“We’re not pausing, that’s very clear,” Lagarde said at the press conference. “We know we have more ground to cover.”

By Wolf Richter for WOLF STREET.

“The inflation outlook continues to be too high for too long,” the ECB said in its announcement today. “We had long discussions about core inflation and underlying inflation,” ECB president Christine Lagarde said at the press conference, a reference to services inflation spiking to a record 5.2% in April, and “core” inflation (without energy) at 7.5%.

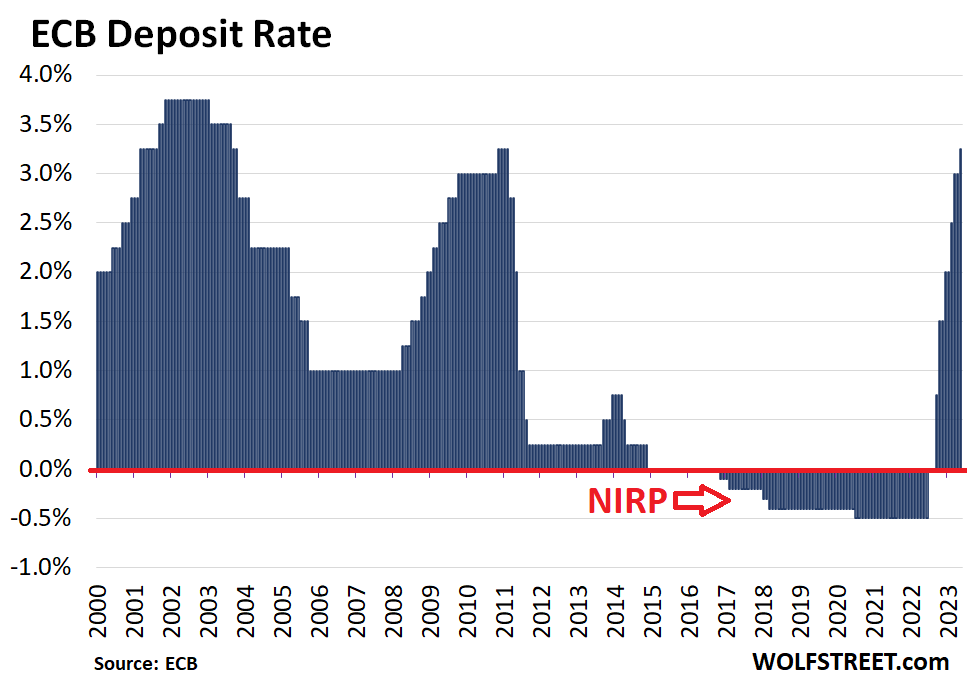

Higher rates: So the ECB hiked its policy rates by 25 basis points, despite stresses in the banking system. Since the rate-hike cycle started in July 2022, the ECB has hiked by 375 basis points, raising the deposit rate from -0.5% to +3.25%, the biggest rate-hike cycle in its history, to the highest rates since 2011, to fight the worst inflation in four decades. “We’re not pausing, that’s very clear,” Lagarde said. “We know we have more ground to cover,” she said.

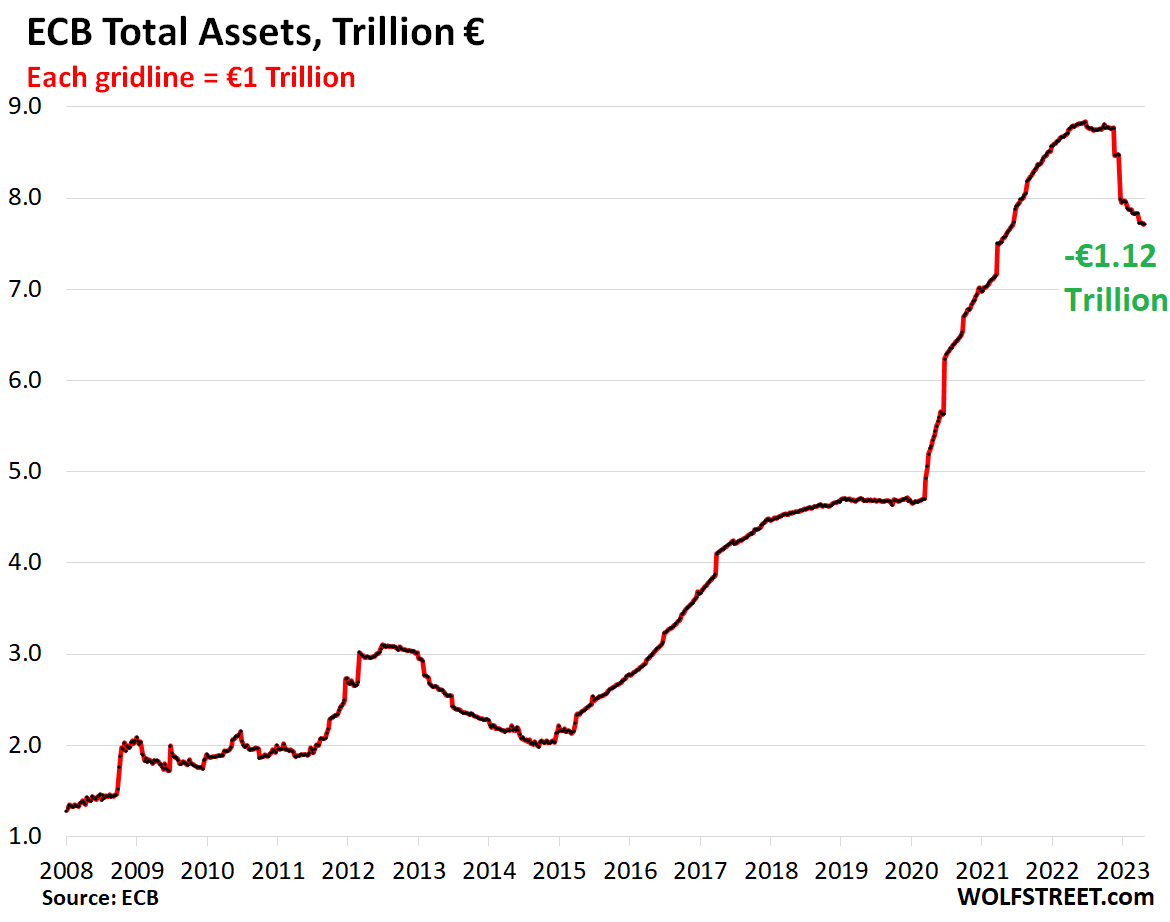

Faster QT: The ECB also announced that it would sharply accelerate its Quantitative Tightening (QT) program related to its bond holdings. It has already started to unwind its loans last year. The bond holdings started to decline this year. In total, the ECB’s balance sheet has dropped by €1.12 trillion since the peak in June last year.

Lagarde made numerous comments in the press conference to hammer home that there will be more rate hikes: “We’re continuing this hiking process,” she said. “We know we have more ground to cover,” and “this is a journey, and we have not arrived yet.”

She also said – reiterating what the monetary policy statement said – that corporate loan demand was “really, really down,” and that reports from companies indicate that rates are now restrictive.

She said that some governors had wanted a 50-basis point hike, and others a 25-basis point hike, but none wanted to keep rates unchanged.

QT to accelerate.

Back in the day when the ECB was still piling up assets and ballooning its balance sheet, it used two tools: Initially, it relied on giving out highly incentivized loans to banks (without collateral); then, as it saw that the Fed was buying piles of bonds, the ECB started to buy large amounts of bonds as well.

As part of the start of QT last fall, the ECB made the terms of the loans less attractive, and banks began repaying them in huge chunks. This year, it started unwinding some of its bond holdings, by letting maturing bonds roll off at a pace capped at €15 billion per month.

Today, the ECB announced that it would remove the €15 billion cap and will let the roll-off proceed at whatever rate the bonds mature each month.

The ECB holds €4.89 trillion in QE bonds (“securities held for monetary policy purposes”), as of the current balance sheet. These bond holdings fall into two categories: the Asset Purchase Programme (APP) and the Pandemic Emergency Purchase Programme (PEPP).

It’s the €3.24 trillion in APP holdings that are currently being reduced by QT, capped at a roll-off of €15 billion a month through June. Today the ECB announced that it would remove the cap in July, which will roughly double the pace of the roll-off of the APP bonds.

Total assets have plunged by €1.12 trillion from the peak last June. The large vertical spikes and plunges since 2020 are due to the loans (the Targeted Longer-Term Refinancing Operations or TLTRO III):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So just to be clear, this means the ECB will no longer buy any bonds (even to partially replace maturing bonds)? That’s astounding! The Fed is doing the same with MBS but not with treasuries.

With the government bid now withdrawn maybe we might start getting true price discovery. The ECB has been much more aggressive than the Fed this tightening cycle, probably because inflation is worse in Europe.

FWIW, this might have spillover effects in the dollar markets, if corporations start issuing dollar bonds due to the tightening of the euro bond markets. That is, some of the ECB’s tightening efforts might spillover into the US market, which, IMHO, would be a good thing because the Fed has been way too timid with its QT pace.

Yes, that €3.2 trillion pile in APP bonds will run off as it matures without replacement.

The Bank of Canada is doing the same thing with its GoC bonds.

The BOE is doing it too, plus they’re actually selling bonds outright. They have HUGE LONG maturities that won’t mature for many decades, some in 70 years or whatever, so selling might be necessary.

Wolf I have new android 12 tablet that constantly crashes on this site but works flawlessly everywhere else. Not sure if others are having issues.

“Today the ECB announced that it will cut the cap in July, which will roughly double the rate of tapering of APP bonds.”

Wolf, I don’t understand, why are you saying it will ”double” the rate of decline in APP bonds?

After reducing all restrictions on APP, there should be no cap. That is, until now the ceiling was 15 billion euro per month and from July 1st there should not be any ceiling and everything on maturity should evaporate…..

There is no cap or “ceiling.” Bonds mature on maturity dates. So I looked at the maturity schedule from July 2023 for the 10 months through April 2024, and I added up all the maturities — they fluctuate between €9 billion (in December, holidays) and €53 billion, totaling €273 billion, which averages out about €27 billion per month. So in October 2023, the runoff will be €52 billion, in December 2023, the runoff will be €9 billion, etc. That’s the natural runoff of the APP portfolio. To reduce it more quickly, they’d have to sell some bonds.

Thanks Wolf

Now it’s clear.

“So just to be clear, this means the ECB will no longer buy any bonds (even to partially replace maturing bonds)? That’s astounding! The Fed is doing the same with MBS but not with treasuries.”

The fed statement is that they reinvest into mbs the principal payments exceeding 35b per month, as well as rolling over treasuries after 60b. Whether mbs principal payments reach 35b is a different story.

They also do small operations, ~100m or so at a time, of mbs.

the “small value operations” are designed to keep testing the system. They’re for buys AND sells at various times. Just to practice! So they know how to sell MBS, they’re practicing it with small-value operations.

I’m going to go buy a Walker and some tennis balls so I can be Comfy when this QT is done. Haha

Did you trip over your tennis balls, lose grip on your walker, and fall on your head? €1.12 trillion QT in eight months!!!

Look at the chart.

It still begs the question. Why is the FED Slow Walking?

Not QE, not QT, QS. Stalled.

kam:

Banks are failing, housing prices dropping. What more do you want from QT?

I don’t understand the math. QT at 15 billion Euros a month equals $120 billion over eight months. But 1.12 TRILLION Euros in QT over eight months equals 140 billion Euros a month.

READ THE ARTICLE. There are loans and there are bonds. They’re running off separately.

The grave is comfy.

Wolf, you mention banking turmoil in your headline, but is the risk for Eurozone banks as high as it is for mid-sized banks in the US? I’m sure there are some that mismatched the duration of their assets to their liabilities, same as in the US, not to mention a few long-time zombies like Deutsche Bank. But are there the same widespread dangers due to things like thresholds for stress tests and such that the US has? I’m no expert, but I got the sense that Eurozone (especially Germany) has a high number of small to medium size banks, rather than a couple of TBTF giants, so the health of mid-sized banks is pretty critical for the Eurozone.

Since Credit Suisse went down the tube, there has been talk of contagion to Eurozone banks. And there are stresses in the banking system that the ECB is “monitoring.” At the prior meeting, they said that they will address those issues with liquidity measures, if needed, but keep rate hikes and QT on track.

Rates have not risen as much in Europe as in the US — the ECB is well behind the Fed, so banking stress in the Eurozone may be also behind the stress in the US.

European banks are more poorly managed than US banks and hold long duration debt instruments with lower rates than US banks due to ZIRP. It is unlikely that they are properly hedged against the interest rate risk they currently face. The absence of a banking crisis so far is due to the belief that the ECB will, like the Fed and FDIC, do whatever it takes to avoid bank runs. If that belief turns out to be mistaken the EU will go in the tank very quickly once the duration rot on bank balance sheets becomes newsworthy.

So, is it my imagination, or are the major central banks in lockstep with each other? I don’t remember that always being the case.

Cordianared chaos

Since their officials all go to the same schools and drink the same Kool-Aid, they tend to act in the same ways. I did some research years ago and looked at how Strong, Norman, and Schacht were actively colluding in 29-30 to try and manage the global crash (which actually started in Austria, not Wall Street, but that’s a long story). Today, I think it is a confluence of background and ideology more than active collusion that gets the central banks to act in tandem.

No. Pigs will fly through the skies of major cities before the Fed removes all caps on its QT, as the ECB has just done.

I don’t see any information here that is going to stop me from getting short up to my eyeballs.

If apple disappoints tonight that may be a good trade.

It’ll be “better than expected” or “not as bad as feared.” It always is.

Beat expectations. Mildly up after hours.

Way to go, ECB. I am very, very sad I didn’t go long Euros a few months ago when the USD rate was ~1:1. That was a no-brainer trade.

I’m very sad I didn’t hold onto more stocks than I did, during the GFC plunge. The day after I capitulated, Bernanke pulled a major move that buoyed stocks, versus my new cash stash. Central bankers pull a switch, and down the chute you go. All I had to show for it was some nifty tax losses for a long time. (Not even a souvenir t-shirt.) It was an expensive learning experience.

Not at all sad at anything as of now as I know from the dust I came and to the dust I go back :-)

May we all find a beautiful day!

The long term M2 chart going back to 1960 shows there has been only one observable drop in M2: July 2022 to the present.

1960 up to Jan 2020…..slow steady rise in M2 with only minor ripples.

Jan. 2020: M2 = 15.0T an unprecedented Canaveral style blast off

July 2022: M2 = 21.7T apogee of the M2 rocket’s vertical ascent

Mar 2023: M2 = 20.8T rocket trajectory definitely heading down

So far, the M2 drop has been only 4%, but picking up steam. Look out below………

M2 is an arbitrary goofy measure: it excludes deposits >$100K for some arcane purpose. It simply refuses to “look” for “all the money”.

Just a sweet spot false dawn where the ECB looks responsible but the pain hasn’t yet arrived.

Standby for chaos in EU, when real price discovery shows its face.

I’ve got a strong feeling that in the future when this period of time is studied the conclusion will be the Fed and the ECB simply made the critical error of not raising rates much higher and quicker. It’s gotta be pretty obvious by now that .25 rate hikes are accomplishing very little to reduce inflation.

As someone said the choices are your money buys less stuff or you have less money to buy stuff with.

My guess is that eurozone banks used TLTRO to borrow euros at -0.30%p.a. and invested the funds in US fixed income market. That worked well until ECB started hiking and then EZ banks sold US assets, bought euros and repaid TLTRO loans. That maybe the reason why Euro got stronger against dollar.

In theory, central banks should be acting in their respective economies’ best interests. Will higher rates, help the US economy re-start manufacturing?

The ostensible answer: (1) by default, higher rates make life harder for global south emerging market exporters, so the slack has to be picked up domestically….

(2) local labor costs are much much higher than China…so higher rates have to concord with that supply side price inflation .

(3) companies are getting “fiscal tax breaks”. The LOL-named “Inflation Reduction Act” is all about government subsidies!

The fact that other central banks are copying the reserve currency is not surprising and carries no information. But the problem with the EU imitating bullet point (3) above is that the it’s very hard to do national subsidies within the EU framework. France, for eg, won’t like Germany giving German industry fiscal subsidies etc etc.