The spring selling season is here, folks.

By Wolf Richter for WOLF STREET.

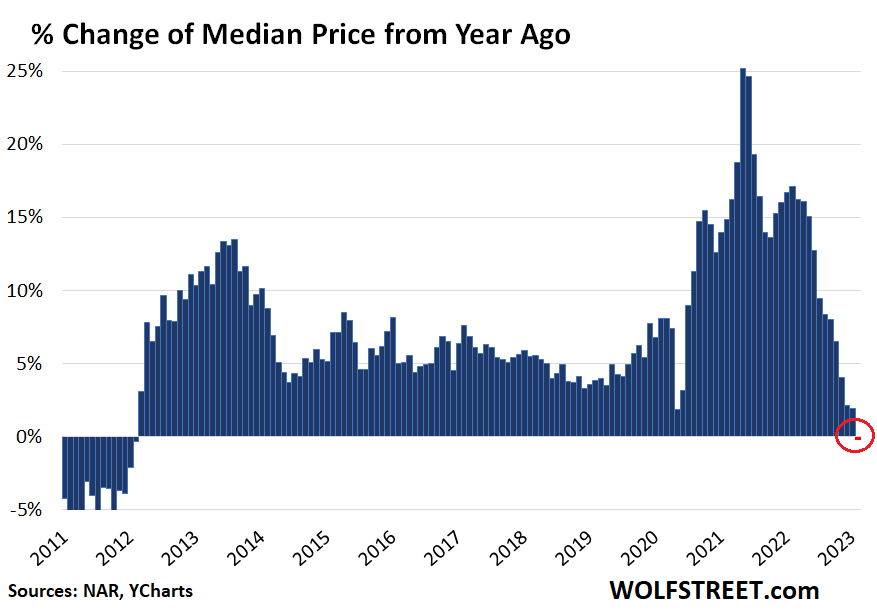

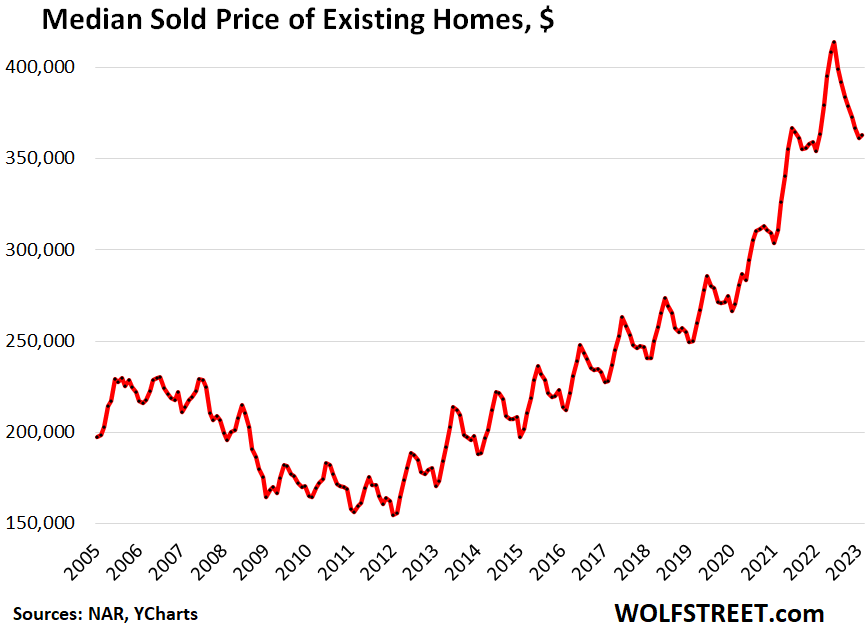

The median price of all types of homes sold in February, at $363,000, was down 0.2% from February 2022, according to the National Association of Realtors today. This was the first year-over-year decline since February 2012, when the market emerged from Housing Bust 1 (going into Housing Bust 1, the first year-over-year decline occurred in August 2006).

The year-over-year decline came despite a small uptick in the median price from January. But that uptick was far smaller than the increase a year ago, and so year-over-year, the price dropped (historic data via YCharts):

The median price of single-family houses fell 0.7% year-over-year; but condo prices were still up 2.5% year-over-year.

Lower prices will help unfreeze the market, and that’s starting to happen, if barely: “We’re seeing stronger sales gains in areas where home prices are decreasing and the local economies are adding jobs,” the report by the National Association of Realtors noted.

The median price has fallen by 12.3% from the seasonal peak in June 2022, (historic data via YCharts).

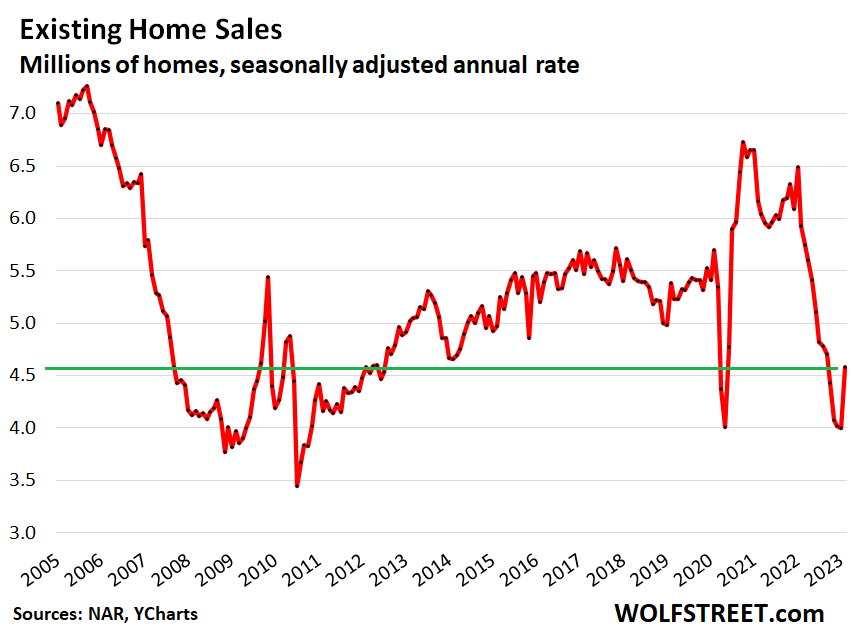

Sales of previously owned homes rose by 14.5% from deep-dismal in January, which had been the lowest sales since 2010 during Housing Bust 1, to a seasonally adjusted annual rate of sales of a still dismal 4.58 million homes. The increase came after 12 months in a row of month-to-month declines.

Year-over-year, sales were down by 22.6%. Compared to February two years ago, sales were down 25.8%.

Priced right, just about any property will sell. But not enough sellers are wanting to price their properties right just yet.

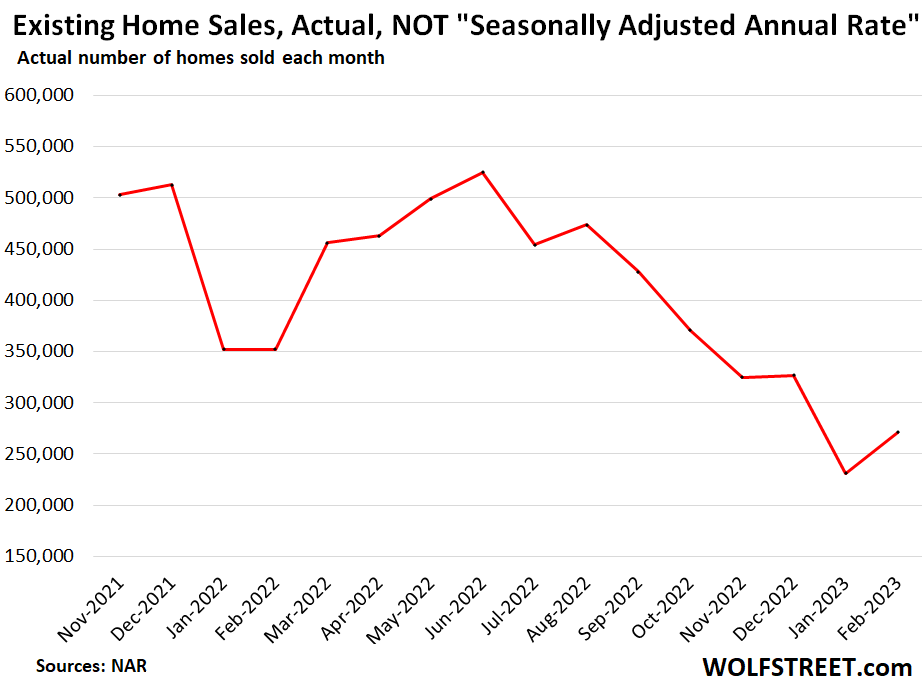

Actual sales in January – not seasonally adjusted, and not as annual rate – rose to 271,000 properties, down 23% from a year ago:

Sales of single-family houses, based on the seasonally adjusted annual rate, rose 15.3% from January, to 4.14 million houses, which was still down 21.4% year-over-year.

Sales of condos and co-ops, based on the seasonally adjusted annual rate, rose 7.3% from January, to 440,000 units, which was down 32.3% year-over-year.

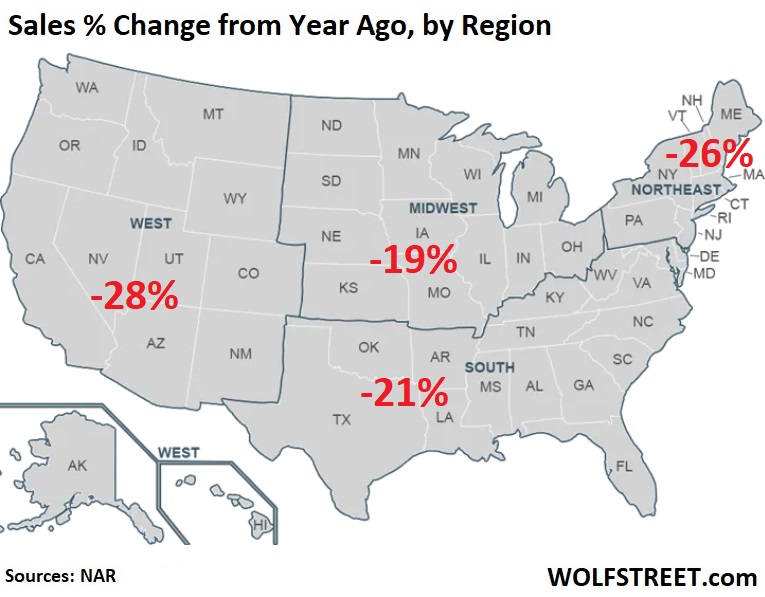

By region, year-over-year sales plunged in all regions (percent change from year ago, map via NAR):

All-cash buyers – often investors and second home buyers – rose to about 76,000 properties (28% share of 271,000 actual sales), from January’s roughly 67,000 properties (29% share of 231,000 actual sales).

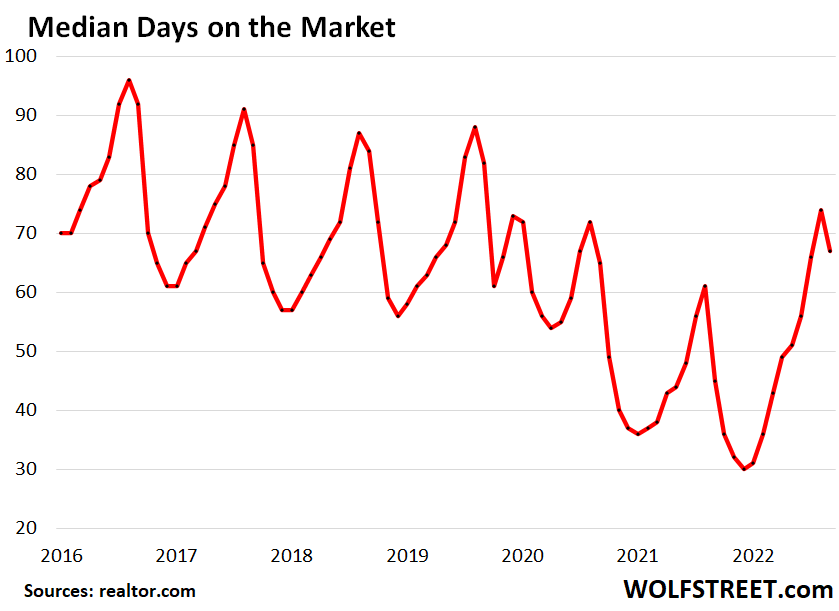

Median days on the market before the property is sold or the seller pulls the property off the market, at 67 days, was up by 50% from a year ago (data via realtor.com):

Months supply, at 2.6 months, while still low by historical standards, was up by 50% from a year ago.

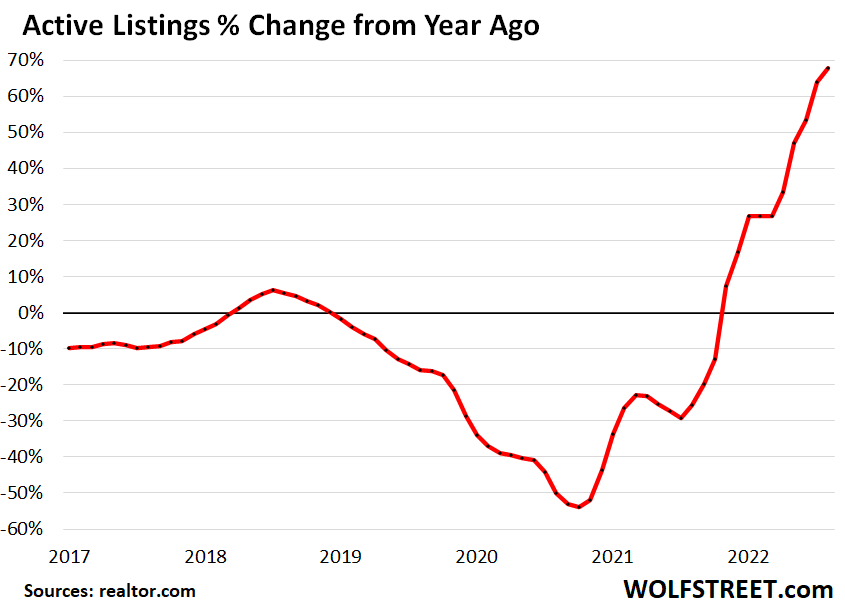

Active listings (= total listed inventory minus properties with pending sales), at 578,000 properties, were up by 68% from a year ago. In absolute numbers, active listings remained low by historical standards, as potential sellers are still trying to outwait the increase in mortgage rates, and as many potential buyers have pulled back (data via realtor.com):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Anyone out there have a good feel on the residential real estate foreclosure situation currently?

Creeping up from historic lows during the pandemic, but still very low.

Home prices will have to fall a lot further for a lot longer before foreclosures become a big national issue.

NAR: “Distressed sales” (foreclosures and short sales) accounted for 2% of total sales, same as in Jan.

The number of consumers with foreclosures:

Here are delinquencies which come ahead of foreclosures:

https://wolfstreet.com/2023/02/17/why-the-fed-can-let-the-housing-bust-rip-a-look-at-mortgages-helocs-delinquencies-foreclosures-and-whos-on-the-hook/

I think a lot of us who are looking to sell our houses in the next 1-3 years are very fearful of short sales like happened during the housing bust. It is one thing to drop the price, another to compete with “jingle mail” neighbors in which the banks simply want the house sold instantly to cover the loan principle.

It is kind of zero sum when you think about housing and stock market. If the Fed caves to the “Break or Brake” mantra, then housing prices could rise with inflation, as ultimately stocks get sucker punched if/when inflation comes back with a vengeance in short order.

Honestly I’m considering panic selling my stocks if the Fed pauses this week with no increase in FFR. I’ll probably cost average out if markets go euphoric and place it all in short term treasuries, going from 60% to 100% of liquid assets. I’ve been playing this market game forever, time for a break and focus on moving a house that somehow tripled in value in 11 short years. I’ve made good money walking away from Vegas tables on luck streaks, how is this any different as it all seems too good to be true with free money policies working forever out as planned by our oligarchy system elites.

Time to downsize and simplify all of life’s aspects due to exponentially increasing uncertainties…anyone else feeling the same way???

Looks to me like everyone will reduce their life style. What’s the difference if one can’t afford a product or service like in the Great depression or has plenty of money but the product or service is not available? No difference. You will start to see your neighbors cut there own lawn etc. One big factor I consider when looking to buy something is, can I service it myself. If not I pass for now.

Yort 2.0,

An old rule of thumb is never be afraid to take a profit.

Good luck to you.

I’m curious how the failed banks deal with their mortgage portfolio?

Could a failed bank force a homeowner to seek a new mortgage at a new higher rate?

Sufferinsucatash,

During late 80s early 90s via the Resolution Trust Corporation (RTC), notes were sold and serving companies put in place to send statements and collect payments. No changes in terms and conditions.

I did not have insurance or property tax escrows. I’d say the value of my property (a 5 unit apt building) versus the purchase price, mortgage and equity was never in question.

In those days one had hard copy originals of all docs; nothing on line.

Refinanced with another bank several years later, no prob.

“Could a failed bank force a homeowner to seek a new mortgage at a new higher rate?”

That has never happened before. Neither has mortgage forbearance ever happened before but it did.

A mortgage is a contract and if a new bank acquires a contract, I don’t think they can just tear it up.

We had a mortgage with Countrywide in 2008. Our loan was just sold off.

Most home loans today are owned by the US Government via Freddie, Fannie, FHA, VA. I suppose if the US Government decided to rip up the contract and re-write it, we’d have no recourse. Things would have to be very bad for that to happen.

“Neither has mortgage forbearance ever happened before but it did.”

Nnnnnnyes. Forbearance is a classic way of trying to give the borrower some time to get their ducks in a row.

What was new was “mass forbearance” pushed by the government. That has never been done before.

Just looked at the NOD list for this week in Reno and it went from years of 1-3 a week to 30! One week does not make a trend but it was a shocker to behold.

Out of curiosity I created a search query on auction.com in 2020 or so and then forgot about it. This month I started getting multiple emails per week with the results.

Interesting, given the exuberant confidence people have had in that area the past few years…

Wolf, while prices dropped for the first time, it is minuscule compared to the 10 year gains. This was the Fed’s grand plan, of course, to inflate away other inflation with real estate and stocks. This will/is backfiring, as asset concentrations at the top 1/10% increase exponentially relative to the Fed’s lack of basic math skills. Thus, more homeless, more people with jobs living out of urban trailers and vans, but less people stuck with overpriced homes with adjustable rates. The latter is key, and I don’t think we will see a foreclosure ramp even close to that of 2010. Perhaps, it is just me reaching for a different angle on this, and I am completely wrong. In any case, I do think the big builders are/will be in trouble as they will have to sell these massive developments that are under bank commitments. Of course, the Fed could secretly or not-so-secretly fund/support/bail out that too.

This is just the beginning. Housing Bust 1 took five years from top to bottom. Be patient.

according to the charts above,,,

from ”start” of the vast increase in the 2nd derivative of all the charts, the ”anomaly” happened from 2005 to 2014

so more like 9 years than smaller…

just saying, but especially just saying for those with money burning a hole in their pocket(s)

> last one took 5 years

Surely with the higher leverage, faster hike and general interconnectedness we are looking at a faster peak to through. 3 years tops?

Hoping Georgist is right. One thing we didn’t have last cycle as well was a bunch of folks from HCOL states moving where they pleased and bidding up prices with their HCOL salaries, only to be called back to the home office or forced to find significantly lower paying local jobs when they refuse the call. I think our dear government must be asking/threatening our biggest quasi-monopolies to bring people back as it solves half of the housing affordability issue.

Agree, with further firmament:

RE prices will unconditionally fall because they can (as you point) and the risk sentiment is ripe. Some say: Going down the risk totem pole of asset classes, after the fall of NFTs, SPACs, Luna, FTX, and a round of bad bankers bank spanking, it is good time for RE (as an investment) to take the 1st trashing.

Anecdote

Family friends are building an apartment in their new house’s basement for the AirBNB purposes… Now… In 2023. They talk to me about the expected monthly return on investment [$$$$], and are already indebted up to their ears. I’m like “Cool”.

RE must take the first leg down, or we are lost forever.

I see this too. A lot of GenXers are like deer in headlights that the boom times either 1. have ended or 2. will ever end. They purchase services like its going out of style. Upgrade their cars constantly. They are making high salaries but I do not think they understand fiscal prudence.

A bankruptcy attorney might have to explain their options.

I doubt GenX’ers are like deer in the headlights. They are in their 50’s now and they are a very cynical bunch. They have been thru multiple recessions, layoffs, housing crisis, and stock market busts.

That’s first graph will not turn into anything like 2009 & 10. And don’t worry Elizabeth Warren & the UNIparty RINOs will ensure mortgage & rent relief are trotted out WAY before foreclosures get rolling.

Very easy to get a feel for it when it’s essentially zero.

More layoffs in April may change this. New round starting with Meta and Amazon. We still have to see if it’s more lip service and less action.

Don’t know how long the big tech can fool fund managers and investors. Big Tech is too top heavy with executives that are drawing multi million dollar cheques, and there is No one laying off these executives.

The drop in price seems like a squibble when compared to the monumental changes in the other graphic, metrics that have you have meticulously documented.

If I were a betting man, which I’m not any more, I would bet that the FOMC decision tomorrow at 2 PM Eastern will be a 25 bp increase in the interest rate paid for cash. The experiment with QE seems to have run it’s course.

What, I believe is a more important message from Powell, is how the regulatory Fed will remedy their systemic failures. AI would zero in on the obvious that the private banking interests are the puppet masters behind the screen making the Fed to fuck up.

Markets are dictating the rate hike expectations to Fed and J Pow is following.

No wonder real rates remain negative, inflation remains high and Fed balance sheet chart looks questionable!

There are three big asset classes for the typical person. Stocks, bonds and residential real estate. First two are liquid and respond pretty quickly to Fed policy. Everything that had a price at zirp has a different price at Fed funds rate of 5% with housing taking the longest to reflect reality.

Fed was about 1 year too late getting started plus one year lag on policy means they let bubble go on for 2 years too long.

Remember what stock and housing prices were in 2009. We haven’t fixed anything, just added more leveraged and transferred some risk to shadow banking system where its not marked to market.

Bread and gas are going to be $10 or we are going back close to 2009 asset prices. That is the choice.

Why not 2019 asset prices? Seems more reasonable. Interest is bringing the bottom up really fast. It is an invisible bottom, no one knows where it is. One could guess.

sufferincash,

You might be right. but we were still under sway of zirp then. Fiscal deficit is running 7% of GDP. If Powell is serious about 2% he is going to have to turn the screws really hard to offset drunken sailor spending.

It’s gonna take some time to get things back to some sort of equilibrium. What a true mess that 0 interest rate policy plus buying MBS got us into. Could be a solid decade from start to finish to get things more normal imo.

We don’t have a decade to fix this high inflation and broken free markets.

People are getting screwed. The system of reward that capitalism thrives on is now broken in US.

Productive work no longer yields desired rewards and this lack of incentive is hurting real economy, production and supply of goods and services.

This facade created by QEs, causes US to look good on paper, while getting weak, poor and backward in real terms.

Couple in the rise of China, and it’s easy to see, this weakness will doom the empire, that will destroy both the dollar and our way of life.

This is definitely a Defining Moment for us. We need to re tool and have a big 5th inning.

Productive work doesn’t yield desired results? Priced a trade lately?

A lot of this is malarky. A tradesman can about write his own ticket as most fools can’t change a light bulb without a youboob video.

Case in point: A quote for a neighbor to remove and cap off a propane tank. $145. Took the dude about 5-10 minutes and maybe $5 in parts, including loading the tank onto his truck. That extrapolates to $910 per hour. Another case: Replacing a contacter on our heat pump. $494 – which also took about 10 minutes. The part cost $20. He quoted $385 for a capacitor I paid $15 for and did myself. Plumber? $75 to replace a $4 wax ring (local guy who feeds off the community and not trying to get rich).

Where the breakdown is: Those guys come back and fix their mistakes for free. The pols and bankers expect you to pay again and again.

Fire the gerontocracy! 89 year old people (Feinstein) belong in a rest home, not making government policy. The Geezer in Chief is another example.

Tradesman here. Time on site is no proxy for work time. Materials markup covers cost of doing business. A normal workday in many trades will consist of 3-4 billable hours. The other time gets eaten by travel, organizing tools, paperwork, “free” evaluations, phone calls, texts, emails, payroll, taxes, every busy-body in the parking lot tying you up for 15 minutes with questions, trips to supply houses, restocking the van, training on the latest and greatest technology and techniques, licensing requirements and keeping up with changes, poop breaks (got a 5 gallon bucket? No time to stop before I get to the next job, back of the van is as good a place as any to go), fetishizing over new tools, pestering from the wife (smartphones suck), trading pictures, questions, questionable material and complaints with other tradesmen (smartphones are awesome), and far too many other things. Sure I showed up and fixed whatever problem you had in five minutes, but no one pays me a salary to sit at a desk for 8 hours. I can’t make a living charging you $25 for something you could do yourself with a $5 part!

dont forget the time it took the tradie to answer the call, travel to and from your neighbour’s and then dispose of the tank probably 1.5 – 2 hours, no way did he earn $950 an hour

…that’s one of the banes/attractions of DIY – you eat your own overheads…

may we all find a better day.

Firstly, I have no problem with your sentiments which seem to be strangely familiar.

I wanted to take the opportunity to expand on a concept that you cited, equilibrium. An elegant concept, that has been shown to be mathematically correct about chemical reactions, the Gibb’s free energy of formation.

Hardly a description of the financial markets. A collection of good hearted hucksters, I suspect.

As far as the introduction of AI into the hive as being a threat to humanity, I’m currently withholding my judgement which is that this is not going to end well.

Every person will have an alter ego that is more nasty, more dogmatically insistent. If one were ingenious by nature, they might discern a potential conflict between programmed machines and human beings.

All anyone sees with AI is dollar signs or the toy that keeps on giving. Alarm bells over technological shifts have been raised in the past to little effect.

It seems to me that art is the designated victim in the next iteration of the world rotating on it’s axis.

I’m concerned that artists, notorious truth tellers, will be accosted by a machine demanding that we perform some kind of procedure that conforms with a protocol thing that has been ordained as the way we do things.

A grey, dreary dystopion future without hope is what AI offers.

Why ? Because the people promoting this technology have only monetary profit in mind when they really should be considering the damage they are doing.

Let’s pool our collective intelligence and imagine the benefit that the current release of a digital predator into the soft environments of our communities. I don’t think it’s a good idea either.

The ability of monetary stimulus to incite irrational buying of worthless company stock, which has been amply exhibited on this site is an example of consensual hallucination.

It is not AI, it is fake AI. It is code on how to write a sentence correctly. Basically it googles the info and then spits it back out to you in a fancy sentence. Not AI.

Speculators are still loading up on land, while at slightly lower prices and volumes. People have zero confidence in the FED and the dollar, preferring to spend the money instead of hold it. What good is a 5% return on a CD or treasury when you’re still losing a few percent a year to inflation?

This situation is far from over, and now everybody is screaming FED pause or pivot. There’s one thing that I think is guaranteed – the value of the dollars in your bank account will continue to erode in rapid fashion. They’re stealing everything.

This mentality is partially what has caused the housing super-bubble. This latest housing bubble began in 2014 with massive QE that was in response to taper tantrum, but otherwise no Main Street crisis in sight.

The response to QE and ZIRP was to dump all the liquidity into housing, driven by a reasonable fear of hyperinflation, turning the existing bubble into a super-bubble.

If this hyperinflation does not come to pass, interest rates remain high, and QT continues, there are absolutely zero fundamentals that support the current housing prices. Not demand. Not “lack of supply.” Not lack of building, supply shortages, land shortages, or any of the other unfounded excuses pushed by real estate propagandists.

Housing is one of the most irrational asset classes, driven by delusional, magical thinking such as “real estate always maintains its value or goes up.” Much of this is due to confirmation bias from people who already own real estate and have much of their own net worth tied up in a highly leveraged illiquid asset. They *can’t* bear a housing market crash, or they will be ruined.

The housing market right now is like Wily E Coyote in the Road Runner cartoons. He runs off a cliff and briefly defies gravity, floating in the air, until the moment he looks down, thereafter plunging into the abyss.

“”there are absolutely zero fundamentals that support the current housing prices”

LOL, as you will see as “fundamentals” in many of the comments below to counter this point. So and so just sold their house for X over or close to asking and there are 18 buyers waiting, it was sold in less than a week. Listing is still too low and everyone is jumping at buying ASAP…

In this age of insanity we live in..maybe anecdote is about the same as fundamentals

I do think Joe blow is still “awash in money” in his head. It is a fantasy every middle class $156k+er is living in”

Taylor Swift’s Eras tour is not worth $800-2000 people.

It’s just not, it’s a stadium. She’s using you.

I’ve often wondered who pays that kind of money to see any performer or ball sport. I still remember sitting in a bar in San Diego with two Stupid Bowl tickets in my pocket. Some scalper came through and offered me $2K for each (this is in the 90’s) and I took it. My wife wondered why. I told her we could buy the best TV on the market, watch the game (if I gave a wet crap about it) and still have the TV when the game was over.

These people are trained monkeys. I’ll toss a quarter in their hat, but not make them bazillionaires so they can infuse me with their virtue signalling. As the Dixie Chicks were told back in the GWB days: Shut up and sing or your life will be over.

The best bands with a handful of exceptions are best seen in a small to medium club/theater. Stand as close as you like, meet the band at the stage door after, maybe the singer will hit you up after his set, or so I’ve heard.

What boggles my mind is how people can afford these tickets without pulling out the plastic and paying for it for months thereafter. A fun night out every so often is nice, but it seems paying these excessive prices for a few hours entertainment from mega pop stars is chasing the dragon and feels like a sign as a population we’ve approached max saturation of the consumerism high.

I ended up having to rent a house again after renting several tiny condos while waiting for some semblance of sanity or at least stability to befall the housing market. Expensive as hell and yet I got lucky in that its a real nice place for the price and area. But gotta admit, rent or own, being in a house is not a huge lifestyle improvement, just different. More space, yard for the kids/dogs, but more upkeep and money. The experience does not justify locking in a 6%+ mortgage for 30 years on a house worth at least 40% less than you paid for it. In my opinion, anyway.

Still holding a tiny sliver of hope all the city evacuators will flock back to their old defaults in Brooklyn and realize AirBnB is going downhill, free up the housing around here again. AirBnB is one of the worst thinks to happen to affordable housing shoppers next to black mold and foundation issues.

There is a simple reason that the delusion of perpetually rising home prices is so firmly ingrained…because it has worked for many decades, with only brief pullbacks.

But we have hit an inflection point. Interest rates cant/wont drop down like before and incomes are stretched to the breaking point to purchase a new home. There is simply no more room for people to buy into the market at higher prices.

It will take a good long while for the mindset to change. Housing is now a poor investment over the long term.

And…..You have to live somewhere.

Or they have to change their expectations of what a house should be….. It might not be that 3,000 square foot custom home with an ocean view. Might be 1,100 square foot 3/1 on a 5K lot with formica countertops.

For those who are old geezers, what was your college dorm like? Mine was concrete block walls, gang showers, and a bed and desk bolted to the wall. Vinyl flooring. A 4 drawer dresser (also bolted to the wall) and a closet the size of a gym locker. No pool. No lounge. No sushi bar. No nail salon. No nuthin’. Compare that to today’s university housing.

with lenders now full of systemic risk, you would think a loan could be very hard to come by soon. All the risk of the bubble is concentrated in the lenders. They allowed these valuations to stand and loaned up the valuations. The buyers just rode the FOMO bus. But the buyers can just salvage their money and walk away leaving the banks the bagholders. Alot of guilty parties here but the Fed is guilty. Imho when the systemic banking crisis hits from repricing, the Fed cant save as before because of inflation going to hyperinflation. My view is hyperinflation is worse than depression because depression is just an extreme cleansing of a cycle whereas hyperinflation is the end of the fiat currency and the end of the Fed itself. So without intervening equilibrium will settle to the mean: incomes..just like it used to be. A true fundamental. According to this fundamental after the massive layoffs upcoming do the math to see what houses will be valued at. What is the average household income of your city and how much house can that buy at 7%?(remember average household income AFTER massive layoffs)).

El Katz, there are plenty of us buyers who would be perfectly content with a 2-3br/1ba with formica countertops, in fact, its all we’re trying to buy.

Unfortunately, every idiot with HGTV and cash to burn has bought them all up to be AirBnBs or otherwise overpriced rental units. The ones those people won’t touch are completely unmortgagable partial or total teardowns which most can’t take on, and wisely so.

Many low to moderate income home shoppers are just seeking stable housing and to get out from under a landlord, not investment property or an IG yuppie palace. Like said above, you have to live somewhere, even us peons.

I love how everyone here talks about finance and stuff, but can’t you see how all of lies and so forth are spilling over into every other aspect of society? Bad money pushes out good and so forth, but i think you can apply that to everything in society. Bad actors push out the good and then everything collapses

Take another Xanax and relax. Everyone living in this country is very lucky to be here. America is the land of opportunity for those who are willing to work hard. The lazy people in this country will always have an excuse for their failures…and they will always blame someone else.

Read up on toxic positivity, sometime. You’re lousy with it.

Myopic comment. There are a lot of people who work hard and scrimp to save. I worked hard to attain my BSN( putting myself through school in my 40’s) and worked all through the pandemic in the Covid ICU. My wife also fell ill and has been unable to work since 2015.

I am no slouch and always try to do the best I can at work, but I am falling behind. My paycheck has been gang raped by inflation and I am losing financial ground daily.

So am I lazy? Or has irresponsible monetary policy and an unfortunate illness caused my struggles.

Be careful when you make broad and ignorant generalizations like that

America used to be the land of opportunity for those willing to work hard. Now it’s more like the land of opportunity for those already born into wealth, and the land of just getting by for those willing to work hard. Case in point, the median rent in the US has risen by more in the last three years than the median income has since 2000. In those 23 years, median rent has doubled and median home price has tripled, while median income hasn’t even breached a 15% increase. Couple that with sharply rising costs for other basic necessities, like food, healthcare, utilities, transportation, and healthcare, and we’ve got a disaster in the making.

Sure, some people are just unmotivated and there’s little you can do about that, but when 2/3 of the country is living paycheck to paycheck, that’s far more indicative of systemic problems than laziness.

It has often struck our notice that the course our city runs

Is the same towards men and money. She has true and worthy sons:

She has good and ancient silver, she has good and recent gold.

These are coins untouched with alloys; everywhere their fame is told;

Not all Hellas holds their equal, not all Barbary far and near.

Gold or silver, each well minted, tested each and ringing clear.

Yet, we never use them! Others always pass from hand to hand.

Sorry brass just struck last week and branded with a wretched brand.

So with men we know for upright, blameless lives and noble names.

Trained in music and palaestra, freemen’s choirs and freemen’s games,

These we spurn for men of brass…

-Aristophanes “The Frogs” 405 BC

Sounds like Jack Sparrow NGL ;)

It seems like the Tech crowd really has lost their mind. Buy a Tesla at ridiculous rates. Worship anything Tech, follow musk’s every bowel movement with vigor and awe. Put 1/4 of your salary in crypto. Ask Chat bot what you should wear today? These people are nuts.

me thinks, SVB lived and breathed this culture too much.

Real estate prices are falling faster than they appear, because our level of underreported inflation means the prices are declining more in real dollar terms. That said, the lower size of Gen X (so they will demand higher wages and get them) means, in popular areas, the prices will not fall as much but only until they decline to levels affordable to them, as more and more millennials must sell their real estate due to their limited retirement savings. Luxury real estate will fall more. Whatever you do, unless you are a tech-savy drug lord (LOL) who needs crypto mining to launder drug profits, avoid cryptocrap!

My tablet’s crazy auto correct must have been produced in Germany because it keeps auto-capitalizing words as in German. LOL

Well, speculators have been able to work their way to the bottom of the totem of admiration let alone the jealous inclination every one of us feels about the super rich.

‘It hasn’t reached the level of the Russian revolution where they killed the royal family. There doesn’t currently be a need for such draconian measures as insurrection. Like every American that ever lived, I lived through the propaganda that defined acceptable or not.

Prices are far too high for most prospective buyers, unless they already have substantial equity.

I’m a current renter due to personal reasons but have done the math. I can buy lower housing costs through a higher down payment but most people without substantial home equity can’t, making them debt slaves whether they realize or admit it or not.

I’m not referring just to P&I either, but “all-in” costs.

I too am a renter by choice, sold my house 2 years ago for way too much. (poor couple). Real Estate taxes have to be killing them vs. what I was paying.

Waiting for prices in AZ to get closer to pre-pandemic. Tracking homes and have seen markdowns 4-6 times totaling $ 40K or more just since October.

Questions, seeing a lot of UCB (under contract) then boom back on the market. Wondering if lenders are starting to get skittish of the overvalued asking prices and appraisals not coming in where expected?

I sold my Phx house October 2021. Made me an offer I couldn’t refuse. I too am renting by choice and waiting. Yes, prices are going down but have a lot farther to fall before I’m buying. Still way too expensive.

I also looked at some listings this morning and saw several

go pending, then get relisted within a month. I assume the buyers got nervous and walked from the deposit, or the dwelling couldn’t pass inspection, or the buyer couldn’t get a loan.

There is reason for nervousness in an overpriced declining market with thin volume. Big price moves can happen, and the trend is down.

I’m noticing that as well, many back on market. I’m thinking you are correct on lenders,

I am in AZ and see that too. Some joker took their house off and came back with a higher price and then is currently walking it back down. Not sure if this summer will be a good time to buy a small condo, I need a place to stay and am tired of my apartment raising rent on me each year.

Rent a bedroom,from a empty nester = double win

The home owner’s insurance, HOA fees, and property tax shock is coming in right now. Seen tax bills go up in certain areas in my locality (small city) experience as much as 60% increase, particularly in lower income areas. More “reasonable” increases in higher income areas around 40% increase.

Credit card debt is piling up, variable rate student loan payments are soaring, food prices high, gas prices high…and as Wolf has shown, people are outspending inflation with revenge spending. My car insurance bill jumped by 20% from six months ago. Budgets planned in 2021 are getting smashed.

PBS just put out a great documentary showcasing the Fed’s poor decision-making since 2008, where they interviewed the leader of a Food Bank in LA – there are more people collecting food now than during the height of the pandemic.

Because of all the programs available, foreclosures are taking nearly a year from first delinquency to eviction. The last of the rental assistance ended in Summer 2022. Since then, local rental units I’ve been tracking (small urban area) are already down 20% and still falling. In other words, rents are already falling, though no one is reporting on it.

This is a slow train wreck in progress. A very slow train wreck.

That PBS documentary is pretty well done, it released at perfect timing too after the whole debacle at SVB.

To hear them interview Neel “the devil” Kashkari and the tone-deaf comments he made about jobs and their policy…the FED should just hide him in the basement to not further embarrass the little credibility they have left.

“That PBS documentary is pretty well done, it released at perfect timing too after the whole debacle at SVB.”

Was it? I watched the first 15 mins and turned off in disgust. You guys didn’t notice how they were rewriting history with regards to 2008 and onwards?

Yeah that timing was super convenient wasn’t it……….

Anybody notice lately how its always the government and the corporations who start all the panics the last two decades?

Phoenix, I agree. Good documentary. And it showed how both Bernanke and Powell bent under the pressure of a stock market tantrum. Added to it was Trump slamming Powell for raising the Fed rate and threatening to fire him. I’m confident that Powell never “needed” the job but just didn’t want to be thrown out and humiliated.

You must have noticed that Kashkari had an answer before the interviewer even finished his sentence. Pure rationalization. And an ego bigger than the great outdoors.

Phoenix_Ikki,

I live in Minneapolis where Mr. Kashkari presides over the Federal Reserve Regional Bank. He was in the local paper yesterday with an interesting take on Governor Walz’s proposed rebate checks for the state’s budget surplus to be dished out to Minnesota citizens.

From ‘Could Minnesota’s proposed rebate checks fuel even higher inflation?’ 20 March 2023:

“Federal Reserve Bank of Minneapolis President Neel Kashkari has said it has given him pause as states in the region, including Minnesota, consider using a portion of their significant budget surpluses (over $17 B in MN) to distribute rebate checks to residents.

“As a taxpayer, that sounds pretty good to me. But as a monetary policy maker, that sounds like more stimulus. And that’s putting more money in people’s pockets to go out and spend on airplane tickets and food and buying things.”

He added, “On the margin, it’s probably a little bit inflationary and makes our jobs a little bit harder.”

Kashkari has no say on what the DFL (Minnesota Democratic-Farmer-Labor Party) House, Senate and Governor do in Minnesota. But he does have a vote on the FOMC this year. Tomorrow will be the day we find out what’s up with the Fed’s rate policy. Neel will have his say.

HowNow,

Neel is one of the engineers who designed the guidance system for for the James Webb Space Telescope. He has a B S & M S in mechanical engineering. Yeah, the dude really is a Rocket Scientist.

DanRo – rocket scientists where (to shamelessly borrow from other commenters) mebbe rocket surgeons or brain scientists might be better employed…

may we all find a better day.

“there are more people collecting food now than during the height of the pandemic.”

Same in far northern Ca. In addition there are tons of empty storefronts. 2 towns in particular look like a deep depression and other towns are creeping down there. I think there are more empty storefronts than in the worst part of the GFR, but then, the wholesale pot industry has been sinking like a rock for the last 3 years or so up here. It’s been taken over by large companies that think they can afford to sell wholesale below cost sometimes because of money coming in from their stocks. They were aiming to “control the market” rather than make much of a profit.

clarification; more empty storefronts in those 2 towns than during the worst of the GFR.

Are there more store fronts? Or are the failed enterprises something worthy of survival or just a hobby that could never generate a profit? Beanie Baby, record, and books stores were hot at one time too….

Is the location suitable to the product? I watched a TV show last night that featured a “scent library” business. WTF is a scent library? I can’t imagine that store lasting more than 90 days (and it will only last that long if it was capitalized to last 90 days). It won’t last 5 minutes on it’s own merits.

Property taxes in general do not go up with assessed values. The taxing entity has to increase their budget for taxes to go up. My assessed value went up by $150k for 2023 but my property taxes are virtually unchanged.

In locals with property tax rate pegged to valuation, say 2-3%, the taxes go up automatically. When prospective buyers overpay, they raise the taxes for the entire neighborhood.

Petunia, No they don’t. As the assessed value increases the tax rate goes down. The taxing district votes on a budget then, the budget is divided by the assessed value of all property in the district to determine the rate.

It depends on the laws of municipality. Some can, and do, follow assessed values. Others don’t. Lived in both kinds of environments…. Prop 13 in CA didn’t give a rat’s patoot what the budget was. It was capped. OR? Not so much.

In low tax (sic) Texas, properties are taxed on the assessed market value. They are assessed every year.

Your assessment goes up 5%, your taxes go up 5%.

But people are still out spending like drunken sailors. Try booking a flight, or a cruise vacation, or a hotel stay, or even go out to dinner.

And the inflation on those things is ridunkUloss. Perhaps all the demand is what is making them inflate so much? There has to be a terminal velocity reached for these people to stop traveling.

Interesting, I just jumped ship on an old auto policy. I saved $800 a year.

Perhaps, shop around.

Let me know what happens after you make your first claim.

Excellent is more appropriate. Gave a very clear analysis that is easily understood by people with little or no idea of what has transpired over these last 15 years.

“The median price of all types of homes sold in February, at $363,000,”

How many jobs does a Medium wage earner have to work to afford that price?

Renters in apartments will do ANYTING to get into a home. Apartment living is getting unbearable.

renting v. buying is one decision.

Living in a crummy place v. living in a nicer place is another decision.

They can move to a higher-end rental apartment or house. Or they can buy something, but that’s not a 100% cure either. Lots of homeowners don’t like where they live, and don’t like the house they live in, constantly complain about all kinds of stuff, and regret having bought… documented in lots of surveys.

The different issues have to be separated.

This is a very good point that many dont understand.

I live in a house that has had subsidence issues caused by trees in neighbours gardens. Both neighbours have refused to remove the trees. The insurance claim has been going on for eight years and the homeowner has had to pay for investigative work out of their own pocket.

Last month another part of the house also underwent subsidence movement which will be a separate claim.

I bought a pretty nice Townhouse in Tucson to stay in while I build my Winter house. Rental apartments seemed overpriced and not very appealing, plus I’m 72 and have never rented a house or apartment. I bought my first house when I was a college student and rented out rooms…..

“Renters in apartments will do ANYTING to get into a home.”

Until buyer’s remorse hits.

72% of recent buyers have regrets about their purchase, and almost all the reasons circle around paying too much or having to rush the process, in other words, they regret “doing ANYTHING” to get into the home.

I think if you can — you’re probably better building a place from scratch. You have considerably more latitude over the situation & materials used, and can possibly even collaborate on the design phase, depending on your aptitude for such things. Might be more of a headache & more expensive than buying an existing equivalent, I don’t know; but I can see how the connection one might develop with a unique space like that could prove profound; of course, the tradeoff is the inevitable heartache of getting too attached to something like a place over time. Places change; people change.

If you’ve got the stomach for it, it’s better to be perpetually passing through. That’s all any of us are doing anyway. Too many landscapes to breathe in in one lifetime to lock into just one — especially some blah little cul de sac in suburbia. Comfort is the enemy of adventure! The older I get, the more I think Dr. Dorian Paskowitz had the right idea(s).

A good life goal might be to ensure that the last thing you glimpse on this planet is not the sight of some ugly ceiling fan as you stare up at a popcorn firmament toward eternity.

bf:

If you’ve never built a house, you don’t realize the compromises that have to be made to meet budgets.

My roofing dude started out building a house on land he owned. Then COVID hit. His lumber package escalated to stupid heights. So, trying to dodge a bullet, he went to ICF as a substitute. Took months to get the plans approved (not counting the redraw and engineering). Original budget was @ $1M. He’s currently busting $2M in Cave Creek, AZ. He’s 38. Sold everything he owned (rentals, cleaned out his bank accounts, and took a hard money loan). Watching the horizon for wisps of smoke.

My formula is buy a view with a house on it. The house can be changed. The location not so much.

And I find it hard to believe that 72% of people regret their home purchase. I guess their caviar dreams didn’t match up to their White Castle budget.

72% of buyers have remorse?

ROFL, I have NEVER met anyone who said I regret buying a house. Let’s say you don’t actually like the house or the location, just the fact that your equity doubled over the past few years makes buying versus renting a no-brainer. What have renters to show for besides ever increasing rents? I absolutely hated renting. Never ever will I go back to renting.

Carlos, El Katz,

Forget the Utuber (I watch quite a few) but he cited a survey: buyers remorse at 65% (67% ?). Pre pandemic was 35%.

He then went into detail as to what were the factors for the remorse with associated percentages.

Yah, it’s over 70%, I was surprised, but here it is, reasons are mixed….

https://www.cnbc.com/2023/03/11/75percent-of-americans-who-moved-last-year-have-regretsheres-the-no-1-reason-why.html

I’d love to live in an apartment but waiting for kiddos to be out. few more years.

I am a home owner and I think SFR living is over rated.

Apartments blow. They kick down the door to come in anytime they want to “check on things”. Wake you up at all hours. If you are a people person its ok, but you have to go by their whims. If something big breaks, its a while to get it fixed. Overall it is OK, but owning a home is much better IMO. You are treated with much more respect.

Speak for yourself. I’ve been paying the same rent since 2019. I would be WAY poorer if I owned.

Why would you expect a median earner to afford a median home? That implies that everyone, from the lowest earner on up, can/should afford a home. I think (hope) we can agree that the lowest end of the earnings distribution, the young workers especially, can’t be expected to afford to buy a home.

A few inconvenient facts. Back in 1996 when the minimum wage was $4.75 an hour which is about $10k annually, I bought a house for $30,000. Making a little more than minimum wage, it would have been possible to actually afford a mortgage on that house. So the idea that you need to be some sort of high roller to afford a house is a relatively new concept. Less than 30 years ago almost anyone who had a job could afford to buy a house in Texas. Will we ever see those days again? I doubt it and it illustrates just how this country has been destroyed.

According to Wikipedia 50 countries have higher homeownership rates than the US.

Yes some of these countries don’t have the greatest homes, worse case many are what we’d call shacks. But Taiwan, Singapore and Norway all have high standard of living and are over 80% (Norway just over 80%).

We are at 65%.

China is at 90%. Oh but they overbuilt perhaps, other issues, etc.

If the survey is accurate 90% is considerably higher than 65% (and probably falling… investors to contend with today who rent them out).

Romania at 96%, about 15 to 20 countries over 80%.

If apartments were all of stellar condition in the US it could make a lot of sense to rent.

My apartment is from the late 70s, early 80s.

Its fine for me except not sufficient sound insulation between floors, top and bottom.

Only a problem with one tenant (I’ve lived here 23 years, had about 7 people below me over that timeframe).

But with China at 90% I contend they have bragging rights. Some homes are quite small I understand but on the other hand they probably are newer than our homes (US) on average.

If indeed 90% of your population owns a home … it makes it more likely the median wealth person can own a median priced home.

To your point… suppose the US thirty years from now is such that only the wealthiest 30% can afford to buy a home. Then the median wealth person cannot buy ANY home let alone the median priced one.

Aside: The Chinese ( I believe) don’t own the land. They do however pay off their property taxes upfront at time of purchase.

So while the US person owns the land they will always pay property taxes on it… so the land ownership seems not a reality in practice.

You really don’t want to live in a typical Chinese “home”. Just saying.

In many of the countries you mention a “home” is an apartment in a big block of flats. We are not talking a “house” like in North America.

In general people are willing to put up with less privacy and less space than in NA. Lived in Asia for a while in a rented 4 bedroom 2 bath flat, that we rented out three bedrooms in, including to couples at times – so 6 people in the place (washing machine was on the balcony). We did this while married – and saved a lot, but gave up privacy. How many folks in NA would willingly do this?

You believe data out of china. bless your heart. ;)

In addition to what James Woodsworth says, the culture of moving around the country for work is much stronger in the US than most countries, particularly the countries you cite. There’s probably no reason to ever move for work in Singapore or Taiwan, and even in Norway the population is small with only a few significant population centers. For a lot of people in the US, many of whom can afford to buy, renting just makes more sense because of the flexibility it provides and the high transaction costs of buying and selling a home.

I’m a proponent of home ownership because I think it invest a person in their community, but understand it does make sense for a lot of people for personal and economic reasons. I don’t know the details, but also suspect that other countries have much more multi-generational living where a home stays in the family and keeps getting passed down. Except maybe in Hawaii, that’s not common in the US. It raises the question, if a young adult moves from a rental back to a house owned by their parents, does that effectively increase the home ownership rate by removing one renter?

China is an oddity because I believe the government still owns the land, as you note, and controls migration between the countryside and cities. Is it “ownership” if you don’t own a key component of the property? These dynamics make it difficult to compare homeownership to the US.

That’s one-half of the problem.

The other half is that I’m never buying into an area of town or a neighborhood in this price range or noticeably higher, as it isn’t what it used to be.

Why season the discussion in this murky think tank-y language? It frames the would-be US homeowner as a kind of presumptuous and/or — dreaded of all dreads — entitled a-hole.

I’ll say it, and probably nobody’ll agree with me — every American should have a crack at owning their own little patch of blue, especially if home ownership is going to be relentlessly promoted & elevated in the manner in which it is in this country. Renting is a strategic move, and often a damn’d shrewd one. Why buy the cow?…

However, when it’s the only game in town because every wannabe uncle pennybags and their second nephew buys up SFHs in what might otherwise be a homespun community in Anytown and then goes on to sublimate his or her lust for passive income as some kind of wholesome grassroots utility to the masses…well, screw that jazz.

In the words of the other Lebowski: Get a job, sir. It’s actually freakishly easy these days.

Well, maybe Uncle Pennybags had a plan and the other guy didn’t. That might make the difference.

I don’t know how many of you kept track of your neighborhood friends, but I did. Most are broke. A few did prison time. Some died (one drowned working on ship propellers in LGB, one didn’t last 30 seconds in Vietnam (got shot as he got off the transport), another died in the WTC. A few did extremely well (those with stable relationships). The rest? Probably eating cat food.

It’s all choices. I learned long ago that, for me, the pursuit of “stuff” was far more rewarding than actually catching it. I have a few investment vehicles… which were sleds when I bought them, but things changed. The E30 M3 that no one wanted in the 90’s is now a 6 figure car. Original. Low miles. Right color. The E36 isn’t far behind and the goombahs destroyed eligible E46 M3’s and a pristine one with a third pedal is worth more than it sold for new. Would I buy any of them at today’s prices? Not on your life.

Housing is the same thing. Look for the opportunity. I’ve never bought in the “A” location…. I always bought in the “A-” location. Same amenities, same schools, 5 minutes away. Different zip code? Fine. No non-correctable defects (like freeway wash or airport noise). Less cost of entry and higher upside potential.

Oh, sure — plans are all fine & well, particularly whenever the goal posts aren’t on roller skates and the playing field isn’t on fire.

Plan dinner; live your life.

Thanks and agree with every comment above me. THEY sure did screw things up.

Wolf, and others, my friend recently used a program from AnnieMac Mortgage called Cash2Keys to purchase a house. Have you heard of this? If so, can you explain if I am understanding correctly?

As far as I can tell, a branch of the lender (AnnieMac Private Equity) submits an all-cash offer on behalf of the borrower (to me, an ultra short-term loan) for a fee of about 1.5% of total price/UPB, which is then “forgiven” if AnnieMac provides the actual mortgage. What are your thoughts on programs like this?

I have no thoughts on this. And I’m fine with having no thoughts on it, LOL.

I was outbid on a vacant townhouse in NY (seller used it as a rental) last year by someone using a similar program, looks from Google that C2K is NJ only. Listing agent made sure to communicate my offer was higher (FHA), but the seller preferred the faster cash transaction because he wasn’t collecting rent on the place.

Three months later I get a call that the seller was considering my offer again and would get back to me by day’s end. Apparently the seller had waited, waited, and waited, but after the buyer couldn’t secure the cash loan and ran out of excuses the seller finally backed out of their deal. Mind you, we would have closed inside of 45 days buuuut I’m not bitter. Anyway another all cash buyer swept in at the zero hour and Bob’s your uncle I’m still renting. I assume the seller kept the earnest deposit.

Based on that I would deduce that kind of financing could potentially be more of a headache for the seller than straight cash but I’m not sure if the sellers know its not a straight cash deal from the jump. And seems pretty risky from the buyer’s end upon review of the C2K program.

Musk is out screaming for a half point rate cut with CPI over 6%. Ackman is calling for a pause. The billionaire oligarchs are putting the screws to Powell from all angles, with the help of politicians like Elizabeth Warren. The little people have no chance in this system.

If the FED does cut, all the speculators won, and they will poor into all risk assets, and assets period, which includes housing. This will set fire to the inflation inferno and accelerate the full scale destruction of the country. All bets are off at that point as to what the end game is, but it will not be pretty.

Musk is funny. He borrowed a HUGE amount of money — something like $13 billion — to buy Twitter. And rate cuts would hugely benefit him and his baby, Twitter.

These people are all the same, Ackman too: when they open their mouth, it’s for the exclusive purpose of manipulating things into their favor.

If you want to know what’s good for them personally, just listen to what they say.

They’re really nauseating, and I can’t stand them. But you said it yourself, Wolf, something like “there is no greater power than 50 billionaires.” I have never been so disenchanted with the entire system in my life. The more wealthy these folks became, the more power they wielded over everything.

“there is no greater power than 50 billionaires” is the first part of my statement. The second part is “with big megaphones.” The second part is crucial too. Both Ackman and Musk have huge megaphones, particularly Musk. When they say something, it’s instantly dished up via social media and MSM to just about everyone out there.

2, 4, 6, 8

If not a billionaire

You don’t rate

Go team!

“The more wealthy these folks became, the more power they wielded over everything.”

Why do you think they want CBDCs so bad?

Enchantment has its time & place, to be sure — but the shits being shitty sure does furnish some good grist for things like introspection, philosophy, art, comedy, and – more generally – new ways of thinking/modes of knowing. The front burners have never been as hot as they are now in my lifetime. ‘08 was just a bit of gas…I say, let the bastards & their stooges do their worst if it brings out your best.

bul – my man.

may we all find a better day.

LK,

You’re right about philosophy. When I watch and read the news, it is frustrating as hell, and easy to get pissed off thinking about it. But, we can’t change world events at an individual level.

What we can do is enjoy life and take pleasure in each day. That’s my philosophy.

El Katz has it figured out about finding a home with a view and location. My one and only home owned, which was bought 28 years ago, has that. Life is good.

Crybaby is going to cry, normally it would be a non issue if our government would just ignore this Ahole and the any billionaires like him. Unfortunately that’s often not the case though…

Btw, if Pow Pow does cut now, someone needs to “tattoo” Arthur Burns 2.0 on Pow Pow’s foreheard, Inglourious Basterds style and give him a collar and leash to wear so his billionaire friends could use it to take him for a walk..

For a guy that claims to want to do the right thing to fight inflation and one that’s representing an organization with very little credibility, let’s hope Pow Pow doesn’t sink that low.

Powell capitulated to corporate interests twice already, I’ll be pleasantly surprised if he doesn’t this time.

Same thing here in Canada with the real estate agents imploring the BOC to cut interest rates.

They want the neverending housing bubble to continue while food prices increase every month due to inflation.

Just remember that when there was outrage during the disability benefit freeze in 2018, a Minister replied that “the best social assistance is a JOB”.

And in 2022, in response to the cost of living crisis, the deputy PM insinuated “Have you cancelled your Disney+ account?”

But to cut interest rates to make loans cheaper for billionaires, that would anger the French people a lot.

Seems to me the real estate people should realize that the lower the prices, the more buyers can qualify for. More buyers means more commissions (in the future). Simply short term thinking.

Not sure about other countries but here in the UK you don’t need any qualifications to become an estate agent.

Many of the overpriced homes were purchased by real estate agents for speculation. They figure they are always ahead because they don’t pay full commissions to buy or sell. Now with high interest rates, they can’t sell at a profit, and cutting prices is not an option for them as well. They need the rate cut to get out of their investments.

The real estate people don’t thrive on churning numbers of “ups”. They thrive on the commission on high end properties. What’s more work? 6% on 4-$250K properties or 6% on one $1M property? Who’s more likely to not give a wet crap if the property needs updates/repairs? The poor guy selling his wife to afford a $250K house or the guy/gal buying the higher end property that knows they’re going to gut it anyway?

I always buy good bones that’s ugly. Paint, moldings, door and cabinet hardware goes a long way. Watch trends. The porcelain “wood” flooring is the new Nehru jacket of housing. So’s the Home Dumpo backsplash tile that looks like a bucket of Lego’s threw up.

I’d be so happy if we could get rid of the current realtor business model. They have everyone convinced they need a realtor, and they don’t. Still trying to understand why I am paying a commission for someone to advertise my home on Zillow which anyone can do. In AZ, the RE forms are preprinted. It doesn’t take a genius to read the GD forms and complete the transaction. Hopefully, one of those NAR class action suits wins which many say could upend the current business model. One can hope.

In Canada, the real estate industry is like an oligopoly.

Even using the world r-x-a-l-t-o-r is a word that is a trademark by the Real estate agents in the industry.

Bloggers who are critical of the real estate bubble get sued for using the Toronto Real Estate Board trademark believe it or not.

I believe a lawyer that specializes in estates is cheaper. There are also services where you can pay a minimal amount to have your home listed in the “listed by agent” part of the listings. Which get more views. They then refer calls to you.

I concur, Fed up.

How about when you want to sell you show up at an advisory office. They help you put a price on it and point you to resources to list. When you have a buyer, both show up at the advisor to check all the boxes like whether you’ve had an inspection, and to cover a few basic things that the lawyers bury in those pages. And then fill out the paperwork. Should cost maybe $1000 for the service instead of 5%.

Yeah, ok, I hear the claims of “value add” and how clients will overpay or sellers will sell too cheap. I’m sure there’d be some inefficiency, but the savings would so far outweigh that. What do Americans lose in commissions per year? I would guess $50 billion. WASTED.

You can easily get rid of it. It costs about $400 to sell a home by owner. I have sold 4 of my own and 3 of my close friend’s homes this way. Sign a contract and mortgage company does the rest. It is really quite simple.

All u need is a title company ,really easyRealtors are biggest SCAM ever

A good realtor is worth the cost. They can get stuff done you can’t even imagine. The last one held a deal together that netted me just shy of the cap for married filing joint (aka $500K). The rest was “off book” in furniture and contents (that she got a chunk of).

The purchase of a home is an emotional purchase, not entirely (or rarely) logical. Someone has to hold that illusion together to maximize the profit. Our last home was sold to a couple where she was preggers…. and their whole goal was to get into a house prior to her dropping the kid. We’d have never known that without her.. and the entire transaction was orchestrated around that reality. That little tidbit paid her commission as we garnered a higher price because we were flexible.

However, a shi**y realtor isn’t worth the powder that it would take to blow them up.

Your mileage may vary.

Real estate salesmen don’t care about prices. Prices can go up or down or stay flat. It makes no difference. They care about selling. Thats why theyre called real estate salesmen… duh!

As a matter of fact, they hate markets like this, not because prices are falling, but because nothing is selling. Sellers want too much for their homes. Buyers think the market is going to zero. So theres a total stalemate and nothing sells.

No sales = no commissions = no income. It has nothing to do with the direction of the market.

You really don’t know much about selling a house, do you? Realtor’s always stretch the price…. they make more money that way. Especially if you, as the seller, incentivize them to do that very thing.

I love naive people. (Realtor’s don’t care about price…. Hahahahahahahahaa!)

CCCB, I think you make sense, El Katz not quite as much.

Although it depends on the market !

2020-2021 re agents were apparently in the driver’s seat. Probably many got greedy because … well they could. And STILL made a relatively quick sale.

So yes push the listing price hard… with so many buyers you might get it and get it in just a week or two or three.

But me. 1995. Took me 5 to 6 months, mid February to early August to sell my home. Realtor for 4 months, FSBO last two (with buyers agent). Sold for 8% less than original purchase (new home, 1986, in very good condition). More of a buyers (maybe neutral) market.

If its a slow market my guess it makes sense to get the seller to lower the price so you can sell it ….

rather than not.

Example:

400K house. Per appraisal say.

Its a neutral or buyers market.

Re agent would seemingly be better off selling the house in 3 months at 390k rather than 9 months to squeeze out say 405k. Lose $400 to 800 commission but if you can thereby triple your sales you’ll be way ahead (5% commission:

3 sales in 9 months w/ each having a 19.5k commission versus one at 20.25k.).

Thats a big maybe, tripling your sales, but the idea is clear. The extra (2) transactions can greatly outweigh the small loss on the per transaction commission (750).

So as is often the case it is somewhat situation (context) dependent … something that is under appreciated in our society. Stated differently, people too often overgeneralize.

There is a whole chapter in Freakonomics about whether realtors work to get the best price, or just push to make the sale, get paid, and move on. Spoiler alert, the are not your friend.

Both buyer and seller RE agents want the house sold to collect commissions.

They have to be better psychologists than salespeople.

I’ve had some friends back out of houses after inspection due to the trauma of finding 5K in repairs needed on a 300K house. The buyers want the 5K at closing and the sellers don’t want to give it. Both the buyer and seller RE agents wanted to close and collect their commissions. In this case, both the buyer and seller RE agents were not good therapists. and the deal fell through and nobody won. All over 5K. A good RE agent would calm all nerves and hysteria and take some of it out of their commissions to collect the real money.

Another point that benefited us (buyer) by using a RE agent about a decade ago.

The seller had added up all of the improvements (they were nice) and added their memories to their asking price. This was about 50K over comparables in the neighborhood. We really liked the house and offered them 50K less. They were so insulted that they didn’t even counter offer. We continued looking at other houses and 3 weeks later the seller RE agent told the buyer RE agent that they’d be willing to accept an offer of 45K less.

Thanks to the RE agents, I considered this a win for all of us. We bought a house that we liked at a comps price and the seller sold the house at a comps price. The RE agents had enough therapist in them to work out a deal between all of us.

The inspection turned up about 1K in repairs. The RE agents split it and we all came out ahead.

If you sold a house a decade ago, just don’t look at the comps price now. It is too depressing. Maybe we should have kept it…….

House prices in most areas have always gone up over 10-15 years. This time, many have gone way up and are settling now to reality. Reality meaning that they still up from 10-15 years ago.

Twinkytwonk: No qualifications in the US either, and it shows. There may be a few good ones, although I haven’t met one worthy of my business yet.

NOT a fan of the current RE mkt sales situation either fed, but must add:

In the last sixty years or so I have had very pleasant dealings with agents and brokers in five states who have been honest and competent and sometimes very helpful in convincing sellers or buyers to meet my objectives in deals.

As for every type of service, trades or white collar, there are good ‘uns and sorry ‘uns…

Vintage: the difference between realtors and many other white collar professions is that with realtors there is a low barrier to entry. It’s not hard to get a license, hence, more bad ones. The test is ridiculously easy, at least in AZ. I see no point to them. I was a FSBO 20 plus years ago and had no problem getting through the transaction. It’s not rocket science. I see no point to paying someone 5, 6% to sell my home.

Qualifications vary by State. A broker has more qualifications than an agent, at least in Az.

Look at the real estate stats…. find the agent/broker who has the highest level of success in your market and go with them. They likely “love” where you live and can sell the dream.

With the “arms length” transactions, few sellers ever meet the buyers. When you sell a house, it cannot be an emotional sale… just because Ellie May’s height tabulations are on the door jamb doesn’t make the house worth more to a buyer…. only to you.

I’ve told my wife on several occasions: I don’t care what the buyer does to the house after the check cashes. They can knock it down for all I care. It’s a pile of bricks and sticks. Take your photo albums and move on.

Elmo Muskrat:

The TSLA Pump: “we’ll sell 50% more cars…”

The TWIT Dump: “well, gee, I had to cover those losses at TWIT….

According to Elmo Muskrat – this is a quote – TWIT is “a plane that is headed towards the ground at high speed with the engines on fire and the controls don’t work….”

These billionaire idiots like Musk and Ackman are making themselves even more loathesome by foolishly and dangerously whining for a rate cut when the US desperately needs ongoing interest rate hikes and QT to stay financially and politically viable–they already have billions and never have to worry about money, still they’re so greedy, they’re basically screaming to endanger US national viability and social order by pushing inflation even higher and fueling social unrest. (Inflation is the main reason for the LAUSD teachers going on strike and shutting down our 2nd biggest school system and much of Los Angeles with it, and that’s tip of the iceberg). All for the sake of their narrow interests. Pure scum, because US national survival exactly what’s at stake right now in the inflation battle, and the upcoming Fed decision (and it’s discipline to keep tightening) may be its most important in decades.

Like my old prof once said, poorly controlled inflation has brought down far more great powers and major empires than any war ever has, and the US is at a dangerous cross-roads now both at home and abroad. There was a report last month about the Saudis and other big oil producers growing more furious about USA inflation ruining the value of their dollar sales and holdings, and exporting enough inflation to threaten social unrest in their own countries. That’s what the “dollar is reserve currency” false assurances don’t get–like my old prof also said, there’s never just one one reserve currency, there’s several plus commodities and other holdings in portfolios, and they’re not going to continue maintain large USD stashes if that asset is guaranteed to lose value from inflation. The dollar is now a fast depreciating asset, and if the Federal Reserve displays timidity and unprofessionalism by a rate cut, or even failing to hike, the rest of the world would see that as a signal that the Fed has given the green light for inflation to soar out of control and make the dollar worthless, and they’ll dump their dollars and USD denominated assets like mad. The Saudis and other oil and commodity producers are already diversifying and setting up exchanges to sell goods in other currencies, and even though the RMB isn’t free-floating (they don’t want a Plaza Accords sharp rise there), it’s pegged to a currency basket and not just the dollar, they won’t let it fall if the dollar is allowed to inflate away.

It’s even more dangerous back home, those teachers are striking in LAUSD because they can’t afford to live even in the far outskirts of the city, inflation just for rent and groceries is insane there. And that’s just the beginning–looting like they had with Argentina’s peso crisis back in the 90’s, higher crime and shoplifting and social unrest are all coming here if we don’t get inflation down, on top of worsening polarization in a country with 400 million firearms. It’s not enough just to reduce inflation because previous inflation has already shot up costs way beyond American incomes, prices have to come back down. That’s another thing the idiotic pivot mongers and squawkers forget, even just 1 percent inflation right now would be painful on top of the heavy inflation we’ve had since 2021 (the 2 percent “target” was always made up, just some random number pulled out by a New Zealand bank), so disinflation is a fool’s concept. We need not only minimal inflation (less than 1 percent), we even need a period of deflation to get prices back in line with American’s salaries. Fortunately the housing bubble is starting to deflate a bit but like Wolf’s been saying, it’s gonna be many years before it reaches a more reasonable level, and then then there’s all the other asset bubbles in the everything bubble mess.

Good read.

Let’s hope that the FED continue the rate hikes and not pander to asset owning billionaires so that they can get cheap loans and get their stonks to the moon.

Americans, and Canadians are becoming more aware of economic policy and how the current system benefits the asset holders.

When the LAUSD teacher produce a student that can add, subtract, and multiply plus complete a coherent sentence, they’ll be worth something. Most students can’t achieve minimum competency in reading, writing and arithmetic. Yet people wonder why this country can’t produce anything.

Let them strike… forever. Leave the classroom and don’t come back. Ever. Plenty of trash to pick up along the 5… and 110…. and 105… and 610….

You have good comments.

But too many Americans seem obsessed with the 1% (or 0.1%).

Huge numbers of middle middle class and upper middle class Americans (50 to 85% percentiles) benefit from owning assets: stocks, bonds, housing or any combination thereof. Of course they don’t benefit as much as the 1% in absolute numbers but still benefit mightily as supporting their standard of living.

I’ll say it again: as to lifestyle differences…

The lifestyle difference and opportunities between someone at, say, the 70 to 90% wealth&income level and someone at the 15 to 30% level is greater than between the

1% (99% to 100%) and 70 to 90% crowd. Not in absolute numbers of course, but in stability, opportunity, and general contentedness.

The 70% to 90% crowd sits pretty well with stability, opportunity, and general contentedness.

FWIW:

I know deflation is a dreaded word but I wish we’d get it for 5 to 10 years.

Deflation, not mere disinflation.

Especially the necessities: housing. food, utilities.

Housing will drop ,only really appreciated during Covid. Food not going down much ,too much demand . Energy has a 50 year supply,fossil fuels only going to appreciate,why do you think they’re pushing alternative fuel options . Money won’t save you rich or poor

You said a mouthful. Awesome comment.

The past year of tightening has only brought home prices (and stock prices) back down to 2021 levels. Given we’re closer to the end of the tightening cycle than the beginning, the parabolic move since 2020 (which is already on top of a decade of price appreciation) are unlikely to be reversed.

Buy-the-dip mentality is still widespread: every time mortgage rates retreat even a little, buyers flood into the market. Same with stocks.

Policymakers have an enormous incentive to unleash the money printers every time there’s a hiccup in the economy. Not only do they enrich themselves spectacularly, the asset valuation gains are hard to reverse, and they don’t suffer political consequences either.

Lost in your assessment is how local wages would be able to support inflated house prices long term. Because they can’t. Brief speculative bubbles where house prices divorce from fundamentals because of money-printing are possible, but they ultimately pop and crash into oblivion.

The long term trend of house prices reflecting local incomes has been the case for the entire history of real estate, save for the money-printing era. How do you propose they are going to levitate house prices above what local incomes afford. If they are able to levitate house prices, why are they crashing now, and why did they crash in 2008? Why wouldn’t they have just kept them levitated or increasing?

The “this time is different” reason is the rise of work-from-home (which is down substantially from 2020 but still far more common than 2019.)

A lot of wealthy buyers from San Francisco, Manhattan, et al. drove up prices across the country.

There is no actual “this time is different”. Just wait until rates “blow out” years from now, regardless of what the FRB does or does not do. Either that or the USD is going to crash.

There will be no voluntary “printing to infinity” at the expense of global reserve currency status. The public, markets, and economy will all be “thrown under the bus” to preserve the Empire, with no reservation.

Depth – could be that many involved only know the money-printing era and wouldn’t study and integrate longterm history if you offered to pay them…

may we all find a better day.

It is regional. The West region did take a pretty good price cut. 10% or more from the peak.

My flyover region maybe is down 5%

Black Knight came out with a report of affordability per 150 top MSA based on data from people who have mortgages. Worst city was Los Angeles. 63% of monthly income goes to the house payment. San Diego, San Jose, and San Fran were all above 50%. Other hot areas like Seattle, Miami, New york were all above 40%.

Now in the midwest, many are still below 30%. The City I live in was 24%….up form 19% pre covid. 19% was very affordable. 24% is still affordable. The bottoms 10 were all from rust belt cities…and even Chicago and ranged from 20% to 24% Those areas are not in a affordability bubble.

Zillow has a tracking report that indicates where most of your out of town home searches come from. The most searches were for my midwest city was from Los Angeles and Denver. LOL My realtor friend said the past two years 50% of her clients are from those two cities. There is affordable housing in the U.S. I saw another map and 40% of all counties in the U.S. median home price is below $150k. The the next 40% is below $350k. So 90% of the counties in the U.S. have median priced homes below $350k. It is just the top 20% counties are expensive. If you do not mind living far from Ocean, or in a desert city running out of water, or near a mountain range…there still is affordable housing. But investors are snatching them up.

posted before grammer check. LOL 90% of all counties have median home prices below $350k. Top 10% are expensive.