From 2022 peaks: San Francisco -11%, Seattle -10%, Las Vegas -6%, Phoenix -6%, Portland -5%, then Denver, Dallas, San Diego, Los Angeles, Tampa.

By Wolf Richter for WOLF STREET.

We like the S&P CoreLogic Case-Shiller Home Price Index because it’s based on the “sales-pairs method” comparing the sales price of the same house over time, thereby eliminating the issues associated with median price indices (see “Methodology” toward the end of the article). And we like it because it shows the 20 metros it covers in all their individual glory. But we grumble because it lags months behind: Today’s index for “August” is a three-month moving average of home prices whose sales were entered into public records in June, July, and August. That’s the time frame we’re looking at here today.

By contrast, the National Association of Realtors already released its national median-price index for deals that closed in September – an actual national metric, and not just covering 20 cities: It fell for the third month in a row and is down 4.7% from its peak last year (June 2022), making 2023 the first year since the Housing Bust that the seasonal peak in June was below the peak in the prior year.

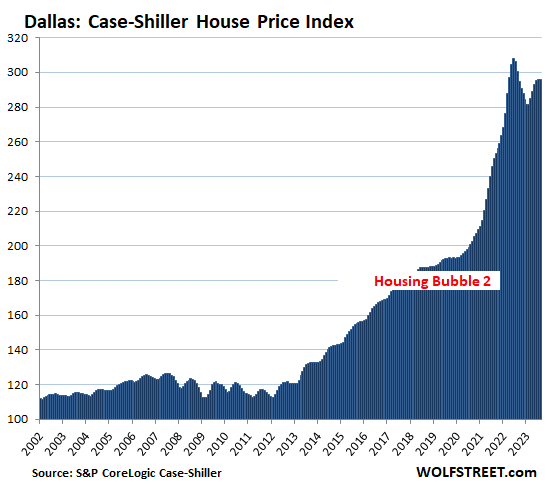

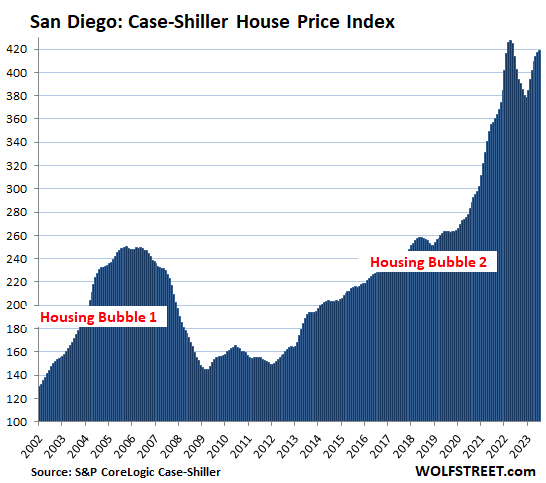

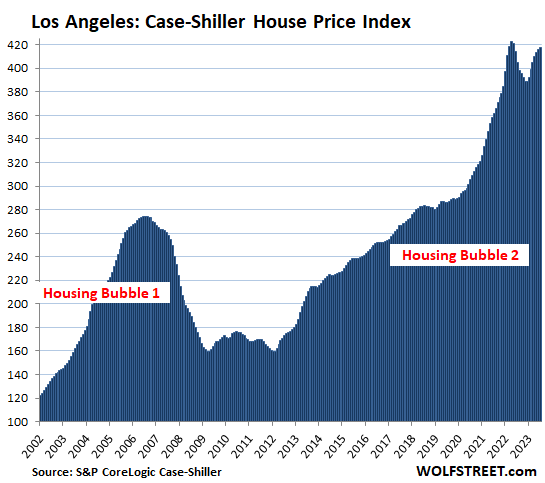

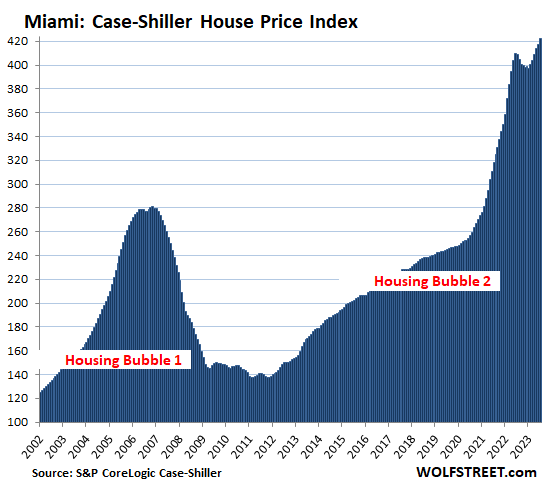

It’s Home-Price Inflation. By measuring how many dollars it takes to buy the same home over time, the Case-Shiller index is a measure of home price inflation. The indices were set at 100 for the year 2000. So today’s index values of 422 for Miami, 419 for San Diego, and 417 for Los Angeles are up respectively by 322%, 319%, and 317% since 2000. Miami is thereby the #1 Most Splendid Housing Bubble in terms of home price inflation since 2000, followed by San Diego and Los Angeles. To be included in this list of the Most Splendid Housing Bubbles, the metro must have experienced a home price inflation since 2000 of at least 180%. Dallas made the cutoff with 195%.

By comparison, Consumer-Price Inflation, which tracks price changes of goods and services that are consumed by, uh, consumers, was 82% over the same period since January 2000, according to the Consumer Price index (my discussion of CPI is here).

So here we go with the numbers from the S&P CoreLogic Case-Shiller Home Price Index…

Prices are below their 2022 peaks in 10 of the 20 metros in the index (% from peak):

- San Francisco Bay Area: -11.2%

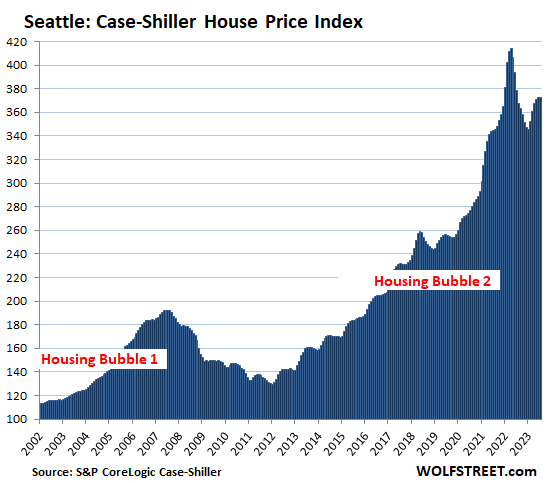

- Seattle: -9.9%

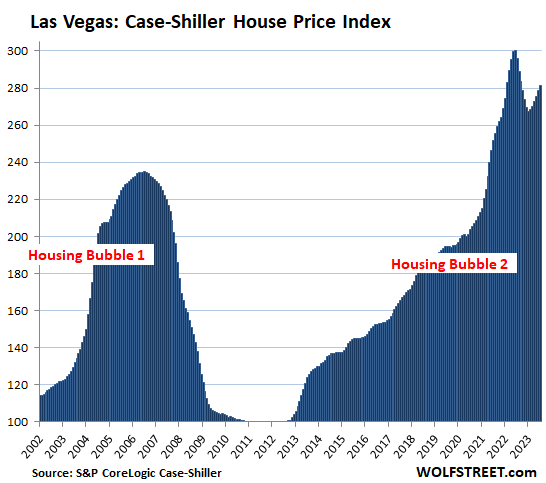

- Las Vegas: -6.2%

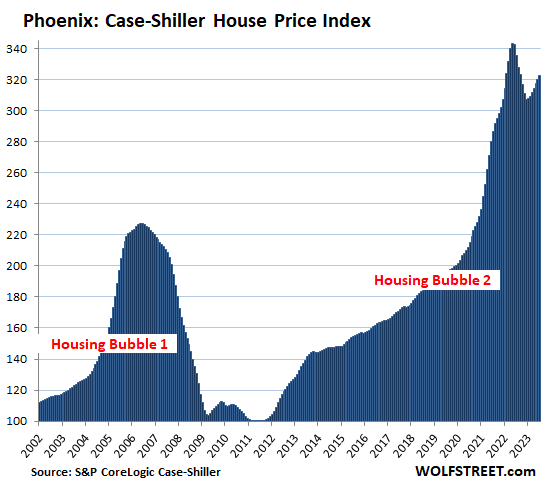

- Phoenix: -6.1%

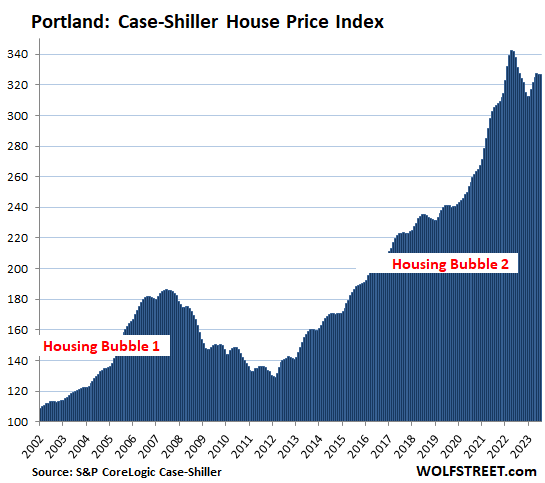

- Portland: -4.6%

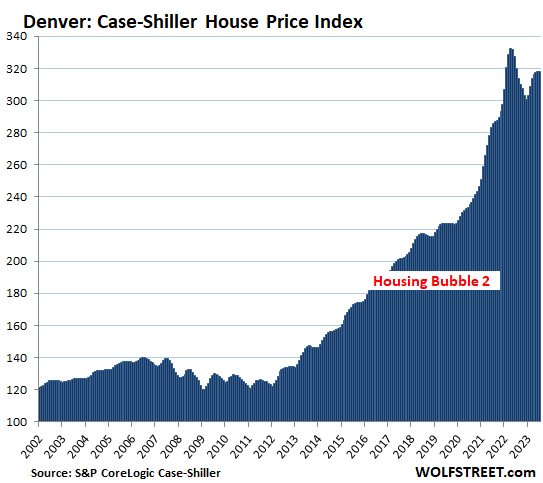

- Denver: -4.3%

- Dallas: -4.0%

- San Diego: -2.0%

- Los Angeles: -1.3%

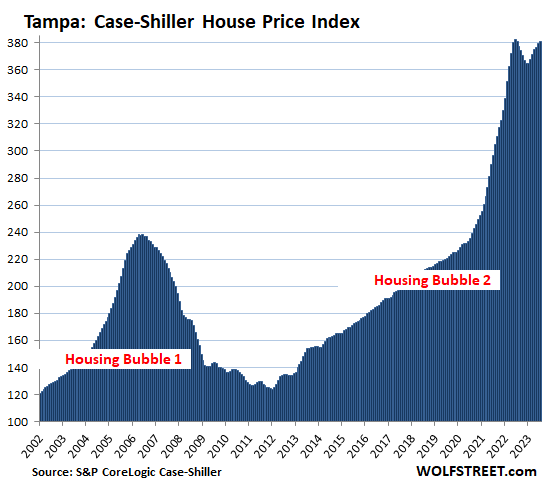

- Tampa: -0.4%

Prices set new highs in 6 of the 20 metros in the index (% year-over-year):

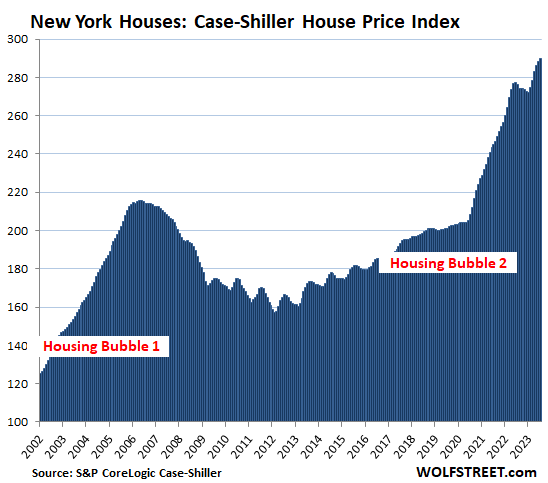

- New York: +5.0%

- Detroit: +4.8%

- Atlanta: +3.4%

- Miami: +3.3%

- Charlotte: +3.0%

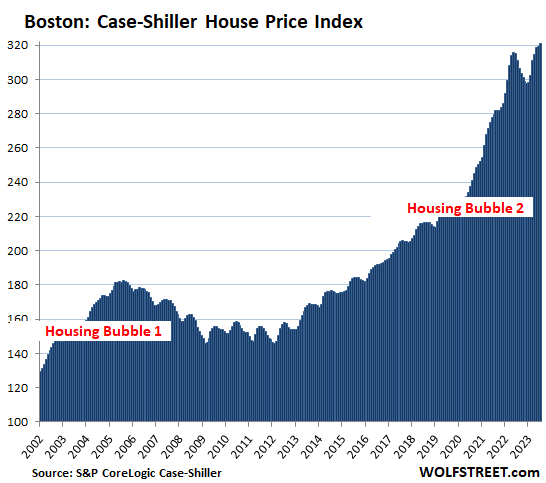

- Boston: +3.1%

The most splendid housing bubbles by metro.

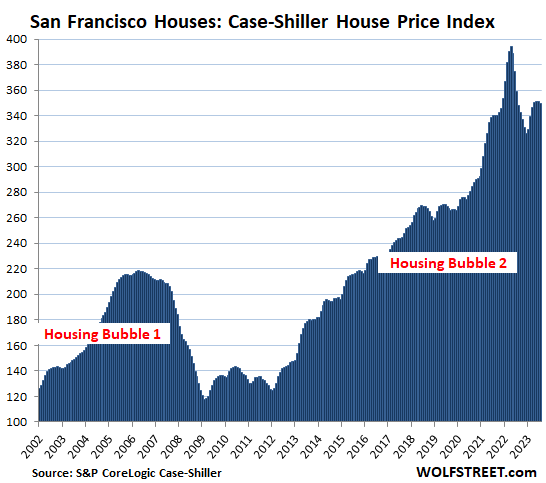

San Francisco Bay Area:

- Month to month: -0.5%

- Year over year: -2.5%, the 10th month of year-over-year declines

- From the peak in May 2022: -11.2%.

Seattle metro:

- Month to month: +0.2%.

- Year over year: -1.5%.

- From the peak in May 2022: -9.9%.

Las Vegas metro:

- Month to month: +1.1%.

- Year over year: -4.9%.

- From the peak in July 2022: -6.2%.

Phoenix metro:

- Month to month: +0.7%.

- Year over year: -3.9%.

- From the peak in June 2022: -6.1%.

Denver metro:

- Month to month: -0.1%.

- Year over year: -0.6%.

- From the peak in May 2022: -4.3%.

Portland metro:

- Month to month: -0.1%.

- Year over year: -1.5%.

- From the peak in May 2022: -4.6%.

Dallas metro:

- Month to month: -0.2%.

- Year over year: -1.7%.

- From the peak in June 2022: -4.0%.

San Diego metro:

- Month to month: +0.6%.

- Year over year: +4.1%.

- From the peak in May 2022: -2.0%.

Los Angeles metro:

- Month to month: +0.5%.

- Year over year: +3.2%.

- From the peak in May 2022: -1.3%.

Tampa metro:

- Month to month: +0.4%.

- Year over year: no change.

- From peak in July 2022: -0.4%

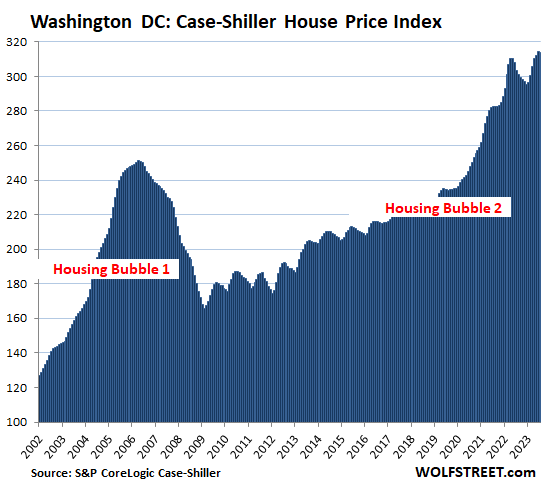

Washington D.C. metro:

- Month to month: -0.1%.

- Year over year: +3.4%.

- From high in July 2023: -0.1%

Boston metro:

- Month to month: +0.6%.

- Year over year: +3.1%.

- Set new high.

Miami metro:

- Month to month: +1.2%

- Year over year: +3.3%.

- Set new high.

New York metro:

- Month to month: +0.5%.

- Year over year: +5.0%.

- Set new high.

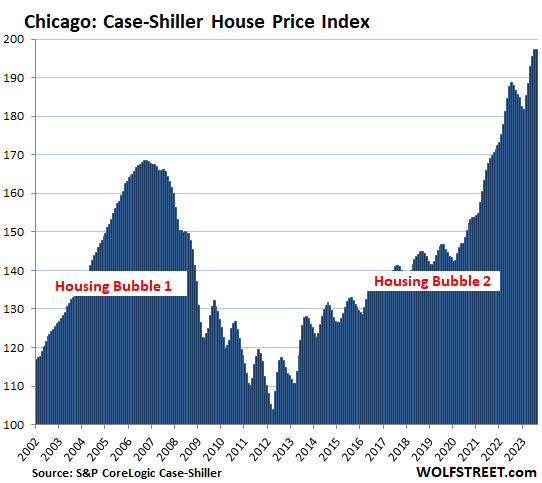

The remaining 6 of the 20 markets in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had far less house price inflation since 2000, and don’t qualify for this list of the Most Splendid Housing Bubbles. But in 2022 and 2023, these metros were the ones with the biggest home price increases in percentage terms even as prices have fallen or flattened out in the expensive markets.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices, but it lags months behind (37-page methodology).

The Chicago metro doesn’t qualify for this list, with an index value of 197, which is up by “only” 97% from 2000, and 93 points below the lowest-ranked metro of the Most Splendid Housing Bubbles, New York (index value = 290). But here it is anyway:

- Month to month: unchanged at high set in prior month

- Year over year: +5.0%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Be interested how long it can remain this way with many realtors seeing incomes decline. Anecdotally I get 3 to 5 calls a week asking if I want to sell my house. I vary my response but lately it has been “3 million in unmarked bills.”. Hopefully they have solid reserves from the massive commissions during the asset bubble rise.

3 million dollars…

one would think you were talking about a castle in Europe and not an old termite-eaten house in the USA

Good Realtors don’t care much about prices. They want a house they can sell, and they want a buyer they can sell it to, at whatever price, and they get their commission. No house, no buyer, no commission.

Any data on the way overprice Washington DC metro area ?

RTGDFA 😍

Looks like a nasty verdict came in this afternoon against the realtors on the national anti competition lawsuit.

Too bad realtors, you might need to look for a second job and maybe home sellers and buyers can have a much fairer experience

rodolfo,

When it comes to court cases, we don’t count our chickens until they’re hatched. This still requires the judge to determine what’s going to happen, and then it will be appealed endlessly. This will take years.

I just looked at Zillow for Burlingame (~10 miles South of SF) and saw a $100K “Price Cut” where the list price for a 1,550sf 2 bedroom 1 bath home (on a 4,860sf lot) is now (after the “Price Cut”) $3,100,000. I’m guessing it will sell for well under $3mm (My parents paid $27K for a bigger Burlingame home on a bigger lot up the hill in 1967).

Once the bubble starts deflating the realtors will make money all the way down, they just need something to get it moving.

It’s already deflating. Here is the National Association of Realtors’ take on it, as of September, so not as far behind as the Case-Shiller. Looking for lower highs and lower lows:

https://wolfstreet.com/2023/10/19/median-price-of-existing-homes-falls-further-peak-was-june-2022-demand-crashes-price-cuts-jump-supply-days-on-market-rise/

I was thinking the same way, anticipating the summer season. But what about year-over-year in Los Angeles, solid +3% ?

In between, I also stay on the side , waiting the wait game for the price adjustment, LOL

“It’s already deflating” one can only wish. What if this happens: technical recession early next year> lower bond rates>lower mortgage rates=more demand due to higher affordability?

There is this notion that a recession means higher unemployment and lower demand for housing but doesn’t it usually impact the little guy who cannot afford to buy in any scenario anyways?

Patrick B,

You’re forecasting, based on your vision, and that’s fine, and it may be colored by wishful thinking.

I’m not forecasting, I told you what is already happening and is already showing up in the data, which is a different thing than forecasting.

Wolf,

I appreciate the difficulty in getting metro level sales *volume* data (but Case-Shiller must have a proxy somewhere) but without volume data, we lack a metric for your favorite anti-inflation measure “The Power of No” (as in “No Deal at That Price”).

Prices can remain elevated for a long time (The Rich Will Always Be With Us) even as transactional volumes evaporate, quickly eroding the demand foundation for said high prices.

CS gas sales pairs count. Go look them up.

If this is like the eighties crash, a third will exit the biz.

I once offered a small farm for sale in discussion with the original owner. He offered to return the amount he had sold it for. I thought about taking him up provided he gave me the total in silver coin. Did not say this as he was a very respected banker friend!

NAR just was sued for 5 Billion $

Looks like no more buyer fees.

Cha Ching! $$

:)

*buyer’s agent fees

No more.

Slip them a 20 for gas

sufferinsucatash,

When it comes to court cases, we don’t count our chickens until they’re hatched. This still requires the judge to determine what’s going to happen, and then it will be appealed endlessly. This will take years.

The NAR was rated the top political conressional lobbyist in 2022.

https://www.opensecrets.org/orgs/national-assn-of-realtors/summary?id=D000000062

housing demand comes from the government addiction to printing money, everyone is ditching their dollars to any form of assets, and housing comes first. I don’t believe we have housing shortages, we have money printing addiction problem. Look at how many empty properties we have then you know

Chicago is attempting to pass a sales transfer tax that is 2-4 times higher, tiered on house sales above $1M, to pay for homeless. Some other cities have already passed the “Mansion Tax”, and others are looking to pass soon. This could play a role in the next few years on city housing prices as a 10% tax could hit those between $1-$2M, which is the average in many high cost sites for the working class citizens, not the top 0.1% who could afford it easily.

Plus some states have sued and won billions against the realtor commission collusion cases addressing the 5-6% fees. If the Fed govt gets involved, which looks likely if housing folds and we enter recession, it could be very bad for the entire industry…TBD

Point being, the entire shelter complex, including both retail and commercial, has a lot of very volatile variables that are going to be difficult to predict how they all play out in the next few years. The “shelter economy” could be a mess for many years, and looking back it will be obvious that the Fed, govt, and banking cartel should have not monkeyed with the housing markets for financial and political gains over the last few decades.

Any clue to why there is an east/west split in housing price changes?

Tampa is going down, Miami is not. East-West split?

I think Monkey Paws is refering to the fact that its mostly east coast metros making new highs, and mostly west coast metros still off their 2022 peaks. I noted this as well.

I was just being facetious. I understood.

What is really happening is that the lower-priced metros saw the biggest price increases in recent months: Detroit, Atlanta, Charlotte, Cleveland, Minneapolis, Chicago… they all saw month-to-month increases in the 0.8% to 2.7% range over the past five months. Annualized these are double-digit increases. That’s where it was happening. But in Chicago that spurt ended. In Minneapolis and Cleveland, prices fell this month, and you can see the rounding off top. So even in those lower-priced cities, the steam is starting to come off. But that’s really where the biggest divisions were: between very expensive metros and much less expensive metros.

Wolf, is this a measure of buy-to-occupy homes? In Suburban NYC we have a ton of ‘luxury’ housing with many units unoccupied. Huge complaint of the locals in areas like Poughkeepsie, White Plains, etc. who are getting priced out while half of ‘The Lofts on the Hudson’ or whatever sit dark at night.

There have always been and always will be super wealthy folks around here eith their RE investments, but the past 10 years its been absolutely nuts with luxury developments of condos, townhomes and SFHs that seem to keep empty.

Wolf, is there any way for us to check trends in specific locations? What would you recommend as the best way to check?

On FRED you can find house price data for specific states and specific counties. The county data is only updated once a year.

I’m not aware of any way to get “real-time” housing data except for the specific blessed Case-Shiller metros.

Note that the FRED data is actually FHA data which is from government-backed mortgages. So that data is skewed because it systematically excludes all cash sales and all sales funded with mortgages that have not been backed by the government.

West coast FLA has Red Tide.

I recently spoke with a realtor from Huntsville. He said investors are still grabbing every property they can, renting them for market rates and pocketing a good return t BP each month. They will hold those properties as they appreciate in a 5-10 year time horizon. No wonder sales are down and the 30 something’s can’t afford a house.

Can’t catch a falling knife if the knife isn’t falling. :(

Maybe in Huntsville miracleville. But for the US market overall, this is unadulterated BS. Investors have massively left the market.

Huntsville is still on the boil. Lots of federal

dollars make their way through Huntsville.

Huntsville is the fastest growing area Alabama.

As far as the second fastest growing area in Alabama goes, it is slowing and houses are sitting .

Agreed. A big part of that too is how Federal salaries are rated. A good paying, secure, job in AL is a big deal. And with all the drone/missile/rocket requirements the current wars are generating Huntsville is not going to slow down.

A city with way more people moving in than out will still see its real estate rise, QT or not. But that can’t be the situation for all cities at the same time, and it very much is not the situation for some bigger cities where people are nevertheless saying “OMG housing shortage, the new normal, homes only go up forever, etc.”

Hmm, in my hood, you can’t buy a house and rent and be cash positive as the yield on treasury bills/bonds have increased a lot.

It makes sense to buy bills/bonds, earn interest risk free and sleep peacefully. You’d still come ahead with this risk and effort free than being a land lord.

But thanks to these people for keeping the transactions going, we need knife catchers for price discovery.

It is vey very slow but indeed going down in price.

We need much higher for longer. 8% mortgage rate is not cutting it really .

I’m calling b/s on this.

The typical decent SFH in Huntsville is being listed at a price that, with a 20% down payment, would result in a monthly payment of $2500-3500.

Other SFHs of similar quality appear to be renting for just $2000-$2500 per month. So if investors are borrowing to get into homes, they’re buying the right to break even, if they’re lucky. And more likely lose a few hundred per month.

If you’re suggesting they’re doing all-cash deals, then after expenses, taxes, insurance, they’re probably looking at $1500 profit per month, or $18,000 per year. On a 425k house, that’s a return of 4.2%. No one with any sense is making that deal. Not with the risk of loss of principle and the risk of damage to the property or unexpected large repairs. There are hundreds of ways to invest 425k with less effort, lower risk, and higher rate of return.

I agree but you always have knife catchers or people who think real estate can only go up. They are not sophisticated investors.

My friend sold a condo/townhome in San Diego for 850K to a buyer who bough it cash and then rented it out for $4K/month.

The Tax + special assessment + HoA + INsurance alone was ~$1500/month.

That was actually a really “good” trade in SD terms. There are plenty of $4+ mil homes renting for $10k.

If someone already has a couple rental homes it is easy to add a couple more (and it won’t cost $1K a month in expenses unless you are in a high property tax-no income tax state). Homes have gone up ~4% on average nationwide over the past couple decades so that puts you at ~8% pre tax and a lot higher after tax if you have other passive income to offset the depreciation (if I found a $425K house anywhere in Northern CA that I could rent for $2,500/month I would buy it tomorrow).

Wolf, what do you say about this kind of thinking? Or more to the point– for those of us who have owned rental properties for 10+ years, do you think ongoing appreciation + rents (long-term rentals) – holding costs still means holding them makes sense? I guess the question do you feel confident that there will be a crash and then no recovery for a long time? I’m other words, any existing landlords should sell?

If your business, or part of your business, is being a landlord, and it’s working for you, and you like doing it, then why would you end your business?

Sure, you could sell your properties and maybe walk away with lots of cash, and then what? If you’ve got your units financed long-term fixed rate, then you really don’t care about what prices and interest rates do. All you care about is your tenants and your properties. So if you have to lower rents to keep and attract good tenants, well, so what? And you get tons of tax benefits. So maybe it’s no longer money just growing on trees, but that’s all right.

Apartmentinvestor

“ if I found a $425K house anywhere in Northern CA that I could rent for $2,500/month I would buy it tomorrow”

You can find that in Phoenix, right? And hoa’s will be much lower in AZ compared to CA. Phoenix won’t appreciate a lot over the next years I assume. But 30 years from now, due to inflation, you should be fine?!

I have a new construction with no CDD no HOA in the Tampa area that you could leased for $2500 and the asking price is $384,500 if you’re interested!!

A couple in their 30’s is using “Brooklyn Money” to buy a place in Jersey.

According to NYT

apparently Brooklyn money is 900k

They are data analysts

He bikes she bakes.

/s

Realtors are often full of crap. Here in South Florida, I’m seeing units that sold for way too much at bubble prices (either in 2022 or more recently) and the delusional “investors” listing those houses or apartments for rent (at presumably the prices they need to cover their costs, because we all know they have a god-given right to make money!) and those apartments sitting for months, until the delusional seller finally starts reducing the rent.

“Realtors are often full of crap”

Often????? LOL

Have been studying Huntsville for about 3 years as potential second home location , prices got stupid, that is a technical term, just as everywhere else between Q3 2020 and now, apartment developers joined in and the market is well on the road to overbuilt by 20%. Currently rentals are sitting empty in all neighborhoods and especially in the new garden complexes along 565 from downtown out to Decatur. Apartments.com lists approximately 3400 available units, if you add in the small complexes not listed there but on zillow and realtor there are about 4,000 available rental units in Madison County, add assorted renovations in the pipeline, unopened buildings and AirBnBs and you can see a storm brewing.

Please see :Real Page Analytics – Which Markets Could Be Most – and Least- Impacted by Apartment Construction and your eyes will be opened.

Oh and recently I began to look at rentals due to the purchase prices and if you dig down, prices are dropping and concessions are rising. Listing times are through the roof.

I think we will being those lateral sawteeth for quite a few years.

Nah, it will totally crash. “First slowly, then all at once” has some science behind it. We’ve seen these comments before the last crash. Then bam – foreclosures as far as the eye can see.

I wonder if the saw teeth aren’t the result of return to the office. At least I read an article about this happening to some of Florida’s new residents.

The New York graph may hint at this.

Hey, it’s funny you mention “return to office”. Today I got this email from our company’s CEO. I replaced the company name with XXXXXXXX.

—————————————————————

Dear XXXXXX Colleagues,

In recent meetings and conversations with XXXXXX employees across the organization, one question that we often receive is related to our workplace requirements. To bring greater clarity and consistency throughout the Company, today we are announcing that all non-manufacturing XXXXXX employees are expected to be in front of customers, with supply partners, or in a XXXXXX office or facility at least 3 days each week with one of those days being Monday.

This requirement is designed to further cultivate a more collaborative, higher-performing culture to, in turn, help accelerate our performance in 2024 and beyond. Other than Monday, in-person days should be set and agreed upon with the employee’s manager to ensure we maximize collaboration, enable opportunities for team building, and facilitate events where in-person presence is required. As always, employees are welcome to exceed this in-person expectation to ensure they meet the needs of their role.

We plan to continue to approach workplace expectations with flexibility in mind. Specific schedules for an employee’s in-person days will be assessed and determined by an office employee’s manager based on the role, including consideration of an employee’s start and end times. This approach allows us to cultivate a collaborative higher performing culture while also addressing the work-life balance considerations for our employees.

This in-person requirement will apply to all non-manufacturing XXXXXX employees and will go into effect January 1, 2024. Any requested exceptions should be raised to your manager and respective HR Business Partner, and any approvals will be provided by HR Leadership.

Almost all companies are calling their workforce back to office.

If jobs can be effectively done remotely, then why not outsource high paying jobs to cheaper geography where you have abundance of professional English speaking workers.

Love seeing the dog whistle buzz sentence..every one of these return to work memo will have them…

Honestly, I would must rather they keep it short and just say STFU, you’re coming back in the office because I want you to. Straight to the point instead of this numbing long note try to convince no one..

“This requirement is designed to further cultivate a more collaborative, higher-performing culture to, in turn, help accelerate our performance in 2024 and beyond”

@Phoenix_Ikki,

Exactly! That is why I don’t attend our company’s Town Hall meetings. They take 1 hour to say what should take a couple minutes.

Scott,

Define “Requirement”

Yours Truly,

Your Employee??

Back in the day, there was collaboration in the supply room and late hours of the office holiday parties.

Any requested exceptions should be raised to your manager and respective HR Business Partner, and any approvals will be provided by HR Leadership.

HR business partner? HR in my experience has always been staffed by witches and warlocks. Been awhile though. Probably now staffed by more WOKE folks.

I feel bad for the corporate youngsters out there.

We have the same memo planned at my shop (large international group with US HQ, I am in Germany), but not yet communicated for Jan 24 onwards, 3days minimum in the office with a not-very-subtle nudge to do more days as well. Here in Germany 3 days are usually not an issue for people, but of course we have less commute compared to the US.

The WFH policy and subsequently RTW policy looks like a labor bubble to me. Many people who were working 2 jobs remotely thus doubling their income are going to have to quit one of those jobs and return to office for the other. That’s potentially a 50% cut in wages. Maybe that could bring some if this drunken sailor spendings down, no?

My wife recently got a similar email (works in biotech/pharma). She had a prepandemic WFH job that they negated with a company wide return to office edict, no exceptions. She left the company found a decent wfh job in the same field, but was quite annoying for us.

Smart Wolfstreet commenters, please help me understand something. If someone works 2 jobs from home, and has to give one up because it’s physically impossible to be in two places at once, then that creates a job opening. Obviously the worker might have their income cut in half, but the increased demand for workers from all those extra one-at-a-time jobs would drive wages up, wouldn’t it?

Not sure. But it would probably increase productivity. And that would be a good thing.

Makes sense about the productivity. I know a few people who have multiple screens and sit at home “attending” multiple virtual meetings. I question how productive the exercise of having these meetings is at all, but from a fairness standpoint, I can see how it’s perceived as gaming the system. Making people come into the office would put an end to that practice, if that’s the reason for ending WFH.

I wonder how many people will outright reject return to office? For many people, it is no longer economically viable due to household debt levels and commute costs (gas, maintenance). And then there are those people who moved to a remote location, and are now priced out of coming back, whether renting or buying. Don’t believe me? There are hundreds of desperate testimonials on tik tok, just surrounding the gas price issue, much less the other.

Where was that article? I’ve been hearing anecdotes about this, but haven’t seen it written up by anyone.

I’ve seen a lot of places that have done “surveys” and “research”, and they are all coming up with about a third of employees at risk of “changing jobs” if forced to end WFH. That said, the sample sizes for the “surveys” are often sufficient, but they are probably self selected responses, rather than random samples that Gallup or other real pollsters would use. I still haven’t seen a big name pollster chime in. Youtube is another matter, there are hundreds of desprate videos on this topic, but that is not necessarly reliable. So, there is a preponderence of anecdotal evidence, but I am still not seeing any professional studies that could be extrapolated to realistic numbers.

Can’t beleive San Francisco with all its charm is down 11%. Unheard of. What makes San Francisco unique is every day is Halloween.

It’s not unique, others following on the heels. Dallas not far behind. See my close-ups of both further below.

On the bright side(for you Wolf), it looks like you’ll be able to write these “Most Splendid Housing Bubble” articles for years to come.

Not so great for those of us waiting on the bubble to pop.

I started the series 2017 to document the surge in home prices but just haven’t changed the series title yet. But I should change it. Maybe The Most Splendid End of the Housing Bubble, or similar

Look at the top 10+ charts closely. The whole top batch peaked in mid-2022, then fell, then bounced some this year but without setting a new high, and from that lower high, they’re now either already heading down or are in the process of turning around. The Case-Shiller numbers are 3-month moving averages, and they move softly and predictably. On a month-to-month basis, it might look like this: +0.9%, +0.6%, +0.3%, +0.1%, 0%, -0.2%, -0.5% -0.8%…

The whole top batch is going through this process in various stages. It’s hard to see in these 20-year charts because all the detail gets lost. But it’s easy to see in the numbers.

So here are 2-year charts. I just picked San Francisco, but the top batch is going through the same process in various stages. And Dallas looks almost exactly like it.

The Case-Shiller lags the NAR’s national median price by about 3-4 months, and the NAR turned around three months ago.

Why the bounce? Excuse me if you explained this earlier. I do RTGDFA, but sometimes I miss something. Exaggerated seasonal effects? But not in Vegas, but then Vegas does not really have profound seasons.

Knife catchers and lack of inventory

That must be the “we’ll lock in a good price now and refinance next year” stage of denial

Someone is going to have to write a book about that six-month period earlier this year. All kinds of things briefly went nuts.

I recognize the charts. They look similar to QQQ.

Yep, just the dead cat from oversold levels last year since the recession didn’t materialize and inflation has gone down. Now everyone is realizing it’s higher for longer and the 🤡🤡🤡 roller-coaster has just started!

Seems like the housing market has levitated itself into the new working baseline. Meaning we can expect them to begin their march to ATH.

My expectation would have been that the increase in FOMC rates would have driven prices down however these last few years seems to have chewed up and spit out logic.

Drop the rates to near zero and the housing market shot up well above the previous markets as shown across the market graphs above

I don’t think they will. On an inflation-adjusted basis, prices will probably stay in a range of anywhere from -5% to +5% appreciation through the rest of the 2020s, and maybe partway into the early 2030s. That’s INCLUSIVE of any actual appreciation, regardless of whether any inflation occurs (which – it will).

My advice: buy now, or get a high-income skill that allows you to buy soon. Prices aren’t going down anytime soon, and neither are interest rates.

“My advice: buy now,…”

Most idiotic advice ever.

“get a high-income skill…”

Good advice

“… allows you to buy soon”

Most idiotic advice ever.

Are you that SCARED about your RE asset prices?

They clearly didn’t RTGDFA or LATGDFP (Look at the pictures).

Wolf,

The comment by Economic Armageddon does not make any sense.

Economic Armageddon is leaving out an important word regarding their investment thesis: -¨annual¨.

Since the word ¨annual¨ was left out, Economic Armageddon´s forecast is for prices to stay flat, because ¨it¨ believes appreciation will only be 5% cumulative until early 2030s, so one can guess 2032, and it would mean a total of 5% appreciation spread out over 8 years, which is very little appreciation.

Obviously the downside of Economic Armageddon´s forecast is limited to 5% spread over 8 years as well, so houses will ¨trade¨ in this range for 8 years, which is not a lot of depreciation.

Economic Armageddon also believes this range is inclusive of any ¨actual¨ appreciation, but no indication is given regarding the drivers of the actual appreciation, and hence the thesis is not stated clearly and is leaving out an important piece of information.

Finally, the ending ¨advice¨ makes little sense, and is even contradictory, because if it were indeed the case (cumulative range trading of plus-minus 5%, one could wait until 2032 to buy a house, which is the opposite of advice given.

Wonder if NAR got their own version of ChatGPT..if they do, guess they found this site.

My work recently rolled put their own version of ChatGPT for internal employee to use, kind of hilarious to see these companies tripping over themselves chasing after hype that no one will use…

@Phoenix_Ikki if EA was a NAR Chatbot he would have said now is a good time to buy “or” sell. Almost 90% of Realtors will tell you it is a great time to buy “or” sell with a straight face (not having any idea that it can’t be both things at the same time).

People buy the monthly payment. Banks lend based on monthly payments. If interest rates keep going up and prices stay the same or go up, does that make sense? Try math once in a while.

Yes. Get a high-income skill, so you can enjoy the relative financial insouciance of the upper-managerial class, who don’t notice overpaying as much as if they were to overpay with income from a gig where they feel every minute of their labor being extracted in nickel & dime increments.

With over $20 trillion in liquid assets and, finally, substantial interest returns on those investments, the Fed’s current state appears only moderately effective. There might not be a bubble burst; instead, we could transition to a higher equilibrium. Forward indicators suggest the economy will surprisingly accelerate in the next few quarters. So, fasten your seatbelts! It will take the market by surprise.

Who has “$20 trillion in liquid assets?” The Fed has $7.9 trillion in total assets.

Checkmate

I meant it that all of us hold that much liquidity, not the FED. We lead the economy, the FED is a laggard.

Ciprian

OK, that may be about right.

He must be including things like the combined market cap of the entire stock market as liquid assets.

Suburban single family homes located in all major US larger metropolitan areas are hot. That is the strongest appreciation segment. On the flip side, Downtown condos are, for the most part, in the dumps. I have seen Chicago condos on the better side of town that are at 2019 prices. Suburban single family is the new trend, and I am hoping it has legs. Keeping my fingers crossed, as all my eggs are in that one basket.

Every data point in here is single-family houses. Most of them are suburban SFH because this is metro-level data. There is no condo data included here. The CS has separate condo-data for some markets, but I didn’t include them here. These are huge metros that include even distant suburbs. For example, the “New York Metro” spreads across several states and includes these counties: Fairfield CT, New Haven CT, Bergen NJ, Essex NJ, Hudson NJ, Hunterdon NJ, Mercer NJ, Middlesex NJ, Monmouth NJ, Morris NJ, Ocean NJ, Passaic NJ, Somerset NJ, Sussex NJ, Union NJ, Warren NJ, Bronx NY, Dutchess NY, Kings NY, Nassau NY, New York NY, Orange NY, Putnam NY, Queens NY, Richmond NY, Rockland NY, Suffolk NY, Westchester NY, Pike PA.

Yes. Manhattan condos/coops are down 11%.

That ‘farm’ owned by Chicago Public Schools on the southwest side @ 111th / Pulaski is about to be turned into a campground.

It’s not a true housing bubble article here until SoCalJim joins the party…as always LOL

All we are missing now is Kunal the bay area bull..then we got a party going

Phoenix, SoCal has the largest aerospace business in the country, and thanks to the wars, it is booming bigtime. Very very strong demand for rental properties from all the ex tech workers looking for a new gig.

I thought the same in 2006-2007.

Big issue right now is affordability. Something has to given in, don’t know what.

Are you a realtor or land lord ?

Just curious.

Far as I remember, SoCalJim mentioned he had beach houses in SoCal :)

Maybe he’s diversified geographically since then.

U.S. housing will never be affordable again.

Someday, a bout of deflation will hit the US economy, and homes will become much more affordable. Someday, that will happen.

Deflation isn’t measured in asset prices, but in consumer prices (goods and services that are consumed). Asset prices go up and down all the time, no problem.

Yup, as American Yale Professor Irving Fisher said: “Economics is an exact science”.

Howdy Folks. This will take a long long time to iron out. This RE bubble is the same as last time and again it is not. May take years without any real pop but just slowly hissing to the bottom?

Theres a great scene in Peewee Hermans last movie where he shows the Omish what he does for fun. I’d imagine its what you’re talking about.

Regarding Chicago, one of my siblings bought a very nice home in an upscale northern suburb (Northbrook) in the early 1990’s. It’s shocking what it’s worth today. Not much appreciation in value at all, especially if compared to nice suburbs of most East and West coast cities.

The midwest has really not had all that much appreciation since the 1990s. My house has appreciated around 2% since I bought it in 1999. The past few years they have seen some extra appreciation but not like the east and west coast.

Lots of these bubbly charts are for big cities. There are still affordable options in mid sized cities.

I remember during HB1, houses on the West coast experienced 30% to 50% price drops. The midwest saw about a 5% to 10% drop. We will probably see something similar again.

The taxes are through the roof, property tax, sales tax, all of it. And its the Midwest, and sucks for weather and politics

I can already picture the comments…not around here in paradise SoCal! and below is the proof, see going back up again. Further proof everyone wants a piece of the 405 rush hour traffic or get some good rocking from the next big quake…

IMHO…these markets are truly hopeless..

San Diego metro:

Month to month: +0.6%.

Year over year: +4.1%.

From the peak in May 2022: -2.0%.

Los Angeles metro:

Month to month: +0.5%.

Year over year: +3.2%.

From the peak in May 2022: -1.3%.

Bend is up as well.

In the long run the Bend housing market is a dead-man-walking. Its economy is pretty much based on RE, home construction, retiree’s and remote WFHers. Inflation and rising energy prices will eventually doom it.

Was thinking the same thing…lots of breweries, though.

Bend is also small (around 110k people). It has had linear growth, about 2500/yr, for the last 30 years.

Even ignoring the COVID weirdness I think there are enough new WFH’ers and tech retirees to sustain it for many more decades.

Though I can’t figure out how prices are still increasing right now. You’d think there’d be a pullback when all the COVID WFH people are being forced to move back to Portland.

Serious question:

Putting LA aside as LA is undesirable for so many reasons.

Re SD, has anyone ever met someone that said SD is a crappy city because (fill in the blank)?

The only downside to SD I can think of is the homeless issue and/or traffic. But you have that in any west coast city, don’t you? Any other bad things about SD specifically?

And, putting cost of living aside. Yeah, anywhere on the west coast (especially CA) is unaffordable for the avg family.

Compared to the 90s and earlier, it sucks now. It takes about 10 years for the shine to wear off but it’s a great 10 years I must admit.

I am born and raised in SD, and I probably will never leave, but here are the cheif complaints:

Completely unaffordable – many many people I went to high school with have had to move away to somewhere cheaper.

Mini LA – pre Covid traffic was getting horrendous. Covid has helped clear it up a bit but it’s almost back to where it was.

PatB. – if it hadn’t been taken long ago (I left in ’76, family there since 1910), you’d be welcome to my spot. (…if the massive development, associated increased population density and everpresent water-demand issues don’t give you pause, reckon it must be ok, then…).

may we all find a better day.

I have been in SD county for 33 years. The city of SD sucks because of chronic mismanagement & corruption, no funds left for even basic infrastructure (worst roads of any major US city), city is even making homeowners pay for sidewalk repairs in front of their property and assume liability for said sidewalk, downtown homeless is at crisis levels, and the city/state are determined to destroy SFH neighborhoods by overruling zoning and allowing huge “density bonus” infill developments that can turn your neighbors house into a multi story apartment building with no offstreet parking. The city and state also decreed tenants didn’t have to pay rent during Covid (but owner still have to pay mortgages). Besides all of the above its great! North county San Diego has some towns that are much better than the city of San Diego.

Definitely in uncharted territory for this bubble…looks like every market is forming that open mouth shape at the top and some like Miami even developed an under bit shape now after a rip roaring spring season bounce, this is something that didn’t happened last bubble…observationally this is weird…who knows, maybe housing bull is right and this time is different…

Or that mouth shape is ready take a big one in before falling over in a dramatic fashion…

Nice update. I think there is always some seasonality, but the last peak is vastly fueled by the Spring 2023 money printing spree by the FED.

No, it most certain was not.

I noticed Wolf’s charts show Washington DC is holding up quite well.

Month to month: -0.1%.

Year over year: +3.4%.

From high in July 2023: -0.1%

This is what we are observing on the ground in DC and close in suburbs. Things do vary by Zip code but not by much. Even in the far out suburbs (20 miles out) I noticed a shortage of existing homes for sale.

BTW, “Washington DC metro” — not D.C. — which includes DC, Calvert MD, Charles MD, Frederick MD, Montgomery MD, Prince Georges MD, Alexandria City VA, Arlington VA, Clarke VA, Fairfax VA, Fairfax City VA, Falls Church City VA, Fauquier VA, Fredericksburg City VA, Loudoun VA, Manassas City VA, Manassas Park City VA, Prince William VA, Spotsylvania VA, Stafford VA, Warren VA, Jefferson WV.

Yes, it has held up well, eked out a new high this summer, but is now also in that topping-out process:

Yep, Things have held up well all over the Washington DC Metro area, even in the basket case counties of Prince Georges County. That’s because the houses are more affordable in that county. My friends in the appraisal business are doing a very good business in these areas. We only work the center city of Washington DC, not the suburbs, but we get data from these other areas from MLS etc. Even with the high crime in DC the prices are holding up. There are few new homes there to compete with existing homes. And there are few existing homes for sale. Realtors are starving.

Double Top???

If wages can’t go higher and rates remain higher for longer where are the “bigger fools” to provide qualified buyers. Remember the Zillow exit? There are very large firms with real estate holding that are now experiencing increased tax, insurance and labor/management price increases. Is another Zillow dump possible? Real Estate is not a liquid investment and the best part about America is when one economy excludes you from participating you move to one that your family can grow into. The rust belt happened for a VERY real reason, and an “u[side down” mortgage from 2009 is not a fond memory.

All bubbles have bag holders who know its going higher, until it doesn’t.

Wolf – Some mistakes in last two lines. Hoping you will come back and say there is mistake in first two lines too (it is -5%)… :)

Month to month: unchanged.

Year over year: +5.0%

Stayed a high set in in the prior month.

*** chicagfo

The Chicago chart didn’t make it, and then it got garbled. The chart has meanwhile made it.

I’m in one of those that set a new high. As a 40+ yo renter. Lucky me.

Couldn’t get a mortgage because I’m self employed and needed a larger down payment. Now I have the down payment but no longer have enough income for the insane mortgage payment.

I really don’t understand who’s buying/able to buy in my market.

It’s irrational to expect people to act rational…to answer your questions on who’s still buying…can’t fix stupid and FOMO cocktail combo especially when it comes to flipper investors..

Plus, who wants to be peasants and live the stigma of renting and fail at being owner class and American dream…. /s

Hopefully I’m not simply being xenophobic, but there seem to be a relatively high proportion of Chinese investors in our particular market. And that’s consequential because the market volume is so poor right now and they can have an outsized effect.

I think there’s some kind of visa process/loophole local agents are exploiting, and their clients are less price sensitive because of the dual motivation to get their money out of China and themselves over to the US.

@random50 a sign that a market has Chinese buyers are lots of “8’s” in the list price. Another home on Zillow in Burlingame (that also had a recent “$100K Price Cut”) has a list price of $2,888,888.

P.S. If anyone tells you it is “racist” to say the Chinese like 8’s have them Google when the Chinese summer Olympics started (It didn’t just happen to start at 8pm on 8/8/08)…

The chinese government actually has their own police here to do unsavory things to their flock over here IF they get out of line.

So does India and Pakistan and Russia and … the list goes on and on.

They are actually having to ban the caste system in some states cuz immigrants bring that BS over here to a completely free country. It’s disgusting to see, like misogyny mixed with brutal repression. Whole workplaces have it in some areas. It’s insane, and I wouldn’t have believed it except I see it.

How is it legal? How is it overlooked? I guess cuz of populism on the rise again.

It’s not xenophobic to say…sadly this has been happening in SoCal in areas like Irvine. Arcadia, San Gabriel..etc for many years even before this crazy run up. Flying over buying and out bidding local buyers cash, park their money because they don’t rightfully trust their own government so hey let’s go somewhere else with lax control safe haven instead.

What’s sad is that maybe the recent RE wrecking doesn’t seem to affect the rich Chinese buyers only their regular citizen get the shaft…I guess they will continue on and turn neighborhood one FOB at a time..

I sold a house in the San Gabriel Valley a few years ago. The realtor said all the potential buyers (eight in total) the first day were Chinese. A Chinese eventually bought it.

Random50, just curious as to what price range you were looking in? Those who are self employed might get a slightly higher rate, but unless you have major loopholes in your 1040s or are stretching your debt to income ratios, you should qualify for a mortgage no problem.

Nunya, horribly non-standard situation unfortunately.

As self-employed also, I have had a hard time with underwriters. I’ve had to walk them thru my tax-returns, P&L, etc, and even then they still think I make a lot less then I do. I’ve had family members that make 1/2 what I do qualify for more house just because they are w2. Oh well, their loss I say. I’m happy renting right now.

I experienced the same thing a few years ago when I was a paid by mileage trucker. As soon as a mortgage company heard I was a trucker on cpm, they’d nearly hang up the phone in the spot. Half the time they wouldn’t even give a reason. I finally found a guy that told me, switch to an hourly rate and we can get you approved in under a week. CPM won’t get you anywhere without 3 years of tax returns at the same company, in the same position. Change jobs and you’re SOL for another 3 years.

Luckily or maybe unluckily I didn’t buy a house during that time. And by the time I had switched to hourly trucking jobs the housing market had ran away from me and long left me in the dust of 350k dollar single wides without power or indoor plumbing and the current 8% interest rates.

But the good thing about being a trucker is I can always sell my soul back to a company and live out of the truck with a UPS store “residential” address in South Dakota. That’s a good thing right? Right?

Same, and the taxes keep going up. We’re in Chicagoland-this is a tax assessment year in some areas and ppl getting 3k increases on their current 10k prop tax. Many are selling but they are still high, and getting 2021 prices, even for older houses that have no updates.

It’s no surprise that prices have dropped somewhat with the quick and large rise in intersest rates. If our federal government actually gets its deficit spending under control, a more significant drop in prices might be seen. Otherwise, the housing market correction will be like watching paint dry.

Is it a bubble if it doesn’t end?

It’s ending as we speak. You’re watching it live.

The Bay Area housing market is far from slowing down; in fact, it’s still going strong. Homes in San Mateo County, my own neighborhood, are getting snapped up in a matter of days, not weeks. While there may be a slight correction, it’s not substantial, especially when you consider that mortgage rates have surged by 5% over the past two years. Sunbelt cities are still experiencing a red-hot housing market. I’m inclined to think that your prediction might not be entirely accurate.

Anne Weltch,

San Mateo county, median price -12% from peak. No biggie, this just started. RE corrections takes years, not months:

I don’t know wtf is up with NYC. It must be the low taxes, easy living and fantastic weather we have been experiencing.

Manhattan real estate market is stone cold dead, almost no buyers.

Prices might be down as much 20%. Lots of price drops, very few sales. No idea how low prices would have to go to sell.

We’re trying to sell our one bedroom co-op in Manhattan Valley. In near perfect condition. We’ve dropped the price 8% from what we paid in 2015 before we renovated and put a bunch more $ in. Crickets!

Hear the same from everyone.

Rental market was hot through September, but hearing that’s dead now too.

“*** chicagfo”

Is this a typo or am I missing something?

A chart didn’t make it and instead stuff got garbled. It’s there now.

As much as I hate to say it because Im gonna catch hell, this housing bubble is very different from the last.

2008 was the culmination of massive fraud in the mortgage and banking industry with buyers and mortgage brokers lying about incomes and faking tax returns to qualify for loans to buy two, three, four, five properties to flip for a quick profit.

This rampant seculation by buyers buying multiple properties with low or zero downpayments and putting up only a few thousand dollars to reserve unbuilt properties led to massive overbuilding and reckless overlending by banks.

The end of the era of speculation, sloppy lending and buyer fraud was what precipitated the last recession. This time around, housing is still overpriced and it will suffer into the next recession, but nothing like it did in 2008-2011.

I built and sold my last homes in late 2023 and early 2024 and just returned from a trip back to Texas to see how things are going.

The market there, as in most places, is split into two distinct parts. Those who are hoping to sell -and those who HAVE to sell. Most who are hoping to sell are priced at 2021-2022 levels and sitting unsold. Those who have to sell are dropping prices slowly or quickly, depending on their situation.

The bottom line is that when you absolutely have to sell a property, the sales price is well below ask, unless its a trophy high end property or a new build offering big buyer incentives.

This is going to be the bubble that deflated long and slow, instead of popping loud and fast. High interest rates and high prices will do their job over the next couple of years. Think late 80’s, early 90’s markets.

I think your comment is very reasonable and similar to my thoughts regarding this housing bubble 2. The difference is that unlike the late 80’s/early 90’s, there is a large group of millennials that are eager to buy but can’t due to affordability issues caused by rising interest rates and sticky housing prices. It would seem logical to think that this rising interest rate environment would cause housing prices to drop faster than what we are seeing, but sellers aren’t eager to sell and trade their 2.5% mortgage for a nearly 8% mortgage, so both buyers and sellers are out of the market and we are seeing this balancing act in the housing price index charts as seesaw turbulence. I agree with your idea of slower deflation like what happened in the 90s (with more turbulence), but with the potential of rebounding fast if interest rates start dropping and wages continue to grow as they react to inflation. What is limiting demand right now is not sentiment but affordability.

CCCB

The key factor today is the shortage of inventory, due to many people being locked into low rate mortgages. A lot of these people will not sell. Even if forced to move, a lot of them will rent out their properties in order to keep the low mortgage. Rents will keep going up making it a good investment. So, there will not be a crash in prices like in 2008/2009. I don’t see any parallels to that period.

Swamp Creature, what’s your basis for saying rents will keep going up?

Rents will go up because people need housing. If they can’t afford to buy, then they will have to rent. Supply and demand will cause prices on rents to rise even while sale prices go nowhere. This is happening as we speak in the Swamp and neighboring suburbs.

I’ve read that apartment construction was (not now ?) at an all time high sometime in the last two years. Well as great as it has been since the 1970s is actually what I read (graph provided as well). More supply might help keep prices stable.

Spot on CCCB. And the proportion of “have to sell” properties will remain depressed until the black swan(s) emerge. The swans have been conspicuously missing up to now.

The most glaring absence has been the lack of large-scale layoffs, which typically accompany periods of aggressive interest rate increases. Has not happened yet in this counterintuitive economy.

As noted repeatedly in previous threads on this topic, the people who are now locked into low interest rate mortgage loans WILL NOT give those up unless they must. And one of the “must” black swans is job loss.

Wolf has previously noted that real estate prices are one of the last shoes to drop in periods of interest rate increases. That certainly seems to be the case thus far. Maybe that long-expected RE price decrease is finally taking hold.

I think housing prices will drop just based on interest rates and selling on the margin. For significant price drops, all you need is inventory to rise from .5% to 1% of homes. With 10% of homes on the vacation and rental markets, along with higher for longer interest rates, this seems more like a probability than a possibility, and the chance for downward price overshoot is substantial. The government fiscal situation is so bad, the help likely won’t be there.

When you throw in retirees sitting on huge home equity, eyeballing opportunities to cash out the home and put proceeds into a guaranteed LT 5-6% income stream, it could get very interesting. These retirees don’t want to see their home equity dwindle.

I raised this cash out opportunity with my older neighbor, and she was near flabbergasted. It’s something she hadn’t thought of. When it came to downsizing, she was thinking of renting her current place out. She was not factoring in opportunities to capture the gain and invest proceeds elsewhere, while avoiding rental hassles.

It seems a lot of RE owners out there need help with the numbers and opportunity cost of holding RE in overpriced markets. RE prices move slowly but surely when clear mathematics take hold.

Stagflation of the housing market will prevail, continued shortages accompanied by higher prices.

There is an acute shortage of BUYERS! That’s the only real shortage there is.

“long and slow”.

As to the RE Bust of 2007: I believe it was approximately 4 years peak to trough nationwide. One data set i looked at showed median prices topping June, 2007 and bottoming January 2012. So 4.5 years.

It wasn’t until March of 2016 that the median prices were back to the 2007 level.

Other data sets might vary from this but not by that much.

Of course different regions (states, cities) of the country had in some cases very different experiences.

1980s, 1990s: select areas and cities had crashes that took 7 to 10 years typically to recover.

I lived thru one in Texas.

I agree wholeheartedly that this market is poised to take a steep downturn, however it won’t be a straight line… because of the pent up demand and constant articles pushed into everyone’s faces. These articles are almost all penned by some real estate company consultant. What I think might happen is a hilly downslide until people finally realize it’s going down. But I’m no expert.

so how’s that ‘trickle down’ economics sponsored by the super rich and made operational by the Fed via QE and ZiRP working for ya all? that red v blue fight is just a charade. the real fight is the billionaires and super rich v everyone else. remember how they all got their huge bonuses after Housing Bubble One went bust. The Fed and Treasury had their backs. And when Covid hit, they all got their humongous covid relief loans first … a fraud bigger than that leading to Housing Bust One. That ‘excess savings’ didn’t come from someone who got a $1000 covid check. It went right into the uber rich pockets. So for Housing Bubble Two, don’t expect a dramatic fall … the Fed will protect the super rich at all costs.

Wolf – any chance you could share a zoomed in version of the Boston metro chart?

Boston was one of the 6 metros on the list of New Highs, and you can see it:

And, I was banned for posting an article describing the multiple offer situation in Wellesley … which is a wealthy suburb of Boston. You thought that post, which was an analysis from a well respected Wellesley realtor, was misinformation.

You posted an ad/promo by a realtor, from that realtor’s website. If you’re going to advertise or promote something, anything, on my site, you need to pay me with a wheelbarrow of USD. And if it’s a real estate ad/promo, you need to pay two wheelbarrows of USD. Crypto ads/promos cost three wheelbarrows of USD. You know how to contact me (“Contact us” tab). I’d be happy to make a deal with you. You can promote hell, and fine with me as long as you pay. No free advertising on my site.

RE promoters trying to weasel out freebees from me – that’s their and your MO. They’re swarming all over this site every time there is an article on RE. Insidious trolls, they are.

*modus operandi

Wellesley isn’t just wealthy – it is one of THE WEALTHIEST Boston burbs.

Not a great representation of the overall Boston metro to share an anecdote from, imo…

DM: Housing market is headed for a 1980s-style recession, Wells Fargo warns, thanks to ‘higher for longer’ interest rates

Soaring mortgage rates and the Federal Reserve’s aggressive rate hiking campaign could tip the housing market into a recession that echoes the slowdown of the 1980s, Wells Fargo has warned.

DM: Home buyers finally win – Real estate market rocked after jury in landmark anti-trust case awards $1.8 billion, saying realtors conspire to keep commissions on sales artificially high…

A Missouri jury has handed down a landmark ruling against the National Association of Realtors and several large residential brokerages for artificially inflating commissions. Approximately $1.8 billion, a figure that could climb as high as $5 billion, is set to be awarded to homeowners, with the case expected to have significant ramifications over the real estate industry. It was determined that realtors were capitalizing on decades-old rules that locked in commission rates despite home prices growing ever higher, allowing them to take home increasingly large sums. The ruling is the first of two major anti-trust lawsuits filed over issues in the industry, including preventing homeowners from being able to lower costs despite many people now able to find homes online and bypass the need for a realtor. As the decision came in on Tuesday, several major real estate firms including RE/Max, which settled before the trial, and Zillow saw their stocks fall amid uncertainty over the impact of the case.

There were a few of us here saying this was happening in San Diego. We were shouted down, or as best as one could shout someone down from a basement with a keyboard. This increase comes as no surprise to any of us. Why were our observations so horribly received? All we were doing was passing along what we were seeing in the market. A few months ago I said there would be some interesting surprises in the upcoming most splendid reports. San Diego is essentially an island surrounded by the ocean to the west, Mexico to the south, mountains to the east and Camp Pendleton to the north. Massive tracts of thousands of homes are no more and haven’t been for 20 years. There’s only so much land and no matter how you slice it, couples with kids want a house with a swing in the tree and a white picket fence and that’s getting harder and harder to find here. Also the fact that it was 86 on Halloween today. It’s a beautiful place and folks keep coming here.

“There were a few of us here saying this was happening in San Diego. We were shouted down, or as best as one could shout someone down from a basement with a keyboard.”

Yada-yada-yada. You’re looking at your own wishful imagination and not at the data. This is a close-up of San Diego, it’s the same rounding-off pattern, look for lower highs, lower lows:

but but but Wolf….this time is different!!!

It’s quite amazing how many in SoCal truly believe in the paradise hype and their market is invincible and some kind of Shangri-La. For crying out loud, it’s San Diego, not Monte Carlos. Nice pockets of areas but as whole it’s just another major city with plenty of traffic and problems to go around…

We’re not invincible. Look at 2008. We’re just not getting obliterated like what was hoped for by so many.

Sales in SD have slowed to a trickle. Only the rich escaping LA and SF are driving demand. And 86 is not good, you’ll be neck deep in wildfires for the next several months until you get the tiny bit of rain the area gets annually which will then wash all the garbage into the ocean, making it too polluted to surf.

There’s much better places to live; I know, I left 17 years ago and its one of the best moves I’ve ever made. Clean air, clean water, clean ocean and no traffic!

Where to?

“A few months ago I said there would be some interesting surprises in the upcoming most splendid reports. San Diego is essentially an island surrounded by the ocean to the west, Mexico to the south, mountains to the east and Camp Pendleton to the north. Massive tracts of thousands of homes are no more and haven’t been for 20 years. There’s only so much land and no matter how you slice it, couples with kids want a house with a swing in the tree and a white picket fence and that’s getting harder and harder to find here. Also the fact that it was 86 on Halloween today. It’s a beautiful place and folks keep coming here.”

___________________________________________

I heard a similar routine spun in the late ’80s, right before prices went on a 5 year slide to the tune of about -16%. I also heard the same routine in ’06, right before prices plunged – 40% over the next 6 years.

It’s all been said before. The actual truth is SD is in no way immune from a steep decline in prices – not in the past, not now. The show is just starting.

Houses that sold for a 100k 35 years ago are selling for 1M today. I suppose it all depends on how you look at it. All of us in San Diego could be wrong, though. Seems we’re wrong here. Exactly what is it that some on this site are expecting to happen in San Diego? Million dollar homes to drop to 600k, drop to 100k like the late 80’s, drop to the 20k my mom paid for her house in the 60’s?

I suspect people would argue/prefer that affordability for these $1M homes (taking into account both rates and prices) would drop into a reasonable range for folks with the requisite income levels.

For example, I see a 1300 sqft 3br 3ba home in SD listed for $1.1M. With 20% down, the monthly payment is over $7,700.

If you apply the old advice of not exceeding 28% of gross income, this would require a household annual income of over $330k, which is in the 94th percentile for SD metro.

Is it reasonable to expect that a household in the 94th percentile for income would be willing to spend $7,700 a month for a small, cramped, moderately updated cottage with backyard views of the MLK freeway and frontyard views of a dollar store across the street?

My gut tells me that this is a home more suited for a family in, say, the 75th percentile range, max. That’s an annual household income of $165k. Which would equate (using the 28% rule) to a max monthly payment of $3,800.

At current interest rates, that equates to a price of $550k. Do I expect this property to ever reach that level, probably not. But it does illustrate just how far prices are from what real people can actually afford. It also illustrates just how disruptive the low rates have been to pricing. The past few years of low rates have convinced some people that a small SFH between a freeway and a dollar store is rightfully worth anything close to a million bucks simply because it’s in SD.

I personally think society will be better served by having house prices be affordable by people in an income bracket roughly matching the quality of life indicated by the property itself. So yes, I’m totally in support of a shock to housing prices as soon as possible, even if it means certain people see a couple hundred K knocked off their net worth.

What’s it worth having a super expensive house if you can’t sell it because no one can afford it?

“Home prices rose in August to a record as a shortage of

homes for sale kept the market competitive. The S&P CoreLogic Case Shiller National Home Price Index, which measures home

prices across the nation, rose 2.6% from a year earlier in August, compared with a 1.0% annual increase the prior month. The August level was the highest since the index began in 1987. On a month-over-month basis, the index rose a seasonally adjusted 0.9% in August.”

WSJ 11/1/2023

Only providing this as “more information” as published in the main stream media.

One thing for certain, the market is becoming more illiquid as the supply and the actual sales drop.

Charts that have their scale stop at the top of the sheet are suggestive.

Single family homes still getting “scooped up” in the Greater Boston area, especially across northern MA into southern NH. Small pool of buyers and sellers driving the market at this point. A decent proportion of all cash sales from boomers also reflect an insensitivity to increased rates for many buyers in this market.

I know a few people personally that have recently bought on the expectation that mortgage rates will soon fall so they can refinance (millennials, no surprise). Risky assumption, but for anyone that hasn’t become a homeowner yet, being patient has offered no rewards thus far. Rent in the greater Boston area rent is atrocious, as are home prices, so pick your poison.

Waiting indefinitely for a home price crash that may never come (At least in New England), is a risky gamble for a huge cohort of younger buyers waiting to enter the market. The fact that 8% rates haven’t produced a sharp drop in prices is strange. Must be associated with the lingering effects of biblical levels of money printing and gov spending.

I wonder if Boston’s historically overpriced rents have something to do with it.

Anecdotally, my monthly PITI (southern NH) is less than the rent at every Boston-area apartment I’d ever rented.

8% has brought existing home sales numbers down to 2009-2011 levels, prices are going to lag that.

The opportunities to cash out RE in many parts of Seattle is huge right now. A nice 3/2 home in good school district is selling for around $1.7 million. The rent potential on that same home is only $3,900 per month.

Let’s run the numbers on that.

By selling for $1.7 million and investing proceeds, you can achieve a SAFE 6% income stream of $102,000 per year. You can reinvest the return to make it grow and beat inflation, if you choose.

By renting the same home out, you get AT-RISK gross income of $47,000, less RE and maintenance expenses of say $15,000, for total AT-RISK income stream of $32,000.

Which is better – SAFE income of $102,000/YR, or AT-RISK income of $32,000 per year? No brainer, right?

For these reasons, I see Seattle RE going nowhere but down, perhaps substantially.

In Seattle, even if you are sitting on a nice 3% mortgage, the same analysis applies. You get paid $70K/year to rent v buy. For many higher income people, that level of savings is hassle, but for moderate income folks and financially minded people, that is real money. So why not rent temporarily until prices adjust? Each person must weigh the lifestyle factors involved, but the finance aspect of it is clear and indisputable.

You are assuming that the seller would get the entire 1.7 which is not true at all. RE fees and transfer costs, capital gains taxes and others. You are also assuming that 6% safe is easy to get. Please let me know where I can get that rate as I see only about 5.3- 5.5 now.

You are also assuming rental rates, but they are climbing every year if even by small amounts and will continue as buying becomes less available. Pretty good dividend if you bought right. You are getting a house for free over time. And don’t forget tax advantages. Stock market guys always like to tell me how the market over time has outperformed housing. I always laugh at that one. My personal experience has proven that to be wrong on many levels. YMMV.

15,000 a year for expenses? Lol that is a terrible assumption unless you are really bad at being a landlord. Not including mortgage expense if you have one, that is stupidly excessive.

Lots of assumptions that are in reality wrong.

Sell now and take a loss as in timing the market, or hold long-term and benefit greatly when the market shifts as it will? I’ll keep my rentals thanks.

Come on Doug, recognize the plain evidence in front of you. You get a safe 6% return simply by buying treasuries with a small mix of Triple AAA private debt.

Sitting on overvalued RE with potential for price declines and rent is nowhere near safe, especially with chances of recession in 2024.

Doug,

Regarding the maintenance cost, you need education on Seattle. $15,000 of annual expense is being generous, with RE taxes alone on a $1.7M home upwards of $12k and roof/siding maintenance also very high in the mossy wet climate.

I’m telling you facts on the ground in Seattle, where I live. You should listen.

@Bobber if you want to sell and need the money I am not going to talk you out of it. When my grandmother died in the early 70’s my parent’s friends told them to sell her home in SF that my grandfather bought for $3K (less than 1/3 the cost of my most recent mountain bike) and take the ~$30K and invest it. They kept it and Zillow says it is worth $1.8mm today. I think prices will keep falling in most markets (and start falling in markets where they have not yet started falling) in the near term, but I’m betting that nice homes in good areas around Seattle and SF will be worth more a decade from now. If I had to bet I would guess that they won’t go up as much as they did in the last decade (A home in West Queen Anne listed for $1.63mm last sold for $762K in 2012) but I still expect them to go up as inflation marches on as it has my entire life. The CA minimum wage was $1/hr ($8/day) when I was born and next year it will be $16/hr ($20/hr for fast food workers). The West Coast of the US has a lot of problems but still hs a lot of good stuff. Lots of rich Chinese have decided the West Coast of North American is a good place to park cash in RE (I’ll start to worry when rich Americans start buying homes in China).

DougP and ApartmentInvestor – what about rent control? How do you guys factor that into your overall equation here?

@MM I’m fine with the current CA statewide apartment rent control (max increase of 5% + CPI wit a max of 10%) and since it has started I have never raised a current tenant rent to the max (I raise units to market when people move out). I don’t see rent control getting worse any time soon with vacancy control (like Berkeley and SF had in the 70’s and 80’s before it was banned). I know a long time (second generation) SF landlord (with two buildings in the Marina district) who gets around rent control by renting to only good looking young women since they almost always get married and move on allowing him to re-rent the units at market rent.

ApartmentINvestor,

You are correct about the high foreign demand, but that appears to have evaporated. Every open house in my neighborhood (East Side) was crawling with immigrant demand from Asia and Eastern Europe. The past several months, open houses are completely dead.

The rent v buy equation is just too out of whack.

Two of the biggest problems in the West (and last 5 years NW especially):

1. Wildfires

2. Drought

This past year not as bad as the last 7 years on average. I believe we had only one day with toxic smoke and only about a week to at most 10 days of smoke here in Eastern Washington. Much worse than that in 3 recent years.

September used to be my favorite month here. Most DEFINITELY not now…it is in the epicenter of wildfire season. I am hoping, but not betting on, that this year was a turning point for less fires (better prevention, better and more rapid fire suppression).

We’ll see.

Somewhere below I have a reply that has to do with wildfires, heat (drought) in many parts of the NW.

Clarification:

I mentioned toxic smoke. Literally not figuratively.

Air Quality Index over 300.

Two or three years ago had 4 of them, peaked at 499. Max is 500.

My lungs are probably the worse for it. No joke.

Used to be just east of the Cascades but Seattle has been getting a dose in recent years. And southwest Oregon a huge dose of it. Idaho yep. British Columbia you betcha.

If enough trees burn that might be the solution ?

Comparing unlevered returns to levered returns disqualifies you from providing advice on investments. 6% safe assumes 0 reinvestment risk as well. A 2% cash return +1% appreciation with 3-4x leverage is both riskier and much higher than 6%.

Doesn’t work like that.

You must depreciate the property and create a phantome cash flow of 3%/year. Tax free: lets say 36k. You also must include the equity build up, let’s say 25k. Then you tax deduct your interst: let’s say 25k. Tax free. Then the inflation rate applied to the current total interest running: let’s say 5% of 1 M, is 50K. Tax free. Then you add the rental income of 47k/32k net. Tha’ts north of 100k post tax. Meaning north of 150k pretax. Taxes and currency/inflation variations are what makes real estate a superior investment. I ignored appreciation to stay on point. But it’s job I agree.

Welp, on the walk this morning the mediocre airbnb flip house just hit the market. Judging by the lack of cars, this house lost money every single month it was for rent. Given it was flipped in 2021 and given the $1.98 beauty queen treatment it is going to lose even more money on the final sale price.

Real estate. Humph.

‘To be included in this list of the Most Splendid Housing Bubbles, the metro must have experienced a home price inflation since 2000 of at least 180%.

Personal factoid: Sold my hse in Nanaimo, Van Isle for 370 in 2014. Today at least eight hundred K more like nine. Note: not since 2000, since 2014 so prob equal Miami. .

Re: all this talk about avoiding recession. It was Fed determination to avoid recessions by lowering interest rates that got us here. In classical economics. i.e. before Greenspan ‘tamed the economic cycle’, recessions were considered a normal part of the cycle. Sure, the Fed should consider THEN lowering rates, but Greenspan would lower them at the hint of a recession, like for the Y2K imminent disaster.

Humans are always going to chase money, and hooking onto a boom will always be the easy way to get it. For every innovator there are ten who want to ride along. So booms, whether through Klondike gold or Dot. Com gold will always happen, as will the resulting hangover: recession.

To correct housing aka ‘shelter’ prices to make this essential item even vaguely affordable, deflation in housing prices needs to happen. But given the size of this component in GDP, this can’t happen without a recession.

The latter is not nice but in MYOP it’s the lesser evil. Re: the ‘hard landing’ metaphor. There is a saying by aviators, partly joking: ‘a good landing is one you walk away from’. The world will not end if 25 % of the 250 % increase in my old place is retraced.

Aviation humor, but true. When Hawker was testing the Harrier Vertical Take Off and Landing ‘jump jet’ in the sixties. one of the test pilots was former Luftwaffe. He was one of the first to find out that you can’t back off power until almost touch down. His very hard landing put landing gear thru the wings. He exits the cockpit and says: ‘that makes 11 Allied aircraft destroyed’

IN my city San Diego, prices rose 62% at/after pandemic. Now it has gone down piddly 2% from peak.

In essence , prices have not really gone down,.

Patience. RE is not crypto.