We’re not even getting peanuts? EU regulators came out today and said, no, no, no, that’s just in Switzerland, not in the EU.

By Wolf Richter for WOLF STREET.

One of the elements in the takeunder by UBS of Credit Suisse was that CHF 16 billion (about $17.3 billion) in CoCo bonds got wiped out totally, while shareholders got wiped out only almost totally. Swiss regulator FINMA, when announcing the deal on Sunday, said that CoCo bonds would be written down to zero, in a sense subordinating bondholders to shareholders, which is like a total no-no very-bad-boy thing to do, because normally, shareholders would get totally wiped out first, and then bond holders would start taking their turn.

Turns out, there were some clauses in the documents of the CoCo bonds, issued in Switzerland, that allowed this under certain conditions and triggers. But no one ever reads any clauses, and so it came as a surprise, shaking up the $275 billion market for these creatures that came out of the swamp of the Financial Crisis.

What are Additional Tier 1 CoCo bonds?

CoCos – short for “contingent convertible capital instruments,” also known as Additional Tier 1 (AT1) bonds – were created in Europe in response to the financial crisis as a way to boost bank capital without diluting existing shareholders. Before, a bank would have to sell shares to raise capital, thereby diluting existing shareholders. With this instrument, they could weasel their way around selling shares and still raise capital for regulatory purposes.

CoCos are perpetual bonds – they have no maturity date, and the bank doesn’t have to ever redeem them, but it can redeem them at certain intervals, such as in five years. European banks offered them in major currencies to appeal to investors in those countries.

In general, CoCos are designed to be bailed in when the bank gets into trouble, either by converting them into nearly worthless shares or by writing them down to zero. They therefore provide a capital buffer; and for regulatory purposes are considered equity capital.

In return, CoCos offered a relatively high coupon interest. For example, more recent Credit Suisse CoCos came with a coupon interest of over 9%; Deutsche Bank issued CoCos with coupons over 6%. These were tempting coupons in a world of Negative Interest Rate Policy.

Banks in the US don’t issue CoCo bonds. They issue preferred shares with similar features that allow banks to raise capital without diluting existing shareholders. When the bank gets in trouble, those preferred shares get bailed in after shareholders get bailed in. This happened when SVB Financial collapsed on March 10. The $3.7 billion in SVB preferred shares collapsed from around 70 cents on the dollar to near zero in one fell swoop, with the ultimate outcome still uncertain.

We’re not even getting peanuts?

What tripped folks up was that shares of Credit Suisse didn’t get totally wiped out first. The buyout offer by UBS was an exchange of one UBS share for 22.48 Credit Suisse shares, which valued Credit Suisse shares at roughly CHF 0.76 (down 99% from the peak in 2007) and down 60% from the close on Friday. Maybe this was a nod toward institutional investors in the Middle East that had poured so much money into Credit Suisse.

So shareholders are getting some peanuts. CoCo bondholders had been under the impression – not having read the clauses – that their CoCos would be senior to common shares, and that they’d get some peanuts, if shareholders get peanuts. But now, they aren’t getting anything, not even a single peanut. And this hit CoCos all around Europe today.

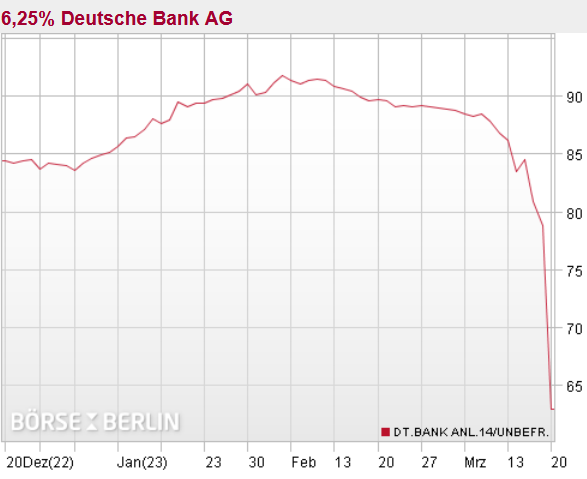

For example, Deutsche Bank 6% CoCos plunged today from the already beaten down level of about 79 cents on the euro to 63 cents on the euro (chart via Börse Berlin):

EU regulators try to soothe the CoCo market.

EU regulators – while happy that the Credit Suisse mess is getting sorted out “in order to ensure financial stability” – are not happy with this decision by regulators in Switzerland, which is not part of the EU. And they came out, as regulators do, with a joint statement today, emphasizing that in the EU, the capital structure will not be usurped, that common shares will be bailed in first and totally before any bonds are getting chewed up.

In the statement, the ECB’s Banking Supervision office, the EU’s Single Resolution Board (SRB), and the European Banking Authority (EBA) said:

“The resolution framework implementing in the European Union the reforms recommended by the Financial Stability Board after the Great Financial Crisis has established, among others, the order according to which shareholders and creditors of a troubled bank should bear losses.

“In particular, common equity instruments are the first ones to absorb losses, and only after their full use would Additional Tier 1 be required to be written down.

“This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions,” the statement said.

The one that may have gotten away.

But, but, but… Credit Suisse issued $2.5 billion in CoCos that are similarly structured, but are counted as Tier 2 capital, rather than Tier 1 capital. And these CoCos have “an unusual structure,” and “will presumably remain an obligation of the enlarged UBS, alongside CS’s senior bonds,” CreditSights said in a note, cited by Bloomberg.

When an analyst asked UBS CEO Ralph Hamers if this AT2 bond would also be written down, he said, “we’ll have to come back to you.”

While Credit Suisse’s AT1 bonds have plunged to a couple of cents on the euro today, the AT2 recovered and traded at 75 cents on the euro, according to Bloomberg.

Finally over.

Credit Swiss has been teetering on the brink for years. It has been hobbling from scandal to scandal, each time losing billions of francs along the way, and each time, its shares got beaten to a new record low. And all along the way, new investors were bamboozled into investing billions of dollars in this thing to boost its capital and keep it alive. And the money just vanished. The culture of risk-taking and doing shady deals was something that could apparently not be changed by the CEOs that came and went. Or they didn’t want to change it – despite rhetoric to the contrary – because they were focused on boosting the share price or whatever. The SNB wouldn’t let it collapse, and regulators didn’t force it to straighten out. But a lot of losses to the Swiss public and investors could have been avoided if this creature had been taken out the back and shot years ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yes, “No One Reads Clauses Anymore” and the stock market is driven purely by headlines and hopium.

Case in point, the Fed’s loans to banks and FDIC is being interpreted as PIVOT and QE (“The Fed’s balance sheet grew by 300 billion last week”).

Perhaps after 14 year of QE, no one can even believe that there won’t be another rescue.

“the stock market is driven purely by headlines”

Q: What Percentage of Trading Is Algorithmic?

A: About 60-75 percent of overall trading volume in the U.S. equity market, European financial markets, and major Asian capital markets is generated through algorithmic trading, according to Select USA, in 2018.

I forgot to read the “FINE PRINT” too!

Luckily though my “credit suisse” 5 oz gold bar seems to be trading at same value, “thanks” to UBS buy out!

I’ve always been curious about that. This isn’t Ma and Pa Kettle’s market anymore. That’s for sure.

Price is what you pay, value is what you get. If you are long term investor you don’t need to know too much wore than this “to get a 10% long term return on SP500 you need to be buying it at around 1 X sales.” Price to sales currently around 2.3.

Interesting financial “instrument” (always loved how they Econ guys use that word) games.

Reminds me of Soros’ comment at his Congressional dog and pony show after the GFC. Essentially said, “They can keep inventing this stuff faster than you can make law regulating it”

Side note; I always thought CS and DB “Ultra High Net Wealth Funds” were huge black boxes with massive washers and dryers and worm holes to ?, in them…but I’m sure there are others.

Oh, the EU now claims that it would touch coco only after bailing in Shareholders.

Wolf, is it even legal for ecb to do this?

It’s perfectly legal to bail in CoCo holders after bailing in shareholders — if that is your question.

Bitcoin at 28k. Sry haters

Down from $65K, LOL

Bitcoin is a mania, and those that got in early and cashed out profited greatly but eventually, Bitcoin will bite the digital dust.

“Bitcoin defies deniers as it surges 74% YTD against a backdrop of Fiat banking collapses.”

My made up headline. Sorry….couldn’t resist. What matters is your entry point. If you bought Bitcoin January 1st this year, that’s a great return. But…but…the hardest question is always when to sell?

Bitcoin (and many of the other cryptoscams) are often advertised as “sure investment” (which it never intended to be) and “solid as gold”. Essentially they’re nothing more that digits in a computer database, which also is advertised as secure and out of reach of the big bad governments, because it’s “distributed”. It isn’t – just every full node keeps a copy of it, and this is a far cry from the definition of a distributed database.

In many cases the approach used to “create” or “mine” new units is described as “work”, but how anyone with a common sense could accept the waste of electricity to perform completely useless calculations, is beyond me.

Furthermore, aside from the cryptoscams being complete waste of electricity, they’re alse a complete waste of a silicon – the big mining farms are usually based on ASICs, not FPGAs, which means that those chips, once burned, can’t be repurposed for anything else. As for the electricity wasted in order to brute-force a solution of hash evaluation – well, the reason why China threw them out is not because the Bitcon (and no, it’s not a typo) was a competitor to the renmimbi, but because of the electricity waste, which at the time was a very big issue for CCP.

In many cases the network that facilitate the transactions is defined as a peer-to-peer network (which is true) of “independent” nodes (which is false). The more appropriate metaphor is to describe it as a network of printing presses, produced by the same factory, which has to simulate work, in order to convince everyone else that their product has “value”.

“But the CoinBase shows me that the ‘coins I’ve bought are worth this amount and that amount”, sometimes coiners say to me. Wrong – the number you see on those sites is what it’s going to cost you to obtain something that’s essentially a hot air. That’s the price you’re going to pay for your greed/stupidity/both.

“This and that celebrity own coins and they said that they’ve made a lot of money by holding them” – another common theme. Sure, they may’ve bought them, probably as an ad trick to incentivise other fools to buy into the same scam. But did it occur to anyone that until you cash out, you essentially have nothing? And how many times cryptoexchanges had to shut down withdrawals, when a run on them occurs (a behaviour remarkably similar to the one adopted by the banks when a good ol’ classic bank run happens). Those “celebrities” may advertise, but essentially they’re looking for a bigger fool to offload. Finding a bigger fool willing to buy hot air is actually very easy. Finding a bigger fool with enough money to by the scam at the current prices for sufficiently long time (so the price won’t fall fast and hard) – that’s nearly impossible, because the only entities with this kind of money are the institutional investors like hedge funds, private equity firms, family offices, etc. And in this game they’re anything but fools – they’ve invented it.

And last – did occured to any crypto-zealot that it’s actually very easy for the central banks, especially the Fed, to take Bitcoin out of circulation – they only thing they have to do is just to continue the QE, the inevitable inflation would push the price of the Bitcoin up, taking it out of reach to pretty much everyone. And current HODLers – they’ll be left holding the bag simply because they won’t be able to find anyone to sell to. Not at these prices.

JA,

What was SVB if not a rescue of *uninsured* depositors (ultimately backed by fiat paper)?

Who knows… Some said SVB was somehow an instrent in Venezuela “oil for drugs” trade, and that was the reason PVDS was headed by an ex-spy last five years. And when SVB went down Venezuela claimed huge losses and stop oil export, and by rumors are cracking down on their official cryptocurrency.

I do not see how all those events could be related, but there are voices saying they were (maybe just making pretense)

Too bad I can’t insert gif in comments, just your imagination and image a picture of Nelson from The Simpsons pointing at the Bondholders and go “Ha..Ha…”

Can’t say I feel sorry for leaving this much money on the table by not reading the fine prints..

My imagination can’t help be immature based on your comment – Nelson going Ha Ha and adding new meaning to “lderHOSEn !

Although your comment re nelson of simpsons ”resonates”,,,

IMHO,,, a better analogy would be Nelson at Trafalgar,,,

But yours will be better understood by WE the PEONs ”these days”,,, even though the other appears at this time to be much much more appropriate to the current situation…

With, unfortunately, THE great confusion/involvement of GUV MINT being the ”kicker” for all of us on FIXED INCOME who will continue to lose out to the trillions of manipulations AKA derivatives ”HIDING IN THE background.”

May WE all be blessed and guided by the GREAT SPIRITS!!!

Credit Suisse always struck me as the European version of First Union.

The First Union that had such a poor rep, that when they “merged” with Wachovia in 2001 they got rid of their name and took Wachovia’s.

But it was always amazing the blow up they had before the fallout from 2008 did them in.

It was the wonderful Wachovia that took the mess over – at which time “Wachovia” was the fourth largest bank holding company in the US – it allowed the gray banking tradition to continue. Though I don’t think anyone in North Carolina has been calling the shots since 2008.

That was before Wach got nailed for the extensive money laundering they,,, and many other USA banks were doing in those days R:

Had an ongoing ”bank relationship” with local Wachovia folks who quickly were fired for being too customer friendly, such as cashing large checks out of hand, signature loans and HELOCs,,, etc…

Many changes to many banks in 2007-12,,, BUT:

HERE WE ARE AGAIN,,, eh?

What was the long term game plan for getting rid of debt at 6-9% interest ? I can’t imagine borrowing at that rate without some kind of sound business plan for eliminating it. This was a business and presumably operating to make money. Was there just no contingency plan for the circumstances that came about as interest rates rose ? Just caught with their pants down ? Compelled to just go with it as free money flowed into their coffers ? The decisions must have been considered reasonable if people were still buying and holding their stock. I never bought the house of cards theory hook line and sinker but this sure sounds like it.

Most of this debt is callable after 5 years. So if the bank felt they had enough reserves to no longer need this capital, or they had cheaper sources of raising the capital, they could simply call the bonds, redeem at par, and shut them down. The key, though, was that this was at the discretion of the bank. That meant there was no forced maturity. So in times of market stress, it would be better for them to pay 6-9% and keep things going, and then, during times of market peace, they could redeem the bonds at their leisure and replace with cheaper funding.

Consider it an insurance policy: no bank relied on CoCo bonds for the majority of their capital. But it was a nice buffer to have in case the SHTF, and so they willingly paid an extra premium to have it around. But if they felt it was too expensive and other sources of capital were better, they could always reduce their CoCo bonds by calling them.

They could also reduce the face value of the bond when their capital fell below a predetermined level. Also, if they didn’t want to pay the interest one year they didn’t have to.

Wolf, what is the implication of this on US bank preferred stocks that are perpetual and count towards Tier I capital? Thanks

Preferred shares got bailed in along with common shares in both bank failures we had here — SVB and Signature. That principle seems to hold. There is nothing particularly unclear about it, the way I understand it.

SVB Financial, the holding company, filed for Chapter 11 bankruptcy last week, so we’ll see how all this gets sorted out in court. There are some assets left in the holding company that are not part of Silicon Valley Bank, so this situation is different from Credit Suisse. There may be some crumbs left over.

One interesting wrinkle is that SVB Financial had $2B deposits at SVB Bank, thus they are guaranteed by FDIC. So in a very round about way FDIC is backing SVBF bond holders because the $2B from SVB will be used to pay off SVBF bondholders. Just a quirk of the FDIC guaranteeing all deposits.

Venkarel,

The $2B is not counted as a deposit from the holding company, but as equity to the bank and the corresponding debit was cash when they downstreamed the money.

Gary,

Why would that be? From what I can tell they are two separate entities. Granted I do not know the banking sector itself but GAAP does not call for a deposit too be recognized as equity. It would only be such a credit on the banks books it it was a capital contribution in some manner (stock sale, capital injection by existing shareholders, treasury fund, etc) or if it was a related parent/subsidiary company (which it does not seem to be again the banking sector might be weird) and considered eligible for consolidated financials (in which case it would be an inter-company transfer). In most other cases, excluding the payment of goods or services, a cash transactions offsetting T account from a cash debit will be a liability (in this case deposits).

Venkarel,

You are right, the banking sector is weird. Typically, a bank holding company (BHC) is a shell used for capital raising, non-bank activities and provides more flexibility. I am guessing in other sectors, the parent company is not a shell, but actually creates wealth for the shareholders.

In banking, the wealth is created primarily by the bank and to some degree, other non-bank subs. Even if a BHC has other non-bank subs, the bank is the biggest sub and the primary income generator.

The ability to issue debt and downstream the proceeds as capital to the bank is one of the key benefits of a BHC. The debt resides at the BHC, but the bank will make dividend payments to service the debt. See link for pro/con of BHC structure: https://www.troutman.com/insights/advantages-and-disadvantages-of-bank-holding-company-structure.html

Wolf,

In a recent thread on banks, I almost mentioned that DB has been too quiet lately.

Nothing, another bail out for the circular firing squad

Is any of this “real money”? So where’s all the people jumping off of high bridges or out the windows of tall buildings? There’s no collapse until we get some “splat” going. Then we can call it an event. Meanwhile, cash dilution continues in care of your friendly idiot packs in charge.

None of it was mine, so none of it was “real money”.

We are early in the tightening cycle for much stress right now. Sad to say the layoffs, defaults, divorces and splats will be coming up as we get into a recession. Its been a slow inflationary grind down for close to two years, but I say the worst is probably in the next 12 months.

These things run in a pattern. Inverted yield curve, financial blowups and the last shoe is massive layoffs as businesses do what they must to make debt payments.

“A pattern,” or one of several possible? Maybe it’s time to re-start the speculation about the shape of possible recessions, as capital letters: a quick “V”-shape, a longer “U”-shape, and abysmal stepped-down “L”-shape, a bifurcated “K”-shape, or whatever chaos a Powell capitulation looks like.

I think the last one is “O”-shape, with Powell chasing his tail and going in circles. Even if I’m wrong, I hope we don’t find out what shape capitulation looks like.

Yeah, I’m actually kind of surprised how much market stress we’re already seeing given we’re still very early in the tightening phase, the economy is still humming along, and people still have money to spend.

I’m a little worried about what happens when the screws really start getting tightened. For now, Cash is definitely King!

Cash is not a great investment in the face of inflation. It’s better than everything else, but the best investment is to just spend the cash now on stuff that you want/need.

The pandemic also taught us all that no matter how carefully you plan your investments, life can quickly rob you of the time you thought you’d have to enjoy them.

If Powell wants people to stop spending he needs to make putting of spending FAR more attractive than it is right now.

I’m waiting to see what happens to the American car companies. Their business strategy has just about abandoned affordable vehicles. Free money, cheap gas, and a testicle-tight hold on regulatory framework turned their brains to mush. Most of the world gets a decent level of econobox options but we do not. We also have strict prohibitions on imports – they must be 25 years old or meet expensive USA-specific design and crash testing requirements or, in our most popular segment (pickup trucks and other large SUVS) be subject to a huge 25% import tax if they’re produced abroad.

Wolf pointed out that people can mostly just drive what they have for longer. We’ll see how this works out in earnest when the captive finance companies feel real stress and cheap money is no longer available to finance very expensive vehicles.

Re early in the cycle…everybody in finance knows how abnormal/distorting ZIRP was, so they are moving pretty fast in the face of unZIRP

Meh. With an election around the corner and US controlled Poland positioning to transition the proxy war into kinetic war – the printing presses and factories will be humming soon enough!

No splats EVER again at high levels. Plenty at low levels, like a drug addict is sort of a slow splat, and some fast ones even in grade school and up, as more are getting a picture of their likely future….or have arrived already.

My Mom said during the 29+ crashing their were splats all over, including small town bankers all the time. (no real tall buildings, had to use a gun or rope to be sure)

During GFC people even drew chalk “landing strips” and body shapes in the Wall Street area for them, (google it) but NOTHING AT ALL HAPPENED, except one European Noble unknowingly feeding friends to Madoff who shot himself.

We are NOW dealing with an ENTIRELY new breed of cat. No shame, no honor, no sense of duty, no empathy.

Trump is an EXCELLENT example.

NBay – as you so aptly refer to Aristophanes’ “men of brass” in a more recent post…

may we all find a better day.

Yeah. It wasn’t long after that play that the “men of brass” sold out to the Romans and their 1000 year empire began.

Really glad there are some people here who think about more important things than how to get a bigger house and car. It’s still economics. Take care.

There is still about 900 billion in extra savings in customer accounts from all the money given out during COVID. Another year of burning this money off and we will see the underlying economy in tatters.

Real estate markets are frozen, with few buyers and sellers. It is going to take another six months for the prices to really fall and enter a more stressful time period.

Gametv,

Sincerely asking…since most/all Covid programs were income-replacement, what is the source of those incremental savings?

Are you saying the savings increase is from 2021 asset run-up (what’s left of it) or truly from Covid programs that did more than *replace* shut down income.

I think if we can identify the main sources, we can learn something valuable.

Unless you are president o that put bond holders behind political allies and destroyed 100 years of contract law in the GM bankruptcy.

“which is like a total no-no very-bad-boy thing to do, because normally, shareholders would get totally wiped out first, and then bond holders would start taking their turn.”

Violating the absolute rule of creditors’ priority is a big mistake. Too bad the powerful have been doing it from day One, and often for more concentrated selfish reasons than USA political alliances. But that’s no excuse. We are seeing it happen already in this crisis, and we haven’t even had a crisis yet.

Be interesting to see what is happening with the small details. Well before Ukraine invasion I purchased some stock in a Russian O&G company. Then, of a sudden, come the sanctions. Here’s the interesting part – no official policy from the gov’t. Brokerages simply froze all sale/purchase options for Russian stocks. Got it. No problem. So, I contact my CPA, the Brokerage, my Congress Critter: can I claim a short term capital loss? Response: we have no idea…there is no policy for this….how would you document the loss without a corresponding sale?” Another way of stating “F you, we will appropriate your ownership rights whenever we choose.” Lesson learned.

You do know I guess that GB II signed the GM bailout BEFORE Pres O took office, explaining: : ‘I didn’t want him to have a crisis on his first day in office’

Nick Kelly,

Pardon my ignorance, but you are speaking of two different things.

The bankruptcy and dissolution of ‘100 years of contract law’ as stated by 2banana refers to the the resolution of GM assets in July 2009. It absolutely was a product of the Obama administration.

You are speaking of the bailout loans offered by the government to attempt temporary solvency for the Big 3. Absolutely a product of the George Bush II administration.

Confusing these in your comment reflects some blend of ignorance and propaganda.

Wolf, you cannot imagine how much I appreciate your compass.

Lacking congressional backing, Bush diverted cash from the Troubled Asset Relief Program, which Congress had passed in October and was supposed to be restricted to rescuing banks. “I didn’t want there to be 21 percent unemployment,” Bush told a meeting of the National Automobile Dealers Association in Las Vegas in 2012, explaining why he acted as he did. “I didn’t want history to look back and say, ‘Bush could have done something but chose not to do it.’”

Why do you trolls try to drag Wolf into your own agenda? It makes you look VERY stupid.

NBay,

Since you have responded to my post, I will assume you are referring to me as a troll.

You have made no point. Regardless of how George Bush II tried to help the auto industry with the TRAP funds, as you point out, it had nothing to do with the GM bankruptcy that Nick is muddling with the TARP bailout. Seems you may suffer the same confusion, or perhaps you are the troll.

Ok, I’m a troll……as my step gramma from Sparta NC said,

“Ever what you want”

What’s the saying? “Don’t invest your money in things you don’t understand” ?

Granted, with all the “innovations” and instruments that have come out in the last decade, one can’t be faulted too hard for being caught on the wrong side of a deal.

Just their response.

The bondholders would have to be something like seriously decadent Euro-stereotypes to not get what a CoCo bond meant.

They understood. I think Wolf exaggerates for some flair here. You don’t buy tens or hundreds of millions worth of bonds without a room full of lawyers and accountants. Most of the holdings are going to be part of a larger diversified bond portfolio. The bond portfolio managers just didn’t care because nobody believed those clauses would ever be triggered. You take some (in their minds, small) risk that some bonds might zero in exchange for the higher coupon.

Truth is those portfolios are down way more in 2022 as yields rose. Add another $17b to the fire.

Those CoCos are PUBLICLY TRADED, and they’re volatile, and any retail investors around the globe can buy them and trade them, and they DID buy them. This BS that they were marketed only to the buy-and-hold pros is just BS.

I never said they were marketed _only_ to institutional investors. Retail lost too, obviously. [Though not in the UK, where selling them to retail was banned by the FCA.]

What _I said_ was the pros did read those contracts and were perfectly aware of the terms because they have lawyers. We can assume at least a few of the more savvy retail investors read and understood the terms as well.

What _you said_ was (quote) “no one ever reads any clauses,” like the terms were something an archeologist discovered in a tomb this weekend.

Saying that “no one” read the terms is an exaggeration. Artistic hyperbole. [I wouldn’t use the word “BS” because I’m polite that way.]

Now, I think I want to buy some. What the hell & what the heck, it’s only money :)

Still, if the terms of conditions stated the bonds could be bailed in before the shareholders it is legal.

That some bonds have different terms and conditions and that may throw a spanner in the works for the financial industry is a different story.

Lesson learned is that a bond may not be equal any other

bond and the terms of conditions must be read like the spec sheet when buying a new car or anything else.

Kinda like students loans borrowers that don’t want to pay them back?

“But no one ever reads any clauses…”

Hey, if Silicon Valley entrepreneurs can be protected from their decisions by the government….

There may be an argument that government policy helped create the inflation in university fees and the rising tide of credentialism that is depressing an entire generation from advancing in life stages (amongst other disatrous changes in the university system), but I feel you as someone who took on and paid off his student debt.

LK,

“There may be an argument that government policy helped create the inflation in university fees and …”

You cannot have the government subsidize an industry with trillions of dollars and it not create the inflation in university fees we’ve been witnessing for DECADES. The student loan program is an abomination.

The solution? Wolf stated it several years ago. Abolish student loans, build bare-bones educational institutes without highly overpaid administrators, as much online learning as feasible and eliminate all of the extras such as, coffee bars, deluxe athletic facilities, …

If people want to pay for all the extra sh*t then fine! You pay for it, not through government subsidies. I’m just getting started so I had better stop.

Yeah I get it, massive bloat caused by government subsidy, the educational-industrial complex a parasite on the system. But here we are. I am grateful that my degree program was provided for by government grants all the same.

I recently finished Allen Bloom’s book, “The Closing of the American Mind,” and I was moved by his analysis of the university system (from ’87) and what happened during the Civil Rights era to undermine its core mission and principles.

Look, market psychology has taken over everything in the U.S., never more evident with Web3 and its Financialization of Everything. I don’t know where this all leads but I do better understand the ambivalence towards higher education expressed by some beyond the luxury offerings on campuses.

2 things true at once.

Students deserve no sympathy or help with their loans.

We should bulldoze colleges and stop subsidizing and do barebones as mentioned.

AGREE with you totally RF:

As one who ”worked” every day when not in class and sometimes/DAYS,, later or earlier when in classes at my colleges/universities.

IMHO, recent good folks who used to be able to ”work” their way through college, etc. have absolutely been screwed by these incredible increases in ”COSTS” of college mostly due to the unbelievable increases in costs due to SO many increases in ”administration, etc. ”, that have either NOTHING or VERY little to do with QUALITY OF EDUCATION…

“But a lot of losses to the Swiss public and investors could have been avoided if this creature had been taken out the back and shot years ago.”

But that applies to ((much) much) more companies than Credit Suisse alone.

And they couldn’t understand why they were getting such good rates. If it looks too good to be true……

Treasuries next?

Countries do not go bankrupt. They just print more money.

It seems like Steve Hanke is the guru on this. Once nobody wants your trash fiat, you need to establish a currency board and peg your currency to some decent currency that your citizens will accept or already use in the black market which is usually the dollar. Hopefully the Fed and treasury will protect the dollar status for a few more decades.

I am waiting for the next shoe to drop. That is when they may have to capitulate.

If regional banks got into trouble with rising interest rates, what about all those hedge funds who gobbled up the easy money and sold leveraged bets to chase yields. The opposite is happing now.

You now have customers taking money out of their saving to spend on things because of higher inflation, pulling money out of low yield investments to go into treasuries, etc. Investable cash is moving into treasuries.

Liquidity is drying up and something else is probably about to break.

How are zombie companies going refinance their debt payments that will be coming due when everyone would rather be in treasuries.

The goal of just 2% inflation has now also become “transitory”, and that goal will be changed higher, and it will stay higher for a long time.

They can’t balk at raising rates or they will lose total control, and there will be hyperinflation

They should have planned for that if they haven’t already. Everything you are describing seems to be the logical consequence of an environment with rising interest rates to combat inflation. The party is over.

Won’t someone think of the hedge funds and zombie companies?! They know not what they do!

Black swans are not a long shot anymore.

Implicit

They are being ‘shot’ before they even hatch!

In Western Australia it’s on the flag!

Bravo, both of you.

ru82

“Steven Blitz, chief U.S. economist at TS Lombard, pointed out the problem in a prescient report entitled “Is a Small Bank Problem Brewing?” weeks before the SVB debacle broke. Not only were these institutions more aggressive lenders than their larger peers, he warned, they also have a larger concentration of loans in commercial real estate, which has big problems, especially in the office-building sector.” (h/t Barrons)

Will this be next DOMINO to fall challenging The Fed (CBers) which keeps on digging further?

Maybe Powell is a genius. Quickest way to get inflation down is to have a banking crises. Banks stop lending. People don’t want to borrow. Otherwise it is going to take a couple of years.

Trouble will continue until the collapse completes a survivable balance just as predicted a long time ago:

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered…. I believe that banking institutions are more dangerous to our liberties than standing armies…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.”

Thomas Jefferson

I am not a historian but I think John Sherman in 1891 is the one who said this. I love the lines but want make sure Wolf Street stays the great news source it is. The speech was about the Sherman Antitrust Act, which was designed to prevent monopolies and promote competition in business. However, the quote has since been misattributed to Jefferson and continues to be circulated as such.

Yes, I have heard that it might have been someone else, but I still like the content.

The Fed is not a private bank. This is a conspiracy theory.

It is not a public bank either. It is considered both, supposedly.

Choose the AI promoting the data and the aother AI will call it a conspiaracy theory, while programmersx just continue writng the algorithms.

Who really knows the “truth” . There are only algorithmic probability guesses that something is not not truth.

When the US entered WWII it ran huge deficits, paying to build planes, ships, tanks payroll etc. etc. with that danged ‘fiat’ which some people seem to equate with ‘fake’. This was, not of course, lent by private banks, which would not have anywhere near the amounts anyway. The entity creating this command currency was then and is today the USA. It also issued a fiat, literal translation from Latin ‘a command’, that the Empire of Japan would cease to exist.

The Fed is engaged in the same activity as the BoE, the Bank of Canada, the BOJ etc. None of the latter do this ‘member bank’ kabuki. The Fed Chair can listen to them, why not, but he decides what to do. He does not represent them and is not responsible to them.

If the “Federal” Reserve Banks (i.e. A very specific select group of U.S. Banks NOT owned by the U.S. Government) have SHAREHOLDERS, which I am certain they DO, AND if said shareholders PROFIT from Federal Reserve policies, which they most certainly DO, then it is NOT a “conspiracy theory” to state that the profits are PRIVATE, not public.

You can split financial hairs on that irrefutable reality until the cows come home, but it is certainly NOT WE-THE-PEOPLE (i.e the “public”) that profits from Federal Reserve policies. If you labor under the view that when the “Federal” Reserve buys U.S. Treasuries, it is “acting on behalf of the U.S. public”, you need a reality check.

The U.S. Department of the Treasury IS a PUBLIC institution. The “Federal” Reserve is NOT.

If private interests profiting from the Fed’s actions makes the Fed private, then the US Airforce is private because of all the profits flowing to defense contractors. Incidentally, the largest profits from Fed actions, or as most agree, its mistakes, have gone to home owners. We now have the first generation that will be poorer than their parents.

…it bring the Marx’ to mind (Chico & Groucho) going down a list of contractual clauses, tearing off each as unnecessary, arriving at the sanity clause and Chico tearing it off and declaring: “…nobody believes in Sanity Clause…”.

may we all find a better day.

“Whatever it is, I’m against it!”

fyi, this scene was from “A Night at the Opera” (1935).

…thank you, Whole. (…and, upon reflection, I think Chico’s line was: “…everyone knows there ain’t no Sanity Clause…”. Sanity or Santa, seems the nature of existence of either remains lodged firmly as a topic of debate…).

may we all find a better day.

Swiss gvt/central bank put up a 100billion $$$$ credit backstop for UBS to swallow the toxic pill! That’s per capita of the american federal reserve putting up 4 trillion$$$ for a single bank merger!

That’s a flashing red sign of how bad not only CS balance sheet is but also UBS’s! But, of course, the majority of eu and american banks are insolvent, not just due to their treasuries but their loan books!

It indicates nothing about UBS’s balance sheet.

If someone is getting a 9% yield in a 0% country, and they think their bond is safe as houses, is Cuckoo, not Coco.

Off topic, but reminds me of the Harry Line comparison of Italy and Switzerland in the “Third Man.”

Incredibly clear and concise explanation on all this. Thank you.

Fine print never matters … until it does.

HaHa love those guys, and one of the last lines in the skit is apropos to the topic at hand. “Thre ain’t no Sanity Clause in these contracts”

+++

The best outcome for a government is also to not enforce any bondholders priority in cases where it exists. Taking their money to prop up a bank is a one time urgent event; i.e., no worry about repeat customers. If the shareholders are wiped out in the stock market, the event is slower than a sudden government action and the hands of the government can be camouflaged by “market conditions.”

“This deal is bound to generate legal and political resistance,” said Octavio Marenzi, CEO at Opimas, a management consultancy focused on capital markets.

Los Angeles-based Quinn Emanuel Urquhart & Sullivan said in a press release Monday that it was in talks with holders of Credit Suisse’s AT1 capital instruments, also known as contingent convertible or CoCo bonds, about options for pursuing a lawsuit or other legal recourse.[..]

Quinn Emanuel has some experience in this area: The firm represented an international group of CoCo bondholders after they accrued more than $1 billion of losses when junior bondholders and equity investors in Banco Popular, formerly Spain’s sixth-largest lender, were wiped out when the bank was sold to rival Banco Santander..”

(h/t Marketwatch)

Guess Wait n Watch.

FDIC insurance also has a special clause about “assessments” being paid by all member banks (in other words by customers). An associated clause involves bailing out depositors above the $250,000 limit if by not doing so, a systemic threat to the banking system is perceived by the regulators. This is of course a judgement call. The special “assessments” will be used to bail out such deposits over the $250,000 limit, where necessary. This could happen, or is happening, with the deposits of the customers at SVB with over $250,000, who are generally wealthy, well-connected, supporters of the Democrat Party. The whole thing stinks. I have moved nearly all my money from banks to short-term Treasuries. Note that short-term Treasuries also have much higher rates than any bank account so I am not losing anything. I left enough in the banks to write some checks and pay some bills.

During the Credit Suisse presentation of COCO bonds,(chart NOT included) in a typical write down scenario, shareholders are the first to take a hit before AT1 bonds face losses. That’s why the decision to write down the bank’s riskiest debt — rather than its shareholders — provoked a furious response from some of the bondholders.

Realizing that the chaos and fury among AT1 investors could spark the next leg of market contagion, on Monday morning European regulators rushed to reassure investors that shareholders should face losses before bondholders after the takeover of Credit Suisse Group AG wiped the bank’s Additional Tier 1 debt while preserving over $3 billion in equity value.

Junior creditors should bear losses only after equity holders have been fully wiped out, according to a joint statement from the Single Resolution Board, the European Banking Authority and the ECB Banking Supervision, who apparently were NOT consulted on Sunday during the whirlwind decisions that preserved some equity value at CS while wiping out its entire AT1 tranche.

Judging by the market action, investors aren’t sticking around to find out. All kinds of risky bank debt tumbled on Monday and analysts predicted far-reaching consequences to Europe’s funding market. The market for new AT1 bonds will likely go into deep freeze, traders said.

Consequences of this CBers action will slowly roll out in the coming weeks. Guess, don’t forget read the small print at the bottom, when buying Corp Bonds.

Wolf, thanks for all your insights. Could I ask for a prediction? What is the Fed going to do this week? Will it surprise the markets? Thanks!

I will for sure tell you what the Fed did, and what it says it will do in the future (dot plot, Powell, etc.).

I told you in the past what the Fed said (dot plot, Powell, minutes, etc.) it would do in the future. The last words it spoke indicated 25 basis points. I haven’t heard anything out of the Fed since then. So that’s where the needle is now stuck, and we’ll have to wait till we get there to see if the Fed moves the needle.

Small Banks and the CRE

Per GS, it appears 80% of all commercial real estate lending goes through small and medium (<$250BN) banks

JPM calculates that per the Fed's weekly H.8 data, small banks have accounted for the lion’s share of CRE lending relative to larger banks. As of February 2023, small banks account for a staggering 70% of total CRE loans outstanding excluding multifamily, farmland, and construction loans. If the mortgage spreads are expected to remain wide, CMBS spreads will remain wide as well.

As JPM fears"what started as a spread widening episode in IG mezz in the week leading up to SVB’s collapse has infected AAA CMBS this past week regardless of format." What was a lingering and contained CRE issue until the recent small bank crisis, has spread across the entire CRE risk stack, and is now a ticking time bomb that threatens the solvency of the entire small bank sector.

For Fed/CBers it is 'whake a mole' game, being repeated again and again. Interesting days are ahead.

NO, NO, NO. 80% of CRE lending by BANKs goes to mid-size and smaller banks.

The MAJORITY of CRE lending isn’t in the banking system but with investors via CMBS, insurance companies, PE Firms, pension funds, bond funds, Blackrock, you name it.

This was BANKING data only. JPM was clear about that. Good grief. Don’t people have a brain anymore?

Quit dragging this BS into here that you pick up out there. I saw this shit too. I know where you got it from. If you want to wallow in this stuff, fine, but don’t drag this shit into here.

Thank you again for keeping this important topic in front of your readers. I agree the majority of CRE loans have been offloaded by banks to other entities. But a very significant portion remains on their books. According to an article by the Financial Times today “Small Banks, big reach”, quoting Barclays analysts who expect office valuations to decline by 30 percent over the next few years, “In a severely adverse scenario in the Feds latest round of stress tests, large regional banks had the most ‘overall downside potential’ from the commercial real estate”. There are some good charts which don’t copy over.

Banks have $2.8 trillion in CRE loans, roughly 12% of their total assets of $23 trillion. Total CRE value is estimated at around $20 trillion.

Some CRE segments are doing well. Others are starting to wobble. CRE isn’t just offices and retail. A lot of retail loans have already been written off or written down because that has been going on for years. Banks have set up loan-loss reserves to cover additional losses.

But yes, some regional and smaller lenders are heavily exposed to CRE, and Rosengren when he was still head of the Boston Fed had been pointing at that years ago, that was his thing, and he said years ago that some smaller lenders will fail because of it, and the rest will lick their wounds and get through it.

Sure, the office sector is in trouble. That has been a theme here for a long time. Banks are a minor player in the office sector, and the office sector is only a portion of CRE.

Thank you for making clear what is accurate and what is false.

Well done!

Wolf

“CMBS, insurance companies, PE Firms, pension funds, bond funds,..

These are apparently under ‘shadow- banking’ system.

Where do they get money/loan/funding PREDOMINANTLY from to buy these CRE properties?

TBTF Banks, Regional or small to Medium ones?

My apology if I seem continue to bother/fester you. I wanted some clarification on this issue. Thank you, for your patience.

“Where do they get money?”

— CMBS are purchased by bond funds, insurance companies, etc. A lender writes the mortgages, securitizes the mortgages into CMBS, and the SELLS the CMBS to bond funds etc., which get their money from 401k holders, etc.

— Insurance companies get their money from premiums of the insured.

— PE firms get money from investors in their funds.

— Pension funds get their money from contributors to their pension plans.

— Bond funds (mutual funds) get their money from investors buying them.

Banks are not exposed to these loans. Banks hold their own CRE loans.

Wolf

My previous 2 comments as a response(above) to you, have been deleted without counter response. I understand this is your blog and your right.

Thank you.

You didn’t even read my comment, or didn’t understand what it says, and you came back with unrelated BS including a copied WSJ article from 2021. You didn’t even read the date!!!

READ MY COMMENT and attempt to understand what it says.

Your original comment was an intentional mis-reading of what JPM said. You picked that BS up at ZH, and the error is with ZH. I told you so. And you came back with more BS without understanding where you and ZH screwed up in reading the JPM data. You piled BS on top of BS, there is no discussion possible.

the “linguistic bureaucracy” especially of the financial economy overcomes the worst terrors of Kafka

Well said. The term like “Force Majeure” (I haven’t seen that weasel word masterpiece for a while, but they way things are going I do not doubt that we may see it again VERY soon) and other gems of financial legerdemain like that word, “Convertible” (to whatevah “instrument” it says right there… except for that “probably nevah gonna happen” fine print) should communicate Caveat Emptor loudly to anyone with common sense.

From now on the AT1 bonds are known as CoCo Puffs….

Perfection!

love it dj:

thanks,,,,

Snap, Crackle and POP!

Has anyone seen any reference to the status of various ETN’s issued by

CS such as USOI, SLVO…etc?

I mostly washed my hands of all this last night Mr. Richter while reading your rebuttal’s in your comment section.

It is easy to do for me as I have near zero exposure to the banking syndicate. No skin in the game so to speak. Still I find it entertaining, saddening and maddening if I think what could have been possible for honest folks lives if this corrupt repeated swindling fraud never started.

I agree I have had enough of Credit Suisse as you have.

Wolf – on a somewhat related note, what are your thoughts on the central banks changing the international credit swap lines last night from weekly to daily, to increase dollar liquidity. Meaningful or a nothing burger?

Item #5 (I posted this 3 times yesterday, LOL)

1. Those swap lines have been open for many years, and I have been reporting on them monthly in my Fed balance sheet update for a LONG TIME. And now they’re new? LOL

2. Swaps are not QE; they’re an exchange of currencies. 7-day swaps unwind after 7 days, the Fed gets its dollars back, and the other central bank gets its currency back.

3. not “worldwide”: but Bank of Canada, Bank of England, Bank of Japan, ECB, and the SNB.

4. Today they changed when the 7-day swaps can be initiated. Used to be once a week. They changed it to any day of the week.

5. The change seems to be designed to give dollar liquidity to SNB (in exchange for CHF) for the UBS-CS deal on Monday.

6. The SNB last used those swap lines in Oct 2022 to provide dollar liquidity to CS. After a few weeks, the last swap was unwound and the balance was 0.

This is the exact wording from the Fed:

“To improve the swap lines’ effectiveness in providing U.S. dollar funding, the central banks currently offering U.S. dollar operations have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 20, 2023, and will continue at least through the end of April.”

Got it – thanks!

Spot on but it’s getting better.

Bank of England is real still.

Bank of Germany holding on barely.

Didn’t they expand these swap lines to like 36 and 49 days or something before? Forgot the number of the days the loans could be initiated as paid back, at that time from recollection, indefinitely.

Next: First Republic Bank.

“Until recently, the bank, based in San Francisco, boasted $176 billion in deposits and an enviable list of wealthy clientele.”-NY Times 3-20-2023. It operates 93 offices in 11 states primarily in New York, California, Massachusetts, and Florida. It’s about one-third the size of Credit Suisse. Expect the FDIC to declare its failure to be a systemic risk. A director of First Republic: “Ms. Shilla Kim-Parker is the CEO and Co-Founder of Thrilling, a venture-backed, climate tech company in the apparel resale space.”-First Republic website. I wonder what a “climate tech company in the apparel resale space” is.

Looks like another SVB.

Maybe she rebranded Good Will & St Vincent stores.

Someone installed an air conditioner in a junk store window?

That’s just what Fred Sanford would do. He would define his business as a “climate tech company in the luxury items resale space”.

#4 bank crisis this month.

I’m not even going to look at this one.

Expect many more by next weekend.

There is a way to stop this financial catastrophe.

It’s going to cost you 25% of one 10th a silver 1961 dime for my solutions.

Not even a single peanut?!?

A lot of sad financial elephants out there….(grin)

Wiping the AT1s while preserving some equity value may be legal but it doesn’t seem smart.

…anymore? Hardly, if ever, is better — especially of the investors.

My understanding of the situation is that people may have in fact read the fine print but that since CS didn’t actually go bankrupt or meet the other fine print conditions, the AT1 bondholders should not have been wiped out. I think there is a big difference between people not reading the fine print and people reading the fine print and FINMA changing the rules mid-flight. It seems there is a lot of rule changing in the middle of the game going on lately (e.g. FDIC insuring all SVB deposits). Wolf, what are your thoughts on which clauses actually reduced AT1s to 0 before the shareholders?

In this animal farm utopia of equal rights before the law, when the zero sum game shows up, you get to find out whether you are one of the more or less equal ones.

So Wolf, I think you’re both right and wrong in blaming the AT1 bondholders for their predicament.

First, you’re right. Swiss AT1 bonds have unique provisions that the rest of the European banks (falling under EU regulations) don’t have. Which means UBS and CS CoCo bonds are somewhat unique.

The biggest uniqueness is that they’re actually not convertible to equity. They can only be written down. Normally this isn’t much of a distinction, because if the shares have already been written down to zero, then who cares whether you’re written down or converted to shares worth zero? The effect is the same.

But in this case, where the shares actually do have some residual value (albeit peanuts, as you say), the difference between a direct writedown to zero vs. conversion into equity shares actually does make a difference. Regardless, this shouldn’t affect non-Swiss bonds because I believe all of those don’t get written down, they get converted into equity.

And second you’re right that the fine print never mentions that equity shares have to go to zero before the bonds get bailed in. The bonds trigger based on when a bank’s capital ratio falls below a specific level. It says nothing about share price. Technically, bank can fall below that level and not be bankrupt, and still have shares trading at some (probably distressed, but non-zero) level. So there was never any guarantee in the fine print that the shares would go to zero before the bonds get written down.

So I think that legally, the Swiss regulators were within their rights in what they did. IANAL and I’m certainly not a securities lawyer, and when $3bil is on the line, there will be very expensive lawyers duking out this very question, so who knows what they conclude, but I agree with you that what they did seems legal and well within the terms of the bonds.

But I think you’re wrong in that, by violating the spirit of seniority, they’re doing a lot more damage than whatever benefit they felt they’d gain by giving $3bil to shareholders instead of bondholders. Yes, it makes me vomit a little defending vulture funds who gleefully hold their clients to the fine print and then scream “no fair!” when FINMA does it to them. But subordinating the AT1 bonds to shareholders, even if legally within their rights, sends a really bad message and will basically shut down the entire AT1 market, thereby eliminating one of the major legs of the financial reforms put in place after 2007/8.

AT1 bonds had 2 big advantages (for banks and regulators): their clear terms about when they would be automatically bailed-in, and their perpetual maturities reducing rollover liquidity risks. Without AT1 bonds, we’re back to what we had before the GFC, which was senior unsecured debt, which, while technically available for bail-in, usually ends up being a drawn out political battle to force write-downs. They don’t get converted fast enough to deal with fast-moving market conditions.

And to what purpose? What exactly are the Swiss accomplishing by giving the shareholders $3bil? If they had simply wiped out both shareholders and AT1 bonds, allowed UBS to keep the $3bil and reduce their own guarantees by the same amount, FINMA would have done a bigger service to Swiss taxpayers than what they did now. With the added benefit of not spooking the rest of the AT1 market, including the AT1 bonds of UBS, who is already looking shaky absorbing the mess that is CS.

If upending the norms of seniority (even if not actually violating any laws) was done for some greater good, then maybe it was worth it. But I don’t see any greater good here. Unless the Saudis were threatening to Jamal Khashoggi the SNB chief, I don’t see what purpose was served by throwing $3bil to the shareholders. And certainly raising the cost of capital for UBS, while reducing investor interest in its bonds, can’t be considered a good thing at this moment in time.

So yes, legally what they did was (probably) perfectly fine and even I love the schadenfreude of people who live and die by screwing over people on the fine print getting screwed over themselves by the same tactic. But aside from the schadenfreude, I fail to see what purpose was served by their actions.

If off he washed his hand of this days ago.

Try to catch up

Lune,

Can I follow you?

I’m into this

” But subordinating the AT1 bonds to shareholders, even if legally within their rights, sends a really bad message and will basically shut down the entire AT1 market, thereby eliminating one of the major legs of the financial reforms put in place after 2007/8”.

I know it’s to simple for FED not to do?

Great post! Thanks for laying this out so clearly.

I’m missing when the Swiss taxpayers gave $3bill to the CS shareholders? What do you mean by that exactly?

Tom,

They didn’t give money to CS. But what they did was guarantee future losses.

UBS paid CS shareholders $3bil. In addition, UBS agrees to take the first $5bil in losses on the winding down of CS’s assets. And then FINMA agrees to backstop the next $9bil in losses after those $5bil (I believe those are the terms, but the numbers may be slightly off).

If FINMA didn’t force UBS to pay out the $3bil, they could have let UBS keep that money but be on the hook for the first $8bil in losses rather than $5bil. UBS’s net exposure to losses would be the same, while Swiss taxpayers would have more protection before having to pay out any losses.

Now this may not matter if CS’s losses are $17bil. But anywhere in between those numbers, Swiss citizens will have saved money.

Sorry, last sentence should be it may not matter if CS’s losses are less than $5bil or greater than $17bil.

Lune,

Thanks the for further explanation.

All I can say is 50,000 jobs and $570bln AUM is no small cookie to swallow.

Great post, Lune. Unintended consequences inbound …

Anyone find it funny: plain old bank deposits are on “hair trigger” for running for the exits, AND YET, exotic CoCo perpetual bonds, with dense legal terms and conditions attached find buy and hold investors who are “shocked, shocked, i tell you”! Bizarro world.

It’s all about yield.

Remember when Milton Drysdale was worried that Jed Clampett would pull his millions out of his bank ? I imagine that

scene is being played out in the minds of

all small town bankers .

Lol wasn’t Ella May trying to Elope.

BTW Ella May was portrayed by Donna Douglas in all 274 episodes.

She is and still is a real pin up girl.

Curious what people think. I was looking for companies that just seem overvalued and found WDFC, the company that makes WD-40. Sure it is a very stable business, but revenues are declining and yet it trades for 40 times p/e. I also noticed it had 93% institutional ownership. Seems like the high p/e ratio is just held up because the institutions are just willing to park money there because it has low risk.

So I am curious if people feel that there are many companies that have very high institutional ownership and are very stable, yet highly overvalued? And could these type of companies come under pressure from selling if institutional owners need to raise cash levels?

They’ll jettison the “cats and dogs” before they dump the staples. But, when push comes to shove, “when the paddy wagon shows up, even the good girls go to the slammer.”

Absolutely agree that stocks are vastly inflated. The P/E ratio indicates how many years it would take for a company to just earn back the price of the stock, let alone profits. These valuations are based on the greater fool theory or people had no choice but to play the stock market casino due to the Fed’s repressive interest rate policies.

The following ensure that the stock market casino keeps going:

(1) Preferential tax policy of 15% on dividends versus interest

(2) 401(k) contributions in the hands of large financial institutions which can roll the dice as they please without any control invested in the wage earners. This also allows these financial institutions to cream away a piece of the income as management fees without any risk whatsoever.

A whole lot of policy changes including a basic tax-free bank interest of 4-5% and more investor control of their 401(k) – are necessary to keep the economy growing in a sustainable way. This will allow retail investors earn reasonable returns from their savings without taking excessive risk.

Anyone see this happening? I don’t. Not in a million years.

game – my understanding is that WD40’s late inventor and controlling interest stood firm that the company manufactured/marketed ONLY ‘WD40’, and nothing else, having become such a big dog in it’s field that, like ‘Xerox’, it became part of the common lexicon, as well as the field’s reliably-dominant product. Subsequent to his passing, the company has placed its imprimatur on a wide range of automotive chemicals – a crowded, competitive market (rife with snake oil), but with none of those products, unlike the one that ‘brought them to the dance’, having any features to truly distinguish them from the existing competition. (See ‘Growth via Designer Label Effect’).

may we all find a better day.

While reading clauses is important in this case, the way that FINMA handles on Coco bonds is an absolutely joke.

In order to be converted into ordinary shares or completely written off, there are generally two conditions:

1. CET1 capital ratio falls below a pre-determined threshold;

2. The bank itself or regulator declares Point of Non-Viability (PonV).

In the case of CS, its CET1 capital ratio of 14% is still far beyond the threshold which is publicly known and has been reiterated by CS, Swiss Gov and presses. Thus, point 1 above is not applicable.

For point 2, the Swiss press conference held on Sunday where Swiss regulators had explicitly emphasised this is not a ‘bailout’, but rather, a commercial deal excised by UBS along with the assistance from Swiss gov. Point 2 is also not applicable.

I believe the market is getting shocked not because of reading clauses properly but the fact that Swiss declares at their discretion to still write off the Coco bonds despite the general conditions to trigger LAMs are not met.

LOL. There was no more CET1 capital. It was all gone. It was fake, and everyone knew it. That’s why the buyout required the huge backing by the government and the SNB. UBS bought a gigantic hole.

but how is it possible that CS had an investment grade ranking (it still has BBB+)? And how it had sufficient regulatory capital according to last reporting? How should we treat ratings for other banks?

SVB also collapsed with investment-grade ratings, LOL

https://wolfstreet.com/2023/03/11/svb-financial-had-investment-grade-credit-ratings-from-moodys-and-sp-up-to-collapse-then-ratings-got-slashed-in-one-fell-swoop-to-default/

“How should we treat ratings for other banks?”

Ignore them.

There seems to be a lot of scrapping the bottom of the barrel here tonight .

Take it for what it is.

A wipe out of thousands of good honest people.

F***ing discussing

There never were “good” and “honest” people amongst investors – how could there be!? The investment game is about taking other people’s time & money, right from the very beginnings of “The Market”, when contracts for slaves and spices from colonies were traded in coffee shops.

Working sucks, now go get a job…

Creative financing or whatever they call it, is a fail.

A big leg down is coming and then another and then another.

Gaming the system with lobbyists works, until it does not.

Nafda and the whole off shoring of work is playing out as a big fail in the US and Europe.

We are years away from the inevitable but it will come.

Get a Job!

I think a 60 stock / 40 ten year treasury portfolio returned around 13% annual returns for ten year period ending in 2022 while nominal GDP growth rate was around 4%. Add to that housing bubble 2.0 and it shows the wreck the Fed is having to unwind from Zirp policy.

One and one no longer equal two?

Smash those numbers until they do!

We are not even close to capitulation.

Lune,

You are way out in the baseball left field.

All these plays have come to past and is really old hat. The Bonds are wipe out right along with the treasures. That’s the killing field of this international financial chess movement.

Nah Nah Nah

Nah Nah Nah

Hey Hey Hey

GOODBYE!! CS

In the US, preferred stock is listed on the balance sheet under shareholders’ equity, not liabilities…

Mmm, “undeserving” is doing a lot of work there, not really liking the implication about those at the bottom, as if they are the only ones “leeching” off the system as Kennedy might frame it.

Most of America is getting the bill for quite a few other things, like foreign policy decisions, but hey, I’m the sucker for not understanding what “Defense” meant in Department of Defense.

Excellent well written article with a very good financial analysis.

….”shareholders would get totally wiped out first, and then bond holders would start taking their turn.”

Kinda makes you wonder just who is on the shareholder’s list.

Named as AT1 or additional Tier 1 Capital, or the way these markets operate, automatic teller 1.

I am not sure when the AT1 bonds were issued by CS. But if we assume they were issued 14 years ago as a result of the financial crisis and carried a 9% interest rate, then the bondholders received a 3.25% annual rate of return over the life of the bonds. (For a $1,000 bond, I modeled an annuity with14 annual payments of $90 each. A 3.25% discount rate gives an NPV for the 14 payments of $999.54.)

Different assumptions yield different results, but an original purchaser of AT1 bonds might not have done that badly in the zero interest rate environment of the past decade…

Over the years since the Financial Crisis, CS issued numerous CoCos. The 9%-er was a more recent one. I think the early ones had 5% and 6% coupons.

But yes, investors if they bought in 2012 and never sold, came out OK-ish. But anyone who bought more recently took a big bath. That’s always how it goes. Ideally, you would want to buy early and sell a year ago 😎

Yep. And they might even do better in the next decade if they buy some real thrash like DB CoCo’s and DB keeps being the unflushable turd that it is and remains steadfastly cirkling the drain. Which I belive it will.

Michael Milken started out making a ton of money on the fact that a well known bad situation is often exaggerated by “The Market”, meaning that yields on junk-y bonds can be grossly mispriced in relation to their actual risk.

Oh great! Jamie Dimon to Republic Banks rescue!!!! Stock up 35%.

Like I said before, we’ll know the economy is on sure footing when the names Dimon, Blankfein, Griffin and others are washed over like words in sand.

Banking is a utility, not a growth engine. We need structural changes, not increased ineffective regulation. Put the bank CEOs at the kiddy table while the adults discuss the plan.

“Put the bank CEOs at the kiddy table while the adults discuss the plan.”

The CEOs are the ones who decide who is at the table to discuss the plan. :(

I use the term “banks”, “leveraged hedge funds”, and “investment funds” interchangeably. It’s hard to tell the difference these days, but some of these businesses get access to low cost capital via government guarantees and systematic protection, while others must rely on legislative sway.

MW: Pimco and Invesco had the biggest holdings in Credit Suisse CoCo bonds

They don’t care. It’s just Other People’s Money.

Exactly. And they are siphoning away a tiny piece of the returns all the time and giving multi-million dollar bonuses to themselves. When the shxx hits the fan, they just claim that no one could have foreseen this happening.

Meanwhile, our 401k regulations keep the money flowing to them whatever happens.

Rinse, Repeat.

I’m CoCo for cuckoo clocks!

…stoppit, XC, just stoppit!

may we all find a better day.

Lol!

Bank problems? What problems

Stonks to the moon 🌝. What a country

There is a reason why these bonds are called “Additional Tier-1”.

It is because in the seniority structure of the bank’s Balance sheet, they are Tier-1, meaning they *should* take on losses last, after the shareholders.

If a bank issues such bonds as Tier-1 assets and has them in that seniority in the balance sheet while at the same time putting in a clause that says they are the exact opposite, that Shows that Switzerland as a financial market might not be the Switzerland we used to know any more.

But the brand name obviously still works.

Looks like the Swiss regulators realized they accidentally were about to detonate a financial neutron bomb and 7 Seconds before it went off a Double-o agent came to the rescue.

They called it off and Tier-1 still means Tier-1.

These guys are dangerous.

Bonds get hosed while some shareholders get their money? Seems like all the “rules” have been abandoned. Just to save someone’s (?) bacon. How the heck can anyone invest with rules changing like this?

I wish I could find the document with the clause everyone is talking about enabling this. It really highlights to me how everyone parrots assertions without anyone citing anything, which could cause a lot of woozle effect in the world.

Here is the document for one of the Tier 1 Capital CoCos. I uploaded the PDF to the Wolf Street server to have it on hand in case the CS website vanishes.

Look for “viability event” and “Write-down event”:

CreditSuisse-t1-xs0989394589

(a) Subordination

In the event of an order being made, or an effective resolution being passed, for the liquidation or

winding-up of the Issuer (except, in any such case, a solvent liquidation or winding-up solely for the

purposes of a reorganisation, reconstruction or amalgamation of the Issuer or the substitution in place

of the Issuer of a successor in business of the Issuer, the terms of which reorganisation, reconstruction,

amalgamation or (except in the case of a substitution effected in accordance with Condition 13(c))

substitution (x) have previously been approved by a meeting of Holders in accordance with Condition

13(a) and (y) do not provide that the Notes shall thereby become redeemable or repayable in

accordance with these Conditions), the claims of the Holders against the Issuer in respect of or arising

under (including, without limitation, any damages awarded for breach of any obligation under) the

Notes shall rank (i) junior to all claims of Priority Creditors, (ii) pari passu with Parity Obligations and

(iii) senior to the rights and claims of all holders of Junior Capital.

sounds to me like they were not treated senior to Junior Capital.