Not encouraging: core PCE price index refuses to come down, has moved sideways since July last year.

By Wolf Richter for WOLF STREET.

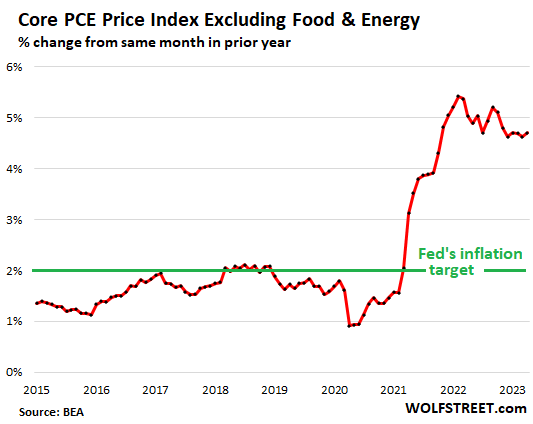

The inflation index favored by the Fed, the core PCE price index – which, by excluding the food and energy products, is a measure of underlying inflation – re-accelerated in April, as services inflation re-accelerated back into the red-hot zone, and as durable goods prices rose, after falling for months, driven by a jump in motor vehicles and parts.

Inflation is just churning from one product category to another, falling here but popping up again over there like the arcade game of Whack A Mole. And so the core PCE price index continues to be stuck near the 5% level, when the Fed’s target is 2%. And the Fed uses this core PCE index as yardstick.

On a year-over-year basis, the core PCE price index jumped by 4.7%, same as in July 2022, and up from a 4.6% increase in March, according to data from the Bureau of Economic Analysis today. It has now gone sideways at just under 5% for nearly a year, and is not coming down, but is only shifting from category to category.

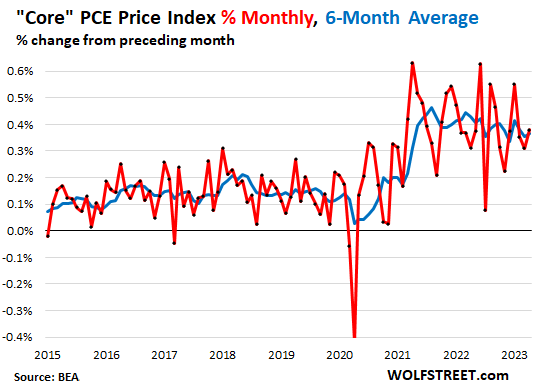

On a month-to-month basis, the core PCE price index has jumped up and down since 2021 around the 0.4% line (annualized just under 5%). In April, it rose 0.4%. This is just not encouraging:

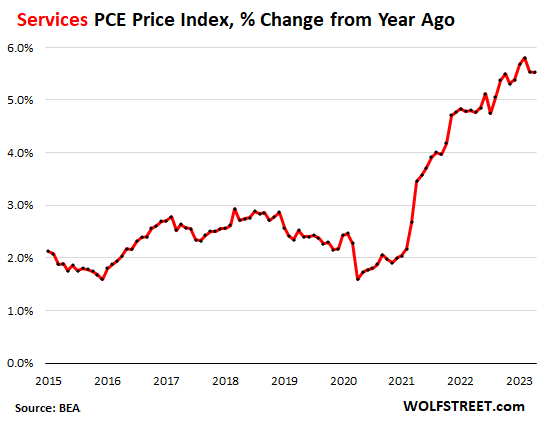

Inflation in services re-accelerated in April from March, driven by spikes insurance and financial services, and “other” services such as personal services, and big increases in healthcare and housing costs.

Inflation is particularly difficult to wring out of services, but services is where the majority of consumer spending ends up: healthcare, housing, utilities, education, travel, entertainment, restaurant meals, streaming, subscriptions, broadband, cellphone services, etc.

Year-over-year, the PCE price index for services jumped by 5.5% in April, same as in March. February, at 5.8%, had been the worst since 1984:

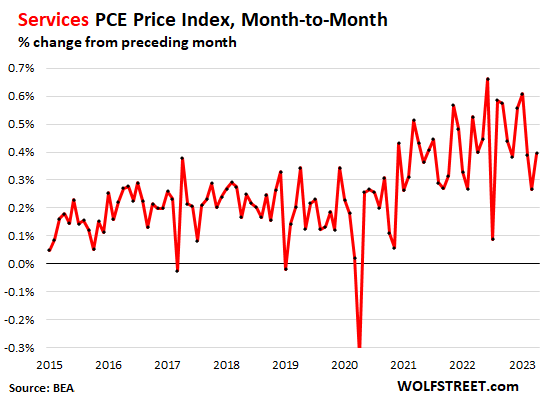

On a month-to-month basis, the PCE price index for services re-accelerated to an increase of 0.4% in April from March. Healthcare jumped by 0.5%, insurance and financial services spiked by 1.2%, other services, including personal services, spiked by 0.9%. But transportation services fell by 0.8%, and food services (such as restaurants) and accommodation were roughly flat, after spiking in March, inflation Whack A Mole.

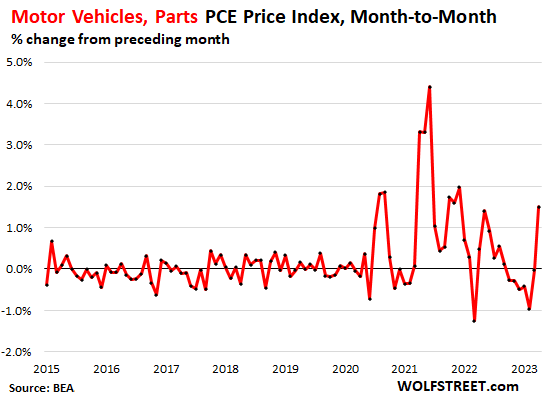

The PCE price index for durable goods – new and used vehicles, appliances, furniture, etc. – turned positive in April (+0.2%) from March, after being negative on a month-to-month basis for five of the past six months.

The turnaround was engineered by a month-to-month spike in motor vehicles. Six weeks ago, we predicted that this would be coming, based on underlying price data in the auto market that were already performing a U-Turn.

On a month-to-month basis, the index for motor vehicles spiked by 1.5%, after having been negative for the prior six months:

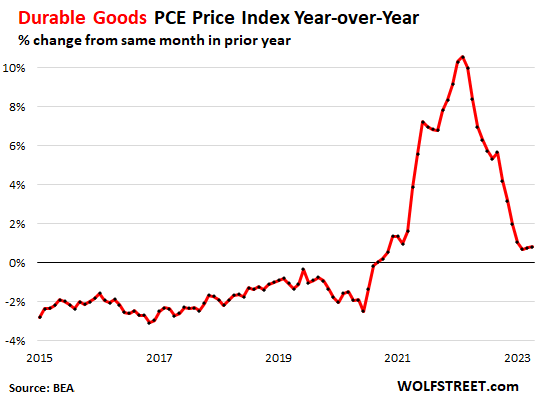

The PCE price index for durable goods, on a year-over-year basis, rose by 0.8% in April, same as in March.

In normal times, this index is negative, as efficiencies in manufacturing and transportation, forced by competition, drive down prices for the same product over time. In most cases, improvements to the product – compare a cellphone 20 years ago to a smartphone today – allow producers to charge the same or a higher price. The costs of these improvements are removed from the calculations of the index (hedonic quality adjustments).

Just by not being negative, as in normal times, the durable goods index contributes to the higher inflation readings:

The PCE price index for gasoline and other energy goods spiked by 2.4% in April from March, after having plunged in March (-4.6%). This stuff is volatile, which is why it’s removed from the “core” indices. Year-over-year the index was still down 13.5%.

The PCE price index for food was roughly unchanged in April compared to March, after having dipped by 0.2% in March from February, which pushed down the year-over-year increase to 6.9%, the least bad increase since January 2022.

The PCE price index for clothing and footwear rose by 0.4% for the month, and by 3.1% year-over-year.

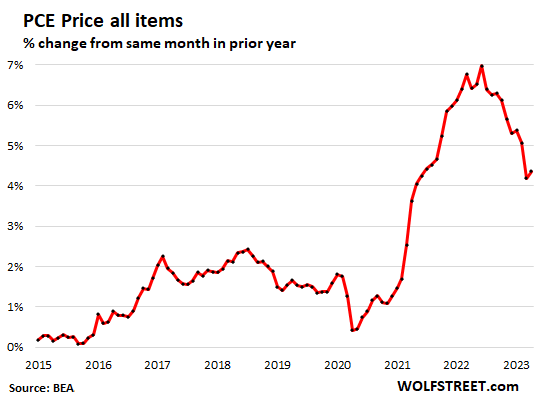

The overall PCE price index re-accelerated to an increase of 4.4% in April compared to a year ago, from an increase of 4.2% in March, pushed down by the year-over-year plunge in energy prices.

The fact that the overall PCE price index is lower than the core PCE price index is the result of energy prices that plunged in prior months, but that have now stopped plunging.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf is spot-on that the PCE doesn’t perform the medical service adjustment. The CPI would be even higher without the downward adjustment. If rent reaccelerates this month, we would have a big CPI and PCE number coming in June.

My healthcare costs are actually declining because this month I dropped my dental insurance. Just fighting inflation one less consumable at a time.

Well, you can still thank your lucky stars that at least you weren’t “forced” into some universal health care coverage like the rest of the “socialist” world has, right?

I mean, NOT having dental care, or NOT being able to afford basic health services, is your God-Given American Free Market Right!! lol. You’ve “earned” that freedom from dental tyranny, so cherish that free market every bit as much as it cherishes you… (end sarcasm)

On a side note, by comparison, here in Japan, all medical, with an annual total physical check (plus a 10 dollar lunch coupon usable at a dozen high quality nearby restaurants for afterwards to boot) and free dental care twice a year costs me a whopping…37 USD per month at this exchange rate…Yes, I am aware how woefully “unfree” I am compared to my previous life in the US…(sarcasm stuck in default mode, sorry)

I forgot to mention, last year I dropped my “free market” optical plan. Also to help beat the transitory inflation.

Entrenched inflation, is no other country on earth paying more then US T Bills ?

Higher for longer.

The pivot mongers are shocked, I tell you.

The stock market no longer cares about pivot. Instead, hedge funds are borrowing money at 5% (0% real rates) hand over fist & speculating on Big Tech / AI stocks for +25% returns overnight.

MW: ‘The economy is still too hot for the Fed’: Chance of June rate hike rises further above 50% after inflation data

For those who save a lot, increasing rates just means more money to spend. Inflation affects people differently, so if you drive a 12 year old Honda, own a house (paid off), or live in a rent controlled apartment, and are not in debt, inflation is less of an issue. Sure utilities hit everybody the same, as does insurance, food and energy increases, but these are actually not huge components of my budget. So I say to the Fed, keep raising rates. And don’t be too surprised if these increases are not knocking down inflation. Rate increases are a stimulus for many (most?) boomers and retirees.

As an aside, many are using Treasuries as their new savings accounts (buying directly or through money market funds). This is and will continue to be a huge problem for commercial banks. Vanguard and Schwab provide checks, allow direct deposit, and will make recurring payments. Schwab also provides a debit card, Vanguard does not.

But in order to get to the state of having a 12-year-old Honda and a paid off house, you have to put your money towards your mortgage and avoid spending it on a nice car or any of the other categories tracked by core PCE. If you pay off your mortgage early, that cash could very well go to the Fed who will shred it.

With 2.9 percent mortgages the homeowners would rather spend than save at that low rate. I have no Mtg but both kids have 2.9 percent rates and would rather travel and vacation and make other spends with their cash than reduce debt. They don’t mind their mtgs with jobs to pay for them . Savings rates high cheap mtgs and cheap car payments from previous times keeping the spending high from the employed.

Perhaps part of the Feds plan is to shrink the banking system to divert more domestic savings to buying Treasuries ? I agree with the first part of your comment completely. Thus far Ive been able to reduce expenses faster than price increases and also enjoy the income from 4% in online savings banks and Treasury Direct.

I have TBills maturing June 5 – wonder if I will get paid on time.

The politicians who threaten government default for attention and publicity are also invested in stocks/bonds/real estate/etc.

You will be paid on time because they want to be paid on time.

Could be the Fed wants only four or five very big banks, like in many countries. However, banks of all sizes can play important roles in the economy. But if Chase is going to pay .01% on savings accounts, and smart people can get 5.00% in Treasuries, then Chase is basically relying on stupid people for deposits or deals they made with customers for big loans.

Don’t worry about Treasuries. Even if there is a government default, the government will give priority to Treasuries, and everything else will have to wait if necessary. I am not sure of much in the financial world, but I am sure of that. Treasury just announced an auction of $169 billion to take place on May 30, to be issued on June 1 (a 13 week, 26 week, and 161 day). I’d jump on those, but my money is tied up in other Treasuries, and I like to hold to maturity.

I think inflation is a serious issue for those who saved for retirement and refuse to put their money into the stock market casino.

Serious enough that I am not fooled by the fact that thanks to normal interest rates I can earn some cash on my savings. The problem is that thinking that cash is “new extra money” is foolhardy since your nest egg just went down in value more than the interest earnings you made.

So spending based on the idea you have “mo money” is frankly daft.

As I mentioned, inflation affects people differently, depending on their lifestyle. If you don’t buy a lot of stuff all the time, like for example buy a new car every two years or buy the latest fashionable clothes or have a lot of debt, it will affect you less than a consumer junkie. I put most of my windfall interest income back into my savings (I buy more Treasuries).

It is daft to think that everyone’s extra income has to be divided by the inflation rate to get their real income. It works at the macro level, but not necessarily at the micro level.

You can hide under your rock all you want. Eventually, you will have to come out and pay the price increases we the consumers are seeing out here.

Almost everything has doubled in price. Dove soap repackaged their soap at Sam’s club and now the price per ounce is double.

Businesses are onto the consumers trying to stay out of the fray. But eventually your money will be diluted just like the struggling people’s.

All correct, and that’s a lot of us more frugal saver types have been pointing out with increasing impatience, the stupid spendthrift habits of too many Americans (a lot of them the speculators fueling these asset bubbles within the Everything Bubble) make things miserable for the rest of us too. Because in over-spending without restraint or common sense, and often going into debt to do it, they wind up building in expectations that lead businesses to hike prices across board, and making things miserable for the rest of us. We’ve been seeing a lot of what you’re seeing, and it’s especially disheartening when Costco and Sam’s Club start pushing the prices way up too.

At least Aldi and Lidl, and the Latino supermarkets in Texas still seem to keeping costs down, but there aren’t that many discounters holding out anymore and then prices shoot up everywhere. And yes we all do feel some inflation. It’s bad enough when inflation hits non-essential items and luxuries–that’s one place Americans in general can help by stop paying stupid prices (we’ve had stern lectures with some of our own family members lately wanting to buy overpriced iPhones and Teslas, which has saved us tens of thousands of otherwise wasted dollars in just the past 2 months). People need to learn to live within a budget there. But it’s even worse when it hits essentials, that’s a lot harder to dodge aside from shopping at the discounters and down-sizing our meals. And growing more and more in our own gardens.

Hi Wolfe,

I’m a lurker here and not always understanding what you report on but trying…and find your reports a nice balm from what the media spews out everyday.

In your opinion why is this happening? The corporations are having a filed day? What needs to happen to make mess stabilize so average people can live without going to the poor house? Respectfully, Newbie

Easy money from the Federal Reserve was restarted as policy by Alan Greenspan in 1987, in part to ease Reagan’s tripling of the national debt. Moneyprinting and artificially low rates enabled deficit spending, borrowing and the wealth effect. Consumers spend more when the nominal value of their assets increases, and when the cost of borrowing is minimal — real rates have often been negative!

The bubble began when Greenspan lowered reserve requirements by 40 percent. Assets were no longer “e-bound”.

A good 👍 point about Easy Al. From LTCM to the Dotcom bubble, he owns them all.

The fix is to keep rates high enough to reward savers and to rein in inflation. The reason they don’t like to do it is that expensive money 💰 slows the economy and causes asset prices to fall, thus unwinding the wealth effect. The current asset bubble is arguably the largest in history.

There are just too many people spending too much money. The Fed needs to collect dollars and shred them.

Inflation remains high and getting entrenched , consumer spending firm, stock market speculation returns.

How can the Fed pause?

The people on the FOMC are going to be wondering about that too.

How wide is the chasm between Point Wonder and Worry Knob, and can the Friday’s Off Motorcycle Club make that Evil jump now that they ride artificially intelligent electro moto scooters?

The FOMC is all about politics and optics. They would raise the rate in June but because it would look bad they will wait till July. Then they will be playing catch-up. Another rate increase will follow in August.

Mortgage rates just went to 7% around here, FOMO buyers are out there in droves.

Even the “Listing from hell” one block from me just closed and the buyers moved in.

Core PCE is high, so how would raising rates in June look bad?

Except… tightening credit has not really materialized as jawboned earlier. Since credit availability has barely budged vs the level of tightening expected, the original reason to pause has been taken off the table.

No. The FOMC (Federal Open Market Committee is all about making POLICY DECISIONS without regards to politics or so-called ‘optics’ and all decisions are made by consensus of the 12 member FOMC.

Wolf you have been on target and the FED won’t pause. Inflation will reaccelerate. My belief the FED wants housing to decline since that was the most damaging inflation to the lower and middle class. Housing though slow, is declining. As the fringe more forced RE sales occur (death, illness, divorce) comps will decline. But if they FED increases that would create more interest income to be spent on services? A difficult spot. Help me understand. Your thoughts?

They cannot pause.

And once the markets realize they are trapped, all hell will break loose.

How is the Federal Reserve in any way ‘trapped’ whatsoever?

Any attempt to fix the “growth” constraints caused by high interest rates will just cause inflation to move even higher.

Higher for Longer. H4L.

Starting to look like we’ll be seeing 8% FFR, unless demand (employment) cracks first.

Credit to those many who predicted for years that asset inflation would morph into price inflation. Lest we forget, Nvidia yesterday is a reminder that asset inflation is sticky, too.

Nvidia is a reminder of the grotesque amount of liquidity in the system.

We’re living in a different world now. It’ll take years(decades) for wages to catch up. I don’t think assets will come down. As a longtime homebuyer wannabe, this sucks.

I say just buy it. Because inflation is eating the future cash.

House prices are falling, and the decline will reaccelerate now that mortgage rates are rising again. Rates could go much higher. Remind yourself what has happened. We have just had the most insane monetary policy in US history. There is a very long way to fall.

Woud love to see some “cumulative” charts of these indexes included….

the gains stacked upon the gains.

Rate of change charts can hide the “sum effect” of ever smaller gains promoted by some as “progress or even “success”.

This was about what the Fed is looking at, not what you’re looking at or would “love” to look at. And the Fed doesn’t look at a cumulative chart, it’s useless and meaningless and silly for our purpose here, which is not a seminar about human suffering or whatever, but very specifically about where the Fed might be going next (that’s why “Fed” is the first word in the title).

But here you go:

Thanks for posting.

The Fed SHOULD be looking at this, IMO… Just as the chart of the decline in the purchasing power of the dollar since 2000 that you often post.

Lesser increases on top of this spike is not a victory, though they will claim it to be so.

“Human suffering” is “citizen suffering” is “holders of dollars” suffering.

The Fed understands that perfectly, a small but continuous and constant decrease in purchase power is actually a good thing in their eyes — it fights sticky prices (like wages.) *I* don’t agree with that, so don’t bother trying to convince me, but the Fed does.

As a result if they were to look at the chart you want them to look at, they would just shrug, get out the level and protractor, and figure out where the slope of the line is too steep for their liking and smile about the rest. They would tell you — correctly — it changes nothing about their world view, it just takes longer to interpret with a level and protractor then by glance looking at the % change chart.

In short, the Fed looking at your prefered chart would not change their world view at all; they know and like most of that, just not the parts of that line that are “too steep” or “too flat.”

It is tough to draw a green disinflation arrow on this chart.

longstreet,

Drive-by BS line.

it shows that you STILL don’t understand “disinflation.” It’s defined as a lower annual rate of inflation than before — in other words, the annual rate of inflation slows. This chart shows the INDEX, and not the annual rate of change of the index.

However, on this chart you can see the few months of “deflation” in 2008 when the annual rate of inflation was actually negative and the index dipped, as the price of oil collapsed.

Price stability at work, good job fed.

Yet the market is on a massive tear today with NVDA & debt ceiling.

Eventually this casino will end. If there’s one thing that is certain, a majority of people do not learn from history.

Next two years are going to be brutal, the Fed will have to get aggressive to get this down to their target of 2%. Some of the folks hear believe 4% is the new normal. We will find out soon…. Pedal to the medal on interest rates or we will be In 70s boogie time.

They need to drain liquidity at a faster rate…or at the very least at the rate they promised they would. This letting it roll off gradually isn’t finishing the job.

I agree with you that there is still vastly too much liquidity out there, and that it is going to take a long time to properly drain it at the current rate, but the issue is the system is super sensitive to the rate of change. Even if one needs to “go faster” to get back to normal in a reasonable amount of time, the “going faster” can, at some speed, start to do more damage then the “being too far away from normal.” Thus the conundrum, we have far to go, but can’t go too fast without making things worse.

Obviously then the questions become, “what is too fast” and the cost benefit analysis of how much faster we should or shouldn’t go from here. These are good questions that I can’t answer. The only obvious solutions to me are that they never should have gotten us this far from normal to begin with, and they should have used every moment following any of their distortions where the economy looked stable to do at least a little QT and maybe the ocassional rate hike to help make the safe baby steps back toward normallacy at all the numerous moments where it was possible. But now that we are here, we have to grind back to normalacy at a safe and stable rate even if it is painfully slow relative to what needs to be covered.

The QT pot is almost empty. The rate of QT at this point is irrelevant since inflation is already entrenched now. Since the QT pot was small and finite from the start, the rate of that QT mattered — a lot. The Fed opted for slow drain, when fast drain would have had an actual effect on markets. Within two years, the QT pot will be completely drained at the current rate of money destruction, and QE will have to be restarted. This QT episode was botched badly, and in the end will have essentially no worthwhile effect, in spite of the great potential it had.

@JeffD

“The QT pot is almost empty”

What? How so? Do you mean we can’t do more of it before something breaks. Because in terms of how much more is available to be done, we are talking trillions of $$$ — that is an awful lot more that could be done, and a long, long, long way to go.

“Since the QT pot was small and finite from the start”

Finite, sure, in the sense that trillions of dollars are technically not-infinite thus they must be finite, but it is not a small number, it is a very large number and it still is a very very large number.

“Within two years, the QT pot will be completely drained at the current rate of money destruction,”

uhhh, the fed is doing what, $95 billion a month, that is $1.14 trillion a year, so to go from over 8 trillion (where we are now) to about a 4-5 trillion new-baseline is like three to four more years from where we are, being about half a decade of total time since their start. That is not a small pot or “over shortly” or done “within two years.”

@Nat,

Wolf did an analysis on this a while ago. The $8 Trillion balance sheet at the Fed can’t even go down to $4 Trillion, much less to $0. And dumping that huge pile of MBS it owns is a huge problem you barely hear anyone in mainstream media cover adequately.

FED would never get aggressive. If you look at their body language and what they have done so far, they have been signaling the market that FED is there to protect the assets from falling.

If they have been really sincere, they would have raised by at at least 50 bps during last meeting but they raised by 25bps and sent signals that pause is coming, no matter what the inflation is.

I think WR is the only one, along with few readers think that inflation is still too high but rest of the world along with FED and market think other wise.

If the Fed is protecting assets, then that means they are not protecting the dollar. They can’t protect both and can only save one at the expense of the other. For now they are protecting the dollar via QT, o/n RRP, and higher EFFR. They would be dumb to destroy the dollar, but I think Congress will do that for them. Rates need to be 2% above CPI/PCE (either headline or core, whichever is higher). I still remember getting a 9 month 4.55% BoA CD around 2008-2009 with inflation below that rate, which isn’t that long ago. Negative real rates will continue to create problems…look at UK and Japan right now.

If the Fed has to choose between saving the currency and the bond market, they will choose the latter.

The Fed promoted malinvestment, “we forced the investor to take more risk” and now are forced to protect those so positioned, lest there be systemic risk. The 3 bank incidents and FTX were just a peek behind the curtain.

Plate spinning and juggling.

2% inflation is the Fed’s stated target. If 2% were their real target, they would be pulling money out of the system at a MUCH higher rate and they wouldn’t be thinking about even thinking about a pause. At the end of the day, we refuse to pay our government’s costs and debts with tax revenue at will, so we will pay via inflation against our will. The Fed isn’t staffed by dummies… There’s a 0% chance that they were caught off guard by hot inflation showing up after printing $5+ trillion in only a couple of years. My 4 year old already has a rough understanding of the effects of printing money. Inflation was the plan all along.

Let’s also not forget that our Fed was already found to be front running their own policy decisions with personal investments, and that’s only the couple of blatant cases who were dumb enough to get caught. Not to mention pretty much every member of congress and the banking class who owns the Fed all having a vested interest in keeping this bubble afloat since they participate in these “investments.”

The next two years will indeed be brutal because inflation will be brutal. The brutality will not have anything to do with aggressive Fed policy.

Tax revenues are at record high levels in the US, and what has increased by around 50% over the past 2 years is federal spending which is which there is a $2.2 trillion a year deficit problem and that is what needs to be urgently addressed.

Agreed. I neglected to say something like “a blend of tax revenue and spending cuts” as I have in other posts.

But at the end of the day, we are not bringing in enough tax money to cover government expenditures. Sure tax revenue is up nominally (a lot of that due to both asset, product, AND wage inflation), but spending has grown at a much faster pace. And because there is no political will or voter appetite for cuts to spending and/or tax increases, we will pay through inflation. Even worse, inflation is a regressive form of taxation… The poorer one is, the harder they get hit.

They are “addressing” it by raising spending to $2.6 Trillion/yr with the debt ceiling bill ($4 Trillion spent over 18 months, I saw somewhere).

Not Sure..

“2% inflation is the Fed’s stated target. If 2% were their real target, they would be pulling money out of the system at a MUCH higher rate and they wouldn’t be thinking about even thinking about a pause.”

Indeed. 3 years of 2%, without compounding, = 6%.

Last 3 years….circa 20%. To say that was a miss is an understatement.

The YOY metric falls short of what really transpired. Measuring from when the initial inflation problem developed (3 year ago) should be the starting point.

The issue is that if 4% inflation in the USA becomes “the new normal”–or even just 2 percent on top of the inflation that’s already kicked in to make groceries, rent and vehicles more and more unaffordable–then that also means the rapid end of the US dollar as a reserve currency, or at least as “the” reserve currency to the relative of exclusion of others (it’s of course common for multiple currencies to serve that role). Even as it is now like Bloomberg just reported, countries across much of Asia and other regions are now demanding payments in their own currencies and rejecting USD payments that used to be standard, for obvious reasons–a reserve currency isn’t worth the name if it doesn’t hold it’s value, that’s the whole point of what a reserve currency means. The only reason the bleeding hasn’t been worse, is that the Federal Reserve at least has signaled it’s intention to bring inflation well under control, and has moved in that direction with rate hikes and consistent (if inadequate) quantitative tightening. If the Fed then backs off and lets inflation run hot, not only will it spark massive social unrest among Americans who are already hard pressed to afford essentials (not a good thing with 400 million firearms circulating around), it’ll also be the last straw to convince the rest of the world that US financial managers aren’t really serious about actually preserving the value of their currency. Which by definition, makes it useless to hold in reserve, and they drop it even faster.

It’s a modern version of why nearby states and even Roman citizens themselves got fed up and stopped holding Roman dinars in reserve when the mint got ever more aggressive at debasing the coins with every new minting, it defeats the entire purpose of having a reserve for assets. Internationally speaking, this also just exports inflation and fuels even worse affordability for basics in many countries that are already teetering over the edge, in which case the leaders quite literally fear losing their heads if unrest spreads. So their ditching of the dollar is done for purely utilitarian, rational reasons–if JPow and the Fed don’t seem to be aggressive enough at preserving the US dollar’s value and throw in the towel on inflation, then the rest of the (and for that matter, more American citizens, just like in ancient Rome) will in turn also see less and less reason to store their own value in it. Once again it’s what Paul Volcker realized decades ago, and what Powell and the Fed really, really need to be urgently reading up on.

The fact of the matter is that there is no other currency than can even vaguely or remotely challenge the supremacy of the US Dollar either in terms of use in global transaction or as a stable reserve currency either now or in the foreseeable future.

For a beach dude, you make a lot of sense.

I’ve come to believe that “being” the reserve currency is a poisoned chalice. The reserve currency issuer ends up with trade deficits, higher debt, dependence on non-domestic manufacturers, and higher unemployment. Purchase of the dollar by non-US government forces UP the value of the dollar, making the US less competitive in global markets. Less competitive equals higher unemployment.

The fact that the US allows its currency to be used as a global reserve without preventing the gaming of the system that enables trade partners to maintain their surpluses hurts the vast majority of Americans. The trade-off of buying (heretofore) cheap stuff is having fewer and fewer well paying jobs. Reserve currency is hardly an exorbitant privilege and more of a burden.

For those of Wolf’s commentators old enough to remember the D-mark, one of the big pushes for the Euro was to REDUCE the value of the German currency to increase exports. The D-mark was increasing in value and hurt the export economy. The introduction of the Euro worked (for Germany).

No other country wants to take on the role of the reserve currency. Everyone wants to run neo-mercantilist trade policies at the expense of the US. There may be some bi-lateral trade deals, but China isn’t about to give up its export economy and ongoing increase in wealth to become the reserve currency (which is what would eventually happen).

A move away from the USD as global reserve currency would be short term pain / long term gain for the US generally (and the converse for the rest of the world). That’s why it’s not going to happen except at the margin.

Except there isn’t just one reserve currency, that myth is part of what’s been misinforming so much policy so far. As it is, currency reserves across the world are already diversified, and while the US dollar has been the most held of those currencies it’s been losing its position quite steadily over this inflationary period, not necessarily to just one currency but to a basket of them. And it isn’t just alternative reserve currencies that the USD is “competing” against here, it’s also local currencies (where it’s been rapidly losing ground, that’s the point of the Bloomberg article) and even commodities and other asset classes. Ultimately the USD is just one asset among many as a way to preserve value, and if the US dollar doesn’t do that any longer, then its position gets steadily eroded by a thousand cuts from other assets, whether other (foreign) reserve currencies or others. That’s why it’s basically irrelevant whether a single other currency does or doesn’t knock the dollar of its perch–its position is being eroded by a host of alternative options for countries to preserve their value better.

Now, like FastEddie pointed out below, losing more of its reserve currency status wouldn’t be a bad thing in itself for the USD, like he said it’s a poisoned chalice in many ways. The overvaluation of the dollar has made it harder to maintain many of our key industries which have been hollowed out and caused great damage to the American heartland, this is a big reason why the United States has been struggling with the opiate epidemic and a high suicide rate with such a low life expectancy. So some erosion there may be a good thing, but it depends a lot on how and why it happens. A controlled devaluation can absolutely be a good thing. This ironically is what China does with the renminbi–the true value of the yuan should be much higher but the Chinese policy has been to deliberately knock down that value to help exports. There are good reasons for the rest of the world to object to that, but for now, China’s used it to help boost up its own export industries while allowing a gradual increase (nothing like the Plaza Accords), accelerating once its industries and factories are fully in place to manufacture at low cost and there’s less reliance on currency devaluation. That would actually be a good thing for US industry, but a loss of currency status due to inflation and failed monetary policy is absolutely not good for the country holding that currency, because of all the damage both back home for financially stressed citizens and in trading abroad. It’s another of the many lessons Paul Volcker laid out in the textbooks we used in econ class, and the failure to learn these lessons is causing great damage to America today.

NVDA is not the market. Their bloated stock price and market cap are pulling indicies up. Look at the divergance between the S&P 500 and Russel 2000 lately.

The dirty little secret is that 4% core PCE inflation IS the new normal. NO one has the guts to admit it. In fact, the Fed is hoping that they can get somewhere near that rate in the next year. LOL

“You have to pass through 2% to get to 4%, so ‘Mission Accomplished!’ “, Commander Powell said while standing upon the deck of the aircraft carrier USS Nimble Nutz taking on Perrier water at an alarming rate.

Its not a secret. They are just intentionally not admitting it. They are stringing things along. Reminds me of that Sewol ferry incident in Korea or that cruise ship incident off Greece where the captain and crew told everyone its all fine and then bailed off first and a bunch of people including many kids died when the boats sunk…

I can’t understand this stock market. Has to be a pump and dump but it keeps climbing and climbing. The housing market is coming down but way too slowly. Where is the point this implodes?

What’s that saying, the market can remain irrational longer than you can stay solvent.

They are bleeding us dry on purpose… And people are gambling like the casino the market is, hoping they get out in time before a major crash (whose low point may still be higher than 2020 lows in dollar amounts due to inflation). Fattening up hansel and gretal and now grinding down to bones with intentional inflation.

The bagholders didn’t want to be bagholders so they are socializing the losses on to savers and the common man via inflation. Ugly…

Actually, very few stocks are up in the broad markets in the US, and only a very few tech stocks that have anything real or imaginary to do with so-called ‘AI’ are up which is what is driving the indices for the Dow, S&P 500, and particularly NASDAQ higher this year.

The trillions of dollars (debt) that was created is still sloshing around keeping everything afloat and seemingly everything is ok. Except we’ve had 3 of the 5 biggest bank failures in history the last couple of months. What could go wrong?

We just sold our house for almost $1.6M and will become renters for the time being. Bring on higher rates.

Congrats! Sold at the high

Renting = shorting the Realestate market

Smart people did this in 2015, 2018, and 2020. They’re still renting. Good luck!

lol at comparing the ZIRP and QE-fueled real estate bubble market of 2015, 2018 and 2020 with the mounting interest rates and QT in 2023. Even as inflation continues to soar higher and place greater pressure on the Fed. We haven’t had inflationary pressures like this in 4 decades, it’s nonsense to try to compare the current period with conditions from 5, 10 or 20 years ago when inflation was much lower.

The problem is….. when is the stock market going to realize this?

How many insane rallies have we had with with this new lately?

There’s still a lot of bubbling froth that doesn’t reflect the broader market, like SoCalBeachDude pointed out there’s a huge divergence between the S&P 500 and Russell 2000 and the huge majority of stocks are way down. The S&P, Dow and especially NASDAQ are still heavily driven by stupid hype, largely in AI, just like in early 2000, partly due to the way the idiot trading algorithms have been set up (another example of how “artificial intelligence” is actually making us dumber). The evidence of this is in the valuations, the P/E ratios are just at outrageous levels even in comparison to the tech bubble of the late 1990’s, for a broader range of stocks. And Nvidia’s report wasn’t even that good when you break down the numbers, it was a lot of hopium and wishful thinking without much real evidence of good sustainable business which in turn drove broader equities measures for index funds. The broader issue is that for now, the Fed rate is still below inflation and there’s too much liquidity due to the ridiculous loose monetary policy during the pandemic, so those funds are chasing returns that for now, with the current inflation, are still better in at least some equity markets (and crypto and NFT’s, ridiculously enough). This changes as interest rates continue to rise and QT accelerates, but this is another indictment of Fed policy as being too timid and slow. Volcker understood that you need to act aggressively and decisively to tame inflation, half-measures just aren’t very effective, and the US is paying ever harsher consequences for failing to get this inflation in check more effectively.

Went to the grocery store in Denver and contemplated heads of iceberg lettuce for $3 each.

Refused to buy on principle.

This is the new normal, I’m afraid.

That salad is not going to make itself.

I suspect some of the increases are the pandemic profit data manufacturers have. They realized

“wow, we made soooo much money when the supply chain was ‘stretched’. Who is to say consumers will not pay these prices?”

So they crank up the prices to pay their bloated board of directors salaries.

Yep, which is pure price gouging and nothing else.

Indeed. No better description, and Americans need to be a lot harsher at turning down these price increases. Shop at discount stores, look for cheaper non-brand alternatives, even grow more in our own gardens. Price-gouging like this needs to be punished, not enabled.

I just sent a picture of a head of butter lettuce to my husband at Harris teeter. $7.49 was on sale from $8.99. For a head of butter lettuce. Sh*t is absolutely out of control.

I asked for a balloon for my 1.5 year old and she gave her the balloon and handed me a price tag of $4.99 that I was supposed to scan on my way out. For a SINGLE balloon. $4.99!!! ONE BALLOON. Needless to say I didn’t pay for it.

I go to 3 grocery stores a week to shop the sales.

I can’t anymore.

Good for you. There are a lot of ways to fight this inflation, but one of the keys is for Americans to stop being so incredibly stupid and clueless to the point of going deep into debt to pay these inflated prices. We’ve traveled to other countries and notice consumers are a lot pickier about keeping in a budget, and not wasting money–a skill that too many Americans have somehow lost the ability to do.

It’s one thing when inflation hits in inelastic areas like healthcare (which should be a crime punishable by years in jail with a scary cell-mate, to force those costs on sick people). But a lot of the inflation is in discretionary goods where there’s no need to spend that much “for the brand” or for other dumb reasons where the cost way exceeds the value. We saved tens of thousands of dollars in our extended family recently by putting our feet down and having some stern lectures with the young-ins about wasting good money on overpriced iPhones and Teslas, among other things. There needs to be a lot more tough love like this around the country, to stop wasting money on food that gets thrown away or overpriced take-out, or on other junk that we just don’t need. Not a bad idea to encourage more backyard and community gardens too.

The ugly truth is that the Fed raising rates is just a tool to create a recession, and it will be the deflationary forces from a recession that finally break the back of the current inflation. I seriously doubt that the Fed and Biden Admin have the stones to do what needs to be done. Numerous analysts believe that the Fed remains accommodative until the Fed funds rate exceeds the rate of inflation. Speaking of which, the Fed’s numbers are suspect as Wolf has pointed out via the Fed’s trickery with health insurance and rents.

The health insurance adjustment is limited to CPI and does not affect the PCE price index here.

This may be considered conspiracy but this country has been on a financial engineering mode for a long time — Keep the asset prices, especially stock and real estate prices elevated, so that the foreigners will keep on depositing their earned and or ill gotten wealth here ($1T from China, $1T from Japan; all SA funds …..) while keeping the core inflation under control so that the peasants won’t complain or revolt. That FED financial engineering still seems to be active in the market as the market makes new high even when the interest rates are moving higher (none of the financial theory are working in practice).

Unfortunately now the inflation part has gotten out of control of FED hand – whether it is free money or the loss of lot of blue collar workers due to COIVD (and who knows how many undocumented workers really perished or ended with long COVID and left the country; I understand that the Pilipino community that has been legally supplying a bulk of our medical services staff took a big hit and that has started some question / soul search among them of their choice of work). With the Financial engineered economy, there is no way of Paul Volcker type inflation control, lest all will collapse. So, I guess FED can only keep praying and hoping the inflation will fade away by itself.

Isn’t the base effect supposed to be pulling down the inflation numbers at this point, or is that primarily for May and June? If inflation is increasing despite the base effect, yikes.

May and June, headline CPI, due to big oil price increases in Spring 2022.

We can also look at M/M increases, which don’t have base effects. A M/M gain of +0.165% is consistent with +2% annualized inflation. We’re not anything close to that in recent months.

Another great update on inflation, Wolf! Many people – not on this site – don’t understand the cumulative effect of inflation. A stable or slightly lower rate of inflation looks good to many, but it’s still increase on increase. 5% inflation on $100 is $5, but 5% on the new price of $105 is $5.25, etc., so the same rate of inflation produces a larger increase.

Wouldn’t that be considered compounding?

Powell will do nothing because it’s his idiotic fault, from his panic’d $15T M1 money supply print in April 2020 when covid arrived! He created this mess and it’s too embarrassing for him to eradicate it any way but too slowly!

There was no $15 Trillion increase in M1 in 2020.

Unpopular opinion: A missive sudden rate hike is needed to shock the markets. These small incremental’s are notworking as the economy and consumer spending just do it and inflation keeps going higher. If this continues any longer, lot of people will become poor by the time inflation comes down.

Concerned_guy,

I couldn’t agree with you more. The Fed is making the same mistake they did when they said inflation was transitory. It’s all too little, too late. Unfortunately, many people are having to suffer because of the Fed’s poor decisions.

The FED is not making any mistake neither are they stupid.

They are working as designed and serving their elite masters, friends and families and themselves.

We need to take away this notion that fed works for common people and are concerned about them.

Don’t go by their written mandate, go past it , and you’d find the truth.

Jon,

Yes, you’re probably right. There’s something about Powell that I don’t care for and what you state is most likely the reason. He and his buddies only care about keeping asset prices inflated and to heck with everyone else.

Even with incremental increases, at some point the markets will break. Look at 2000. The final increase above 6% FFR finally popped the tech bubble.

I don’t think a single sudden and large increase would even break this market or economy. There is so much money out there in rich folks land that this game will go on for a long time regardless of rates. We’re just going to see rich getting richer, and everyone else getting poorer. That’s my unpopular opinion.

Hey Wolf, how about showing the #’s with food & energy please

Nope. Distraction. I’m focused on core PCE and services PCE here because that’s what the Fed and Powell now constantly cite. All numbers they use are based on them. So here they are for the next meeting. That’s why “Fed” is the first word in the title.

Fed can’t really do much now other than to keep hiking rates, cause massive job losses to “fix” inflation. The drop in mortgage applications is no joke, it’s only a matter of 3-6 months before the stats catch with reality and stock market takes a massive hit. There is literally NO major lender left for MBS. Banks? nope. No one wants to be another SVB with long term loans. Fed? Nope, doing QT instead. Hedge Funds? Nope. So who’s gonna lend? that’s right interest rates have to go waaaaaay up before anyone lends money again and they will lend less, not more.

If only JPOW had some sense. Even after it became the clear the vaccines were working, he kept talking about transitionary inflation and worse, kept printing money for 6+ months…

On the fiscal side, the politicians are not living in reality. Both parties borrow and spend more than we can afford. Both parties cater to their bases who expect free money every election cycle … hence, we continue to borrow to infinity.

I suspect mortgage rates will march even higher to reflect the duration risk in an environment of high inflation/rising rates.

As always they will follow the 10 year US Treasury plus about 3% for standard mortgage rates.

Ditto the 10 year – still way too low imo.

No way I would purchase that kind of duration for less than 5% right now.

I sure hope so!

Regarding the equity market, it seems to me the debt ceiling fear effect is actually having the opposite reaction. Instead of falling on fears of a deal not being made in time spooking the markets lower, every time we hear words of optimism, they zoom higher. When there’s some pessimism, they go down just a bit…my guess is if they do reach a deal in time (no guarantee), it will be a big “Sell The News” event….after all, the focus will get back on the reality of the actual economy and the markets and the only change having a deal from the way it was before these fears kicked up, is the Fed Gov’t will have a bunch less money to spend then initially thought… As always, I could be wrong.. it could just go to the moon..

The Fed pretty much has no choice but to hike in June now, or they’ll face mounting credibility risks going forward. Skipping a meeting will only embolden speculators to take shots at them. That takes the top end on rates to 5.5%.

They’re going to have to hike again in July to 5.75% if the market doesn’t respect their June hike, and they’ll need to be able to credibly threaten to take rates to 6% regardless.

Savings rates revised down, inflation revised up, it’s a big party for those spending on credit, not so much for those working and saving. There’s simply no case for a pivot whatsoever, even if a couple more crappy banks kick the bucket.

Fed number #1 goal is price stability, consumers have been left stranded by QE bonfire and escapades. I’d like to 6 month treasury at 10%. Get all you can while can attitude pushing inflation at the core. Our federal government budget dictates the mind set of America. The rug that will never be pulled from under our feet. Step right up to the model credit union to the world, non stop printing press. Infrastructure crumbling, while all the future idea thinkers sit in a room, not wanting to face reality.

If price stability is the feds goal they should be eliminated. Does this chart of the dollars purchasing power look like price stability to you?

Will wait for Mr Wolfs analysis of the FEDs new dot plot. Pretty sure the higher for longer synario will continue to play out. That 70s 80s Disco Fever is getting louder…….. Looking forward to higher interest rates and they NEVER should have been soooooooo lowwwwwww……. Bring it FED.

I’m missing the chart where it shows the break-down by specific category.

MSFT closed @332.89 > BB #4 Oct 29/Nov 1 2021, 332/326.36.

MSFT daily log : between Apr 25/26 MSFT opened a huge gap and built a

Lazer tilting up : Apr 26 low to May 24 close // parallel from : Apr 28 high.

Today MSFT closed at the Lazer top on the resistance line.

Two things at play in the markets.

Without the ability to increase debt, the Treasury has been prevented from issuing in the rough ballpark of 600 billion in incremental bonds. This has starved the overall markets, which causes money to push into equities, seeking return on investment.

The removal of the overhanging risk of default means people are piling into risk equities, on the assumption that once debt ceiling is raised everything will be good.

The opposite is true. Once debt ceiling is cleared, the Treasury will be issuing on the order of 900 billion over the coming 3 months of incremental debt (that includes catch-up on balances and funding for the on-going monthly deficit). At the same time another 200 billion over 3 months of QT is likely.

So investors piling into equities at high prices now will be fighting against a Treasury that is selling bonds at an incredibly rapid pace.

I would also think, just a thought, that as the Treasury increases supply of bonds it will force interest rates higher and the relative attractiveness of equities will fall. Since short term rates are tied to Fed policies, it is the long-dated bonds that will see the biggest moves.

I havent done exact math, but I believe that the QE that Japan and China were continuing to do in late Q4 of 22 and Q1 and with the drawdown in Treasury balances that would normally fund deficit spending, we have experience only a trickle of balance sheet normalization in aggregate from central banks.

But the next 3 months will be far different. I dont have a crystal ball, but it seems like buyers expecting a big summer rally in stocks are up against a huge liquidity drain. If long term rates rise based on increased supply, high tech investors are also fighting a battle against a higher discount rate used to discount cash flows off in the distance.

I expect mid and long treasury rates to rise for the reason you have explained… a big increase in supply after the debt ceiling is raised. I’ve wondered if the recent increase in 10 year rates is a move by the market in anticipation of this effect. Some may contend that the recent growth is due to the

X date approaching, but it seems like that could only explain the behavior on the short end.

Here’s the Fed logic: 2% inflation equals price stability and so 4% inflation actually equals 2% inflation. The US is running at effective full employment now and that’s good for society and so a declared pause is coming in either June or July for an indeterminate time as the Fed hopes the huge Covid helicopter money drop finally starts to lose momentum over the next twelve months. One big geopolitical shock could kick the US into double digit inflation; the Fed is rolling the dice once again with an asymmetrical bet.

Pause will send inflation even higher. More rate hikes to come. Pivot mongers still mongering. 2024 is going to be chaotic.

No rates are not going higher. June pause, ai stock market fomo, ath by September, equities only place to be for next decade. Sorry bears!

You’re funny. Look at a three-year chart of the S&P 500. The S&P 500 has gone nowhere over the past year, it’s flat for the 12 months, despite massive ups and downs in between, and it’s down 13% from Jan 2022 and back where it had first been in May 2021.

The Nasdaq is down 20% from Nov 2021 and is back where it had first been in Nov 2020. Sorry.

People like you don’t come around on the many days when stocks tank. You just show up with your stuff when they jump. We know that program.

“We’ll all be buying houses in the metaverse, paid for with NFTs”

Come Dec, we will see if SPX is still above 3600

I on the other hand will be holding the Long Putsky….

I may be laid off by the time we get through this recession, but I’ll be much richer….Taking a sabbatical until the sun begins shining.

Roy you’re going to need a bigger boat to hold that BS.

“Shares of Dollar Tree plunged more than 16% in intraday trading Thursday after the company fell short of Wall Street’s earnings expectations for the most recent quarter and slashed its profit outlook for the full year.”

Even Dollar Tree customers are cutting back. Costco, Home Depot, and Low’s missed earnings too. Many stores in SF and elsewhere closing down due to rampant shoplifting (e.g., Walmart in Portland, OR).

Inflation is everywhere and the only pig that accepts the Fed’s lipstick is the stock market.

DM: Now the Treasury secretary says the US could run out of money by JUNE 5: Confusion as Janet Yellen sets new default ‘x-date’ – giving negotiators longer to find a way to avoid economic meltdown

Treasury Sec. Janet Yellen now says the federal government could run out of money to pay its bills by June 5, pushing back the date of potential default by four days.

The FED continues to shit the bed. In hindsight, their decision to step back the rate hikes from 75 basis points has proven to be another colossal policy error. Of course it was intentional, but an error in the context of their supposed mandate. They are intentionally entrenching inflation.

75 basis point rate hike would definitely surprise the market and show who is the boss. Or a sudden announcement of increasing QT to 200 billion per month could be even more devastating for the bloated equity market. But we all know they would not even contemplate it; their job is protect the wealthy at all costs. No one can hold them accountable because most ordinary people don’t even know what the Fed does. We have plenty of bread and circus to keep them obedient and entertained.

The US is at effective full employment; that half of the Fed’s mandate has been accomplished at the cost of between 4% to 5% PCE inflation which the Fed is accepting for now. The Fed is going to announce a pause either this coming meeting or next and hope for slowing inflation; Wall Street will see that as a green light for the next phase of the big party. If mortgage rates hit and persist at over 7% the Fed will start buying mortgage bonds again.

I really don’t think they’ll buy mbs again.

I agree. I think the fact that they continued printing $120 billion a month after January 2021 when it was clear that the main parts of the pandemic would be over shortly was intentional. They weren’t surprised by the inflation. They were just surprised that people called them out on it.

Mortgage rates exceeded 7%this week. The resilient real estate market remains a problem for the Fed. They won’t buy MBS anytime soon.