Suddenly lots of talk the 10-year yield will revisit 5%, which is funny just a few months after Rate-Cut Mania.

By Wolf Richter for WOLF STREET.

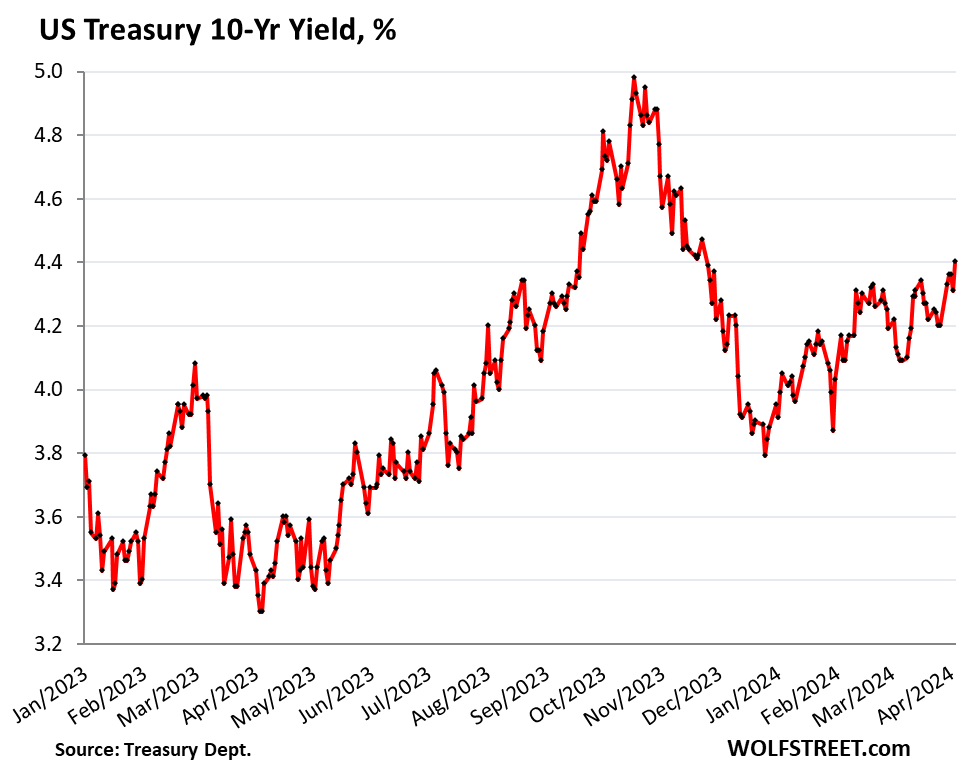

The 10-year Treasury yield rose to 4.40% on Friday, the highest since November 27. During rate-cut mania in December, the yield had dropped below 3.80%.

Those moves in recent days and weeks added up, and they point to a gradual recognition in the bond market that inflation rates will be higher than what they’d been before the pandemic, that 2% inflation isn’t going to happen, and that the super-low interest-rate environment over the past 15 years – culminating in August 2020 when the 10-year yield was down to 0.5% – is over.

What comes next is unknown, but it’ll likely entail higher inflation of the type seen in the 1990s and before because the Fed isn’t willing to crash the economy and the labor market just to get to 2% inflation.

That means the Fed will keep its policy rates fairly high – high enough to not let inflation spiral out of control, but not so high as to crash the economy and bring inflation down to 2% – and yields will be higher too to compensate for the higher inflation, everything will be higher, like it used to be, and the bond market is adjusting to that scenario.

Now there’s suddenly lots of talk that the 10-year yield will revisit 5%, where it had briefly been in October, because inflation will be higher for longer, or forever, which is funny after Rate-Cut Mania, and the yield would have to compensate for inflation over the 10-year period, plus some.

Obviously, “forever” here doesn’t mean forever in the cosmic sense, but in the bond sense, meaning beyond the maturity date of the bond.

It’s interesting how the narrative in the market changed so quickly. From November into mid-January, there was the Rate-Cut Mania, with the market for federal funds futures seeing very high probabilities of five and six rate cuts and even seven rate cuts in 2024, spread over the eight Fed meetings.

And then the Fed started pushing back. It came out with a doozie of a push-back FOMC statement after its January meeting, and repeated it at its March meeting. And we had two awful inflation readings in January and February, on top of the upward trend of the underlying metrics that started last fall.

The “dot plot” from the March FOMC meeting showed that the 19 participants were nearly evenly split, with 9 seeing two rate cuts in 2024, and 9 seeing three rate cuts, and 1 seeing four cuts, leaving the median at three cuts. But if only one of the three-cutters becomes a two-cutter by the June dot plot, then a two-cuts scenario comes out of that meeting. This March “dot plot” was a warning sign that those three rate cuts may vanish.

Since then, lots of Fed officials gave speeches, fretting about the path of inflation, and walking back their own rate-cut expectations.

Yesterday, Minneapolis Fed President Kashkari said the quiet part out loud: Maybe there won’t be any rate cuts in 2024 if inflation keeps going “sideways.”

Today Fed governor Bowman came out and said out loud: “While it is not my baseline outlook, I continue to see the risk that at a future meeting we may need to increase the policy rate further should progress on inflation stall or even reverse.”

They’re talking about short-term policy rates, not longer-term yields. And they’re fretting that something big has changed in the economy: That even the 5.25% to 5.5% short-term policy rates, that were supposed to be “restrictive” and that were widely expected to throw the economy into a recession, have not been restrictive and have not slowed the economy.

On the contrary, economic growth and the labor market accelerated in 2023, and the labor market has maintained its rapid growth so far in 2024, creating jobs at a rate of 3.3 million a year in the first quarter, which is hot, and hotter than it was in 2023. And financial conditions have eased, and markets are in la-la-land.

And so folks are wondering what kind of policy rate would actually be “restrictive” if 5.5% at the current inflation rates is not restrictive. If inflation on a three-month basis and six-month basis is 4% or 5%, where would policy rates have to be to be restrictive?

The three-month core CPI accelerated to 4.2% annualized, the highest since May 2023, and the three-month core services CPI accelerated to 5.6%.

Policy rates are 5.25% to 5.50%. They need to be higher than inflation rates to be restrictive; there is widespread agreement on that. Just how much higher is uncertain.

There are a lot of inflation measures in the US. But if we use the three-month measure of core CPI, which was 4.2% in February, neutral policy rates might be 6.0%, and anything below would still be stimulative.

Obviously, everyone is just guessing. Inflation has come down a lot, but now it’s heading higher again. The path of inflation is very uncertain, as we have seen. It could turn around and go down again, but that seems unlikely now. Inflation frequently dishes out head-fakes.

The economy and the labor market have been growing at an above-average pace, and yet policy rates have been above 5% since May 2023 and above 4% since December 2022. With that kind of growth, and the inflation we have, they’re not restrictive.

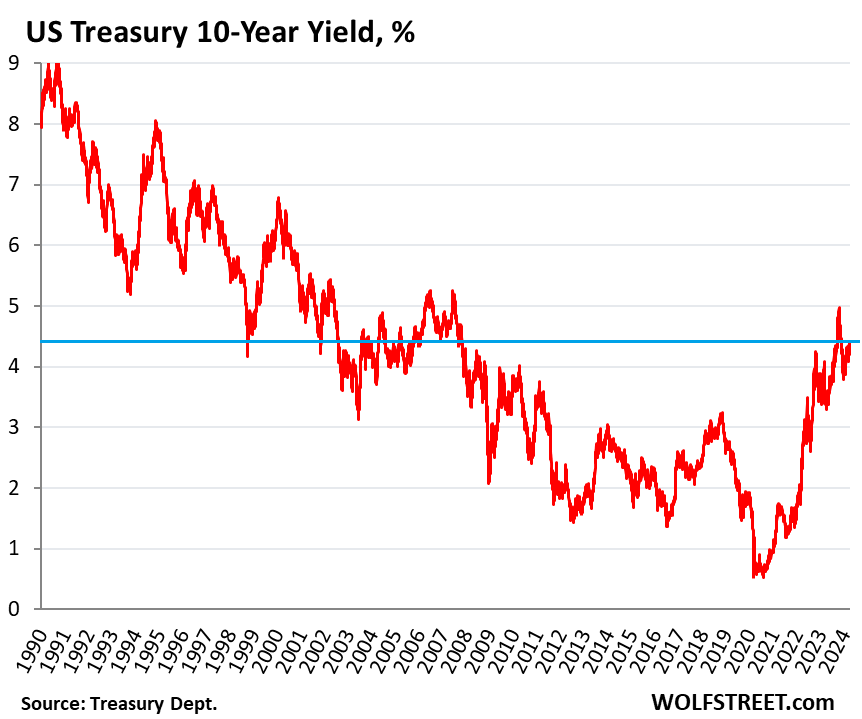

And the bond market is adjusting to this scenario and it seems is just heading back to the old normal – the normal from 20 or 30 years ago, as we can see in the long-term chart:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interest rates are returning to normal and the economy is doing fine.

Apple-

What is “normal” in the new secular inflation world? Isn’t that the question the bond market will grapple with over the next decade or two?

If we’re in a cycle like the one that led to the last interest rate peak (1981), my guess is that rates will vary (sometimes greatly) from year to year, and they will trend significantly higher before the next secular peak is achieved.

Finally, as rates grind higher, stuff will break, and there will be phases where the economy — most notably employment — will NOT be doing fine.

We wont see 70’s and 80’s style interest rates unless we have a huge jump in inflation.

Back then it was caused by a 400% increase in oil prices. That increase worked its way into virtually every product and service.

It’s not likely we’ll ever see that again, with the US now the world’s largest oil and gas producer and exporter.

CCCB-

Point on oil taken, though oil has been notably volatile and famously difficult to predict over the past 150 years, due primarily to the high capital investment required to unearth it. Shortages and gluts have always occurred. (Daniel Yergin’s The Prize is fascinating…)

Aside from oil, can you imagine a loss of faith in US treasury securities based on the enormous and growing federal deficits for any reason? Not talking about hard default or the like, but a buyers’ strike where thoughtful bond holders decide to hold off on longer term purchases (like many commenters here) in order to get a higher rate next month, or next year. In the face of huge issuance needs, that will one day be a problem, in my estimation.

I’m a nervous senior, and I’m not as worried for me as I am for my grandkids. Double-digit interest rates are not something I’d bet against forever, though timing is certainly impossible to call.

It’s not just oil. War profiteers (many of whom I knew in my childhood and youth) from the Military Ind Complex extracted an immense amount of money during the Cold and THEN ESPECIALLY the VIETNAM WAR.

And similar to today, these now ultra rich assholes did NOT put that money back into what I call “the real economy” where 70-80% of us reside….so our “stuff” cost more.

Seems simple as hell to me….but no fancy econ terms used.

WTF is “secular inflation” John H? Your whole comment seems based on it.

Sounds very impressive and Econ knowledge laden. Can it be graphically (a picture) shown for a moron like me?

Hint: I like histograms best. Thanks.

Make that “ENOUGH” of that money. The rest went under the “rich man’s mattresses” (my own econ-term). Although the groundskeeper and his staff at golf courses like Hilton Head and Beech Mountain, and around DC, etc, probably had jobs….non-union, though. They HATE unions and would rather slip them a $20 and be a big shot for whatever audience they had.

What the hell, since you likely won’t respond to the likes of me, I’ll guess…….

“Secular Inflation” means God isn’t causing it?

So I googled it…..basically it is chronic vs acute, slow, vs fast…..measured against what?

Past “inflations” I guess? Except NOT in Zimbabwe, so IT has a time and geographical (distance) dimension to it….General Relativity would likely describe it better?

Maybe God did make it.

Oh, and make it not self, but nieces and nephews, and their kids and anyone of the same ages, for me, too, John.

We have been planetary pigs for far too long and had better unwind our stupid ways FAST.

NBay-

Pepper and Salt cartoon in yesterday’s WSJournal was self-revelatory. Two old guys sitting on a bench in park. One says to other:

“I hope the world could put aside its differences and unite around what I think.”

Cheers!

Just the first page that comes up will do, unless (hopefully) you read more of it.

There are NO SIDES to this problem…it is ALL of ours….ALL of us caused it……..mankind and YOU and your offspring will NOT escape it by getting richer….the top .01% may think they can, but it will involve nasty social activity.

Exactly! The 18% of drop in new home prices is nothing more than lopping off the froth. I’m firmly in the camp that expects the next few months to solidify no rate cuts this year. Then by July, we will be looking at a 25-basis point increase. The Fed stopped 50-basis point to soon IMHO, but like Wolf says the Fed doesn’t want a recession. They need to run off their balance sheet by another $1.5T before the helicopter money printing machine restarts.

Personally, I’m looking forward to a return of the 5% 10YT and 8% 30YFRM. The housing market needs a lot more downside brought to bear.

The amount of deficit spending has created a self-sustaining jobs market. Very buoyant, indeed.

Hi Wolf, fwiw, the positive economic / jobs report hide the impact of large ongoing federal deficit spending offsetting higher Federal Reserve interest rates and QT. As the federal deficit and the interest charges on the 33 Trillion federal deficit continue to climb, we are heading for the realization that inflation won’t go away without addressing federal deficit spending. So the 10 year bond may need to stay in the 4-5% range until the growing federal deficit is addressed – if it is. My point is the soft landing has been achieved by massive federal debt bingeing and the delayed financial stress of higher interest rates, especially on housing, CRE, and business. Not everything depends on FOMC management.

As the cost of financing the national debt continues to increase, there is less government money for programs. 2023 to 2024 is expected to cost an additional $120B. They need to find this additional money just to keep spending even. What are the chances of that?

The one number to keep in mind is “interest payments as a percent of tax receipts” because tax receipts are going up too:

https://wolfstreet.com/2024/03/31/curse-of-easy-money-us-government-interest-payments-on-the-ballooning-debt-v-tax-receipts-amid-higher-interest-rates-inflation/

Yes, but the interest payments as a percent of tax receipts will easily surpass what it was in the 70’s and 80’s. The debt has been growing exponentially. CONgress refuses to balance the budget and gold is finally calling “bullshit” on all of this.

Interesting times, especially with the second wave of inflation coming ashore…

But tax receipts can’t grow to the sky? At some point, they will slow down and/or mean revert.

Then what?

Inflation automatically pumps up tax receipts. That’s just what inflation does, it pumps up the amounts of everything: prices, wages, dollars paid on prices and wages and incomes, etc.

It seems unlikely that rising interest payments will have any impact on spending. It just means: we borrow more to cover interest plus whatever more we wish to continue spending.

Tax receipt is going up because of the assets balloon and the savvy one cashing out (even if they have to pay taxes). Once and if that deflates, he retail bag holders won’t pay any capital taxes for the rest of their lives! The key in the mail phenomena!

Hey, sorry about my question the other day about T-bills rolling off. My bad! I read through your linked article which did a great job explaining how the Fed is using T-bills to meet the $60B cap.

Thanks!

Wolf,

Someday it would be interesting to see an overlapping chart/separate charts next to each other, showing each of the components that yield the chart above (accumulated G debt, interest rates, and tax revenue by year).

Each of those items tells an important story across time.

Since accumulated G debt ain’t done nuttin’ except go up (except for 1 year, sorta, I think) and I don’t think the average tax rate has been hiked much (easier to do stealth printing, er…”easing”, to “raise revenue”…sigh) that leaves interest rates as the driving factor over much of the last 40 years.

And, miracle dictu, the G controls interest rates too (along with tax rates and, in theory at least…ahem…G spending/debt accumulation rates).

It’s good to be king…controlling so many levers of power.

Cas127,

This chart shows interest payments and tax revenues, quarter. The chart below shows interest payments as percent of GDP. These are my quarterly charts. All you have to do is read the articles — this last one was published on March 31:

https://wolfstreet.com/2024/03/31/curse-of-easy-money-us-government-interest-payments-on-the-ballooning-debt-v-tax-receipts-amid-higher-interest-rates-inflation/

Wolf,

“Inflation automatically pumps up tax receipts.”

I thought – for personal income tax brackets at least – the levels were indexed to inflation.

Perhaps that was a reform done and subsequently undone.

Cas127,

Only the tax brackets are indexed to inflation so you don’t move into a higher tax bracket due to inflation. To use a simplified illustration: If you paid 15% on $100,000 in income in 2020, and there was 20% inflation in four years and your income due to inflation rose to $120,000 by 2024, you’re going to pay the same 15% but on $120,000 in 2024. So you’re in the same tax bracket (15%), thanks to indexing, but you pay $18,000 in axes in 2024, instead of $15,000 in 2020. And therefore, inflation inflates tax receipts. It’s one of the universal fiscal truths.

The annualized interest expense at the end of FY ’23 (i.e., more than 6 months ago) was $1.025T. If the Fed doesn’t cut rates between now & the end of FY ’24, this figure will grow to at least $1.3T. That’s WAY past an extra $120B. The Fed, for some unknown reasons, hasn’t updated this number in over six months. Gee, I wonder why?

BS. Read this:

https://wolfstreet.com/2024/03/31/curse-of-easy-money-us-government-interest-payments-on-the-ballooning-debt-v-tax-receipts-amid-higher-interest-rates-inflation/

Cassandro,

I believe you are 100% correct.

One line in Wolf’s posting caught my attention …

“ …they’re fretting that something big has changed in the economy…”

Your analysis that it is huge overspending by the Federal Government seems entirely spot on to me.

The next big cliff is the upcoming expiration of the 2017 Tax Cuts & Jobs Act in 2025. Most (but not all) Americans are likely to pay higher tax rates if the cuts are allowed to expire – which just might be the medicine needed to slow an overheated, high-inflation economy, especially given the FOMC’s reluctance to tighten more.

Congress has no incentive to deal with it before the elections. But typically, regardless of the outcome, they are “resolved” by both parties exchanging spending for more spending, then throwing everything onto the deficit.

They will just keep all those cuts in place.

I hope!

About 2/3 of tax payers will blow off the TCJA additional payments without skipping a beat. It’s the other 1/3 of the population that could potentially cause problems, such as rising delinquencies. Unfortunately, the magnitude of the impact will be determined through the discovery process in real time rather than through forecasts/projections. Brace yourself, and hope it is not as bad as it could potentially be.

The only thing unusual about today’s interest rates are the 10+ yr rates are too low. Nothing restrictive about this environment.

This week Kashkari spoke about possibility of no cuts at all. But he gave 2 cuts in March dot plot. Same for Bostic too. He was in 2 cuts camp; now he has moved to 1 cut and that too in Halloween time. He clearly stated out timeline unlike others.

Logan is even talking about possibility of rate hikes as possibility. Low but still a possibility. Same Kashkari said Rate hike is not off the table.

This just shows that those 2-3 dot plots are extremely optimistic scenario. Its just matter of time. Next 2-3 months higher than expected inflation readings and most will move to no cuts or 1 cut dot plot by June meeting.

Unfortunately Logan and Kashkari are not voters for 2024. Many Dem/Biden appointed are Federal Reserve governors and permanent voters. They are very dovish in their talks. Goosbee is not voter this year. But I am hoping they stick to their job. (Kugler, Barr, Jefferson).

Americans HATE inflation. It behooves any politician of any stripe to do whatever it takes to get inflation under control if they want to be reelected.

BINGO!

I am around these types more than is good for me and there is nothing they fear more than something people are mad about that cannot be spun.

Like high grocery bills… or large gas station signs announcing the price of a gallon of gasoline… you can’t talk your way out of those!

“americans hate inflation”

agreed.

but HOW MUCH do they hate it?

not enough to go out and protest.. not enough to reign in their spending.. and certainly not enough to ‘recall’ their local/national agent of the oligarchy to change anything.

sorry wolf but despite MANY MANY great insights and observations that you provide us with your articles/commentary, the second part of what you write here just isnt correct..

the only thing it behooves politicians to do is to keep their donors happy and keep themselves in the good graces of those who REALLY keep them in offlice.. not the dull peons out there who couldnt even name their own ‘politician’, much less call/write/communicate anything to them about how much they hate something.

its sad.. truly

but thats just the reality of it…

and i believe you made a comment in the previous article that:

“They’re not cowards in Congress. They’re free-money addicts.”

and therein lies your own repudiation of the comment you make here.. “free-money addicts” WILL NOT do ‘whatever it takes’ to get inflation under control.

“americans hate inflation”

Corporations love it. There are just a few people out there getting dirty stinking RICHER and still finding ways to jack the prices.

Americans are fat and lazy because the last 60 years of prosperity has caused them to be. That’s why I want some real hardship to toughen our pathetic “countrymen” up.

I take great pride in not knowing my representatives. It doesn’t matter whether I get Person A or Person B as regardless of intentions going in they become beholden to their party and to the system. Your ability to influence things is basically drinking from the same Kool aid that says climate change is just about personal responsibility.

I will agree keeping donors happy is how the system works as you stated and of course why money won’t be removed from politics not will there be term limits which is why most of them could be cast on The Walking Dead. Ever wonder how they can consistently outperform the market! Not hard when you set policies that impact it.

Billionaires owning major media companies is part of this too. “Democracy Dies in the Darkness”. lol.

NObOdy; if you notice a

yellow hue in your swimming pool, it could be the work of the dull peons.

But I doubt it was the uneducated that gets the credit for this fine fickle, blame God, or yourself.

Apple-

What is “normal” in the new secular inflation world? Isn’t that the question the bond market will grapple with over the next decade?

If we’re in a cycle like the one that led to the last interest rate peak, it’ll vary (sometimes greatly) from year to year, and it will trend significantly higher before the next secular peak.

Oops-

This comment was meant to be in response to Apple’s opening comment above.

How about Wage & Price controls? Any possibility of that happening before the election?

No.

Let’s hope not!

You’re fantasizing.

Already happening.

Look at rent control laws in California. Coming soon to a state near you.

Wolf may disagree with me, but rent control, especially eliminating vacancy decontrol, is a form of price controls.

You should expect to see age and price controls being trotted out. They will not be called that, but they will be.

There is a book on 4000 years of inflation, price and wage controls, etc. (I can’t remember the title, but it is something like “40 centuries of how not to fight inflation”).

These are just impossible to fix political dynamics, and politicians will always push price controls (and later wage controls).

I would love to get Wolf’s perspective on to what extent he thinks California’s rent controls are the type of price controls that typically occur in inflationary environments…

We’re already working under wage controls. Doing an appraisal with a manditory home inspection bundled has VA fee structure that is so low that its essentially wage controls under another name. $625 for about 30 to 40 hours of work. We could make more flipping hambergers at McDonalds. If you’re gonna freeze wages then you should freeze prices as well. Nixon did and Burns printed money so as to create a landslide re-election. Go for it!

“Do you remember.., your President Nixon…woo-woo-woo…and the bills you had to pay?” – Bowie

We’ve been under an equivalent to Wage & Price controls since 2008, and that is the Fed’s quantitative easing, designed to manipulate price discovery in debt markets. There is a lot of cascading price discovery if debt is manipulated to cause negative real interest rates on savings which subsidizes lower interest rates on borrowing.

That results in an asset tax on savings, used to subsidize borrowing for corporate share buybacks, and is called “transmitting monetary policy”.

Now, they’ve been on an hiatus from this policy for awhile with quantitative tightening. But, I wouldn’t bet dollar one on this practice of quantitative easing not returning.

We’ve been on a managed price discovery regime since 2008 more than more not. That’s the 21st century equivalent to wage and price controls.

My hope is that either all of the lawsuits against RealPage go through and shut them down, or they’re shut down by congress, and we can get some kind of competition in rentals again. So far it’s looking promising with everyone and their dog piling onto that lawsuit, including the DOJ and some states. They also just introduced the “Preventing the Algorithmic Facilitation of Rental Housing Cartels Act of 2024” into the senate (S.3692).

Our congressmen are all going to be charged with fraud on the American public. It seems that at least 75% are complicit or they would be shouting it from the mountaintop. Throw them all out and in jail.

charged with fraud???

by whom?

complicit or not, there wont be any jail time or even losing their seats for the vast majority of them..

where do you get these fantastical ideas from??

The real way to stop inflation is to peg the dollar to a commodity basket, which would stop run away printing by the Fed. But they’ll never get anywhere near that solution, so inflation will continue to run hot.

Good lordy. Did you see the prices of commodities spike by hundreds of percent in a few months and then totally re-collapse? Is that what you want the dollar tied to? I’d say we have enough problems already.

I dunno Wolf, maybe we should return to the ‘Gold Standard’?

“Americans HATE inflation.”

True…but in a playbook as old as…Biden, it ain’t the G’s fault…its Mars/Snickers.

(Biden ***really*** needed a Snickers…)

Great..bond rates going to all time high..but the real rate of inflation from the highest deficit in US history and interest payment on it account for (actual) double digit inflation..wonderful!!.. you’re losing less on bonds than you were before

Until this Wednesday when the CPI and inflation data comes out. Then rates will fall again on Thursday when the PPI comes out. That was the dead cat bounce in interest rates we just witnessed.

Brent Crude back to $91.17 as I write…… Keep your eye on it as it could be tickity tock time.

My “Gas station from Hell” is still posting $4.79/gallon for regular in spite of the recent surge in crude prices. I expect to see $4.99/gallon in the next few days.

Some countries tax interest and others do not. In the countries that tax interest, there are two interest rates. One is the rate that the payer of interest pays, the other is the one that receivers of interest receive after paying any tax on the interest. My question is: in countries that tax interest, does the interest rate become restrictive when payers of interest pay interest at a rate greater than the prevailing rate of inflation plus the so-called natural rate, or does it become restrictive when receivers of interest receive interest, net of tax, at a rate greater than inflation plus the so-called natural rate? And, of course, why?

My point is that real received interest rates after tax and adjustment for inflation remain solidly negative. Savers are having their savings watered down by inflation. The longer they hold their savings, the less they have to spend, so obviously they are motivated to spend on anything they want or need as quickly as they possibly can.

You’re absolutely correct.

Savers who are genuinely savers are not motivated by inflation to spend. By definition, nothing motivates them to spend. They are motivated only to save.

Signed,

Your Friendly Miser.

The logic (or lack thereof) of these “your money is going to be worth less next year so spend it now” crowd shows how financially illiterate they truly are. “Buy that new *toaster* today because it will be $10 more next year!” – failing to consider that the toaster, itself, will be worth $5 at a garage sale the day after you buy it.

What you eventually learn from having cash reserves is that it reduces the level of anxiety in your life. Get a flat? So what? Buy a tire. Life goes on. Kid needs braces? So what? Take him to the orthodontist and pay cash. HVAC blows up? So what? Get it repaired. Vs. OMG! What am I going to do? OMG! OMG! OMG!

3 classic kinds of risk management:

1) reserves (savings) (my favorite),

2) diversification (I have houses and cash, opposite ends of an inflation/deflation barbell), and

3) insurance (but wow! talk about inflation!)

But allow me to add the vast one:

4) government bailouts. The anxious spenders and boosters seem implicitly to believe bigtime in 4).

Some savers like me don’t really have more stuff to buy.

And it seems the longer I hold my savings and the less I spend, the more I have to spend. Just my personal experience.

“My point is that real received interest rates after tax and adjustment for inflation remain solidly negative”

Maybe if you’re only earning 3-4% in a regular bank account, but T-bills currently yield 5.4% (and are state income tax free), and you can earn a much higher yield if you go out a little on the risk spectrum.

If you want real yield you have to do the work for it. I think this used to be called ‘investing’ back in the day.

MM

Not an ounce of productivity there. Rent seeking (no investment in the productive sectors) is five times GDP compared to real productive spending. The cure? A wealth tax on property. This transfers the rents to the public sector.

Wolf,

Oct-Nov 2023, US Treasury played markets by tweaking duration of their securities sale. They reduced 10 year and above auction sizes and increased Bills and notes. That put a lid on demand of 10+ yr securities.

This helped them to defer higher yields to future. Clearly they were also counting on FED to reduce the rates.

Can Treasury keep doing same till election is over? Based on your earlier articles more than 7-8 T is due for refinance this year. So it will be hard for Treasury to keep using same strategy. I would like to know your thoughts on this? Thank you.

The Treasury was facing 5%-plus 10-year yields in October going into November. Yields had gone parabolic over the fall. You can see that in the first chart. So they switched tactics to take pressure off longer-term yields, which makes sense. Otherwise they might have had 6% 10-year yields. They still increased longer-term issuance, but only a little, and not as much as they would need (given the huge pile of new debt that needed to be sold) to keep the ratio of T-bills to notes and bonds steady.

They can maintain that for a while. This is not related to the election, most voters don’t pay attention to it, and mortgage rates have already priced in higher for longer. Eventually, they’re going to have to increase longer-term issuance, but they will do everything they can to push down longer-term yields, every administration does that and should do that, because for taxpayers, who have to pay the interest, it makes sense.

In other words, dupe other countries into buying low yield bonds by offering nothing in return like what yellen is doing right now.

Are they really being “duped” or just stupid?

Is anyone being forced to buy long term bonds at these crap yields?

“but they will do everything they can to push down longer-term yields, every administration does that and should do that”

Isn’t an increase in longer term rates needed to truly fight inflation. If everyone thinks the higher short term rates are only temporarily high, their behavior will, and has, reflect that. I think higher long rates are needed to help settle things down and actually slow the economy.

This commentary thread is the stuff I’ve been most closely watching here. Like some other regular readers of Wolf, I’ve had funds parked safely at the short end of the yield curve earning over 5.3%, while waiting and watching for the potential opportunity to rotate into longer-term Treasury bonds, if and when those yields rise to a similar level of return. And back in Oct-Nov 2023, was not happy when first reading about the “Yellen shift” to the shorter end of the yield curve, reducing the source of upcoming 10-year through 30-year bonds, ostensibly to suppress longer-term yields. To Wolf’s reply above, I’m curious as to how long the Treasury can maintain this play and hold back on issuing the long-term instruments. I’m also waiting to see if/when the bond market really pushes back hard enough to help drive a significant increase on the coupon rates on new Treasury issues.

The treasury does not like funding >20% of the debt with bills.

The Fed is in a tough spot given the looming election and the clear trend of warming inflation.

Cut rates in summer and inflation may get even worse, in which case Trump will blast Biden.

Keep rates “as is” and hope that inflation eases slightly into summer & fall (which may be wishful thinking at this point with most indicators like jobs, oil, etc. showing inflation tailwinds).

Message that more may need to be done, and maybe even raise .25 in July and risk tanking the stock market (which wouldn’t help Biden either).

The Fed took a celebratory lap a little to early last year, and now is in an unenviable position. Damned if they do, damned if they don’t. At least in terms of becoming a major election focus.

I am not seeing the Fed’s “celebratory lap.” They stopped raising rates when it was apparent that inflation was dropping. Inflation is NOT spiking right now… it is just drifting upwards. So the Fed is keeping the rates right where they are… just like they said they would.

I agree with you that they won’t raise or lower them this year out of political concerns… but that is if inflation doesn’t leap forward or the economy decline dramatically.

But at the moment they are hardly damned at all… they simply don’t need to do anything. Just watch what happens and hold their breath until December… only eight months away.

“they stopped raising rates when it was apparent that inflation was dropping.”

(and then proceeded to telegraph AT LEAST 4 RATE CUTS in 2024 with the december dot-plot)

^—- look, i found that ‘celebratory lap’ for you.

but of course they ‘simply dont need to do anything’. what fed chair or member of the fed has ever been held to account for anything they’ve done? they can lower, raise, whatever.. then just come up with some rationalization for whatever they decided to do.

see, thats the difference between gov’t ‘work’ and the private sector. (minus the megabanks) when they f*ck up, the gov’t aint goin nowhere, and their job isnt either.

but if you and i start a business and borrow money to launch a product/service that doesnt perform well.. then we very well may go bankrupt.

the point is.. the ‘chain of consequences’ is VASTLY different between gov’t decision-makers, and everybody else.

so yes, unfortunately.. you are correct. they dont NEED to do a d*mn thing.

Having lived for a long time my experience has been that 2% inflation is abnormal, 4 to 5% is normal and can rapidly grow to much more than that unless interest rates rise quickly. However, politicians fully know that this doesn’t buy votes and they can very readily create delays in many ways until the numbers race up to well over 10%, as happened in the 1970s. This was partly due to the Vietnam war, and it looks like history is going to repeat itself. How independent are central bankers when the defence forces run out of bullets? Deficit spending will take on a new meaning.

There is no better site than this for getting a read on what is happening with the economy and the FED. Rich in relevant information, presented with clear, accurate and unbiased commentary that I a able to digest in a short read. I value this so much that I made a monthly donation. Thanks Wolf!

Inflation should take into account the cost of money, this is the feedback loop that creates the inflationary trend. Interest rates are low, the cost of money is low, investment and cost of production is low. Interest rates high, cost of money high, costs of production high. They all feed back.

So in the same trend that interest rates have fed back lower for decades they will now trend higher imo.

I would be extremely interested to see what the inflation rate would be if the costs of borrowing were included. So e.g. in the UK asset inflation the cost of money not included in the headline inflation rate. Historically (last twenty years) the cost of money has been falling. So you could make a plausible argument that the inflation rate has actually been understated (in the sense that a falling price has been left out of the RPI basket). Now its the other way around but the US (and UK, Euro) are heading into a higher inflation environment carrying maxed out debt from the low inflation era. This seems like inevitable defaults not just higher interest rates. Examples in the US are the bank failures. For the UK a water utility is just failing, there is also a risk the government can’t roll over debt -and- have the BoE proceed with QT.

I think all of these things come to the US because as a larger economy, the process just takes longer, its not the case that the US is immune because of the petrodollar or being self-sufficient in energy. These things are great but they don’t help with too much debt.

Some of these issues are discussed in Peter Zeihan’s book “The End of the World Is Just the Beginning”.

“I would be extremely interested to see what the inflation rate would be if the costs of borrowing were included.”

Including the borrowing rate in inflation measures is total stupid BS for two reasons (though some central banks do a little of it):

1. The inflation rate would have shown MASSIVE DEFLATION for many years since 2008 as borrowing costs were pushed down by central banks. That would have caused central banks to lower interest rates even deeper into the negative, which would have pushed DEFLATION to new highs. Do you see how stupid this would be???

2. If you include borrowing costs in inflation measures, the central bank’s monetary policy action then does to the inflation measures the opposite of what monetary policy is trying to do:

— if it hikes rates to reduce inflation, it will cause inflation measures to go UP

— if it cuts rates to stimulate the economy and get inflation to rise, it will reduce inflation measures.

In other words: by including interest rates in inflation measures, inflation measures give you the wrong signals as a direct result of monetary policy actions. (the Bank of Canada has been struggling with that).

There is a lot of bullshit being circulated about inflation measures, and I’m sick of it.

But this is my point. That lowering borrowing costs by central banks shows up as deflation.

Borrowing costs are embedded in the economy.

Lowering rates -has- “measured” deflation, and enabled them to be lowered further.

Its a self-reinforcing trend and it has been anyway even without including borrowing costs in the inflation measurement.

Interest rates trended down to zero. Now the trend is going the other way.

But this is total bullshit. Lowering borrowing costs is NOT deflation. The price of your food rises 20%, and rents rise 8%, and autos are up 12%, and insurance is up 20%, and CPI shows “deflation” just because the Fed cut rates? People who say that this is deflation when actual prices jump are just nuts. It’s just total bullshit. Which is why the BLS removed mortgage rates from the CPI.

Larry Summers: “Inflation Reached 18% In 2022 Using the Government’s Previous Formula”

Interest is the price of credit. The price of money is the reciprocal of the price level. Low and high interest rates may thus be both evidence of either tight or easy money.

See: Recent developments in bank deposits

https://fredblog.stlouisfed.org/2024/03/recent-developments-in-bank-deposits/

That’s the opposite trend of secular stagnation.

US inflation in the 2000s and 2010s obviously came down because of China and its cheap factories. A $1000 television in the 1990s was equivalent $200 by the 2010s. US inflation is creeping back up in the 2020s as America unwinds from China. But don’t discount the emerging AI boom. That’s going to bring longterm US inflation right back down again in the next 1-20 years. Office workers (half the workforce) will be able to do much more with much less. For example, I’ve increased my blogging productivity by +500% with an AI tool. My “cost to blog” has more than halved.

Has the quality more than halved?

Lol yeah did the AI bot give you that 1-20 year timeframe

Undoubtedly AI will change some things just now impacting white collar work more similar to gains in automation. That isn’t a bad thing but from the US perspective how do you deal with reduced employment and require tax revenues to fund ever growing costs? The US is #1 in healthcare in all the worst ways but significantly bringing down administrative costs would be a positive, unless of course that just becomes more profit to an industry that shouldn’t be profit driven to start with.

ChS,

I remember graduating college in 1990 and believing the entire health care system would be evolved so anywhere you went in US and ideally most of the world that access would be available. Not sure if intentional or just incompetence but still not close to having unified systems, which AI would in an ideal world would need.

I agree WebMd, Mayoclinic and others are great and appreciate we have good doctors here albeit in a dsyfunctional system. When I was overseas doctors didn’t want you to ask questions as it was an afront to their power. Nice to utilize the Internet to take responsibility for health and ask good questions. Admittedly they tell me more fish and less red meat and I have selective listening.

“Admittedly they tell me more fish and less red meat and I have selective listening”

Thankfully you have access to enough information to know the vilification of red meat for health reasons is BS.

ChS,

I find out interactions interesting. I never thought meat was vilified, simply that to lower my cholesterol I should eat red meat in moderation and I am not very good at that. Growing up in a super size culture has its consequences! Reminds me of The Great Outdoors and the 96er!

So the interwebs have made you so smart that you can diagnose illness…..just like a doctor.

If you want to learn to do actual diagnosing, go to med school.

The arrogance of those who read websites…..

OutsideTheBox,

You have no clue about what you are commenting on. I brought my infant child into an ER for an issue that the doctors couldn’t figure out and her regular pediatrician couldn’t figure it out. With some effort and access to a lot of information, I was able to figure it out. Several other examples, but that doesn’t make me qualified as anything, nor does it render doctors useless. The point is, if you are willing to self advocate and are willing to put in some effort, there is a lot you can accomplish.

Talk about fucking arrogance

Glen,

My point was the medical industrial complex has vilified red meat, much to the detriment of the patients they claim to be helping.

Of what useful value to anyone is your ‘blog?’

Yes, if the blog needs 50% less of its operator’s inputs, how long until it needs 100% less?

If it’s written even partially by AI, very likely close to nothing. In fact, the social value is probably negative, as AI-written garbage has begun noticeably to clog search results on Google and DuckDuckGo.

Yes, absolutely this. It’s difficult these days to wade through numerous search engine results leading to useless AI articles, before finding something that’s actually helpful.

Perhaps someday the technology will be good enough that we can’t tell. That day is not today.

“That’s going to bring longterm US inflation right back down again in the next 1-20 years.”

Quite bold of you to predict such a specific timeline.

“But don’t discount the emerging AI boom. That’s going to bring longterm US inflation right back down again in the next 1-20 years. Office workers (half the workforce) will be able to do much more with much less. For example, I’ve increased my blogging productivity by +500% with an AI tool. My “cost to blog” has more than halved.”

Some positions may be eliminated. High level thought positions are augmented by AI at some level, but lower level positions can be outright replaced. Much of what is offshored or an offshore target right now already has low output quality so AI with a LLM and resultant hallucinations is actually still a step up.

Some areas like marketing may find headcount reductions. Productivity increases are a double-edged sword, especially in business belt-tightening times like we appear to be destined to enter, whenever this “bubble” deflates.

There’s a lot of hype around AI right now, and for word smithing with heavy editing it’s either helpful (low thought output) or harmful (things like Wolfstreet which require significant amounts of high-level logic/thought). It only takes a few minutes to course correct hallucinations in marketing material.

I would not want to be in a position with a core focus of written output which isn’t significantly derived from original ideas and reasoning. If the output just needs to look like everything else out there, the current type of AI being developed is a job replacement waiting to happen. Inflation coming down due this is going to be via reduced spending due to job destruction.

It’s a plus to productivity in some office work and software work. The cost has not been factored in yet. If internet is any guide, the loss of job won’t be too high. The limited monetization of llm has become a factor in slowing down the current craze.

I noticed a few weeks ago that Chase has already cut the rates it pays on CDs across the board. Even tho there’s been NO Fed rate cut.

So they’re anticipatorially screwing their customers.

1. Yank your money out and put it into T-bills on auto-rollover at your broker or at TreasuryDirect.gov. 1-4 month T-bills are paying 5.3%-plus

2. Nope, banks don’t adjust deposit interest rates based on what they see in the future. They want to get their borrowing costs (interest on deposits) down, and if they have enough deposits, they lower the rates. If they need more deposits (after people yanked their money out), they offer higher deposit interest rates on some of their products. And they’re screwing their loyal customers by offering them 0.01% until they yank their money out.

1. I always wonder what bank thinks as they see me plow millions into Treasuries.

I remember telling a simple teller at the bank once that I would happy to keep my money in my savings account, if not for the absurdly low rates they offer.

#2. Wolf, not put you in an awkward position, but I would love to see you write an article on what the Federal reserve would do if the Fed chair was Wolf Ritcher

#3. Love your blog. Like I follow Lacy Hunt, I read everything you write.

The absolutely last thing I would want to be in my life is Fed chair. I like my gig here. I can say pretty much what I want without blowing up markets and ruining everyone’s day and having the President tell me daily on X that I’m stupid and that he’ll fire me if I don’t change my mind, and having Sen. Warren tell me that I’m a “dangerous man” because I hiked policy rates a little bit and unprinted some money. I don’t even want to think about what I’d do as Fed chair. That’s a job from hell. No thanks.

One of me dads friends way back when took a Security Of The Treasury gig,me dad asked why he took gig and he responded he would do less damage then others being considered!

Howdy Sacramento. Your location?? If so, not every place is peace and love. The FED realizing The Lone Wolf is out there??? You would soon be reading he killed himself or was killed…..

I sure hope the Lone Wolf has guards at his lair……..

I get that Wolf wants no parts of the Fed chair gig, but hypothetically speaking, in place of Powell I’d love to see Wolf standing at that podium and addressing all the idiotic questions at the tail end of each post-meeting Fed press conference…that would be real entertainment!

Yes, I’d love to stand at the podium, my special reporter-Taser in hand. I would even do my hair for that:

“I just answered that.” ZZZZZZAPPPP, “next question.”

“Leading question.” ZZZZZZAPPPP, “next question.”

“Stupid question.” ZZZZZZAPPPP, “next question.”

“What does that have to do with monetary policy?” ZZZZZZAPPPP, “next question.”

“That wasn’t a question, but a story, and you’re trying to get me to say something about it that your hedge-fund buddies could interpret between the lines as “Wolf was dovish,” and then spread around the media and the internet that ‘Wolf was dovish.'” ZZZZZZAPPPP, ZZZZZAPPPP, ZZZZZAPPPP, “Next question”

Jamie Dimon should include a free pair of replica White House cuff links with every CD.

Even with higher gas prices, Summer travel is right around the corner followed by holiday season. I would have thought if we saw any slowdown it would have shown itself, but clearly not. I have already dropped several thousand on flights, hotels and concerts and that doesn’t count what I spend when I get there. YOLO!

Waikoloa Hawaii for 2 months starting in May of fun and scuba. We just need to spend more money for more fun at 70 with max SS.

Tip: The beach in front of Mauna Lani Beach Club is a hidden gem for snorkeling. You can park at one of the 12ish free parking spaces available at Kalahuipua’a Historic Park and take the short and beautiful walk down.

Although a lot of people are nostalgic about the economy in the pre-pandemic period, we haven’t seen yields near this level since the GFC — and obviously during that period inflation was minimal.

The nostalgic yearning to believe we’re headed back to low prices, because of an election is absurd in my book.

The article states: “That means the Fed will keep its policy rates fairly high – high enough to not let inflation spiral out of control, but not so high as to crash the economy and bring inflation down to 2% – and yields will be higher too to compensate for the higher inflation, everything will be higher, like it used to be, and the bond market is adjusting to that scenario.”

The FED actually does not know what rate is “normal” or restrictive enough, because the 0 % rate experiment warped the economy is such a way, that everything is a “guess”. There can not be a “normal” rate anymore, because the last decade was abnormal. So the FED can not determine what is restrictive anymore. Is it 5,50 %? Maybe it’s 6 %? Or maybe 7 %?

Also: if a 5,25 % rate will be the new normal for the next 5 years, there is no guarantee that the amont of liquidity, which is already in the system, is not inflationary – even at these rates. Inflation becomes part of the system, it’s a hydra with many heads – you cut one off, and there’s the next one.

This battle is far from over. You can not have a “red hot” economy and labor market if the rates are restrictive. Something needs to break first. Recession is the only way to battle inflation.

Perhaps but recessions of the scope you are talking about are avoidable because the rich come out richer and the poor, poorer. This is for a lot of reasons but mostly a result of actions governments take such as lowering interest rates, special economic incentives such as tax breaks, and of course monetary and other policies that flood the market. The goal of course is to protect markets but what happens is markets and assets rise without corresponding economic output. This is why billionaires get richer and more millionaires are created.

A soft landing, in other words, protects the most vulnerable as the wealthy do fine either way.

Is I’ve said many times before, the Fed’s current position may actually be restrictive in the long-term, but inflation needs to be fought in the short-term. With RE and asset prices making new highs, and inflation still running hot, it’s time for short-term focus to reduce inflation.

Who really cares if rates go up .25% if your stocks and RE gain another $100k? The stock and home owning populations will keep spending like crazy due to the wealth effect. The federal government will keep spending as well.

We can’t let the lower classes deal with more 3-5% inflation after the recent 20% inflationary spike. It’s time for the Fed to worry about the inflation rate RIGHT NOW, not achieving an ultra-soft landing three years from now.

Bring on the bear steepener.

That would be nice a bear steepner bond of my dreams!!

Many people on this board have been saying the rate pause and slow-walking of QT were overly dovish. It looks like they were correct, given the sideways inflation and record-breaking asset prices.

The Federal Reserve has continually erred on the side of inflation, and for a reason, I believe. We’ve crossed the Rubicon. There will be no return without carnage.

So what carnage are we looking at? I assume your reference to the Rubicon and carnage were figurative rather than literal, although not like civil wars aren’t part of America.

Who knows what the carnage will be?

I believe the Fed will continually err on the side of inflation until pent up, insurmountable forces take over, but I’m planning for opposing outcomes of recession/austerity or hyperinflation, using a barbell strategy.

One thing is ultra-clear to me. The status quo with ever-increasing debt/GDP ratio and liquidity/GDP ratio is unsustainable. I wouldn’t be surprised if there is a Minsky moment Monday, or a gradual journey to hyperinflation over the next decade. Once you begin the practice of printing money, alongside deficit spending, anything is possible.

If I were forced to take one side of it, I’d say the Fed will do everything it can to avoid recession until hyperinflation is knocking at the door.

Already seeing the carnage with all these “dollar” stores closing. Those stores are a big help for those at the lower end of the economic rungs. They are going to be buying higher priced items in lower quantities. Plus you have the jobs lost.

True, many dollar trees shutdown and 99 cents only closing completely. I am sure the decline in retail plays in too. Still plenty of low cost grocery options which have relatively good prices(Food for less, Grocery Outlet,etc.). I sense on some level the time was up for those types of smaller stores and others will fill the need if not already.

14,000 folks are now being fired at 99 Cents Only stores here in California and Arizona and Nevada as of 04/05/2024 as that entire retail chain rapidly liquidates.

Those stores were no longer a help for the poor, and hence they are now shutting down. Prices of *all* items in the store rose 25% to 50% in a *single day*. What sort of other business owner out there would do that, and expect their business to continue as a going concern?

Dollar stores are a bad deal for the poor. Look at the unit price of each item and you’l find them cheaper at the discount grocery stores e.g. market basket, aldi etc.

I have quite a few dirt poor friends and I’ve been telling them to stop goiing to dollar tree for the last year for this reason.

…one should have the totally-achievable mastery of basic arithmetic before worrying about acquiring ‘math’. (…this now-common semantic conflation makes me see too-much eye-glazing among those who might be termed ‘poorly-educated…).

may we all find a better day.

Even some of the crackpot economists out there, who have defended QE, ZIRP, etc., are saying the same thing – that the way inflation is now calculated shows a favorable number versus how it was handled back in the days Wolf refers to. We are being lied to and gaslit.

Odd how for the past few months as the Fed-obsessed mainstream financial media have been carpet bombing readers and viewers with rate cut talk, the bond market has quietly been hiking rates. One of them has been dead wrong and I don’t think it’s the market.

Surely it is not the financial media who is wrong, as they are composed of the best, brightest and most objective that our society has to offer.

I was at my favorite Thai restaurant yesterday eve. They now have put price increases in on nearly every item. No more new menus. The are written in by hand. That’s not a good sign that the recent inflation spike is transitory.

Pad Thai is now $18 at all of my spots. Was $13 or $14 not long ago.

Prices have broken through my quite considerable indifference barrier. Businesses have not helped themselves with these auto tipping terminals, either. And you can’t not tip without getting stink eye and crap service, even though what you’re tipping for is a few seconds for someone to go get a pre prepared item and put it in a to go bag.

I think we’re personally on the verge of a major cutback. Not because we need to, but because the prices have become too noticeably terrible value.

I sure hope so, because everywhere I see, people are falling over themselves to pay absurd prices everywhere.

Prepared foods (casual fast food take out, restaurants, etc.) are where I’ve noticed prices really get out of hand.

I make a point to only patronize those places which I see as only having raised prices to cover their costs, as opposed to just being greedy. For example, the deli that raised their breakfast sandwiches from 6.25 to 6.50 in 2022 and now to 6.75, rather than the places that have raised their prices 30-40%

Went to breakfast at a local Denney’s with a friend yesterday morning. This was a location where three years ago, there was up to an hour’s wait for a table on Saturday morning. We walked right in at 8:00 AM and the place was 1/3 full. Our two omelettes were $13.99 each and with coffee, the bill came to $33.00+. AARP card did get us 15% off though.

The service was mediocre, at best.

So long Denney’s for breakfast going forward!

In my view, the 10 year Treasury has been broken ever since GFC. The Fed and Treasury influence to manipulate rates with Zirp did a poor job of anticipating post pandemic inflation.

With the distortion in place from GFC Zirp and now the pandemic, it’s unlikely that anything normal is on the horizon.

Additionally, the amount of overall economic speculation and decrease in risk management amplify the disconnect previously related to term premiums and the general concepts related to safety and hedges.

It’s actually amazing that it may not be safe to own a ten year Treasury, because of future value risk. If that’s the case, yields will likely continually push higher.

The late Milton Friedman argued that excess government spending via the money printer is a major cause of inflation.

He even pressed the emergency stop button on the printing press and said that he stopped inflation temporarily lol

But it’s weird how 2 years after the pandemic stimmies were wounded down that inflation is hard to get down.

There’s still an enormous amount of money sloshing around from those “easy money” days, pay has gone up significantly, and the government is deficit spending at 7+% of gdp so I’m not surprised inflation is ongoing.

Have you seen the Government spending this year? Not slowing down at all.

The new House speaker is even worse than the last one. He hasn’t cut a dime from the Federal budget. We’re still spending at the levels of the Pelosi budget and then some. He needs to be removed ASAP.

Howdy Youngins. We will make it through this in years if not decades. LONG way to go…… Pay down personal debt and find more freedom…3% ers should look at HELOCs. You can t move for 30 years so use that equity to your advantage……

DFB

So people with a home that is paid for can’t

move either ?

You got some goofy logic there…….

Howdy Outside TB. How can you be a 3 % er if you have no mortgage.

Kinda goofy too.

DFB

You make constant reference to “hostages” – that people with FAVORABLE housing finances “entraps” you in a home.

Complete nonsense.

A low interest mortgage opens the door wide to a paid off mortgage via additional principle payments.

It is as favorable to have a low interest mortgage as it is favorable to have a paid off morgage.

No hostages at all.

“A low interest mortgage opens the door wide to a paid off mortgage via additional principle [sic] payments.

It is as favorable to have a low interest mortgage as it is favorable to have a paid off morgage.”

Its even more favorable to have a low rate mortgage, but loan money back to the US gov’t at double the rate rather than paying down the principal.

“3% ers should look at HELOCs”

Why would I trade ultra-low-rare debt for that with a higher rate? I fail to see your logic here.

Howdy MM or should I say Prisoner? HEE HEE. HELOCs are a great investment tool if you know how to use them. You also just proved how being a 3 % er makes one a prisoner. Read what you just typed.

TO those 3% ers. Why trade? What if you have to trade????

Explaining about being a 3% prisoner is like explaining what a Starter Home is. You will not understand the world of a squirrel and that is AOK anyway……

HELOCs are a loan, that’s all. With a 3% mortgage, no need to take on higher percentage debt unless absolutely needed. DFB, I think you are still living in the past! LOL!

Anthony

Notice that he is simultaneously promoting being a “squirrel” and being a borrower.

Yeah……sure.

Wolf,

Philosophical question for you:

Why does history repeat itself?

The answer to that question determines whether we have a 1970s style spiral, or whether it is nipped in the bud by the Fed.

My guess is that history repeats itself because the dynamics of human nature don’t change, and then in similar situations large groups repeat past mistakes, even if they know better.

What is your opinion?

In my entire life, I have never observed that history “repeats itself.” But there are some parallels occasionally, and some similarities.

Fair enough.

Wolf

According to Mark Twain:

History “doesn’t repeat itself”

It “Rhymes”

Howdy BVW. Bell bottoms came back. I admit, keeping my leisure suit may be silly but in a few more years?????

Because 80%+ of the population cares much more about how nice their watch is instead of understanding how the world works. Everyone sets their priorities based on personal factors. It’s not wrong. It just is what it is.

Inflation expectations are now embedded, and we can expect every bill we pay (cable, utilities, insurance, etc..) to continue to increase yearly. This is the worst scenario possible for the Fed in combating inflation.

This is also going to become political over the summer, as the FED cannot lower rates, are getting hammered on their portfolio of MBS, Bonds, IOER, and 90% of the country is suffering.

Twice today at the grocery store I saw customers combing through their receipts looking for ways to cut costs, and answers to why prices keep rising.

If Biden wants four more years, he will need to replace Yellen and Powell. They are too old, and their miss on inflation (transitory?) deserves consequences.

The ship for anything changing between now and November sailed a long time ago. It’s all down to political spending in 7 states to win a few tens of thousands of voters here and there. I just hope whatever happens the focus continues to be on reducing inflation while maintaining employment.

Biden is too old, too! Well, maybe his “handlers” aren’t?

I like that rate chart! I can see all the Fed cuts going back in time and for what reason they did. The bull run in bonds has come to an end since 91. The recession calls and rate cuts have not happened. I expected a recession but bought into the yields on money. Staying short duration until who knows when. Thanks Wolf! Great commentary as always.

“And they’re fretting that something big has changed in the economy: That even the 5.25% to 5.5% short-term policy rates, that were supposed to be “restrictive” and that were widely expected to throw the economy into a recession, have not been restrictive and have not slowed the economy.”

And yet when I said at the time that the “pause” was reckless and too soon, I was accused of “wanting to burn it all down.”

Well, don’t you want to burn it all down. The millionaires were next on your list… the ones living by the sea…the rope thingy.

No objection here

So was I. And all I wanted was for policy to be actually somewhat goddamned restrictive.

I think the course of rate hikes has been correct. It’s the QT part they screwed up on. It should have been swift and large when the liquidity was bleeding out people’s eyeballs, and the economy could handle large draw downs for a short period. It would have sent a message, and markets would have listened, while at the same time not collapsing. This QT thing is new, and they don’t understand the psychology behind the tool… yet.

PS I believe hikes have been in correct increments and stopping point, once they started hiking. Clearly, they should have started tapering QE and hiking about eight months earlier.

@Depth Charge,

$1.85 Trillion in corporate bonds were issued in 2020 with 5yr rates as low as 0.80%. Rolling those bonds over will have rates of at over 5% next year, and how far over is unclear. The money from some of that bond issuance was likely levered (5x? 7x? 10x? 15x?) for further investment. The long and variable lag crap applies to these types of debt. If anything, the Fed will probably have to cut at least twice this year to start the “non collapse” trajectory for lower rates as those bonds come due next year. Even a low 4% Fed Funds rate next year will cause some of these people who need to reissue debt to go under, “some” meaning more than usual.

Those bonds only need to be reissued if they mismatched the duration of their assets and liabilities. I expect some did and they should suffer the consequences thereof as well as their equity and debt partners. Some of us passed on those deals/partnerships. Saving them causes moral hazard. Those who matched duration risks can take their profits and look for more deals that make sense instead of taking foolish risks.

So what are y’all investing in with little to no risk? CDs? T-bills?

I think CDs are still at around 5%

I’ve got everything in CD’s and short term Treasuries. Getting 5+ % with no risk. F..k the stock market.

Howdy Broker Dan. T Bills at Treasury Direct. NO brokers or opinions.

T bills to avoid California taxes on it. 5.4% or so and doing 13 and 17 weeks with auto reinvest. If longer duration yields go up I can simply end auto reinvest and put in longer. I use Ally for in and out account as 4.3% isn’t bad for that purpose. Reduced but keeping many equity positions since capital gains would be brutal.

Always use Treasury direct for sort duration.

I will recommend Lending Club bank for In/Out account and other misc savings which we need handy. Gives me 5%. I used to use Ally but it was always less than Lending Club bank. Almost by 75BP.

I went with Ally because of the very easy ability to create a trust account online. Not clear why this is such a problem for so many institutions. My parents had one account outside of trust and had to deal with probate.

Glen,

I used to face same issue for Trust account. Lending Club also I use Trust account. It was fairly easy when I opened it.

Just sharing the info…

SRK,

Thanks. The more you know the better! Plus not like I can’t have my cake and eat it to, although I suppose that is one expression I constantly misuse.

Treasury money fund (SNSXX/SUTXX). Tax free at the state level and you can take out any day no penalty and it pays over 5%.

Z: That’s good stuff. And there’s also SNAXX, if state taxes are not an issue.

For me going completely risk free is a little too conservative. I’m at bbout…

20% T-bills & agency bonds

60% specialty credit instruments (high-yeld bonds, sr. secured debt, BDCs, CLOs, etc.)

10% one single stock – a microcap energy company I’ve held for years that pays a nice dividend

10% shorts against housing and TLT

My goal is a 10% annual return.

Don’t forget about I-bonds.

True but 10K limit(15K if able to work via tax refund) runs out quick and of course only liquid with no penalty if more than 5 years.

I also like Treasury Direct for having no broker or sketchy issues like a certain brokerage making it appear you have cash after you sell some stock, but actually, the stock sales need to settle over a few days and if you buy something, the system doesn’t warn you that the “cash” isn’t clear yet, instead, in a few days you’ll get a notice saying you took out a margin loan, even if you had and still have more than enough extra funds in a MM to cover it. So be very wary of brokerages due to this because small and unaware margin loans can quickly snowball out of control. So if you have an IRA, supposedly the only alternative to a brokerage account is a bank, can’t use treasury direct for an IRA, but can you buy treasuries and CDs from other banks through a bank IRA? Another good thing about TD is they seamlessly reinvest T-bills with no time gap while a certain brokerage for some reason can’t or likely chooses not to do that and you’ll have to put your funds into a MM, which have some risk, for a week if you want interest until the next auction of the same duration.

If we’re tired of inflation we need to accept that spending needs to be cut substantially and for a long while, and we need to start living frugally, otherwise it could be a bigger shock at a more inconvenient time soon, but sadly it seems like that might be the only way for us to realize we’ve been wrong.

Not that it matters a bit or means anything about treasury spreads, I just looked on Fred, for:

3 month treasury minus 10 year Real treasury and got an interesting spread that was last seen August 1989.

Well, to clarify a bit, I drew a line from the high point of this cycle, from last summer, and the spread has come down a little since then, but it’s going higher.

That’s an interesting time for inflation and rates, and this was an exercise where short rates in relation to the Real 10.

Wolf,

What do you think about the argument for diversified utilities (XLU) as a bond proxy? The idea being that the dividend payments go up annually as inflation goes up (meaning dividend compounding), as opposed to medium term or longer duration bonds (where inflation risk is bigger).

Obviously, with something like XLU there is a need to stay on top of technicals and market shenanigans, but it seems like it makes more sense than people investing in TLT.

Mike Wilson was making this point earlier because he said the people pushing long duration treasuries simply are not grasping the magnitude of inflation risk, and he was saying he thought being in a diversified utility fund was probably safer than a 30 year treasury.

Do you feel that there is increasing recognition in the investment community of this dynamic, and if so, do you believe this could portend a shift in the 60/40 portfolio?

If there is a shift, due to mechanical flows there could be a major run up in rates once consensus shifts.

Lots of utilities went bankrupt over the years, including huge ones such as TXU (Texas) and PG&E (California, twice). So don’t confuse utilities with safe assets, such as T-bills. Utilities can have their charms, bonds and stocks both, but they’re NOT risk-free. So returns would have to be much higher than T-bills in order to compensate you for the risk the utility might get in trouble (but that’s not inflation risk, which would be on top of it).

I agree that longer-duration notes and bonds (of any kind) are currently not compensating you for the inflation risk going forward, market is only slowly coming out of denial. I have no idea why anyone is buying 10-year T-notes at 4.4%.

I just looked at XLU… only a 3.35% distribution yield. Gross! Might as well just buy treasuries at that point.

I currently hold a utility income MF, but even with its 8.5% distribution rate, its one of my lowest-yielding funds.

Watch out for “yield “ distribution rate can easily be cap gains or capital distributions

“That means the Fed will keep its policy rates fairly high – high enough to not let inflation spiral out of control, but not so high as to crash the economy and bring inflation down to 2% – and yields will be higher too to compensate for the higher inflation, everything will be higher, like it used to be, and the bond market is adjusting to that scenario.”

Is it the government spending that is keeping the economy humming along?

if yes, even if the Fed keeps its rates where it is, would any curb on government borrowing (though not because they would like to) do the trick of crashing the economy?

In this case are we back to ZIRP and QE?

Wolf, how does inflation come down with the stock market hitting new highs? People feeling richer and richer will keep spending….

And with the election coming up, would the fed actually say anything that could cause the market to pull back 15-20%?

Add peak housing bubble prices in most areas and that’s why nothing is slowing down. People with houses and assets feel richer than they ever have in life, and are spending more than ever.

Mb,

Can’t imagine most Americans look at stock market and keep spending. The top 10% own 90% of the stock while the bottom 50% own 1%. You can pull different numbers but the jist is the same. Of course Americans do have some in pension or 401 plans but those aren’t exactly liquid and spendable.

Guessing the commenters by and large here are in a different position as my interest in financial markets and interest rates is because I have investments. If I was living paycheck to paycheck I probably would have less interest in local and global markets. Admittedly there are also a decent amount of savers and of course people inheriting money as the boomers continue to reach the elder years.

Any system that looks upon savers(id est, ours) is an evil entity and should be crushed under the jackboots of economic reason.

Wolf-

What was your thought process behind using 1990 as a starting point for the last chart, on which I think the blue line represents more normal rates?

Extending back to the beginning of the secular peak of interest rates in 1981 might have provided a slightly different conclusion as to what “normal” rates might rise to (if we are lucky enough to avoid an ugly over-shoot!)

Not meaning to sound at all critical, but I know from your past articles and comments that you have thoughtful reasons for your selected data points.

Thanks for any additional comment.

The problem with these 5-decade charts is that you cannot see the recent events. It’s just kind of a line straight up with a fist at the top. Every time I choose a time span, it’s a compromise. The longer the time span, the less you can see.

I’ve posted this chart before. It covers the entire 40-year bond bull market and the years before and after. It hasn’t changed in months because you cannot see the changes. You’re just looking at a rough picture of ancient history. If you saw it once, that’s enough.

Also inflation in 1970s and 1980s was often far higher than in this cycle. I lived through that cycle as a young adult back then, cutting my teeth in the work force. Just no comparison to this cycle. It was really bad inflation. So it was NOT a “normal time” with “normal rates.” Those were extraordinary times, with the US on the brink.

Unless yields shoot way past 5%, the chart is going to look the same next time. So just remember it. Stick it on your fridge, it’s kind of cute:

Wolf – thank you. (Your patience (and understandable episodes of exasperation), given the spread of ages who frequent this fine establishment (…and, I hope, a growing-if grudging willingness to listen, if not agree, with respect between those generations…) never fails to amaze me…).

may we all find a better day.

Agreed. This chart definitely shows how different generations can have different expectations of interest rates! It’s not just because folks are clueless, they’ve never experienced what others have. While they may understand in their head, it’s not in their gut.

Sympathy for that can be hard to come by. I’m not sure I’m up for more teaching (like Wolf) and less complaining though. :-)

CC – well said. ’tis always a narrow and rocky path we walk ‘twix our intellect and our emotions (and the right of the soldiery to complain is never trifled with by a wise commander). best.

may we all find a better day.

Professor emeritus Pritchard never minced his words, and in May 1980 pontificated that:

“The Depository Institutions Monetary Control Act will have a pronounced effect in reducing money velocity”.

Thus, we got Greenspan’s Great Moderation.

“checking deposits have remained elevated since the pandemic, between 24% and 26% of GDP.”

That is the opposite senario as secular stagnation. Therefore we will have higher interest rates going forward.

Ah those waiting for the other shoe to drop can keep on waiting. We are bigger than US Steel. America’s economy is “too big too fail.” Jobs are plentiful, wages are up, and travel and entertainment has never been better. This will go down in history as the greatest economic expansion the world has ever seen. If you want Shock and Awe and discouraging news, see the college graduates in China who are dumb founded by their future prospects.

Wolf, perhaps an article on the reason for Rate Cut Mania.

Who, what(tf), where when, why?