Homebuilders and developers have adjusted to new reality of higher rates, growth back on track, for single-family since February, for multifamily since August.

By Wolf Richter for WOLF STREET.

Confronted with mortgage rates that make it tough to sell houses at May-2022 prices, homebuilders have adjusted, and in their quarterly reports, have spelled out how: Building smaller houses, “de-amenitizing” the houses (cheaper appliances, countertops, etc.), buying down mortgage rates, and piling on other incentives. Prices of many construction materials have also dropped. As a result, contract sales prices of new houses have dropped by 18% from a year ago, and sales volume has held up, while sales volume of existing homes have collapsed.

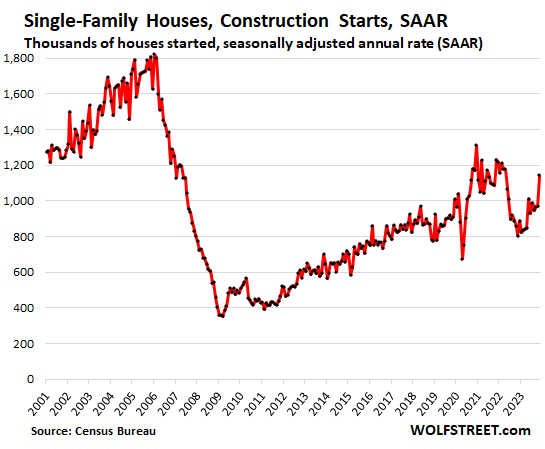

So construction starts of single-family houses in November rose by 6.6% from the prior month, to 86,100 starts not seasonally adjusted, when normally in November, construction starts drop.

This big unusual rise for November shows up in the seasonally adjusted annual rate – which adjusts for the typical drop in November: It jumped by 18% month to month, and by 42% from the collapsed levels last November, to an annual rate of 1.143 million starts, the highest since April 2022, according to data from the Census Bureau today.

Note how construction starts plunged starting in the spring half of 2022 as surging mortgage rates began to bite, unsold inventory began to pile up, and homebuilders were pulling back on new projects; and how construction starts bottomed out early this year and then recovered as homebuilders shifted to smaller houses, fewer amenities, and big mortgage-rate buydowns.

Homebuilders sell houses in various stages of construction, from not-started to completed. By completing a house without having sold it – a “spec house” – a homebuilder “speculates” what buyers might want, down to the finishes. Here we’re talking about construction starts of single-family houses, whether or not they have already been sold.

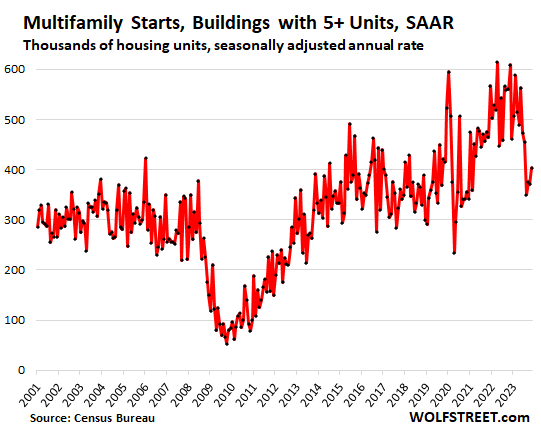

Construction starts of multifamily housing units in buildings with five or more units (such as in condo and apartment buildings) had entered a boom during the pandemic, setting multi-decade highs.

But then the interest-rate shock in late 2022 and in 2023 clobbered Commercial Real Estate – particularly the office and retail sectors which got waylaid by structural shifts, and also the multifamily sector – when soaring mortgage rates could no longer be covered by rents, causing all kinds of fallout, with landlords walking away from properties and lenders – many of them investors, not banks – taking huge losses.

And developers of multifamily properties pulled back, in part due to the difficulty of finding financing for projects whose numbers no longer work out with these higher mortgage rates.

But, but, but… not seasonally adjusted, multifamily construction starts rose to 33,300 housing units (condos and apartments) in November, the highest since July.

Seasonally adjusted, construction starts rose for the third month in a row, after the plunge through August, to an annual rate of 404,000 units, also the highest since July.

Multifamily projects tend to be big with long lead times. High-rise projects where construction started in November were in the planning stages years earlier. So these are long-term trends. But before construction starts, developers can slow down the process, and then they can start construction when they have their ducks all lined up in a row.

In many densely populated urban cores, multifamily is just about the only type of housing that is getting built, and much of it is higher end, because that’s where the money is in expensive cities. Single-family construction takes place further away from urban cores.

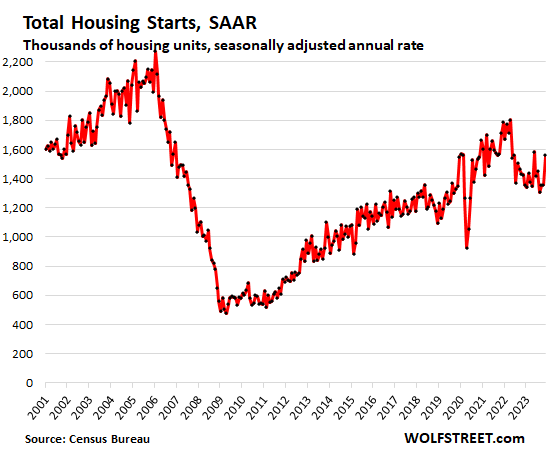

Total housing starts, single family and all multifamily, jumped by 14.8% month-to-month, and by 9.3% year-over-year, to a seasonally adjusted annual rate of 1.56 million, the highest since May:

So there “was” a big slowdown in housing starts, for single-family through last year, and for multifamily through the summer, but since then, homebuilders and developers have started to adjust to the new reality of higher rates, and growth is back on track.

And this is what we have seen in other parts of the economy, where consumers and businesses have adjusted to the higher interest rates. And the economy – despite big issues in certain corners, such as CRE debts and CRE property values – has managed to grow at unexpectedly high growth rates, and the most anticipated recession ever, which was supposed to come in 2023, never came. Instead, the economy grew at a red hot pace in Q3; and in Q4, it appears to be tracking at a solid growth rate that is more typical for the US.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Everyone seems to be adjusting to higher costs. That doesn’t bode well for inflation in ’24.

The overall economy has largely adjusted to higher rates, and that’s not good for bringing inflation down.

But it’s good to see housing construction rise, this is future supply of housing.

A couple of years ago when I was telling you guy “Inflation is transitory”, Here is what I secretly told my private club : “New Inflation target range is 4% to 5%. There will be no regression but I will ensure that the bottom 50% get more miserable than last real recession”.

I did exactly what your article said. As a small builder, I stopped building (in TX) when mortgage rates went from 3% – 7%. The homes I had already built all sold for top dollar and if I had more I could sell them now.

But I’m not going to risk money earned on previous homes in this market and I don’t use debt. The numbers are too skinny. Material and labor costs are still well higher than they were pre-pandemic.

Lot prices are triple what I paid in 2018. I don’t see lower prices coming except through downgrades in size and finish quality.

Here in bullhead city az new construction offers for under 200k 2 bed 1 bath 1,200 square feet, with attached small garage on lots around 4,000 sq ft.

Watching Zillow for a few years these new constructions for these prices don’t jive with older mobiles selling for the same prices IMO.

Lol. The water truck will come by each Friday.

CCCB,

As a small builder, you would also have trouble buying down mortgage rates. It’s easier for the big homebuilders, they have their own mortgage companies.

Are there any numbers oh how new home square footage/design has changed?

Do you know what’s happening in Canada? We seem to have huge immigration numbers (both legal and illegal) and nothing being built. Is that correct?

1. yes, huge immigration numbers. Canada’s population grew by 3.2% year-over-year solely due to immigration. By comparison, the US population grew by 0.5%.

2. things are being built, but not enough. You cannot ramp up housing construction as fast as the government encouraged migration to flood the country over the past two years. It was a huge shock to the housing stock, and will continue to be.

Major freigth forwarder DHL price adjustment for ’24; +8.9%, builders will get similar increases.

Yeah I just sold a kidney to keep up with higher costs of everything. Don’t worry my other one is good. There’s always a way to come up with cash when you need it.

California just passed a law, SB 9, which allows extra housing to be built on existing lots and for splits and so forth by streaming permit process. Hopefully that can help with housing as well. Likely will take time to fruition and in some areas may run into difficulties.

As if everybody wants higher density, and to live like sardines in a can. Landlords, the devil’s gift to humanity, will like it. As for me, no thanks.

TBH, I like living like a sardine in a can. I have everything at my fintips, er, fingertips, plus for free the gorgeous views of miles of the Bay and the City that come with living in a vertical sardine can on a hill. I’d get really tired of looking at my neighbor’s house, a fence, and the street all day. But you and lots of other people like that, which is great. The good thing is that we can all choose where we want to live, and thankfully not everyone likes to live in a sardine can, or else they’d all be full.

What’s the premium on that condo with a view?

DawnsEarlyLight,

The median premium for a view is 1 arm and 1 leg.

Wolf, Just check that rent renewal spike, it will soon be 2 arms and 2 legs.

Probably then you will realize why everyone else isn’t as bullish about the economy as you.

Leo,

In terms of the “economy,” it’s doing just fine. Growth in Q3 was hot, way hot. Q4 growth looks to be in the normal-ish range of 1% to 3%. The average long-term growth of the US economy before the pandemic was 1.9%.

The problem is inflation, which triggered the higher rates, and if it goes away largely, will trigger rate cuts.

A rent “renewal spike” translates into higher services inflation, which translates into higher core inflation, and if that movement is big enough, you can kiss those rate cuts good buy. Here is services inflation, and it has been reheating on a month-to-month basis, in part on continued sharp month-to-month increases of rents.

So I’ll just repost this here:

https://wolfstreet.com/2023/12/12/beneath-the-skin-of-cpi-inflation-november-core-services-inflation-accelerates-as-rent-cpi-glows-in-the-dark-insurance-spikes/

“The acceleration of the three-month moving average in September, October, and November is very disconcerting”:

You mean the traditional building pattern, the world over, until the US got addicted to the automobile? Where resourceful humans economize the use of materials to live in people-scaled places. How horrible. And then to denigrate it as if this is bad? If you don’t like it, move on.

But unlike the rest of the world, the USA has densely populated cities separated by huge swaths of absolutely nothing. Its a huge amount of land.

That’s why trains make sense in Europe but not here.

The US transportation system was based on various kinds of trains before the pivot to car dependent design after WW2. Just because you have a lot of land doesn’t mean you have to sprawl. If anything you’re destroying a lot of potential wealth by doing so – by forgoing leaving it as wilderness or farmland, by assuming all of the new, objective net loss in taxable value when building suburb vs city there, and in a variety of other negative externalities associated with the world’s least productive and sustainable land use.

Don’t get me wrong, I wish travel by train was more abundant and practical in this country. I try to ride Amtrak at least a couple times per year.

But the reality is, most passenger RRs could not exist without subsidization. Also telling that almost all ROWs are owned by freight RRs, because moving freight by rail is profitable.

@William Leake I’ll agree that some landlords are evil, but just like Wolf likes living in a “sardine can” lots of people are happy that there are good Landlords who work hard and deal with everything related to owning real estate so they have a place to live for a few months or a few years without having to think about maintenance, repairs, insurance or property taxes. Not many 18 year old kids that get accepted to a college out of state want to deal with owning a home or condo as a college freshman (and if they go to grad school in another state for one to three years it foolish for most people to spend the time and money to buy a home or condo that you know you will soon have to sell.

I liked the landlord of the last duplex I lived in. Really nice guy who genuinely cared about his tennants and keeping up the place. He also told me horror stories of nutjob tennants he had, like one that set his bushes in the back yard on fire.

He also worked as a contractor and always seemed busy. I tried to help out with little things around the place.

“Landlords, the devil’s gift to humanity, will like it.”

Really, us mean landlords who provide a needed service.

Before you start trashing people you should try working in the business. There are plenty of lousy tenants that make it a tough business.

Not mean — just avaricious work-shy parasites capitalizing on a broken system which tilts the table in favor of avaricious work-shy parasites. But no, commodifying a fundamental necessity for survival is not mean, as I see it.

@Bullfinch,

Dig deeper, shallow hate is shallow reasoning. What do you propose would solve the avaricious work-shy parasite problem?

Who will purchase and repair the next property and offer it without being paid for his time or materials? Do we have enough golden souls to work for free to house everyone else?

Are you a golden soul?

You can take the metrosexual out of the sardine can, but you’ll never take the sardine can out of the metrosexual.

I tried living in one once. I kept getting the urge to leap over the balcony. The trash chutes terrified me. Plumbing issues in one unit affected multiple other units. Someone is always trying to deep fat fry a turkey at 4 am setting off the fire alarms. Driving round and round and round up the garage levels with speed bumps every 25 feet. Multiple car break ins. Someone leaving a pontoon raft in my parking spot. And H.W, the purple finch that liked to hang out on my Directv dish every early dawn to chirp his heart out and make sure I was awake to hear him. We had no bay, but we had a nice freeway to look out over.

I had that experience. I’m ok with it being a part of my past. I’m also ok with it staying there.

Maybe you should have tried a different neighborhood? I have a lovely view from my apartment in sf

Investors are trying to build a new city in California, approximately around the Travis AFB.

Right under the flightpath of military aircraft? Those people are really smart, aren’t they?

I live in Tucson, right below the final approach to Davis Monthan AFB.

…suggest a review of Miramar NAB in San Diego County. Though having left the area by ’77, I understand that noise complaints from the Mira Mesa development, built adjacent, with full view of the fighter base which had long preceded it, prompted, in part the Navy’s ceasing of aviation operations there (to be replaced by Marine Corps rotary-wing operations (from their former El Toro facility), which friends in the area tell me are noisier than the prior jet aircraft activity…). Never underestimate the power of the willfully-ignorant NIMBY (…or the impact of unintended consequences…).

may we all find a better day.

Hmm, I got a lot of responses from my short quip.

Okay, I imagine some landlords are fine, I have just never met any. As for apartment living, it obviously depends on what kind of apartment it is and who the tenants are. Views don’t interest me, they are always the same view. How many times do you have to look at the same view. Sunsets, however, are usually different enough, so that would be a plus.

I would also not much like living in these new subdivisions where you can spit from your open bedroom window onto your neighbor’s bedroom window (if you are lucky their window will be open). They are one story condos with lawns.

I would like a couple of acres with good neighbors all around. But all you need is a neighbor’s constantly barking dog to wreck ones life. If you find a place you like, stay there, even if you are a sardine. People are different and thank goodness for that.

BIG TRAP–LOWER RATES WILL STIMULATE GROWTH AND SPECULATION

WHICH WILL BRING BACK INFLATION WHICH WILL PRICK THE BUBBLE

@tom havens: Exactly. Services inflation is still there. And there is considerable QE and deficit spending in the system already. The folks who wade in too early are going to be in for a big surprise!

Unfortunately, the Fed has to be slapped around by inflation because they are too busy right now kowtowing to the banksters and politicians.

Issue is not housing supply.

More construction will eventually end up in housing glut.

The population hasn’t doubled in the past 5 years yet house prices have. Why?

It’s the deranged policies of the Fed tinkering with the value of money that have pushed everyone into housing as an inflation hedge.

I see lots of houses sitting empty everywhere. Investment properties.

Imagine buying gas and the volume of the gallon keep changing, it’s impossible to predict how people will react but eventually they will stop playing.

The Federal Reserve has nothing whatsoever to do with prices of housing anywhere in the US. The very same US Dollars are used for oil and the price of oil and petroleum products have plunged dramatically.

Yes, but most people don’t take out a 30 year collateralized loan to purchase oil.

Mortgage rates in the US are based on yields on 10-Year US Treasuries plus around 3% as 10 years is the average duration life for a typical 30 year mortgage.

That’s right, the Federal Reserve buying mortgage bonds definitely had zero effect on buying housing. Also, it’s proven statistically there is zero correlation between the federal funds rate and prevailing mortgage rates. And the wealth effect the Fed people always talks about applies to all assets EXCEPT housing, everyone knows that!

Are you saying that if the fed had not bought up all those mbs back in the day, that housing prices could have corrected, may have become most affordable so that most anyone could have purchased one?

Then why did they do such a horrible thing?

“The Federal Reserve has nothing whatsoever to do with prices of housing anywhere in the US.”

This is the dumbest comment on the internet.

SOL,

You are correct. What the Fed did for a decade and a half was keep interest rates artificially low. This kept mortgage rates low. So, what happens when mortgage rates are low?

The monthly “nut” buyers can spend, which is related to wages and income gets tilted to higher priced houses at the 3%, or lower, 30-year fixed mortgage. Low mortgage rates, set by the Fed policy, create more demand for housing. Prices then go up. Supply & Demand.

“What we are dealing with here, of course, are the purportedly “unintended” but predictable effects of the Fed’s heavy-handed attempts to set interest rates rates below–and usually deeply below–market based levels. That is to say, the Eccles Building may not have intended to cause soaring home prices or now to cause owners to keep properties off the market in order to preserve low long-term mortgage rate, but that’s exactly what their foolish interest rate pegging policies have caused to happen.”

-Published today, and written by David Stockman.

SoCalBeachDude,

I encourage you to read the entire essay, “How The Fed Wrecked The Dream Of Homeownership” by Mr. Stockman.

LoL. SOL, thank you for clearing this up. What else can be said really.

Yes, someone with literally no understanding of finance.

We need to remember though and inform others that the Fed governors are nominated by the President and confirmed by the Senate so together we can stop the devaluation of the dollar and suppression of rates fueling this housing and inflation mess by demanding accountability of our representatives at the ballot box. Vote out the Senators, Presidents, and whatever other officials are putting these Fed governors in place. I think this can get lost in all the focus on the Fed. They have shown that they can’t be trusted to do what’s right so we need to take charge and put in people who will.

The Chinese leverage everything to the absolute hilt. Lower rates means lower mortgages for them and hundreds or thousands of extra properties. This is what drives up prices. This is how things work up in Canada but the same Chinese might be working their magic in America as well.

I totally agree.

FED has had no impact on whatever kind of inflation we are seeing in general and in housing to be specific.

FED is a benign institution which has been power to print trillions at their whim. But these printing have no impact on anything.

/sarc

Also remember, FED would move mountains to keep asset prices at permanently high plateau.

Blahahaha. Say what?

“Fed has nothing to do with housing prices?”

Fed printing money & buying Trillions in mortgages back securities while buying bonds & lowering rates to 0% during the pandemic had more than a little to do with housing prices.

Asset price inflation = wealth effect= stimulus

-Ben Bernanke.

No, the issue is certainly driven by supply. Even looking back to 2012-2019, prices had been rising nationally significantly faster than general inflation. 20 years ago, the average household spent about 23% of its income on rent. A decade ago it was 26%. And at the end of last year is when that average hit 30%. Meanwhile average age of first time home buyers marched upwards. Theres a backlog of people who want to own homes who cannot. If theres a proper level of housing simply misallocated due to investors, we must over build to destroy those investments. They will obviously not allow things to normalize on their own.

The population has not doubled partly because the largest generation that would have led us to substantial, non-immigration, population increases did not have the income to purchase enough residential space they felt necessary to start popping out kids. Millennials now make more money and not uncommonly dual income no kids (but with some type of furry pet). At the end of the day we need additional supply so that even those with an existing home can shuffle around. Someone who is looking for a different home to buy and must or willingly sell to buy a different home does not increase supply. Having additional supply helps facilitate the shuffling of homes as well as supports a growing population. We need supply.

Seems to me. Demand requires a ready, willing & able buyer. We’re missing the “able” part.

@Gomp,

Without a willing and able buyer, the price is just an ask. There must be plenty of able buyers to support the current price of homes.

Eastern Bunny,

>Imagine buying gas and the volume of the gallon keep changing, it’s impossible to predict how people will react but eventually they will stop playing.

Actually, you can play this. Gasoline gets more dense (contracts) as it gets cold, so for every 15 degree (F) drop in temp, you’re getting ~1% more gasoline in your nice fixed gallon. :-)

Ok, back to arguing about housing.

There is correction for temperature in the gas pump.

Could this be the beginning of the hypersupply phase?

lol no

For this, you need to wait for dep recession which may never come as FED would bring on their money printing bazooka.

The Federal Reserve is withdrawing money from circulation and will continue to do that well into 2025.

Home Prices Drop In SoCal, And Experts Predict It To Continue In 2024

Home prices are expected to keep dropping for much of Southern California over the coming year, the Los Angeles Times reported….

2024 is going to turn into a buyer’s market in most places.

Not unless the inventory of existing homes goes WAY up to compete with new homes.

Not unless interest rates go back up, because if they go lower, as the fed signaled they could, a lot of buyers will be coming out of the woodwork.

If we have the long awaited recession, maybe they’ll drop, but remember, this isn’t a housing induced recession like 2008, so don’t expect a price collapse.

The Federal Reserve Federal Funds Rate and other interest rates they set has nothing whatsoever to do with mortgage rates which are based on 10 year US Treasuries plus about 3%.

CCCB,

I didn’t say there was going to be a total price collapse. But inventory is building.

People already aren’t rushing to buy at builder incentives of a fixed 5.5% rate for 30 years, so what makes you think everyone is going to rush back into the market if rates go down? Inventory will continue to build. A buyer’s market is coming.

Exactly! Unlike 2008, everyone is waiting to buy the dip in housing, stocks, or whatever their fancy is, and they are flush with cash this time. Which means there will not be one.

The price to income ratio for buying a home is way out of whack, worse than it’s ever been. Yet you think everyone is flush with cash and waiting to buy. Lol!

I sort of agree. Used homes likely are not going to come on the market unless there are lots of jobless people. They probably refinanced during ZIRP and are not willing to move to a more desirable home or location just to go back to a higher % of take home income gone for a roof. They shall begrudgingly stay put, so it is up to new builds and commercial/office conversions to increase supply relative to this demand where current home owners are out of the selling and buying picture.

Houses come onto the market all the time when folks die, get jobs elsewhere, or seek to upsize or downsize.

Unless we have no recession ever, I don’t think price would drop.

It is possible, FED would rather inflate away the issues than face the issue.

That’s what the LA Times is predicting for 2024 here in SoCal.

It depends on the market… and the type of home. In a macro sense, the population in the US is barely growing, and is averaging about 0.1% growth per year. When you look at Wolf’s numbers and see that new housing starts are enough to house 1% of the population of the US, per year, it is apparent that supply should be rapidly outpacing demand – even in a down market. However builders are very savvy and are only building in booming markets where the demand is outpacing supply. The only possible answer is that some markets are seeing an increase in housing vacancies (in the traditional sense). If you dive into housing vacancies, there are many different causes/types. People who own more than one home, people who buy properties for short-term rentals, people who hold vacant properties by choice, and others. Additionally, there is a big difference between cash buyers (who represent about 1/3 of existing home buyers) and those who depend on financing. New housing and housing for first-time home buyers will probably continue to see tight market conditions in 2024. Existing homes will probably continue to be all about location, location, location. The hottest markets will continue to be hot, while cold markets will get even colder.

In my 1/2 built neighborhood ~50 miles north of downtown Houston, TX, five new foundations were poured within the last three weeks. There is no trouble selling homes here (starter homes – 1,200 – 2,600 sq. ft. in size) and the builder is buying down the mortgage rate to 5.99%.

The homes are selling for about $175/sq. ft.

@Anthony A. Do you know the lot size of those $175/sf homes near you? I read something a few months ago that the CA Median Home price is still over $400/sf with a median lot size of ~8,000sf, but I have been seeing new single family home developments in CA in recent years on lots as small as 3,000sf. (P.S. For those of you in other states who think your your housing is expensive I just looked at Redfin that says the median price per sf in Palo Alto, CA is $1,780/sf – a little more than ten new homes north of Houston)

Palo Alto is a bit of an exception. Average in CA is about $425 sqft. My house is worth about $250 sqft but I got for around $180 in 2016.

Actually it’s worth nothing until you sign on the dotted line to sell it.

Please disregard my comments. Thanks

My lot is 4,600 sq. ft. in size (40′ x 115′). This is pretty typical for this area and these new homes. Some lots in the neighborhood are bigger and some smaller, but not by a lot.

Several builders are “covering the landscape” with these new homes around here (Conroe, Texas). Much of this area was sparsely developed many years ago with small farms.

This is not the same type of living I had in Connecticut where I had a 3,000 sq. ft. Colonial house on 3 acres. But this is plenty big for this old widowed retiree and a small dog.

FWIW an “average” lot size in the heart of downtown Chicago is 3000 square feet. This is for a row houses/townhouses.

It just seems that nationwide residential asset prices are going to float +- a few precents for a long time while inflation persists. Some markets are going to be worse off which seems mostly West of the Mississippi and plenty of markets seem poised to keep steady.

2024 is going to be quite interesting. Americans that were able to refinance during ZIRP have plenty of discretionary income to spend and they are getting good nigh risk free returns with CDs or treasuries. I know Boomers who have delayed retirement partially because of higher prices, but also because of continued pay raises which both are due to monetary inflation. They have a home almost or fully paid off and getting returns on their savings while making nominally more money. All of this may help keep near the Federal Reserve’s 2% inflation goal. Which begs the question why would they lower rates?

As long as people who own assets believe that the Fed has their back, they’ll never sell. At the most extreme point, there will be 0 sellers, as everyone will be convinced that it’s better to hold than to sell. That’s what the Fed would have to avoid if it was sincere in trying to protect the dollar.

Come on Einhal. You’re smarter than that. You know who the fed works for and what their “mandate” is. The dollar is not a part of it.

Nor are home prices. The fed got WAY out of their mandate, balywick, whatever you want to call it, when they decided that housing prices were too high and they needed to bring them back into line.

That’s what this whole shitshow is about. Now they’re trying to get back to reducing inflation (price stability) and full employment after getting their asses handed to them for unsuccessfully trying to control housing costs.

Maybe it’s why they have a specific mandate.

Actually, the dollar is part of their mandate. That’s what “stable prices” is about.

They didn’t decide housing prices were too high. They decided assets were too low, which is why they embarked on rampage of printing.

I wouldn’t be so quick to dismiss the idea of the Fed defending the dollar. I’d argue its part & parcel of their inflation fight.

Consider that the Fed is trying to ‘out-hawk’ other CBs by having the highest rates, which benefits the exchange rate.

Additionally, tools like the FIMA repo facility are designed to make holding treasuries more appealing to other countries, thus keeping them from straying to other currencies.

The Fed doesn’t exist in a vacuum – they see what’s going on in the rest of the world.

Its not quite that simple. Houses have carrying costs. It doesn’t make sense for a property to it empty, costing money in taxes & upkeep, based on a theoretical, unrealized future gain.

On the other hand, someone who bought their house to live in migt choose to never sell because, well, they’re living in it.

Agreed. But if they think the price will appreciate more each month than the carrying costs, they will hold.

Actually I think you’ve got it backwards:

If the Fed “pivots” (man I hate that word now) to QE and lower rates, that would be letting the dollar tank. By keeping rate high they’re defending the dollar.

If the housing market has to be frozen for a bit to bring home prices back down to earth, so be it.