Too little too late? Japan had trade deficits for years; a crushed yen is not good. Needed now: Big QT & rate hikes to bail out the yen.

By Wolf Richter for WOLF STREET:

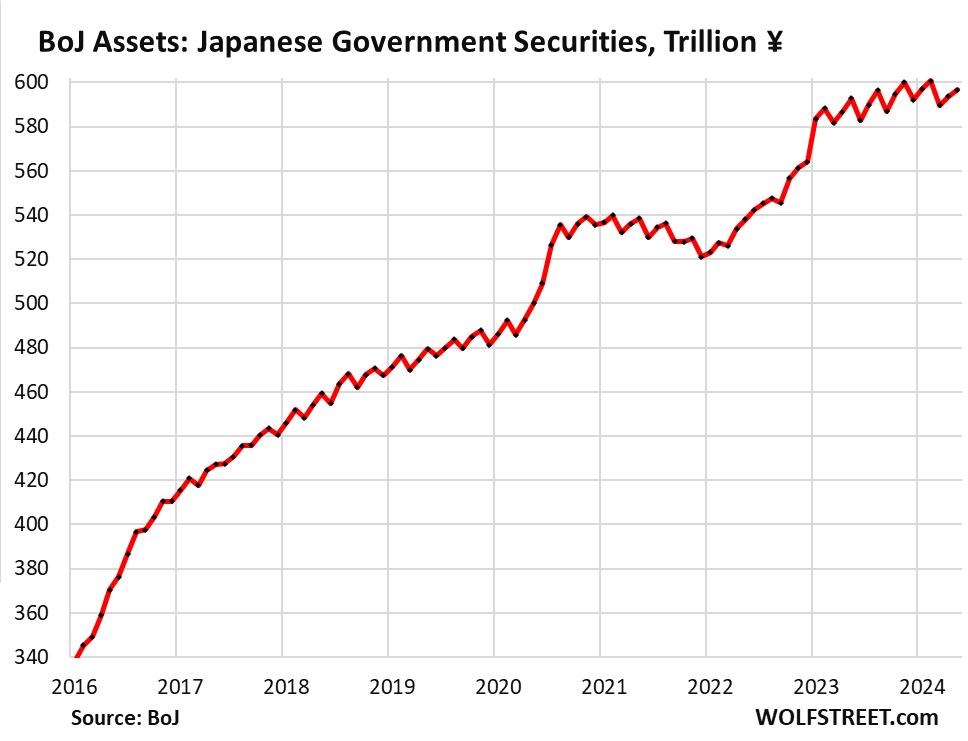

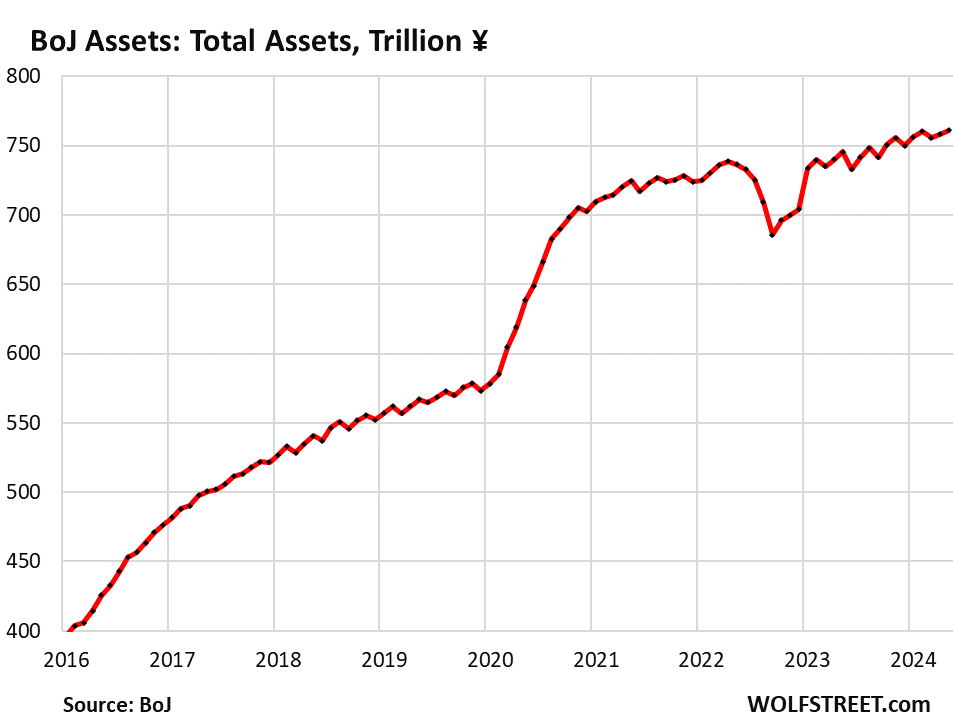

The Bank of Japan’s holdings of Japanese government securities – so Japanese Government Bonds (JGBs) and short-term bills – have been roughly flat since August, with a downward bias in recent months.

Its JGB holdings run on a three-month cycle: Every third month, a large batch of long-term bonds mature and come off the balance sheet, and its bond holdings fall that month, but then it purchases replacement bonds over the next two months, and its holdings rise again. So down big one month, up two months in a row, over and over again.

Its holdings of government securities at the end of May rose to ¥596.7 trillion ($3.8 trillion), the second month of increases, to be followed by a decrease in June, according to the BoJ’s balance sheet released today. That ¥596.7 trillion in May was:

- Down from the ¥600.8 trillion three months earlier (in February);

- Down from the ¥600.1 trillion three months before that (in November);

- Up a hair from the ¥596.4 in August. So QE has effectively ended in August:

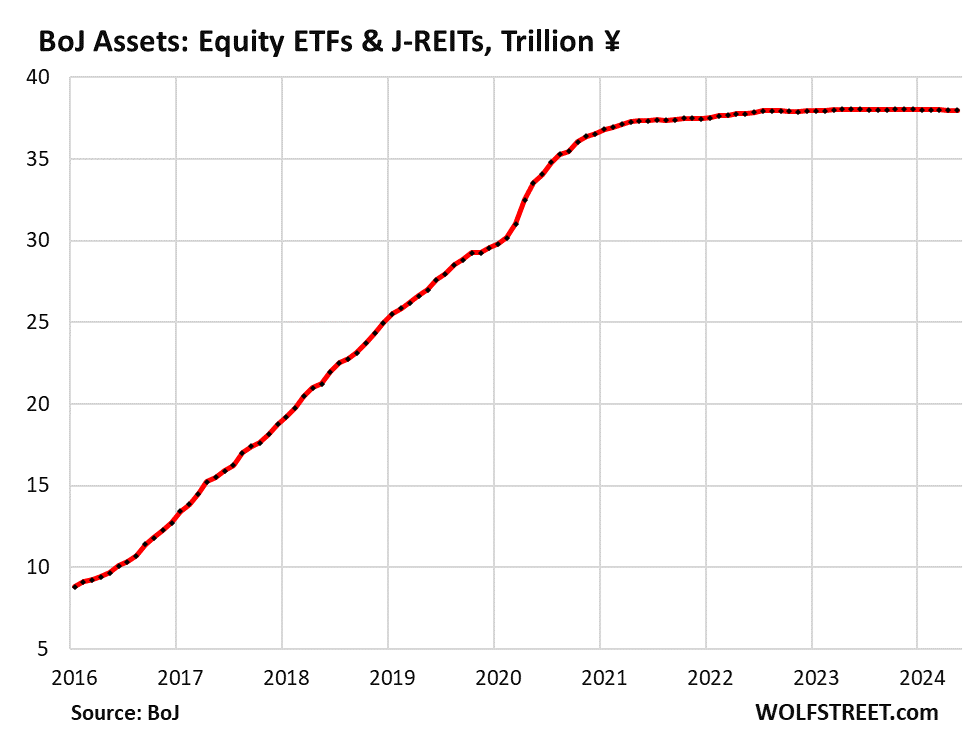

Equity ETFs and Japanese REITs: The BoJ stopped buying equity ETFs and J-REITs in 2022, when they’d reached ¥38 trillion ($244 billion). It carries those instruments at cost, not at market value:

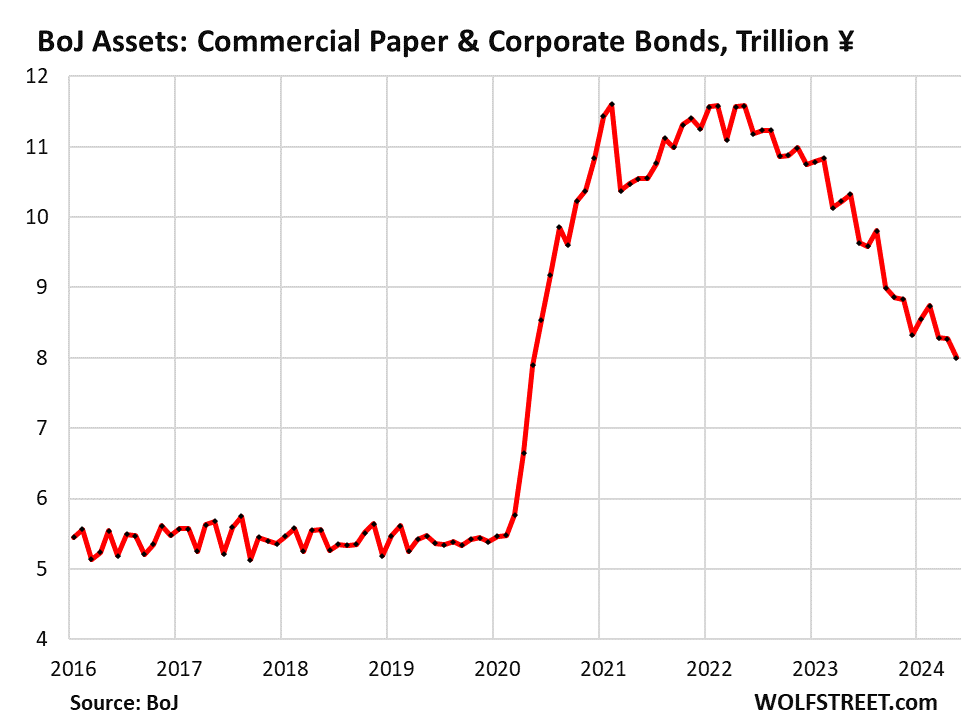

Commercial paper and corporate bonds: It stopped buying commercial paper and corporate bonds two years ago, and they have started to mature and run off the balance sheet since then. It carries corporate bonds at amortized cost. They’re now down to ¥8.0 trillion ($51 billion), from ¥11.6 trillion two years ago:

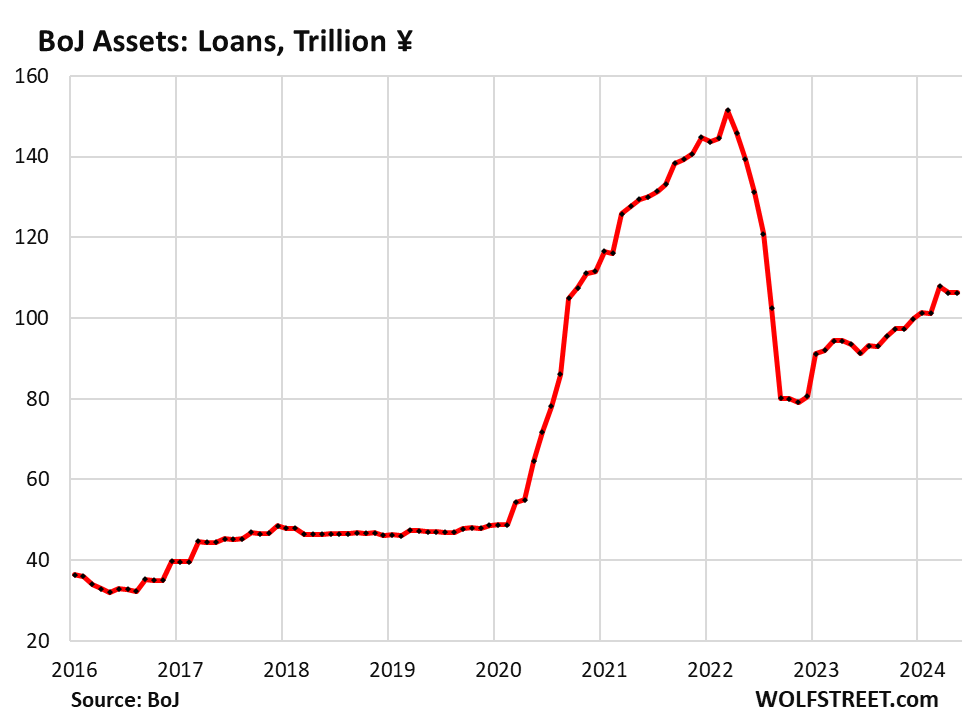

Loans: As part of the pandemic stimulus programs, the BoJ lent money directly to banks and other entities. The total amount of loans outstanding more than tripled from ¥48.8 trillion in February 2020 to ¥151.5 trillion at the peak in March 2022.

At the end of May, the amount of loans outstanding was unchanged from April, at ¥106.3 trillion, and down a tad from March, but down by about 30% from the peak in March 2022:

Total assets – which include the assets above plus gold, cash, and foreign currency assets – have been roughly flat at peak levels for the past four months, at ¥761.1 trillion ($4.89 trillion):

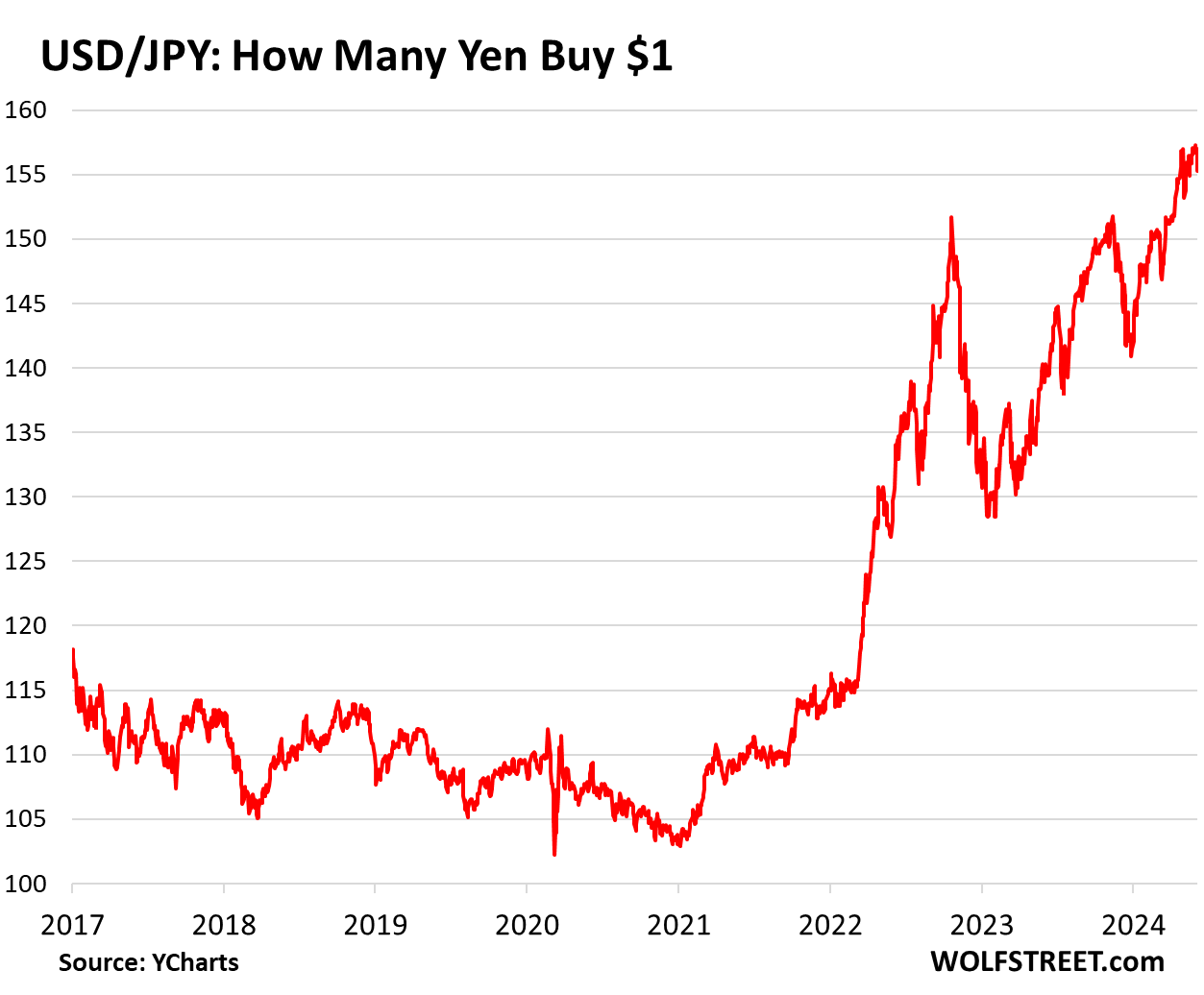

The yen paid the price.

The BoJ is under heavy pressure to do something functional about the yen, which has plunged 43% against the dollar since September 2022, when the Fed started talking about hiking rates, ending QE, and pivoting to QT.

The yen has plunged despite repeated interventions by the Ministry of Finance, including the record interventions between April 26 and May 29 when it sold $62 billion in USD in the foreign exchange market to buy ¥9.79 trillion in yen, to prevent the yen from crashing through the 160 mark.

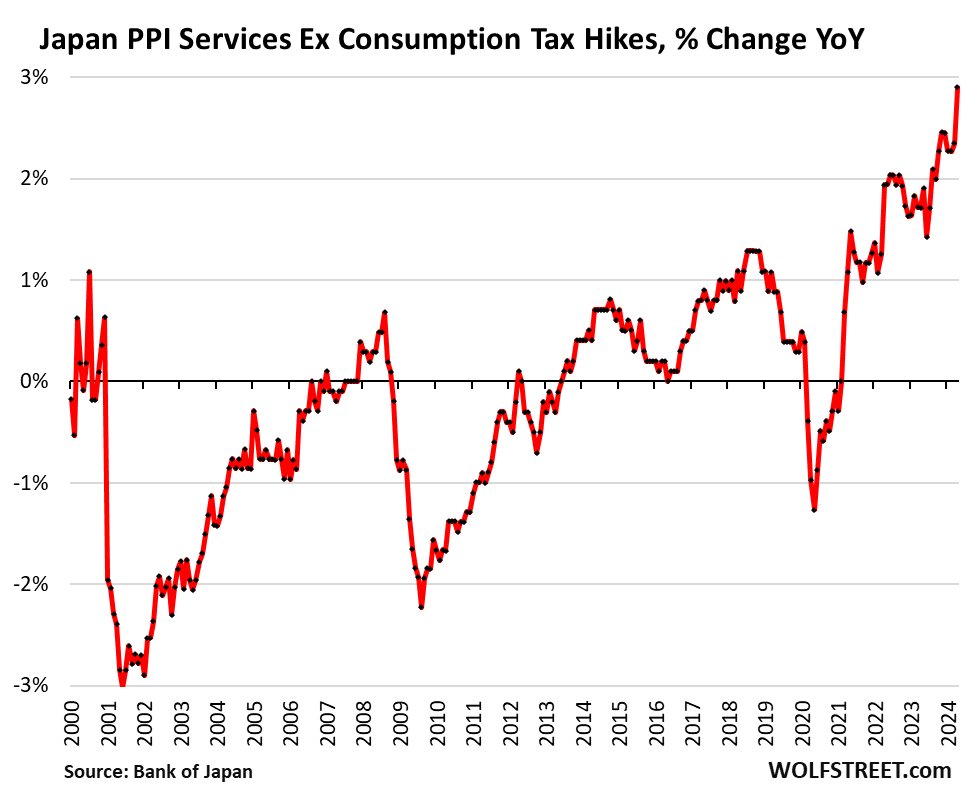

Inflation is surging for Japanese companies.

The producer price index for services that Japanese businesses buy jumped by 0.82% in April from March, after a similar jump in March from February, according to data from the Bank of Japan. On an annualized basis, both those jumps amounted to over 10%.

In the data that exclude the consumption tax hikes in the past, the April spike boosted the year-over-year increase to 2.9%, the worst jump going back to 1991, with prices in some categories jumping by 5% to over 7% year-over-year, such as Civil engineering and architectural services (+7.5%), other technical services (+ 5.9%), training and development services (+6.7%), machinery repair and maintenance (+5.5%), or waste and industrial-waste disposal (+5.1%):

Due to trade deficits, a crushed yen is not good for Japan.

Japan has run annual trade deficits every year since 2010 except in 2016 and 2017, thereby importing more than exporting. And since 2022, the crushed yen has made these imports much more expensive and has widened the trade deficit.

Crude oil, coal, and natural gas (in form of LNG) are imported. So the plunge in the yen caused energy prices in Japan to spike since 2022, on top of the global price spikes. The government has had to step in to subsidize energy costs at the wholesale level.

In addition, all major Japanese manufacturers have offshored a portion of their production. For example, most of the Japanese vehicles Americans can buy are made in North America, and a weak yen doesn’t lower their costs and doesn’t make them more competitive. Even Japanese production gets hit by the crushed yen because supply chains of Japanese manufacturers run through China and other countries, and the crushed yen makes these imported materials and components more expensive and raises their input costs.

The Bank of Japan is responding, but at a ridiculous snail’s pace.

The BoJ can do something functional about the yen: it can hike interest rates in a big way and start large-scale QT.

It already hiked, but only once, and by a ridiculously minuscule 10 basis points from the negative to 0% in March. And it already ended QE last year. And it announced that it is backing away from Yield Curve Control by reducing its purchases of JGBs.

These moves were not enough, leading to the plunge of the yen, and the record intervention by the Ministry of Finance in April and May to slow the bleeding.

What is now required to prop up the yen is actual and substantial QT and substantial rate hikes, not another 10 basis points, which would be ludicrous, and markets would see it as such.

The BoJ seems to have gotten tangled up with the US tightening deniers in 2022 and 2023, believing perhaps that the Fed could never hike as much as it did. And starting in late last year, maybe it got caught up in the Rate-Cut Mania and was apparently expecting that the Fed would cut multiple times in a big way in 2024 to bring US rates down and toward the BoJ’s rate, so that the BoJ wouldn’t have to hike rates much or at all. But instead, higher-for-longer continues to be the strategy in the US, and the Fed is in wait-and-see mode as inflation remains stubbornly high, and the BoJ got caught with its pants down, and the yen paid the price.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

But it’s soooo good for tourism. That’s all you read in Japan.

Japan is hosting the World Expo next year. There are widespread reports in the media about cost overruns, construction delays, countries pulling out, and low public interest. These are typically the kinds of events that would draw tens of millions of visitors from around the world. Is foreign tourism really that popular in Japan right now?

Yes it is. March 2024 was the first time Japan exceeded 3 million overseas visitors in a single month according to the Japan National Tourism Organization.

I go to Japan quarterly for work. Japan is “new on sale ;-) ” and is absolutely over-flooded with tourists right now to the point it is annoying lots of people, including me (think Yosemite levels of tourism).

Parts of Tokyo like Shibuya are now pretty much completely overrun with Ft. Lauderdale quality of tourists and you no longer feel like you are in Japan with all the English signs all over targeting tourists. It is a huge change.

Golden Gai (in Shinjuku) as well, is pretty much only tourists now, almost no more Japanese people. Signs are mostly in English, people (foreigners) are drunk and rude. They also litter all over the place and make a mess all over. It was not anything like this pre-covid.

Train staff..etc. are now annoyed, and no longer polite like they used to me..its just too much.

The sooner the yen goes back up to something more reasonable to reduce the sheer numbers, the better. :-)

That’s so horrible. Japan is, like, the best place ever without tourists.

The last time I was in Okinawa (maybe 2016, so before the yen being so low) the Chinese started coming, so it went from this peaceful wonderland with no litter (even without trash cans, as in the rest of Japan) to a place where there are always idiots, lots of trash, all the coral broken, etc.)

The only possible worse tourists would be the Brits (and Germans) and all their descendants (including USA). And these people will just never know how pathetic their sheltered experiences are compared to if they were real travelers.

Mrs. Watanabe is pleased, though.

In the end, holding a currency requires an act of faith – faith that that currency will hold value…and certainly that the G controlling the currency will not act so as to intentionally gut the value of that currency (by printing).

But when the G becomes enormously indebted, fewer and fewer people believe the G will act in good faith – since printing is the sneakiest/sleeziest/surest way out for a G, from intractable problems of its own creation.

Yes, “Full Faith and Credit” as it were, but isn’t “printing” what has happened to every single fiat currency regime throughout the history of humanity?

Human nature? What’s your point?

Lots of things can be shoved under “human nature”…

Child abuse, defecating in public, murder, etc.

My point is that progress was traditionally thought of as acting so as to reduce such things/the probability of such things occurring.

Running your government/economy upon a principal of fraud (money printing to fund every DC desire) used to be thought of as a bad thing – very likely to lead to worse things.

That’s my point.

The fact that it has be explained is telling in itself.

If DC’s desires are convincing enough, they can be funded through voted taxation not silent, systemic dilution.

“If DC’s desires are convincing enough, they can be funded through voted taxation not silent, systemic dilution.”

That would be a first in human history, that’s my point. Hedge accordingly.

100% absolutely the truth synthesized down to its simplest form. AMEN

I remember Japan as the cheap products producer of the 70’s and can see China falling into the same trap, although it would take some political changes (China being more territorially aggressive) and another 40 years, by which time I won’t care.

I won’t go to China until they allow you to rent a car *without* a driver.

A few months ago all I was hearing about was the yen carry trade and how the unwinding could be something unexpected that may blow things up. Could this be why the BoJ has been slow to increase rates?

The Yen dropping 35% means a bonus 35% to carry traders whenever they unwind. They could not get “blown up” when such a giant windfall awaits.

That is even assuming the BOJ prioritizes the profits of currency gamblers over the financial health of the entire country. Possible, but why?

Does Wolf know how to speak Japanese? Nothing to do with the article, just curious.

I studied it for a while in Tokyo (1996 and then a few years later again), and could have a basic conversation if the conversation partner used the grammatical level of politeness that I’d studied (for example, verbs change), which was not often the case. I could read the two syllabaries (hiragana and katakana) but never learned to read more than 200 kanji, if that many, and so effectively could never read anything of importance. And so my Japanese was largely useless, despite a lot of work, and I gave up, and by now I’ve forgotten everything I ever knew, and I’m fine with it. So to answer your question: No, I don’t speak Japanese.

Howdy. ˌlōn ˈwo͝olf

urufu

That is almost exactly my experience with the Japanese language. It was still interesting to study just to understand how completely different a language can be, though.

(Also to help decipher the rarely seen picture-less menu)

So it looks like my Disneyland Tokyo trip will still be on next year? Shallow.. but very cost saving for my family compared to the USA option. I do hope they work all this out, such a drastic change for everyone there.

Not shallow; just smart. I’m pretty sure you will love Japan and find it to be a country of polite people as well as beautiful and clean. The food is spectacular!

The Japanese government never addressed the main issue which was the domestic saving instead of consumption, and the fix which they have carried on for decades is public infrastructure spending to compensate i.e. the government spent the cash instead. Now game over sadly. Politicos, look good or save the economy, a choice they can’t make responsibly.

I have seen the yen at 240 to GBP so its not impossible for the yen to weaken further although its ridiculously cheap already. The Japanese have already started howling about the sheer numbers of tourists coming in.

However, as an aside, I think its not impossible that the US is moving into a recession with a high debt load and the Fed will have to lower rates, in which case the yen won’t be so bad next year. Thats just an opinion though.

So the FED’s high interest rates are bankrupting other central banks along with the US banking system as well. FDIC reports 63 now dangerously close to going into default. $590 billion of bad debt…all in the futile attempt to show the FED has control of the economy..Yeah Powell, great job!

You got a lot twisted. Read this about the FDIC’s data, including the Problem Bank List and the unrealized losses:

https://wolfstreet.com/2024/05/29/status-of-banks-unrealized-losses-in-q1-worsened-after-brief-rate-cut-mania-relief/

“So the FED’s high interest rates are bankrupting other central banks”

By out-hawking other CBs, the Fed is defending the dollar and the treasury market.

Notice the Bank of Canada just cut.

5.5% is high? ha okay.

the fed is trying to protect the dollar. if that’s bankrupting other central banks, it’s because of their own poor management.

Japan $1.2T is the largest foreign owner of US treasuries. Dividends are soaring . Toyota is sold out. It’s bringing a lot of dollars to Japan. WTI is down to $73. The yen is down ==> export might rise.

The Defense industry is flourishing in Germany and Japan. Rheinmetall will sponsor Borussia Dortmunt, the most liberal club in Germany, in the next 5 years. Borussia 0:2 Real Madrid 4 days ago in Champions League final.

Perfect, thanks!

I will just add, that Shanghai Accord is long broken, Chinese Yuan is quite overvalued and authorities are trying their best to hold PEG (negative around 2%) against USD to prove to the world that the currency is stable. Once Yuan is devalued lower, Yen will gain some strength, and the BRICs will be back decades in any attempt to replace USD, no matter how much gold they have accumulated.

“End of dollar” has been proven all wrong and is still sitting at the top. LONG LIVE THE KING!!!

“Chinese Yuan is quite overvalued”

In the end, currency demand/value is a function of the (international) demand for a country’s products/real assets.

Considering the massive explosion in Chinese exports over the last 20 years (quite probably unparalleled in human history) I’d like to hear why exactly you think the Yuan is overvalued.

It seems to me that the CCP usually acts to artificially *lower* the value of the Yuan, so as to keep the export explosion/trade surplus boom going and going and going.

There might be some short term factors arguing for organic Yuan weakening…but that is against a background of the Yuan being artificially weakened for decades – creating massive pressure for Yuan *strengthening* in the long term.

I’d like to hear the argument for the opposite side.

Basically, all Asian currencies are at all time lows (double digits down), but Yuan is down only around 2% YTD. SHANGHAI ACCORD BROKEN. Check Asian exchange rates.

Logically, this put tremendous pressure on Yuan (cheaper exports from other countries?). If China wants to save their export machine status, they will be forced to quickly devalue their currencies to stay competitive.

Just go to Japan, make ~0% loan, invest in manufacturing around China and avoid China expensive exports. More and faster YEN/Asian currencies are falling, more pressure on China. Plus think of tariffs on Chinese goods, it does not help either.

PAST IS NOT THE PRESENT. While in the past Yuan slowly weakened, also other Asian currencies slowly weakened, there was a balance. Presently, other currencies are falling in much higher pace then Yuan, thus imbalance. As Wolf states YEN “plunged 43% against the dollar since September 2022”. Where is Yuan? Go check other currencies exchange rates.

They make many wonderfull things that are 100% made in Japan and prices are now great compared to what they were a few years ago. Picked up a new set of Mititoyo digital calipers, a Handsaw, and a Cast Iron Dutch Oven that is so finely cast and machined that it can cook a stew with 25% of the water needed with other methods because the lid fits so tight.

Also I just learned you can now buy Japanese Cedar fencing boards 25% cheaper than Western Red Cedar and they are straighter and kiln dried. A new distributor for Japanese grown and milled cedar just opened down the street from me. Who would have thought that one day we would buy lumber from Japan.

Hubberts C- will have to do a deeper re-dive into this, but remember several decades ago that Japanese interests were purchasing and submerging massive amounts of Western North American raw timber (though unlikely, makes me wonder if any of that cedar might be returning homegrown, given Japanese export-labelling regs?).

may we all find a better day.

From what I’ve heard, the BOJ doesn’t care as much as we do about exchange rates; it’s not even part of their overall mission. Their singular objective is to drive up inflation to a sustainable 2%, riding the global wave out of their Lost Decades. The tanking yen is merely a regrettable side effect.

That’s the whole issue here: Japan (government, not people) wants inflation while the rest of the world is fighting it.

The BOJ cares about exchange rates, and works with the Ministry of Finance to intervene in the markets. This turn of events is very problematic because it pushes the BoJ to do something it might rather not do: tighten. And you see that in the balance sheet already.

Market intervention has been broadly accepted by Japanese culture for a very long time. As my father use to say “losing world wars has consequences”. However, this does bring up another important point, specifically that the culture of the country is very different from that of the US. Culture matter, when it come to what is considered acceptable behavior.

Intervention can work for some time, but are heavily limited by amount of US assets owned by the JP government (J-GOV). Once they run out of foreign assets, the game is over.

J-GOV is simply buying time with interventions for BOJ to do something about it, and trying to prevent any quick declines in YEN.

If J-GOV runs out of US assets, the whole system in Japan will collapse, unless G7 steps in. Does not matter what culture it is, it’s basic finance.

Any fast decline/advance of any country’s currency is detrimental for local economy.

LOL! Modern “finance” is complete BS. As a society, the Japanese, in general, are a homogeneous, well-disciplined culture. ALL of the fiat systems die, period. New deals between trade partners can happen and entire systems can be scrapped very quickly. History is very clear on this. The point is, when the system does collapse, how does the underlying population respond. Think about, how would the average resident of Chicago respond versus the average resident of Tokyo.

If the current financial fiat system die, it will be replaced by a new monetary system. “The clever heads” will gather and try to not to loose the power.

Amid the chaos around the world, scrapping for power, there will be potentially wars on physical and economical side. Once the power struggle is resolved, the new monetary system will raise.

Does not matter what an average Joe from Chicago and Hiroshi from Tokyo thinks or does. They will be put on altar and sacrificed for greater good (power?).

I would not say the BoJ ended QE, they continue with a much less pace as before. Their balance sheet still expanding not much especially regarding the JGB portfolio, but it expands. Commercial and corporate bonds purchase amounts and frequency slowed down a bit, and J-Reits fluctuate from time to time in the balance sheet, but no big deal.

My view is also, the BoJ will maintain their policy for a longer period of time, and watch what the other central banks do.

Given how high Japan’s national debt is, how much can they afford to raise rates before they start to get into issues?

Higher rates produce higher incomes. Half of Japanese government securities are held by the BOJ, and the BOJ remits its income back to the government, so that’s a wash, in terms of interest expense. The other half is held by institutions — pension funds, banks, bond funds, etc. — and by individuals. Higher bond yields generate higher cash income that is then taxed at many of these entities, thereby creating higher tax revenues. In addition, other fixed income products, such as bank CDs, and money market funds move along with it and also generate higher cash income for their holders, who are mostly households, and they’re going to spend some of this cash from interest, creating an economic boost, which ripples into more tax revenues, including via the consumption tax. Long-term 0% interest is a destructive policy, and moving away from it will be good all around.

Raising interest rates may help the yen, however, the existing BOJ bondholders would suffer losses and those losses would increase as interest rates increase. No easy answer. They can buy yen (with the BOJ’s other currencies) but this is a temporary and limited solution.

If existing bondholders hold to maturity, they will not suffer any losses. So if they’re not forced to sell, then there are no losses. Bank runs (that force a bank to sell) are not a thing in Japan because the government guarantees in full all “deposits for payment and settlement purposes” (checking accounts, business accounts, payroll accounts, etc.). Interest-bearing CDs and savings products have limits on deposit insurance. An SVB-style bank-run would not have happened in Japan because those were mostly business checking account holders that yanked their money out, and they would have been fully guaranteed by the government. But in terms of trading profits by investors, well, the BOJ famously doesn’t care about them.

I’m wondering where their equities go, with tightening.

> “ETFs and J-REITs …. It carries those instruments at cost, not at market value ….”

So if and when marked to market, a nice chunk of BoJ’s portfolio could take big losses, and the equity markets be propelled downwards even more? Why would it carry those instruments at cost?

Right now, the BOJ is sitting on big gains. If it sells those products, it will book those gains.

If the market drops sharply, those gains will eventually vanish. If the market drops even more sharply for longer, then it might have a loss on its hands. If market value “has fallen considerably” below book value, the BOJ will book an impairment charge. It would do so on two dates per year, mid-fiscal year and end of fiscal year. The fiscal year goes through March.

Meanwhile 80% of Japanese population is getting crushed with inflation. My electric rates will increase 46% from June. We already pay 30 yen per kwh. 65% of food is imported, 99% of fuels, metals , fertilizer, animal feed. They can’t even grow hay, wtf.

It’s time for a bad joke. I bet the average, couch potato Japanese is thinking to himself: I wish I had put my Yen into a real currency, Bitcoin !

Your presentation of the official data of a foreign government is squeaky clean as far it goes. The Japanese, rightfully, should do what maximizes their utility, measured in units of a util.

From my perspective, I need to step back and evaluate the veracity of the historically obnoxious norms of the next generations. Seems to be all wrong. But they are in charge.

The Japanese economy is an exception to the world in which I became aware of the Fischer Theorem of Free Trade that states that the currencies of trading partners will automatically adjust to establish economic equilibrium between imports and exports.

The complete insider has been buying Japan.

Buying a guild society for pennies on the dollar.

Not with USD but with yen borrowed in Japan.

The Japanese have de-valuated their currency by 40 sum percent.

Perhaps, a savvy move by an island nation dependent on an export economy.

The world wide monetary experiments are being unwound in a coreagraphed manner that reassures the future victims that they will be pleased to be paying more for less.

BOJ is slow to raise rates because all of that interest cost on their pile of debt would blow out government coffers. I don’t know the percentage of government budget that would be consumed by interest but it might would be close to 50%.

It’s not that bad.

1. Over half of the Japanese government debt is held by the BOJ, and the BOJ remits its income back to the government; so there is effectively zero interest expense on over half of the debt.

2. higher interest rates generate higher interest income that is taxable, not just on government debt but on all yield products, including CDs, money market funds, and savings accounts. The Japanese have quite a bit in savings in these accounts, and they’ll be making money on them and paying taxes on their income from them, so this will increase revenues for the government.

3. Higher interest income by consumers (retirees!) will at least in part be spent — so consumption goes up, and that is subject to the national consumption tax of 10%, so it’s generating additional revenues.

There are other factors. So when it all washes out, the hit isn’t nearly as bad.