor.com has “Median Listing Price.” But listing prices don’t turn into reality necessarily, as price cuts have reached multiyear highs as percent of active listings.

Real Estate Broker in Washington State here.

It is prohibited to tell anyone what the contract price is in a pending sale contract. MLS is not supposed to know, and the NAR is nor supposed to know.

Is there a certain amount of knudge-knudge-wink-wink going on? Maybe.

I doubt very much that there is a national dataset for the prices of pending contracts.

Howdy Folks. They sure built this BIG Bubble, now what will they do? Hopefully the Lone Wolf Charts have shown their final peak. Hows new home construction going?????

@Debt-Free Oh, you are a funny guy.

You can’t get a building permit in a place where sensible people would want to live.

Nothing has changed.

That is how new home construction is going.

Interesting. I love real estate economics.

My late middle aged, real estate profession friends tell me that everyone is waiting for a rate cut for things to heat up again. They are suffering for sure after weathering the great recession and pandemic. I knew rates would have to eventually go up but I didn’t see how abrupt it would be. The fed could have eased the pain by acting sooner I think.

I still think that sales are impressive given how high mortgage payments are now.

I just feel like there is still a huge demand by aging millennials to finally settle down with a house and kid. We will see.

Building more houses will help the new house buyers a bit as well. The developers over did the luxury apartments as I predicted when I saw them going up all at once which is hurting rent prices.

“The Fed could have eased the pain by acting sooner”

And it did act… and succumbed to a bully. Then backed down and (as usual) waited until it was “too late” and thought they could catch up.

The Fed is a destructive force and is always late.

Late to come, late to leave. Higher for longer means: we will not move until the ground is shaking.

@Jdavis

Agree.

Perhaps some are catching on to the great lie! How much home you can afford!

All the numbers courtsey of those selling shackes for as much as they can get.

Home ownership has many costs and most are spending more than they can afford.

If your home is more than 20 percent of your net worth, your on the wrong path.

If your not spending 5 percent of your homes worth on upkeep every year, you are falling behind.

I owned a home for seven years. I had zero costs during those seven years. I keep hearing what a hassle homes are and how everything breaks, but I just never saw any of it.

You either owned it in a lucky window of time between things breaking, or you neglected something that the next owner needed to fix.

Also consider the expenses of upkeep, i.e. mowing the lawn, so you have to buy a lawnmower or pay someone to do it.

It’s the big things that matter. New windows, roof, foundation problems, driveway and concrete, special assessments, fire and water damage, mold, termites/rodents, repainting and caulking, plumbing/electrical, etc.

Your best chance of avoiding these issues is with homes that are 3-15 years old. New homes and old homes sometimes have big undisclosed problems.

“If your home is more than 20 percent of your net worth, your on the wrong path.”

I admire your principles, but this doesn’t seem even remotely practical. Am I missing something? Shall everyone with less than $1M saved resign themselves to renting?

Right?

Also, my home is the major reason I have negative net worth.

So, I reckon it’s also ALL my net worth?

@Bear Hunter for the past 50 years the “rule of thumb” has been 1% of the cost of a home for repairs and maintenance (you don’t need to spend $100K a year to maintain a $2mm condo in the Bay Area or spend $50K/year to maintain a $1mm home on a $1mm lot somewhere else).

P.S. Most people that bought $200K homes 5 years ago with less than $10K down FHA loans don’t think they are “wrong path” living in homes worth $400K-$500K (with 25 years to go on a <4% mortgage).

Nonsense AI:

Best ever RE mentor, long term owner of many rentals, ALWAYS used the figure of 10% approximately 40-50 years ago; however, to be sure, that was back in the days when he could and did buy houses in SoCal for about 1% of what they sell for these days…

With the vast increase of cost of doing biz w current free lance RE repair and maintenance folx, I suspect his 10% will come again unless owner/landlord folx do their own repairs, etc…

And Good Luck with that for most LLs, after whose ”repairs” I and my crews in the Bay area did TONS of work to fix their work…

Forty years ago in 1984 (the year the Olympics were in LA) the median price home in S. Cal was ~$150K.. The CA Minimum wage was $3.35/hr or ~$7K/year, a good handyman/painter would work for $10/hr or ~$20K/year and a real good handyman worked for $15/he or ~$30K/year. 10% of a $150K home is $15K and you did not need spend that much to maintain a home (10% of the purchase price has almost always been “more” than the “gross” rents for a decent rental rental in CA. P.S. The average cap rate for a decent apartment unit in S Cal in ’84 was ~8% (sure they were higher in N. Hollywood and South Central where most apartments had bullet holes in them) and most decent rental homes had an even lower cap rate so anyone investing 10% in CapX was taking spending close to double his NOI on the property.

Thanks for the numbers. The idea that (market value, principal dwelling)/(net worth) should be < 20% suits my own prejudices. But what is it based on? And what is the source for your 5%/yr number for upkeep? Personal experience? As owner, or landlord? What does this upkeep number include? A very superficial search of the web gives numbers from 1-4%/yr. I am not picking a fight, I have no experience with real estate and would like to understand your statements better.

If you want to get into rentals cheap, buy a fixer-upper and fix it up yourself. Then you will have an appreciation for how long things take and how much they actually cost (vs contractors), plus some skills u can apply elsewhere. You can even live in it while u do it if you have the stomach for it and avoid paying two sides. Refi the reno costs into it when rates are lower too if you want.

Limit your purchase amount by understanding eventual sunk costs (get estimates on repairs as needed) vs mortgage payments and rental rate market locally. That’ll keep you out of trouble. As they say you make money in real estate when you buy it right.

That will also keep your upkeep costs under 1% with good long term tenants btw.

If, early on in your ownership, you purchase the tools necessary to do repairs, you’ll be able to fall into the 1% range. The initial startup is sometimes painful, but good quality tools (ones with cords, not batteries) will last nearly forever. You’ll probably lose it (or it will be stolen) long before you wear it out or break it. I still have my Porter Cable magnesium circular saw…. bought it in the 70’s. My first was a POS Skilsaw that was dangerous to use. Didn’t know what a good tool was. Once that sunk cost is in, repairs get progressively cheaper. Battery tools are fine, but keep in mind that they’re not “forever tools” because the battery technology changes and replacements are either unobtainium or absurdly expensive.

On a $400K house, 1% is (obv) $4,000/yr. Some years you won’t spend that. Other years you’ll blow the doors off it. The key is to build reserves so you don’t have to hock your first-born to keep the box from caving in on your head. I’m a relative maniac about maintenance. Maintenance is usually cheap (like fixing that small leak or caulking a gap in a shower) before it becomes an entire roof tear off including the sheathing, or tiles fall off the wall leaving you with soaked moldy insulation and crumbling drywall.

All of this takes discipline. The purchase of the house is the easy part. It’s the cost of ownership that’s the killer if you don’t pay attention to what the structure is telling you. Smells. Dripping sounds. Rattles. Squeaks. Clunks. Banging noises. They all tell a story. Fix it before it breaks and you’ll usually remain ahead of the game.

“If your home is more than 20 percent of your net worth, your [sic] on the wrong path.”

Doesn’t that exclude anyone with a mortgage and not enough assets to pay it off in full? I thought net worth is assets minus liabilities.

People don’t always comprehend the term “net worth”. In many cases, a house is usually the bulk of ones’ net worth.

However, even if you apply that 20% number to total assets, it’s still lunacy for most people.

CNN: Housing market ‘stuck’ until at least 2026, BofA warns…

MW: Walgreens stock headed for 27-year low after earnings miss

WBA -24.68%

Walgreens’ junk bonds among biggest decliners in high-yield market after earnings disappoint

The US still has cheap properties compared to Canada. Friends just bought a 1 acre property with 2 old (500 sq ft and 700 sq ft) cabins on lake waterfront. The bank would only give them a 15 year mortgage because of the cabins were built in the 50’s and falling apart. $They paid 1.3 million CAD with $4500/month payments. It’s almost impossible to find anything decent under $500k in most cities. Rates are at about 5% here. Building costs are at least $400/square foot. I have friends from Romania who are moving back because they just can’t afford to retire here. Prices have dropped here but in most cases not much and with higher rates most people are now priced out. Sellers are still asking insane prices.

The builder in my new development where I bought last year is once again putting up the 5.99% mortgage signs for the remaining unsold 8 – 10 homes (all built). Before the end of 2023, those signs vanished.

These are smaller houses, roughly 1,200 – 2,300 sq. ft. in size on a small lot in a nice new area of town (~40 miles north of Houston, TX). Sales have been in the $175/sq.ft. range. From what I can see, about 95% of the neighborhood is owner occupied purchases

These last few home sales will close out this area of about 200 homes. Roughly 1/2 mile away, another new neighborhood is breaking ground.

The condo owners in Hawaii are concerned about increasing insurance costs, HOA improvements and decreasing rental customers. I secured reduction of $3k/ month for million$ condo for 3 month rental now in 2024 and again in 2025. Working with another million $ townhouse owner for additional 2-3 months in 2025. Past rentals rates $10k to 8k per month reduced to $7k to 6K per month. Also seeing similar with rental inquires in FLA. However FLA owners are still living in la la land and not business responsive. We are booking more Waikoloa Beach Hawaii with business smart owners.

Mid-May to now weather every day 85/70F, ocean 80F and no rain in Waikoloa Beach. Rest of Big island had rain early May to now result a green paradise. The world is changing fast SHOP !

Hey Wolf have you been following the RealPage lawsuits?

Another site that re-publishes your articles from time to time wrote an article on it (Titled: A National Cartel Fixing Rental Housing Prices: The Scandal Continues to Grow) but I’d be curious to know how you view the impact on the housing market of unraveling this information-sharing middleman in combination with the NAR stuff happening in July.

The story is wild from what I see, and it seems to meet the definition of price-fixing/collusion to the tee. The FBI raided Cortland Management in Atlanta on 5/22 as part of the investigation.

Cortland is a big operator where I live (Raleigh NC), and the fact that their apartment rents are numbers like $1423/month makes me think everything comes out of an algorithm.

There’s a great quote from the FTC chair in 2017 : “Is it OK for a guy named Bob to collect confidential price strategy information from all the participants in a market and then tell everybody how they should price?” Ohlhausen said. “If it isn’t OK for a guy named Bob to do it, then it probably isn’t OK for an algorithm to do it either.”

The months’ existing home supply will have to punch up towards 6 months before there’s going to be meaningful, broad base home price declines. And it’s anyone’s guess as to when that will happen. It’s reasonable to think that a fair amount of the new existing homes inventory is more investor related than homeowners. EVERYTHING in terms of its final move towards recessionary pointing levels is skewed by the massive refinancing of the Fed’s near-ZIRP policy and huge federal budget deficits. It’s all on a very slow burn.

In 2022 supply hit nadir. It’s rising in rolling hills to low/mid level area.

I’m thinking that newly built and used product will be put on the market at lower prices once it makes sense for the owners to dispose the assets that are occupied based on projected lower returns due to evolving profit trade offs on rents and time it takes to sell the occupied asset at x price.

For the empty held properties that are not yet on the market, depends on time velocity curve of price decreases. If I leave my selling price of one of my assets unchanged (and keep holding not for sale the others) and I actually get the price I want in 6-8 months, maybe that amount will still exceed what I would get if I sold today for a cheaper price plus my holding cost. It’s a gamble I know, but that’s why one owns multiple properties. One shouldn’t liquidate their portfolio all at once, correct? But as Wolf said we need to look at the aggregate. I’m sure there are countless properties losing money right now but if one has enough on their portfolios financed with cheaper cash the average could still give one flexibility. Please also remember a cash sale doesn’t mean the individual hasn’t borrowed the cash in a separate facility at another point yet having the freedom to deploy as one sees fit. That’s where exceptional banking relationships come into play.

The 64 dollar question now becomes, will home prices drop down to a reasonable level of affordability? Back in 2010 and 2011 there was basically a half off sale in the Coachella Valley, I hoping for the same this time around.

DD:

Depends not only on the ”locationx3” that some folx think is the only discernable reason, but also on local jobs/industry moves, etc.

There was a time on the Space Coast of the flower state when houses went far below minus 50% when NASA projects ended,,, some folks were selling for 10 cents on the dollar from what I have been told…

And then zoomed once again when new projects commenced.

RE in 1929 was similarly crazy,,, and some old folx such as I am, having heard about that crazy time when properties changed hands more than once a day,, can see quite similar dynamics approaching once again.

IMO, houses are, or should be, for homes.

This reminds me of my thought during my recent HOA meeting:

Condos are meant to be investments, not homes!

My family is the only owner occupied unit (only a 5 unit HOA, 4 residential/ 1 commercial, also used by the owner for their business).

The financialization of everything is permeating everything.

I want to buy a home. I don’t want to get price gouged. I live in the Bay Area, but I could live anywhere because I am a remote worker. Should I relocate or wait it out for the market to soften?