Down from 2022 highs: San Francisco -12%, Seattle -11%, Portland -6%; Denver, Phoenix, Las Vegas -5%; Dallas -4%, San Diego -2%, Los Angeles -1%. But new highs in 8 metros.

By Wolf Richter for WOLF STREET.

Today’s S&P CoreLogic Case-Shiller Home Price Index for “October” is a three-month moving average of home prices whose sales were entered into public records in August, September, and October. That’s the time frame here. It uses the “sales-pairs method,” comparing the sales price of the same house over time, thereby eliminating the issues associated with median prices and average prices (see “Methodology” toward the end of the article). But it lags.

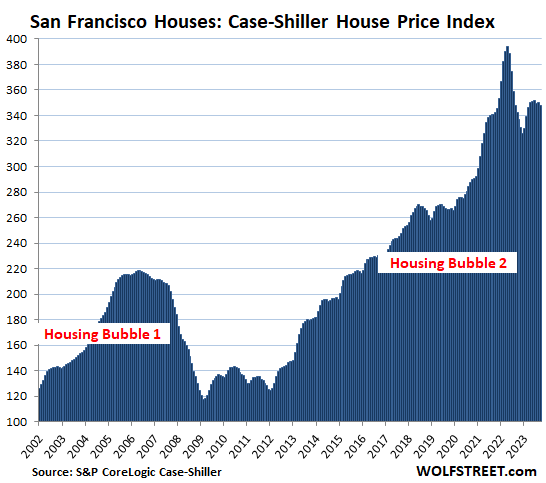

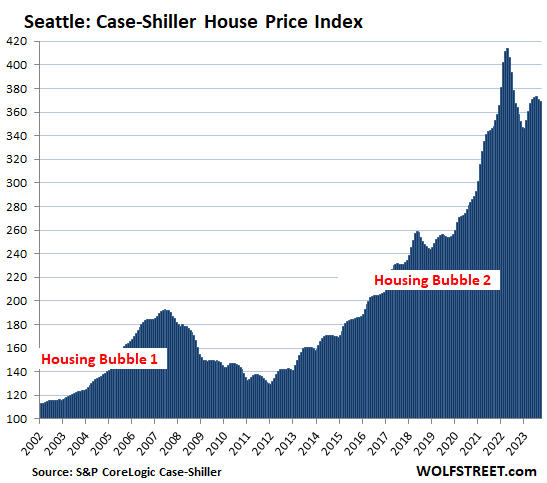

The story here is about the individual metros of the 20 metros covered by the S&P CoreLogic Case-Shiller Home Price Index where home prices soared to ridiculous levels, multiplying by factors of three and four since 2000.

The “most splendid Housing bubbles,” we started calling them since about 2017 to track their astounding surge – and what their fate is now.

Nine of the 20 metros in the Case-Shiller Index were below their peaks in mid-2022. Nine metros had month-to-month declines (Seattle, Denver, Tampa, Washington DC, Portland, San Francisco, San Diego, Dallas, Minneapolis). And 8 of the 20 metros set new highs.

Prices below their 2022 peaks in 9 of the 20 metros in the Case-Shiller index (% from their respective peak, Case-Shiller month of peak):

- San Francisco Bay Area: -11.7% (May 2022)

- Seattle: -10.9% (May 2022)

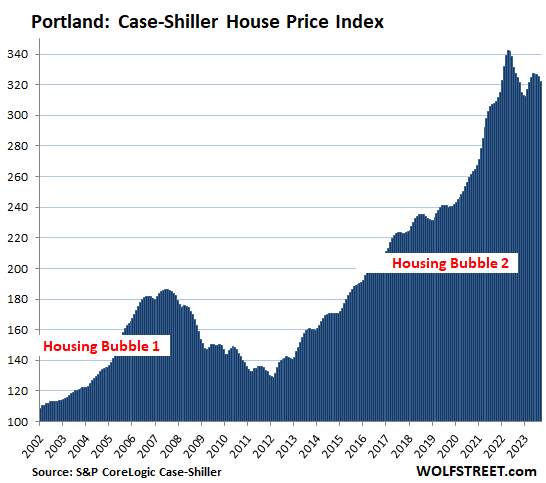

- Portland: -5.8% (May 2022)

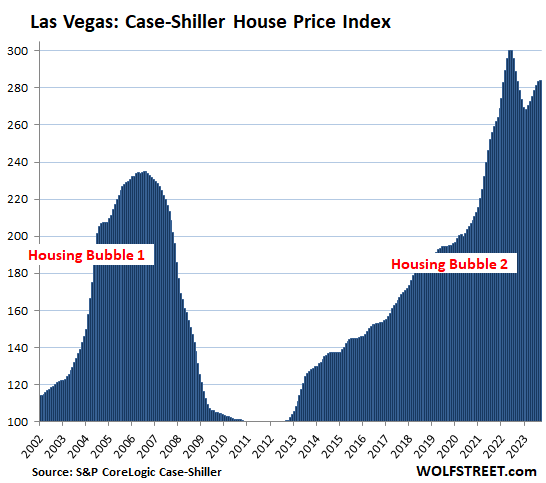

- Las Vegas: -5.3% (July 2022)

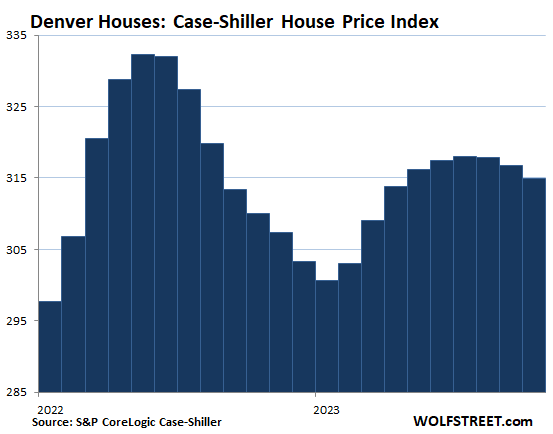

- Denver: -5.2% (May 2022)

- Phoenix: -5.1% (June 2022)

- Dallas: -4.4% (June 2022)

- San Diego: -2.1% (May 2022)

- Los Angeles: -0.8% (May 2022)

Prices set new highs in 8 of the 20 metros in the index (% year-over-year):

- New York metro: +7.1%

- Detroit: +8.1%

- Chicago: +6.9%

- Boston: +6.6%

- Miami: +6.7%

- Cleveland: +6.4%

- Charlotte: +6.0%

- Atlanta: +5.3%

The most splendid housing bubbles by metro.

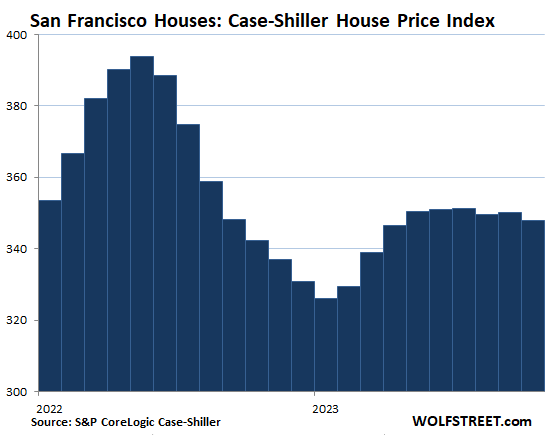

San Francisco Bay Area:

- Month to month: -0.6%

- Year over year: +1.6%

- From the peak in May 2022: -11.7%.

The closeup of San Francisco:

And here is the long view:

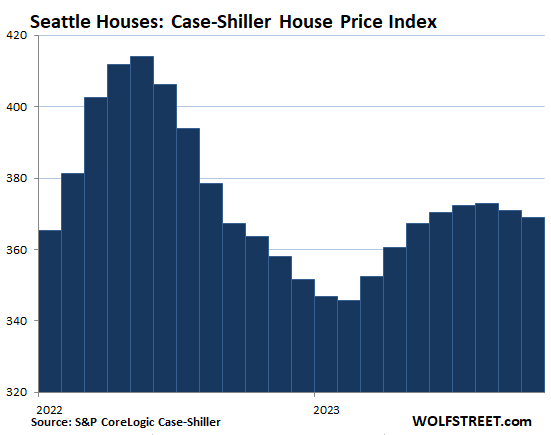

Seattle metro:

- Month to month: -0.5%.

- Year over year: +1.5%.

- From the peak in May 2022: -10.9%.

The closeup of Seattle:

And the long view:

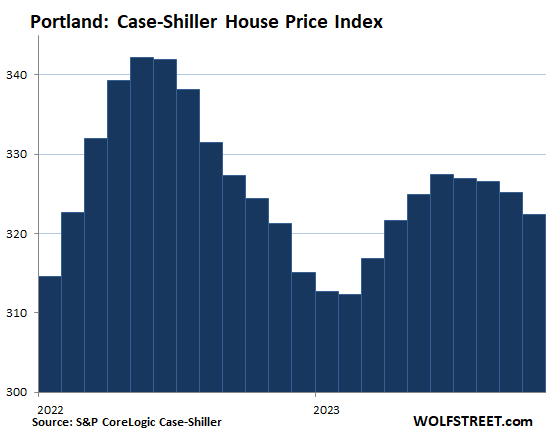

Portland metro:

- Month to month: -0.9%.

- Year over year: -0.6%.

- From the peak in May 2022: -5.8%.

The closeup of Portland:

And the long view:

Las Vegas metro:

- Month to month: +0.3%.

- Year over year: +0.1%.

- From the peak in July 2022: -5.3%.

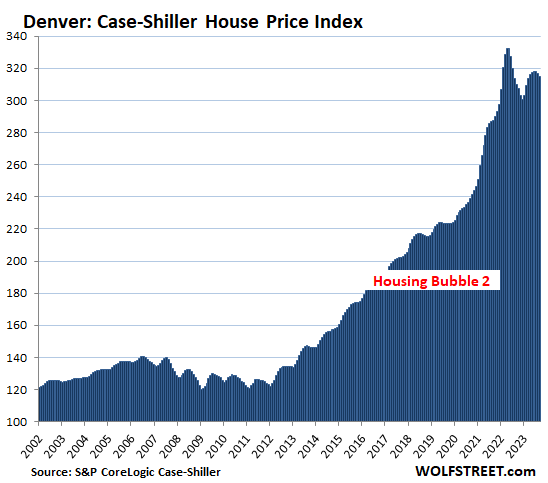

Denver metro:

- Month to month: -0.6%.

- Year over year: +1.6%.

- From the peak in May 2022: -5.2%.

The closeup of Denver:

And the long view:

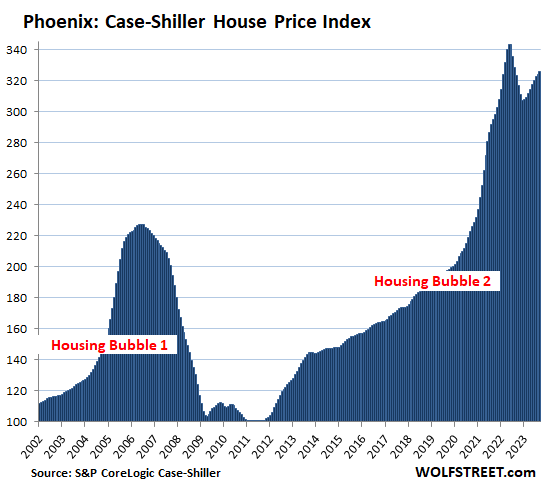

Phoenix metro:

- Month to month: +0.6%.

- Year over year: +0.9%.

- From the peak in June 2022: -5.1%.

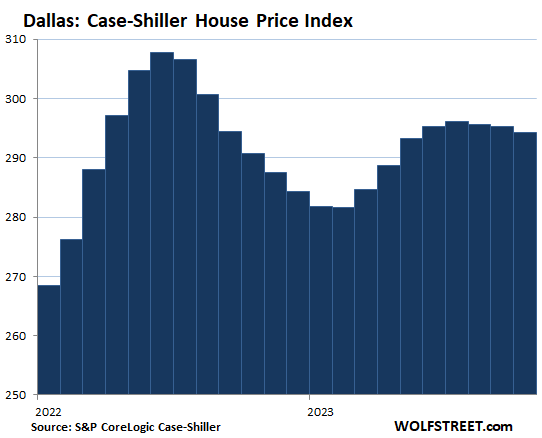

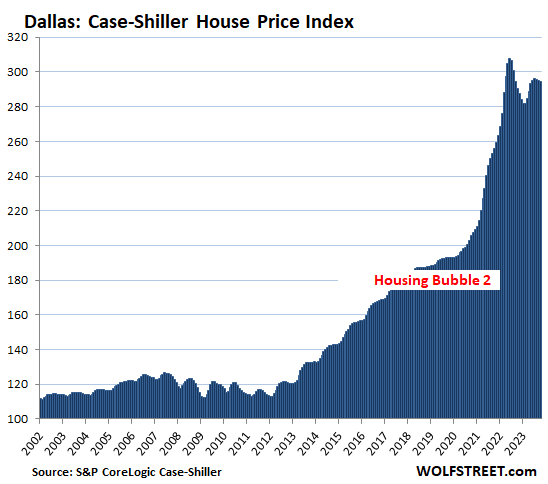

Dallas metro:

- Month to month: -0.3%.

- Year over year: +1.2%.

- From the peak in June 2022: -4.4%.

The closeup of Dallas:

The long view:

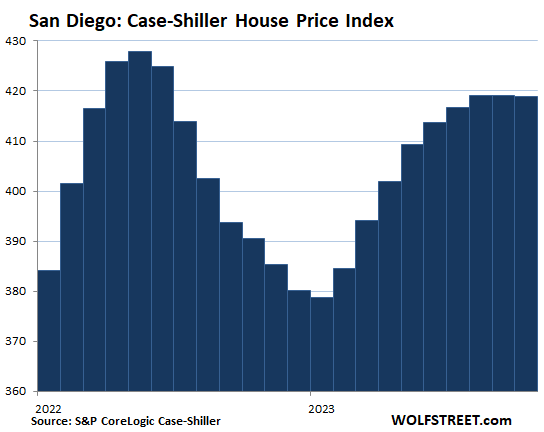

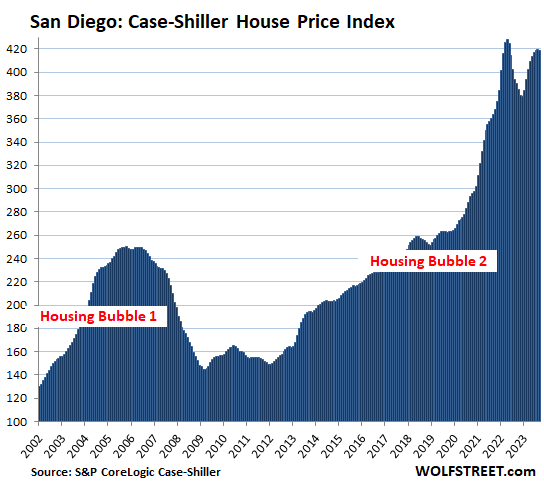

San Diego metro:

- Month to month: 0.1%.

- Year over year: +7.2%.

- From the peak in May 2022: -2.1%.

The closeup of San Diego:

The long view:

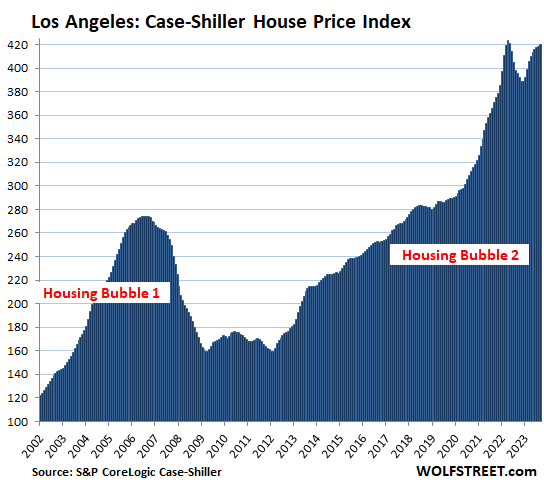

Los Angeles metro

- Month to month: +0.4%.

- Year over year: +6.1%.

- From the peak in May 2022: -0.8%.

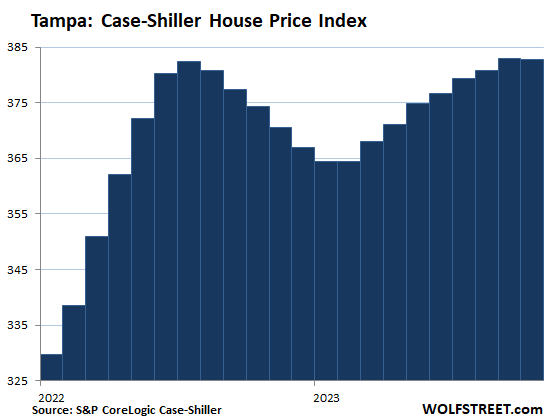

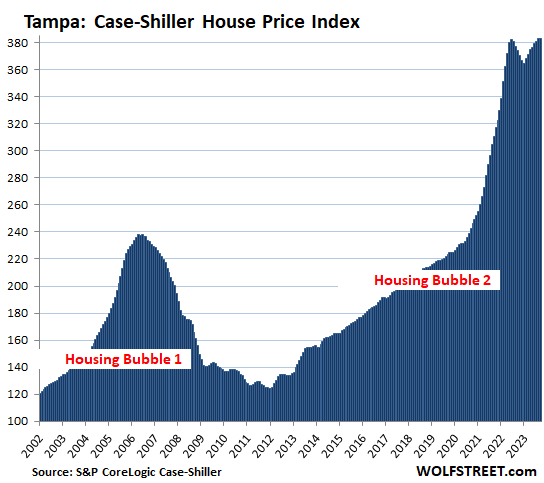

Tampa metro:

- Month to month: -0.02%.

- Year over year: +2.3%.

- October and September were just a hair above the previous high of July 2022.

Here is the closeup:

And the long view:

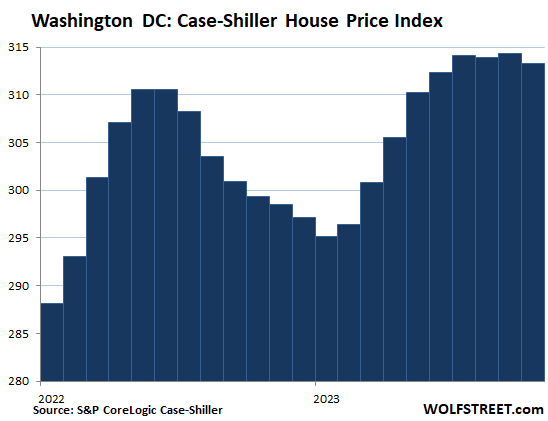

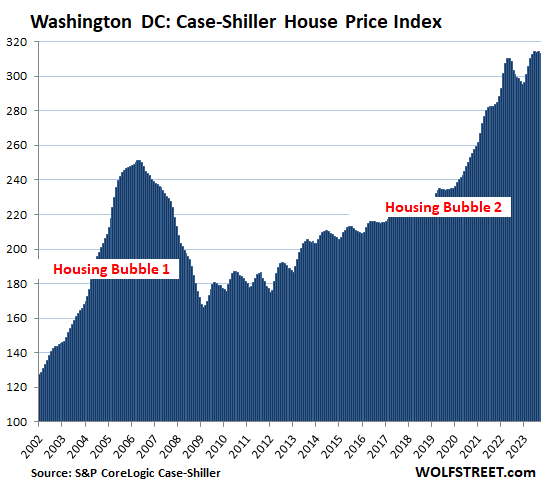

Washington D.C. metro:

- Month to month: -0.3%.

- Year over year: +4.7%.

- The prior month had been a new high.

Closeup of Washington DC:

Long view:

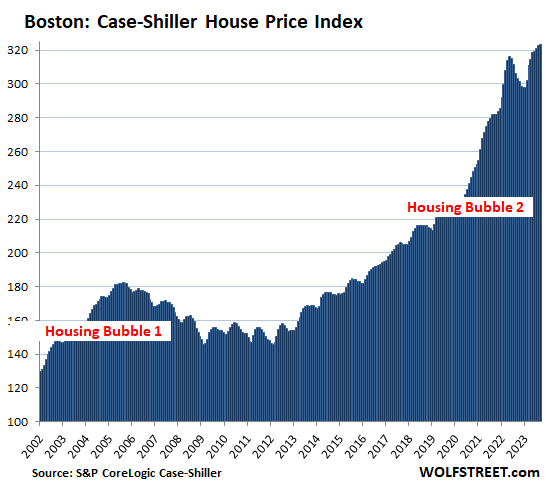

Boston metro:

- Month to month: +0.3%.

- Year over year: +6.6%.

- Set new high.

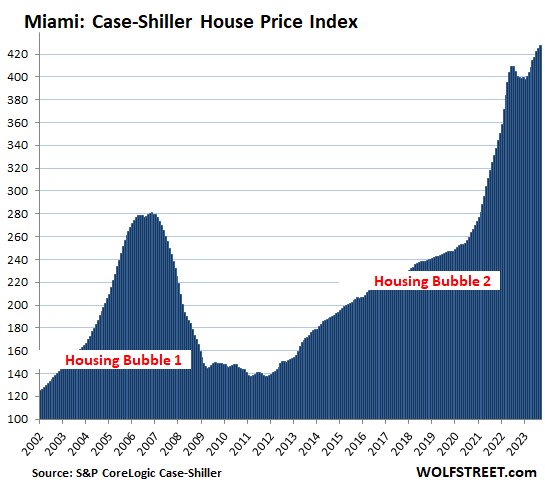

Miami metro:

- Month to month: +0.6%

- Year over year: +6.7%.

- Set new high.

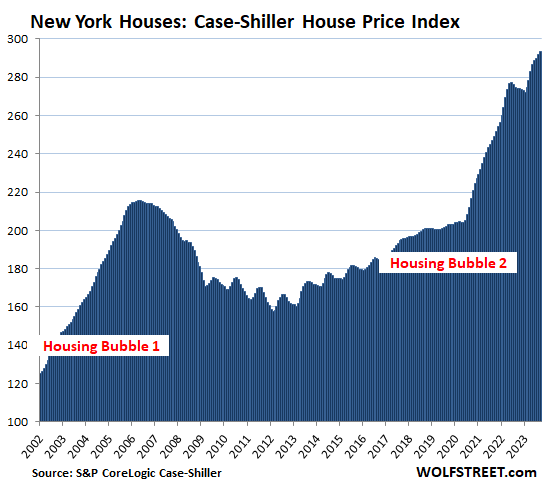

New York metro:

- Month to month: +0.5%.

- Year over year: +7.1%.

- Set new high.

To be included in this list of the Most Splendid Housing Bubbles, the metro must have experienced a home price inflation since 2000 of at least 180%. The indices were set at 100 for the year 2000. So today’s index values of 427 for Miami, 420 for Los Angeles, and 419 for San Diego are up respectively by 327%, 320%, and 319% since 2000.

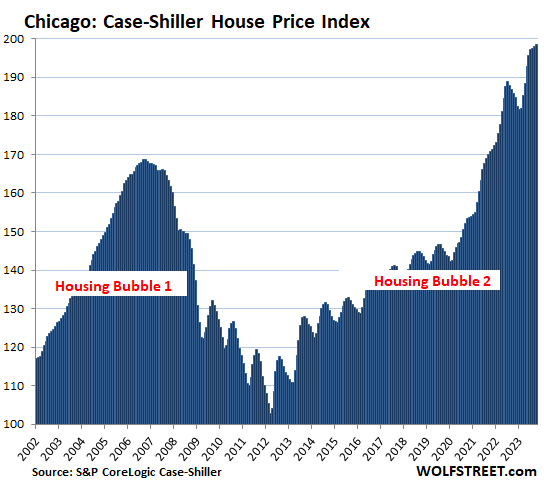

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had far less home price inflation than 180% since 2000, and don’t qualify for this list of the Most Splendid Housing Bubbles. But in 2022 and 2023, these metros had big home price increases in percentage terms, and the month-to-month increases continued in October, except for Minneapolis, where the index has now fallen for the third month in a row.

Chicago, with an index value of 198 is up by “only” 98% from 2000, and is therefore among the six Case-Shiller metros that don’t qualify for this list. But it saw a massive surge since May 2020 – thank you, halleluiah Fed money-printing – so here it is anyway:

- Month to month: +0.2%

- Year over year: +6.9%.

- Set new high.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices (37-page methodology).

Home-Price Inflation. By measuring how many dollars it takes to buy the same house over time, the Case-Shiller index is a measure of home price inflation. So Miami, for example, had 327% home price inflation since 2000. To be included in the “Most Splendid Housing Bubbles,” metros had to have home price inflation of at least 180% since 2000. By comparison, the Consumer-Price Index (CPI), which tracks price changes of goods and services that are consumed by consumers, was 82% over the same period (my discussion: Beneath the Skin of CPI Inflation, November).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Will cutting interest rates restart the housing bubble mania in the US? Canadians are betting that a -0.5% decrease in interest rates will increase the price of $2m Toronto houses into $200 million dollar property titans.

If you mean FED funds rate dropping, that does not necessarily mean that mortgage rates would drop. They might only drop the FED funds rate to counteract an increasing long term bond yield. But I am not sure if lower mortgage rates would skyrocket prices in America as lower mortgage rates may get those ‘stuck’ in their current homes to list. Which brings those people back into the supply and demand equation and it also means more vacation/rental homes listing as people think they can finally sell their additional properties. You’ll also notice not a single city West of the Mississippi made a year over year high.

I’m gonna say that’s a Yeah there good buddy.

If you want a house prob better get one in 2024. Otherwise we’re going back to bidding wars for sure if rates drop aka insanity.

What’re people bidding with, their blood?

I believe they call it ‘a buyer’s market’.

The long bond (5, 10, 20 and 30 year) unfortunately is falling hard today but I warned everyone the bottom would fall out of interest rates before January 4th 2024. They’re killing me.

What interest rates are you talking about?

One would hope that this is an underlying reason for the Fed to continue with the higher for longer mantra.

Yes, once the Fed starts to lower rates, there’s a high probability that the housing market will slowly start to head higher, assuming we’re not at the start of a recession.

Speaking of which, it’s highly doubtful we’re going to see a recession outside of a black swan event with the level of deficit spending Washington is engaged in.

Massive DC spending IS the Black Swan few people are talking about…

Yes.

Not just DC but state, county, and city governments are spending money like there is no tomorrow.

News flash…there will be a tomorrow and it ic not going to be pretty.

It’s hard to say when our reckoning will come as it relates deficit spending, but it’s not likely to be in the next 12 months.

Massive deficit spending can be the reason for higher yield on long term treasury bonds unless fed does qe.

This would increase the mortgage rates over time.

But I believe that its a matter of time for fed to stop qt and start qe.

5 percent now down to sub 3.9 percent on the 10 year treasury bond is what I see. I’m seeing the bottom fall out of long term rates.

AI replacing jobs could be the black swan event.

Lol, I have done automation for a long time in Windows.

AI has vast knowledge no intelligence. Can’t do complex tasks,

I myself am building a virtual assistant chatgpt with said automation. It doesn’t understand its purpose. The AI does not have the same abilities of a human its an advanced autocomplete.

Automation as is now is extremely expensive to deploy and maintain.

“Will cutting interest rates restart the housing bubble mania in the US?”

By the time the Fed cuts rates that’ll mean something economically important has broken. Banks don’t like lending into that kind of turmoil, which is why when the Fed ZIRP’d the FFR by the end of 2008, it still took the banks many years before they offered mortgage rates under 5%.

Higher FFR now will eventually mean higher unemployment, more defaults/foreclosures/added inventory, etc, and it won’t take much more inventory to start a negative cascading effect in prices.

With long-term yields dropping, the risk of banks having grave financial problems is easing dramatically. With all the extra spending, employment is NOT going to turn negative anytime soon, and housing defaults will not rise appreciably without unemployment rising dramatically. The economy & labor markets are likely to stay positive throughout 2024.

The concern for the Fed will the economy start to reheat up again early next year? If the 30YFRM breaches 6%, then housing will turn higher which could happen in the next 30-45 days.

I don’t see the Fed cutting rates at all in 2024. Deficit spending will keep everything relatively buoyant.

Of course it will restart the mania. Just look at what’s been happening to stocks, bonds, commodities, virtual funnymoney etc. as rates fall. There is an inverse relationship between interest rates & asset prices for almost every category of financial asset, and real estate is no different.

“During the 2000-2002 collapse, the S&P 500 lost half its value, the Nasdaq 100 lost more than 80%, and the Fed eased aggressively and persistently the whole way down. The same was true of the 55% collapse of the S&P 500 during the global financial crisis of 2007-2009.” -Hussman

*restart* it? Speaking as somebody in the nearly 50% of metros hitting an all time high, it doesn’t feel like it ever left.

Home price appreciation this year has (generally speaking) not been at a parabolic rate.

“Mania” means going parabolic. (For example, 2020-21 home prices & stock prices, 2023 stock prices.)

I don’t see mania, but lower rates will ensure that existing home prices never really took a hit and the 18% drop in new home prices would be at risk of slowly chipping away to the tune of 5-10% throughout 2024.

Right!!

Well it depends on what you mean constitutes a rate cut. I mean if you are talking about zirp which Powell reconstituted after Trump tongue lashed him. Then I think the asset prices of housing would be likely to exceed the current irrational pricing.

If we are talking a pct less than the current 7 pct, that is a different kettle of fish. The current market of sustained asset prices in at least three identified asset price bubbles is a dilemma. My first impression of the likely marginal rate from changes in the market price of risk, the interest rate is that it is facile like a wet noodle or spaghetti.

In chemical thermodynamics there are two important quantities, entropy and enthalpy, one path dependent and the other not. The path being the distance from whatever current state one finds themselves and equilibrium. In the economic sense, enthalpy is the equilibrium price, how we get there is the entropy.

First, of course is an understanding of what equilibrium is, if it actually exists. What is the equilibrium price in the housing market ?

The data suggest that the housing market is at equilibrium and that sales will increase if the mortgage rates decrease.

Thermodynamics may not be a great analog for made up financial / economic models.

Prince reminds me more of temperature, a known quantity that reflects the energy of the molecules in a system.

Thincrust is right about thermodynamics. The fact that his name is thincrust and not deep dish is further proof of credibility. Thermodynamics and electrodynamics are so encompassing that all of the other areas of science are essentially derivable from those areas of study. A more accurate comparison would be to compare the financial system to particle physics, the most bullshitted and bastardized version of modern science. The premises of particle physics (quantum physics, quantum mechanics) alone are self defeating.

Eric Dollard (look him up) said something like…..

“They invent words, then make a career of talking about the words they have invented.”

The 30YFRM is already down to 6.61% or almost 150 basis points in just 6 weeks.

Pssh….this is pathetic of a decline to say the least…maybe the naysayers are right, this time is different in these markets. I still hold out hope, however small, maybe these markets are the tail end of the Titanic rather than the front end like SF or Las Vegas..matter of time, so far it doesn’t look too encouraging.

San Diego: -2.1% (May 2022)

Los Angeles: -0.8% (May 2022)

I suppose I’ve been a naysayer so will continue to say nay… there’s been no significant correction here in San Diego and it’s pretty evident by the flatline close up in the charts above. These data are from October and just published (2 month or so lag). Just wait and see what the most splendid reports are going to be like in February and going forward. Ask anyone in San Diego what the market is like right now and they’ll tell you that it’s nuts. Junk 1400 sf stuff asking 1mil. Nice stuff selling for 1.2, 1.4 etc, and I’m only really paying attention to 92115. The city as a whole is seeing anything but a bubble popping. I’ve given my opinions as to why this is happening several times and usually get bludgeoned so will spare this comment of that info, but it’s pretty obvious to anyone living here why it’s happening.

A flat lined market for 18 months in SD.

The issue is no one wants to sell and no one wants to buy. Prices are staying up on the hopes that the fed will cut soon and RE will start growing again. It’s like cutting off a heroin addict. Home values were going up 40% YoY or more once Covid started. It’s hard for people to accept their houses aren’t worth what they were in May 2022 and homes values aren’t experiencing double digit growth every year.

I watch the market closely and homes come on the market at a 2022 price level. It sits for two weeks then gets marked pending and then is delisted.

I also can’t see how prices can stay elevated when the rent to buy ratio is so high. It’s more than double to buy right now. A home in my neighborhood rents for $4500. To buy it would cost $10K per month. How can that sustain?

Don’t count out the power of FOMO and insanity….apparently everyone else have tons of money…I must have missed that boat somehow…

There’s folks with money out there, and they’re not necessarily only from San Diego. Lots of tech folks are moving here from other locales. A couple of weeks ago there were close to 3100 homes listed and last week that dropped to close to 2700 with the new pending number being almost exactly that difference. What I’m seeing is two groups of sellers, those who don’t want to pop the 1mil mark so price at 950-999k and those who know that they can justify well above a mil so price at 1.2 and more. I’m guessing it’s something psychological realtors are telling them to do. My guess is anyone sitting on the sidelines has missed the boat. Rates have moved slightly down but around what they are now will be the new norm for a while. Folks who bought when rates were super low lucked out and got the “sale” rate. I seriously doubt you’ll see any rate increases in 2024.

One other thing to consider is that all of the money printed isn’t just gonna unprint itself. It’s there and raised prices of all assets, not just RE.

Prices are staying up because under normal circumstances we’d be in a recession and a dramatic rise in unemployment would ensure there’s a broad housing price decline across all cohorts of homes. $1.7T in federal deficit spending and high local property tax revenue will ensure there’s no recession outside of a black swan event.

So since 2016 houses went up 100% (a clean double) and prices have declined 5%. Wow this is great

Mathematically, prices only need to decline 50% to wipe out the entire 100% gain.

To get a big housing bust like 2008 you need mass unemployment, lots of low-quality loans, or both. Neither is true today.

There’s lots of bad loans being given to many of the people buying homes to rent out as Airbnb’s. You don’t even need to have a job to get some of these loans. And you can get them with little down payment. Once there’s a recession and unemployment goes up, many of those who bought Airbnb’s will scramble to sell and another housing bust will occur because the housing inventory will be saturated.

We are in a housing bust. Existing home sales have collapsed.

https://wolfstreet.com/2023/12/20/here-come-the-new-listings-of-existing-homes-prices-drop-further-demand-remains-at-collapsed-levels/

You can’t focus on prices right now (existing home prices). Price discovery takes a long time with an illiquid asset (without forced selling).

Here is the price chart from that article, with home prices through November:

The definition of bubble here is homes that have increased 180% since the year 2000??????

All that means is they kept up with inflation during that same period of time. An asset that keeps up with inflation isn’t in a bubble. It’s simply keeping up and is only an average investment by my standards.

The most splendid bubble : John Singelton, 82, an Aussie, net worth $800M, 10M Hawaii love house, dumped his sixth wife, 44y, after getting a heart attack. He married number #7, also 44Y, bc she makes him happy. Denis dated beauty queens, tv stars, 60 min reporter, high society ladies, who like his great sense of humor and buybacks.

$800 mil? Wheel him on in, I’m not a picky woman.

“My dear, would you like to be my widow.”

I don’t know if we can call it a bubble after 2024 if it doesn’t soften more. It’s been inflated way too long. Then again I’m super impatient waiting for “affordability”

Well I plan on buying a house in 2024, which with my luck means I’ll be buying at the peak and then we go down from there. :)

Will you buy it to live in it? (that’s usually what houses are for)

Yep, as long as I don’t have to relocate for a job. I need a 3 car garage at this point and renting a house with a 2 car garage isn’t something I can continue with. And I will also be keeping the 3 cars for life so selling those not in the cards.

Just buy it and live in it. Do like Warren B. and I did. Live in that house for the rest of your life. What you pay for it doesn’t matter one wit.

“I need a 3 car garage”

Sell one of the cars and use the funds for a down payment on a more reasonably-sized property that you can actually afford.

MM, not going to need a down payment. Cash buyer. I don’t finance my cars and won’t be financing my house. New job in 2024 is out of state and I want to make certain the full remote setup is up and running before buying that large of a purchase.

My argument still applies. If you had the money for three vehicles but didn’t put enough aside for a house, perhaps reconsider your financial priorities.

I recently had a friend complaining that he might have to sell his Maserati in order to afford a down payment on the house… I told him that maybe the house should have come before the Maserati.

MM, huh? I specially said I’m a cash buyer for a house. I have three paid off cars plus enough cash to buy a house right now without having to finance. I’m holding back until my new job early next year can for sure be done fully remote across country otherwise I’d have to move across country. At what point did I say I didn’t put enough aside for a house? Re-read and try to understand.

Z33, My advice would be to keep your beak dry, I hear a swan could arrive in 2024, a black one.

You have to live somewhere. Buy a house you like in a neighborhood you like

Just plan on staying in the house for 10-15 years.

Don’t over spend, invest in other assets besides your house.

You will be okay.

Its not a bubble, it was a jump 4 to 5 years into the future of existing price trends, that will slow the price trend momentarily while general inflation catches up, and then continue. Until the average age of first time homebuyers starts decreasing, its a sign of shortage relative to demand, and it is still increasing. Will take decades of massive construction efforts to reverse that trend, and thats never going to happen. I wager for Gen A, purchasing a home will be seen as the last step before retirement, to lock in a fixed price shelter payment, relative to rent that would increase 7-10% annually in retirement, and be unsustainable on a fixed income. Housing will no longer be something to build wealth, but merely something to avoid total wealth depletion in old age.

That’s quite the fantasy you’ve got there. Care to point to any time in any place where such a thing has even come close to happening? Even in hugely limited places like Singapore? Maybe Japan? Believe me, if it gets anywhere near what you described you’ll have far more pressing problems.

One place is like that: Hong Kong. If you do some research on how the resident there is got crushed, you will have some knowledge of that kind of system.

There is no mechanism for the US as whole to reach that lunacy and Hong Kong is already down 20% from their peak. There are no greater fools waiting to drive up assets.

Please tell us another good one.

Are you waiting for affordability by one income households or two income households? Two income households are the normal unlike in 1944.

The East up vs the West down.

I wonder if the higher general population density of the entire East vs the lower general population density of the entire West is causing this divide?

Or are housing prices higher in the West on average?

I don’t know what is causing this divide but it draws my eye

Prices in the West experienced a much greater increase during the Covid boom than they did in the East, at least I believe so. Especially in western Mountain towns like mine, prices increased 80-120 percent in two years, vs around 42% nationally. So even with 10 or 12% price drops, prices are still up massively from 2019.

What you are describing is just your local price gouging.

This, obviously, is just your own local egregious price gouging.

The weather is better out West. Less humidity and no hurricanes. ;)

You get all 4 seasons in the midwest but no scenery ….but on the plus side you can find affordable homes.

There was a massive property rush in the interior West during the pandemic, particularly in ski towns, everything went bananas. Also the economy of the West is very tech dependent (silicon valley money quickly arrives in the ski towns and the secondary cities like Denver and SLC). Tech was until recently off. The combo of those factors made prices run way up during the pandemic and now there is some correction. Not nearly enough.

Happy1 –

Those places you disparage tend to become more popular over time, which drives up prices…

A lot of the money that moved from Vancouver, Canada back on April 20th 2017 to Seattle moved back to Vancouver recently.

Looking at all the charts, there weren’t really any ‘dead cat bounces’ in Housing Bust #1. It was down down down…and then up up up. Then a short downturn this past year, now heading back up. Didn’t see that in Bust 1. I honestly wonder if in a year or two, Wolf will still be referring to this as a “Splendid Housing Buffle” and “Housing Bust #2.” I am in real estate and have been waiting for two years, and not seeing much of a dent here in the Rockies. Even a 10-12% decline since the peak isn’t overly dramatic when prices increased 40, 50, 70, 100+%, depending on location, during the Covid spike. The next couple years will be interesting. I’ve given up on predictions. When asked, I tell clients that in a year, prices will be lower, higher, or the same, and I absolutely guarantee it. I would like to see them come down, dramatically. I can broker transactions in an up, down, or sideways market. Affordability concerns me greatly.

I will never change the name of the series, “the Most Splendid Housing Bubbles in America.” I started calling it this way in 2017 to track the crazy home price increases in those markets. Even if prices decline a gazillion percent, I will keep calling the series “the Most Splendid Housing Bubbles in America,” manifestation of Dark & Dry Humor®

The pop is still part of the bubble or at least a crucial part of the trend. More here are hoping for the pop, rather than the peak.

If prices decline significantly, then the Splendid Housing Bubble moniker will be especially appropriate—as it will have proven to be a bubble!

This time around we don’t have a mass of resetting loan types, and last time around didn’t have Trillions of extra Stimmiez to fuel our drunken sailors.

It’ll end at some point, no matter what the used-house-sales-types tell everyone. The Fed has yet to engineer any soft-landings, and this time isn’t different enough to matter much in the end result.

I’m hesitant to say “this time is different,” but this time we have much more systemic debt, and significantly more complexity and interconnectedness (i.e. RISK) in our credit system.

Isn’t that different?

“Isn’t that different?”

Sure, different in how much worse it’s going to be, I suppose. :-D

This time around the gubment (or the “Fannies”, “Freddies” and “Ginnies”) own 90% of the mortgages. That’s the difference.

They even made a Song about it.

It’s called “I’m back in the USSR”.

Paul McCartney performed it on Red Square in Moscow after the end of the Sovietunion. He might still make it to Times Square this time.

Just closed on a house in Phoenix today. Why? Because I needed a house, the seller standoff isn’t ending, and I found one I can afford.

If the market dumps next month, that was me, you’re welcome!

Hope you got a good deal. Prices in not so good areas of Phoenix are at a premium. The Fed is criminal for what they’ve done. I know what you mean, though. I’ve said if I take the plunge and buy again at these outrageous prices, we’d have the biggest crash in a history. It would be just my luck.

I think too many people focus solely on monetary policies and ignore the demographics of the population. More people at the end of their careers $$$, more changing jobs $$$, and more retiring in an upcycle of the market $$$ add to the climbing prices despite rising rates.

Don’t give the fed too much credit.

The Fed bought billions of MBS and hundreds of billions of federal debt in 2021 and 2022 well after any pandemic crisis, driving mortgage rates way below market and causing the 30-40% run up in home prices. There is no one else to blame, this collosal mess is courtesy the Fed.

Seriously? The unnecessary QE during the pandemic, the unnecessary helicopter money dropped in everyone’s laps during the pandemic, ultra low interest rates for years even when not needed caused this mess. It was Fed and government intervention that gave people the means to move and buy up houses all over the place, especially during the pandemic. It was not normal migration due to changing jobs or retiring.

If you like the property, and you can afford the payments, I think you made the right decision. Just watch out for the town coming in and raising your prop taxes because the sale will trigger them to reassess.

Congratulations!

Not one person in this commentary knows what will happen with prices, including myself, and I am in the real estate brokerage, construction, investment and management businesses. Best thing to do is buy when you’re ready or when you need to.

One thing is for sure. The folks predicting a crash for the last five years missed out on one of greatest wealth building markets in history. Maybe that’s why they keep wishing for a crash.

YouTube is littered with real estate crash bros predicting a massive crash. With some click bait headlines stating we are already in one. But you are right, more correctly the are ‘wishing’ for a crash, as a few of them have admitted they are ‘waiting’ to be able to afford a house. The worst one out there is Nick Gerli of ‘Reventure Consulting,’ which is a consulting company in his own mind. He called it an absolute ‘top’ in June 2021, which was only halfway in to the boom. Amd posts weekly videos about the devastation in the housing market. It’s quite humorous. More humorous are the fans thanking him for his content every week.

Crash Bro is big business now.

There is no shortage of idiots like me who would gobble up negative predictions, because it gives us dummies the illusion that we’re finally ahead of the curve.

Then I found the channel you mentioned, and other charlatan “analysts” on Twitter, and realized these people are just selling exactly what their audience wants to believe.

Doomsday seldom arrives on time, and a lot of folks missed out on opportunity believing the crash narrative these past several years.

Yep.

In the Seattle area prices have tripled in the last ten years [2012-2022].

So what if they drop 10% in 2023-2024?

The population and the financial ability to buy a house here are going up much faster than the supply is increasing.

Where can prices go but up [in the long run, especially factoring in inflation and deficit spending]?

In many markets, the top of the chart resembles a two-pronged fork, which might skewer today’s buyers.

If inflation takes off again, things will get interesting. Good news is priced in, bad news is not.

Plus, as those reverse repos on the Fed’s B/S continue to drop, QT could really start to take hold of matters, assuming the Fed does not panic (again) and lick the boot of Wall Street. The boot is still wet from the last panic.

I’m beginning to believe it’s not a bubble. It’s looking more like a permanent adjustment higher in prices due to the gross excess of “new” money that was printed, that will apparently never be removed.

About $1.2 trillion has been unprinted so far since July 2022.

“Stocks seemed to have reached a permanently high plateau…”

Renowned economist Irwin Fischer, 9 days before October 1929 crash

Oh! that’s good!!

“I’m beginning to believe it’s not a bubble. It’s looking more like a permanent adjustment higher in prices due to the gross excess of “new” money that was printed, that will apparently never be removed.”

The Fed’s stated monetary policy continues to mislead people into believing inflation will be averaged over time to achieve a 2% target, but the reality is any above-target inflation will never be reversed as that would create a deflationary threat to our fragile artificial overblown asset markets.

There should be no dispute about this. We just saw 20% inflation in three years, which is 14% above target, yet the Fed has no plan to reverse or average down the inflation overages. The actions and results stand in complete contradiction to stated monetary policy.

I wish the Fed would be transparent and honest by formally revoking its averaging regime for inflation targeting. The Fed should clarify that 2% inflation target operates as a floor. To the extent there are inflation overages, the overages will permanently embed in prices, meaning future realized inflation will be something above 2%, and perhaps multiples of that, as witnessed during the 2020-2023 period.

Monetary policy misrepresentations do great damage to the public, particularly those parties who need to accurately predict future inflation.

Look at that Phoenix chart since 2020, and the Fed let it happen. Prices aren’t down nearly enough. It’s criminal.

Bernanke caused the GFC, by restricting the monetary base, or required reserves, for 29 contiguous months. The money stock was restricted for 48 months.

Powell has restricted the means-of-payment money stock for 21 months. If Powell continues with holding the money stock constant, house prices will show their greatest declines in just another couple of months (>3 months).

The bond market is ratchetting rates downward. I can give you all the dates I’ve got money coming due next year. The bottom will fall out of rates right before each of those dates. One of those dates is March 21st 2024 so rates will fall off a cliff again right before then. January 4th, February 12th, February 26th, March 21st and a bunch of money in October.

The data show an interesting bifurcation. All prices that are lower than their highs are in the west or mountain states. All prices that hit record highs are in the east and midwest. No exceptions. I don’t know what to say about it, but it is strange.

“All prices that are lower than their highs are in the west or mountain states.”

Also Dallas, which is only kind of in the West.

Also, they’re off their highs from over a year ago — May through July 2022. There are other metros on this list that are off their 2023 highs, but that’s not a big deal.

Ya’ll saying Texas ain’t in the West? My oh my.

Well considering the war between the eastern civilizations of the world can end in an instant if our leaders look at a globe (map of the earth) and turn it enough so that the US is on the right side and asian countries are on the left side relative to the the north-south axis, all of this posturing between east and west will evaporate. The reality is that there is no conflict between east and west. They are non-specific terms to obfuscate the attacks of the Post Roman Empire (US-British-French) on the rest of the world while framing it as a religious and cultural war. The situation is similar on a continental scale in the US between eastern and western geography and the red / blue 2 brain cells max politics.

I meant to write the wars between the eastern civilizations and western civilizations (east vs west – a false rhetoric of the last 20 years)

Fort Worth is the easternmost western city; Dallas is the westernmost eastern city.

I have called 12 of the last 2 housing bubbles.

Tyler, I am on a similar boat, thought the 2018 housing price dip that occurred when the FED started rising interest rates was the end of the current bubble. The FED reversed course at the end of 2018 and when Covid hit I was shocked at how fast housing prices climbed, reminded me of the 2006/2007 runup. It would be interesting if Wolf had a sentiment indicator based on the comments here. In 2022 we would see peak negative sentiment with most agreeing that the bubble was bursting as interest rates shot up. Then we would see a climb toward positive sentiment as the comments have shifted to the possibility that the bubble will continue to grow as interest rates drop. As we move further away from 2022, it becomes clearer to me that the momentum is building toward the next leg up in housing, so for those that are stuck in bubble burst mentality, I wish you the best of luck as the housing market passes you by.

I hope you’re putting your money where your mouth is and levering up to buy every house you can.

Einhal, I got lucky and read the situation correctly and bought as many houses as I could during the 2008 housing crash. It wasn’t much since I wasn’t a rich man, but I did what I could. I don’t think in my lifetime I will see another opportunity like that, so I decided that whatever leverage I have from my 2008 housing investment I would invest in something else, which primarily has been the stock market (Unfortunately not as lucky reading the situation there). That way I am not putting all my eggs in one basket. My message is for those that need a place to live and can freeze their housing costs at today’s rates and prices and can look forward to the day they can refinance at lower rates and actually reduce their housing costs. A severe crash will come at some point, but when will it happen? People have been waiting for it since, I don’t know, around 2016, I called it in 2018, then I thought maybe Covid would do it, but still no crash. Instead prices went up by a lot and people waiting for the crash may now be priced out. The economic games are sad and I wish it wasn’t like this but it is what it is and you have to make the best decision you can for yourself by being knowledgeable, using critical thinking, avoiding herd mentality, having the right balance between greed and fear, and knowing what is best for you and your family. It’s hard and you don’t always come out the winner, but at least you feel that you tried your best.

beatlme, that’s a very down to earth way to summarize things and an honest telling of your position and nothing controversial about what you are saying

By the last third of 2019 I saw many signs that the economy was slowing, which seem to be a delayed effect of shifts made during 2018. Construction work was slowing down, flux in the labor pool and wages was increasing, and interest rates were shifting. You’re not the only one. I see very little discussion about this considering that it seems like a key portion of the recent economic timeline of the last 2 or more decades. The importance of this time period is that it shows that the US government is running an outright pyramid scheme (which is not a new concept). What was shown in 2019 and 2020 is that the US government is willing to move goal posts, make up rules on the fly, pick winners and losers, shift heavily towards more of a state controlled economic system, and stick it to those who try to operate based on the logic of limiting risks, practicing prudence, real work, integrity, and innovation.

I agree with all this. Functionally, we’ve become a banana republic over the past 10-15 years. It’s just that the rest of the world hasn’t figured it out yet.

Up in Canada the Chinese cities lead everything they move first in price and the rest of the country follows those cities.

And this is how media reports the same information…..

“Home prices post biggest gains of 2023”

https://www.cnbc.com/2023/12/26/sp-case-shiller-october-home-prices-post-biggest-gain-of-2023.html

The 20-City Case-Shiller index inched up 0.1% month-to-month, the smallest month-to-month gain since it fell in January and now roughly matches its Jun 2022 high.

They’re talking about the year-over-year gains which are a result of the base effect from the plunges a year ago.

I think we should start a house price pool – like the old office football pools.

All the so called housing experts here pick a case schiller price for Dec 2024, or whatever date and sends Wolf $100. Winner keeps half and Wolf keeps the rest for keeping us all informed about the economy and well entertained.

442

There has been futures trading based on the Case-Shiller index for 2 decades(?), the CME Metro Area Housing Index Futures. You can just play with that. I know a market-maker for these futures (at least he used to be). Not a high-volume thing.

Curious if you have any opinions on housing prices in desirable resort towns and how that may be affecting the large metros or suburbs.

I think that remote work is here to stay and certain percentage of knowledge workers have fled the cities/suburbs for good. My anecdotal observation in my small mountain town is that home prices have somehow hung onto peak prices even through interest rate rises (3%->7%). Could metro home prices be falling now because some percentage of higher paid workers have relocated and are refusing to move back?

Remote work is NOT here to stay, at least not as it existed in 2020-2022.

I am in my 30s. I know many people from college and grad school across many industries.

Under 10% are still fully remote. Most are hybrid. Hybrid is great, but it still means you have to live sort of near your job.

It’ll take a while to unwind, but unwind it will.

I second this.

Remote work is going away and most companies want people back to office 3 or 4 days a week.

I speak from companies I know and company I work for.

The company i work for laid off lot of people and most of them were remote.

Ditto

My prediction? I think this winter is going to be the last, best time to buy a house in our lifetimes, so take advantage of the “low” prices while you can.

Case-Shiller is clearly saying the “bust” is over. In the next few months we’ll see the usual winter pullback in prices.

Next year, when mortgages go under 5%, is when the bubble goes much higher than anybody ever thought possible.

Too bad they don’t have a vaccine for FOMO.

The 30 year mortgage rate generally hovers at 3% above the 10 year treasury.

If you think mortgage rates will be under 5%, you’re saying that you think the 10 year will be back down at 2% next year.

I’ll take the other side of that bet.

FHA mortgages already down to 6.06% today.

So very hard to know the future…

Under 5%, highly unlikely given the long-term average 30-year rate is 7.76% since 1971 and inflation is still inflated.

There’s a disconnect in the timing of your predictions. You may be right mortgage rates can go under 5% next year, and house prices can correspondingly go higher than anybody thought possible. Contrary to your assertion, though, this will probably still not be the “best time to buy a house in our lifetimes.” It will only mean housing is even more overpriced in the short-term. A “lifetime” is a very long time and I suspect at some point in that extended timeframe prices will once again align with fundamentals.

But prices don’t have to drop to historic or income based norms for you to be wrong, prices only need to get closer to those norms than they are right now.

I bought a lot of homes cash in December 1982. So far in most cities that was the right time.

“Next year, when mortgages go under 5%…”

You sound quite sure of that….

There is still an excess of money pumping up the economy including stimulus in the factory area. If we have faith in the “C suite” they should be able to pump up the stock prices with buybacks filling the capitalist’s pockets; using already corporation borrowed money. Companies with debt to refinance at higher rates or better yet not refinanced due to credit risk should help cool off the overheating.

Mr Richter I came across an article about Wall Street derivatives. The article says 3 US banks: JP Morgan Chase; Citibank, and Goldman Sachs hold 157.3 Trillion dollars of derivatives. 77 percent of all the derivatives held in the USA. These trillions of dollars in derivatives vastly outweigh the assets of these banks. Is this an issue we should all be concerned about or is it just the way business is done these days? Warren Buffett calls these derivatives trades a ticking time bomb. Do you agree?

Stock options are derivatives, and they’re huge. Interest rate swaps are derivatives, which banks use to hedge against interest rate risk, and what caused the banks to collapse in March was that they did NOT engage in interest rate swaps, or not enough, to hedge against rising interest rates. Airlines use derivatives to hedge against fuel price spikes. US oil and gas producers use derivatives to hedge their production. Every time you see “hedge,” think derivatives. And someone is on the other side.

Notional value is meaningless. If you buy $1,000 in call options, the notional value could be huge, but the most you’re at risk for is your $1,000 investment. And someone else makes that money. Zero sum.

Buffett is the biggest hypocrite ever. His companies use derivatives all the time.

I think the problem can arise when institutions aren’t using derivatives to hedge against some exposure they have, but as an independent gamble.

The problems that DID arise this year was that the “institutions” did NOT use derivates (interest-rate swaps) and collapsed.

Hedging is used in agriculture all the time. You just need a knowledgeable banker who won’t pull the plug on you when making million dollar a day margin calls.

Forgot to add: hedging means you have the cash asset on the other side offsetting the futures (derivatives) loss. This is because we are basis traders, I did it for almost 40 years.

Ok thanks that article had me all stirred up. I thought 2008 was about to repeat. Thanks for the info sir.

Spot on Wolf. It’s like when certain individuals (cough, cough JPM’s Kolanovic) claim 0DTE options are going to *cause* a 25% 1-day drop in equities. Come on, now!

I just bought 2 SPY 1 month 470/465 debit put spreads. It cost me $220. The notional value is $187,000, but the most I can lose is $220. I don’t see how these hedges are some kind of ticking time bomb.

“Buffett is the biggest hypocrite ever.”

Essentially true but is that fair?

We have to play the existing game or be marginalized – and maybe better men opt for the latter. For the rest of us there is latitude in how we play.

[I can name two other activities that Berkshire participates in that WB has stated he is against.]

I also thought these articles about the derivative time bomb were hilarious. $157 trillion in notional! OMG! So deceptive.

Steelers Fan

“The article says 3 US banks: JP Morgan Chase; Citibank, and Goldman Sachs hold 157.3 Trillion dollars of derivatives.”

This is the epitome of “systemic risk” in my opinion. The nature of individual derivatives (e.g. a small lot option position) is relatively unimportant. The risk lies in the “counterparty risk” which ties your holding (and your market response) to your expectations of the ability of the counterparty to perform their part of the transaction. Tied to that is the “first mover advantage” phenomenon, which can lead to panicky “runs.”

The bigger the pool, the more interconnection, and the more likely a bout of fear leads to mass liquidations.

Long Term Capital Management (1993-98 RIP) is one of many examples of the rush-for-the-exit phase of portfolio derivative positions previously thought to be logical. They left much carnage in their wake.

Just one guys opinion, of course.

Those charts are shocking. Not sure how these prices are sustainable…

If this article I read has its facts right. Goldman Sachs has 538 Billion in assets and holds 51.6 Trillion in derivatives. I mean it seems like they can make a bet on something and force the market to make the trade profitable without the collateral to do either. The three major banks mentioned in an earlier post hold 157.3 trillion dollars in derivative trades which is 56.74 trillion more than the GDP of the entire world. Does QT ever affect their ability to do stuff like this or does the party just keep on going forever.

Housing is just like stocks, bonds, and all other assets.

Never before have investors paid so much for so little.

Ultimately, home prices should be a function of what they rent for, and stock prices should be a function of dividends/earnings.

Right, now they’re both grotesquely overvalued.

But who’s to say rents won’t just climb up instead of house prices coming down?

I’m not really clear what keeps rents in check other than landlords’ affordability criteria. And I suspect those affordability criteria will quickly get relaxed if they start getting in the way of being able to make a profit, as is currently the case on any recent investor purchases in many locations.

Where is the money for rents to climb up going to come from?

Unlike luxury goods or stocks, there’s a limit to how much of the housing stock can be rented by the rich.

“Where is the money for rents to climb up going to come from?”

People will cut back on eating out or buying stupid stuff on Amazon when they have to choose between that or their lease.

Everytime I had a landlord raise rent, it was still cheaper to stay & pay because moving would have cost more.

MM, and what would that do to the rest of the economy if everyone was spending all of their money on rent?

It would be like a neo-feudal society.

Most of us aren’t putting every spare penny into housing. I *could* pay 50% more in rent. I’d be utterly miserable at having to do it as it means the landlord sucks up all the fun money and savings. But it’s not like housing is optional.

But many people are. Unless landlords band together to collude, how do you think the pricing power would work?

“what would that do to the rest of the economy if everyone was spending all of their money on rent?”

Maybe folks would learn to live within their means and get some financial discipline out of it.

My previous roommates were always short on their portions of the rent, yet somehow found the $$ to order DoorDash and get stuff from Amazon on a weekly basis.

Also, consider the comment above about not being able to afford a house because he “needs” a 3-car garage for his three cars.

Most people live much more pampered lives than they’re willing to admit.

MM, even if you assume that is true, why should all the productivity of the economy inure to the benefits of the landlord, and no on else? That’s ultimately what you’re advocating.

“But many people are. Unless landlords band together to collude, how do you think the pricing power would work?”

If that were true, I don’t think we’d be seeing anywhere near as many “drunken sailor” posts by Wolf as we do.

In normal times, I think the “I want a good tenant” landlords keep the “whatever the market will bear” landlords in check. But our local market is now starting to see some staggeringly high asking rents, because that’s what’s needed to cover the carrying costs for the over-sized new builds that are struggling to sell now they’re impossibly expensive, and to cover the mortgages for the latest round of rental investors. Some of them are being achieved because there’s not much supply, and now the broker comps are kicking in for the new listings.

Einhal, look at it the other way:

Why should a landlord get stiffed on rent just because spoiled college students “have to have” their $10 mocha latte every morning?

Competition from other landlords & rentals, really.

But I’d argue landlords still have pricing power. Not sure what % of apartments are rented for students by their parents, but there is a lot of that in the Boston area.

I had one landlord brag to me that he could charge whatever he wanted because there was no shortage of wealthy college parents who would sign leases for their kids.

(NB: this was circia 2015. This landlord owned ~20 properties, mostly tripple deckahs).

Affordability, rent and mortgage 6,7,8 times average annual income of middle America.

Inflation wins as long as buyers are willing to buy less with more.

I think it is more so that Americans are 5 to 10 years behind in understanding the value of the US dollar and get the impression that assets are overpriced. Assets are likely overpriced, but the dollar being overvalued relative to it’s supply is the real problem. The financial class get a huge running head start and shifted into assets. That’s how things got this way. There are no rules to the game. If the people running the poker game start to think they will lose, they will grab the money off the table, flip the table over in the face of the players, and run. That’s what happened in 2019 through 2021. If the game really goes the wrong way and the house really loses control too fast the house pulls out a gun and shoots all the players in the face and the paper money is irrelevant because there will be no debts to be paid to the dead. That’s the financial motivation for wars and that is the motivation for the US to attack china.

What you are telling us is that Americans are under paid.

It’s all relative. It depends on what you are considering and what you are comparing it to. Simply put, if you are comparing 2023 wages to 2019 wages, many americans are getting paid less, some are getting paid more. I believe one of the goals of the massive money printing was to devalue wages of the workers in industries that require a large labor force, without destabilizing the business environment. This is what made inflation a preferable path compared to a recession. Wage pressures will building heavily by 2018 for sure and continued. Those were wage growth pressures that were building but unrealized for many because companies kept asking more of workers while keeping wage growth very low or flat. With that kind of labor market and wage pressures, too much of the balance of power would eventually shift towards workers in ways that would likely be destabilizing (strikes, massive job turnovers, etc.) so instead of going through a recession to restore the balance of power back to being heavily skewed towards large corporations and employers, inflation was used to keep the wages flat for longer without having a recession. Pay has gone up but not anywhere near to what has been lost to inflation. The goal was to have the business profits (price increases) front run wage growth by a minimum of two years so that the lack of recession and continued growth of the businesses occurred by skewing the wages. This will continue. People may still be able to squeeze out raises, but those raises will usually have a two year delay at least relative to what has been lost to inflation (price increases). Let me put it like this………the companies increase prices and hold that level for two years. Workers get too grumpy and finally after two years the company has to budge some and give in to some amount of wage increase. In the meantime they got away with asking more money for products and services yet their labor cost did not increase. By the time they increase the wages after those two years, they increase the prices again and the workers feel better and it takes a whole year or more before the fools realize that things are more expensive still. They get an increase in wages and then prices go up more. This process will stop like a person who takes a good beating and finally stays down. When the workers can eat another two year period of inflation and then finish that off with no increase in pay, there is a chance that the cycle of inflation is reverting to what was possible in the past of much lower inflation rates. (I’m not assuming or hoping for 2% inflation in the far out future though no matter what happens). This equates to workers getting their spirits broken and accepting a loss. It often takes people a long time to accept a loss. They will be worse off but the real detail is that they will need to consciously accept the loss and lower standards instead of the loss being realized long after it actually occurs.

Which leads me to the conclusion that monetary policy is still in control of the markets.

More importantly, they intend to engineer an outcome that inflates the economy, over time, that covers all the losses from a renegade banking system, saymo, saymo for the past 50 years.

Of course. What else is even an option anymore.

What about East Mercia? – Asked by the Knights who nit! “Ikky Ikky Patang!”

The worst economy is unemployment with a loss of all benefits, income, health insurance, home, family and human resplendence.

From that perspective, the last thing I want is a screeching halt to the good times. The Fed screwed it up by pausing, reflating asset bubbles that had deflated a third of the way.

You have to have an Ivy League education to be so intellectually refractory.

At the end of the day, value is a moving target.

Seems like supply will just need to outstrip demand considerably and unless something unforseen happens housing prices will generally stay elevated as lots of building going on but also lots of pent up demand.

Importing demand is a good way to rig the system. Immigration as an economic numbers and averages manipulation strategy vs a moral or quality improvement strategy. Low fertility rate and low US-born citizen birth replacement numbers are great because we can import population growth while suppressing the power of the local people so they cannot oppose destabilizing and economically detrimental policies. Population growth without a growing a unified opposition is an excellent strategy if you ask me. You can drown out any opposition and have a continuous supply of people who have undefined legal status who are afraid and not knowledgeable enough of the system to know what is going on. Their kids might figure it out. By then, those kids are not desirable as workers so bring in more people who can be taken advantage of and promote things to reduce the births of the native born population.

Very well written satire.

On the ground I am beginning to see some very small cracks in the consumer. 20 year re investor and licensed in CA & AZ ( live in San Diego) Recieving an uptick in sellers responding to my cash offer marketing in Phx. They have this in common.

They bought well, would have several hundred k equity from original purchase with a sub 4% interest rate.

They took out a heloc and have spent it.

They still have equity, but maybe(barely)enough to sell with traditional commissions and fees. Or maybe not.

They are employed but were not able to qualify for a new refinance. AND cannot afford the 1st and second any longer. ( several have stopped paying)

My offer ( nor others like me) won’t get them out of there situation and I have little incentive to buy anything but a GREAT deal right now.

So is it possible in a upswing market we have consumers who look good on paper but are falling apart with very few options. Equity makes little difference if you can’t pay your bills. If the market continues to largely trade sideways and we see even a small job losses we may not be on as solid footings as numbers show. People have more access to all kinds of credit these days. Stronger mortgage standards and higher credit scores don’t prohibit people from making poor choices. 🤷

I think the cracks in the system is people not working and living off of other people through financial paper games. Based on government intervention, what do the cracks matter at this point when the government shows over and over that it’s willing to come and patch cracks that amount to anything by bringing in a money printer on trailer and injecting money into any crack they don’t like. As long as the cracks are on the roads that the financial class drive on, they don’t mean anything anymore and don’t indicate anything. Since you’re in San Diego and seems to be using the roads that the financial class use, I would expect those cracks to not amount to anything at this point.

True, much of the success of the iPhone came through tax payer funded creativity. Apple packaged a bunch of it together and now just withholds advancements so they have something new for next version. Not sure I ever saw my return on those investments!

This is october data, which is when rates peaked. Since then the 10 year is down over 1%. I don’t follow mortgage rates, but it’s probably down a simllar amount. The higher rates brought down sales volumes, but some buyers are stil paying what ever is offered to them at these sky high prices.

In the last 2 months the bubble probably already started inflating again.

Here is November median price by the NAR — I’ll just repost it here since you might have missed it above. The median price dropped a bunch in November.

Mortgage rates won’t make any difference at all until they fall a lot more — if they do. They’re at 6.6% now.

It took 2.5-3 years for the last bubble to start the sharp drop. From what I see we are at the 2 year point with a choppy top, not a smooth one like last time.

From a topping perspective, it would be surprising for the market to drop sharply until another year has past.

And of course we do not have the adjustables, adjusting higher this time.

Give it time.

Wolf It would be interesting to look at these prices compared to that of gold. I suspect that they might look slightly worse than what you have pictured

In terms of barrels of oil to buy your shelter (2000 – 2023) house prices are even worse. Copper & housing follow an almost parallel track however.

And if you look at home prices in terms of Beanie Babies, they look amazing.

Ha! I knew a couple down the street in the 90’s who were serious about funding their daughter’s college education with Beanie Babies!!

You speak truth, Johnny5.

since 2000

housing has tripled

gold has gone from 270 to 2050 so 7.5 times

just want to add timing matters from 10 years housings doubled and gold has gone from 1200 to 2050

timing matters

since 2013

housing has doubled gold has gone from 1250 to 2050

since 2020 golds done nothing housing is up 33%

The right thing to benchmark against is household income, aka the affordability metric. People buy payments, not prices.

From 1/21 through 12/23 (three years) we’ve had what? 20% inflation (compounded?). I look at these graphs and take 20% off the top due to the deflated value of the dollar. As others have pointed out, if you looked at the Case Shiller numbers in “real” dollars – or against inflation hedges like gold – the spike is much lower.

What about if you look at it in terms of actual cost? Very few get on the housing ladder with cash. The combination of price and interest rate rises has spiked the cost into the stratosphere.

Google “Inflation is nearly back to normal. But high prices have changed Americans’ lives”

First article I’ve seen from the mainstream media that demonstrates how a return to 2% still means that all of the previous price increases stick, and how a booming housing and stock market doesn’t benefit everyone.

I see your point but prices almost always go up just at a lower rate. You have to offset the recent inflation against wage gains and those to come. For example, several large employee groups, such as fast food workers in CA will go from just over $16 to $20 minimum wage. This is s good thing as significant wage increases in this type of industry can be offset with minimal price increases. Lots of other states/localities increasing minimum wages as well. Admittedly rents are significantly higher, among other things.

What would be interesting in how inflation has increased relative to wage increases. Drunken sailors are not called that for no reason.

How is it a good thing when most all of those ‘workers’ in fast food will be fired and shown the door to the street in days?

Glen,

“What would be interesting in how inflation has increased relative to wage increases. Drunken sailors are not called that for no reason.”

Adjusted for inflation, “real” per-capita disposable income is up by 4.3% year-over-year in Nov:

To provide a several dollar raise to fast food workers very little needed to be past on to the consumer. Some well run franchises the impact is minimal. Several good articles lately on the topic.

Wage growth vs. cost of living doesn’t have to be a zero sum game. The basis of most human civilizations and things that have been considered progress are the result of things not functioning off a zero-sum relationship. Without some mix of innovation, increased productivity, increased satisfaction and fulfillment, and increased standard of living, there is likely to be something much more negative than the neutral situation of a zero-sum game. Agriculture, Manufacturing, Skilled Trades, Engineering, Scientific Research and Development, Practical Accounting, and Quality Management have all resulted in growth that seems to show that human cooperation and activities can result in trends that are mutually beneficial to the majority and not a zero-sum situation. I wish I could say that it were that simple though. I get the impression that the zero-sum vs positive growth and benefits for most perspective is reinforced or falls apart based on the period of time under consideration and by changing the bounds of the timeline under consideration changes the summarized results profoundly. The human impact on the conditions of the natural environment, ecosystems, and landscape are I think the largest and most serious example to be considered for the analysis of whether or not a zero-sum game or even a mutually beneficial positive growth situation can be maintained in perpetuity or at least an extremely long time scale in comparison to recorded human history. Agriculture has profoundly benefited people, but it has also profoundly changed the local and even continental ecosystems and climate regions. Manufacturing has provided wealth distribution and easier living but it has also been consuming and reducing the physical mass of living things on the planet. There is no going back to being hunter-gatherers. It’s not just a matter of more people, there are is vastly less physical mass of living animals to hunt and quantities of meat out there to be had in the natural environments (what’s left of them). The green revolution of agriculture brought us to the 1900’s era of changes and progress. The industrial revolution overlapped the green revolution and added another layer of change and easier living. The data and information availability revolution is causing many shifts now. (I mean, where would we all be without our precious social media right?, just joking, that’s not what the whole focus is.) How has valuation and investing changed and been affected relative to 25 or more years ago by the quicker access to data and information, pricing, vastly faster transaction speeds, and an exponentially larger set of eyes and mines combing over and getting involved in investing compared to just a 3 or more decades into the past. Thankfully the government can invent new things like 401k’s to juice the system harder so that the average fool can be forced into the gambling hall and shaken down every so often. We were all waiting for the shake-down right? That’s what we learned from the previous recessions. But there are no rules to the game and so when everyone has finally learned their lessons, the best ways to shake down those who have learned the lessons of the past is to simply change the rules to the game and shake them down from a different angle………………Inflation + No Recession = Smile in Your Face while still having the same overall goals and results.

Or instead the workers can be let go…interesting article today about Pizza Hut in California laying off all delivery drivers and shuffling that function to a 3rd party like Doordash, Ubereats, Grubhub.

Pizza Hut just outsourced that end of its business to companies that specialize in it. Other restaurants did this a long time ago. Nothing to do with minimum wage.

Einhal,

“First article I’ve seen from the mainstream media that demonstrates how a return to 2% still means that all of the previous price increases stick,”

Is that a surprise to you??? That is how consumer price inflation works. And always has.

When consumer price inflation ends, prices don’t broadly fall back to where they had been. That is just NUTS to assume. Where does this BS come from? That would be massive “deflation.”

People have gotten huge pay increases, many of them by changing jobs. People that now make $100,000 but made $80,000 three years ago, they would need to give up that $20,000 and go back to making $80,000. That’s what you’re talking about, and that’s why deflation cannot really happen because it would wipe out those salary gains. Only a catastrophic collapse of the labor market would produce that. And the COLAs would need to be reversed, etc.

People that complain about lower inflation only meaning that prices rise more slowly but don’t go back to where they had been need to get their head put on straight.

I know that’s the way it works (although it shouldn’t) and no, it’s not a surprise to me. But it is a surprise to the average American, because the media presents it dishonestly, as though a slowing in the rate of increase constitutes a decrease.

I don’t, and never have, bought the deflatoin bogeyman. I think it would be a good thing in terms of restoring trust in the dollar.

You are right that many people (but not all) got wage increases, although I don’t think the wage increases are that productive when you consider the price of housing and other assets (I consider asset inflation just as bad as CPI inflation).

I don’t see why the now 79 year old widow who had $400,000 in savings in 2019 deserved to have 25% of it confiscated. That’s who inflation hurts, those who had savings but don’t work.

Many of those people now ‘making’ $100,000 a year would be lucky to get $20,000 and when they don’t want that they’ll fall to ZERO as the USA economy gets rid of a lot of those people.

I totally disagree that a return to the past prices is a “catastrophe.” That reads like a line straight out of the FED’s playbook. It would only be a catastrophe for the rich. The working classes and the poor would benefit.

And the middle class would benefit too.

BS. If overall prices decline in a persistent manner, of the kind you’re dreaming about, wages will decline, including yours. The whole economy adjusts to declining prices. If my company has to cut prices in order to sell its goods or services, I’m going to have to cut costs, and I’m going to start with cutting wages, and since every company will be in the same boat, employees can job-hop from lower-paying job to lower-paying job. You might enjoy that (“blow it all up”), but it would be catastrophic for the economy.

Wolf, for those of us who live below our means, it would be great. Our salaries dropping by 20% with prices dropping by 20% also means we’d be better off.

This is just a bunch of bullshit piling up here.

if you earn $100k and spend $80k (“we live below our means”), 20% deflation will shrink your income by $20k to $80k; and your spending by $16K to $64K, and instead of saving $20k, you’re saving $16K.

But that may be just dreaming because you will likely lose your job in the cost cutting, and your income goes to $0k.

If you look back at the FED notes. The main reason for QE was to reduce unemployment which was above 9% at the time. They new it would drive up assets.

Here is a nice quote to understand the thinking for the economic dial and knob turners. To put this in context, losing the purchasing power of your savings because of inflation.

” We should be happier to have a job than to have our savings protected.”

~ Christine Lagarde, October 2019

“The main reason for QE was to reduce unemployment which was above 9% at the time. They new it would drive up assets.”

No, initially, the main reason was to drive up asset prices, especially prices of homes and MBS, to save the banking system. And then, after the banking system was saved, the main reason was the wealth effect, and as asset holders got even weather, it was then supposed to stimulate the economy as the wealthy would be spending some of their gains. Bernanke explained this to the American public in an editorial. Obviously, all this can be dressed up as concern for employment.

The natural state of the economy is a slight deflation. Because people get more productive and do more with less. Productivity improvement is the real deflation and doesn’t necessarily require cutting costs or wages. Everyone benefits from increasing productivity.

What’s different about rents and housing prices?

It’s the Fed that formally established a 2% “average” inflation targeting regime.

Until that formal policy is reversed, wouldn’t reasonably people expect periods of above-target inflation to be followed by periods of below-target inflation, so that inflation averages to 2%?

If the Fed won’t allow averaging to happen, the public should be warned about this, given it contradicts formal policy that was stated earlier.

“HOUSING IS THE BUSINESS CYCLE” — Edward E. Leamer

There have now been 12 boom/busts in housing since WWII. If Powell holds the line, we’ll get through this one too.

So, I am not sure this qualifies as a bubble and is nowhere near the bubble of 2004-2007, when I was looking for a house in South Florida. Then the subsequent crash in 2008-2010, which still has lingering effects today. I think today we have market driven prices. We had rock-bottom interest rates during the pandemic and those who wanted to buy homes or upgrade to bigger homes did so. They are now locked into interest rates that are less than half of current rates, therefore they are reluctant to put their houses up for sale. My neighbors tell me that, too. They are stuck with the golden handcuffs. This all causes fewer homes to come on the market with many more homebuyers chasing very little inventory – classic supply and demand. It will take a few years for all of this to iron out and it will depend on how fast and how long it takes the Fed to bring interest rates back down. Cheers.

Again, those people who are reluctant to sell also are not going to be buyers.

It’s a net zero change.

Not so sure about that. We’re seeing people nearing retirement (including early retirement) who would normally sell and downsize instead turn landlord and buy with cash essentially released from the massive asset windfalls they’ve enjoyed.

Lots of retirees are trying this in the Greater Boston area, too. But, financially-speaking, they are bringing a knife to a gun fight.

My former neighbor across the street is a retiree living with her son (who has special needs as a result of a car accident 25 years ago). She actually sold her house and moved to Florida because she could not manage to purchase a second home as an investment in the area.

The kicker is that when she sold her house – she did so at a price fully $100K above the upper bound of the Redfin and Zillow estimates to an investment group that gave her 8 days to move so that the young couple (who both had biotech jobs) they were renting to could move in upon their agreed upon date.

MW: A record share of S&P 500 stocks have underperformed the index in 2023 as ‘weirdest bull market in decades’ marches on…

Patch: Pizza Hut to Lay Off Thousands Across Southern California

Citing California’s industry-wide minimum wage increase in 2024 and a switch to third-party delivery apps, Pizza Hut is ending an era.

Pizza Hut just outsourced that end of its business to companies that specialize in it. Other restaurants did this a long time ago. Nothing to do with minimum wage.

It will be New Year soon Wolf,

Don’t let the B*ggers get you down!

All the Best!

FRED Money supply (WM2NS) vs Median House Price (MSPUS):

1980-1990, M2 up 106% Housing up 94%

1990-1995, M2 up 12% Housing up 5%

1995-2000, M2 up 34% Housing up 33%

2000-2005, M2 up 36% Housing up 36%

2005-2010, M2 up 32% Housing down 4% (GFC)

2010-2015, M2 up 38% Housing up 30%

2015-2020, M2 up 31% Housing up 14%

2020-2023, M2 up 34% Housing up 31%

If you want to know where asset prices are going, look at how the money supply is growing. On decadal times scales, slow M2 growth = slow house price growth. Fast M2 growth = fast house price growth. There are almost 14 times as many dollars floating around now as there were in 1980. 14 times! This is a no-brainer. With the exception of the GFC years, house prices generally follow the money supply. There’s no splendid housing bubble. Prices have increased because the value of the dollar has splendidly decreased, same as it’s always been.

“house prices generally follow the money supply. There’s no splendid housing bubble.”

M2 money supply peaked in July 2022 and since then dropped by nearly $1 trillion.

M1 Money Supply peaked in March 2022 and has since then plunged by $2.5 trillion.

Care to revise your statemen?

“Care to revise your statement?”

Not at all. M2 dropped with QT and then flattened out beginning in May 2023.

M2 was rocketing upward so housing was rocketing upward. M2 then dropped and has flattened out. The charts in this very article have largely dropped a bit and flattened out. The national median house price? Dropped and then flattened out.

I mentioned “decadal timescales,” but it’s actually quite astonishing how quickly asset prices reacted to M2 destuction via QT and then how quickly the house price trendline flattened as M2 has stabilized. Lay FRED’s M2 graph over their median house price graph… Even when zoomed in over the last 5 years, it’s uncanny.

If the Fed acts responsibly, they’ll choke M2 a while longer and let regular folks catch up to a flat housing market at least a little. As we enter the era of the $20/hr fast food job, it’s clear that they’re catching up fast via wage growth. When 2 McDonalds grunts can pull in $83k/yr household gross, there will be no housing crash. Brought to you by an M2 that is still $5t above 2020 M2.

M2 (NOT M1) flattened out a little. M1 didn’t flatten out at all.