And a look back at the head-fakes core services inflation dished up last time with this type of inflation.

By Wolf Richter for WOLF STREET.

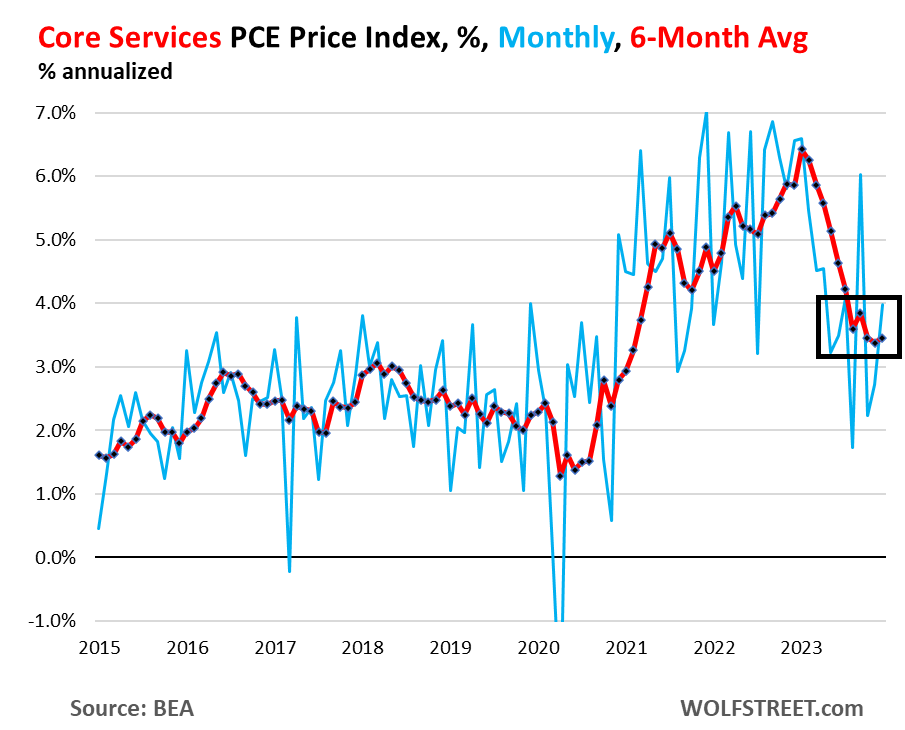

So right up front – and the Fed has been talking about this, though no one listens: The “core services” PCE price index has gotten stuck at 3.5% over the past six months annualized, and accelerated to 4.0% month-to-month annualized in December, with housing inflation stuck at about 5.7% over the past six months annualized, and with other core services components still red-hot.

The core services PCE price index rose by 0.33% in December from November, the second acceleration in a row, according to data from the Bureau of Economic Analysis today. This amounts to an increase of 4.0% annualized (blue).

The six-month moving average, which irons out the huge ups and downs of the month-to-month data, accelerated to 3.5%, and has been in this range since August, after the sharp deceleration in early 2023 (red).

Core services is where consumers spend the majority of their money, and they matter. Which is why Fed governors have said in near unison that they’re in no hurry to cut rates, but have taken a wait-and-see approach, with an eye on core services. And if it goes away, fine.

But on the surface, the PCE price index looks encouraging, and this has been the trend for months, with the overall PCE price index at +2.6% year-over-year in December, the lowest since March 2021; and with the core PCE price index at +2.9% year-over-year, also the lowest since March 2021, and aiming for the Fed’s 2% target.

The factors for the year-over-year cooling in these inflation measures have been the same for months: plunging energy prices, sharply dropping prices of durable goods after the huge spike in 2020 and 2021, cooling food inflation (with prices still rising from very high levels, but slowly), and favorable “base effects” when compared to a year ago.

But energy prices don’t plunge forever, so that will go away; durable goods prices don’t drop sharply forever either, though they can drop for a while longer to unwind some more of the price spike they’d been through in 2020 and 2021; and the base effects are going to get timed out this year, when the base of the year-over-year comparisons become the lower inflation figures of 2023.

A similar scenario has emerged in the CPI inflation index for December, which we discussed in detail with lots of charts here.

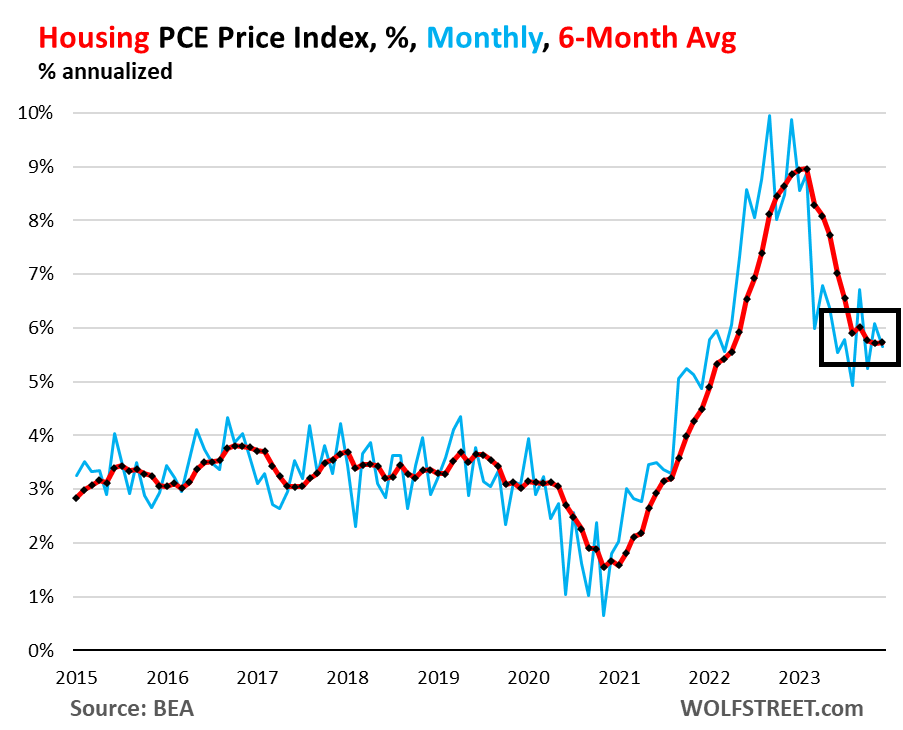

Housing inflation, still red hot and not cooling anymore. The PCE price index for housing rose by 0.46% in December from November and has been in this range since March, after the sharp slowdown early in 2023. This amounts to 5.7% annualized (blue in the chart below).

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings; imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings. It’s the largest component of core services.

The six-month moving average annualized, which shows the more recent trends, also rose by 5.7% in December, and has been in the same range since August (red).

So it looks like the PCE price index for housing has gotten stuck at 5.7%. This stubborn inflation in housing is a blow to theories trotted out for 18 months that housing was lagging, and that we know it will go away as an issue, etc., etc. The increases are less hot than they had been, but remain hot and have become persistent.

The major categories of core services in the PCE price index, as a six-month average of month-to-month changes, annualized:

| Core services, major categories, 6-month average, annualized | ||

| Housing | 5.7% | Description and chart above |

| Non-energy utilities | 2.5% | Water, sewer, trash |

| Health care | 2.5% | Physicians, outpatient, hospital, nursing care, dental, etc. |

| Transportation services | 6.1% | Auto repair & maintenance, auto leasing & rentals, public transportation, airfares, etc. |

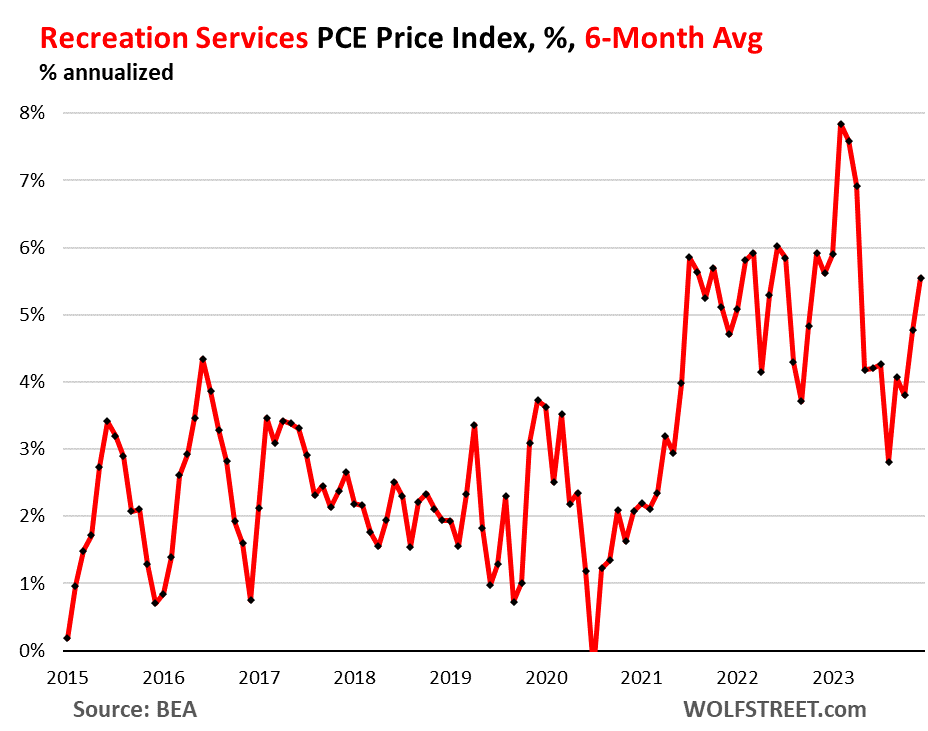

| Recreation services | 5.6% | Concerts, sports, movies, gambling, streaming, vet services, package tours, etc. |

| Food services, accommodation | 2.8% | Meals & drinks at restaurants, bars, schools, cafeterias, etc.; accommodation at hotels, motels, schools, etc. |

| Financial services | 3.5% | Fees & commissions at banks, brokers, funds, portfolio management, etc. |

| Insurance | 2.8% | Insurance of all kinds, including health insurance |

| Other services | 0.1% | Collection of other services |

Inflation in Transportation services and Recreation services is accelerating on the basis of the 6-month moving average, with the PCE price index for Transportation services rising by 6.1%, and the index for Recreation services rising by 5.6%:

![]()

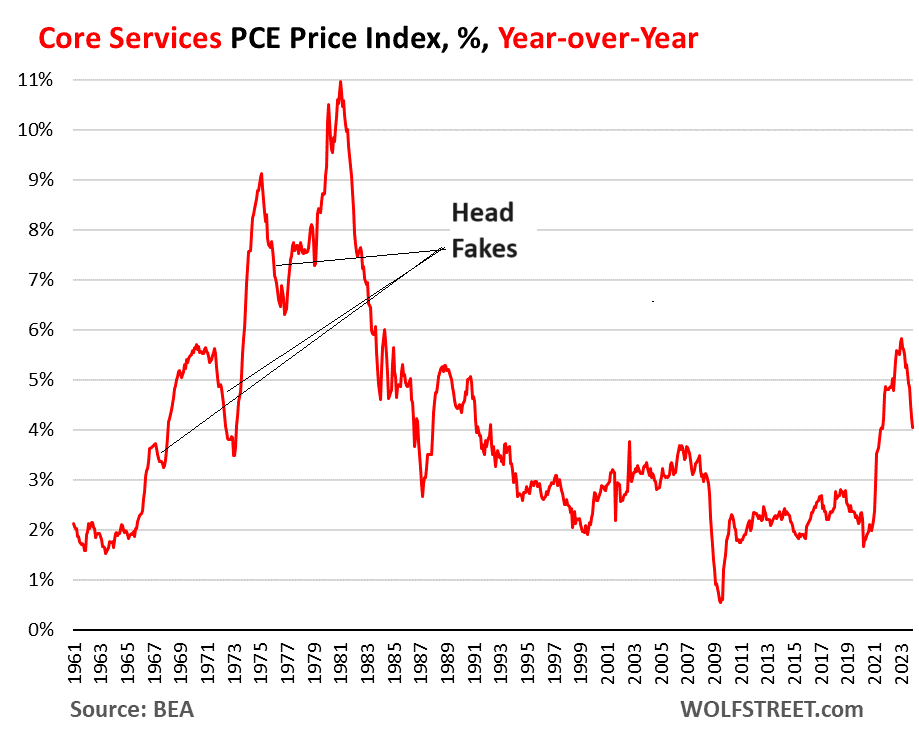

The head-fakes last time.

Inflation in services turns out to be tough to beat, and it can dish up big head-fakes. Last time we had this type of surge of inflation, so that was in the 1970s and 1980s, we thought repeatedly that we had inflation licked, only to find out that we’d fallen for an inflation head-fake. There were three head-fakes in core services on the way to the peak of 11% in 1981:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Jerome Powell said he would use all the tools available and now the Federal Reserve consensus is wait and see. When the Federal Reserve was actually doing something, wait and see is doing nothing; however, apparently the Federal Reserve feels that not actively debasing the currency (Quantitative Easing) is something the Fed should be applauded for.

Wait and see in terms of cutting rates. So yes, doing nothing in terms of cutting rates.

The Fed is at 5.5% and QT. The Fed is doing a lot, with overall PCE at 2.6% and core PCE at 2.9%.

In the last 6 months, reserves are up by about $350 billion and assets are down by just over $500 billion. (and the total assets chart appears to be flattening?) The Fed’s QT seems awfully benign lately. I tend to agree that they are setting themselves up for an unpleasant surprise based on your article today.

Why do I hafta waste my time with this stupid stuff?

RRPs plunged to $570 billion, including by $70 billion over the past two days, and by $1.8 trillion over the past 12 months, and some of that cash wandered over to reserves. Everyone knows that, except you. I explained it here:

https://wolfstreet.com/2024/01/19/feds-balance-sheet-qt-liabilities-rrps-1-78-trillion-from-peak-to-590-billion-but-reserves-rise-to-3-6-trillion-as-liquidity-drains-and-shifts/

Reserves are a liability, not assets. Same as RRPs. Cash wanders from one to the other via the financial markets and the banks, on the same side of the balance sheet, and the flow has no impact on the size of the balance sheet because both are liabilities.

The BTFP got arbitraged by banks until the Fed closed the loophole on Wednesday. Until then, the BTFP increased, and the amounts borrowed ended up in Reserves as part of the arbitrage. READ THIS:

https://wolfstreet.com/2024/01/24/effective-immediately-fed-shuts-down-arbitrage-opportunity-with-the-bank-term-funding-program-btfp/

Over the past 6 months, total assets dropped by $566 billion, not including yet the big Treasury runoff on Jan 31 (they run off on the 15th and end of month). With the end-of-month runoff, it’ll be closer to $600 billion. Which is close to $100 billion a month, which is over the $90 a month cap.

And dropping though may stall

Any thoughts on why housing is so sticky? With rent increases going away one would think drops would continue, not stay up tgere.

The simple answer is because inflation. More money == more people with money to buy things. So housing is a thing to buy.

Money inflation has its pragmatic effects, where’s the productivity of things that are pricey that the cure for high prices is…high prices, you’d think building more housing would come into play-takes some time but…

Statically, the rate of price inflation may be twice the benchmark of 3.5 at 7 pct the upper bound of the 1.96 standard deviation of the expected response, maybe yes and maybe, no.

Hardly a rousing celebration of the success of an inflation slayer Fed, that turned out to be the cause of the whole thing !

Activist monetary policy in support of the banks, whatever it takes. No law was ever meant to apply to the aristocracy that was about to lose their shirts, an anal puckering experience for sure.

Capitalism, as a notion, is normally distributed. Not a profound dictum by either party whose Congressional representative is actually a paid lobbyist for someone. DC ain’t a virgin.

The mainstream media were clapping like seals. The usual puff pieces without any nuance. I don’t think I’ve ever seen one article in the mainstream media that points out that the cumulative inflation since 2020 has been 25% (according to the CPI). That prices will never go back down; that they will just increases more slowly (for now at least).

“That prices will never go back down”

That’s wrong. Fuel prices have already plunged, and durable goods prices have come down a lot, with used vehicle prices in a historic tailspin.

What’s not coming down are prices of services.

Tailspin? Second chart above. It’s a long way to 140. Its a seven year timeframe and remarkably stable for the first half.

Yes they’re making progress with QT. You’ve taught me that. But 2.9 is 40% above the target of two.

I’m still learning.

With housing, rental increases are generally staggered based on lease expirations. Let’s say the market rent increased 6%. It is true these increases persist each month but do we say the renewals last month increased 6% so this percentage is still a current gauge?

It doesn’t work that way. These rental surveys go by address of the dwelling.

The Census Bureau (which does those surveys) has a large pool of randomly selected addresses in its housing survey pool that stays the same over time (with some replacements). Let’s assume there are 100,000 rental units in this pool of addresses, and each address receives a survey every six months on a rotating basis, and whoever lives in this units at that time has to fill them out with the current rent. Then the Census Bureau compares this to the rent data of the same unit on the prior survey six month ago, and to the prior figure 12 months ago, etc. and so they get actual rents paid by actual tenants over time.

With rent-controlled units, there may not be a lot of rent increases. But when the tenant that paid $1,500 leaves, and the unit is then rented out to a new tenant at market rent for $2,000, the new tenant then ends up getting the survey a few months later, and they’ll put in the rent they pay, and the data then picks that up.

So it picks up actual rents paid by tenants in the same units over time. Since this is a very large survey of lots of addresses, the process is pretty smooth. This is very good rent data, the best we have.

Do you think they will ever hit 2018 prices again or is this a new normal? CPI on durable goods are painful!

Durable goods are a mixed bag, in terms of inflation:

The norm for consumer electronics is to get cheaper AND better. That has always been that way. For the last 30 years, furniture has gotten cheaper, but not necessarily better. It used to be well-made US couches, now it’s couches put together somewhere else by cheap labor. New cars get better but more expensive as a rule. Used car prices can fall, but don’t often. This is a historic plunge for used cars, and no, it will not go back to 2018 levels. It might work off 1/2 or maybe 2/3 of the 2020-2021 spike – it already worked off 1/3 of it – and that may be it.

Prior to 2008 you could buy a car battery for around $30-$40 at your local parts store. Today they can be had for roughly $170-$225.

This is the kind of BS about inflation that kills me. People lie with anecdotal examples.

You can buy a battery at Walmart online right now for $69. The most expensive one is $179. Napa sells batteries for $133. Lots of batteries advertised below $100 today.

In 2008, decent batteries were a lot more expensive than $30. That’s just more BS from you.

Back in the early 1990s, we were selling Motorcraft batteries at our W/D at wholesale price for more than you imagined the retail price was in 2008. That was a nice part of the W/D business. We had a special battery truck (drop-frame and side doors, like a beverage truck) that went around to dealers in the multi-state area to deliver new batteries and pick up old batteries.

I guess the point is that the Fed will NEVER allow deflation in aggregate.

Granted some prices will fall but prices of the overall basket are 18% higher since early 2020.

During the same period Disposable personal income is up 24%. Since this is not per capita, there is no easy way to tell if consumers were better off or worse off

1. Agree with your deflation comment. In my entire life, we only had a few quarters of it.

2. I generally don’t allow links though I sometimes make an exception. So I took out your two links.

3. Here is per-capita disposable income, annual, which what you were looking for but couldn’t find. It increased 7.6% in 2023 from 2022, and by 23.4% after 2019.

4. Here is CPI, as index values. It increased by 19.4% since the end of 2019.

Wage increases will surely keep the CPI increasing.

A lot of wage increases depends on such ephemeral, impossible-to-measure traits as … psychology.

Women, for example, get fewer raises than men because in general they are less confrontational and more fearful of being told no. So they just don’t ask.

My mother passed away on New Year’s Day. I’m gonna go out on a limb and guess that you never met her.

@Halibut,

“My mother passed away on New Year’s Day. I’m gonna go out on a limb and guess that you never met her.”

That’s a good one!!!

The fed still has work to do. Rate hike instead of cut in March?

FED would never ever surprise the market aka their masters by hiking rates no matter what the inflation is.

Do you remember when inflation was at 9% plus, FED did nothing other than parroting transitory word.

Of course, all inflation is transition, goes up and down over time.

“imputed rent for owner-occupied housing”

I found this confusing, and just read the BEA’s factsheet on it.

It seems like the BEA just looks at what similar properties actually do rent for, and then uses this average to calculate the imputed rent for owner-occupied houses.

But: if rents are structurally too low, as I have opined before, then PCE is /understating/ the true cost of the home to the homeowner. Put another way, the homeowner is losing money as a landlord renting to him/herself.

“true cost of the home to the homeowner.”

… is irrelevant because a home is an asset, and assets don’t go into consumer price inflation, which is consumption based (“consumer”). So the BEA and BLS figure housing costs as a service (“Shelter”), and one of the ways to determine the cost of this service is rent. I explained this a gazillion times. That’s how the US figures housing inflation. Note that housing PCE is HOT. It’s not like it’s keeping down overall PCE. So don’t gripe!!!

No disagreement from me about my home purchase not being “consumer spending” like you say. That BEA fact sheet explained exactly the same thing on the 2nd to last page.

But Wolf, I keep thinking about your CS vs OER chart, and the huge divergence between rents and home prices. Sure homes aren’t consumer spending, but overpriced homes are pulling rents up.

You’re right that I shouldn’t gripe – I was lucky enough to lock in a 2.7% mortgage. But all the new homeowners aren’t so lucky.

But I think I see your point: existing homeowners aren’t (yet) getting squeezed, but new buyers will be from higher prop taxes, mortgage interest etc. And that will eventually/continue to be captured in PCE housing as rents are pulled up by home prices.

Look at that chart for the period of the Housing Bust: Home prices PLUNGED and OER continued to rise.

Now OER is rising a lot faster than home prices.

What’s you’re problem?

The problem is the lag. The Fed doesn’t factor in home price inflation as it occurs, so it does ZIRP for six years thinking there is no inflation. When inflation in OER starts to show up, home prices may actually be falling.

I believe the current approach to shelter inflation understates it overall and leads to timing problems as well.

It’s not a black white issue, and the results have not been good for prospective home buyers.

No problem at all. Just thinking (typing?) out loud.

Thanks for all you do.

Is what you call core services from line 14, table 2.8.4 in the NIPAs?

I don’t use that table. It’s line 376 in the table I use.

I miss LBO (Left Business Observer for the audience)! But this is a great reminder for me to check out the radio show, which I haven’t listened to in far too long.

No rate cuts unless employment weakens with inflation stubbornly sticky.

Housing is becoming a big enough problem that Washington and various states are probably going to have to act.

Markets can’t do anything about the housing problem. In fact, as long as the economy is strong I think they will exasperate the problem.

Good. As long as they don’t exacerbate the problem.

From 2023 to 2024 (1 year) my car insurance went up 28.2%. GEICO, North Carolina. Honda CRV and Accord. Clean record, no accidents, tickets or claims. 72 yo.

I call that inflation!

The CPI for auto insurance is 21%.

You have to wonder with Car Insurance inflation so out of whack if there is some collusion between these insurance companies? With the legal requirement to have car insurance in every state I would think some State AG Offices would take a look at this.

That is high but costs have gone up for repairs and of course if car is totalled. I was an idiot and backed into a pole and had to have fender and tailgate outside panel replaced. Almost 8K although only $500 on deductible. Parts cost very little but labor was massive. Not sure what deals insurance companies work out with auto shops but 1/3 of the price of the car when new to do simple non structural repairs.

I believe Car insurance companies claim they lost $33B in auto policies last year or so. But hey, I also buy Florida property and hurricane insurance so…yikes.

Why wouldn’t any company be holding the pedal to the metal right now? It’s what business is about, pushing up the profit margin in any way possible, especially corporations. This time is the best opportunity in years to make an extra buck if you’re in the right position to do so.

Insurance is a captive area of our lives we have no choice but to pay. More money from you is more money for the giants to play the markets and buy back stock, have you noticed the Dow, 500, and Naz lately? Besides, the FED and Congress salute and support such over-achievement of our darling corporations.

Among the reasons for the surging auto insurance premiums are the soaring repair costs and the replacement costs that have exploded. Our vehicle was totaled last fall, and we saw this first hand. Just stunning — the amount we received for our car. Also stunning that the vehicle repair costs were so high that they exceeded 80% of the value of the 2018 vehicle, so that the adjusted totaled the vehicle (it was rear-ended). Used vehicle prices exploded by 60% in two years. That’s a cost increase for insurance companies. Repair costs must have increased by 30% and they continue to increase.

The other reason is that the inflationary mindset had kicked off, and consumers were willing to pay those insurance premiums, at least initially, and insurance companies got away with raising them. That’s the core of inflation. That’s why it’s so hard to get services inflation to come down.

New high tech cars are made to be expensive to repair. It’s almost a joke there are so many sensors and self-braking, self-driving features that I can’t see any sane person trusting with their lives.

So you lose on the car price, long term repairs and now insurance. But I do think all the insurance companies see the word ‘inflation’ in the headlines and think they can get anything they want.

For those of you who don’t know, the insurance prices are regulated by state boards. Your rate increase will depend on how corrupt your local board is.

Insurance costs are a function of replacement costs, so if the car prices suddenly rise, you’ll have a follow on of rise in insurance. Same with homes.

I wonder what component of it is related to the increasing cost of disasters, with insurers bailing out of the property markets in Florida and California etc. Yeah crashes are expensive but you flood a city and that’s a lot of cars underwater. If I were an insurer in CA I would be stashing away all the money I could get.

I’m going through a personal injury insurance claim right now with Geico insurance company. These people are so clueless and incompetent it is no wonder insurance rates are skyrockiting. The claim adjuster forced me to have the medical providers go through my Personal Injury Protection coverage vs my Blue Cross Health insurance. Result: they paid out 400% more for the same medical claims. No one beneifited from this, and they used up my $5,000 and now have to pay medical expenses out of pocket.

Perhaps my 28% increase is also because I am now a higher risk due to my age. Anyway I dropped collision on the 2012 Accord, increased the deductible to $1000 on the 2017 CRV, and cut the uninsured motorist to the NC minimum of $50K. This offsets my premium increase, plus a little more (Deflation 😂😂😂). But of course I have less insurance.

Doubtful it’s due to your age. Everyone I know (all age groups) are seeing massive increases such as your 28% and some even more.

Yes, insurance is complicated. For example, people always forget that health insurance gets more expensive as you get older. That includes employee portion of group insurance at work. When the premium rises because you get older, that’s not inflation. That’s the effect of you getting older. And those age-related increases can be big, especially if they’re done every 5 years. My wife’s insurance at work switched the age thresholds to every two years to make the premium increases easier to swallow.

I lived abroad for a year and a half. Signed up for insurance short term when I just recently came back state side and before (until mid 2022) I was paying like $80 a month full coverage on a 2011 Tacoma. After I came back near the end of last year, it was like $110 for what is essentially liability on the same vehicle. Both times in Arizona.

I just recently moved to Florida and for that same liability policy on the same vehicle they wanted like $1100 over 6 months.

It’s gotten pretty crazy. I’m 42 with a clean driving record and only one not at fault accident back in 2010.

One of the reasons insurance rates have gone up is the shear ignorance of claims adjusters working for these companies. They are complete morons. I recently had an accident related insurance medical bill which was just pd for $800 by Geico which could have been only $179 if they had used my preferred provider negotiated rate. They refused to pay the lower rate and shelled out the $800 for no reason. The provider was salivating over getting 400% more than the customary and reasonable charges. My junkyard dog lawyer told me, “who cares, don;t worry about it”, you didn’t have to pay it. The ins company did. F$ck em.

Credit card and auto loan delinquencies accelerating.

Let them eat cake.

NVDA price to sales now almost 34.

If NVDA had a patent on AI, it might be worth a quarter of that. But that is not the case.

Our kindred spirt, Sam Zell RIP, noted in the Spring of 2000, that Cisco was a great company, but there was no way that in his lifetime it would be worth that. Twenty four years later it has never regained that valuation.

Wolf Richter has consistently dispensed wisdom, tolerant of dissent, and intolerant of misinformation.

Why did Elon Musk buy Twitter? In the stock market, the sizzle is always better than the steak. He knew TSLA would someday just be valued as an automobile manufacturer. That day is arriving quickly.

I made a wrong comment here about my auto insurance inflation.

I said 80% but it is: 50%.

I got renewal notice with 50% increase, Farmers.

It’s a strange thing. Three years ago I left USAA for Geico in search of lower rates. Each year since then Geico raised their rates until this year they were going to jump $80 a month! In the meantime USAA’s rates had not gone up very much and were now $50 a month cheaper than Geico. So I went back to USAA again.

Escierto

Same here. I went to Gieco after USAA screwed up a major claim. Now I had to use Geico for a hit & run accident with bodily injury. They have screwed this claim up so bad I had to hire a lawyer and sue them. They are without a doubt the most worthless bunch of gangsters , masquerading as an insurance company. I canceled my insurance with them and went back to USAA.

My experience with Geico as well is they continually jacked the rates up after each renewable period. After the third time I had enough.

I Shop insurance every year, without fail. The ‘Loyalty Tax’ is a stupid thing to pay. I have fun doing it and they hate it when you ring back and say XYZ insurance has this bottom line with one windscreen replacement thrown in, if you can beat it I’ll stay loyal :)

There are few places you can get a discount for good behaviour, Insurance is one.

This probably has to do with car prices going up so much in value. Replacing a wrecked car never cost so much.

So my Geico did go up a fair amount. On the other hand, I checked with another auto insurance provider to see if I can get better deals, and they quoted by 2.5x my current rate!

It’s not the premiums you should be concerned solely about. It’s the service you get after an accident, especially one where you were not at fault. I went to Geico last year because of the poor service from USAA on a homeowners claim. What a big mistake! I am now paying a heavy price for this decision. Geico has literally screwed up every aspect of the claim process. The rental car, the fraudulent appraisal of my totaled car, and now the payment of medical expenses. The person that hit us was a physician, and took off (hit & run), also had Geico insurance. I had to hire a junkyard dog lawyer to sue both my Geico insurance company and the at fault driver’s Geico insurance. My lawyer also has Geico insurance. Looks like I’ve lost this case before I’ve even got started.

The US is on an island as far as GDP growth right now. I think the economic softening in the rest of the world is driving down the commodities and goods prices.

The SPRs Strategic Petroleum Reserves) of US, India and China are precarious. China is about to start filling. India has deferred for now. When US and India start topping up ,Crude will rise like anything. Then Inflation….Commodities etc.

Does the US really need to manage strategic reserves when is a world leader in production?

Fascinating head fake chart, thank you, Wolf. Lots of policy mistakes and geopolitical messes in the 70s–the end of Bretton Woods, Nixon’s pressuring of Burns to engage in easy money practices, then the Oil Embargos, and after a while, consumers become resigned to an inflationary mindset, so past price increases get baked in.

The easy money era this time lasted a lot longer, over 15 years. And now it looks like with the drunken sailors continuing to splurge, an inflationary mindset may be baking consumer’s brains again. I hope the current fed has learned a thing or two recently.

Seems clear the Fed will hold for now. Doesn’t appear any benefit to raising rates and could have the opposite affect. Lowering rates obviously a bad thing right now as well as almost no upside. Steady as she goes and hope it continues as enjoying the short term treasury rates right now.

Lot of minimum wage increases coming up so likely some small price increases but also higher earnings so perhaps some rent relief on the lower end.

People like 3%?

Twenty years of 3% takes 70% off the dollar!

Stable prices?

You need to get pay raises that exceed 3%; and you need earn a return on your assets that exceeds 3%.

Back in the day in the 1970s and 1980s inflation was a LOT worse. See the head-fakes chart at the bottom of the article. People just aren’t used to inflation anymore.

There should be ZERO inflation. “Stable prices” means “stable.” They’re running a scam.

I’m starting to move away from the term inflation now like this 2% target inflation term that is used by the Fed. Now I prefer it as targeting 2% currency devaluation per year. When said that way, it’s obvious to me it should be 0%.

There is a reason a low inflation is targeted. Ignorant people don’t bother to learn the “why”… and the “why” is that deflation is self-reinforcing and leads to repetitive economic depressions.

Instead of complaining about a benign inflation level, why not just convert your hoard of idle cash into a productive asset or at least a real asset? Anyone who invested in stable businesses or real estate is doing fine despite the last 20-50-100 years of inflation.

The “commoditization” of the housing market, post GFC was spurred by multiple factors.

Housing touted (again) as a “cheap asset class” beginning near the 2011/2012 bottom,

The ABnB effect, private equity/ REIT landlord (become a landlord for $10/ share with 10% divy),

Pandemic induced refi blitz and tight fisted boomers not wanting to “miss the top” either asking too much to sell or resigning to (record high) the LTR rental market….

SO many factors propping up this corner of the market, all with no major structural downturn in sight.

Even if the “price” of a house goes down, those who will qualify to buy in a higher rate environment (amid whatever may cause the price drip) will probably be more in the “landlord class” than the occupant.

Blessed to have a mortgage/ missed a refi at 1% (based on credit restructuring)… but can afford my sub-4% 30-yr fixed with decent/ steady income.

I know people who pay the same as me for 1/3 the space, renting.

Wolf,

Thanks, as always, for keeping it real…and a fantastic ‘head fake’ chart that puts this report into proper perspective.

With existing home sales frozen and new home sales enabled only by builders’ capacity to offer rate buydowns, appears that rent inflation will remain elevated for years to come. Am I missing something?

Another ‘unintended consequence’ of QE…hardly. Entirely intended at the outset.

Headline CPI just getting warmed up for its second wave.

Fed members have been talking about lowering QT. Wolf, do you think these numbers give them room this month?

What kind of BS are you fantasizing about?

Damn, another keyboard splattered with coffee…:-)

I love this place, but it does cost me keyboards occasionally…

Yeah, but keyboards are cheap.

:-)

coffee, on the other hand….☝🏻☕⬆️💲

…keyboard + coffee sales yielding a ‘cafe spray’ index?

may we all find a better day.

I do hope it was BS but it was mentioned by former Fed members, which one I forgot, that QT might be slowed and eventually stop sometime this year. It is against what I heard from Powel that QT will continue even if target funding rate is lowered.

If you believe QT will continue, what level do you think the Fed balance will drop to? Will it be lower than the level before 2009 or just 2019?

This was the question I replied to: “do you think these numbers give them room this month?” This month = January meeting = NEXT WEEK

Read the effing comment.

Crude oil is approaching $80 barrel. Look for gas prices to go up very soon. My “gas station from hell” never lowered prices when crude dropped $15/BARREL. Still posting $4.79 for regular.

$2.39/gal. today with Maveric discount card and price locating app – varies by 30-40 cents within 2 miles. It pays to really shop around.

Move gas stations, I never encourage greed !

My local was the same and when I asked the owner why he was 20% over the others he lit a cigarette and said ‘Son, its 20 miles to the nearest cheap fuel and you know getting there and back is 40 miles and that has costs’

I said, Sir you have a valid argument and never stopped there again.

I think this “generative AI” is going to give a productivity boost in 2024 that will reduce inflationary pressures due to labor shortages. It may not reverse the situation, but could attenuate upward pressures on wages.

Ah ha! This may explain what I am seeing. “Red hot” indeed Wolf!

Services and housing inflation will drop with hard times. Oil (and cost of goods/food w/shipping) will rise with war. MIC is laying off people, ha. Head fake. We are in the calm before the storm -imho.

While the Fed says it will drive it decisions on the numbers not clear what that criteria will be. Not all numbers are created equal and numbers within those numbers aren’t either as some hit harder on low income groups more than others. Clearly shelter is a huge issue as well as some other service areas while some of the other areas can be better managed with better budgeting.

I’m not suggesting there is a hidden agenda nor even reading tea leaves, simply that is a complex and partly subjective process of which there are no magic mirrors. Along with the numbers Wolf provides along with the dissection of Fed minutes is as good as it gets.

“Housing Stuck at 5.7% for Six Months”

Sell the f***ing MBS off the balance sheet, Powell, you punk.

I remember in the 1970s when President Ford was struggling with bad PR about raging inflation. He had buttons printed up saying WIN, meaning Whip Inflation Now. But when worn upside down, they said NIM which Ford’s detractors said meant No Instant Miracles.

We did get some fantastic toasters and small appliances when the S&Ls were filing it out for business back then.

“Fighting” it out for business

FWIW. i have no opinion on the following but it is interesting

I watched some videos on the Wharton Business college youtube channel. Jeremy Siegel and Susan Watcher claim the Fed has inflation under control. Seigel is actually worried that GDP growth will keep dropping from 4,9% in 3q23, 3.3% in 4q23, and he thinks we may hit 1% in 1q24. He thinks the economy is slowing. He says the Fed messed up by keeping it low to long and says they need to cut soon to not hold it high for too long. Sure, He said there are some sectors that have high inflation still but they should not try to squash every metric to 2% because it could cause a recession He said he is hearing disturbing antidotal employment info. ( i am guessing this is info is not from the FED data sources lol)

Susan’s opinion was interesting too. She thinks the 10 year treasury will drop and thus mortgages will drop to high 5ish or low 6ish but thinks Home Builders will keep doing buy downs to put mortgages into the 4% range. Her video was published before DH Hortons latest earnings call though were they announced losing money on the buy down program.

So it will be interesting to see how their predictions turn out. After all , they are teaching next generations on economics. There needs to be a website that scores economic predictions.

Siegel is a pathetic Wall Street apologist and shameless shill for the stock market. I don’t lend any credence to anything he says

Einhal,

I somehow knew you’d get this straightened out.

:) He’s as bad as Lawrence Yun. A truly detestable human being.

this guy pulls a 1% number out of his ass? even if true, that is still “growing”

it’s easy to be worried about predictions which are not bound by facts but only by imagination

MW: Intel’s stock sees worst plunge in more than three years: ‘Yet another major reset’

Goldman is on board with rising house prices. Here is a comment from their latest research … released several days ago. Goldman said:

“US home prices are projected to increase 5% this year, up from the previous forecast of 1.9%, Goldman Sachs Research’s Roger Ashworth, senior strategist on the structured credit team, and analyst Vinay Viswanathan write in the team’s report. In 2025, prices are expected to rise 3.7%, compared with the earlier forecast of 2.8%. Those forecasts are underpinned in part by signs of momentum in housing prices.”

You can google this statement to find the rest of Goldman’s latest housing forecast.

🤣 Yes, Goldman would say that, wouldn’t they? They also predicted in January 2022 that the Fed would do only four 25-basis-point hikes in 2022, to only 1%-1.25%, those manipulative morons. No one ever digs up their old bullshit predictions. But I remember some of them, and they’re easy to google.

So here is the one from Jan 2022, about the four rate hikes of 25 basis points each in 2022 (CNBC):

Goldman Sachs…. remember the famous quote re “Doing God’s Work”. 😂😂💸💸

So housing continues for the 6th month to be the only leg of the inflation stool. Median new home price has fallen 17% since peak, rent growth below pre COVID trends, but people who have not rented out their own houses believe they will rent for a number–so shelter inflation is high. The shelter inflation data is as unreliable for December 2023 as it was when the number was sub 2% in 2021. But it is all we have and the data is the data. OER is trash.

1. “So housing continues for the 6th month to be the only leg of the inflation stool.”

No, there are other core services of the inflation stool, as pointed out in the article, even with charts here, on PCE inflation. I show even more details in the CPI articles.

2. “The shelter inflation data is as unreliable for December 2023…”

Not it’s not. You just don’t like what it shows (high housing/rent inflation)

3. “OER is trash.”

Not it’s not. You just don’t like what it shows (high housing/rent inflation)

your attitude is if we could just change CPI to where it shows less housing inflation, then inflation would be gone?

I simply wish it was exclusively market based. Inflation was drastically understated early in this hiking cycle compared to real time changes in rents and home sales. We should be able to create better tools in 2023. I am less grumpy about what it shows now than what it showed in 2021 when shelter prices using market data were running very hot. I think we should expect better.

I’m the end, the number is the number over the long term. Doesn’t matter what I think.

The “shelter prices using market data” you mention are “asking rents” and “asking rents” are bullshit fiction as we’ve learned during the pandemic. They’re just landlords wish-lists.

Asking rents are advertised vacant units in the for-rent listings that algos scoop up. Those with rip-off high rents that no one takes just stay in the listings, and the “asking rent” algos pick them up; and those with reasonable rents are taken by tenants, and vanish from the listings, and algos don’t pick them up. So during the pandemic, some landlords got greedy and jacked up their rents, and then the units sat vacant, while reasonably priced units found tenants. When landlords finally gave up playing this game and actually wanted to lease out their vacant units, they cut the asking rends, and then overall asking rents plunged.

“Asking rent” metrics that you like are PURE TRASH. Here is the example of Asking Rents in Newark, NJ, and practically no one fell for it, and people didn’t lease these units, and they just stayed in the listings, while people took the reasonably priced units, which then never made it into the algos. Those crazy landlords then cut their asking rents to get tenants.

And actual rents that tenants actually paid and renewals and new lease signings – this is what the CPI rent index measures – rose at a much smaller rate than asking rents, and kept rising even after asking rents started plunging.

SO here are Newark asking rents during the pandemic, and I trashed them at the time, LOL:

And here is the Zillow national asking rent index with its bullshit rent increases that were just a wishful thinking for landlords, that then had to back off, compared to actual rents paid by actual tenants, tracked by the Rent CPI.

I discussed this a gazillion times, including here:

https://wolfstreet.com/2024/01/11/beneath-the-skin-of-cpi-inflation-december-not-in-the-mood-to-just-go-away/