Lot of demand and supply gone in equal, with no net impact on inventory, but huge impact on sales, commissions, profits, and jobs.

By Wolf Richter for WOLF STREET.

The artificially repressed mortgage rates from March 2020 through March 2022 caused a huge number of homeowners to refinance, including to cash-out refinance, into 30-year fixed-rate mortgages with rates of around 3%, many of them below 3%.

If these homeowners want to sell their home and buy a bigger home or a smaller home, or a home in a different location, or whatever, they would have to change from a 3% mortgage to a 6.5% mortgage, and that’s a no-go zone. So they’re not selling, and they’re not buying. They’ve left the market.

This is bad for home sales, which have plunged, and for real-estate brokers that make money off each transaction, and for mortgage bankers that make money off mortgage originations, and if there are no transactions, they make no money and they have to find another job.

But the 3% mortgage jail has zero net impact on inventory.

When a homeowner sells the house they live in, to buy something else to live in, it has zero impact on inventories nationwide overall because a homeowner who sells their home and buys another home, adds one unit to inventory and subtracts one unit from inventory (+1 – 1 = 0).

All they do is churn the market, which is good for brokers and bankers. But they do not add inventory overall.

So if these homeowners cannot move because they cannot switch from a 3% mortgage to a 6.5% mortgage, it pushes down demand (yes ✔) and it pushes down inventory by the same amount (yes ✔), and the end result is a smaller market in terms of, both, demand and supply.

What actually adds to inventory of homes for sale?

In all these situations below, a home gets put on the market, and no home gets taken off the market, with the result that inventory actually rises. You can think of maybe a few other situations, but these are the big ones:

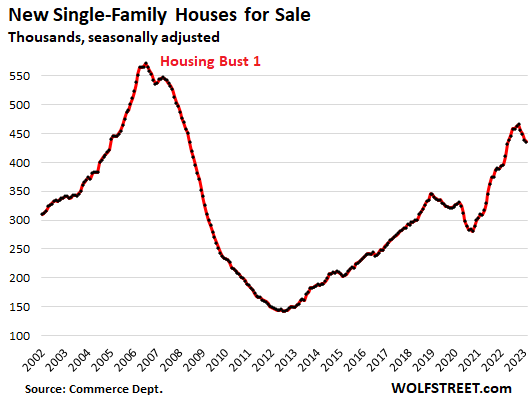

1. New construction. Lots of new homes are being built and inventories of new houses for sale at all stages of construction have piled up massively:

2. Homeowner dies or moves into care facility, and the home gets put on the market. Lot of that going around now.

3. Vacant homes being put on the market. We walked through the Census Bureau data a little while ago, taking the math from the 11 million homes that are vacant year-round down to the 3.5 million homes that could be on the market (rental or sale) but are held off the market for a variety of reasons. If just 20% of these 3.5 million units that are held off the market show up on the for-sale market, it would increase inventory by 75%.

4. Homeowner moves into a rental and puts home on the market. Some of that going around now, as homeowners try to lock in the high prices and to outwait this. I know a few myself, including a Realtor who totally nailed the peak in her local market last summer when she sold and moved into a nice rental house.

5. Homeowner moves in with friends or relatives or combines households. This could be a variety of arrangements, such as caregivers moving in with parents, or two single homeowners moving in together and making do with one home.

6. Homeowner moves to another country for work or to retire, and the home gets put on the market.

With the 3%-ers taken out as Buyers and Sellers, the total market is a lot smaller now, and will be for years to come.

Homeowners selling a home they live in to buy another home to move into adds zero to inventory in the end (+1 – 1 = 0) though that’s what brokers and bankers live off. That’s why the National Association of Realtors and the media, and just about everyone else, are constantly blaming low inventory on homeowners being locked into their homes with a 3% mortgage, when in fact, they’re only to blame for low sales – and plunging commissions and big job cuts – but with zero impact on inventories.

It means that there are a lot fewer buyers, which is what we’ve been seeing, and that there are a lot fewer sellers, which is what we’ve been seeing. In other words, a huge group of BUYERS and SELLERS were simultaneously and in equal numbers taken off the market by 3% mortgage rates, and they’re gone for years to come.

That demand is gone; and that supply is gone, in equal measure, with no impact on the inventory, but with a huge impact for sales, commissions, profits, and jobs.

The market is more in balance than it seems: hence dropping prices.

So now, it’s the remaining buyers and sellers that make the market, and they’re a much smaller group, making for a much smaller market.

The price drops are showing that within this much smaller market, there is more balance, and that buyers emerge when prices are low enough. And when these buyers have bought, prices drop further to pull in the next wave of buyers, which is just a normal market – but on a much smaller scale. And what is gone is the massive churn of homeowners selling and buying in order to move.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This inane buying and selling of houses is a rather inane notion, and it is hard to understand why people don’t just buy one house and live in it forever which keeps property taxes very low here in California with the basis being the original purchase price increase by only 1% of the tax assessment in any year. My parents purchased the lovely home I live in back in Summer of ’58 and I’m happily living in it today in Spring of ’23.

You’d be singing a much different tune if you had to buy that same house and it wasn’t “given” to you.

You are making an assumption that may not be correct. I know many that live in their parent’s home and none were “given” the home. Because of the costs of long-term care, the homes were indebted, and with multiple siblings, they had to actually buy the home of their youth from the trust in order to keep it in the family. While many do inherit homes, not all.

If he purchased, the home, wouldn’t the taxes have reset?

So the parents put the home in a trust that was not controlled by the children? Sounds like the parent didn’t have much faith in ya kiddo. What a shame lol

You are of course correct. Those given homes (or buying at “gift” prices) are in a different position than those without.

I know hard money lender that loves the 3% crowd

they’re making deals to WRAP the current loan and pay owner the equity portion

in that way they keep cheap financing in place

Moving around used to be more common in America, and was a great way for people to pursue opportunity and prosperity that they otherwise wouldn’t have found in the town they were born in.

It sounds like you’ve been very fortunate to receive a house in a beautiful state. Congratulations!

New construction is a driver of real economic activity as it requires a lot of labor and materials to build a house. Selling an existing home doesn’t add much to real economy, but there needs to be a market for existing homes.

SoCalBeachDude – where did you live before now?

Never bought a house to live in on your own before you got given/inherited your parents’ house?

That aside, peoples’ circumstances change; better salary, more space needed, etc.

You can rarely buy the house of your dreams early on, but you can change up.

Considering the fact that I lived and worked through the period of corporate downsizing and consolidation where the number of offices dropped from 18 regional offices to 1 over the course of 15 years. Hard to stay in the same home when the job relocates. Plus the office and job losses were in locations such as Tulsa Ok Denver CO Midland Tx Houston Tx. I had the unfortunate experience of loosing 50 percent of my house value (including Mtg ) . Housing does not always go up. Ask the folks living in Detroit and the NE steel towns or the coal towns .

This has to be a troll.

Nah, he’s just trying to get under people’s fingernails.

Mortgage rates were above 7% only for a few days at a time so that average weekly 30-year mortgage indices were above 7% only in two separate weeks (once in Oct and once in Nov). In early February, they dipped to 6.0%. The last weekly average was 6.3%. Yesterday’s daily average was already above 6.6%. Mortgage rates have been above 6% since September, and they’re still in the same range around the 6.6% mortgage. For homebuyers, nothing has changed.

Could the fall in housing offset the inflation of other goods and services? they’re saying ~6% inflation yoy, but most people are looking at 11%+

Around here they build new homes on the same lot as the old homes. No new lots are available. They tear down the old homes. If you don’t comply a junkyard dog Realtor knocks on your door and tells you that you need to move to a retirement community. A Builder’s shill sends you a flyer in the mail telling you that your home is functionally obsolete, and that it cannot be improved or is not cost effective. They site a young family that would like to move to your neighborhood to take advantage of the good schools, which you are not using anymore. They say that it is your duty to get out of the neighborhood. In other words, you are cruel to stay in the house you’ve lived in most of your life.

My small town (8000 residents) has set boundries; there is no more space. So they changed the zoning, and all the houses on 1-2 acre lots got bought up, and now have 5-10 houses on them. But the infrastructure was designed for the lower population density, and that’s causing some real issues since there’s only 3 ways into town, and it’s a pretty big detour if something closes one of them.

There is something called a “Pump & dump”

And it’s everywhere.

All throughout 2020 to 2022 I saw lemmings jumping enthusiastically over the precipice.

Economics is a lot of fun if you enjoy train wrecks….and I like train wrecks.

everyone leaves this planet the same way u will have a less robust life living in one place just because of money everyone doesn’t have the same priorities

Not sure I would describe rapidly falling house prices as “normal” multiple times

Not “multiple times” but “one time.”

But yes, prices going down after going up is part of a normal market.

Agree and since we had one of the most abnormal and fast run up ever in modern history, let’s hope the way down is just as abnormal and violent, that would only be fair and normal part of the cycle.

Because if price only back down to end of 2019 level, then for many already bubblicious markets it’s really nothing to write home about and historically we would still be in bubble definition like in West Coast as you have shown and wrote about many times before..

If the market in Phoenix was to drop to “end of 2019” levels that would mean a 40-50% drop from today’s prices.

What’s you point again ?

As with stocks, plenty of people are still anchored to super-bubble prices mentally. It is, IMO, a spurious point of reference, built on an unsustainable over-print of money and credit. This is part of why inflation persists. Prices and profits are still, and should be, adjusting. At least we are not heading so headlong into bubble-dynamics for a change. And, a lot of folks should, accordingly, feel less wealthy.

When was the increase bigger in a similar time period in the past?

This isn’t “one of” the biggest housing bubbles in US history, it’s THE biggest one and the Case Schiller charts profiled here prove it.

Phleep,

“As with stocks, plenty of people are still anchored to super-bubble prices mentally. It is, IMO, a spurious point of reference, built on an unsustainable over-print of money and credit.”

FWIW, I agree completely and have seen this mentality first hand.

But what’s so odd about that is the fed was making the cash to buy homes in QT right?

So you went and got a mortgage, say right at the ceiling of your salary. Some would say “that’s too much to take on” but you better bet people were taking them on.

They get their dream house (which was 50% less not 2 years before), the fed gets their jumbo loan for mortgage backed securities.

But now wait, these buyers are now not happy and want to sell.

Is it Tough snikees? Or Sell for a loss?

And if they sell for a loss, who gained from their whole endeavor? Who lost?

Did the fed accomplish anything? or is this housing market a negative byproduct of QE?

Much agree, phleep. I always want to yell at whiners for cherry-picking high water marks as their definitive point of reference. Houses and stocks are still at pretty inflated prices using more normal times as a baseline.

Read the G*d D**n F***ing Article (RTGDFA)

Mr. Wolf, there is a Mister Lawrence Yun on line two calling to say you are, and I quote, “Wrongedy, wrong, wrong! House prices only go up. Buy now or die of cancer.” Shall I put him through?

Just tell Lawrence luny to use his other handle Kunal to post his thoughts on this comment section…telephone call is soooo 1990s..

“Shall I put him through?”

Yep

Lawrence Yun is right for a change. Houses are not going down here anytime soon. They have stabilized. Even Refi’s are starting to pick up. People need a place to live and will pay whatever the traffic will bear. Those waiting for a big decline will be waiting forever. Even the “Listing From Hell” a block from me just went “UNDER CONTRACT” after a small price reduction.

The Realtors have a tough decision to make. Do they pretend to become RE investors and defend their house Zestimates, or do they become honest with their commissions business and force sellers to lower expectations.

It’s time to let go. Chasing high commissions by spreading misinformation will result is much fewer sales resulting in much lower commissions. It’s a bad time to find a side job in middle of layoffs to make for commissions loss.

I encountered a new realtor who sold a home to a neighbor just before pandemic, and was so influenced by the price jump, that when the neighbor hired her to resell the house, she ended up proudly buying it herself at pandemic peak price. In Seattle outskirts that house is now 20% down. Greed, inexperience and jealousy is a bad combination.

Most of the realtors when they pump home prices they do it genuinely .

Most realtors don’t really have the gray matter to look at the bigger picture like the readers of this blog

A realtor I know is very kind and genuine but she is always pumping real estate.

Don’t blame her as this is what she genuinely believes in

Also her livelihood depends on not understanding what’s really happening.

I see the same here.

Many people here are real estate pampers as they are some how invested in rising home prices

Disagree on the comments regarding realtors. A realtor is here to make a transaction. 2% of 600k or 500k. Who cares. But no transaction and no commission. That’s the issue. “Pumping real estate”. Have you ever met someone who said: I don’t want my own house? The idea of renting and paying off someone’s mortgage doesn’t really make senses intrinsically RE doesn’t have to be pumped up. The market makes the price not comments on the internet or lines by realtors.

Realtors are salespeople, not financial analysts or students of market history. They may understand basic economics, but they are still in the sales profession.

Most people are also trend followers going allowing with crowd psychology. It happens with Wall St (even when they aren’t engaging in self-promotion), economists and the ultimate trend follower, government.

Realist,

“Have you ever met someone who said: I don’t want my own house?”

I certainly have, several of them. It’s not most people I know, but I think most people have met someone whose had buyer’s remorse after a home purchase.

Re: Realtors as real estate “pimpers”:

What would one expect them to do? Have any of you ever purchased an item or service when the salesperson told you it would drop in value/depreciate and the service wasn’t worth the powder that it would take to blow it up?

Of course not.

It’s no different than when you present yourself to a prospective employer or client. Are you going to tell them you’re mentally unstable, or about to go bankrupt, or that the last major project you lead had huge cost overruns and ended up being a dismal failure?

Of course not.

Yet you expect behavior contrary to yours from someone else under similar circumstances.

Buying a home is, and always was, an emotional purchase. When you dissect the economic details as some here do, one could come to the conclusion that it just doesn’t pencil. (Of course, buying food doesn’t pencil either as it just turns to crap in short order.) However, people do it every day. In some cases, it does pencil – but that’s normally for people who deal with life in longer horizons and assign a value to housing security for them and their family. Yes, there comes a day when it has to be sold, regardless of the economic conditions. But the same applies to stocks, precious metals, luxury watches, jewelry, and about every other thing you can think of. Have any of you ever taken the rock you bought your wife and tried to sell it back to the jeweler that sold it to you? Talk about getting your a$$ handed to you….

That’s a good point. I’m not sure about other markets but the few RE agents I’ve talked to and dealt with in either Toronto or Vancouver Canada have all been investing in RE, one agent told me him and his wife owned close to 20 properties, though I can’t verify that. With the duration of the bubble and the rate of appreciation I think a lot of them got seduced into speculating, you can only watch your colleagues score so many times before you start to feel like you’re missing out. I wonder how they feel about the current market, probably hoping number of listings stay low through the spring and summer, I’m assuming a big drop in prices over multiple properties would eclipse any income from commissions.

In a normal market, putting your money in something you know best makes sense, as long as you are not overly concentrated and have adequate diversification.

The problem is that this isn’t a normal market and hasn’t been for a long time.

I doubt they own those 20 properties and have them sitting empty. My mother was a realtor for 25 years before retiring after a stroke. At one point my parents owned nine properties… and traded down to four BETTER properties after Hurricane Katrina which they still own in their 80s. They never sit empty for long.

NOT ONLY do Realtors have better knowledge of the local market than anyone else out there… and can swoop down on any good deals that come along… but they also have a steady stream of people coming into the office “looking for a place to live.” In a nation with a 50% divorce rate, such happenings (quick distress sales and a need to rent) are constant. To say nothing of people moving into a community who need to start a job before an appropriate house hits the market (or before they unload their current house).

So if you have a vacancy in your four, nine, or twenty properties you simply let your fellow Realtors know and offer them a commission for telling their clients about it if that is the local standard. As long as the value of the properties doesn’t actually drop (like in the Great Recession) then you will come out ahead in the long run. Sideways movement in prices after a false run-up doesn’t matter if you Buy Low… and have someone else paying the note!

I think it is time to suspend the free money mantra and belief that prices only go up.

As we all know there are bubbles that popped up everywhere and it just becomes unsustainable for anyone to afford anything let alone a house that has artificially skyrocketed 20-30% + in 2 yrs!! The expectations have to come down and everyone should do better and try to achieve some stability otherwise this country really is doomed and doesn’t learn from crises of the past.

I’ve met 1 honest, competent Realtor in my entire personal life. The woman told me not to buy a house I was looking at to buy in 1987 because it was on a busy street and would be dangerous for young children.

Most Realtors are like junkyard dog Attorneys. Only use them when you HAVE to.

“I’ve met 1 honest, competent Realtor in my entire life”

How nice! You met my mother.

But I take you larger point as well… when she retired the average IQ of the profession dropped considerably.

Of course you’re right that nationwide the inventory doesn’t change due to homeowners refusing to sell and move to a new house, but there must be some geographic imbalances, right?

Maybe this means (for example) older homeowners stay put in Minnesota, and don’t sell to move to Florida. Wouldn’t that reduce inventory in Minnesota and increase it in Florida?

Given the huge flow of people in all directions over time, it tends to balance out over time. That said, California has lost population over the past two years, and the Bay Area has lost quite a bit of population, while new housing supply was added, so that’s where you some extra pressure that you might not, or not yet, see in some other markets.

The US overall has had the least population growth in ever in 2021, I believe.

“Over time.” How much time Wolf? Florida residential real estate has been in an asset bubble for years. $1,500 a square foot for absolute dreck. And it seemly keeps on going. Meanwhile, the rust belt has nominal appreciation and in many areas declines in value.

There was an article about TikTok users moving to Peoria, IL (I think) because the houses were going for 50k. The couples just uprooted to own a home there. Wild!

Anyone paying $1,500 per SF for anything less than totally excellent housing in FL is a sucker MM.

The very pleasant, very mixed in all ways, hood we inhabit these days in the saintly part of the TPA bay area has small and medium houses selling if old and needing updating for around $300-325, and then, when rehabbed nicely at around $400-425.

Not in the ”high rent” district far shore, but not any kind of high crime or much at all, etc.,

The Census Bureau estimated a resident population of 331,823,629

in Dec 2020 and 332,588,566 in Dec 2021, which is an increase of only about 0.2%. The increase in 2022 was about double that, i.e. 1.5 million people and 0.4%.

To me this is where the housing shortage narrative falls apart….where are the new buyers coming from? What’s changed is more people (or companies) own multiple properties.

The census was done b4 the pandemic if I remember correctly. Those people were everywhere like flies. I’m going to hawaii in 2029 when the next one is done. bleh

During the pandemic — much of it in the second half of 2020.

Let’s see what flippers can do.

What banks are doing with drop in Long term bonds is to hold till maturity and fudge accounting category to hide losses hoping that either there will be no withdrawals to force them to sell or hoping that Fed will Pivot. We all know how it’s working out :).

Now back to flippers. They can hold hoping that Fed will Pivot (it won’t anytime soon). They can sell at considerable loss, but they are clearly not doing this yet. However these flippers are in worse positions than bankers because

1. Holding a house costs more money than holding bonds (maintenance, utilities, hoa, property taxes, insurance).

2. The borrowing costs of flippers is much higher than that of bankers who were paying 0% on their deposits.

So in non-recourse states, flippers would just handover keys to bank and walk away making the taxpayers eat the losses!

This was a reply to libdis below.

“Holding a house costs more money than holding bonds”

Its also a lot more work than holding bonds.

Right now you can get 5% for doing asolutely nothing with 1-3 year CDs, and just wait till long term rates come up…

I guess the whole flipping market is finished. There are still many getting ready to come on line when you ride around Tampa. Ouch.

Flipping was impacted when the top was in. Many would be flip homes will eventually show up listed as an REO and like in 08 these homes will be in various stages of rehab. I picked up one around 2010 that was down to studs in the kitchen and bathroom. There was a stack of laminate flooring and other materials to finish it but the newbie flipper just waked away. It was a good deal and I did many more as the market was dropping. The biggest factor to success is in the speed of the rehab. I have a formula that determines what I can pay and how long I have to get it ready to list. If the rehab runs long it can wipe out most of the profit. No-mans land is just after the top and before the pricing falls. Once prices have had the first move down you can start to dip your toe in the water. THE biggest question I have is when will the foreclosures start to show up at the court house steps. There are many reasons a home gets foreclosed even if the house has equity? I have to think there is a shadow inventory because of the moratorium? Wolf do you know if there is a backlog?

He’s written on this before. Foreclosures (and other credit defaults) were at historic lows during the pandemic. They’re starting to tick up, but we’re nowhere near the highs of the financial crisis – yet.

I’ve been looking for a house for a few years. Your post is an excellent summation of why the very first thing I do is see when it was last sold…. “ The biggest factor to success is in the speed of the rehab. I have a formula that determines what I can pay and how long I have to get it ready to list. ”

My translation as a potential buyer… “I get the cheapest crap on discount from any place I can, hoodwink local inspectors, and hope that the paint doesn’t peel off before the showing.”

I’d never buy a flip for more than 2% than what the flipper paid for it. Never.

As if laminate vinyl flooring is a special thing.

Heck if you look at the new construction around here I’d take an older house with a coat of paint on it, if the bones r good pretty much any day over the crap that’s going up now.

That being said you make your money on real estate when you buy it as far as I can tell, assuming your exit plan works properly of course.

“Flipping was impacted when the top was in …”

You assume history will repeat itself, meaning your tactic will work again. Possibly. But the FED might not pivot like last time, which will doom anyone trying to replicate your method.

What we all need is sanity in the markets, i.e., for the FED to let the free market do its thing.

I used to watch this show on HGTV. Man those were entertaining to watch them yell at the subs. Then turn to the camera and say “These subs are killing me”.

One of the guys got in trouble for selling “flipping courses” which seemed like cult gatherings.

Strange times man! Strange times

Pretty soon we will have the new and improved Carlton Sheets infomercials back on TV again!

Agreed, and add in:

1. Remote Work, which at the margin will reduce job-induced moves,

2. Decreasing domestic reproductive rates (below 2) and

3. Likely tightening immigration policy

and I don’t see the next big wave of hype starting for a while…at least 6 months :)

I think the “remote work” thingy is what helped drive the explosion in prices in the west including AZ and ID and possibly Austin, TX. Those ignorant folks who fell for that are now being called back to the SF’s, LA’s and Seattle’s of the world.

My company in CA has remote wfh policy .

Many people bought homes far away from office thinking this would continue and moved 2 hours inland

Few months back people got called 2 days a week then 3 days a week now 4 days a week

Just surprised how things changed fast

This just happened “in my area”. Memo went out – wfh/hybrid work going from effective full remote to 4days in/1wfh starting May 1. (Ultimately it will go back to full time in office/plant). Presented with company productivity metrics showing productivity loss etc. It’s not surprising to me, but I’m sure there will be some outcry. WFH seems to have many zealot supporters, but it’s not the best way to run all businesses.

Yup my wife’s WFH job got called back into the office at least 3 days per week. She had a pre covid WFH deal with the company. They reneged saying no exceptions. Very tough for her right now as we had moved for my job. She is back to the interviews. Much less fully remote jobs out there than 6 months ago.

I’m retired and my wife and I travel a lot for pleasure, often to states in and nearby our California home.

During 2021 mainly, we had some different sets of friends who were allowed 100% remote work. It was great – now we had travel buddies who could come with us much more often for trips of a week or two in nearby states or within CA, whereas most of our travel friends are not yet retired.

They would come with us and do about 4, maybe 5 hours at most of work in the morning to just after lunchtime. Then we’d go out and sightsee, hike, have a drink, or whatever all afternoon. Occasionally they’d get a work call or email during the afternoon while we were out, which they could usually dispose of in 5-10 minutes, then back to the fun.

I’m not saying this was the case for all remote workers, but I definitely did not see 8 hours of hard work a day out of any of them during these times. I am a skeptic about the productivity of remote work in such cases, except for perhaps computer programmers and those who can do their most taxing work while alone, and may work all kinds of odd hours during a full 24 hour day. Those were not the types of jobs our friends had, though. Most are now back at the office, if they are still working.

It might just be cheaper to learn who is remote work. Dissolve their position and hire new younger people for less.

I wouldn’t put it past corporate America!

Most layoffs in the first wave at my company were remote, WFH. Now it’s 3 days a week in the office. Covid every week, of course, nobody wants to come back. Managers been getting the Covid, 🤣

“2. Decreasing domestic reproductive rates (below 2)”

I agree.

Boomers retiring/dying and the following replacement generation X is smaller and had fewer kids. But will the first half of the Millennials kick it back into gear. If so when?

My generation Z son, first of the group is spending everything he makes, on food, concerts and fun. Everything but saving for a house or even a car. Even though we spent years teaching him about finances. Good luck housing market!

Why shouldn’t he be spending all of his money? Our policy leaders, mainly early Gen X through Boomers, have set a policy of destroying the currency to pay for current desires.

If there is no incentive to save for the future because the future is bleak, people will respond appropriately.

the ‘future’ has always been bleak if you want it to be … once you start feeling sorry for yourself you quit.

natural selection at work.

JamesO, thinks are much worse than they used to be.

Most millennials are in their 30s now and not having kids. Demographics shows the largest amount of older single women in history. We are heading for a demographic cliff, but not as bad as Europe and Asia.

The demographic cliff is a problem to exponentioal growth economics. To people and environment a decreasing population may not be bad.

Invest in cats and pysch meds ;)

Perfect timing for the global warming Apocalypse! Why save when there won’t be much to buy/enjoy 10, 20 years from now? Many things will be ending quite hmm.. abruptly.

I’m in the #4 camp. I cashed out in Livermore, Calif. (Bay Area) in summer 2021 and moved to Phoenix to rent/wait out the crash.

I think #2 (owner dies) is very significant considering the prevailing demographics.

Millennials are a smaller group than the boomers they are replacing.

Seems like it would imply a housing surplus going forward.

Demographically, the boomers are an interesting case. They deferred marriage but not home purchases. So the boomers started out as single home owners. When they married that left them with 1 extra home.

I’m sure many boomers sold that 1 extra home right away. But others probably held on to it. How large are these two groups? Is there perhaps a sizable shadow inventory that gets resolved upon death when the kids inherit the extra home? That time would be rapidly approaching.

Vanishingly few held on to extra houses for thirty or forty years. Come on.

Seriously doubt those are even relevant numbers. More like outliers. There was dot com bubble crash, 2008 crash that affected boomers and their wealth. Unless they forgot about owning those houses, they would sell those first.

Also, they’re much more forced sellers.

If they’re still alive they need the money to pay for long-term care or just want it to spend while they’re still alive. Pulling it off the market and waiting another year isn’t an option. If they’re dead it’s probably to settle an estate and usually heirs just want the thing sold so they can get their money. Yeah, they can get in fights that delay this, but ultimately people tend to want the money.

In both cases, they don’t care about ruining the comps or getting the highest tick. If you’re a typical broke millennial you’ll take $800k split four ways in hand now even if it would’ve sold for $1m last year.

That’s true, but I think you may be thinking about the youngest silent generation dying off.

That is what I saw anyway, the youngest of the silent generation and some of the oldest boomers kids selling their homes.

Just clean them out and sell them. They do not even talk to the neighbors, whom their parents knew for 30 years! So cold.

Why would you talk to the neighboors?

By 2021, millennials surpassed boomers as the largest living generation. In 2021, Get Z was already larger than Gen X.

Being a late Boomer with friends who are Boomers, I don’t think they are ready to die yet. Most are very healthy and active. 70 is the new 50. I did a quick check in the Sunday Obits and most of the people listed were born in the late 1920s up to the mid 1930’s. These were Silent Generation.

It may be another 10-20 years before the peak Boomer die-off happens. I hope.

It’s funny, people are confusing boomers with prior generations.

It IS funny, as in strange.

I for one, being a ”war baby” (as we born during WW2 are or were called ) see a lot of confusion re: exactly or even approximately the birth dates of any of these groups except for the ”boomers.”

That one, 1946-64, seems clear enough, but there appears to be a lot of difference of opinion about all the others since then.

Is there any solid or official agreement on these?

Thanks,

I am 68 and I run five miles every day. I have no health problems of any kind and take no medications. Nevertheless 70 is NOT the new 50.

But, But….. My employer said to wait to retire. 70 is the new 50! :-)

Great job with staying in shape! That is hard to do if you are Zooming all day at a desk.

Actually ES, it IS for some folks, far damn shore…

NOT ALL equally surely, but some folks are really just ”hitting their best stride” at age 70 these days…

From years of research and following up with deeper dives, it mostly appears to boil down to diet and exercise.

While a GOOD CLEAN diet is definitely a challenge for many, especially if they have either the dough/bread to buy any foods they want or OTOH ”think” they are too poor to buy decent food,,, fact is that the lower on the food chain one eats regularly, the better…

Exercise is similarly challenging but IMHO after SO many years, one CAN get all the exercise needed with almost NO expense and perhaps if that exercise is focused on growing as much as possible at home,,, so much the better…

Again IMO, everyone who CAN,, should be doing their best to spend the TIME needed to grow as much of their own food as poison free as possible…

Growing food at home can be done almost everywhere these days, with various food plants readily available for ”container growing” at almost every/any location,,, and with heritage or similar open pollinated varieties ( that will grow from seeds again and again ) now readily available from Seed Savers and other similar non profits, there is no reason not to do so.

The churn is gone. This makes sense to me, a lot of sense.

People aren’t looking to move up/over/down due to low rates. There are no longer 10/30/50 people showing up the first day a house hits the market or at any open house. Activity breeds activity.

FOMO is over. Buy in some smaller local due to WFH is over.

Markets will settle down to whatever is normal for the area. Listings will sit for the normal amount of days 30/60/90 per location and type of home.

We aren’t used to normal. We are used to free money frenzy. We got used to the stress of rushing out to buy a house right this minute, before prices went up another 10%. Prices aren’t going up, in places they are going down.

I have no idea what happens next. Well, I think I have ideas, but they are probably wrong.

There is nothing wrong with high rates

The main issue is the home prices are still too high

When the prices fall down enough you’d see many people trying to buy homes or trade up

Ditto Jon. I paid 12 3/4 %, price reasonable in the 80s. Worked a lot and got it done. Yes, I understand times are very different.

SFH Home prices are too high because of WFH and people put their commute savings into the house driving prices to the Moon. Also not uncommon for remote tech workers to be overemployed, working 2 jobs doing nothing because the tech companies were hoarding labor. Lots of misallocations in the latest Mania.

I’ve always thought the best time to buy a house is when rates are very high and house prices have settled to a low. The late 80’s at 15% mortgage rates were the best.

You could just refi every 2 years as rates fell and watch your house equity grow.

We might see that again If inflation gets bad enough.

Your mortgage broker must love you. Haha

I send him a holiday card every year. :-)

“They’re going to have to find another job”. I wonder if any of these folks put something aside when times were good?

There were realtors in my office that just got crushed in the 2008 downturn. I remember one that had just bought the new Escalade along with the big house and to do so did not pay any quarterly taxes for at least two quarters. The person said they were banking on two escrows closing to pay the taxes! Both deals fell out and it was just crushing. Just like Wolf said the volume or churn was what may Realtors bank on and base there lifestyle around, never thinking it will end.

I’ve recently met two very young RE agents who think this churn will keep churning. They are buying all the toys, big house, etc. One has wealthy parents and will get bailed out of his mess. The other I don’t know any other financial circumstances.

Remember, todays 21 to 24 yr olds were around 10 when the last crash happened.

This mentality exists because most Americans don’t believe they will financially fail.

I’m not referring to filing for bankruptcy or a temporary “spot of bother”, I’m referring to (the prospect of) an actual substantial decline in living standards or real poverty.

Considering the way most people seem to spend their money, it doesn’t register with them.

My sister and her husband filed for bankruptcy in 2010 or 2011 with a paid off house and $100K in credit card debt. Living in FL, they kept the house and didn’t experience any decline in living standards.

Her husband has a remote job now outside of the country. They have a decent income but not significant savings for someone approaching retirement. They also sold their house pre-pandemic where in the current market, they wouldn’t be able to buy again without some mortgage.

Wait, I didn’t think 20-29 year olds moved out of their parents home until the 30th bday?!

That is what I’ve been seeing. They just are not very motivated or responsible. I don’t blame them, not sure why the young are this way.

They’ll get it together sometime! We will see the little lights turn on behind their eyes and start thinking. :)

Ok last comment for today! I need lunch

I have two friends who in the 2008 bubble too. One started buidling spec houses and went bankrupt. He had a couple of empty houses sitting there for months and finally could not pay the bills. The other friend was a realtor. He had bought 3 houses as rentals. He panicked in 2009 when a couple of his renters lost their jobs and he sold the houses.

The Realtor regrets that decision today but would he have really stayed the course as a landlord?

Making money on renting a single family house is almost unheard off, especially with increasing property taxes. Breaking even is probably best case scenario. Now if you put that money into stock at that time, the return would be much much higher. The realtor has rose colored glasses.

John,

Do me a favor and tell those two Realtors that the Swamp “Doesn’t give a f$ck about their problems”. And try posting something more informative on this Website.

One additional subset of people that I would love to hear your comments about, Wolf, are homeowners who would be selling, but because they have a low interest rate locked in, are opting to rent instead. Would this not restrict supply to some extent, at least temporarily? Asking in earnest as my hubby and I would like to buy our first home (likely will be in Portland, OR as we can’t afford anywhere else on the west coast) and are trying to figure out the best time to do so as much as possible. Currently, we are renters in SF.

JLo,

Not to preempt Wolf, but I am a homeowner carrying no mortgage. My house has been paid off for years. I would rather sell my home as opposed to renting it out and here’s why:

If and when another crisis occurs, and it will, renter’s moratoriums will be reinstated. Because of that possibility, I will not rent my home out, nor will I ever own rental property.

Although I want to sell my home, even in this market, I have decided against it and I will stay put. My decision is based on this very simple chart that you can find here:

https://wolfstreet.com/2023/03/14/services-inflation-rages-at-four-decade-high-sticky-entrenched-fueled-by-rents-auto-insurance-repairs-airfares-hotels-pet-services-food-services-delivery/

Refer to the chart with title: Owner’s Equivalent Rent of Residence (red line) and Case-Shiller NHPI (Purple Line). Notice how, as of the past year, the slope of the OERR has increased. I’m assuming this trajectory will continue. Also, take note that during housing bust 1, the slope of the OERR never leveled off, never declined, but remained positive, even as home prices were declining. For these reasons, I will not sell and rent.

Simply put, as a homeowner with 100% equity, and who would like to sell, I have decided against it because I believe rents will continue to rise and I don’t know how long it will take for housing prices to correct or to what extent. It just doesn’t make financial sense for me so I’m staying put.

I’ve lived in the Portland metro area for 30 years now, so a little unsolicited advice, if you will. Your property taxes will go up by 3%, each year, so long as the assessed value of your home is greater than the real market value (RMV). The RMV has always been substantially higher than assessed value. That could change, but doubtful. This means that if the RMV goes down but is still higher than assessed, your taxes still go up by 3%, annually. This 3% annual increase is statewide and capped.

Now, with regards to county, city and other taxing districts, I recommend staying the hell out of Multnomah county and the Portland city limits. Property tax hell, if you will, local taxes stacked on top of the 3% annual statewide tax. Oh, and by the way, I also live under another taxing authority know as Metro, unique to the Portland metro area, I believe. So, if possible, stay the hell out of the metro urban growth boundary. The urban growth boundary expands every year. My home is subject to 17 taxing districts in all.

Hope this helps.

Good luck to you and your husband.

Jlo asked about people with 3% mortgages. If you own a house free and clear it’s more compelling to sell but if you have dirt cheap debt attached to it which is at a much lower cost than inflation the argument to sell loses some water. I know quite a few people that are keeping their houses with cheap mortgages and renting them out while they go and buy another house or move in with their family. Or sometimes even rent. Most people realize it’s not smart to sell an asset if they are lucky enough to have very cheap debt attached to it. Prices will go up and down but their mortgage is fixed for a period that will surpass multiple real estate price cycles. So they have very little incentive to sell.

Always good to buy ar higher rate abd lower price than vice versa

Thanks for your reply. I appreciate it! I will check out the graph you linked. I also appreciate the take of someone who lives in the Portland Metro area. Question for you – if you are worried about a moratorium on rents during a crisis, if you sell your home and are a renter yourself, would you not benefit from the moratorium during the impending crisis as a renter? I do understand the reason why you would be nervous to rent out your own home because of this though and, of course, there are many other reasons not to sell a house that you own outright.

Wanted to also add a bit about property taxes in Oregon as I, bizarrely, find understanding them incredibly interesting and have dove into Multnomah Country property taxes with abandon. Oregon is especially unique and complicated. You probably already know this and were simplifying, but just wanted to point out that, in Oregon (the whole state and not just Multnomah County), your MAV increases 3% per year, but your property taxes can actually *increase more than that per year* based on the various bonds voted on by the local populace. Ultimately, how Oregon does it is decidedly not at all fair, but I am aware, and it is one of the first things I look at when a property intrigues me. You might find this article by The Oregonian interesting: https://projects.oregonlive.com/taxes/property/map but you can also look up any property’s taxes via county records online and see if they are, what I call, “under water” by multiplying the RMV by the change property ratio for a given year (currently .449). The change property ratio is used to figure property taxes on brand new construction as it obviously didn’t exist in 1995 which is the base year to figure Oregon property taxes. Figuring out what the property taxes would be if the same house were a brand new construction assists me in understanding if a given property is a “winner” or a “loser”, and I also find it useful when considering how much remodeling a particular property might need to become “livable” as remodels increase the MAV as well.

JLo,

Regarding the link to the Wolfstreet article in my post above, please do take the time to read the entire article, not just the chart that I mentioned in my previous post.

“Question for you – if you are worried about a moratorium on rents during a crisis, if you sell your home and are a renter yourself, would you not benefit from the moratorium during the impending crisis as a renter?”

Benefit? How so? Financially speaking? No, rent forbearance would not be beneficial to me in any form.

Having read your reply, you are definitely on top of your game with regards to Oregon property taxes. Just to clarify, your property taxes will go up, YOY, at a minimum of 3%, so long as the RMV is greater than the tax-assessed value. And you’re correct again when noting the YOY increase could be higher. For example, voters could approve an ISD bond proposal.

Even during Housing Bust 1, my property taxes went up each and every year because the RMV was always greater than the tax-assessed value. Over the course of my “home ownership” (yeah right) the largest YOY tax increase has, thus far, been 18%.

And you are correct when you say that the Portland metro area is the least expensive relative to the Bay Area, LA, San Diego, and Seattle. I refer to Portland the west coast cheap seats.

Just to reiterate, I’m staying put. I don’t see how it makes sense to sell and then rent or sell and then buy something else. But I really would like to sell, just for the sake of change. Still working on a gameplan.

Do you guys call grocery bags “Sacks”?

I heard this the other day from some portlanders here visiting Raleigh.

My brain was burning “Sacks?! No no, they are grocery bags!!”

Haha

Yes, they really are called “sacks.” LOL!

Traveler’s Tip: If you ever visit Portland during the rainy season, don’t carry an umbrella!

(+1 – 1 = 0). Thank you! Finally someone has figured out the net zero impact of frozen sales. For months real estate people touted: Nobody will sell, hence no inventory, hence prices will go up. Nobody called them out on it….

It’s similar to the “money on the sidelines” myth “waiting to enter” the stock market.

Why do you call that a myth? Many people (like myself) are 100% cash (treasuries and such) and fully intend to enter the market when it falls to/below fair value.

Lots of other folks right here in WolfLand have said as much themselves.

We ain’t mythical creatures.

When you return to the stock market and buy, the sellers will then have the cash you paid for their stocks. The cash is still there, just in different hands.

ForestThroughTrees:

Comps. I dont care about rates just price which largely is a function thereof. ok, so a small subset of the overall market is ‘participating’ Transactions go down but what about the trend.

With so many people locked into 3% mortgages, a huge part of the market is gone, as Wolf said.

So what is left?

On the sellers side, you have all the situations Wolf mentioned, which is a lot of people. On the buyer’s side, you basically have first-time homeowners, who likely struggle with affordability issues and have the realistic option of renting a nice apartment for a few more years.

Motivated sellers on one side; wannabe home owners struggling with affordability issues and options on the side.

Doesn’t look good for residential RE prices.

When I look at the current RE listings, I’m amazed at the number of sellers who bought their homes only one or two years ago. I sense panic there. They know what’s about to happen.

It is quite amusing to see many sellers still listing their properties at peak prices… It’s going to take some price to find the equilibrium

you omitted the geo-arb buyers. They are less price sensitive going from a HCL area to LCL area. Plus, people do not want to move twice; first to rental housing and then after buying a home.

Until, after a few months of HCL buyers going to that LCL area, the LCL area becomes a MCL or worse. Much of that low-hanging fruit is gone now, after two years of insane pandemic money-printing and rate repression combined with “permanent” WFH opened up the geo-arb trade. The trade got crowded…go figure.

There are still LCL areas, of course, but the number of them that any HCL buyer would actually want to move to is getting smaller.

I might be panicking if I bought a house in the last 2-3 years as an investment and not a primary long-term home (10-15 years). Proportionally to all home owners, I don’t think there are that many.

If you purchased a house before 4 years ago, you are likely doing very well with at least 30% equity and a sub 3% refi rate. Why would you sell? Other than Wolf’s excellent reasons above.

“11 million homes that are vacant year-round” seems strange. Okay maybe waiting for prices to go up, but the costs seem high: property tax, some maintenance, lawncare, HOA (if HOA), squatter-theft risk, fire risk, increased insurance. So why are so many homes vacant year-round?

I am glad Wolf brings up the empty house number as it is a variable that could swing prices short term. But where are those empty houses. I am thinking it is very regional but I could be wrong. Probably most are in vacation areas?

I remember vacationing to Miami area last year. I was there for a 10 days. I noticed most the 10 to 20 story condos around me had hurricane shields drawn down. I would almost say 40%. Nobody was in those condos the whole time. I am guessing those could be lot of the empty units?

“But where are those empty houses.”

I can give you addresses. I’m surrounded by empty condos (there are hardly any single-family houses in my hood in San Francisco), including a building down the street that was completed a few years, sold all condos before it was completed, and is showing nearly no signs of life, except for the occasional folks getting out of an Uber with luggage once every now and then… this is a fairly large building, and I have direct view of the entrance.

The key phrase is “vacant year-round”. I would assume vacation homes are occupied when owners are on vacation, but maybe not. Probably a lot are condos since they require less maintenance than a single family dwelling. It seems odd to buy a house or condo and never use it.

Chinese,Mexican, and Canadian owners. Plus every other global national with money even Russian ogliarchs . M only talks

Money

Bingo! I don’t know how many times we have to go through this. My condo complex is a ghost town – 105 units and at least a quarter of them are vacant. Mexicans love to park their money in San Antonio.

@Wolf great article. Your list is well thought out. Adding to the conversation I’d like to address a more fluid sources that could cause a rapid decline in prices: Institutional Investors and Individual investors. According to bankrate.com “Institutional investors purchased 13.2 percent of all properties sold in 2021, according to a 2022 report by the National Association of Realtors (NAR). Perhaps more concerning is the fact that they bought those homes for 26 percent lower than the state median prices during that period.”

While these institutional bought low, those investors are just that, investors. They are not homeowners. Investors (13% of the market) will soon get cold feet not wanting to absorb losses when they could be making 5% annually investing in low risk CDs or money markets. The benefit of owning investor property is: asset appreciation, ~5% income, depreciation, tax deductions. If prices continue to drop accelerated losses will only be sustainable for so long. It seems to me that this source will be the first to sell thus adding significant supply back into the market. It seems to me that we’ll see a downward spiral as real estate price decline accelerates. Additionally, multi-family properties that were purchased 3 to 5 years ago will require refinancing at much higher rates and thus placing those investors upside down in their investments. There were a lot of first-time investors in both residential and multifamily who came into the market starting in 2020 who will soon need to refinance since commercial real estate financing is generally only 3, 5, and 7 years. There are a lot of institutional investors who will need to immediately write down their losses as they won’t be able to hold them on their books. Institutional investors will need to answer to their investors / boards and thus will take the right-off. It seems that we’re going to have at least the investor portion of real estate come to market over the next 1 – 3 years as both the commercial and residential side come to market thus putting continued downward pressure on the market. We just don’t know how and when The Fed will interject. They always do.

A month ago I met with a customer who inherited a house and doesn’t plan on putting it on the market but instead will turn it into a rental. Another customer bought a new place to move to but said that at 2.85% he never plans on selling his old place and will be turning it into a rental. A year ago another customer bought a run down vacant place and has turned it into a rental. In my neck of the woods (San Diego) investors are buying up anything that has potential to become a multiple ADU property and outbidding the flippers. SFR’s for sale to the happy homeowner in San Diego are not as many anymore, and the notion that lots of houses are being made is simply not true in this area. We’re surrounded by the ocean, Camp Pendleton, mountains and Mexico. Urban infill is the name of the game here and most of that infill is multifamily and ADU’s for rent, not for sale. These numbers and notions may be true elsewhere, but they aren’t here. Those of us who say this are immediately shut down but that doesn’t mean that what we’re seeing and commenting on here isn’t true. I’m not sure about the rest of Southern California, but there’s an incredibly short supply of inventory here (new sales are outpacing new listings among other things). At the end of 2022, days on market was up there but has since dropped to 5-14 days more or less for anything priced right and desirable. Junk is sitting 30-60 days and absolute junk is sitting a long time. Just saying what I’m seeing (and to clarify, I’m NOT saying that we’re in a hot frothy market with never ending record setting house prices or other stuff the red meat lovers like to attack).

There’s others saying this same thing in the comments section. We’re going to need a support group with how we get bludgeoned.

What you don’t get is that they ARE putting it on the market — the rental market, and there is arbitrage between the two, it’s the same house, for crying out loud, buy or rent… that’s the arbitrage. Anyone renting that house is one buyer less in the sales market, and reduces demand further in the sales market. Think this through a little. That’s exactly what we’re seeing now. You’re citing one reason why DEMAND is so low in the sales market and why sales in San Diego have plunged by 33% yoy, and why the median price has dropped 11% yoy.

While what you say may reduce demand somewhat, most renters do not have the financial means to buy a house, or simply do not want to own a house. I suggest the rental market and the house-buyer markets are pretty much mutually exclusive, although there is certainly some bleedthrough. I have not seen too many listings (in California) that say “House for Sale OR for Rent”, but of course some probably exist. I am prepared to be enlightened.

Well, Wolf did say above – “think this through a little”.

There have been a lot of other posts on this blog about ~5% brokered CDs, etc.

Say there are two identical or very similar houses in Southern California (and Southern California is big enough for this to be the case), one for sale for $1.5M, and the other for rent for $6000 per month.

If I have $1.5M, I can either buy the for-sale house and then pay 1% property tax per year ($15k per year expense), or I can buy some brokered CDs at 5% ($75k income per year) and move into the rental ($72k per year expense). I come out ahead almost $20k per year renting, I avoid the risk of falling prices, and I haven’t even included other costs of homeownership, like maintenance, or the fact that homeowners insurance premiums are higher than renters insurance.

And on top of that, the $1.5M house probably doesn’t even fetch $6k in the rental market.

You are wrong. Plenty of renters who want a house and have the means to buy, but don’t for a host of reasons.

William Leake,

It seems you don’t understand a big portion of the rental market: mid- to high-end rentals. And that’s where the money is. Landlords understand it, builders understand it, and that’s where nearly all the money has been going for years. And that’s what EVERYONE is now building.

For many people with plenty of money, it’s a lifestyle choice.

Build-to-rent, where they build entire subdivisions with houses designed for rentals, is the biggest thing for homebuilders right now, they’re all doing it, and they understand the market. These are NOT cheap houses. They’re NOT for people who cannot afford to buy. They’re nice houses for people with relatively high incomes who just don’t want to buy because they like the hassle-free flexibility of renting.

Then look at the rental markets in NY City, San Francisco, Boston, LA, San Diego, etc.: lots of dollars:

Median asking rents for 2-bedroom apartments. This is “median,” the rent in the middle, not “higher end” or “luxury” (Data from Zumper National Rent Report):

New York, NY: $3,820

San Francisco, CA: $4,000

Jersey City, NJ: $3,330

Boston, MA: $3,200

Miami, FL: $3,500

San Jose, CA: $3,270

Los Angeles, CA: $3,300

San Diego, CA: $3,100

Washington, DC: $3,200

Arlington, VA: $2,990

Higher-end rentals in Manhattan cost $10,000+, in San Francisco, it’s $6,000+. These are for people who make lots of money. Renting for them is a lifestyle choice. You’ve got to understand that, or else you’ll never understand the housing market. Landlords understand it, builders understand it, and that’s where nearly all the money now goes (is there going to be a glut? sure, but that’s how it is).

The reason you don’t see “House for Sale OR for Rent” is because the processes of buying or renting are different enough that both sellers/landlords and buyers/tenants need to decide which one they’re doing before they pick a particular house, not because the two markets are completely unrelated.

If you own a house, you just need rough numbers to decide between selling or renting it out, so comp sales or comp rentals. You can go with something automated like what Zillow and Redfin provide or look at comps yourself. Then rough future estimates of other carrying costs are easy to come up with as well. Once you decide between selling or renting, the process of prepping the home for customers to see is different. Prospective tenants will not do a home inspection, for example.

Same on the other side. Zillow and Redfin can give you cost estimates that are close enough to decide between buying and renting. If you want to *buy* a house, you need a mortgage preapproval, or you need to have your liquid proceeds for a cash offer consolidated in a way where you can present a statement of funds as a substitute. For renting, you just need a credit check. It will affect your search criteria as well (our lovely little Johnny just turned 3, so maybe the local high school’s rating is not too relevant for our rental).

I could pay cash for my current rental. There’s just such a juicy arb with rents so cheap why would I want to buy? I agree it’s that way for a majority of people but I think it’s becoming more common, I know lawyers and investment bankers who are renting because of the arb.

To all the replies below to my comment, please note I did write “or simply do not want to own a house.” I am actually in this category.

I wonder if there are numbers on Wolf’s “build to rent houses” as a percent of all new houses built, say over the last year. I would guess it is a rather small percentage. If it is a high or moderately high percentage, it might explain some of the weird things happening in the housing market.

The renting luxury lifestyle is really fun.

Then going to owning is ALOT of bills.

So what Wolf is saying is true. A lot of people choose the easier and funner lifestyle.

until they realize they are just spinning their wheels in life and want to own a home.

That’s a hasty generalization. Three different people I know that bought over the last six years rented hovels beneath their means in order to save fairly prodigious sums by way of self-induced poverty effect. One guy sold his place here in Austin & lived with his parents for 5 years (surprisingly, this did not seem to stunt his dating prospects) sinking the money he made into an ultimately failed business.

A lot of people rent strategically because they remembered HB1 and even though HB2 made some winners, the casino atmosphere makes some of us wanna die so much we’d rather sit things out for as many hands as we can.

Here is a detail, if there is a deep recession that brings unemployment many of these many people with 3 percent 30 year mortgages may lose their jobs and then be forced to sell urgently. And no one knows what will happen tomorrow, let alone what may happen in 5, 10, 20, 30 years. For me, a mortgage with such a long term is a super risky venture.

Forced selling, that’s supposed to never happen. Apparently, most people’s lives are so predictable and they are so economically stable instead of being mostly broke.

Or so I keep hearing.

Agreed, there is always going to be some degree of forced selling and with unZIRP just underway, the hit to labor markets (likely biggest driver of forced selling) is only just starting.

Ditto for aging population (Boomers now 59 to 77 yrs old…with peak cohort 68) – aging likely second (or first) rationale for motivated/forced selling.

As far as those 3%/30 folks go, how many of them do you think purchased cheap in 2010-2019, then took a huge cash out refi (or series of them) as their home increased in price?

So rather than “sitting pretty” some of those folks *could* be vulnerable to being upside down, struggling to afford their mortgage payment, etc. (It did happen in 2008. You never knew that your neighbor with all the toys was living on serial cashout refis – until the ability to refi stopped)

Juliab,

Actually, its pretty risky for the lender of such long term debt.

Think about the duration risk: would you want to *buy* 30YR treasuries right now? Of course not.

In a period of inflation & rising rates, holding long-term debt with a low fixed rate is a winning trade imo.

MM

US 30 year fixed mortgages are guaranteed by you the taxpayers not the banks. That is, the risk is at the expense of the American citizen. But if the owner of such a mortgage is fired, gets sick or something unpleasant happens to him during these 30 years, understand that the risk is entirely at his expense

Juliab,

No disagreement from me – however I’d argue that anyone taking on homeownership should have funds set aside for emergencies and shouldn’t be living paycheck to paycheck.

Why should I pay off my 5% and profit off the spread?

You’re right that folks who don’t have emergency funds set aside will be in a tough spot in the event of a job loss etc.

That should be:

Why should I pay off my sub-3% mortgage early, when I can ladder CDs yielding above 5% and profit off the spread?

MM

I kind of agree with you that people should have a buffer when taking out a loan, but how many people do you think with FOMO and this bidding had a buffer for the tough times. I don’t think there were many. I think most bought on the edge of possibilities

Would the bailing put of bank deposits by FED usher in another rally in the stock market? Market things so.

Have the banks ever offered any kind of mechanism by which one can “transfer” the 3% mortgage to a different property? I’d certainly give moving much more thought if there was a way to take my existing mortgage rate with me…

Of such things, financial innovation is made. Value is unlocked. Might be a zillion-dollar idea.

Yes, the idea is just missing the small little detail of “what’s in it for the bank.” If you’re paying 3%, they would like their principal back, please.

Ah, right. So the innovation would have to come from outside the banks. And the transfer fees would have to be substantial. Still, there’s a start up for everything. Or was…

How would this work when lenders have to pay 4%-5% today to get the money you want them to keep lending you at 3%?

Banks/lenders are just middlemen between depositors/lenders and borrowers.

I don’t think that would make financial sense since your bank can now earn a higher interest with the cash that they lended to you earlier.

Banks make money on fees as well, there is definitely value here to be captured. Case #1, no transfer of mortgage, no sale and no purchase of houses (to transfer the mortgage to a new home you would have to purchase it and I assume sell the old house) = $0 additional dollars for anyone (over the mortgage interest). Case #2 – A transfer of 3% mortgage that is accompanied by a sale and purchase of a home. Realtors get paid, title gets paid, notaries get paid, inspectors get paid, banks get paid, etc.

Transferring a 3% mortgage to a new loan at today market rates automatically means the mortgage is worth substantially below par. No way the fees make up the difference.

If it was such a great idea, it would be a common option. Obviously, it isn’t.

Is it possible for a homeowner to go into the secondary market and buy his or her specific mortgage at below par, but above market price? This could help facilitate the sale of a home.

As things currently stand, both homeowners and mortgage owners will make a profit if a house sells–the owner from the sale of an appreciated home and the mortgage owner from the payoff at par of a mortgage that is currently worth less than par.

The problem is that the homeowner controls the sales decision while the mortgage owner receives a substantial benefit, and thus certain economically beneficial sales will not take place. Since mortgage holders would rather have their money back if they can reinvest at a higher rate, they would likely be willing to accept a bid for the mortgage that is less than par, but high enough to make it profitable to sell the mortgage and reinvest at current rates.

Someone needs to figure out how to facilitate home sales that involve purchasing 3% mortgages at a market premium rather than paying them off at par. Both home sellers and mortgage holders would benefit from this.

Most US residential mortgages are securitized. No practical way to allow the borrowers buy the mortgage back on their property.

It’s theoretically possible to do that with any bank retained mortgages. Not sure accounting rules give any lender an incentive to do it. Recognizing these losses would probably also negatively impact meeting earnings targets and someone’s performance bonus.

It would be interesting to learn what percentage of residential mortgages are originating bank held vs securitized, today vs., say 1983.

My guess is that many, many, many fewer rez mtgs are originator held (wikipedia entry – moral hazard…)

The rate is the price of money, not a bonus you are entitled to

@HollywoodDog – Banks never wanted to make 3% mortgages. That is why the GSEs bought/backed 98% of all under 4% pre-covid loans since 2010 because banks did not want to hold a 3% artificially low rate mortgage for 30 years. The risk/reward was not there. Look what has happened to all those MBS value once interest rates when up.. The regional banks are hurting who bought MBS and those are guaranteed. No worry about foreclosures. But if they held the home mortgages, not only would they be getting killed on the interest rate hike, they would have to be worrying about home loans on their books going into default. Just think if they also held all the home loans too.

Now with higher mortgage rates, banks may actually hold onto the loans.

For such a program to happen, it would need to approved they the GSEs. since in a round about way, they own more than 50% of all outstanding home loans.

I think what possible outcome that could happen if we have a bad recession is what happened during COVID. All government backed (GSE) loans will be able to go into forbearance until a recession is over. This will help prevent any housing crash. Just my opinion

Thanks for explanation of the mechanisms involved. This is just one of the reasons I’m not a banker!

A zillion years ago, they had what was called an “assumable mortgage”. Not a new idea, just not the best deal for the bank/mortgage company.

VA loans allow that.

A 3% interest rate is helpful. however, one’s life’s choices should not make it the most amazing thing ever. Especially not a real advantage in society. Because it really is not, in the grand scheme much of anything.

There are so many people who live on the churn.

There are 1.5mm realtors. That is 1/100th of all jobs alone. Plus mortgage brokers, plus a lot of the construction industry, plus home furnishings (everything from appliances to mattresses to bathroom tile), landscaping, home inspection/appraisal, etc. etc.

We’re over here talking about how much impact 10k jobs here and there and tech will impact the economy when we’re on the precipice of millions having the rug pulled out from under them.

THEWILLMAN-

I am counting on it.

“having the rug pulled out from under them.”

You mean like the tens of millions of USD savers for the last 20 years, who had their interest revenue expropriated by the Fed, so that phony, doomed demand could be ginned up to triple housing prices, even as American intl competitiveness rotted away?

still mostly running full tilt on the backlog, but the backlog is shrinking.

That rug really tied the room together, Mannn!

These people are mostly blood suckers, living off the productive work of others.

This may be reflected in the vacant homes mentioned here, but in our region many of the homes bought just before and during pandemic were 2nd and 3rd homes of upper middle income earners from NYC, DC, and Boston, rationalized by expanding stock portfolios. As inflation becomes more deeply entrenched and rates go or stay higher and institutional stock market participants sober up, many of these 2nd and 3rd home owners will list. And of course, people who bought with ARMs or have other variable rate debt, esp those at the lower end of the income range, will lose their homes to foreclosure. And finally, the builders, small and large, who entered the fray during the big run up, will be forced to sell at lower prices. Inventory will increase. I’m seeing newly constructed homes that were initially listed at $1.2 mil dropping to $1, and below already. The unwinding has begun.

I’ve heard the low interest rate mortgage referred to as golden handcuffs. Not sure if this is a real thing or something someone was trying push.

I called it the “3% jail” in this article. At least you get to sleep in the jail. Handcuffs are too restrictive.

Prepaid for appreciation you most likely will never realize to borrow money you could never afford when rates are at more natural levels.

Is there much supply potential from owners of multiple homes (vacation home) potentially selling one of their homes?

The Fed broke this market.

They injected a fake interest rate environment…..and now the ramifications.

Real Estate brokers will be slowly going out of business.

And now the stock market is becoming a seesaw, whip saw rerun….as people wait for the next “sound bite” from a Fed person or Congressman.

Not to mention the convoluted bond market, inverted yield curve, gyrating 2 and 10 year notes.

Remarkable that traders complain of a lack of liquidity in a market that big.

People and traders can read economics….no one can guess the next sound bite, policy decision.

be fair, give some “credit” to the reckless irresponsible multi trillion fiscal stimulus

@Wolf Somewhere else I read an additional argument in support of the shrinking market hypothesis: the demand was very much pulled forward by those sub-3% mortgage rates.

Yes, that’s an additional factor. And now they’re locked in too and off the market as buyers and sellers for years to come.

I consider myself an example of this. The low interest rates of 2020 sent us house shopping when we really weren’t in the market before. It worked out well for us, entirely by luck.

In the brief period of mid-2020 where low rates met “normal” prices, it was like houses were on clearance sale.

Don’t know where you bought, but prices haven’t been normal in nearly ten years.

My little rust belt town has been shrinking for years. A few manufacturers still hanging on and we are one of them. Otherwise our economy is propped up by growing corn.

Houses are still tethered to reality here. I realize that isn’t the case for probably the majority of the American population living in bigger cities though.

We bought our house at about 50% of today’s replacement cost. Not out of the ordinary around here. The prior owners did a lot of renovation and lost their butts on it.

@ Wolf: How about the financial industry creates an innovation in this instance and introduces “transferable mortgages”? E.g. a current homeowner which a 500k mortgage sells his home and buys another home while transferring the current mortgage onto the new home (obviously the collateral has to be similar). The terms stay the same and no need for taking out a new mortgage at 6+%.

You’re forgetting that the financial industry would lose a HUGE amount of money by transferring 3% mortgages when their cost of new money is 5%, and when they could write 6.5% mortgages instead. Banks are not a charity.

Maybe you can start a SoftBank-funded startup in Silicon Valley that offers this service, and after it blows through $1 billion in investor cash, it lays everyone off and shuts down. OK, you can pay me 10% of your VC funding as reward for having given you this awesome pitch for the next unicorn.

Where’s my checkbook?!? 😂

I can attest to this. I know someone who got in at the absolute bottom of the rates with a 30yr at like ~2.Something. That mortgage is non-transferable, not even to their heirs. It says it in the fine print.

I get your points, makes sense, nonetheless I’d like to elaborate: