Armed with income increases that outran inflation by a wide margin in 2023, they continue to splurge, no matter what.

By Wolf Richter for WOLF STREET.

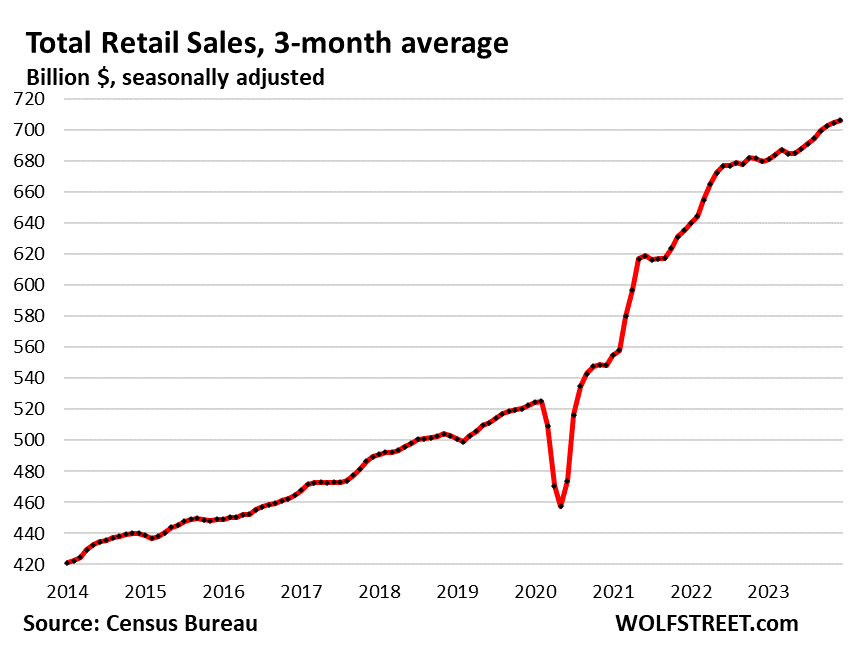

Total retail sales jumped by 0.6% seasonally adjusted in December from November, and by 5.6% year-over-year, to $710 billion. Not seasonally adjusted, retail sales jumped to $771 billion, according to Census Bureau data today.

Despite price drops in many goods that retailers sell. These sales increases come despite price declines across many goods that retailers sell, especially durable goods and gasoline, while inflation has moved solidly into services [We discussed this in detail: Beneath the Skin of CPI Inflation: Not in the Mood to Just Go Away]. So adjusted for the negative inflation rates in many of those goods, retail sales would have jumped even more. This will crop up in the inflation-adjusted consumer spending and GDP data.

Here, for our charts, we’ll use three-month moving averages; they curtail the artificial headline-drama of the monthly squiggles; and they bring out the trends. The three-month moving average of total retail sales rose by 0.2% for the month and by 3.9% from the same period a year ago. Note the slowdown a year ago, and again in the spring of 2023:

Some retailers keep hitting it out of the ballpark, particularly ecommerce and restaurants & bars. Motor vehicle dealers came out pretty good too, as did some other retailers.

But other types of brick-and-mortar retailers are coming off the pandemic bubble, such as Building Materials stores. And others are in permanent decline, such as department stores, furniture stores, and electronics stores: Consumers are buying this stuff now massively online rather than at the brick-and-mortar stores – a phenomenon that has produced what I’ve called since 2016, the Brick-and-Mortar Meltdown, where I’ve documented some of the biggest mall failures and retailer bankruptcies, of which there have been hundreds, from the biggest one (Sears Holding) on down.

Hallmark of our Drunken Sailors.

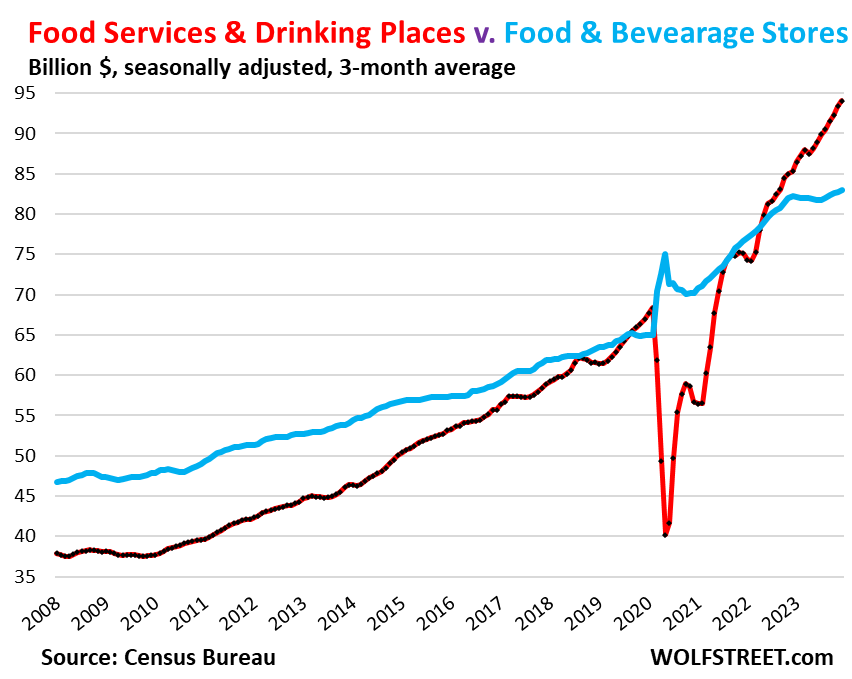

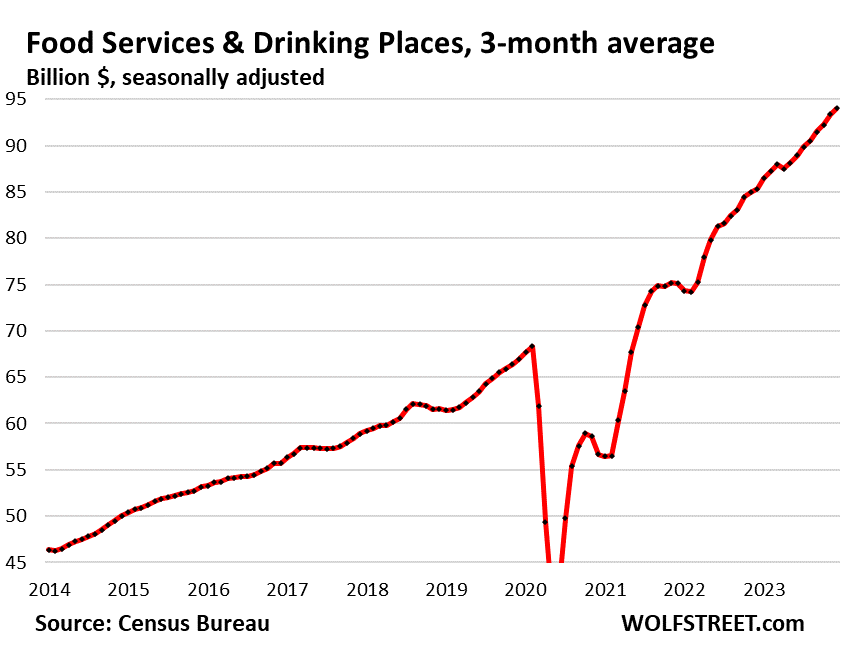

Americans are now spending vastly more money eating and drinking out than at grocery stores; and they’re pushing this trend to the next level, eagerly paying for the “experience” or the convenience. They could save a lot of money by eating at home or packing lunch, but no, our Drunken Sailors – as we’ve come to call them lovingly and facetiously because – gotta have some fun.

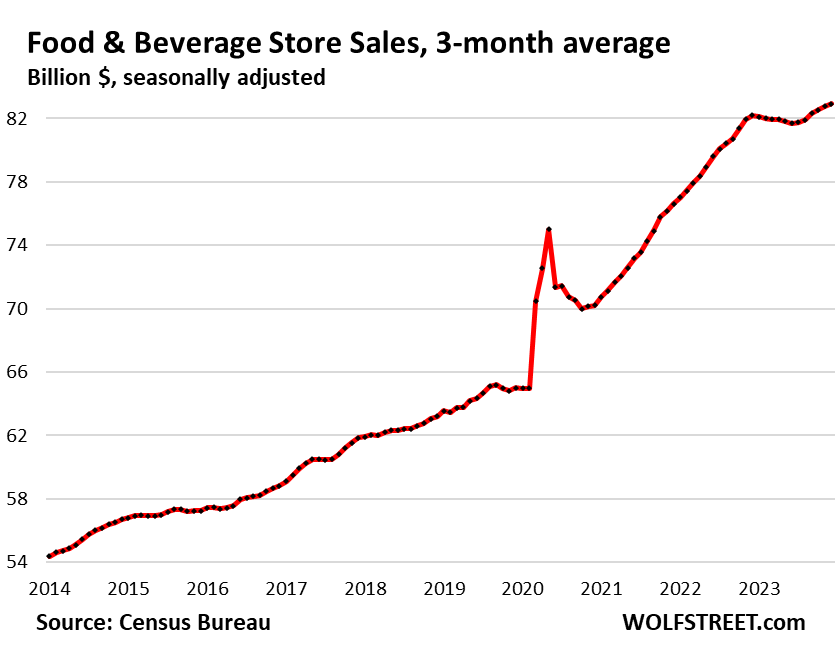

In the chart below, shows sales by “food services and drinking places” (red) and sales by “food and beverage stores” (blue). The amount spent eating and drinking out is astounding, and it keeps shooting higher, even as sales at food and beverage stores have essentially flatlined after the pandemic price-spike ended:

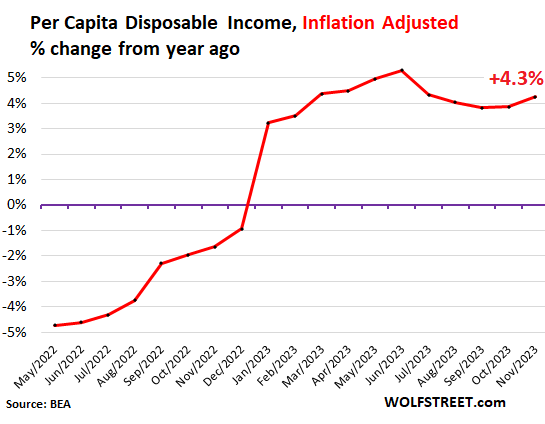

Where does this money come from? Surging real incomes.

Per-capita disposable income, adjusted for inflation (total income from all sources minus payroll taxes, adjusted for inflation), jumped by 4.3% year-over-year. In other words, disposable income is outrunning inflation by 4.3%, after having falling behind inflation in 2021 and 2022.

This surge in real income is what fuels the spending binge. And yet, consumers are still saving part of their income. Maybe they aren’t drunken after all, they’re just earning a lot more money?

Our Drunken Sailors are pushing back against rate-cut mania.

Consumers are in no mood to slow down, very obviously. There is no landing at all. They’re cruising in the stratosphere. They’re earning more than ever, and they’re saving some of it, and they’re blowing the rest, and therefore are continuing to help fuel inflation. They’re heavily leaning against the rate-cut mania that inexplicably broke out on Wall Street in November.

The Fed is watching this nervously. The Fed’s rate cut views – maybe three later this year, it indicated – were all prefaced by, and premised on, inflation going back toward its 2% target. But our Drunken Sailors keep splurging as if they were trying to make sure that inflation will not do that, that it will stay high, and maybe go even higher, so….

Retail sales by major segment of retailers.

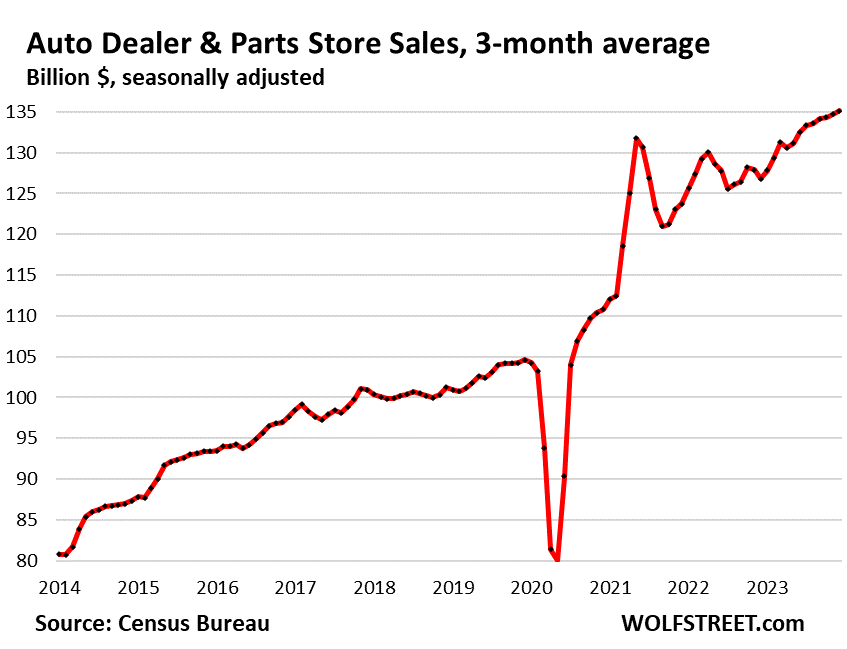

New and Used Vehicle and Parts Dealers (19% of total retail sales):

- Sales: $137 billion

- From prior month: +1.1%

- From prior month, 3mma: +0.3%

- Year-over-year, 3mma: +6.6%

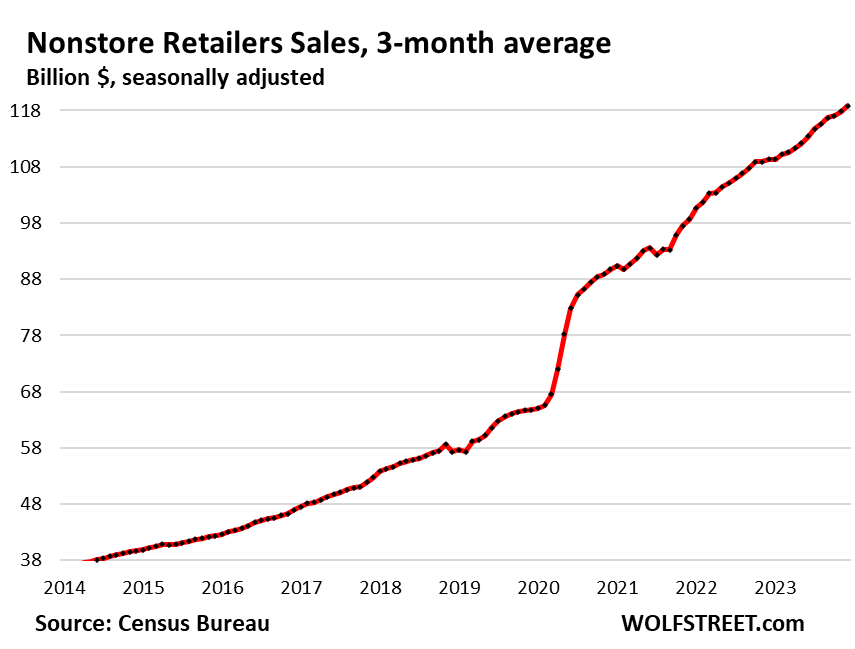

Ecommerce and other “nonstore retailers” (17% of total retail sales), ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $120 billion

- From prior month: +1.5%

- From prior month, 3mma: +0.8%

- Year-over-year, 3mma: +8.7%

Not seasonally adjusted, sales at nonstore retailers ($142 billion) were the #1 category in December, beating by $10 billion the auto dealers ($132 billion not seasonally adjusted).

Bars & restaurants (13% of total retail). Our drunken sailors are splurging at “food services and drinking places,” as they’re called, with 10% year-over-year spending growth, under the motto, YOLO?

- Sales: $95 billion

- From prior month: 0%

- From prior month, 3mma: +0.7%

- Year-over-year, 3mma: +10.2%

Food and Beverage Stores (12% of total retail):

- Sales: $83 billion

- From prior month: +0.2%

- From prior month, 3mma: +0.2%

- Year-over-year, 3mma: +0.9%

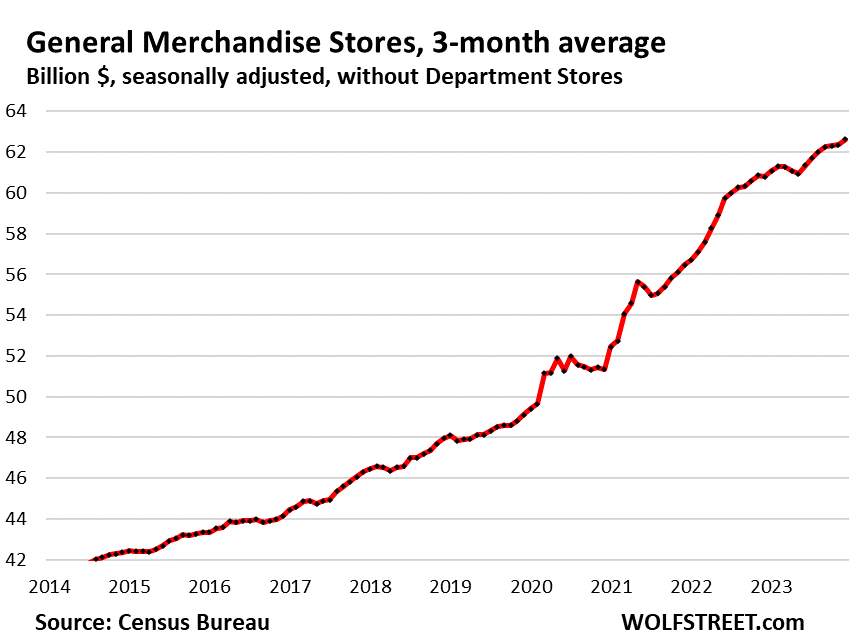

General merchandise stores, without department stores (9% of total retail).

- Sales: $63 billion

- From prior month: +1.0%

- From prior month, 3mma: +0.4%

- Year-over-year, 3mma: +3.0%

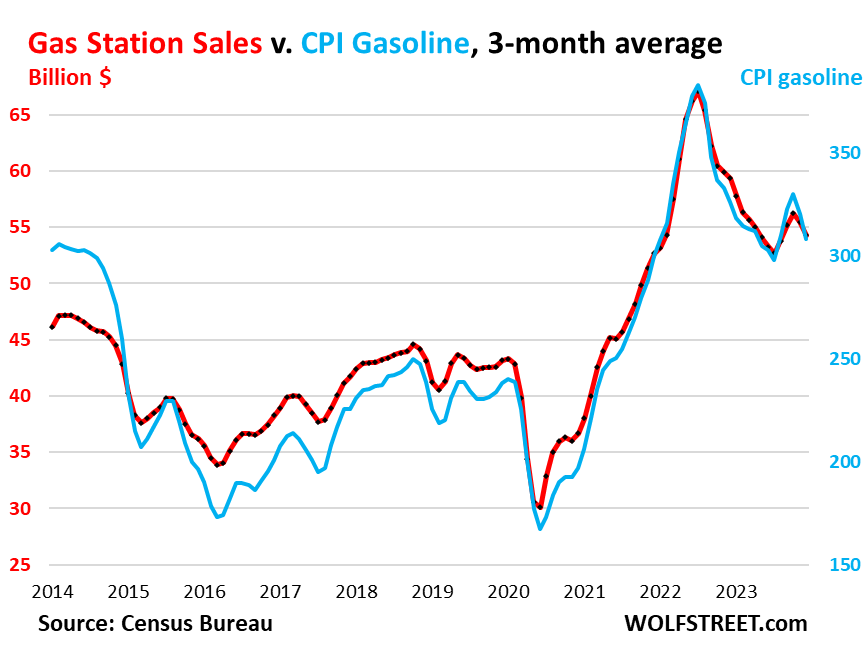

Gas stations (8% of total retail sales). Sales at gas stations move in near-lockstep with the price of gasoline:

- Sales: $53 billion

- From prior month: -1.3%

- From prior month, 3mma: -2.2%

- Year-over-year, 3mma: -8.5%

This chart shows the three-month moving average of the CPI for gasoline (blue, right axis) and sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis):

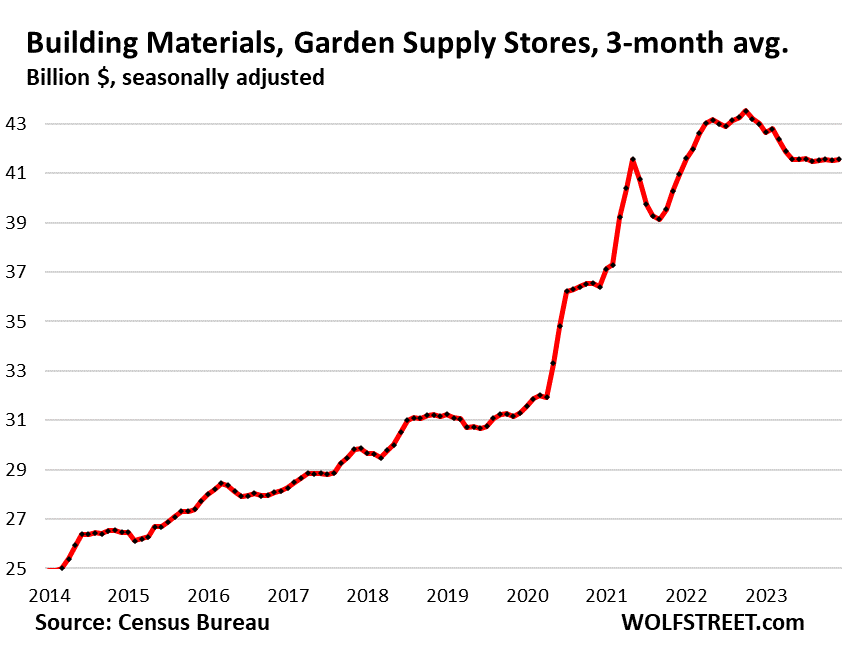

Building materials, garden supply and equipment stores (6% of total retail). Pandemic bubble peaked in October 2022, and then deflated. Since May, sales have been flat:

- Sales: $42 billion

- From prior month: +0.4%

- From prior month, 3mma: +0.1%

- Year-over-year, 3mma: -3.3%

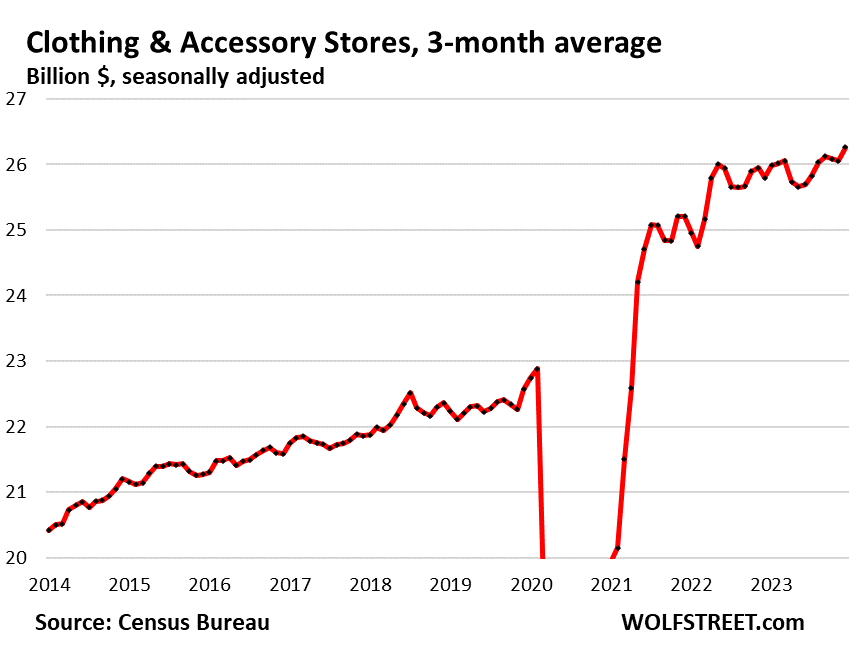

Clothing and accessory stores (3.7% of retail):

- Sales: $27 billion

- From prior month: +1.5%

- From prior month, 3mma: +0.8%

- Year-over-year, 3mma: +1.8%

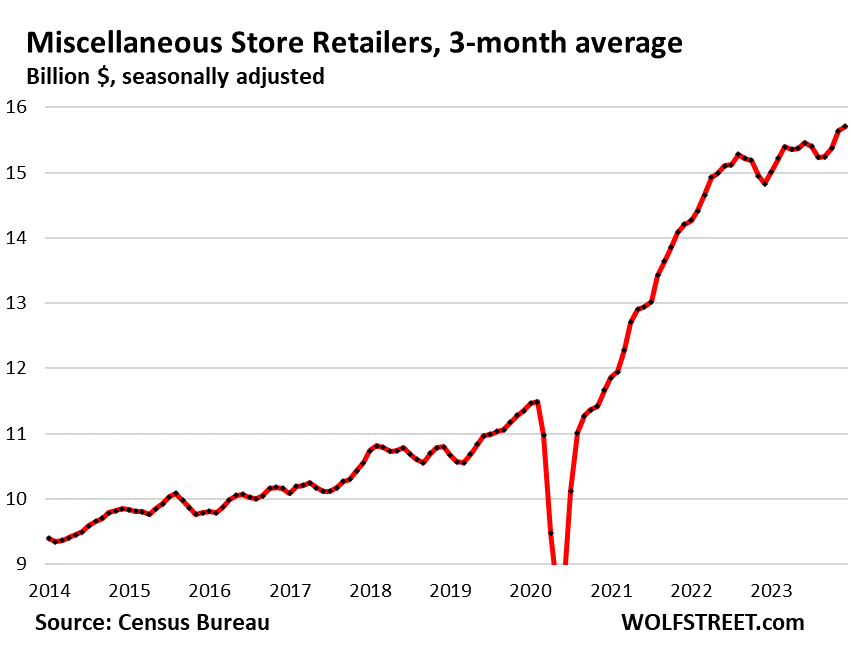

Miscellaneous store retailers (2.2% of total retail): Specialty stores, including cannabis stores.

- Sales: $15.8 billion

- Month over month: +0.7%

- Month over month 3mma: +0.4%

- Year-over-year, 3mma: +5.9%

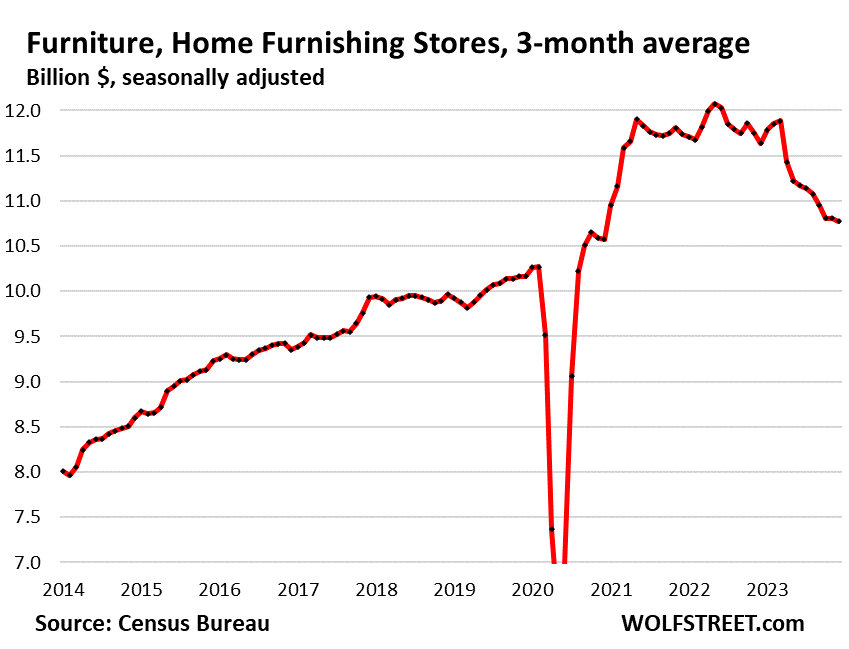

Furniture and home furnishing stores (1.5% of total retail). A big portion of furniture and furnishing sales have moved to ecommerce, where online retailers and platforms dominate. This is what’s left over at brick-and-mortar retailers that specialize in furniture and furnishings:

- Sales: $10.8 billion

- From prior month: -1.0%

- From prior month, 3mma: -0.3%

- Year-over-year, 3mma: -7.4%.

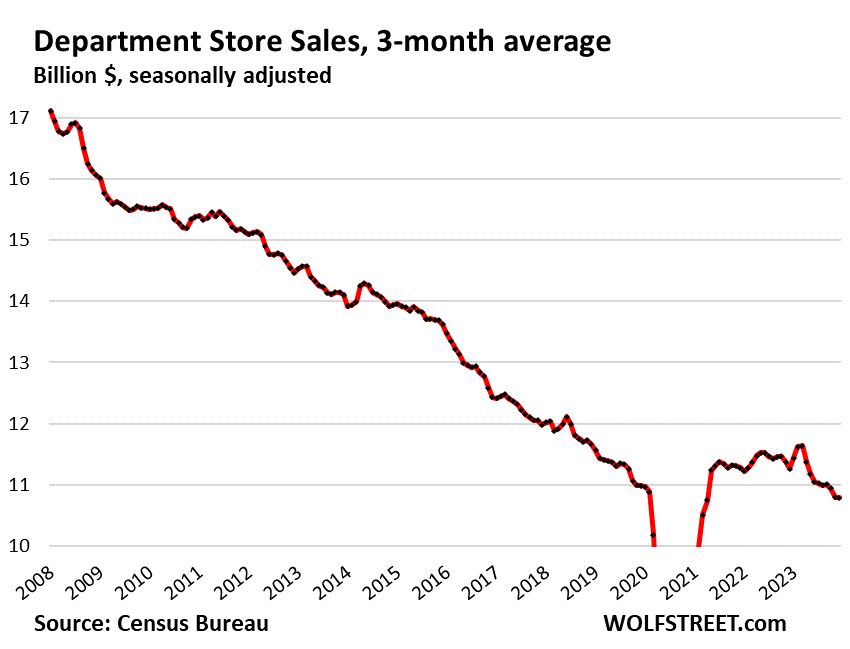

Department stores (now down to just 1.5% of total retail sales, from around 10% in the 1990s). Ecommerce sales by department store chains are not included here, but are included in ecommerce retail sales above.

- Sales: $10.9 billion

- From prior month: +3.0%

- From prior month, 3mma: 0%

- Year-over-year, 3mma: -4.2%

- From peak in 2001: -43% despite 22 years of inflation.

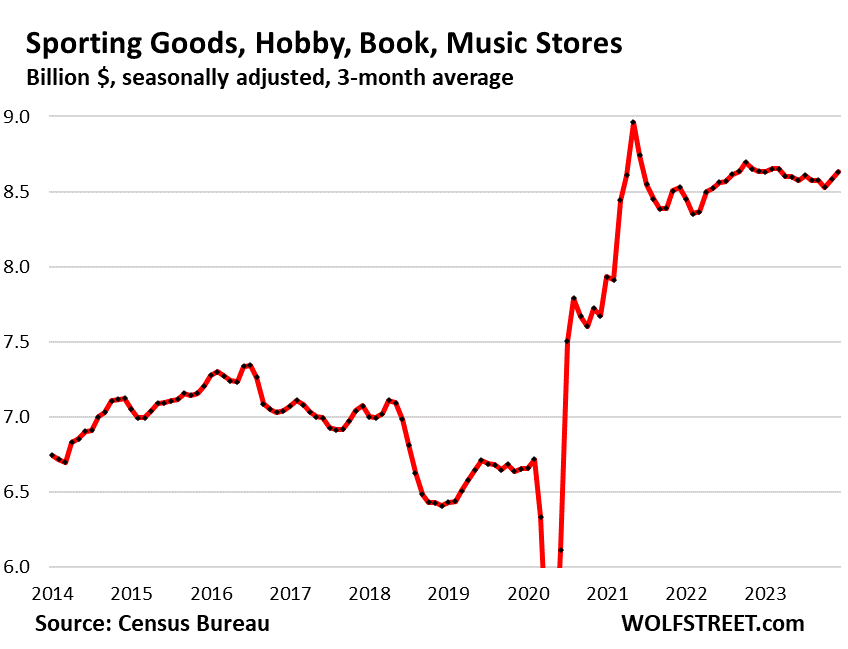

Sporting goods, hobby, book and music stores (1.2% of total retail). This chart is one of the many pandemic specials. Have more people gotten permanently interested in outdoor activities, reversing the pre-pandemic trends?

- Sales: $8.7 billion

- Month over month: +0.3%

- Month over month, 3mma: +0.6%

- Year-over-year, 3mma: 0%.

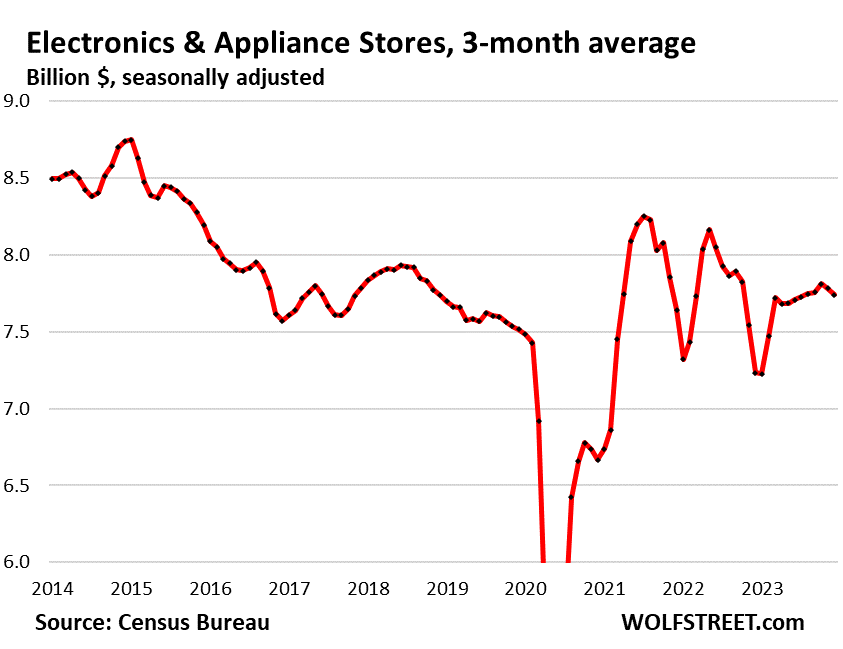

Electronics & appliance stores (1.1% of total retail):

- Sales: $7.7 billion

- Month over month: -0.3%

- Month over month, 3mma: -0.5%

- Year-over-year, 3mma: +7.0%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My plan is working. Spend all your earnings and savings. Then borrow and spend more on what you cant afford.

I will soon have millions of debt slaves at my disposal and my masters would rejoice.

Howdy Mr Powell You certainly have more debt slaves than ever before. ZIRP taught an entire generation not to save $. Along with all the other FED tools used against US, you are doing a fabulous job.

Bernanke destroyed the nonbanks by remunerating interbank demand deposits. This Romulan cloaking device stoked asset prices.

Did you miss the party where Americans disposable income is outrunning inflation?

I’m seeing multi-generation families renting homes

—

we go out to eat every couple weeks

$100+ bill that used to be $60

what we don’t go to are the high priced steak houses

we buy premium steaks and fire up grill instead – still $40

One pattern I’m noticing for all the people complaining about higher prices such as $50 trips to Five Guys and $3.50 bottles of Coke is that they end up buying the products anyway. Because, you know…gotta have it!

Prices will never come back down until enough people both cringe at the sticker shock AND leave it on the shelf.

Ever since the money printing and the lockdowns, it seems like a huge number of products such as houses, restaurants, cars, junk food, etc. have entered a weird economic state where they are neither elastic (demand drops as price goes up) nor inelastic (demand stays the same as price goes up), but rather they are inverse elastic – price goes way up, and demand goes way up along with it.

Somehow I’m certain few missed it but the intercourse of the party in question has been varying to a degree.

Dat’s beaudifo.

I thought this would piss off the FED.

People having money to spend on luxuries is no way to run an economie, surely. This news can’t be good for keeping the polulous under control.

Job losses are what the FED was hoping for to ‘fight’ PRICE-inflation.

The market is giving the finger to the FED’s policies.

It seems to me that the only tool that the FED has mastered so far is jawboning and crawling back and forth on wat was said and/or will be said and/or will be thought off and/or will not be thinking about thinking, let alone talk about thinking about anyting. Creating so much confusion about the direction it is taking that we are coming to the stage where nobody listens to the boy that cried “WOLF”.

That will be the perfect setting for the FED to do what it has to do, because then nobody will pay attention and that’s when policies will work again, at last.

Don’t ask me what the FED will do or will have to do. As i have no clue about anything whatsoever. That’s the good man i am.

I hope i didn’t waste your time to much with saying nothing about anything.

Good article and thanks for the daily splash of cold water on one’s face on a cold morning, aka, the facts.

Since the vitality of the economy of our country is reflected in the ability of the every person to earn enough to spend more, the trends are consistent with joe lunch bucket earning more.

Given the discrepancy between the productivity vs wage hypothesis, the earnings of the labor force is what matters. They can’t spend what they don’t have for long.

MW: 10-year, 30-year Treasury yields hit five-week highs after December retail sales data

The plunge in furniture sales looks very recent to the point that it lines up with the housing market freezing over. Because people tend to buy furniture that matches the new house they just bought?

Sounds right to me, I mean people still buy new furniture for their old place when it gets old or they want to remodel, but moving into a different space is going to be a bigger expense. I’ve also found that at greater distances the move can be cheaper by selling used furniture and buying brand new at destination, depending what kind of belongings you have anyway. Even if the cost is a little higher I can’t see a lot of women passing on the opportunity to remodel for a small price difference😆

Or it may be the first wave of the low sales of housing at the current mortgage rate, ie the monthly payment which doubled with the interest rate. Meanwhile, the owners, stubbornly cling to the concept of extraordinary rewards the world owes them.

Inflated Bubbles are the proverbial land of milk and honey. It is only when they deflate that the foolishness becomes apparent.

“In other words, disposable income is outrunning inflation by 4.3%, after having falling behind inflation in 2021 and 2022.”

I don’t get it. It seems the price level of most retail products rose an average of 20% in the last three years. So a 4.3% , one year rise in income above inflation does not seem all that large. Goods are still more expensive.

My guess is the top 15% earners are driving all this spending. The bottom 85% are cutting back. Drunken sailors = top 15%.

1. No wait a minute. If prices went up 20% over x years, and income adjusted for inflation went up 2% over the same x years, then incomes went up 2% faster than prices, and consumers came out ahead.

That 4.3% you’re referring to is the inflation-adjusted per-capita disposable income gain… it’s ALREADY adjusted for inflation.

2. “My guess is the top 15% earners are driving all this spending. The bottom 85% are cutting back. Drunken sailors = top 15%.”

LOL. You haven’t been paying attention. Income gains were the biggest at the lower levels of jobs. Look at the recent wage agreements with unions — blue-collar workers in factories, airline staff, UPS drivers, etc. Look at the wage gains in lower-level service work… they were forced by labor shortages because people refused to work for the offered wages, and wages had to rise to fill the job openings.

People in the middle class and lower middle class have gotten massive pay increases. In 2021 and 2022, when inflation spiked, they were lagging inflation, chasing after it, in 2023 they’re ahead of inflation. Social Security recipients got 8.7% COLAs for 2023, and they’re spending it. Retirees with some CDs, T-bills, and money market funds are now making 5%-plus on their savings when they made near 0% before. Retirees with $200,000 in T-bills, CDs, or money-market funds (this is NOT a “top 15%” number, LOL) are getting $10,000 a year in interest income for the first time, and they spend some of that. There are about 15 million mom-and-pop landlords in the US, and they’re getting higher rents. This is happening across a very large swath of the US population.

The interesting thing is how folks keep spending like crazy, traveling like crazy, making good money … and yet it feels like 90% of the people in this country do nothing but complain about how terrible things are and how they’re suffering and starving and living lives of abject poverty.

Do we have a mental health pandemic now? The numbers certainly don’t support all the complaining.

People are rightfully pissed off about a lot of stuff. you can see it here in the comments. Every time a price goes up — from OJ to auto insurance — we feel like we’re getting screwed, and it pisses us off. Americans hate, hate, hate inflation, the bad part of inflation (paying higher prices), though they’re not pissed off about the good part of inflation (getting paid more). There are other things that piss people off and have for many years, starting with all the bailout crap that happened starting in 2008. There is a huge long list of this stuff, and different people get pissed off about different things. At the same time, Americans like to work hard and move forward and apply their skills, and learn new stuff, and do new stuff, etc., and they like to make money and spend money. That’s just in our culture. That’s why the economy is doing pretty good, and people are making money and spending money, while they are pissed off about all kinds of important stuff, and there is a lot of anger. I totally see this – including here in the comments.

I forget who explained it…people think the raise they get from inflation is deserved, while the higher cost of living is a ripoff.

Roady, I used agree with that thinking, that only the top was driving the consumption. But it should be obvious at this point that if you are living above the poverty line you are spending on goods and not slowing down. I think we’re still seeing the effects of pandemic related stimulus money whipping the economy into a frenzy. But you have boom/bust industries like houses and autos starting to feel the full effect of the higher interest rates, and if either slows enough to start the layoffs, then who knows where we end up.

Stimulus is long gone,now there spending the the Employee Retention money also ,Inflation Reduction Act .

Flea-

“…stimulus is long gone”

I thought the

– Employee Retention Act and

– Inflation Reduction Act

WERE stimulus designed legislation: both add to the current deficit difficulties, at least in the near term.

Ultimately, doesn’t deficit spending at a multi-Trillion level encourage at least some of the sailors’ spending decisions?

@John H,

Remember every penny of those deficits gets removed from the economy and exchanged for T-bills and T-bonds. It is inflationary in and of itself only when people spend the money on supply constrained products, which was the cause of inflation in the aftermath of COVID when businesses world-wide were shutdown.

As Wolf has explained, the hangover today is in people’s heads, the inflation mindset. People saw inflation after COVID, the media screams about it everyday, and people now expect it and accept it. And corporations are making record profits because they can just increase prices assuming people won’t adjust their behavior.

Kent-

Not sure I agree with you. That there is an ongoing debt inherent in deficit spending is certain. But doesn’t that debt FUND an expense in the present, and don’t the bills carry into the future?

I believe that the programs put in place under the Acts (e.g. climate policy related spending) require ongoing funding, but hope I’m wrong…. please show me otherwise.

Respectfully.

It’s strange that inflation adjusted income is up, but public perception is in the tank. If everyone is making more money, especially those at the lower end, why does it seem like wealth inequality keeps growing exponentially and inflation is killing the poor? Housing continues to show record unaffordability levels. Surveys continue to show people hate this economy, but the data says everything is just fine. Perception vs reality?

Puzzling for sure. People with a high income or frugal habits are prolly fine, but I wonder how it is for families trying to keep up with all the expenses that “good parents” are expected to make (healthy food, utilities, electronics, tuition fees or day care, clothing, sports, vacation, healthcare etc). Real inflation seems higher to me than indices say, and because some costs have gone up overproportionally, a couple of them can quickly punch a hole in a pay check to pay check budget. Is the high spending hiding a binomial distribution, with some saving more and others forced to keep dancing with nothing left for retirement? To find out, one would need to break down the numbers by household type.

can’t wait to get my next property insurance bill

—–

working on summer vacay – gonna need around $7k

retirement – well guess I need to work more in winters

got long list left before summer

gonna spend like drunken sailor pretty soon – have 7 roofs to coat

Because the inflation numbers don’t, in my opinion, adequately give effect to the necessities, so the necessities in life have skyrocketed, and people feel poorer.

No one cares about cheaper LCD TV’s

I think you are making the false assumption that most other people’s “necessities” match your own.

There is a whole young generation growing up who see housing as something temporal and potentially just as much a burden as a goal.

I’m talking about other people, not myself. Do you read the posts to which you’re replying?

Did you ever stop to consider that these young people see housing as temporal as a defense mechanism?

“There is a whole young generation growing up who see housing as something temporal and potentially just as much a burden as a goal.”

Sour grapes…

I read your post and responded to it. You talked about necessities. I responded to that. I am sorry you could not understand what I wrote.

Good luck, it really sounds like you need it.

JimL,

I think you’re defining “housing” too narrowly and only equating it with owning a house. Einhal referenced “necessities” skyrocketing in price and I think housing in some form (owned or rented) is still considered a necessity by the vast majority of people, even the younger generation.

I think Einhal understood what you wrote perfectly well. Unfortunately, you don’t seem to have understood what Einhal wrote.

I think part of it is that people are finally getting real raises after years of relatively stagnant wages…only to see a big chunk of their raises being lost to inflation. They are making up lost ground, but not as fast as they want.

and don’t forget about the higher income taxes you now get to pay

Income brackets are adjusted every year for inflation by the IRS.

I think perceptions can sometimes be deceiving, I base that on my own experience only, but I don’t think the elation we feel when we receive a higher check is proportional to the pain we feel at the checkout counter when the bill is noticeably higher. So unless one does very accurate accounting then I think our perceptions might not always align with reality.

Having said that I for instance live in a very expensive metro, so I think housing costs make up a larger proportion of my expenses than any of the indexes allocate to their baskets. So inflation in that category punches me way harder than it does in the overall CPI or whatever, I mean those indexes are all averages and are not going to apply to all of us equally, if I worked only with people from my region then probably I would be certain that “real” inflation is higher, but I don’t actually know millions of people across my country, only a tiny fraction of that.

Also I noticed people love to complain, virtually everyone I talk to is b*thing about inflation, but I know some of these people well enough to know they’re quite a bit better off this year than they were just a few years ago.

I think housing and cars, two very big ticket items, are the drivers here. My son is a resident MD (meaning he doesn’t make the big bucks yet) in Boston. His 600 sq ft apartment is $3100/mo and it costs him $300 just to park. He wants to buy a new car, but prices are through the roof. All went up in price last year, so he feels inflation.

I paid off my mortgage awhile back and haven’t been in the market for a car for years. I simply changed where I shop for food and I rarely eat out to start with. So I honestly don’t feel any inflation in my budget at all. There are millions like me so there is a big dichotomy in how the average Joe is getting along.

last month I paid off our 1st house mortgage

originated oct ’94

nice having few extra $$ but now I have to save for insurance and taxes

at least we’re now getting close to market rents

I have lots tenants who have stayed put for over 5 years now

accepting our rent increases as we’re still below market

Kent – having a car in Boston is only for the rich.

When I lived in the city (Watertown but commuted to Kenmore) I got myself a little 50cc scooter, which is MUCH more practical for getting around than a full-size car – both in terms of cost and ease of parking.

Because they are worse off on big ticket item affordability — homes and cars. Home ownership is now out of reach for most current renters due to higher prices combined with much higher interest rates. Most renters have to own a car, but they don’t have to own a home, so the car purchase puts home ownership even further out of reach. As a whole, young people who are still renting today without owning have effectively been priced out of home ownership due to the pandemic. Obviously, this does not apply to young people in the top 30% of incomes.

Part of it is perception. There is a whole pseudo-infotainment industry that has grown up that does nothing but prey on its customers fears and spread disinformation. Unfortunately there are lots of people who choose to use these poor sources of information to help shape their views of the world.

Your not talking about Wolfstreet are you??

No. Of course not. He is an excellent source of information. That is why inam here.

I think there are massive differences in individual situations depending on, essentially, luck. We are renting and my wife is in construction which is in a recession (we’re in the UK), so we are getting squeezed like crazy. We’re still fine, but going backwards about 5% a year right now – not a nice feeling. But if we’d bought a house (we almost did) we’d be sitting on a 3% mortgage rate and have loads of spare money. I know people who locked in 1.5% for 10 years after getting big pay rises – they are swimming in cash.

Others I know are still getting decent pay rises, so not really affected either way.

It’s just a huge spread and it mostly comes down to what industry you’re in and whether you locked in a cheap mortgage or not.

It’s just another reason why using monetary policy to control inflation is brain dead. In a sane world the govt would use taxation to pull back spending in the economy so it could target the effects better.

In a sane world, the government would stay out of the markets and never would have done what they did during the pandemic. It was unnecessary, and it has broken many markets, especially housing. Now those 3% mortgage rate holders are stuck in their homes, held hostage by their low rate mortgages. There is nothing healthy about our economy now. It’s a total disaster IMO, created by our irresponsible government and Fed.

Being held hostage by a 3% mortgage is not as bad as you portray it to be.

Stuck in their homes….you mean lucky as F$@$& ?? I agree with the above that everyone would probably be happier if the government stayed out of it and didn’t pick winners and losers. Things would be a lot more balanced if we allowed markets to work and didn’t try to control them like we do. The fed has selected winners and losers and that’s created some bitterness if you’re on the wrong side of the play. In my opinion. For example, if you’re a home shopper right now or a renter, you lose.

Well as the Doors postulated, ” I’ve been down so goddamned long, that it looks like up to me.”

The inequality comparison will have no effect until sales fall. Unfortunately.

A predictably reckless monetary policy based on the non-statistically verified hypothesis excreted by the lunatic, Milton Friedman.

I don’t know. I was in the grocery store yesterday in the freezer aisle and two 20 something-year-old girls next to me were looking at ice cream and commented, omg, I paid three times that much for the same thing yesterday with doordash. Her friend said yeah because it’s doordash. She replied back, but I love doordash! They giggled and walked away. In a couple years, we are going to hear about how the nations youth were victimized by greedy credit card companies extending them credit when they didn’t have the means to pay it back. Then it will be socialized and made part of the debt so that we can All pony up and pay the bill for Gen Z’s doordash.

Meals-On-Wheels delivers for free.

“In a couple years, we are going to hear about how the nations youth were victimized by greedy credit card companies extending them credit when they didn’t have the means to pay it back. Then it will be socialized and made part of the debt so that we can All pony up and pay the bill for Gen Z’s doordash.”

0% chance of this happening Jason. Both situations were made up in your little pea brain

I was on the campus of Belmont University last week and overheard a conversation that was basically the same, and I also listened to middle-aged “friends of friends” talking about the same thing. They ordered groceries and sundries from Instacart and then were shocked that there was a large mark-up on the items, but decided it was worth it so they didn’t have to get out in the cold to buy their wine.

Yeah, what a pea brain. ZERO chance of this happening. What’s next? Student loan forgiveness? Give me a break.

The Drunken Sailors who are spending a lot now are like the grasshopper in the parable. Soon they will be coming to the ant, who was frugal, and asking for aid … and the ant will say no.

No, the Insect Revenue Service will take that money from the ant by force and hand it to the grasshopper.

No, it won’t. The Medical Industrial Complex, backed by PE firms, will do that over the last two years of the ant’s life.

That Wolf, is no joke.

Right on Wolf. Sedentary lifestyles setting us up for a mighty health bill in the near future.

Ironically Wolf I coined ‘medical industrial complex’ earlier today in a conversation with a colleague, weird!

SolomonDreamed,

It’s a great expression. But it has been around for many years. I have used it for a few years. Neither you nor I coined it. It’s very rare that we get to coin an expression.

I’m from Maryland and the number one industry for the state is Healthcare. I’d bet that’s the case for half the country.

Bring back Dr Kevorkian. Most folks would rather skip the last two most miserable years of life if they’re seriously ill. They also happen to be the most expensive and the most stressful on family as well.

We treat our pets better in their last years than we do humans.

In California, the legal exit options have become a lot easier if you still have the wits and strength to sort through it all. Preparation helps a lot too.

I believe our true Drunken Sailors are in Washington DC.

Doesn’t the nearly $2 Trillion Annual Budget Deficit create (directly or indirectly) this strong spending?

And if one assumes that this kind of Deficit spending cannot go on at this pace, isn’t that where the party ends and everyone has to sober up?

This party won’t end for few more decades and there is no perceivable thread to USD.

FED would keep monetizing US Govt Debts if needed.

USD has already lost most of its value in last 2 decades or so.

Inflating away the debt via money printing is the only game in town as of now.

“USD has already lost most of its value in last 2 decades or so”

“Most?” No. But “much” maybe. It lost 40% of its purchasing power over the past 20 years.

A little shocking “Real Disposable Personal Income” saw almost no dip during the great recession. This is income, minus taxes, adjusted for inflation? Large dip in the waning years of covid, likely due to stimulus and covid tax breaks expiring more than drops in income?

Herpderp

You have to remember that oil prices collapsed in 2008, and overall CPI became negative for a few months, then was pretty low for a while and then became negative again briefly. Negative inflation rates have the effect of boosting “real” incomes.

The not-inflation adjusted disposable income actually fell and stayed lower for about a year.

This was not meant to be a reply to this thread. Honestly the reply button confuses me to no end and I often post what I hope is a top thread comment as a reply to some other poster. Im not sure how I manage this. I think if I click reply to a post, then later refresh the page that is somehow cached as where the comment will go.

The dollar losing almost half of its value in 20 years (most of my adult life) should still be pretty darn sobering. You’ve talked about joining medicare recently, so the BLS CPI calculator says the dollar isn’t worth even 1/10th of what is was worth when you were born. You seem like a healthy dude who could go another couple decades… If you and the Fed both play your cards right, you might see a day when the dollar is worth less than your birth year’s penny!

Not Sure,

But it really doesn’t matter to me because I don’t have “dollars” packed under my mattress. My dollars are in assets that are supposed to produce income or capital gains or both. My first job paid $1.75 per hour. A dollar is just a measure that you to measure assets, debts, goods, services, and labor with. That paper dollar in your pocket isn’t really a “dollar,” it’s a Federal Reserve Note — money that the Fed owes you, denominated in that measure. It’s an asset for you that is measured in dollars. It’s a liability for the Fed that is measured in dollars. So for example, a 10-dollar Federal Reserve Note is worth $10 and you can exchange it for something that is also worth $10, and the Fed then owes that dude the $10.

What matters to me is that the value of my labor and assets rises faster than the dollar loses purchasing power.

What is bad is when:

1.) the decline of the dollar’s purchasing power outpaces the increases in the value of labor and assets measured in dollars;

and 2.) when the purchasing power declines so fast that the measure (the currency) becomes useless, which is the case in Argentina, where prices of big-ticket items and services, such as rent, are posted and negotiated in USD and then converted at the time of payment into pesos, which produces all kinds of economic turmoil.

Those two situations are really bad, and they can occur together, and then they’re really really bad. And the whole thing can get out of hand very easily once it starts, and that can be catastrophic economically.

But how much value has the dollar lost compared to other currencies?

It could be worse.

1/11/2024 – Argentina’s annual inflation soared to 211.4% in 2023, the highest rate in 32 years, according to figures released Thursday by the government’s INDEC statistics agency

Buenos Aires very nice place . Lived there in 2018 and 2019. Paid the nanny in usd and maid was getting a raise each week. Inflation before my very eyes . Rent was and still is in USD

Drunken Admirals

Good one, Longstreet!

“We’re all [drunken] Keynesians now”

— bastardization of quote attributed to M. Friedman and used by R. Nixon

Welcome to the new normal…this time is different

That Pow Pow better not be hinting at rate cut in 2024 by the end of this month…

“The Fed is watching this nervously. The Fed’s rate cut views – maybe three later this year, it indicated – were all prefaced by, and premised on, inflation going back toward its 2% target.”

JPowell needs to have a come to Jesus moment. Baring a recession which DOES NOT look in the cards, 2% core PCE inflation is NOWHERE on the horizon. Last week’s 1st-time unemployment claims dipped slightly to $202K.

We’re just one skirmish over in the middle east away from minimum $100 a barrel oil which will push headline CPI back towards 4% if it’s sustained for 3-6 months.

I love your retail sales charts. I wish you could overlay them with inflation adjustment. Thanks. Wolf

For 2023 and late 2022, they would look even better because goods prices have dropped in many of these categories during that time.

But if you adjust retail sales (which are sales of goods) with the overall inflation rate (which is now dominated by inflation in services which retailers don’t sell), you’d be committing intellectual self-immolation.

https://wolfstreet.com/2024/01/11/beneath-the-skin-of-cpi-inflation-december-not-in-the-mood-to-just-go-away/

Food prices largely stabilized after surge:

But services inflation is hot — but retailers don’t sell services, they sell goods:

Wolf, correct me if I’m wrong. I believe it was 1977 when congress mandated the Federal Reserve to not only be charged with price stability but also maximum employment. It was called the dual mandate and it might have been a good idea then but with services now accounting for such a large portion of our GDP, it might make the work of the FED nigh on impossible.

I would love to see your updated chart that shows how much these 5%+ brokered CDs & treasuries are netting the top 40%. They’re the real drunken sailors. The bottom 60% is mostly getting whack-a-moled.

Commenters here are up to the gills with this 5% stuff.

The top 40% have lots of other stuff.

I’m getting really tired of this most-Americans-are-poor BS. People who believe that will never understand the US economy and will always be surprised by it.

I’m guessing – pure speculation – that GuessWhat’s income level is just below the “top 40%” level. There’s an intriguing habit in the modern American to assume that anyone with more income/wealth than himself is slightly less moral than they are. I worked with “high-net-worth” folks for 4 decades, and the trait was universal, at least in my experience.

(Disclosure: ask me who’s rich on my street, and I, too, will point up the street.)

I concluded that this trait was the basis of the “class struggle” and that it irretrievably complicated that struggle. Finger-pointing on wealth is a mine field…

Respectfully.

My math says only the bottom 58% are getting whacked.

I would guess the correlation between one’s percentile income (or wealth) and their belief in where the cutoff is between doing great and getting crushed….is very very high.

Well I hope so. I want my callable 5.5 and 5.7 one years back up there! lol! There is still time.

There are some callable agency bonds with 5.9% coupons and 10-year maturities available right now.

All of them, it seems, are callable, only the most visible defect of the investor light bonds on offer at interest rate that subsidizes the risk.

A 4.3% increase in inflation-adjusted per-capital disposable income is rather large when considered against the average of the last 10 years. I suppose these figures are skewed by the last two years of negative prints. The graph for the last 3 years has so many ups and downs due to the stimulus that it looks like the price of a meme stock.

Yes, the stimulus era was wild in terms of income spike, and then the yoy comparisons were wild too. So I don’t take that chart back this far.

Interest income is an economic engine.

For 12 years all we heard was interest rates being low would propel the economy. But it is really who gets to spend “the imbalance”. With rates low, the government was in the spending mood. With rates more “fair”, the people getting interest income get in the spending mood. Add in near record stock prices and paper gains, one can conclude that 5.25% fed funds really didnt cool off much of anything. And, historically, 5.25% is more normal than abnormally high. Still several Trillion extra floating around in the economy if one looks at the Money Supply trend line established before COVID. IMO

The low interest rates did propel the economy into this economy, struggling to recover from the psychological transition from an era of subsidized risk to a sustainable system,

as hoped for by those guys who took their best shot in the years around 1776.

Howdy Folks. How dare people spend their $ and enjoy life. Bet those old folks that saved $ all their lives and now finally earning interest are spending more than ever before????? Just outrageous behavior of these old people…..

If you need to spend tons of money to “enjoy life,” you’re doing it wrong.

Howdy Einhal. Define tons of money?

My point is that there are plenty of things to get enjoyment out of life with that don’t require spending money.

Our consumerist economy has not made people happier.

Howdy Einhal I cannot speak for others, but spending my hard earned $ makes me very happy. A squirrels life is different I guess……

Well, if the suicide rate in the US is any indication — at something like an 80 year high in 2022 — then it’s not necessarily a fantastical inference that money really can’t buy joy. Americans are better remunerated than they’ve been in decades, but we’re still terrifically miserable.

Woodworking hobbies, collecting LBJ-era hi-if gear, polishing aluminum, chips-n-dips, picnicking on a knoll, hopping in the sack with a gorgeous chick…these are all superior inroads to joy…stockpiling lucre…eh

The ants (inveterate dull-boys with a fetish for toil & amassment) live in abject fear of a bitter winter which may never come; the grasshopper knows there’re only so many springtimes and plays accordingly.

To have a choice of how one lives is a joy in itself.

Debt-Free-Bubba’s choices of when to save, when to spend, and what to spend it on have worked for him… why impose your choices on him? (Aside: his goals might include leaving some of his estate to family or charity. Is that wrong?)

It seems some commenters here hold tight to the impression that their choices and their situations are the yardstick and benchmark for everyone. (Also, anyone not matching them is morally less respectable.) This often bakes a statistical error into one’s thinking from the start, and also misinterprets what a free society is about. Despite the constant political horn-blowing noise/distraction on both sides (exploiting and amplifying these misapprehensions), this society still reasonably fits the definition of being a free one. Many (not all) constraints are self-imposed, and an innate product of one’s choices. Any choice has substantial costs. Many want all the cool fun stuff and complain about the related costs and the bad people supposedly imposing this.

Phleep-

Thought you might appreciate this:

Freedom’s what’s inside the fence,

Of Morals, Money, Law, and Sense,

And we are free if this is wide,

(Or nothing’s on the other side).

We come to Politics (and Sin),

When Your fine freedoms fence Me in,

And so through Law we come to be,

Curtailing Freedom — to be free.

—-Kenneth Boulding, Principles of Economic Policy, 1958

Good to see you posting comments!

Also define ” enjoying life “.

The thing about life, even the pain, eventually becomes a reason to celebrate.

Right. Being buried with the tons of money is much more enjoyable.

Point is, people are spending their money how they see fit, not how you see fit.

I’m with you, Einhal, 100%. We are such a greedy, superficial, entitled country. An economy built on consumerism doesn’t align with my values either.

The costs of rampant consumerism are externalized and pushed into the future (and to regions of the planet we don’t have to look at). This is a “kicking the can” that many have an incentive to ignore, choosing instead to fixate on the cartoon lifestyle aspirations (the reward cheese in the maze), and this week’s good-guy-bad-guy cartoons in the popular media.

I have a different take about the supposition that we are greedy, superficial people, mindlessly spending a private sector income.

The average income is a poor statistic for judging the corrosive effect of a dominant wealth inequality. A better statistic is the median which avoids the Bill Gates walks into the local tavern, effect in which every client of the tavern was on average a billionaire.

America is rich because of the heroic efforts of people that had everything to lose.

dang,

If you’re referring to the disposable income chart, it doesn’t include Bill Gates’s income from capital gains, which is how he became a billionaire. Capital gains are not included in disposable income. It only includes his salary, his Social Security benefits, and his interest and rental income and farm income, if any.

Howdy Folks. Seems like some of the youngins do not understand the old school ways. Work hard, save some of your $ always and you will prosper and should find happiness. Freedom is where you find it. Good Luck

I would think restaurant spending in part would reflect the existence of more dual income families currently. During the great recession often one person was home cooking. Now maybe they are both too tired after work. Also more children are born during a better economy which is even more reason to eat out.

Dual-income households have more money to spend, and they spend more. That has been the big trend all my life. My dad’s generation had money when they had a good job and were single, and they could afford all kinds of crazy stuff. And then they got married and had kids, and the same income had to suddenly feed multiple mouths, and to pay for a bigger home, and all the crazy young-man-spending stopped. Heard lots of stories about that. My generation was the first generation that took two incomes per household for granted, expected it, benefited hugely from it, and enjoyed it. Sure, one of them can take off for a while to take care of the kids or elderly relatives. But after a while, it’s back to two incomes. I look back at my parents generation, and I think, what horror! We have so many more options.

I often think about this. Not sure if it’s better to maximize wealth/disposable income for 65 year olds. At least your father’s generation could afford a great time when they had youth and could really enjoy it.

“At least your father’s generation could afford a great time when they had youth and could really enjoy it.”

They were utterly impoverished by our standards. The “crazy spending” was in their eyes, not in our eyes. They died of small things, such as infections. They didn’t have cars. And eventually those that did, had slow-moving fuming death traps that would be a nightmare today. They barely had a telephone. They had no internet, no computers, no cellphones, and even small things were really hard to do and took a lot of labor and time, like washing your clothes and sheets. It took weeks to get across the Atlantic – my uncle made that trip in the 1920s from Hamburg to New York, we have letters that he wrote back to my dad from New York.

“At least your father’s generation could afford a great time when they had youth and could really enjoy it.”

I think I enjoyed my younger years a lot more than he enjoyed his younger years. But I didn’t have to go through the shock of suddenly having to feed so many mouths with just my income. I got married to a woman with a career, and we actually came out ahead. That was unimaginable back then.

Wolf,

This pretty matches my “lived experience” 100%.

When we had kids my wife stopped working – at a PAID job – to take care of them. And me too VBG.

When our youngest reached full-day school age she went back to a PAID job. And she still took great care of us too!

We boomers had (have) way more options than my WWII generation parents had.

——

By the way … thanks for running such a highly informative blog!!!

As a kid, we lived a comfortable life.

As an adult, we have far more money now.

I remember my mom stayed home and my dad worked. We had one car for the family.

Back then, we didn’t have as many toys as kids but we had the basics.

Vacations involved loading the station wagon and driving. I didn’t fly in an airplane until I was a teenager. We took one flight then to visit relatives and I remember the flight from LA to Chicago was 1000 dollars per person. That would be equivalent to $7000 today with inflation. I can’t imagine paying that much now for a family vacation. We’d load up the AWD SUV.

Better to spend now rather than later when inflation goes back up. Looks like alternating battle of wages vs prices going up together and taking turns which leads in their spiral.

Wolf,

I came of age at the beginning of the two family earners. After enjoying my early years of independence, 4.5 years as a US Marine, I met and married a wonderful lady.

At first we moved about and I changed jobs. Then came family life and working a good oil job. Sure it was many hours of swing work for 15 years, along with growing a garden, and the wife canning most of our food. As my father was a farmer I bought a fat steer from him each year. This was after helping bring scrub milk stock into what could have been easily mistaken for registered Angus cattle. Meat buyers at the local sale barn paid top dollar for any sold at auction.

Turning 42 found me changing job or accepting a promotion to a new career in accounting. Wages became salary, reduced as the company waited to see if I worked. Huge raises for several years followed in line with the hours worked learning the job and improving company reports. This went along some ten years. Then came another promotion but small increase in salary. Six years later after being on the team building new accounting systems usable by computers, evaluating financial systems, and wasting a year’s work as two companies merged and we were locked in on their new system. After implementation of the system I retired leaving the only refinery knowing where their books stood in the corporation. Bragging but received a pay increase two weeks before retiring. CFO said it was incase I stayed around.

Since then I’m back to playing both the market and with what ever we, still married to the same lady today, want to do. So you can have the two income earners as we have watched many follow and somehow never truly enjoy the life.

Right now we are visiting a granddaughter and her husband, both having double majors and jobs. I really hope and pray they find the sweet spot.

A lot of the sailers were spoiled as children, so that is all they know. Their raison d’être is to get money to spend money. That’s all they have ever known. Gambling is ok to but saving? What’s that, you crazy.

I witnessed some drunken sailors spending like there was no tomorrow the other day at a special occasion brunch in Georgetown, Washington DC. The place was a complete ripoff, overpriced, bad food, but good amenities, tourist trap if there ever was one. The place was packed with overweight locals stuffing themselves at an “all you can eat buffet”. I never go to these places but was forced to go this time, and will never go back. What this tells me is there is too much money out there and is being spent on needless consumption. Where is all this money coming from?

“Where is all this money coming from?”

For an answer, see the subheading in the article above that says, “Where does this money come from? Surging real incomes.”

Howdy Lone Wolf. 5.5% interest rate has allowed savers ( Squirrels ) to spend more.. Wife and I spend 30 to 40% more and still save more than ever before…….

Tell us another one.

Dear John. I would love to tell you about this one. Retired savers

( Squirrels ). always saved $. Never spent more than what was coming in. Out of debt for decades, and finally earning interest on our savings. Lots of $ now goes to the kids while we are alive and we are spending more since we are nearer the end than the beginning…………..

This Bubba gets it! Keep it up, friend!

From the reduction of purchasing power of the dollar, I think. And a reduced standard of living for the future residents of the USA, perhaps

SC

Define ” needless consumption “.

OutsideTheBox

You asked so here’s what I mean by “needless consumption”

With the Federal government running 2 trillion dollars in deficits as far as the eye can see, and leaving our next generation, and grandchildren, to a life of servitude for the rest of their lives paying off this debt, I sorry if I’m appalled at the fact that many American’s are joining in, spending money they don’t have with their main concern today buying a $100,00K truck financed to the max, and going out Sunday to an all you can eat buffet and stuffing themselves with bad, unhealthy food at appalling prices. There will be a day of reconning for all of this.

You’re right, Swamp C. Good old .gov should crank taxes up a lot higher so the guy you describe can’t afford to waste that money on that truck. And .gov can then balance the budget!

Perhaps it is you that is the problem rather than them.

I’ll help him: 2024 Ford F150 AWD, decked out to the max ($100,000+ ) sold to a guy who works in an office, lives in suburbia, never goes off road, pays contractors to have anything done at his home.

The largest sailor is the fed govt. And it is spending relentlessly. The consumers are acting in parallel to it. Without the fed govt pushing breaks for spending, the consumers never will and we will leave with continously inflated prices.

Either private acquisitiveness, or government, keep some churn going in the economy. It’s what the economy IS. That, or one can do a 1930s and grind toward a cold freeze. Churn comes with some inflation. IMO. This is far from the worst of all possible worlds. As the real world often is, it is somewhat in-between and messy. It doesn’t neatly fit a desired category.

Right. The deficits must be cut. We are near a scarce reserve’s environment.

Wonder how much spending is via debt?

We are all getting a huge break with oil prices, right now about 72 a barrel.

If the past is a guide this may not last.

It seems to me, but haven’t checked. that the last time oil was this price, the pump price was a lot less.

As it should be. Oil price per barrel might be the same. But the cost to refine it and transport it and everything else should have gone way up with everything else. So even though they may be willing to extract it out of the ground for cheap, I would expect surcharges everywhere else that would result in a higher markup from the past. Makes perfect sense to me, given the cost of doing business has gone up everywhere.

No, it hasn’t at all in many areas.

Where did it get cheaper to transport and sell oil? Do you know of a labor cost reduction since 2019?

The price Spire West customers pay per cubic foot of gas will jump from 40.4 cents to more than 79.3 cents, an increase of 96.2% in 2024.

Wolf:

There seems to be so much mixed signal. The CRE is cratering. Today there was an article where they quoted two FED officials and of course, the big banksters saying some proposed strengthening of reserve requirements have to be scrapped and redone all over. I guess those two would be rewarded with lucrative jobs once they leave FED.

Avi Gilbert of SA has been sounding banks insolvencies and recently of the good possibility

of the beginning of a long term bear market.

Perhaps it is good to be a drunken solder with all the uncertainty of the future.

The Fed’s printing press is still there. It can provide infinite liquidity to a collapsed segment of the economy with the touch of a button. I imagine that is still the main central banking tool to do emergency response to the buckling of some segment of the economy. In effect it works like insurance, except no pool of reserve was built in advance. It works like a tax on the macro economy (as in the pandemic payouts). I’m not saying it is perfect or cost-free, but in past history, crashes simply propagated chaotically across the economy. Maybe that contained them to certain people, but not as in the Great Depression, where the networked economy crashed system-wide and needed a macro response (arguably). My personal response is not to act like the drunken sailor anticipating all this, but that is just me.

It is a scenario that may be wrong.

Years ago I saw a bumper sticker that read, “Eat your desert first, life is so uncertain.”

I think AI is going to take some of the winds out of the sails of the “drunken sailors”. Someone on one of the shows said Google was a buy, because with AI assisted programmers, Google needed less programmers. Customer service rep is going to take a big hit, because chatbots are quicker.

I see generative AI as a force dropping the inflation rate a bit, because I see increased productivity coming out of this. We still need the physical labor jobs for now, because the robots aren’t there yet, but generative AI is going to reduce desk jobs. Any reduction in jobs are going to reduce inflationary wage pressures, at least for awhile.

If you study history books, people said that when Henry Ford started building cars with a production line that it was bad news because it was going to put a lot of people out of work. The numbers of worker hours required to build a single car drastically dropped. Everyone assumed that the number ofbcars being built would stay the same and employment would drop.

Instead, the number of people working on cars went up and the number of cars sold skyrocketed as cars became much cheaper..

It is the same with every productivity advancement ever..

AI is just a productivity advancement. It will allow workers to be much more productive. This means that what they produce will become cheaper.

Sure there will be disruptions to some industries (widespread car ownership really hurt the buggywhip industry), but overall economic productivity increases are good for society. It also people to do other stuff.

I used to like using the chat feature for customer service because it was quicker than a phone call. AI chatbots have made the chat feature useless. An AI chatbot just gives you a script that doesn’t solve your problem, then tells you to state your problem again and someone will respond to it by email. You can do that by emailing in the first place. The AI chatbox feature is worthless.

“An AI chatbot just gives you a script that doesn’t solve your problem”

It’s so damn annoying.

There are still chats with real humans answering them. I’m one of them.

The last thing AI will be programmed to do is take the wind from the sailsl

AI will be programmed for a specific outcome.

DM: Commercial real estate implosion – Blackstone is desperately trying to shift Manhattan office tower at HALF price after 26-storey building’s value tumbled from $605MILLION to $150MILLION

It comes just a week after Shorenstein put the 62-storey Aon Center in Los Angeles on the market for $153.5 million, down from the $269 million it paid ten years ago.

As long as everyone is spending, I will continue to spend. I am not deferring any of my purchases. All my life the prices have been going up. Just look at food, clothing, and shelter plus vehicles. Prices keep going up. The great depression was 100 years ago. I’m spending now, because it’s just going to get more expensive in the future.

Once my fellow D-Sailors stop spending, I’ll follow them and stop too, but all the people I know are spending, so why not me.

Why does it matter what anybody else does as to spending?

And that’s exactly the mentality in this county. Gotta keep up with the Joneses. People will buy for the sake of buying, even if they don’t need it or will never use it, and they will come up with any excuse they can to justify it. They can do what they wish. I just don’t want to hear any whining when they run out of money or lose their job or whatever and have no (or not enough) savings. Don’t expect me to bail you out.

“Don’t expect me to bail you out.”

But, the Fed pushes a button, creating infinite liquidity to bail them out, and disburses this electronically, instantly. This dilutes your savings. It is taxation and wealth transfer, without representation or a democratic process. Arguably it is consciously orchestrated by the elites who harvest the cream from it all, to deploy for fun and more politics. The avid consumers just play into this consumption maze. It is a higher order of farming: farming human behavior. But not the worst of worlds (looking at something like WW2).

Phleep:

Agreed, just hoping we can stop the vicious cycle.

The profligate don’t expect you to bail them out. They rely on the government to bail them out. Their whining matters to legislators and politicians. They vote for a living. You work for a living,, or live on the proceeds of past earnings. The government relies on you to pay the bills. Your whining doesn’t matter, because you still pay the bills. When you stop paying the bills and pull out the pitchforks and torches, the government stomps you. So citizens learn to hide their productivity as more and more of it is siphoned away to placate the mob. In our economic system it’s difficult to hide private holdings of any size, while bureaucracy has become a black hole for our taxes. This cannot improve until legislators and the administration are compelled to spend this week’s allowance during this week. And stay out of future revenues that are usually baldface lies anyway. And stop expecting the rest of the playground to pay for our popsicles while they’re sucking ice cubes.

Dunno DR — I detect a nascent rejection of gross materialism by younger generations. Which I salute. The fact that much of the increase in consumer spending seems to be in services (the ephemeral) rather than on goods (status symbols & other goo-gahs) might suggest that Americans are focused on what they can control for most — here/now — and are pouring some of their newfound solvency into experiences.

We emerged from the sudden bleakness of a pandemic amid whiffs of fascism, world war & the doom-y shadow of AI. It seems not that unreasonable that Americans might feel a little fatigued by and even skeptical of the idea of tomorrow.

Just my observations. I personally defer gratification & save like crazy. It’s just that I think an argument can be made for a more cavalier, impulsive way of being, too — ignoring time & decimal points.

In my neighborhood it always amazes me to see houses with 2 expensive cars parked in the driveway with a 2 car garage filled with worthless junk.

Gotta show off that luxurious lifestyle on tiktok, otherwise what’s the point?

phleep has it sussed precisely. Well done!

I think what some of the older commenters overlook about spending on luxuries is that due to the internet many of luxuries have shifted online and cost no much than an internet connection and a nominal fee for streaming. How many people worked really hard to have enough money to rent a movie at Blockbuster on the weekend (Netflix and other streaming services), buy that latest album from your favorite artist at Sam Goody or Tower Records (Spotify, Apple Music), or buy that magazine with the sexy, scantily clad women (Instagram) or that Playboy or Penthouse magazine with the hot naked women (OnlyFans, P***Hub). Just this week it was announced that Sports Illustrated was immediately laying off nearly half of its staff and that the future of the magazine was in clear danger. So there is a clear shift in habits even with what people do to entertain themselves that is not necessarily reflected in the economic numbers.

Don’t forget the fourteen million home loans that refinanced to a much lower rate during Covid, adding thousands of dollars a year to incomes. There are about 65 million households with a mortgage, so this is a significant number of households with extra money. And 40% of homes are mortgage free. People have money bleeding out their eyeballs, and it’s not just wage increases.

Yes, I know many, many people who are established and middle aged who have seen these insane wage increases while having a mortgage of 600-1000 dollars a month and a tripled home price on 5-10 years.

They’re all riding around in fancy new trucks and SUVs with new toys. Boats, tractors, skidoos, motorcycles, campers, classic cars, etc.

Easy come, easy go I suppose. I guess it’s not my place to judge how people fritter away their money. They’ll all seem to be enjoying life more than me so I can’t condemn them. But I couldn’t imagine holding so many value losing assets and working a blue collar job at 50-60+ years old.

It’s hard not to be tempted by the manifold joys of solvency.

I remember being hand-to-mouth poor in my 20’s…holes in my socks, counting how many bites I could have of a leftover pizza to stretch it out…rolling coins to subsist until payday — “the drippings of my labor” — even the outsized elation following the discovery of a random 20 dollar bill stashed away in a center console, and the taco feast which ensued. Incidentally, I was not unhappy then.

Once I was able to live even remotely less shitilly, I ran full-tilt toward it. For me, razzle-dazzle was having a nicer hi-fi setup & better beer in the fridge. Improved palliates with better active ingredients, we’ll say. At some point, it’s diminishing returns. “You can only have one lunch.”

I note all of this because I bet a lot of the crowd you see running around are similar — all those fancy trimmings you’re seeing are maybe just the most visible upgrades from one standard of living to the next. They’re affording themselves comforts which ostensibly help buffer them the grinding miseries of the toil required to obtain them.

That’s not everyone. But it’s a lot.

Your experience accords with my own. But I still wear socks with holes in them until they really fall apart.

A couple of quick thoughts. I don’t know about the rest of the posters, but I feel a lot poorer today compared to pre pandemic days. Some it is due to inflation, and the rest of it is because my living is related to the commercial real estate market. The latter is starting to get a little better for my practice; however, I’m not feeling any better on the inflation front. I keep rooting for a miracle, prices reverting to pre pandemic levels, but this is seeming less likely with each passing day. The only way prices could revert would be via a deflationary period, and the Fed will do everything in its power to prevent this from happening.

Regarding the US consumer, there is an old Wall Street saying that goes something like this: Bet against the US consumer at your own peril.

I’m wealthier, but feel poorer, due to the thought the Fed can create another 20% inflationary spike, without apology or analysis of error. We know it can happen, because it did.

Also, it seems just about anything qualifies as an emergency requiring renewed Fed interventions.

Hedge fund hiccups

Reduction of speculators’ liquidity

Hint of recession

Stock prices or long-term rates correcting

Overall price discovery

Such threats are now considered an emergency, and the consequences of not acting would be intolerable.

The threat of out-of-control inflation makes traditional retirement planning near impossible. At a minimum, Average Joe will have to scale back those retirement travel plans to accomodate a part-time Home Depot job.

Sorry, meant “accommodate”.

The entire boat is staying afloat through government spending, as it has been for years. If you take just the Deficit spending it amounts to $2.8 billion per state every month.

The only surprise is why retail sales aren’t higher.

Imagine if the government stopped just the deficit spending?

Disaster.

They simply can not turn the spigot off. The FED knows this and tipped their hand by mentioning rate cuts; they are chomping on the bit to reduce rates. MMT on steroids needs low rates or the jig is up.

If you look at percent change in retail sales on a bar graph, YoY, you will see a very pronounced increase from Jun 2023 to now. The x-axis is months. A straight-line fit vs time would give a significant coefficient. However each datapoint uses the previous 11 month’s of data. So it is not as exciting as it might appear.

The same bar graph but with month-to-month data shows a fairly flat line since Jun 2023, but a pretty sizeable increase from Nov 2023’s negative print to now. Well, some people like Wolf say the the monthly data are just noise, but not me. In any case, it is tough to say we are heading into a recession.

I shifted from buying six month t-bills to three month t-bills because the latter now have a higher yield, about 21 basis points as of today. It used to be the other way around. Both three-months and six-months mature on Thursdays so it is easy to make purchases so that all my money is always earning the t-bill rate (no money sitting in the sweep or cash account). They both settle on Thursdays.

“The same bar graph but with month-to-month data shows a fairly flat line since Jun 2023, but a pretty sizeable increase from Nov 2023’s negative print to now. Well, some people like Wolf say the the monthly data are just noise, but not me.”

OK, here we go, month-to-month % change retail sales, seasonally adjusted:

Wow, looks like the economy is in Afib!

Yep. Noise.

“I shifted from buying six month t-bills to three month t-bills because the latter now have a higher yield”

I noticed that too. There’s literally no money in duration right now. Crazy.

The problem is that Powell went off the rails in his last press conference, and most Fedspeak since then has been trying to walk back his inane comments. So Powell sounds dovish, the markets are psychotically addicted to lowering rates, most Fed speakers have since been more hawkish than Powell, and recent data (btw, look at today’s jobless claims) are hawkish. So nobody knows what the f is going on, which is normal. As for me, I like to look into it all, realizing it is likely a futile effort, and eventually just go for the highest T-bill rate.

MW: Jamie Dimon still sees no value in bitcoin after ETFs debut: ‘Please stop talking about this sh—’

@SCBD: Oh, the day Bitcoin goes belly up will be a very interesting day.I don’t know how the government stands by and watches this whole sh** show and the SEC approves Bitcoin ETFs.

Btw, there was an article yesterday on how a 28-year old managed to hack into Bitcoin. I would like to see explanations from anyone who is tech savvy.

$FOMO to $YOLO. The Baby Yoomers vs The Baby Boomers largest populations spending the most money. We seeing more spend money on travel and entertainment, enjoying money through experiences. Traveling demand post COVID is still pretty high. Younger generations are content with renting and having reliable transportation, I-phone and social media. I’m now seeing new vehicle leasing commercials sub $500 notes. There are so many You Tube bloggers raking in money. There is not really a feel of I can’t afford tomorrow Starbucks. I heard on the news that the new middle class income is $120,000/yr. The good ole credit and consumption economy is doing well. Trump will cut taxes again after election, inflation really has opened the eyes of many Americans, the gauge now is it could always be worse. The big debt items of mortgages and student loans are being highly evaluated by younger generations as a want vs a need. Economic freedom, do what you want when you want, and enjoy life.

I understand why you use the term “drunken sailors”, but I think it is pejorative based on societial standards that are changing.

It used to be that a person got married, settled down, raised a family, and worked at the same job for 40 years. Many of these things are changing. Younger people are getting married later, if at all. A greater percentage are choosing not to have kids. Corporations long ago broke the work at one job for life expectation.

Given all of that, more and more are looking at home ownership (and durable goods asset ownership) as more of a burden than a goal. Without the burdens of being tied down with a home, kids, and a job, they are enjoying life through experiences. This includes concerts, travel, food, etc.

I have gotten to know lots of younger people who have great paying jobs that have chosen to live with another (or even multiple friends) where they rent because they know that a couple of years in the future they might decide to move somewhere else and get a different job.

For a person who is constantly switching jobs, moving around, and doesn’t have kids, a house is more of a burden than anything. Renting is far superior. Not owning a home (and renting with lots of roommates) also frees up lots of money to do fun things like travel and eat out.

It isn’t that these people are drunken sailors, it is just that they are living their life to a different standard than previous generations.

Then we throw in boomers. They are retiring in crazy numbers as we speak. Due to social security, pensions, 401ks, and owning a rapidly appreciating house for decades, they are wealthy. What do people with lots of money, lots of free time, and few responsibilities who are facing a dwindling amount of time on this earth do? Spend it. They can’t take it with them.

Between wealthy boomers and shifting cultural norms among younger generations I think spending habits are changing. It isn’t that they are drunken, they just have different views on spending.

“I understand why you use the term “drunken sailors”, but I think it is pejorative based on societial standards that are changing.”

No, you don’t understand since you didn’t read the article other than the headline. So, let me help you out a little. Here are two quotes from the article:

“They could save a lot of money by eating at home or packing lunch, but no, our Drunken Sailors – as we’ve come to call them lovingly and facetiously because – gotta have some fun.”

“This surge in real income is what fuels the spending binge. And yet, consumers are still saving part of their income. Maybe they aren’t drunken after all, they’re just earning a lot more money?”

Actually I did read the article. I just missed that clincher.

I just see so many comments here pejoratively judging those that are driving the spending and I think the people making those comments are missing cultural shifts. The spenders are spending on things they think are important, not what their parents and grandparents thought was important.

As your clincher points out (that I missed), they are not drunken, they are just spending on their priorities and are doing so in a fairly responsible manner.

We are in agreement.

“I understand why you use the term “drunken sailors”, but I think it is pejorative based on societial standards that are changing.”

I am literally a drunken sailor (worked and drank on a boat the last couple summers) and do not find this term pejorative.

“Then we throw in boomers. They are retiring in crazy numbers as we speak.”

11,200 per day estimated for 2024. That’s a lot of Social Security checks. Certainly more than the monthly jobs created.

A huge young generation has been entering the labor force in very large numbers, replacing the retiring boomers with ease, plus some. Generations are a flow.

Geeeeez are sailors now a protected class?

Wolf, I was with you up to the part about “Surging real incomes”.

If you don’t get this, you will never understand the US economy, and you will always be surprised by this growth in consumer spending, and you’ll come up with conspiracy theories to explain it, or fall for the idiocy [debunked here a gazillion times] that this growth is paid for by piling up credit card debt.

I’m one of those drunken sailors but not all our spending was deliberate. This year we bought a new car because it was time, cost $37K. The car was a good deal with a trade-in but it got destroyed in a storm, repair cost $15K. Earlier in the year the TV and washer/dryer broke down and were replaced, $3K. At this point, WTF, I just don’t care anymore, there’s new dining room and living room furniture in my future.

Petunia – Now you sound like a true American!

Are Americans saving a little bit more at least ?

Thanks

No.

At the risk of stealing Wolf’s thunder I’ll say RTGDFA. It literally says “consumers are still saving part of their income’. I suspect posters like SoCalBeachDude who simply reply “No” really mean “not as much as I think they should”.

I was at my local Irish Pub, enjoying the football game and a bear, when a Gen X couple came in and sat right next to us. They both ordered a Mederteranian platter for about $25 each. They each spent the entire time on their phones, took one or two bites from their respective dishes, and the waiter came buy and threw out the remainer of the food, which was about 80% of their order. Talk about “needless consumption”.

People are going hungry here in the streets of DC, and all over the world and homeless are freezing here and I have to look at this?

Maybe you could share the bear? /s

e-Commerce distorts everything. It’s just a black box sucking sales from all categories. It would be nice to see, for instance, total furniture sales from all sources. Seeing the brick-and-mortar sales of furniture fall off is meaningless if it is just shifting to e-Commerce. The same is true for the other categories as well. Unless you look back at the manufacturers it is hard to differentiate. Even then it is difficult as the majority of internet sales are direct imports from a much broader range of companies.

This is NOT about PRODUCT sales, for crying out loud. This is about RETAILERS by CATEGORY OF RETAILER.

Furniture stores are the most pointless brick & mortar businesses (along with other showroom-only stores). Of course sales are falling off a cliff.

No point to having a store in the year 2024 unless you can walk out with the thing you’ve purchased in your possession.

Us crazy older people like to know what we are actually buying rather having it delivered and then having to send it back, which drives up prices hugely for everyone.

No, us older people have always hated going to the store because stores never had exactly what we were looking for, and so we bought by mail-order before the internet, including clothes, shoes, and furniture, and when the internet came along and made it easy and opened up the market to endless competition and choices, we were in hog heaven and splurged online. I haven’t been inside a furniture store or a clothing store or a department store or a shoe store or a sporting goods store or a computer/appliance store or anything like that in at least 15 years. They’re such a horrible stressful waste of time. We’re down to only buying a portion of our groceries and supplies at supermarkets/Costco. All the rest, we buy online, us older people. We invented and built the internet. We might as well use it.