Inflation dished up another nasty surprise. Other costs jumped too. Gasoline didn’t help. This was a broad-based mess.

By Wolf Richter for WOLF STREET.

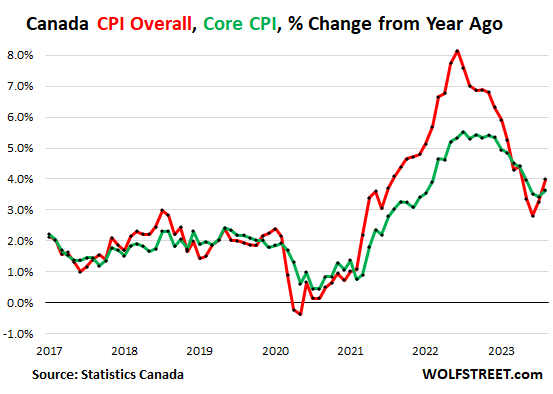

In a nasty big surprise of the type that inflation, once it’s running loose, likes to dish out, the Consumer Price Index in Canada re-accelerated in August for the second month in a row, to 4.0% year-over-year, according to Statistics Canada today, up from 3.3% in July, and 2.8% in June (red line in the chart below). As everywhere, part of it was the jump in gasoline prices. But that’s just a convenient side story.

The scary part is the red-hot inflation in housing: Inflation in rents has been shooting up and raged at the highest rate since 1983; and inflation in homeownership costs also surged.

Core CPI, which excludes food and energy, accelerated to 3.6% (green). June was Canada’s inflation-is-vanquished month. It was fun while it lasted. The other worrisome part is that on a month-to-month basis, inflation was broad-based, on top of the spikes in housing and gasoline.

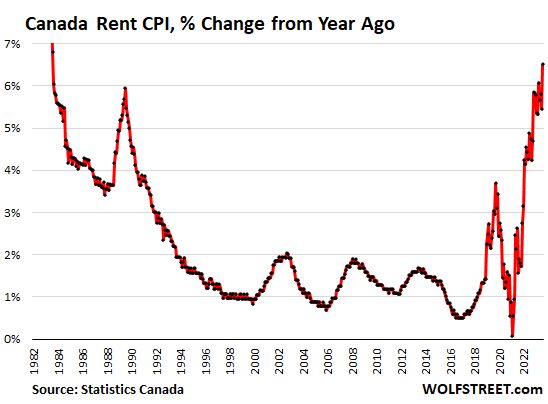

Rent inflation, hottest since 1983. In August, the CPI for rents spiked by 6.5% year-over-year, the highest since 1983. This is another sign that housing – rents and ownership costs – started to fuel inflation, and that inflation isn’t going to just vanish unless housing stops fueling it.

This long-term chart shows what massive problem the Bank of Canada has on its hands:

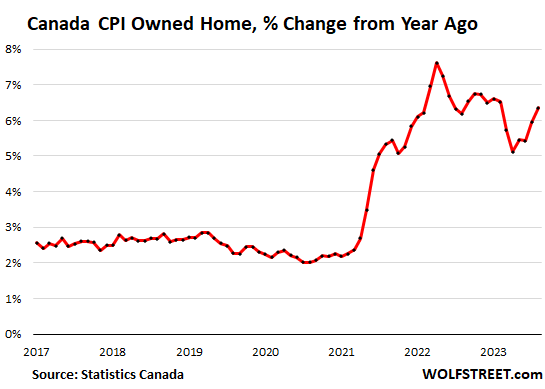

“Among other factors, a higher interest rate environment, which may create barriers to homeownership, put upward pressure on the index,” Statistics Canada said.

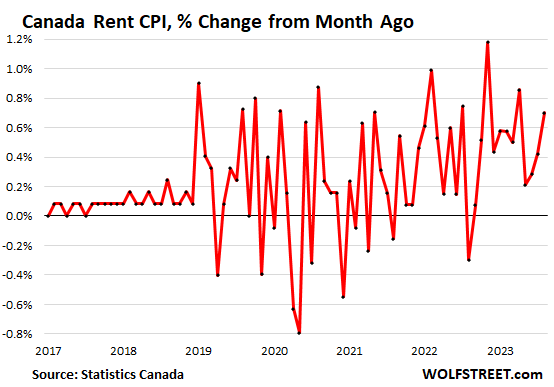

“While rent prices accelerated in eight provinces, those with the fastest price growth were Newfoundland and Labrador (+8.4%), Alberta (+6.5%), Nova Scotia (+9.5%) and Manitoba (+6.1%),” Statistics Canada said.

The month-to-month jump in the rent CPI of 0.7% (8.7% annualized) was the second-highest this year, and third-highest in 14 months:

Homeownership inflation has accelerated on a month-to-month basis in the 0.5% to 0.7% range for the past five months. In August it rose by 0.6% from July. Year-over-year, it accelerated to 6.4%, the highest since February.

This CPI for “owned accommodation” includes (% year-over-year):

- Mortgage interest cost: +30.9%

- Homeowners’ home and mortgage insurance: +9.7%

- Homeowners’ maintenance and repairs: +6.0%

- Property taxes and other special charges: +3.6%

- Other owned accommodation expenses: -0.3%

- Homeowners’ replacement cost (the dropping home prices): -0.9%.

The other worrisome part is that on a month-to-month basis, inflation was broad-based, on top of the spikes in housing.

Major categories showed substantial inflation on a month-to-month basis: Transportation (+0.7% or 8.7% annualized!); clothing and footwear (+0.5%); health and personal care (+0.4%); durable goods, which were supposed to decline (+0.3%); recreation and reading (+0.3%); household operations (+0.3%); food (+0.2%).

The Bank of Canada is now in a pickle of its own making, after having repressed interest rates for many years and after unleashing a massive QE program during the pandemic, that it is now rapidly unwinding. These erstwhile policies had the effect of creating one of the biggest housing bubbles in the world, that is now deflating.

With inflation resurging, while economic growth fizzled, the BoC left its overnight rate unchanged at 5.0% at the last meeting on September 6. With an eye on inflation, it added a clear bias for further tightening: The BoC “remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed,” it said in the statement. It has been mentioning the housing market as a source of concern. So it now has a lot more reasons to be frazzled about the housing market and how it fuels inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Justin seems very pleased with the current Canadian state of affairs and really isn’t interested in changing much of anything.

Because older Canadians don’t care about destroying their own country so long as they are okay. There is no collectivism at all here.

A mix of dog eat dog, high taxes, endless immigration and bad roads.

If you’re in an in demand job and you come here you must be mad. Which just leaves low earning immigrants squished into condos.

Americans aren’t any better. Look at the attitudes of the beneficiaries of Social Security and Medicare, as an example.

yah, because 50% of those ‘earning’ ssi benefits of $850 or less per month to live on

cause they have NO OTHER ASSETS or income

I’m about to raise rent $50 to $600 per month

expect to see many seeking help

—

I’ll report in few months

Ultimately, we’re at the point where it’s all a zero sum game. The pie isn’t getting better in terms of productivity.

Einhal….

I and my employer paid just shy of $400K into Social Security over the years that I was employed (per my statement on the SSA website). At the current rate of withdrawal (my “freebies” in your mind), it will take @ 11 years for me to break even – without any investment return (aka, interest, etc..) ever being paid on a dime of it. Odds are, that $400K would have turned into over $1M if left to me to invest, even in nothing more than CD’s. So, in some ways, many SS recipients got screwed too.

Or did you forget the little detail that, in order for recipients to get payments, they needed to actually put something in and likely earned less because their employer factored that expense into their compensation.

The Medicare issue goes far beyond what you’re harping about. Income doesn’t equal expense – not because of “geezer greed”, but due to medical monopolies allowed by legislative “heroes” and their “affordable health care” meddling (aka the greatest gift ever to insurance companies) and failure to enforce anti-trust laws. Don’t believe it? If you take a generic drug… price it at Walgreens or CVS then look at the same generic at the Dallas guy who owns the Mavericks drug website. It’s astounding in many cases. Geezers like me won’t pay CVS 3x’s more for convenience, even if it’s not my money – and I don’t use my “insurance” at the Maverick guy’s website because it’s more brain damage than it’s worth. (The 3x’s more comes from the fact that MCCPD charges <$1 per pill… CVS mail order charges $3 per pill with "insurance". Without "insurance", it's many multiples higher.)

Excellent post, El Katz. You said everything that I wanted to say in response to Einhal.

“Endless” immigration is an absolute necessity when you have a demographic profile like Canada has. Countries with aging populations have almost no options other than opening up to immigrants from those countries with younger demographics. The immediate drawbacks (housing inflation from added demand in this case) must be put up against the much more painful inevitable alternative.

For decades I read/heard that without greatly increasing immigration Canada will go from having ~7 workers for every retiree to having ~3 workers for every retiree. No amount of technological advance can compensate for that kind of labour shortage.

> no option

How about not making life impossible for families? I completely disagree with you.

Endless immigration from the third world has never benefitted any country in history and Canada won’t be the first.

In response to El Katz:

Whoa, that’s all so wrong.

You seemed to be confusing ‘quality of life’ with increasing population or GDP. Who the hell wants to live in a country (anywhere in the west) where 90+% of the gains from population or GDP growth flow ONLY to the top 5% INCLUDING GOVERNMENT. The destruction of the nation is almost complete.

Speaking of dogs, wasn’t it Stan Rogers who famously compared Canadians to puppies and said, “they just like to be liked.” Foreign real estate investment in Canada, Vancouver particularly, is insane. I heard they’re planning to import 1 million new immigrants a year. We’ve been getting shafted by NAFTA in the US for decades, but the newer front is China shipping finished or mostly-finished goods into Canada, slapping a “Made in Canada” sticker on it and avoiding tariffs.

Almost all steel, when a product is labelled, “Made in Canada” is Chinese steel.

The US is getting shafted LOL!!!

Ever since Canada joined free trade, first with the US, and then with Mexico many of the middle class jobs left. Many of them Manufacturing jobs, 1st moved to the US and then moved to Mexico. If anyone’s been shafted it’s Canada.

Sounds like Ancient Rome except for the part about roads.

Makes you wonder if Jerome will think it’s prudent to “hold” tomorrow when clearly the rate of inflation is going the wrong direction.

The new talking points are “peak rates” (from “pivot” rates earlier) . I’m waiting for 9% CD to commit my capital.

I don’t think we get to 9 percent but possible . With QT ongoing.

I’m 67 and have been saving for years to purchase my first home. On SSDI my savings are minimal but enough to purchase (or so I thought). I have rented for 12 years from same landlord who has within the past 2 years began “squeezing “ more rent from me. Always at Christmas time and $25.00 each time. My current rent is $750. That may seem small to some but it isn’t small on SS. The housing market here in Rockford, IL is terrible. It is a “sellers market” and the sellers and realtors are taking advantage. All nice homes that were within my price range >110,000 are now 130,000+. Only the very worst houses are within my spending limits. Even at 110,000 my payment is likely to surpass my rent because of MRI being 7%+. My son says it is going to get worse. Should I buy something (anything) or stay renting? Thank you for your kind response ~ Linn

There’s more to owning a house than simply making the payment. You have to factor in many expenses that you currently call the landlord to have repaired at no cost to you. There’s that and having to rely on repair people – unless you (for at least a few years) or your son is willing to do minor stuff yourself. Even something as simple as mowing your own lawn requires an investment in a lawnmower.

Home ownership isn’t a panacea for rising rents. There’s a lot of things that need to be done – like picking weeds or mowing a lawn. A condo isn’t the answer as the HOA fees go up in lockstep with costs you have no control over.

Not saying you shouldn’t buy, but do an analysis of what you can truly afford to pay and figure several thousand dollars per year in addition for maintenance, repair and replacement. Most people don’t bother, but having your air conditioner condenser cleaned annually (the gizmo that sits outside with the big fan on it) can cost you what your annual rent increase has been – which, at that point, would make it a break even proposition.

110,000-130,000 for a house is like 1990s prices for most places!

Advise not to publicize these prices too much else everyone will be clamoring for these houses lol.

Listen to El Katz. Very valuable advice.

Even your grandchildren won’t even see 9 percent.

Funny how they express concern, but never do what’s necessary to get inflation under control.

The worker gets lip service, again, while the people with capital rest easy.

Thoughts and prayers for the poor Canadian renters.

The US is in the same ballpark. Asking rents are falling, but continuing leases are still rising at a red hot pace.

Rents are starting to rise outside of Ontario and British Columbia. This has never happened before as the incoming immigrants figure out the math and end up in Siberian land where the winters can turn you into a human icicle. I guess they figured out living in Ontario or British Columbia requires working at least 2 fulltime jobs at the same time to rent a room in a condo or basement. Some are even living in closets now.

Thank you, Federal Government, for spending money you don’t have and a Federal Reserve which prints that money. That is the root cause of inflation, not greedy landlords or corporations, but our own elected representatives in Washington. “Inflation is always and everywhere a monetary phenomenon.” Milton Friedman.

Talk about this inflation or that inflation is nonsense. It starts with inflation of the money supply and will ultimately spread everywhere. An ice cream cone, a haircut or a new car; If the money supply is inflated 2%, everything will ultimately go up around 2%. Some item will increase faster than others. But in the end, prices will all go up 2%.

It boggles the mind to see supposedly smart central bankers determine a 300% rise in RE and stocks in a decade is not a problem, because it’s not reflected in CPI. Its clear that asset inflation migrates to CPI, sooner or later, and a thoughtful person would know that from the start.

These central bankers are indeed very smart. Their smart decisions enriched themselves, their friends and families and the rich people sitting on various kind of assets. These CB folks are pretty rich along with politicians.

Don’t get fooled by the explicit mandate of these CBs. At the end of the day, they are mere humans driven by greed and other vices.

This is BS. They’re imperfect humans which are honestly doing the best they can.

Yes, the CBs set the foundation for this but did so because the alternative was worse: the great recession instead being a second great depression, the pandemic throwing the market/economy into free-fall, etc.

Yes, there were likely better choices but that’s only visible with the benefit of hindsight.

The thing is, you complain about where we are and why but nobody can reliably say where we would be had they acted differently. But I CAN reliably say that you would then be complaining about that.

the Great Recession didn’t just spring out of thin air. Government policy was largely responsible.

So hard to give them kudos on mitigating the worst outcomes from a situation they made. And I do realize I am lumping the Fed, CB and the government all in one heap.

Brian,

Central banks are leading monetary policy for the world. Performance expectations are rightfully very high.

They intentionally overstepped their mandates, fiddling with the long end of the curve. For example, buying MBS, buying BBB bonds, suppressing interest rates for long period below what any rational person would consider a natural interest rate, so as to intentionally distort asset prices. The QE policy was intended to create a wealth effect and protect asset prices of asset holders which is paid for by less wealthy members of society (the overwhelming majority). They designed and created the greatest wealth concentration we’ve ever seen, under the ridiculous assumption there would be some charitable trickle down effect. They pumped housing prices and stock prices to ridiculous levels, effectively denying many young families the opportunity to have financial stability. They continued to buy MBS while inflation was surging and home prices were rising 30-100% during the 2020 to 2022 period.

These are not forgivable “mistakes”. These are huge judgement lapses that fit easily into the category of negligent policy-making from the very start.

Great comment. Agree 300%. Govt LOVE to inflate asset prices in almost all countries, because most voters own their homes and get happier when they check zillow and see their home price go up. Most voters believe that if their home value is going up, the economy is doing good.

“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman.

LOL. I always get a laugh when I see that quote.

It reminds me that “Water is always and everywhere a wet phenomenon.”

That is econ 101. The real world is more subtle. If an increase in money supply leads to incremental productive investment, then prices can actually fall. Most people forget the “ceritas paribus” part from their econ class.

It is always amusing to me when a pedantic, condescending post screws up its own Latin reference.

And yet it kind of proves the point. Everyone has half-assed understanding, but think they know everything. Kind of like McKinsey. I too suffer from not having spell correct on Latin and not really caring because while I forgot the spelling, I didn’t forget the point. But you lost the forest for the skinny, lone tree.

Do a bit of Sherlocking.

“an increase in money supply leads to incremental productive investment”

Other things being equal, newly printed money and credit is wasted in speculation in the stock market and existing Real estate.

Albeit with a tiny amount going into something productive.

“ If the money supply is inflated 2%, everything will ultimately go up around 2%. Some item will increase faster than others. But in the end, prices will all go up 2%.”

2%?

Where do you live?

Australia has looked over at Canada and has said.

“Mate, hold my beer. That’s not rental inflation, THIS is rental inflation”

🐊🦘🇦🇺

See here for the figures for Sydney. Change the locality to see nationwide or other cities.

https://sqmresearch.com.au/weekly-rents.php?region=nsw%3A%3ASydney&type=c&t=1

It’s gone pretty 🍌 in Perth to . I was speaking to a chippie who just moved over from the UK and is% 990 a week. I’m

Noice m8. Oi, you can drop a hundred tenners on a fridge box flat to watch some wagging bogans start a dust up with some deros. Good luck sneaking a kip in though, innit?

Yeah m8, true blue straya for ya roight?

Doesn’t Australia have a C$20 equivalent minimum wage though? In Canada, we have the major city of Toronto using agencies to pay skilled workers minimum wage C$15/hr for doing the same or more work than a public sector counterpart earning C$50/hr with pensions & generous dental care.

I think they have Australian dollars there. So, not real dollars.

The Australian dollars are called dollarydoos. Their change is actually interchangeable with most arcade tokens here in America.

The Ontario (province of Ontario) government announced on March 31, 2023, that the province’s general minimum wage will increase from $15.50/hr to $16.55/hr on October 1, 2023.

All British colonies are the same: the dream is to be a landlord. Financialization everywhere. High immigration to ramp up pressure on housing. I hope the elite get what’s coming.

Feudal England and their landed gentry. Farmers worked and toiled on the land, and the landowners wanted rent for doing nothing.

A Rent-seeking economy is terrible for everyone. Rent, or take a huge mortgage.

This website has shown that Americans are still spending like ‘drunken sailors’, but in Canada, people can’t find money to spend after paying rent or mortgages.

Additionally, Americans are spending more on credit cards, but paying off the balance in full before the end of the grace period. In Canada, Canadians are using credit card debt as a Plan B to buy groceries for survival.

I think you misunderstand the concept of rent-seeking, which has very little connection with the existence of landlords and renters.

It’s a concept about someone occupying ownership of an asset, extracting the profit, and providing no value in return.

Landlords in our system absolutely provide value. They assume the risk of purchasing an asset that could lose value over time. They provide the capital necessary to procure the loan for the purchase of an asset that many renters would not actually be able to purchase on their own. They assume the burden of key aspects of maintenance for the property.

Meanwhile, renters benefit by getting to occupy a home in their desired area without having to make any significant down payment. They don’t assume any risk in terms of the underlying value of the asset. They don’t have to fix the roof or replace the oven if something goes wrong. They also contribute (in many cases to a greater degree than average) to wear and tear of the property.

We have an open system. Renters rent because they choose to. And while many landlords do make a profit, many also take a loss or a small profit. Moreover, in a market like the crazy one we have now, the mortgage payment on a home purchased today would likely far exceed the rent that could be demanded for the same unit. And in this way, renters are actually getting a better deal. They can live in a house, assume very little risk, pay a small amount up front in the form of a security deposit, and enjoy monthly rent below what it would cost someone to buy the same house with a 20% down payment.

Land doesn’t go down in value, unless its in a war zone or humanitarian crisis zone.

And the noveau-terre Canadian landlords expect to profit from their investment, and also gain capital gains on their properties while getting the mortgage paid by the renter.

Zert landlordism is absolutely a subset of rent seeking.

The primary value sold by landlords is the location and they did not create that value.

It’s completely incorrect to exclude landlords from rent seeking. Just ask Adam Smith.

Lastly we do not have an “open system”. Canada operates a combination of:

– artificial scarcity of land, by denying planning and refusing to expand infrastructure

– artificial surplus of people by importing people as the locals cannot afford to have children, to create artificial demand

– artificial abundance of credit by allowing the 4 major banks to create credit against housing at insane levels at artificially low rates

– artificial high demand by allowing any surplus capital anywhere in the world to purchase Canadian housing

Land is a special case as it is finite.

Land value tax captures societal value while allowing the improvements to the building to be captured by the owner.

Canada is an insane nightmare. What they’re doing here is so extreme it’s incredible.

Zest, what you say is true in a real capitalist system.

In a system where the governments and central banks are putting a floor under asset prices, landlords have not taken the risk that they should be taking for the returns you mention.

Most places haven’t gotten away with forcing high immigration, but the financialization and rent-seeking behaviors, have struck nearly every developed economy and quite a few developing ones.

Amazing isn’t it.

What do you think the chances are of all these disparate countries all having the same idea to have the same policies at the exact same time?

And that every single one of them would have huge state coordinated propaganda through news and their education system about multiculturalism, and a false equivalency drawn between criticizing excessive immigration levels and racism to crush opposition, and that despite the policy being wildly unpopular each country would stick resolutely to it?

Leaving citizens in each western country with nowhere cheap to flee to. What are the odds of that just “happening”?

It’s not necessarily coordinated (most of the time), I describe it as “monkey see, monkey do” behavior. It’s not just the west though, Japan was an innovator in this category. We see these behaviors across Asia as well.

More than anything, because today’s world is far richer than any in the past, a bunch of middle classes have formed in countries across the world, as these middle classes got older, they were comfortable with the status quo, taking from younger generations, as the status quo took more slowly from the older generations. They “monkey do, what they monkey saw”.

Now we “monkey wait, until old monkey assets crash”. After that “monkey mad, monkey change into something, something”. It’s gonna be the “young monkey vs. old monkey, fight for the ages.

“a higher interest rate environment, which may create barriers to homeownership, put upward pressure on the index”

It’s ridiculous how you see this theme again and again: blaming high interest rates for the high rent prices, as to imply that it is high interest rates that are keeping people from buying houses, and thus competing for more for rental units.

It is asset price, and asset price alone that has caused this disaster.

Crash the housing prices, and the rent prices will go down with it. Interest rates would become largely irrelevant, because any future drop in rates will allow refinancing opportunities in the future on a lower cost basis (“date the rate”).

But we can’t have that, now can we? Too much funny money “wealth” to cling on to and property tax grift to exploit from inflated asset prices.

My son recently bid 800k on a home with asking of 999K. Homes sold gor 825-850 last year. Buyers need to stop the insanity of paying these try idiculous prices!

Great comment/sound observations

Unfortunately, it’s not just a theme, it’s a nondisclosed government policy to preserve asset price bubbles. It’s amazing that governmental bodies are allowed to spout such nonsense. They have become servants of the top 5%.

“Crash the housing prices, and the rent prices will go down with it.”

How else do you crash housing prices if not for interest rates?

Sell the fing treasury and mbs hand over fist….

Very easily. First, get rid of government guarantees of mortgages. Second, get rid of tax deductions for mortgage interest. Third, make it illegal for non-U.S. citizens or permanent residents to buy residential real estate in desirable areas (with a formula to be determined).

Do all of that, and housing prices will crash, and crash hard.

Land value tax for the win.

Replace income tax.

georgist,

“Land value tax for the win.

Replace income tax.”

Will make me and mom homeless. We are not some smug portly capitalist caricatures. So, insurrection. Governments might not realize they are starting to walk a fine line between conflicting social class interests. A fine mess.

At this moment, monthly rent prices are still much cheaper than PITI mortgage payments.

I believe this because otherwise speculators would be buying up houses for rental investments.

Either housing prices will come down or rent prices will go up to reach equilibrium.

If rent prices go up over the upcoming years, then it would be best to buy now.

If house prices go down and overshoot the comparable rent payments like they did in the US in 2012, then it would be best to continue renting.

It is likely house prices will go down and rent prices will go up until the PITI+maintenance reaches rent payments.

My crystal ball is broken and I’m not privy to any Canadian Fed insider information.

“Either housing prices will come down or rent prices will go up to reach equilibrium.”

Agree 100%

In Canada the average working class person believes the converse is true. Canada doesn’t import “brainiacs” from foreign countries.

I feel like the only way this mess will resolve itself is with a recession, people losing their homes, and prices dropping. A cleaning of all the undeserved wealth amassed by capital owners. Or else, nothing will get fixed.

Yes, problems have accumulated like kindling. Alas, something will break. Big question is how big, deep and wide before new equilibrium. There must be some price for these imbalances.. Not sure if existing institutions can manage that.

You’ll never hit all the “undeserved wealth” as you describe it….

If home prices drop – even stocks – it won’t matter that much. That will hit the younger peeps just as hard, if not harder. It will likely also make mortgages unobtanium but for the gold plated people who don’t need the money in the first place. Ends up making it even more difficult for first time buyers.

Those, who are hoarding cash and the vulture capitalists, will swoop in and it’ll be “deja vu all over again”. You’ll, once again, find yourself standing on the side of the road wondering WTF happened.

Rents won’t come down meaningfully, at least in the US. If you look at the FRED CPI for rent of residence it flattened out for about 3 years from 2007 to 2010, then just took off again.

Rents are already coming down in my locality. We’re talking a 25% drop from early 2022 prices. Meanwhile real estate asset prices are sky high.

Markets appear to correct for rents faster than RE asset prices, as without government interference like eviction moratoriums and “emergency” rental assistance, rental prices are controlled more by market forces. There is still the “only go up” delusion in my locality for RE asset prices, but if that sentiment ever reverses (as it did extremely suddenly in late 2008), then it’s game over.

BTW rents were not bad in 2007, but they are absurd right now. I made peanuts back then and could easily afford a 1 bedroom. A similar inflation-adjusted salary for the same apartment in 2022 would have been hand to mouth. It’s a different ballgame.

Good post. I think the real reason rents correct faster is that owners who want to sell figure they can hold out for the right buyer/Fed pivot/whatever, but a landlord who wants to rent real estate out realizes that every month a unit sits vacant is lost money, so they’re more likely to fill it, even if it’s for less than they want to get.

Asking rents* are coming down.

We are not going to see national rent disinflation for some time if ever. Get used to the new normal.

I disagree. Rents are still too low, vis-a-vis asset (home) prices.

Rents need to correct up and assets need to correct down to be in equilibrium.

In Canada today there’s bidding wars for rentals everywhere across the country.

Remind me what was crashing so bad during the 2008 presidential election season, collapsing so fast that John McCain suspended his campaign vs Barack Obama?

Oh yeah, it was assets.

Exactly correct. The root cause is in letting prices go too hirto begin with.

Rule one of the media: no root cause analysis. Ever!

It’s gotten bad enough for enough people that Other Forms of economy are making a comeback, not controlled by the Financial Industrial Complex. One guy cuts stone. Another makes lumber and paneling. Two guys put together a foundry and restored a Bridgeport, and a couple fired up a kiln and make glass and brick, tile and pipe. Everybody raises crops and has gardens. Teachers get paid in kind and teach Thoreau. Windmills, solar panels, fish farming. Nobody pays income tax, or sales tax, or property tax. Absentee investors don’t take 20% and managers don’t take another 20%. Nobody goes hungry. Nobody spends a lot on vehicles or commuting to a dreary slightly-paid thankless employment. They’re lucky enough to be sited away from the fires but did get a lot of smoke. Cash flow is positive despite the external expenditures, and you can’t call them Marxists because they’re incorporated. Nobody gets SARS-CoV-2. One guy gets a TV bill.

“You wouldn’t think there’d be much money in potatoes, chickens, and wood-chopping, but it all adds up.”

even in a small way people can do similar without the “communal” feeling (not that there is anything wrong with that) definitely available if you look hard enough for it. Local grass fed beef / chickens/ local grown organic produce are available for cash or trade. It takes a little work to find it but it is there you just need to be connected locally enough. We buy local – eat better and save a little money as well. Pay cash with the locals and get credit card charge points with corporations.

You also can’t call them Marxist as it isn’t even close to what Marx believed. If people call me a Marxist or a leftist I simply say “thank you”. I do overall appreciate your point however and good to see what is happening as any gain in peoples condition is an improvement.

There’s a Daniel Suarez novel (which was, at the time, considered science fiction circa 2000) named Freedom that describes exactly what you posted and what steps corporations and the government took to squelch such activity.

The fed made the same mistake by not tightening again in September. It’s going to bite them in the *ss next month, just like Canada

The Fed meeting is tomorrow. Do you know something we don’t?

No, it’s going to bite the rest of us in the *ss.

No Problem, no problem.

You need to be patient with Trudeau-economics.

“Deficits fix themselves.”

To distract the average Government subsidized Canadian, Trudeau is egging Modi on to start a hot war with India. For sure, that will cure Canadian inflation.

Trust me.

Trudeau is egging on the Indians solely to improve his polling in certain areas.

Otherwise, he could not care less.

Look Wolf, it is very simple, first you ramp up immigration to a level miles beyond anywhere it has been before (immigration is at the same volume in Canada as it is in the US currently, despite the US being 9 times larger in population).

Then, when all the immigration drives rents way up due to a shortage of housing, you get rid of this resulting inflation by raising rates. Higher rates will slow the economy by reducing the number of houses that gets built, and presto, problem solved. Er, kind of?

But seriously, there is no ‘overheated demand’ causing accelerating inflation story in Canada at the moment that I can see. Rent is up because of immigration/housing shortage. Interest rates are up because the central bank raised rates. And oil is up because of Saudi/Russian cutbacks on production. None of that is related to people having more money than they used to or wage increases (ie inflation).

You mention that inflation was broad based month to month, but the figures I saw showed that the increase in annual inflation rate from last month was entirely due to fuel prices. Yes, some areas are seeing inflation and some deflation but overall, it is the same picture as last month, except for oil. Good news is that food inflation seems to be trending down.

It seems like our best hope for some relief in Canada is an economic bank shot in which India orders an extra-judicial murder on Canadian soil, the Canadian PM gets pissy with the Indian PM and the Indian PM puts a stop on Indians coming to Canada, so then the pressure on rents can come down and the housing crisis will ease a little bit giving the central bank more room to hold the line on rates.

The US has nothing to do or say about the laws of Canada. That is entirely the business of Justin and his subjects and it just doesn’t matter and is none of the business of the US at all.

Socal, are you sure about that?

Wasn’t long ago Canada was center stage in the escalation in US-China tension with the capture of the Huawei CFO on Canadian soil, at the behest of Washington.

As long as both are G7 nations, this spat with India is a huge deal

US is too busy trying to woo India against China and Russia to notice.

Trudeau is a distraction.

Immigration has been weaponised.

Low rates only force up asset prices if as a precondition demand comfortably exceeds supply. Once this precondition holds, people must bid against one another to secure the scarce (and *essential*) good.

Canada has repeatedly increased immigration, decreased interest rates and banned building enough homes. All of these variables are readily available to the state in real time. They have watched these indicators move in the desired direction and at each moment have either continued down the path, or in the case of immigration, accelerated the rate.

None of this could possibly be a surprise nor an accident, the outcome is trivially predictable.

Why are they doing this? I have no idea.

Is it deliberate? No question.

You’ll own nothing and be happy.

The feeling in the states is that home moaners in the great white north will take grievous losses on their real estate holdings more politely.

The inflationary impact of maintenance in condos and common elements is exacerbated as artificially low maintenance fees including funding of reserve pools finally play catch up see the Canadian institute of actuaries detailed report on this

Hence serial assessment s amd big spikes in fees especially the portion going to reserve pool funds

This of course is also passed on to renters

Further exacerbation is how the green hole grant and interest free loan from Natural resources Canada specifically excludes mid and high rise condos owners versus what appears to be all other owner situations including landlord in situ for single dwelling

I also wonder if the lifting of gst on new rental builds will trigger a wave of renovictions from rent controlled older purpose build apartments that will be bulldozed. And replaced with higher builds

4% inflation trending upwards, but the politicians want the BOC governor’s head for trying to reduce the supply of money by making cash more investable with 5% and 6% GICs and bonds.

You just can’t win with the Canadian political class & their rental properties.

Housing is pretty much a have-to-have. New housing construction and existing housing maintenance is heavily dependent on oil.

Oil is going up and will very likely stay higher as Saudi A and Russia are not going to give ‘ol USA and the rest of the spoiled west a break on their oil.

And in spite of all the claptrap about US fracking saving the day, ain’t gonna happen. Even though the US touts it has been self sufficient in oil, it’s the wrong stuff coming out of the fracked wells. We still have to import a good portion for our glutonous 20 mbd with oversees oil which is the real deal to make gasoline and diesel. High diesel prices (new reality) make for some big time inflationary impacts. Everything ships with diesel.

Inflation is not just from printing money. We now are in an era where diminishing oil reserves is and will continue to drive prices higher. Of course there will be tremendous demand destruction with this but overall, things you have to have will get more expensive.

We might not like high oil prices but need them. Nothing else will slow down CO2 emissions even a little.

Climate change is not a “doom” switch that turns suddenly at 2050 or 2100 but its like inflation a constant tax in the future with higher costs for agriculture products, infrastructure investments, potential geopolitical unrests.

These costs will slowly but shurly add up.

Toby – they’ve been adding for awhile, now (…and adding a great deal of uncertainty-air/freshwater/food, anyone?-to the future of the spacecraft’s life-support systems…)…

Good observation.

may we all find a better day.

I wish Canadians luck. CRE folks in my Class A city on the west coast are in a holding pattern. Nobody wants to be that guy who determines the new asset pricing in X. Smarts folks are listing as “negotiable” or “call the broker”.

Folks are watching carefully what the new comps are going to be. Russian town home guys are still at it and prime projects are moving ahead. Everything else is on hold.

Folks are looking for cash flow and strong, stable rents deals. Empty dirt projects are dead. This is not going to end well for many folks, especially if they have to refinance. They are all waiting for the pivot, lower labor and material costs. Smoking the hopium. Fortunately, I have strong cash flow, no outstanding debt, and large cash reserves. But I am bracing for the storm. I was thinking I might be able to capitalize on this, but I am trying to catch a falling knife. Not a good feeling and I am a freaking drunken sailor.

FOMC will probably stand still this round to support the .50% increase next round. Dunno. Sh1t, I am going to hand out big candy bars to the kids during Halloween. Love to see faces light up and smile when they get them.

Good luck, folks.

Canada has become “challenging” for lower income Canadians. In this province, minimum wage is $14.50/ hr, median income is $60000, Poverty rate 10%, young adults 20%

A few numbers from the internet for context:

Average new car price up 21% in past 12 months to $66300.

Average used car prices up 50% yoy to $35000 in 2022.

Gas is $7.33 per US gal. up from +- $5.00 in 2020 pre pandemic.

Rents up 20% yoy to $1850 for 1 bdrm apt.

Groceries up 44% from 2019.

But CPI is only 4%, so no problem!

Canada is not income related.

You bought a home ten years ago and you work in a basic office job? You’re okay.

You don’t own a home and you earn 5 times the median wage in a difficult, stressful job? You’re screwed. Every raise you get to catch up on housing? Halve it, taxes.

In Canada you can’t work your way out. Stay in your caste.

Although I also agree, they’re massively lying about inflation numbers. Nightmare.

And supposedly Socialist Canada taxes income at the Minimum wage level.

Got to pay all those elite Government Employees and Jet Fuel rides somehow.

Perhaps off subject, but I’ve always wondered why Canada has so few banks, while the US has thousands. Both operate under fiat based fractional reserve banking system including a powerful central bank of last resort.

Is it the result of cultural issues or banking laws that cause the difference?

Thanks to any who care to shed light…

Literally everything is a monopoly here.

There’s no competition except restaurants. And they’re all ponying up to the same landlords.

It’s an economic zone. A company town.

Thanks, Georgist

In banking, is it by law, or evolution, or something else?

LOL! “law” in banking? MBS broke 100+ years of contract law. Remind us, who went to prison?

At least Regan had the balls to send some people to prison during the S&L crisis.

Full feudal society, coming right up!

Milk, eggs, timber. Just about everything produced in Canada requires a membership in the Quota Club. Membership closed.

I think the word you are looking for its oligopoly. There are 5 major banks that operate across Canada. The last major bank failure took place in 1923 when the Home Bank failed. Perhaps that is what encouraged the Federal government to support strong banks and keep out most foreign competition in the industry.

Prior to NAFTA, the economy was propped up by high tariffs and consumers paid high prices for most manufactured goods.

Canada had many small banks but they mostly went bust in the 1930’s depression years

I’ll throw in my observations as a law clerk in Ontario, but I’m no expert so take them with a grain of salt.

georgist saying everything is a monopoly isn’t wrong. Oligopoly is probably the right word. Each business sector has only 2-5 key players that are clearly in bed together, and with the government, fixing prices and service costs. If you want an example check out what happened when US telecoms tried to enter Canada. Or when the trucks suddenly stopped showing up when Target came to town for a year or so. That story is a trip.

For banks specifically, I believe they’re allowed to get a lot bigger in Canada than in the US. National banks are a thing here, and our banks are large enough to not only span the country but to also have branches in the US, and possibly overseas. For example I know TD bank (Toronto-Dominion) has US branches. Maybe they all do at this point.

So the short answer to your question: we have few banks because the ones we have are enormous and they’ve dominated any possible competition. They’re also cozy with the government, though to what extent it’s impossible for a peon like me to say.

Quick note: I might be misinformed on the Target story. I remember reading about their supply chain issues suddenly disappearing once they decided to leave, but that could just be conspiracy nonsense I picked up from some old rag. When I look it up now all I see is that Target mismanaged the move. Like I said, grain of salt lol.

Canadian banks closed accounts of supporters of the Truckers/Covid protesters, without batting an eye.

Ottawa and Toronto are glued at the hip.

The Flu Trux Klan? Who could forget those bozos!

Probably the only thing I supported the current government on was shutting down the Freedumb rally.

Took the government a while to wake up and do something but they did their best, given how inept they are.

The only thing they normally can do effectively is give away free money without controls.

Wolf,

Excellent! Please provide more such analysis in the U.S. markets. I am looking into expending my own property management company. It “seems” like there is an opportunity here. Wealthy folks with real estate assets don’t want to do the work, but want the ROI. New asset purchases is being limited to cash buyers because of interest rates, and many of these cash buyers also looking for property management, which will become increasingly challenging as society further splits into haves and have-nots, so these owners definitely don’t want to do the management themselves. I appreciate your thoughts and data.

“Bank of Canada in a Pickle of its Own Making”

Sort of. They have succeeded in their goal of increasing the wealth of their privileged constituency without causing the labouring livestock to stampede to whatever the modern equivalent of Le Bastille may be, and that can be tricky. Nobody is really happy, but then, nobody is unhappy enough to really change the way these things are done.

Pretty lousy goal, huh? Maybe the goal is lousy.

I have questions.

What exactly is the purpose of an economy? Of finance? Of production and consumption?

1) Is it to support the general population? Is it to feed and house and clothe and educate people so they can be “happy”?

2) Or is it to enrich the wealthy to feed their egos and their lust for power, regardless of the agonies inflicted on those who actually produce that wealth?

What is the goal here? Defining goals goes a long way towards determining outcomes, as well as how one goes about achieving said goals.

If the goal is (1) the means are failing miserably, “for the world’s more full of weeping than you can understand.” Assuming, of course, that one has any interest in understanding it. Even those who aren’t presently miserable aren’t very happy and aren’t very secure, or there wouldn’t be all the economic consternation related on this blog. Most people in the world live on a few dollars a day and their best happiness is producing more generations of people like themselves.

If the goal is (2), it can’t possibly by accomplished. Humans can use up the planet and never get anywhere near achieving the goal of making all the privileged as rich as they want to be. It is always a mistake to feed the rich. It only makes them hungrier.

Maybe the goal should be both (1) and (2), make the general population happy so they can feed the rich who are never going to be happy no matter how much you feed them. This is the purported goal of Project 2025. It’s an utterly phony approach to goal (2).

Perhaps a third way would be preferable. Once (3) has been defined, some path to get there will be needed. That I’d like to see. No, really. Maybe Something Else is possible. I doubt it, but I want to be proven wrong.

Maybe some balance between (1) and (2), which is what we have now, and it’s not working very well at all. See (1) and (2). Would 1.3 be better than 1.7, or vice versa?

Many, but not all, of the better philosophers of such things prescribe a limited version of (2), for various reasons. Depending on how it’s limited we can get some sort of democracy or something like an Anabaptist or Amish or Walden II-type communal living. We’ll want to be careful about that though, because we’d have no Lorenzo the Great or many of the great artistic achievements of civilization. Just don’t fall for Plato’s ‘Republic’ or his ‘Laws’, because he’s been shown to be a failure, even if he can be pretty interesting. It would help a lot to prefer Voltaire to de Maistre.

One should have fun with it, but it should be soon. The world is mostly run in a way that has increasingly leaned rather suicidally into (2). Between the overexploitation of planetary resources, the toxic externalities, and the fleeting nature of limited lifespans, one way or another time is running out, and fast, and it’s going to be ugly. See (2).

I have questions.

How many Canadian homes does Blackrock own, and how many is it keeping off the market to limit supply, jack up prices, and force people into rentals? Would Canadians really be better off as rent slaves than as mortgage slaves? Or isn’t that a consideration?

Would Blackrock be better off? See (2).

There is only thing that can bring the inflation back to prepandemic levels in Canada, US, UK, Europe, Australia, Japan and other developed countries: A solid declaration of the central banks stating that they will bring the money supply to prepandemic levels and keep at that levels for years. The central banks must declare that they will not stop QT until the money supply comes back to prepandemic levels (which was already higher than necessary), even if the rates may go down and they will never ever do QE in next 5 years. Otherwise, inflation expectations will never go down.

Housing didn’t get 50% expensive, money lost its value, because the supply is doubled. Now other goods and services are catching up. It is the basic math of economics. If you increase the supply of something, its value will decrease. Same for the money.

What I see around is that everybody is so confident with all kinds of hoarding, because they think holding debts and assets is much much much more profitable than holding money in the long term. Because with the inflation, debt and savings go down consistently.

“…because they think holding debts and assets is much much much more profitable than holding money in the long term.”

As long as inflation remains high, this will be true.

“because they think holding DEBTS and assets is much much much more profitable than holding money in the long term. Because with the inflation, DEBT and savings go down consistently.”

Huh? Your theory seems to contradict itself.

(word “Debt” capitalized by me for emphasis).

Things are quite nuts economically here in Canada. The CMHC has projected the country needs to build 5.8 million houses by 2030 in order to meet demand (population growth) and to supposedly make prices affordable; of course this isn’t practical or believable. Took 30 years to build 5.8 million and now we’re being told we have 7.5 years to meet that goal. A housing boom taking place while the country’s market is in a housing bubble and consumer debt is high. I think the government’s plan of growing our way out of debt is already unraveling. With an increasing number of people’s funding for retirement relying on real estate, heloc debt high, and Canada’s economy becoming ever more reliant on real estate, this could get interesting and ugly soon. The majority of mortgage terms are due in 2024 and 2025, we shall see. The new housing minister has publicly stated he wants to make housing prices affordable without anyone losing value (he actually said that).

40 year amortization term the new normal?

Agreed the wheels are coming off.

Want my citizenship confirmed ASAP so I have an option in the USA, but of course the Canadian government has a backlog on processing. I’m going to have to get my kids to move school, which I really didn’t want to do.

I made a huge mistake coming here. Never imagined they would do this.

Ps 5.8 mm homes by 2030? Immigration is running at 1mm a year, that is 7mm more people by 2030!

A government that believes it can simply grow its way to prosperity and also build and spend its way out of a housing bubble. Reading some of the quotes from the Montreal summit (yak fest for left leaning governments that Trudeau took part) best described as frustrating on my part and delusional on the politicians part. I’m thinking I need to get American citizenship as well.

Leave then ASAP. You don’t want to be here when little PP takes over from Trudeau

You think Trudeau will leave the financial cupboards empty? Well, the new housing minister did say, “we don’t need to spend more money, we just need to spend it faster”. Or you think PP will have some tough decisions to make? Huh, kind of like, you know, once upon a time there was another PM Trudeau who ran up massive debt. History repeating?

And don’t forget the new federal housing program isn’t building houses, just suggesting to provinces/cities to reduce licensing time. And the “affordable” prices would be near market rents, which are not doable for those that need the (subsidized) rents.

There is no building in smaller towns to re-energize them. A small town with a larger co-op would bring in various merchants and services, thereby rebuilding some of these almost forgotten bus stops (Canada doesn’t have national (or regional) bus service anymore).

“ 40 year amortization term the new normal”

I believe the last update was that 20-25% of mortgages had 50 year amortizations and rising due to negative mortgages.

Folks in the US will not understand this as they lock in 30 year mortgage rates.

I enjoy reading the Canadian stories as somehow I grew up thinking it was the friendly and safe compassionate capitalism country to the North where society and politics and corporations were one big happy family. Not sure where I got that from and not happy to see any countries dysfunction but good to get some facts around it and see same/same but different to the US is more accurate reductionist view.

Comment in regards to the $33 Trillion debt post.

Here is the 2030 US Federal debt projection from CBO:

In 2020 they projected 36 trillion

In 2021 they projected 39 trillion

In 2023 they projected 45 trillion

In three years the projection increased by 9 trillion. Covid was certainly a big factor. But the CBO is only projecting deficits of around $1.5 to $1.9 trillion per year through 2029 Who believes that? The CBO estimates are almost underestimated by 5% to 10% each year.

Things that are probably not factored into the budget

-Future SSN COLA increases

-Ukraine War

-Higher Interest rates

-Unaffordable housing. I think they Government will print more vouchers for the aging retiring boomers who do not own a home and benefited from housing appreciation/equity. I keep seeing more and more articles how some of these retirees are struggling.

Pundits say it will hit $50 trillion in 2020 once the latest ceiling is raised

“-Future SSN COLA increases”

Nah, you can take that off your list. SS revenues come from payrolls, which rise with employment and wage inflation. SS does not contribute to the deficit. It generated a huge surplus over the past 20 years, that is used, if needed, to cover the minuscule shortage over the past few years:

Sometimes for fun, I like to go to open houses. I’m a renter (I’ve always preferred actual investing vs. pretending that buying a big house I can barely afford is investing) but find lately that I would like to own a place so I can paint it yellow and red, and put garden gnomes everywhere. I’m joking a bit, but housing insecurity here in Canada is a real thing and ownership is feeling like a more comfortable option right now.

Anyways, it’s too early to pull the trigger, but talking to real estate agents is illuminating/frustrating – and, lately, open houses have been very empty, so they have lots of time to talk. One guy I talked to on the weekend said, “isn’t it ironic that rate increases and subsequent mortgage payment increases are causing the very thing the Bank of Canada is trying to stop?” After I stopped my palm from hitting my face over and over again, I had to concede that from a perspective of narrow self-interest, he had a point. Even so, I pointed out that this is the flip side of a method of CPI calculation that includes mortgage payments, meaning that all the times the BoC lowered rates in the past, it was effectively masking the inflationary effect of house prices going up. That meant he was essentially complaining that policy that once worked in his favour no longer is, but he didn’t really understand that. It was making him mad, though.

My point is that putting things in the CPI that are immediately affected by rate changes is actually pretty risky. It leads to immediate feedback loops (positive and negative). The pendulum is finally swinging the wrong way for people with big mortgages, but for years I felt like I was in crazy town when house prices here raged merrily into the stratosphere and the BoC didn’t think that was inflationary because they could keep rates low and payments wouldn’t change that much.

TEMPLE

It’s been *completely* obvious that CPI hides asset price increases when rates are lowered, for two decades. It’s also been completely obvious that when rates went back up we’d see this effect.

Now substitute *they* for whomever you like, it doesn’t matter. It’s deliberate.

They *know*. They *knew*.

They know how to get house prices down.

They *know* it’s killing productivity.

Anyone arguing about what to do or how is way behind the curve.

They know how to lower prices and they are doing the exact *opposite* at every single turn.

They excluded price rises from inflation before they let prices rip.

They changed lending from a multiple of primary income to a multiple of household income, which immediately forced women into work at zero benefit as their home now absorbed the extra income.

They did it in every single western nation at the same time, starting in 1997 (when Tony Blair got full backing for PM from every right wing newspaper in the UK as the Labour leader).

They put into every corner of economics that the main expense for every single family on planet earth (a home) was to have its full price excluded from CPI “because its an asset” (not if you don’t own one it ain’t).

It doesn’t matter who “they” are, but I can tell you this: “they” won.

I’m calling it: it’s over. We’re all serfs now. You might think your kids will be okay because you have a rental. They’ll wait and they’ll get that too.

Together we stand. Alone we fall.

I believe the CMHC started factoring in dual/household incomes for mortgage assessments in 1985 or 1986.

Holmes on Homes: “I like Homes”

Excess immigration is the exit strategy for this bubble. No affordable house pushes the prices up and every category as people are forced to go up a level. When the music stops, it will be the people who bought post-2020 that will be holding the bag.