Only 18% of credit-card holders maxed out their cards, less than before the pandemic, but fell behind at a higher rate.

By Wolf Richter for WOLF STREET.

Who are the cardholders that became newly delinquent in Q1? They’re cardholders who’d maxed out their credit cards in the prior quarter, having used up 90% to 100% of their available credit, with all their credit cards at or near the credit limit, according to an analysis by the New York Fed of Equifax data.

But only 18% of credit cardholders are “maxed out.” Not 18% of consumers, but 18% of credit-card users – big difference because many consumers don’t have credit cards at all, but use debit cards.

Credit card utilization is a function of both the amount charged to the card and the card’s credit limit. So people with lower limits generally have higher utilization rates.

Cardholders can also be maxed-out because the lender lowered the credit limit to prevent further spending.

Credit-card utilization rates in Q1:

- 52% of cardholders used less than 20% of their available credit

- 19% of cardholders used between 20% and 60% of their available credit

- 11% of cardholders used between 60% and 90% of their available credit

- 18% of cardholders used 90% or more of their available credit; they’re “maxed-out”

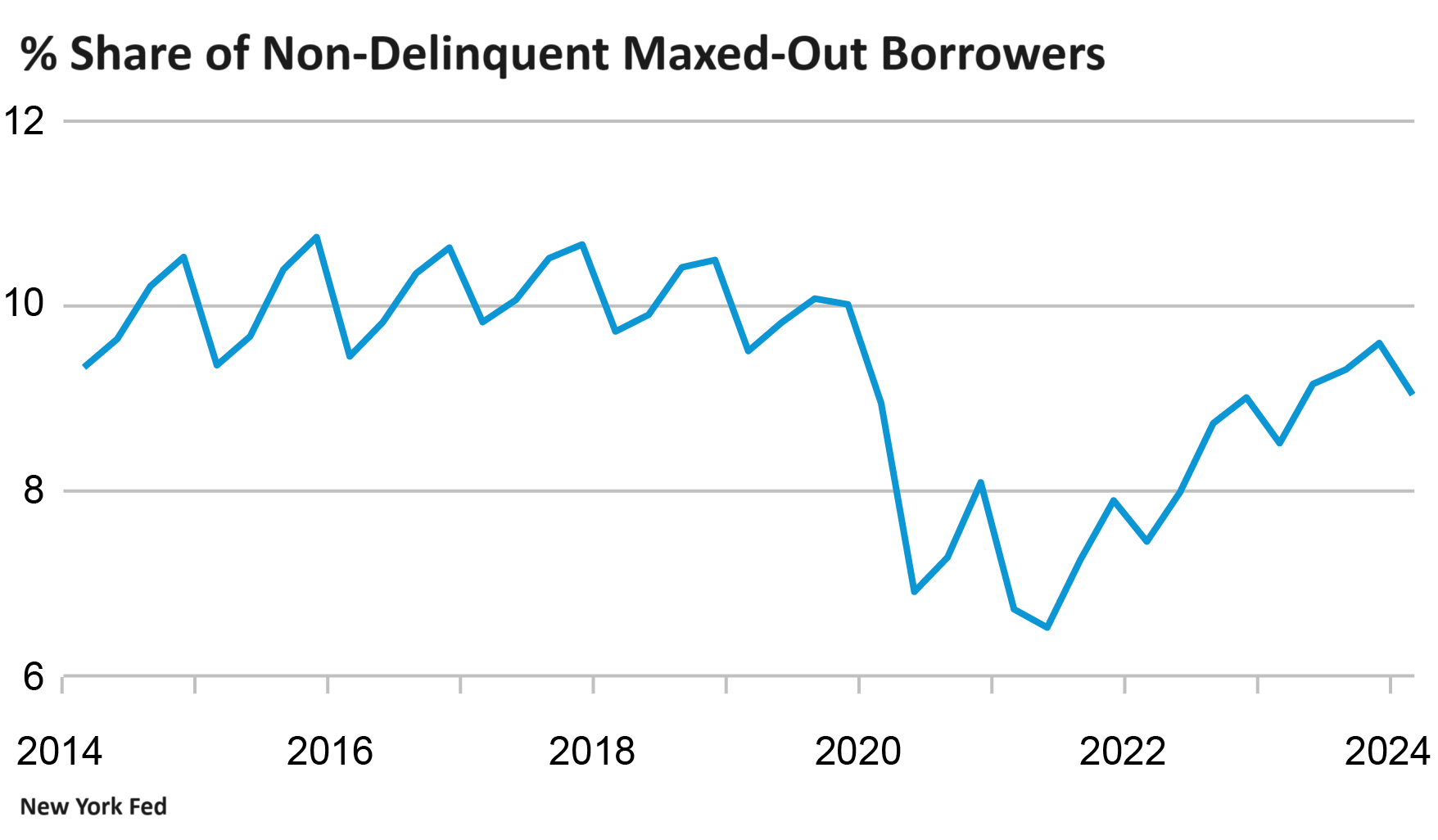

The share of maxed-out borrowers has been increasing from pandemic lows but it still below pre-pandemic levels, according to the New York Fed’s study. In Q1, the share of those maxed borrowers was 18%, and this includes borrowers who were delinquent and those who were not delinquent.

The share of not delinquent maxed-out borrowers hovered around 10% before the pandemic. It plunged during the pandemic as people used stimulus money to pay down their credit-card balances. And it started rising as spending took off again. But the share remains below prepandemic times.

As is typical for Q1, some borrowers paid down their cards from the holiday spending binge and then were no longer maxed out, and the share dipped:

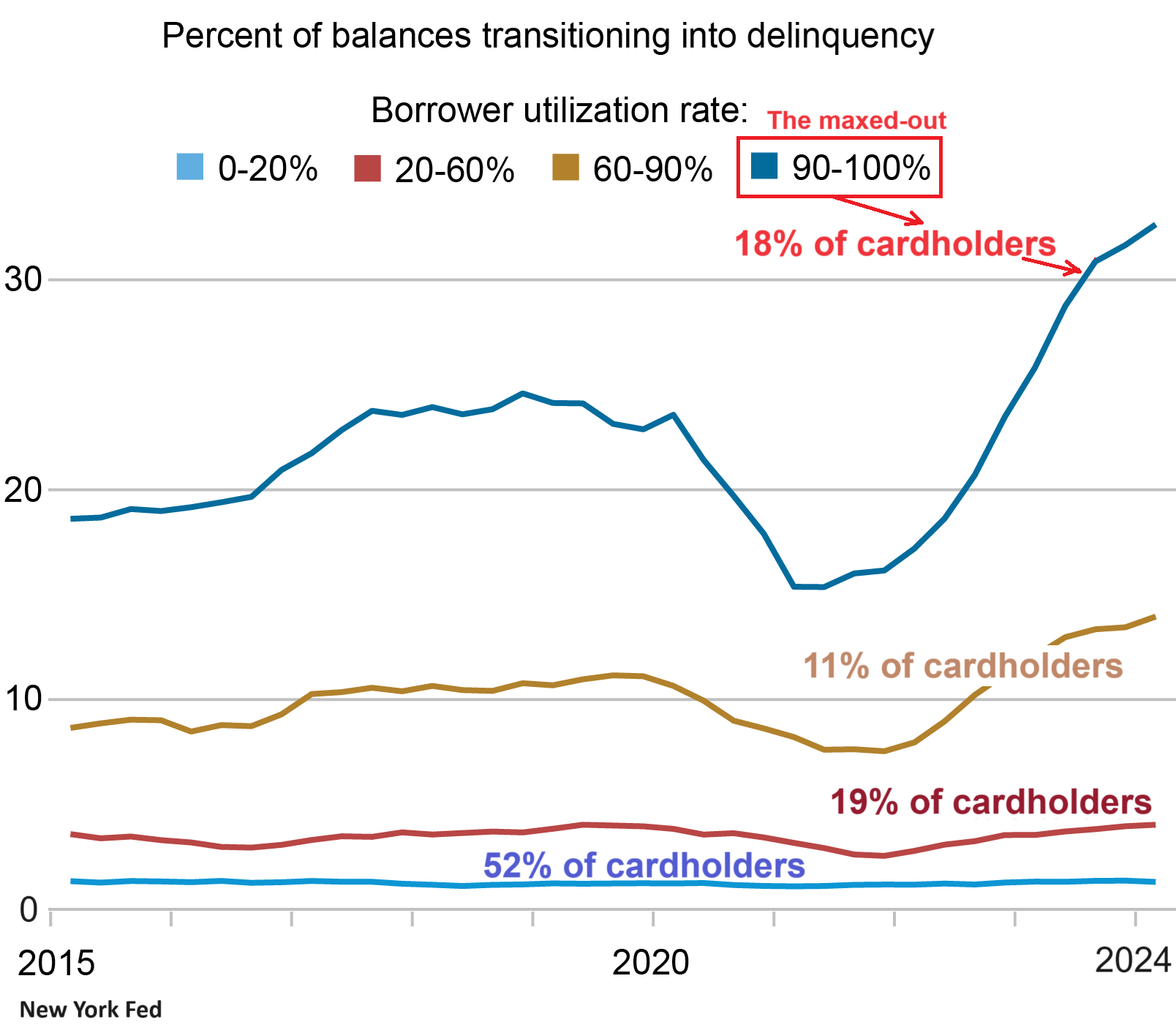

Transitioning into delinquency v. available credit.

Of the 52% of cardholders who used less than 20% of their available credit, only a small portion missed a payment in Q1 to transition into delinquency. Those rates haven’t changed much and are roughly the same as before the pandemic (lowest blue line in the chart below).

People miss payments for all kinds of reasons, in addition to being short on cash, such as forgetting to make a payment, or an automatic payment not happening. So there are always some missed payments that get fixed quickly, and these people then transition back out of delinquency.

The 19% of cardholders who used 20% to 60% of their available credit had experienced a dip in the rate at which they transitioned into delinquency during the pandemic, and the rate then rose back to pre-pandemic levels and remains low (red, second lowest line in the chart below).

The 11% of cardholders who used 60% to 90% of their available credit have transitioned into delinquency at a higher rate than before the pandemic (brown line, third lowest line).

The 18% of cardholders who are maxed out transitioned into delinquency at a much higher rate than before the pandemic (chart by the New York Fed, we added the labels).

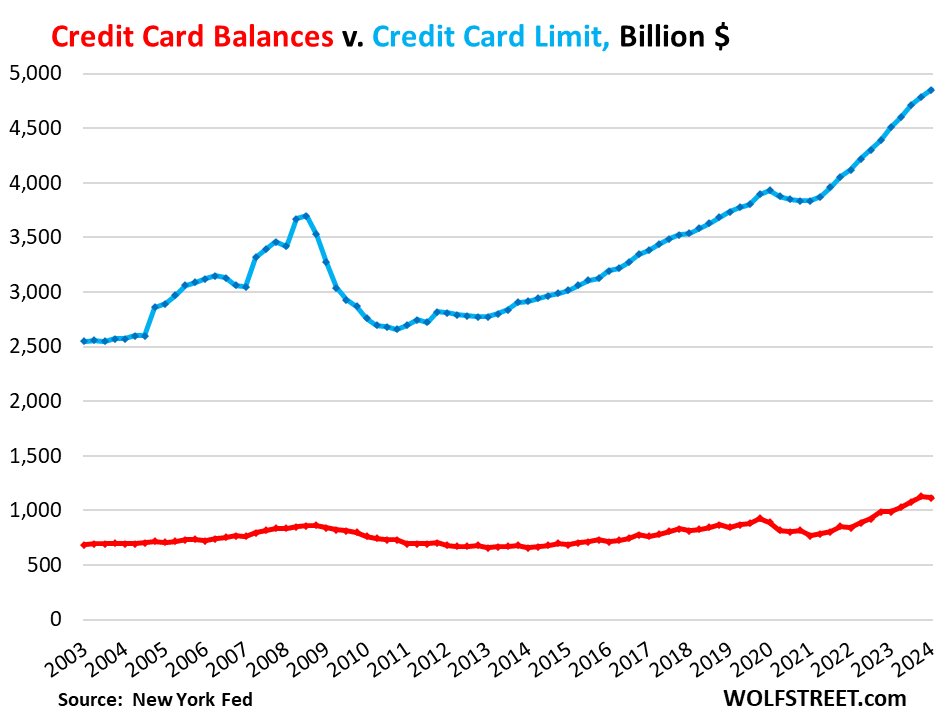

Overall credit availability rose.

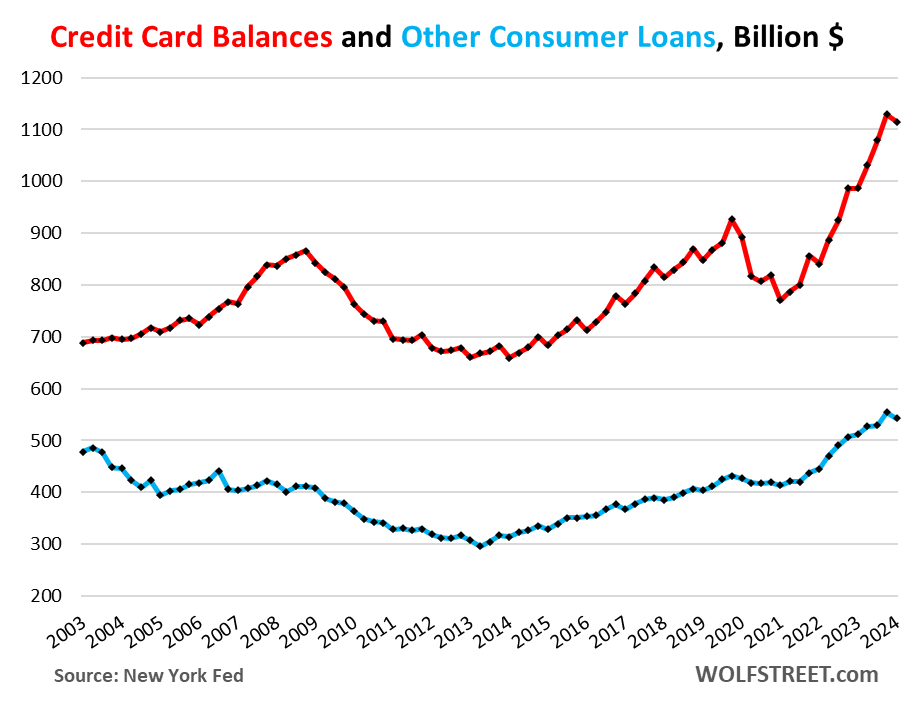

Banks are still trying to get people to open new card accounts, and they have raised credit limits for many card holders, and so the total credit limit surged 9% year-over-year in Q1 to $4.85 trillion (blue line in the chart below).

Credit card balances ticked down to $1.11 trillion (red line). So total available unused credit rose to a record $3.74 trillion:

This sheds some light on the overall delinquency rate.

Earlier this week, we discussed overall consumer debt, delinquencies, third-party collections, and bankruptcies, which remained low; and housing-related debts, delinquency rates, and foreclosures, which remained very low. So here is the part that’s not so low anymore.

Cardholders who’ve maxed out their credit cards in the prior quarter are much more likely to become delinquent in the current quarter than the rest of the bunch.

Only about 18% of credit cardholders are maxed out, so this is a relatively small portion of consumers – given that many consumers don’t even have credit cards, but use debit cards – but they’re falling behind at a higher rate than before the pandemic, and they leave their imprint on the overall delinquency rate.

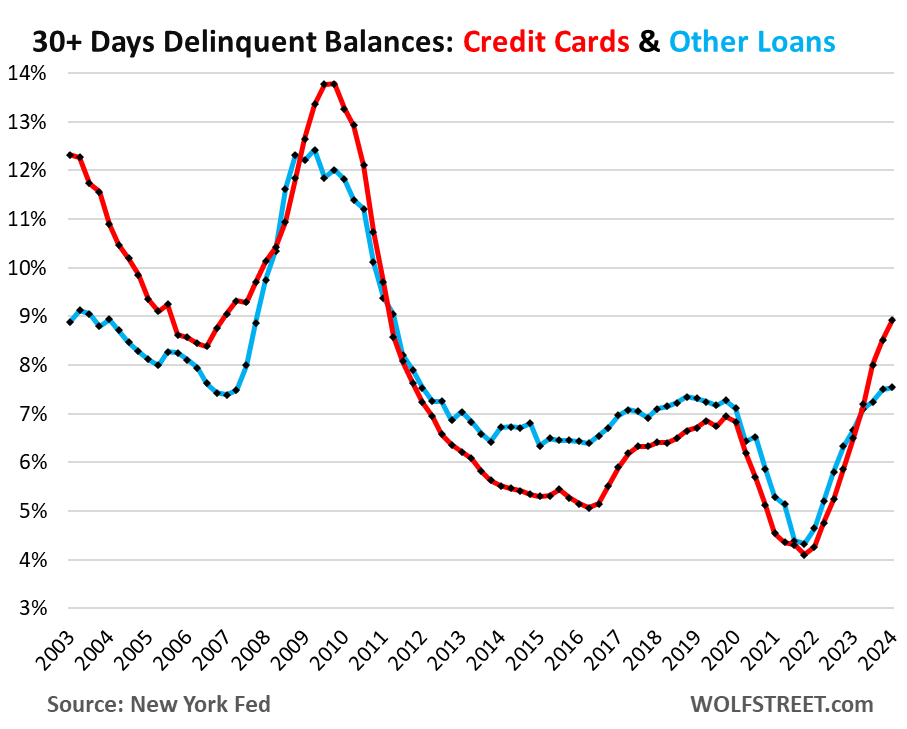

Credit card balances that were 30 days or more past due rose to 8.9% in Q1. In 2019, the rate was about 7.0%. Before the Great Recession, it was between 8.5% and 12% (red line).

“Other” consumer credit balances – personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, etc. – that were 30 days or more past due inched up to 7.6%, a tad above where it was in 2018 and 2019 (blue).

Credit card balances dipped in Q1.

Credit cards are the dominant payments method for consumers, having largely replaced checks and cash. They’re used to pay for anything, from bar tabs to expensive business trips that get reimbursed. Many small business owners use credit cards as payment method for business purchases. Credit cards were used for over $6 trillion in transactions in 2023. And very little of it got stuck as interest-bearing debt; most of it was paid off by due date with no interest due. They are primarily a measure of purchases, not of interest-bearing debt.

Consumers are incentivized to pay with their credit cards through loyalty programs, such as 1.5% cash back or frequent flyer miles, and they do that and pay off their statement balances every month, and relish with the freebees. Banks can offer those rewards and still make money because they collect a fee, such as 3% of the purchase amount, each time a cardholder uses the credit card. Merchants pay for it all.

So credit card balances – monthly statement balances before payments are made – dipped by $14 billion, or by 1.2%, in Q1 from Q4, to $1.11 trillion, according to the New York Fed’s Household Debt and Credit report. A dip is normal in Q1 after the holiday spending and travel boom.

Year-over-year, credit card balances rose 13.1%, as prices rose, and more accounts were opened as more people had jobs, and as consumers spent more (red line in the chart below).

“Other” consumer loans (blue line), such as personal loans, payday loans, and BNPL loans, fell by $11 billion, or by 2.0%, in Q1 from Q4, to $543 billion. Year-over-year, “other” loans rose by 6.1%.

Everything has grown — faster than credit-card balances.

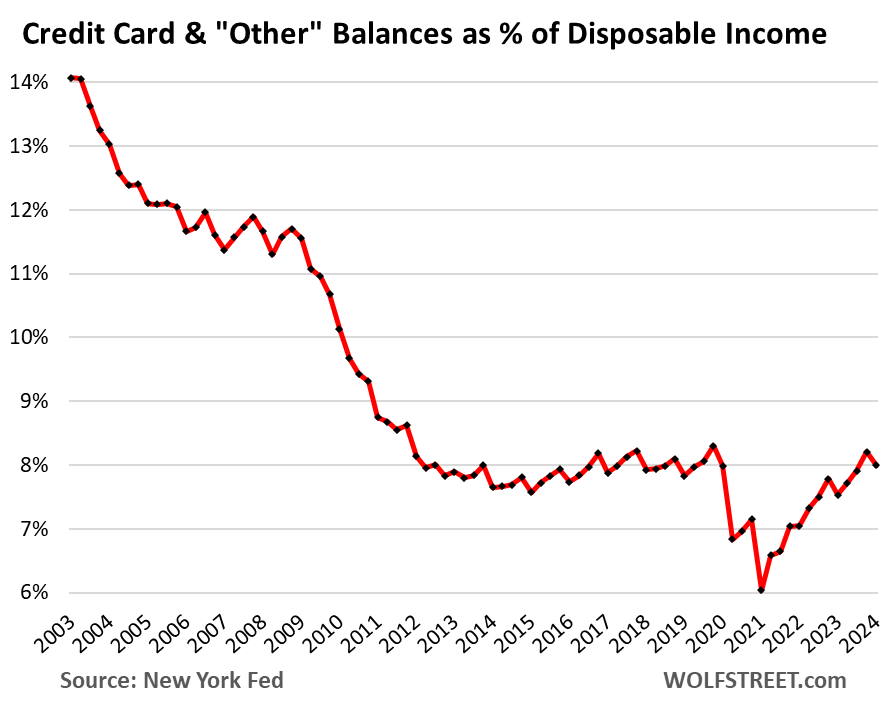

Credit card balances need to be seen in light of the US population that has surged over the years, and of incomes that have surged, and of the number of workers that has surged.

One of the ways to track the burden of these balances is to compare them to disposable income, which is income of the total population from wages, interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc., minus taxes and social insurance payments; but it does not include capital gains.

Disposable income has surged with the growth in wages, employment, rental income, interest and dividend income, etc. (data from the Bureau of Economic Analysis):

- Quarter over quarter: +1.1%

- Year-over-year: +4.3%

- Since 2019: +26.7%.

The burden of the balances of credit cards and “other” consumer debt combined ($1.66 trillion) dipped to 8.0% of disposable income. Two decades ago, that ratio was 14%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I got $200-$250 cashback on 7-8 different cards in the 1st month. That’s approx 300% annualized return on $1K spend. They probably have Harvard graduates working in those companies.

Harvard graduates call it “customer acquisition costs.”

Agree. Outside of Harvard they call it cheese in a mousetrap is always free.

.. to the second mouse.

It is always free to the second mouse!

Quicksilver acquired me by doubling their 1.5% cash back to 3% for a year, then lost me when the promotion ended.

Fickleness is a virtue in the economic realm.

I just keep wracking up the reward points

maxxed out my cc last month – had to make payment mid month

of course I’m deadbeat per cc companies

interest paid since mid 90’s – $000,000.00

—

I keep spending like drunken sailor

roof here, insulation there, 100 sheets drywall next week

painted exterior 2 houses in 2 weeks – $700 paint each

on and on it goes

no I’m not contractor

Only DIS agree mint with this report: ”Merchants pay for it all.”

Fact IS, certainly and certifiably: Consumers PAY for the convenience, far damn shore.

Another fact: Many retail establishments these days offer CASH discounts, and right up front.

WE, in this case the family WE, use them whenever WE see them.

”Back in the day”,,, running full speed around the SF Bay Area, I had a couple thousand$$ in my pocket and took every CASH discount::: however, in those days, I could run a lot faster,,,LOL

I always ask about cash discounts, but am told no surprisingy often.

$5k hot water heater install… no discount for cash, so might as well put it on the CC and get cashback.

You really have 8 or more credit cards??????

Lmao. Yes they do have harvard grads working these things and it’s working. You’re the waaayyyy outlier

Andy is a mouse, treading on the wheel of life. He’s a troll. The best credit card deals are history right now.

Soon a chip in the mouses paw will give it the ability to travel and purchase with out having a credit card. Just put the paw out to be

scanned and receive your cheese.

The children of tomorrow might never see a paper dollar or a credit card

Ok, Karen.

NOT true OW:

Currently receiving CC ”deals” as good as OR better than any, at least better than the last decade or so..

Likely depends of your current credit reports, eh?

I easily have 8 different credit cards.

If I’m making a big purchase (e.g., Christmas gifts and a new Barbour coat at Orvis), if I can get 25% off by opening a card and paying it off in 30 days – sure.

I’m a frequent United Airlines traveler and they gave me a Club Card on promo, waiving the first year fee, 50,000 miles, and a bunch of United PQP (used to calculate status).

I can go down the list, but I’ll play this game all day. ;-)

Not sure exactly how you’re using your cards, but supposedly opening up numerous credit cards, then closing them down, can result in a big hit to your FICO. Some sort of algorithm they use doesn’t care for people being that wily.

I get 0% interes for 18 months plus $200 bonus. I run up the card paying utilities, gas, and groceries. I put my cash in a MMF getting 5.25% plus 3-5% cash back. That’s my arbitrage. When the promo period is over, I pay off the entire balance and pocket the interest at 8-10%.

Interesting data as usual, but can you delineate credit used, available, delinquencies, etc, between different income tranches? For example, the debt as % of disposable income has dropped overall, but I suspect that this is a result of the quite large top-end income growth rather than the growth of each of the segments of the whole CC population combined. Also, are you able to track & chart the cost and subsequent support of those at or near max charge limits paying 25 – 29% interest rates and the margins made from those cardholders to offset the Rewards plans that can range to 5, 7, or 9% of purchases that receive the benefits from the CC companies margins from those high-balance card holders? The short of it is that the high balance/high-interest rate financially enslaved people in low-end finance support the high-benefit Rewards plans for the high-use zero or low-carried balance high-earning consumers at the top end.

Thouhts?

Same BS narrative over and over again. Also RTGDFA.

Low-income people and people with bad credit often have trouble getting a credit card at all. And if they get one, it has a low credit limit, see table below. This concept — low income people cannot have much if any debt, high-income people do — is something you have to wrap your brain around.

1. The lowest-paid jobs got the biggest pay raises over the past three years (due to the labor shortages in those jobs). That has been well documented.

2. The young dentist with big income is a classic example of a high-income person with maxed out credit falling behind on payments because the fancy cars and fancy house, plus the big student loan debt, and the debt from the new practice, are straining the finances. There are a lot of younger people like that – it’s part of the learning process – and they skew the balances upward.

3. Business people and small businesses use credit cards ALL THE TIME for all kinds of expenses. A business trip involving business-class flights and fancy hotels can rack up thousands of dollars in no time, but gets paid off by statement date. RTGDFA. I explained this. This is a huge factor.

4. Credit card balances are statement balances. Most of them are paid off by due date. RTGDFA. I explained this.

5. Low-income people often do not even have credit cards. And if they have one, it will have a low credit limit, and they cannot borrow much. See table below.

6. Only about 169 million people have credit cards. The remainder of the 333 million people don’t.

7. Here is the data by income level, from the New York Fed, which did the study of the maxed-out. Income categories are by zip codes, low-income zip codes to high-income zip codes.

As you can see, the maxed-out credit cards go across all income categories. Note that the lower-income cardholders have much LOWER credit limits, and are therefore maxed out at much lower levels than high-income folks. The high-income earners have a median credit limit of $25,800 and 5.5% of them are maxed out on that! While the low-income earners have median credit limits of $11,300. It’s a lot easier to get maxed out on $11,300 than on $25,800.

I’ll just give you a theoretical example for illustration purposes:

Person A makes $1 million a year, and after taxes has $800K in income (people with that income know how to shelter it). They can very comfortably have $4 million in debt (4x gross income), such as a mortgage, pay $350,000 a year in mortgage payments on that debt, and have $450K left over to spend on food, clothes, insurance, gasoline, etc. and save $200K a year.

Person B makes $25K a year. After payroll taxes, they have $23K left over, which is hard to live on in the US, even without debt payments. A debt of 4x gross income (= only $100K) would be very difficult to support. If this is a mortgage, annual payments would be $5.5K, which would leave $17.5K to live on. If this $100k is credit card debt, the interest alone would be $30k a year, on a $23K gross income. So unless there is fraud involved, this isn’t going to happen.

Do you see why it’s NOT the low-income people that drive up the debt levels — because they cannot borrow a lot. But the higher-income people can drive up debt levels in a big way because they can and often do borrow huge amounts. And some of them will get in trouble and will have to work their way through it.

Also, someone with $1 million in annual income likely spends a lot of money on all kinds of goods and services, and pays for them with their credit cards, and most often pays them off by due date, but the statement balances are huge. People like that can easily put $20k or $30k a month in reimbursed travel expenses and other non-reimbursed expenses on their cards, no problem. And THAT runs up total card balances though it gets paid off every month and doesn’t generated interest bearing debts.

These were just examples for illustration purposes.

On Reddit there’s a person who “churns” a 1000 accounts.

I’m just happy with my rewards.

Once you start investing you see everything as interest rate. And how much is going into your pocket. Avoid any interest rates leaving your pocket, at all costs!

We’re out here on the front lines earning 5%, kneeling, crawling and scraping for that 5!

And people are in Atlanta signing up for modern furniture and paying 20-30% interest on it per year. That’s 4-6 times what I’m in a dogfight for! And they’re losing that much. Craziness!

Wolf,

How does Buy Now Pay Later fit into this dynamic?

Do you think the picture might be worse if we factor those customers in (assuming it is easy to do that given that we don’t get an available credit ratio for BNPL)?

Two ancecdoes about BNPL from my corner of the internet:

1) orders paid with Affirm (our BNPL provider) are a tiny % of total orders

2) orders paid by Affirm are usually for high-dollar items

I recently had a customer buy something using Affirm at checkout, and then re-order the same thing on his credit card bc he wasn’t sure the Affirm payment went thru.

These customers using Affirm are not distressed, they’re just taking advantage of a different way to pay.

Makes sense. How much (approximately) does Affirm charge retailers for the service? Or is it fully funded by the purchaser?

TulipMania,

BNPL is included in “Other consumer loans,” blue line in the second chart from the bottom, as I pointed out in the article.

My understanding is that they take the cut a credit card processor would have taken (~3%), don’t give rewards to anybody, and then collect payment with no interest over ~4 months. If any payments are late, they charge big penalties to the borrowers.

It’s unclear whether the particular pricing is sustainable. I think they’re in VC-backed predatory pricing mode to build marketshare. It’s possible they will start charging a small interest rate on the payments in the future.

Ah you found me out. I don’t need to buy now pay later, but when someone is willing to give me a 1 to 3 month loan for free on a big dollar amount item of course I’m going to take it to smooth out my cash flow month to month. That way I can still partially meet my savings and investing goals but get the items I want now. The real trap is whether people keep piling these on month to month and eat all their free cash.

I just did this with some furniture. Tbh I think they’re great products for those financially responsible.

Bingo – I do this all the time. If I can get zero percent for a period and use it to keep cash in the bank on a big purchase, I’m on board.

I used to use Paypal’s pay in four option. But then I realized its a better deal to put it on my CC and get the cashback. Based on my card’s autopay schedule, I’m only paying a little sooner vs a BNPL plan.

“The burden of the balances of credit cards and “other” consumer debt combined ($1.66 trillion) dipped to 8.0% of disposable income. Two decades ago, that ratio was 14%”

This is quite remarkable actually. Gotta be mostly wage increases right? Would love to see that broken out.

Since 2019: 7 million MORE jobs + wage increases per job + 5.5% interest on $10 trillion in CDs, savings accounts, T-bills, money market funds, etc. compared to 0% before + rental income (red-hot rent increases) + small-business income, etc. etc.

Over the past two decades, employment has soared by 28 million jobs, or by 21%, plus average weekly wages jumped by 80%, etc.

All nominal figures: debt, earnings, etc. apples to apples.

Thanks once again for your very good reporting Wolf:

This mirrors what we are seeing currently in our little bit of heaven here in the Saintly Part, AKA Saint Petersburg.

”Handy Persons” formerly readily available for approx. $20-25, now at least double…

But, you express it SO much better!!!

“Credit card balances need to be seen in light of the US population that has surged over the years, and of incomes that have surged, and of the number of workers that has surged.”

Another potential factor: the culture of putting everything on a credit card.

Used to be you paid cash at the vending machine and wrote a check to the contractor. I recently paid both with my credit card.

Credit cards have become the universal payments device. Debits cards are second. Combined they were used for about $11 trillion in purchases in the US in 2023. They’re super-convenient, for both the merchant and the buyer. And a lot of stuff gets bought online, from plane tickets to furniture, and you cannot use cash or checks online.

Howdy Lone Wolf YEP, great way to make some free cash on the things you need. I needed a motorcycle and they let me charge it to a credit card. At the time 5% back to me…. I waved to you the other day.

I smiled back.

Let us know about the 5% cash back card (my go to credit card is a Fidelity card with unlimited 2% cash back).

I use my debit card when the vendor charges an extra fee for the credit card. I am surprised most small business vendors don’t do this. CC fees to the vendors must be enormous.

Of course, they factor it into the price.

My oral surgeon just made the change from allowing credit cards with no fees charged to me having to use cash, a check, or a debit card. But on the other hand, a plumbing contractor here let me charge 18K on a 2 percent card with no fees. Same way with property taxes. Some counties allow credit cards with no fees and some charge fees.

“I am surprised most small business vendors don’t do this.”

Because customers will piss and moan about the “surcharge” and then buy it from Amazon instead.

The massive “forgiveness” of student loans (and put on the Federal deficit) is not affecting this?

No one has been paying down student loans anyway. It has been that way for years. That’s a constant.

My son is a psychiatric resident in Boston. Has two more years of residency and about $95k in student loans from his time at med school. It is apparently customary nowadays to make the absolute minimum payment on your student loan and have your first real employer pay off your student loan in its entirety on a multi-year employment contract. Apparently this is for MDs only. Us old comp sci majors paid it off the hard way.

If your son has only 95k in debt after four years in medical school, he had quite a lot of help with that from one source or another. The average is much higher, several hundred thousand, due to the outrageous cost of medical education. Also you expose your ignorance on the topic with your comment that it’s somehow bad to be financially compensated for choosing 10 years public service instead of private practice. These jobs are usually long hours and high acuity, helping the hordes of medicaid patients with no resources and being paid far less to do so. Loan repayment exists to level the field so doctors take these jobs. This is the broken system America votes to keep around rather than fixing things with regulation.

I just read that USC, Brown, Dartmouth and a bunch of other schools estimate that it will cost over $90K for ONE (1) year of an undergrad degree…

I had no idea how expensive education had truly gotten until I looked into going back to college. If it’s a university or anything other than a community college, there isn’t a program locally that is less than 15k a year tuition alone.

Most of the 4 year schools have programs ranging from 20k/yr to 60k/yr.

The total tuition cost for a k-12 teacher program was like 80k dollars. For a job that is paying 50k a year if you’re lucky.

It’s nothing like medical school or Ivy League schools but I see a future where either the govt subsidizes higher education and step in to regulate the grifting by the colleges or these colleges fail under their own greed.

I work with a guy whose wife went to Whitworth university out over in Spokane and she is in debt about 230k dollars for a business degree. I doubt she’ll ever claw her way out of that debt. But according to her husband, “the winds of change are upon us, all student loans will be wiped away dude.”

And the bad part is, they might be right. They’ll commit financial suicide and get bailed out and be ahead a free college degree while the working stiffs fall off a ladder and end up homeless because they don’t have workers comp and are forced to work on a 1099 as a company employee. Welfare for the snooty yuppies while the actual poor get kicked in the head day after day.

Good. He needs to clean up the damage the internet has done. Buy him lots of coffee.

It seems like they are a very complicated transfer payment, settled out over long time periods — a $1 trillion injection of cash into the system that appeared as loans orderly loans, and disappeared in indistinct forgiveness. Subterfuge.

Do these non-repayed student loans get picked up as part of disposable income, somehow?

Wolf,

“Many consumers don’t have credit cards at all”?

Google search,

82% of US adults have credit cards, about 190 million.

92% have debit cards, about 242 million.

So the maxed out 18% = 34 million Americans.?

The delinquency rate is much lower than the 32 million, but higher than before the pandemic, a bit odd?

Yeah, I didn’t buy that sentence either. Pretty much anyone who can get a credit card gets one save for maybe the youngest adults and some of the oldest. I didn’t get my first credit card until 25, and now 25+ years later just got my second because sometimes my primary gets used by thieves somehow and I wanted a backup when traveling. Since I applied and got the second I must get 3 offers a week for other cards. Thankfully it’s all electronic so the offers aren’t using up a rainforest every few months.

Home toad,

1. “82% of US adults have credit cards, about 190 million.”

Only 166 million consumers have credit cards at all, according to consumer credit reporting agency TransUnion (Feb 2023 report). So that’s only about 64% of the 260 million adults (18 and over) in the US.

18% of 166 million = 29.9 million.

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

2. In terms of the delinquency rates, read those sections again. I think you’re mixing two things together: The share of the “non-delinquent maxed-out” (=9%) is still lower than before the pandemic (ca 10%) — see first chart. But the delinquency rate of the maxed-out is higher than it was before.

“18% of credit cardholders are maxed out, so this is a relatively small portion of consumer”

1 out of every 5 credit card users have thier credit cards near-to-maxed and it’s getting worse.

Sorry, I do not see that as relatively small portion of consumers and truthfully this might not be the worst of it yet.

Personally I believe we are beginning to see the fallout of the credit score bump during Covid.

no, no, no… 18% of credit card holders is NOT 18% of consumers since lots of consumers don’t have credit cards — see the comment about that. Only 166 million have credit cards, so 18% of that is 29.9 million, which is about 9% of the 333,000 Americans. This is a big country!!!

My statement was “1 out of every 5 credit card users”

But since we are stuck at talking about consumers … you can not consider the entire population, only adults which is roughly at 260 million.

That puts the the number at 11.5%. Put 9 adults into a room, one of them has credit cards near-to-maxed. That is not okay.

The way the numbers show, the acceleration in percentage, and current interest rates no one should be okay or comfortable with what is transpiring.

Only difference from 2008 is that instead of giving credit to those with sub-prime and lower credit scores, people scores were raised to allow lending to them under the guidelines after 2008.

Banksters are going to bankster and with the current economy only a matter of time before its 2008 all over again.

Thanks.

For some reason Karl Malden keeps appearing in my brain.

He was Serbian, his birth name was: Mladen Djordje Sekulovic.

“Don’t leave home without it” American express, payed Karl for 20 years to do their commercials.

Let’s get that 18% to double or triple and then see what kind of crazy Congressional relief is passed.

I would not be surprised to see Congress tell credit card companies that they must reduce debt outside of bankruptcy or force them to lower interest rates.

Congress, just like the Fed, is getting really good at mucking with financial markets and eliminating consequences.

And China just announced a plan to encourage local governments to buy up properties and to help get them completed. I could easily see Congress doing something similar with tons of deficit spending to buy up CRE and convert it to residential housing, whenever possible.

Who the copulation doesn’t use cash back cards?

-Buy $100 dollars of crack. Only costs $97

-Hire a $500 ho. Only costs $485.

-Give $1000 to the Church. Only costs you $970.

Thems some savins!!

“ The 11% of cardholders who used 20% to 60% of their available credit have transitioned into delinquency at a higher rate than before the pandemic (brown line, third lowest line).”

I think this should be 60-90%. Great article, as always.

I found this paragraph the most interesting from today’s post.

“But only 18% of credit cardholders are “maxed out.” Not 18% of consumers, but 18% of credit-card users – big difference because many consumers don’t have credit cards at all, but use debit cards.”

How can you calculate how many consumers there are and what is the definition of a consumer.

Apologize for being naive.

My guess is some are consumers by proxy, like kids going to college or living at home and not working, or simply stay at home parents. They still consume but could be getting the money for goods and services via other ways which is normal.

Doc

Consumers = people living in America = 333 million; their primary job is to “consume” = buy goods and services so that the economy can move forward.

Credit card holders = 166 million; they’re a subset of consumers, they’re better equipped to do their primary job (consume) than the rest.

Maxed-out credit card holders = 18% of 166 million = 29.9 million (maybe); they have done an excellent job consuming, have done it to the best of their abilities, much better than the rest, and now they should get an award, but instead they get looked down upon. There is no justice in this world.

Partial sarc only

Wolf – kudos, kudos, kudos, and thanks! (Among the best of your many-excellent observations/turns of phrase…).

may we all find a better day.

Thanks Wolf for the clarity. I watch a lot of Youtubers and even the ones that are usually pretty level headed fall in the error of just reading the headline information on CC usage and debt. You’re the only one that I have found that actually interprets the data with a level head.

A lot of YouTubers who specialize in equity love to preach the doom and gloom! “Get into crypto before April 9th!”

YouTube is a cess pool of manufactured BS. There’s some good info, it’s just you need a metal detector and rubber gloves to locate it.

That last chart, “Credit card and other balances as a % of disposable income” along with historically low unemployment rates tells me the country is in pretty good shape. I guess I can sell my survivalist bug-out kit: a condo in Portugal.

I see frequent comments about student loans not being paid off/no one is adhering to their monthly payments. My wife and I have grinded her original 220k balance down to 10k and will pay it off in totality in the next few months. At 6% interest that balance would be exploding if we just refused to make payments. Find it hard to believe the new strategy is defaulting on your loans without giving a damn.

All student loans would be forgiven under some executive action like Biden Admin has been doing circumventing Court ruling by finding some loopholes.

I have a friend whose loan of $60K has been waived off.

I believe in paying back loans but people who acted responsibly and paid off their student loans are being fooled.

All the “savings” from the loans just gets spent revving up the American economy.

It was all interest on bad rates anyhow.

Educations should be free.

Incentives must be messed up when being a defaulter makes so much “sense.” Every debt in my life has been paid off to the dime, soon to include the remaining home loan debt which is .2% of my assets.

According to the fed 82% of the US adult pop has a credit card. Not sure if this is correct but 18% of that seems to be a big number.

Wolf am I all wet. Not the first time.

Only 166 million consumers have credit cards at all, according to consumer credit reporting agency TransUnion (Feb 2023 report). So that’s only about 64% of the 260 million adults (18 and over) in the US.

18% of 166 million = 29.9 million = 11.5% of adults.

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

Also note that they’re just maxed out on their credit cards. Only a portion of them also missed a payment. The rest are current and are making payments as agreed.

Thanks!

CIBC Visa joke but real story.

I look after the affairs of an old friend now in a care home. We kept his Visa card in my dresser for a just in case he needs something urgent…a wheelchair, emergency dental work, etc. One month I noticed a $20 dollar charge on the card. Visa’s own bill for insurance coverage for hacked cards, and it took threats to elicit the info. It was an internal charge on his card. Phoned Visa again and got the royal runaround, canceled the card at the bank only to hear from Visa the bank did not have the authority to cancel on my POA. So I then had to get the old guy to phone Visa, (obviously I phoned) from the care home and I answered all their questions etc etc and finally got a frigging cancellation. But the $20 bill kept coming. Every month. So I made a few more angry calls and they waived a portion of the bill. Now, we owe $9.00 and change and they have been religiously sending us a monthly mailed statement for the last 18 months requesting the $9.00. All this on a canceled card!!!! I once sent them Canadian Tire money (points stuff) for a joke. The monthly late fee for the delinquent account is $.06…..yes, 6 cents. It comes by snail mail. I figure the Visa computer system coughs this bill out for what? $3-4 bucks for the envelope, snail mail postage, processing, data retention, etc etc.

Thinking on sending a piece of dog shit back to them in the envelope and hopefully it will ‘gum’ up the sorting/reading works.

This is who is managing your credit card. We even get threats about future credit, for a guy in a care home with dementia…the past owner of a canceled card.

And some people have 8 cards? Really? I have a Mastercard and use it just for gas and some online. If you seldom use a card you will never be in debt. Hell, they kept raising my limit, every year. When it hit $20,000 I had to almost threaten to get them to lower it to $10,000. Use cash and debit for 99% of purchases. Works for me.

Some of us use only what is needful in the world. Others will take and burn everything with no limit. Modern mainstream economics model a human as the latter type. A perfect world is one with no frictions on one’s unlimited desires. That’s why the planet’s most beautiful systems are deteriorating.

“If you seldom use a card you will never be in debt.”

Another way to solve this problem is setting your account to autopay the full statement balance on its due date. This is what I do and I’ve never paid a dime of credit card interest in my life.

The data doesn’t look that bad at the moment compared to historical figures. It will be interesting to see where we are in 6 months and if this steep upward trend will continue.

My 2 CCs have horrible interest rates but haven’t paid them a penny in 6 or 7 years. Used as a convenient payment now, they are paid off long before any exposure to interest charges.

I get daily,…yes daily.. reminders from one of the big 3 credit reporting agencies claiming I should finance my last credit card balance with a loan. The balance they have is 3 months old and was paid off before due as has every CC balance I’ve had. Are these reporting agencies just hucksters trying to sell more credit cards and loans for the banks? What a joke.

Imposter,

We do the same thing.

Which credit card we use depends on what we buy because they have different cash back amounts for different products.

And, like you, we pay off the full amount every month.

Also, we get ‘reminders’ on how we should finance our balances. But at least they are not daily. :-)

The rise in available credit, and credit balances, speaks volumes about where the money is coming from to keep the economy going.

It is anyone’s guess when the music will stop, but most of the chairs have already been removed from the field….

Had to make it to the bottom of the comments to find it, but yes, looks to me like a credit expansion. People are putting it on the credit cards, and they’re starting to max out. It’s going to be an interesting next 6 months of retail sales data.

How do we know how many people actually do not have a credit card? If any thing else, I would think most people would at least have a credit card in case of an emergency. The percentage of people without a credit can’t be very high.

Sorry Wolf. I found the answer in your comment section.

I always use credit card for all of my purchases unless there is a incentive to use cash/debit card by the merchant.

I also rake in couple of grand per year as cashback for using cc.

I had a friend that traveled a lot for his work so he had about 4 credit cards right before HB1. He basically was a contract worker who lived at the location his contract was located so he would stay in hotels for months and the expense the bill.

Well the credit card companies kept raising his limits even though he did ask them. The limits for all the credit card eventually reached about $50k each even though he paid the balance off monthly and rarely went over $5k.

When 2009 crash hit, the credit card companies dropped his available credit over 50% down to 25k or lower. He basically lost 120k of available credit.

What was the outcome. His FICO score when from over 800 to low 700s on no missed payments. It dropped because the ratio of available credit dropped 50%

Discover has done that with my lone credit card. Started out as a secured credit card. After 6 months I think; boom it’s now doubled its credit limit. Another 6 months it doubled again. Which was nice because I was paying it off weekly as the limit was only like 1k dollars. They did this every six months until the available limit was around 6k dollars. The I called and told them to stop increasing it. Several months later it was rounded up to 10k.

Never have paid a penny in interest. I’m sure they want me to go into debt and start clawing back all that cash back I’ve made over the years. I’ll go to my credit union and get a personal loan with an interest rate below 30% though. Meanwhile, my debit card still has a faded activation sticker on it. Don’t even know if I have ever used it. Not even sure if it’s activated.

Yes, FICO scores are a bizarre mess. The pandemic effects boosted/inflated lower FICO scores.

I know this is anecdotal but two mom’s and pops restaurants I frequent have kept menu prices the same this year and now impose a 3% fee to use a credit card. I’m wondering how it will go over with customers and I keep more cash in my wallet to see if it happens more frequently.

In my little slice of flyover, all my mom & pop restaurants charge a credit

card fee. Heck this mom & pop business has not accepted credit cards for 32+ yrs.

The ones that are maxing out their credit cards and are unable to pay are mostly the working poor. Sure, you have some that just spend out of control, gambling addiction or whatever, but those are the minority.

That’s BS that you just made that up because it fits your narrative. Here is the data by income level, from the New York Fed, which did the study of the maxed-out. As you can see, the maxed-out credit cards go across all income categories. Note that the lower-income cardholders have much LOWER credit limits, and are therefore maxed out at much lower levels than high-income folks. The high-income earners have a median credit limit of $25,800 and 5.5% of them are maxed out on that! While the low-income earners have median credit limits of $11,300. It’s a lot easier to get maxed out on $11,300 than on $25,800.

1) “But only 18% of credit cardholders are “maxed out.” Not 18% of consumers, but 18% of credit-card users – big difference because many consumers don’t have credit cards at all, but use debit cards.”

So only credit card holders can be counted when talking about being maxed out. OK. I get it.

2) “Credit card balances need to be seen in light of the US population that has surged over the years, and of incomes that have surged, and of the number of workers that has surged.”

When looking at credit card balances, point one got discarded? Now you lost me. When someone doesn’t have a CC, why count him into the equasion?

To your #1: “So only credit card holders can be counted when talking about being maxed out.”

Correct. You cannot be maxed out on a credit card if you don’t have a credit card. In the US, 169.9 million people use a credit card as of Q4 2023. The rest of the 333 million don’t, and they cannot be maxed out on a credit card because they don’t have one (many of them have debit cards).

To your #2: the number of credit card user has increased over the years. That figure of 169.9 million credit-card holders in Q4 is much higher than it was in prior years. For example, in Q4 2020, it was 159.5 million credit-card holders. So credit card balances get spread out over many more credit card users.

Thanks for taking the time to explain things.

But it still doesn’t feel well to me to smear out the CC balances over the whole population, including those that don’t have a CC. The latter group having no part in those balances.

Look, this site is about the economy, not social studies or psychology. If you want to lament why some people get in over their heads with credit cards — it’s part of the learning process, they’ll eventually figure it out — and feel bad for them or whatever, well, OK, that’s great, but that’s not place here.

I’m just over here paying a little extra on my mortgage every month, not adding any new debts, and stashing savings and investments away, all while seeing how I can keep cutting costs. Interesting to see the results of people increasing their spending as fast as they increase their income, or faster… Credit cards are a useful tool, if you don’t carry a balance. Ultimately people will reap what they sow, all behaviors and actions compound.

Lately I am seeing more businesses asking for checks or will charge 3 percent extra on the bill.

Oe advantge of brick & mortar over retail.

Checks also aren’t subject to chargebacks.

E-commerce* retail.

Credit card balances that were 30 days or more past due rose to 8.9%… when you look at the chart, it appears that these delinquencies have been shooting up hard for nearly 24 months without any levelling off. So presumably the number will shoot above 10% and may go higher yet, into a range only seen during the GFC.