Huge profits in subprime caused specialized dealers/lenders to take big risks, which came home to roost. But prime auto loans are in pristine shape.

By Wolf Richter for WOLF STREET.

Subprime doesn’t mean “low income,” it means “bad credit”; it means a history of taking on too much debt and not paying those debts and other obligations as agreed, which caused their FICO score to drop into the subprime category.

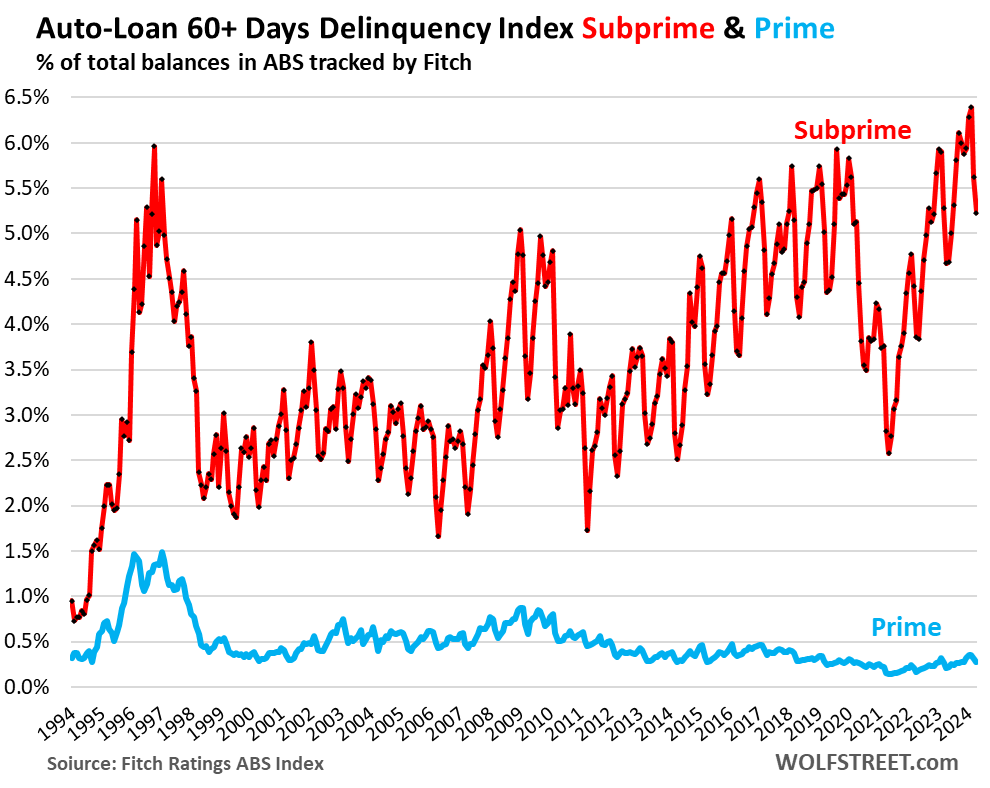

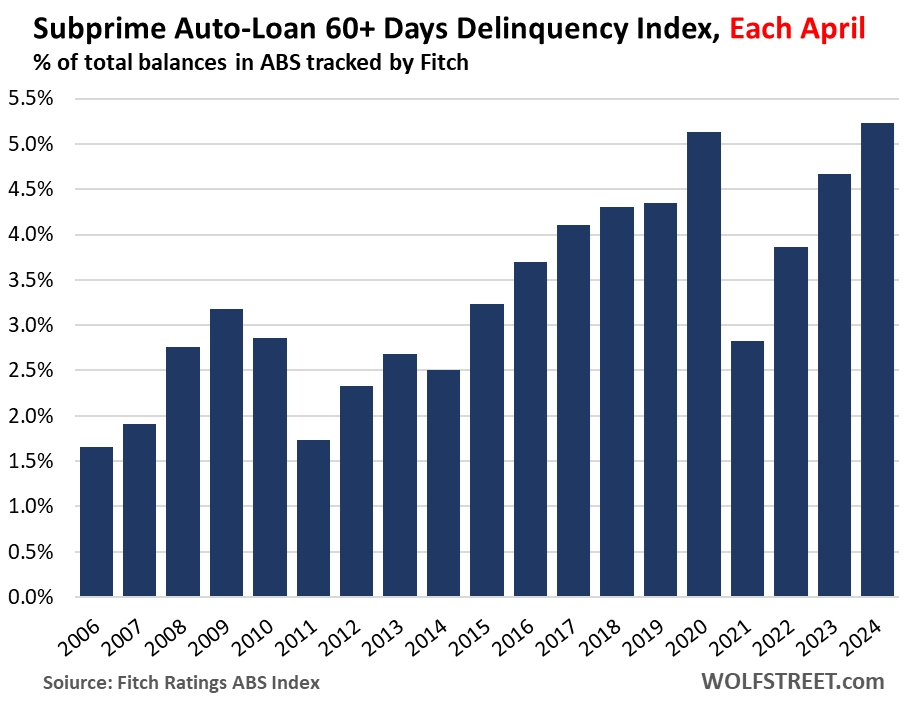

And subprime auto loans are getting into trouble, after the free-money era got them temporarily out of trouble. In April, 5.23% of subprime auto loans were 60 days or more delinquent, the worst April on record, and a hair above the prior record of April 2020, according to the Fitch subprime index, which tracks auto loans that have been securitized into the asset-backed securities (ABS) that are rated by Fitch.

The index is seasonal, with highs every January or February and lows in April or May, as tax-refund season bails out many a borrower. February 2024 had been the highest of any month on record with a delinquency rate of 6.4% (red). But prime auto loans are in pristine conditions (blue).

The Aprils of every year going back to 2006.

Subprime delinquencies were already rising from 2015 through 2019, as subprime lending was getting very aggressive, leading to a slew of scandals, big losses, and the collapse of some PE-firm-owned specialized subprime dealer/lenders in 2018, some of which we discussed at the time, so we’re kind of used to the subprime drama and take it in stride.

The thing is, subprime is a business with huge profit margin on selling the cars, and huge profits on financing the cars at dizzying interest rates, and so specialized companies take big risks to get to those profits, and for some, it ends in a collapse when the risks come home to roost.

Subprime is only a small part of used vehicles, doesn’t impact new vehicles.

With auto loans, nearly all subprime lending is for used vehicles, and most of it is for older used vehicles. The sweet spot is around 10 years old. It’s very difficult to finance a new vehicle with a subprime credit score.

About 61% of used vehicle buyers pay cash, according to Experian. For the 39% who borrow to buy a vehicle, the share of subprime borrowers was about 14% of loan originations. This means that about 5.5% of all used vehicle buyers (those that pay cash and those that finance) get subprime loans. It’s just a small specialized high-risk high-profit corner of the overall used vehicle market.

The subprime share used to be higher before the pandemic, a sign that subprime lending has tightened in 2023, as it always does when delinquencies pile up.

Prices and the mess.

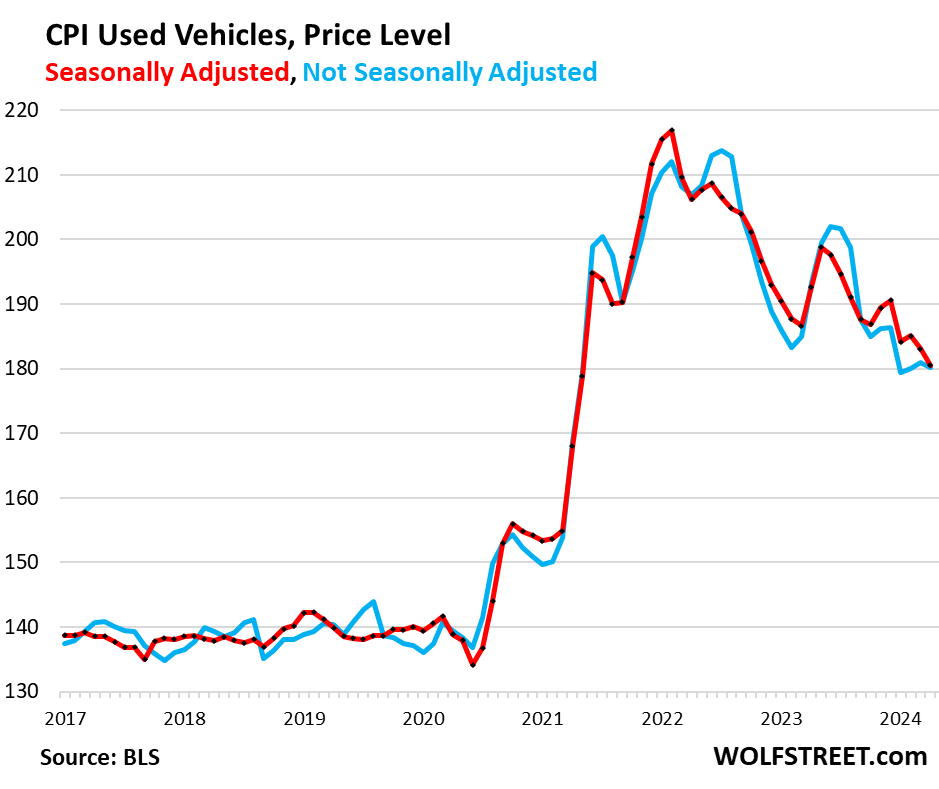

But used vehicle prices spiked by about 55% in 2020 through 2021, and people took out big loans to finance these massively overpriced used vehicles. Since early 2022, used-vehicle prices have given up nearly half that spike, but they’re still very high, and interest rates have shot up. These movements have turned the used-car business upside down.

A few PE-firm owned specialized subprime dealers/lender chains collapsed in 2023, and the largest publicly traded subprime dealer/lender Car-Mart disclosed big problems, and its stock tanked nearly 50% since mid-August, despite the booming stock market.

Losses for investors have been less severe.

The subprime business hinges on the dealer/lender being able to securitize the subprime auto loans into Asset Backed Securities (ABS) and sell the investment-grade tranches of those ABS to pension funds and other yield-seeking institutional investors, and sell the riskier junk-rated tranches that take the first losses to investors seeking higher yields.

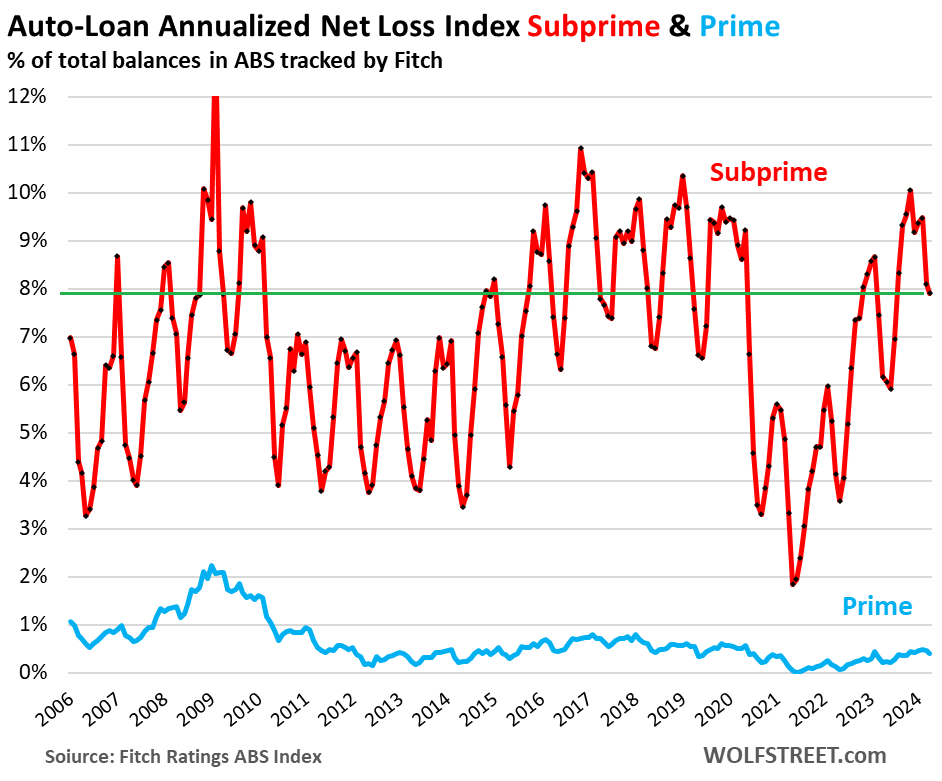

Fitch’s Auto-Loan Annualized Net Loss Index for subprime loans has come up from the free-money lows but has not reached new highs, and has remained in the prepandemic range, which is kind of surprising, and led Fitch to speculate that there was a rotation of delinquencies, where delinquent borrowers, when they got closer to losing the vehicle, resumed payments at the expense of some other debt, such as credit cards, rotating between them.

They’re in essence juggling their delinquencies to stay in a position where they can keep their cars, which has helped keep the losses in the normal range.

Investors earn high yields on the riskier lower-rated portions of the ABS that take the first losses, and those yields compensate investors for taking those credit risks, though it may not always work out.

This subprime mess powered the overall delinquencies.

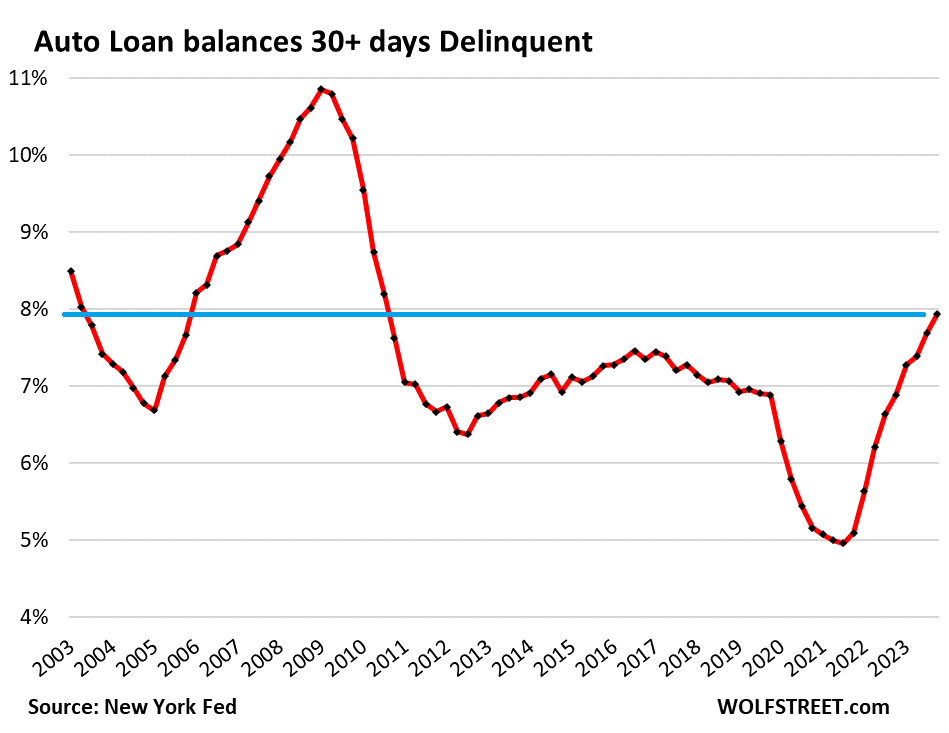

According to the New York Fed Household Debt and Credit Report this week, the 30-day-plus delinquency rate for all auto loans – so 30 days, not 60 days as the Fitch index – rose to 7.9% in Q1, the highest since 2010, and about half a percentage point higher than in 2017. Many of the borrowers who are 30 days behind eventually start making payments again and don’t reach the 60-day stage that Fitch tracks:

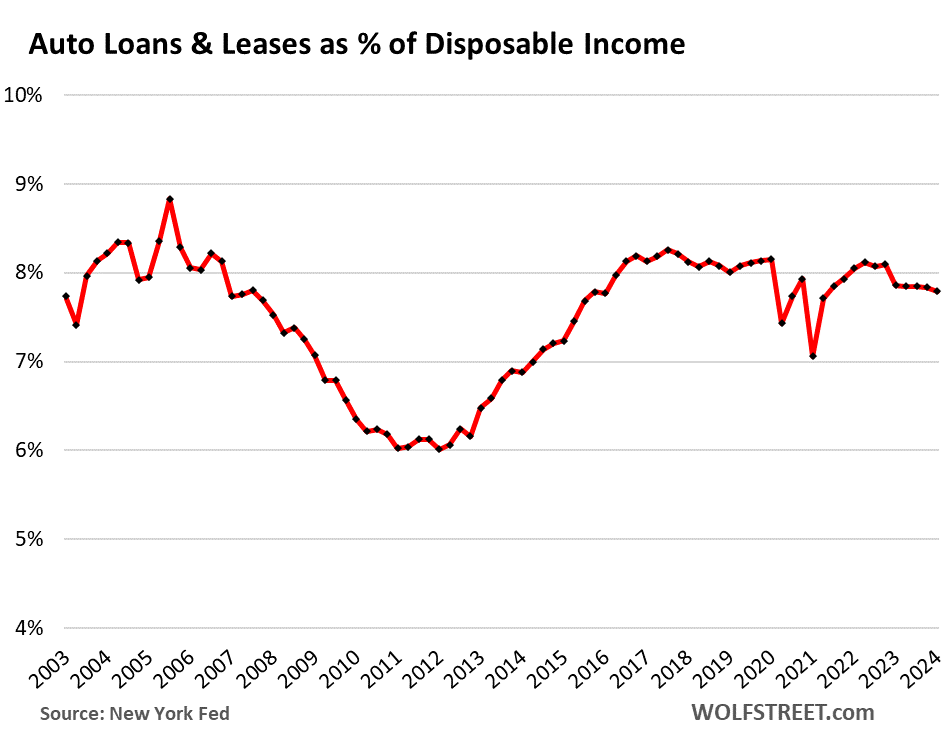

The auto-debt burden is high, due to high vehicle prices.

Surging vehicle prices have caused vehicle debt to surge, and the debt levels have roughly kept up with rising disposable income over the past few years, and ratio remains high.

Note that about 80% of new vehicle purchases and only about 41% of used vehicle purchases are financed, so for people who do finance, the burden can be substantial.

Where the problem arises – as we have seen above – is in the subprime segment where cars are sold with huge profit margins, and therefore at very high prices, and massive payments in relationship to what customers are getting.

Disposable income is income from all sources except capital gains, minus taxes and social insurance payments. This is the income that consumers have left to spend on car payments and all their other stuff:

This concludes our series on Q1 consumer credit.

Earlier this week, we discussed credit cards, mortgages and HELOCs, and the overall credit situation of our not so Drunken Sailors:

Here Come the HELOCs in Household Debt: Mortgages, Delinquencies, and Foreclosures

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So looking at the Auto Loans Balances 30+ Days Delinquent chart, we appear to be about 1/2 through the same cycle that transpired from 2005 to 2009. Overlaying that chart with layoffs, which began to surge in early 2008, suggests we have about 6-12 months to go. before things start to get nasty, assuming we’re on approximately the same 4 year cycle. The next 12 months or so are going to get very interesting. I’m looking forward to seeing the chart push past 9% by the end of 2024. That’s should set the stage for the final act to come in the first half of 2025.

As we’ve said many times here on WS, the ONLY solution for high car & home prices is a good old fashion recession. Specifically, the kind where Congress doesn’t muck with foreclosures. Time will tell. My money is on a whole lotta mucking.

Recently I have a few friends that are laid off and looking all of a sudden. TBD how quickly the market absorbs them, but the one that has been laid off the longest is now knocking on a lot of doors and responses are fairly cold. His termination was December but severance ends in June I think.

Another got cut from a NASA contract, others are photonics engineering types.

I don’t recall this much deficit spending back in 2007. With deficit spending going at this rate, I have a hard time seeing a liquidity issue among consumers who are getting money from the gov’t directly or indirectly to then make a recession.

If one takes a ruler to same portion of same chart as mentioned by Guess What, it also seems 5-10 degrees steeper (just from accuracy of doing it on computer screen.

Most debt, including SubPrime debt is a problem.

It starts with SubPrime, as the poor are the first to go.

A recession will bring other borrowers into question.

When/If the US Treasury ever has a failed auction, the fireworks begin.

How much debt is too much ?

IF House hold debt to income gets too high, bills can not be paid in full.

Car loans will be paid before Home Mortgages, as the debtor needs to get to work for the all mighty paycheck.

Wolf does the necessary work and research.

The US Treasury cannot ever have a failed auction, because the Primary Dealers have to buy the securities. Certainly if a Primary Dealer had a “liquidity problem;” i.e. no buyers from them, the Federal Reserve would open some kind of “window” that essentially would have the Federal Reserve buying similar to Quantitative Easing (QE).

Exactly. The system is set up to support itself. The only question is at what rate the auctions will clear the debt offering.

Obviously this economy is hot with cash and isn’t slowing down. Inflation is much closer to 4% than 2%. I don’t think the Fed can fit or raise before the election, which means the market will set the rates on its own. I’m anticipating 6% 13-week bills by late summer.

At that point what is the rate on a 2015 Honda Civic going to someone with a 550 FICO? 29%?

This.

The auction tails will eventually grow and push up yields, which will keep demand in check.

Subprime debt was only a problem in the GFC because we had so many home foreclosures. That may not happen this time around. We’ve entered a whole new world of Congressional shenanigans in terms of picking winners & losers.

61% used car buyers pay cash

I got asked what I paid for my 2016 diesel 3 years ago

young guy was looking for deal

he guessed $25k

I laughed – $30k? as I continued to laugh

I held out 1 hand with all 5 fingers out

he was W H A T !!!!! as his jaw dropped

said he didn’t want to spend more than $20k

then it’s 20 year old – 2000 f350 ford diesel with 7.3liter

2003-2010 ford diesels are lemons in wait

Had a 6.0 work truck. It spent a lot of time on a flatbed.

Hint: the US treasury, Fed, and treasury markets are set up in a way that it is impossible for a treasury auction to fail. There are built-in safeguards.

MMT guarantees buyer of last resort

Incorrect. Even if the mechanics of the auction don’t fail, but the optics – the perception – matters a huge amount. If and when everyone can see that no one is going to buy at current auction rates, that’ll count as a fail just as surely. The system relies on confidence, not mechanics.

I agree. There’s going to come a time where the bid to cover ratio & auction tail show real panic in the treasuries market. When is a mystery, but I don’t think it’s years and years away. I’ve been saying for about 3 years now, that I think we have an event by $40T in national debt. This event is probably a sustained series of weak treasury auctions that signals Congress needs to act to cut spending.

“If and when everyone can see that no one is going to buy at current auction rates”

That’s not how Treasury auctions work.

If there aren’t enough bids at the when-issued rate, then bids at higher rates will be filled sequentially until all the bonds are sold. Then, all these bonds are issued at a discount to par to reflect the higher yield till maturity vs the when-issued yield. This is known as the action having a tail.

Certainly a large auction tail could be perceived as concerning, but this is a self-correcting problem. A large tail will push up yields and lower bond prices on the secondary market, which brings in new demand. Remember what happened the last time the 10-year poked its head above 5%?

There’s no built-in safeguard that says the bond vigilantes can’t just say no and demand much higher yields.

It’s not necessarily “the poor” (as Wolf pointed out) that are subprime customers. It’s those with a spending problem and live exclusively on cash flow.

Back in my former life, the J.D. Power “Infonet” crowd came in with their monthly market analysis showing us how we (as a manufacturer) were losing registrations to other brands because we cut off incentive offers from our captive above subprime. My question was… so, we pay $X,000 to attract a customer who will abuse the vehicle and then lose our azz when we have to repop the car and then sell it at auction because it likely smells like trash can, was never maintained, and reconditioning would add thousands more to the equation…. Um. No.

Way back when, we had a neighbor who owned a CBOT seat… large home… two Jaguars in the driveway…. private school for Juniorette… mama had a rock the size of Cleveland… and had subprime credit. He had an immense spending problem. Lost the Jags. Then the house. U-haul on the drive at midnight loading what he could in his Ralph Lauren clothing and Gucci loafers.

Credit check should be required to vote

Man, would the GOP owned states love your idea!

I would settle for a civics test….

In other words, there’s a sucker born every minute. The big-truck guys, all alone without anything or anyone on-board prove it.

Just a personal observation, so take with a grain of salt. I bought my wife a Lexus SC430 for $20,000(low mileage dealer maintained cream puff). I am by no means wealthy, as my wife has been disabled for a few years now.

The hate that car attracts is surprising. The wife says she gets cut off all the time. She also has had people flick cigarettes at her when the top is down. Without belaboring the point due to the multitude of incidents she has told me about, it has definitely diminished the joy of having the car(it was a birthday gift when her other car needed replacing).

The overwhelming majority of her bad driving experiences come from pickup trucks and their owners. Maybe they are upset at how much they have to pay each month for their truck?

The “getting cut off” can also be attributed to the low profile of the vehicle she is driving. Low cars are hard to see, even from a not-huge-not-jacked-up 4Runner. I cut off a C8 Corfat – quite by accident – as it was below my rear view mirror field of vision (tailgate interference) and, coincidentally, was darting in and out of traffic, and nearly undetectable in the side view because it was silver in color and lost in the glare.

We have an older BMW convertible. The top of the A-pillar is a tad above hip high on me. We do not tailgate with it. Won’t make a right turn on red or pull out of a parking lot unless we have a clear view of traffic and they of us. It’s far more maneuverable than a F250 and some of those operators of said lumbering behemoths think you’re being cute because you can change lanes in less than a football field.

The cigarette thing I can’t explain. In 30+ years of convertible ownership, I’ve never had that happen.

Same thing happens in my z4. I always try to make sure I can be seen.

My dog is a bigger dog, he’s a Shepard named brandy. The smaller dogs seem to yap a lot, but I have found some of the smaller dogs such like my aunts are excellent cuddlers.

The SCs are good looking cars, so good looking they stand out and draw disproportionate attention.

And, a lot of people know Lexus is an import luxury brand.

And, convertibles are become more and more of a luxury rarity.

And, the middle quartiles of Americans are seeing fairly unprecedented levels of economic stress/threats (mainly revolving around housing and /or existing debt/unZIRP.

And, people tend to exist in their own bubbles…so some of the top most quartile may not fully realize what is bubbling along at a nice roil in the significant majority of America.

Not excusing the bad behavior, just explaining it since the poster seems genuinely asking for feedback.

And things might get worse.

I’m actually pretty surprised that some of the millions of disaffected student loan debtors haven’t lobbed the odd Molotov into faculty parking lots pretty well populated will higher end autos.

The way many trucks owners stomp on the accelerator, you’d think gas was free.

People are ignorant. They probably assume you bought it new and paid a fortune and have a chip on their shoulder that you have something nice. I always drive a 1 or 2 year old car and I always get a snarky comment about how it must be nice to “own that”. I always want to say “Well, your just too stupid to realize that my used luxury car probably cost less than that Chevy that you financed new for 84 months because your an idiot” LOL

It’s different than you think. People know Lexus drivers are going to hit the brakes so they have few qualms about cutting in front. Same with MB, etc.

The cigarette thing – next time that happens get the plates and call the cops. Attempted arson is pretty bad, car interiors go up pretty easily. Really.

Thanks WR for this report.

This thing is too small to make dent anywhere .

Everything is chugging along well.

Agreed. All it’s going to do is make a dent into some investors’ pockets, and it already has, and outside of those investors, no one noticed.

Well…maybe.

But I seem to remember a lot of 2007 era brave talk about how strong the economy was and therefore how easily serviced the then record levels of debt were.

ZIRP resulted in badly inflated asset valuations and unprecedented levels of asset value correlation (the parts of the everything bubble all being correlated to…zeroed interest rates).

To the extent that leveraged asset ownership is really predicated upon using some other leveraged asset as collateral, the whole house of leverage can collapse very quickly…just like 2008. It is simply a latent domino effect.

Subprime auto isn’t like this per se…*but* there is a reason why the subprime mkt exists at all…it allows marginal units to be sold – that wouldn’t otherwise be sold at all.

So those millions of units, in an era of unZIRP may/will go unsold – with the knock on effects for used car dealers…and the knock on effects of *that*

In a highly leveraged economy, things tend to be highly interconnected – even if not explicitly so.

Just ask the pre 2007 brain trust at the Fed.

Well said all this, Cas. I feel like we’re again underestimate the risks and how quickly things can go down-hill with how over-leveraged the US economy is now. Not immediately right now but certainly, by around December or start of next year. This is the danger with things like such massive asset bubbles and running a consumer spending economy so heavily depending on massive amounts of more and more debt. It makes every system more vulnerable to a failure point, and that point becomes closer and closer and more dangerous when inflation drains away people’s spending power even more.

The consumer is not “overleveraged”. The government and businesses are overleveraged.

Everything can be sold, it’s just a question of finding the right price.

Subprime doesn’t enable selling those cars, it merely enables the cars to be sold at a massive profit. And it significantly curtails the supply of inexpensive cars, ultimately harming the people who need a cheap car.

Good to see used car prices coming down. With no inflated asset-holders to manipulate this market, and no subsididized loans to distort it, interest rates are doing what they’re supposed to and depressing prices.

I’m in the pay cash camp for used vehicles and desperately need a work truck. Subprime may be a small part of the market, but they are the ones that have driven prices up.

Would love to know the vehicle make up but I suspect that people who have pushed pickups to astronomical levels are overrepresented based on what the used truck market has looked like.

I too am looking for a cash deal on a nice, low-mileage used vehicle. But I suspect that those subprime car owners are not able to afford proper maintenance on their vehicles. If they struggle to fill the gas tank, are they going to be sure that the oil is changed regularly, etc.? Probably not.

So buy with care.

My old man had to buy a work teuck in that market, it was rough. I’m not sure I’d put the blame squarely on subprime for it though. When all the manufacturers had supply chain issues and the wait time for a new car was 6MO or often more, and the manufacturers focused on the highest margin vehicles with the parts they did have, vehicles few could afford.. Well people still had money, still needed vehicles, but many did not need the top end and didn’t want to pay that much or couldn’t, so they flooded the used market, used car prices skyrocketed. So it’s not just subprime, it’s everyone. With used vehicle prices as high as they are anyone who can manage to wait 6MO or so for their car is going to now because it just makes sense, a car is a big expense, might as well get new for just a bit more, that relieves some pressure in used market.

I do think subprime owners getting repo’d is going to ease the pressure a bit more but IMO it’s wrong to act like they made this mess, I don’t think they did.

It still amazes me that GMC exists as a separate Marque – as opposed to there being just one good old “Chevy Trucks”.

My guess is that GMC’s output really doesn’t end up as work trucks.

But that means hundreds and hundreds of thousands of *annual* *luxury* *truck* buyers – three adjectives that would have floored a younger me.

My current and previous work truck are GMCs. Real simple. In everyway identical to the Chevys – in price and mechanicals. Now when it comes to appearance, the Chevys are beaten with an ugly stick. Maybe GMC have more luxury features on the top end, I don’t know. I peddle in work trucks and base models and there’s always been an equal priced GMC model there. Give me a choice and I don’t want all the Chevy plastic cladding, child-crayon-drawing two-tone coloring and the fugly grilles. I can still be dirty and classy.

Digger,

Very interesting to hear that.

I did some hemi-semi-in depth eyeballing of truck prices maybe 8 to 10 yrs ago and I was pretty convinced that GMC’s entire reason for existence was to slap more/shinier chrome on existing Silverado platforms and charge 50-100% more than the base Silverados.

(GMC also used shinier auto wax).

In fairness, the GMCs did have more luxury trim appointments than the Chevy models…but I could also see those very things getting beat to hell/broken in an actual, daily work truck.

So I’m very surprised to hear about GMC/Chevy price parity.

Perhaps it is a function of the pandemic price spike.

Any other GMC drivers out there?

…might be an old, truck ‘branding/image’ issue (i don’t think there were ever any GMC-badged sedan-class vehicles produced. I understand that there were some technical differences between GMC and Chevy pickups back in the ’50’s/early ’60’s, when GM had their healthy, mechanically-variant BOP divisions alongside of Chev in the sedan classes of that period. I can recall, back in earlier days of multiline GM dealerships, GMC was often seemed offered in conjunction with BOP vehicles, while Chevy dealers were more often a standalone concern…). Oh well, off to do some more 200k frontend work on the ’03 Sonoma ranch truck (p’np Chev S10 parts interchange just fine…).

may we all find a better day.

Cas – my inner anorak prodded me into checking GMC brand history issues, Wikipedia does a fair job, here…

may we all find a better day.

New and used vehicles are still at outrageous prices, what more astonishing is that my state of Colorado has made it too #1 in vehicle theft. Auto insurance is constantly increasing regardless of age group, hard to justify so much cost in a depreciating asset. The infant mortality of American automakers just seems bewildered with recalls and defects for these lofty prices. Makes your wonder if the airbags will even work when the time comes.

Thanks for helping place subprime in proper perspective.

How does the Auto Loans and Leases as a percent of Disposable Income react if/when U3 finally marches upward.

An overlay of your last chart in the article over an unemployment number background, and going several recessions back in time, would be interesting to see for historical perspective. Or maybe total HH debt would be even more pertinent than relatively puny subprime category.

(Maybe, just maybe, the Fed has truly discovered the secret sauce that prevents hard landings rather than just postponing them — in which case disregard my inquiry!)

I think the part of the article laying much of the blame on used vehicle prices is correct. It is one thing for a subprime borrower to make the payments on a $2000 VW Bug ( remember when used car lots had such things), and quite another to make the payments on a $15000 Audi.

In the mid 80’s you could get a nice 60’s VW Bug for ~$2K at a used car lot but the minimum wage in CA was just $3.35/hr (I owned a $2K ’66 Bug with the 50hp 1300cc engine back then) Today with the new CA $20/hr minimum wage you can buy a ~$12K Audi for about the same percentage of your income. P.S. I saw a ’66 Bug sell earlier this month on Bring A Trailer for $26K (more than a new Porsche 911 cost in 1980)…

Putting the blame on used car prices? No. If I put a $1M price tag on a ’73 Vega and some knucklehead pays that… is it the fault of the Vega or the knucklehead?

I put the blame on poor impulse control displayed by said knucklehead.

Cars are a commodity. The values rise and fall – daily. BlackBook has (or at least had) a data resource that updated daily based on major auction activity. Vehicle type, VIN code (determines trim levels, model year, factory source), mileage, etc.. We used it during “stop sales” to calculate dealer reimbursements for losses until we could provide updated parts. Funny part was that we often paid zero on many vehicles because auction prices went up from what the dealer had it inventoried for – likely due in part to the reduced supply resulting from the stop sale.

We would also strategically withhold lease returns for seasonality or relocate them to more lucrative auctions where prices were higher. Online factory auctions have changed the dynamic somewhat but we would also direct vehicles to dealers in other markets who would pay more by giving them earlier access and then eat the transportation costs as it paid dividends to do so.

@El Katz: Being forced to buy a car to get to work at prevailing prices does not indicate poor impulse control, nor doing so implicate the person as a knucklehead.

No one is forced to buy outside their means.

I was just looking at used 09-12 Honda Accord prices, which ranged between $5k and $8k for the rare V6/6MT coupe variant I’m particularly fond of.

More than enough car to get you to work.

A Honda Accord, a nice car for a good price? I’ll take it.

Some younger car buyers aren’t aware a car has oil in it, needs water, a spare tire. They ruin the engine.

If no one taught you, you learn the hard way.

Others are suckers for everything the mechanic suggests, spending hundreds when you only came in for an oil change.

I remember when I got my first vehicle, a work truck, spent a lot of time in the bone yard….a little grease monkey.

MM,

What are the mileages at those vintages? The vast majority of buyers are not “car people” and are scared to death of buying a lemon in the used mkt – especially the deep, used market.

A 2009 model is almost 16 years old at this point and could easily have 200k miles on it – at that point, a lot of “non car people” expect something to break/disintegrate every week – and they can’t fix it themselves…leaving them to the tender mercies of the repair shop…whose bitter experience usually results in…more bitter experience.

And it is easy to say “buy the brand” (Toyota, Honda) but the worst experience I ever had was with a cursed used Prelude, serviced by multiple Honda Dealership vipers.

Buying used is smart (although much less economical than it used to be), but still very threatening to your average buyer…who defaults to higher priced, newer models due to that fear.

More truly buyer-aligned online tools and honest third party programs/services would help with this…but are still relatively scarce considering the auto mkt has been around for over 100 years.

There is a lot of used car info…but a lot of it is bad and suffers from conflicts of interest and/or no real skin in the game for any given car. Ditto mechanic pre-sale reviews…has anybody ever successfully sued such mechanics for missing a lemon?

A $15-20k used vehicle isn’t something people feel good about having to take a flyer on – especially since they can *easily* remember paying the exact same amount for a new vehicle with a 3 year bumper-to-bumper.

Cas127,

The mileages I was seeing were 120-160k. But you do make a very good point re buying used; you don’t know how the previous owner maintained it. I was fortunate to buy my 2011 RDX from family.

I guess I consider buying older vehicles and learning to maintain them part and parcel of living a low-budget lifestyle.

I also think the regular 4-cyl Accords would cost even less.

Slightly unrelated and an oversimplification but the power of the auto lobbies in fighting against public transportation was significant and of course those lobbies still have significant political power(I.e. tariffs on EVs from China) as the party that wins the rust belt wins the WH. The consequences of so little investment forces almost everyone to own a car, buy insurance, and of course the environmental consequences, pollution and so on. There are some local areas that do this well but by and large not too many. Western Europe for example urban commutes are around 15% versus in the US 2%. Nothing wrong with cars but there was little balanced policy.

“as the party that wins the rust belt wins the WH.”

Very,very true but underappreciated. WI/MI/OH/PA tend to tell the tale with maybe 2-3 junior tier players and a larger number of phoney-baloney “swing states” the dying MSM tries to buffalo into existence.

Hell, I wouldn’t be surprised if “walking around” money in *Philadelphia alone* determined half of the close electoral elections in the last 60 years.

Thanks Wolf – great info as always! Any insight into what – if anything – interesting in the antique/classic/collector car market? Remember a recent comment suggesting the market was softening. Always curious what’s happening in the “car toys” world!

Appreciate your work, will ring the bell shortly!

Let me just say this: I love cars, and I love old machines, and I love it even more when they come together. But it boggles my mind to see the price people paid in recent years for what were mass-produced super-mediocre vehicles that are now 30-40 years old, such as the fox-body Mustangs, that came after the Mustang II (disclosure: I owned a 1968 Mustang with a 289 V8 and a three-speed stick, and it was a piece of crap, and I owned a 1978 Mustang II with a 302 V8 back then with a 4-speed stick, and it was better but still bad). The fox-body Mustangs came after that. They were made during the worst years of US auto manufacturing. Mustangs with a V-8 at that time were so front-heavy (rear-wheel drive!) that they were treacherous to drive on slippery roads. Thankfully, those V-8s at the time didn’t have any power. But if people customized those engines to produce more power (I did, turbocharging the 302, modifying it, removing the emission controls, and running it with leaded gasoline, LOL, those were days), the car became even more treacherous, I promise. There was nothing special about the Mustangs of that era. It was just a run-of-the-mill lower-end two-door. I just don’t get how a mass-produced mediocre car like that could have become a collector’s item that people are trying to sell now for tens of thousands of dollars. I think there’s something seriously inflated here. Prices may have come down some, but still, they just boggle my mind. I think 0% for years did a job on people’s brains.

To answer your question: I don’t follow the classic car market closely. I look at some of the auctions and read some of the reports because it’s always fun. But I don’t look at it in any serious way.

I always find car advertising in the US fascinating. It must work otherwise all the companies wouldn’t spend so much money but the lifestyle and features being sold are so irrational. The latest one where a woman is on a horrific blind date and can remotely start and have it back up 6 feet is so representative. Marketing is also societal and cultural so it reveals a lot, I just can’t put my finger on it! My “mid life crisis” wasn’t of material purchasing nature son perhaps I missed that aspect since almost driving off a cliff somewhere in the middle of nowhere isn’t on my bucket list.

BTW, you have a tripwire term in your screen name which has been sending ALL your comments to moderation. Try your old screen name (“Glen”). Would save me a lot of time, LOL

Crazy that you only made 300 HP on a V8. These days a turbo-4 can make more power than that.

300 hp? LOL. My 1978 Mustang II with a 302 V-8 was rated at 141 hp. It was an absolute dog in factory version. A Celica with a small 4-cylinder engine could peel away from it at every traffic light. It was embarrassing that Ford built anything like that (my turbocharged version was hot though, but had lots of problems, not fun to drive).

These were terrible engines and bad cars. And they remained terrible until about 1989 when Ford started making some higher-performing engines, such as the DOHC V-6 (Yamaha designed) that went into the Taurus SHO, or the supercharged V-6 that went into the Thunderbird Super Coupe, or in the early 1990s the 302 that went into the Mustang SVT Cobra, but it was still rated at only 235 hp, LOL.

The Super Coupe was what I always got as a demo after they came out and until I left the industry, they were good cars. These performance versions were the first decent cars Ford had made in decades.

Hagerty’s American Muscle Car Index has been leading the way, down 8% in the last year.

///

The used car prices, I expect, will only go higher. Reason being EVs have no resale market potential until the battery price for a replacement is affordable. (If you buy a 12k car, and you need a 9k battery replaced, it aint much of a deal). With an increasing % of cars bought being EVs, the market of used combustion engine cars will get tighter.

///

I wonder how long before the technology and the battery become cheap commodities. I remember the days of a few MB of memory was $50 and now it is virtually free by comparison. Not sure if I will ever own an EV but hoping my ICE RAV4 holds out until next evolution.

What LouisDeLaSmart said is not on target. Used EV prices dropped because Tesla massively cut its new-vehicle prices, and when that happens, recent-model-year used model prices drop by a similar amount. It’s the spread between new and used that matters. Since Tesla stopped cutting prices, used EV values have declined about in line with ICE vehicle prices. It’s not the battery. It’s Tesla’s price cuts.

BTW, you have a tripwire term in your screen name which has been sending ALL your comments to moderation. Try your old screen name (“Glen”). Would save me a lot of time, LOL

DM: Why some Californians are buying pink pineapples for more than the average household’s weekly grocery bill

A produce distributor is selling an ultra-rare newly created species of pineapple with a shocking price tag. The Rubyglow pineapple is being sold at Melissa’s Produce for $395.

Putting something out for sale to create clickbait-headline stories, and someone actually buying it in an arms-length transaction are two different things.

DM: Target starts price war with Walmart by slashing the cost of 5,000 popular items

Target will be lowering prices on at least 5,000 frequently shopped products across its assortment ranging from milk to diapers, the big-box retailer said on Monday.