Not learned a thing since the Financial Crisis. Relying on ratings, preferred stock holders found themselves bailed in, bondholders got crushed.

By Wolf Richter for WOLF STREET.

Let me just divert your attention for a moment from the collapse of SVB Financial and what it might and might not mean for the financial system or the startup bubble or whatever, to another troubling aspect of SVB Financial that shows that no one has learned anything since the Financial Crisis, least of all the credit rating agencies.

So you know what is coming: The solid investment-grade rating on a company – SVB Financial – that then collapsed with its investment-grade rating, taking investors down with it.

On Wednesday March 8, Moody’s still had an A3 rating on SVB Financial, owner of the now defunct Silicon Valley Bank, as it was already collapsing for all to see. Four notches into investment grade – a very respectable rating!

In the evening of that day, after SVB disclosed a $1.8 billion loss on the sale of bonds, a planned capital raise, and a slew of liquidity measures, Moody’s downgraded it by just one itty-bitty notch, to Baa1, still three notches into investment grade.

Then on March 10, after Silicon Valley Bank was shut down and put into receivership, Moody’s downgraded SVB by 13 notches in one fell-swoop, all the way across junk territory, to its lowest rating, to C, which is Moody’s rating for default. And it said that it will withdraw the rating.

That’s how worthless these credit ratings are if you rely on them for your bond holdings. But they’re good for your amusement, apparently. Here is my cheat sheet for corporate bond credit ratings by rating agency.

Similar with S&P Global Ratings: On March 9, a day behind Moody’s, it downgraded SVB Financial by one notch to BBB-, which is still investment grade.

Then on March 10, after SVB Financial collapsed and was taken over by the FDIC, S&P slashed its rating by 10 notches all the way through junk territory to D, for default, its lowest rating.

Holders of its bonds and preferred stock (like bonds, a liability on the bank’s balance sheet) got the rug pulled out from under them.

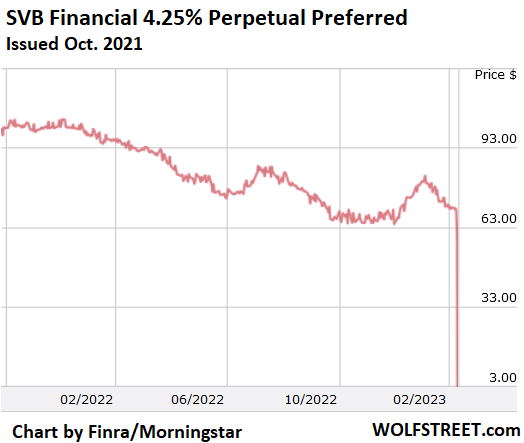

For example, based on bond data from Finra-Morningstar, the $1 billion of 4.25% perpetual preferred stock, which will get bailed in along with shareholders, collapsed in two days from 70 cents on the dollar to 3 cents on the dollar at the close on Friday.

There are five issuances of this type on its balance sheet that got wiped out, combined $3.7 billion. All of them were issued during the Free Money era in 2021.

The good part for uninsured depositors is that this type of debt is designed as a buffer and will get bailed in, thereby removing a liability from the defunct bank’s balance sheet, and leaving more funds for unsecured depositors. So those preferreds are doing their job.

But for investors, it would have been nice to get prior warning from the credit rating agencies that this stuff is maybe not investment grade after all, but junk that needs to come with high yields, before getting thrown off the cliff.

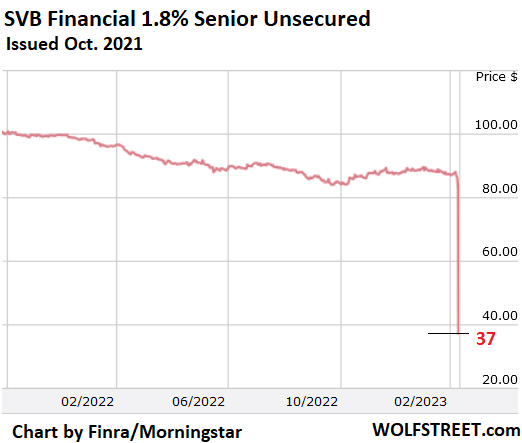

In terms of bonds, for example, the $650 million 1.8% senior unsecured notes, issued in October 2021, also during the Free Money era, plunged from 86 cents on the dollar on Wednesday to 37 cents on the dollar at the close on Friday. Investors who’d relied on the credit rating agencies to protect them from this fiasco got creamed:

Companies obviously go ratings-shopping when they need to raise funds by issuing bonds, because a lower credit rating will cause the bond to have a higher coupon interest, and higher yield, meaning more interest expense for the company. And so there is huge pressure on analysts to come up with a high rating, or the other side of the rating agency will lose this business to a rating agency that will rate those bonds higher. We truly have learned nothing, not even bondholders, who should simply ignore those ratings and do their own homework.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

You should have left the LOL in the article title :)

People complain about this stuff (my sense of humor isn’t always appreciated when a bank collapses).

After tragedy & farce, humor is the only appropriate lens through which to look at anything damn’d thing anymore. Mine is welded in place.

This may (or may not) be the time to point out the exception to the rule: Nothing goer to heck in a straight line.

Wolf, your site, your rules, and some of us appreciate a good laugh…else we’d all be crying instead or heavily medicated like a larger percentage of modern humans today.

Laughter is better than anger, yet few have issues with anger and yet get angry if you laugh at the “wrong” time or “wrong” thing. The laughter cops need to chill as studying those who live the longest, they tend to have a very deep sense of humor. So thanks for helping us live longer…HA!

As far as your rating cheat sheet, the first thing I thought was where is the “GFF” rating (Got Fed F-ed)…HA!

NAH, it’s the CC rating that’s the big one.

Corporately Cornholed

Also a play on a “sport” with an odd name played by those ignorant fools who WILL vote in a savior, for both this life and the next. (Cornhole had a definite meaning when I was in public school and it had nothing to do with tossing beanbags :)’ .

They will be VERY unpleasantly surprised on the first one, and never aware of the second, once they cease to exist as organisms.

“..And behold, along came Yellen of the Fellons, with her not-QE not-bailout ‘special vehicle’ weapon to slay the dragon of iliquidity.” (aka insolvency)

Weapon of Mass Liquefaction – WML 😜

I wish I’d seen the original! An article on all the (other) articles you’ve retitled after second thoughts would probably be a source of great joy for most of us! 😂

I’m appreciating the lol with…….

Good article.

Watered down Volker Rule probably played a similar role in general “inattentiveness”.

I wish Reagan hadn’t destroyed the unions and forced the Dems to switch to Corporate money….resulting in the “do nothing” Congress, I’m afraid.

DAMN!

I just read the next article!

Sticking it to shareholders is a pathetic comfort, especially since the less wealthy ones are in index funds.

Sorry Abe, REALLY truly sorry, but we are a stupid spoiled selfish people.

Go join a Christian church, or shoot dope.

“Man is born free and everywhere he is in chains.” “Man will never be free until the last king is strangled with the entrails of the last priest.” “The world of reality has its limits; the world of imagination is boundless.”

That was from another time, but still all true. I’d update it to the present American situation by inserting “kingS are”, and “organized revealed religion leaders” as “priest” is just one church of many….the one that kept us in the dark ages, though.

Makes you wonder why all the bitching about the CCCP?…..I guess they all SIT (not meet) together OPENLY, or at least the top ones do, so it’s more obvious?

If congress critters all wore corporate logos of various sizes, depending on amount of support (Just like race car drivers!) BY LAW, it would REALLY help sort them all out.

We already know which State or district they are for.

Sure would be great to get back to old style “corruption”, pre lobbyist, yes?

My guess is that time was 1800-1820-30ish?….or less….the States went down first….and fastest.

But they did call them Borers back then…much more appropriate.

In the nineteenth century, lobbying was mostly conducted at the state level, but in the twentieth century, there has been a marked rise in activity, particularly at the federal level in the past thirty years. While lobbying has generally been marked by controversy, there have been numerous court rulings protecting lobbying as free speech. At the same time, the courts have made no final ruling on whether the petition clause of the US Constitution covers lobbying.[1]

Your article is both poignant and a sad commentary about my ability to ascertain value vs price, a fundamental precept of the higher business education industry.I could search appropriate bonds in the AAA category up until about 2000 or so with confidence that the rating agencies had correctly categorized the risk of the likelihood that the borrower would pay the money back. The street is selling the myth on a mound of lies. A former champ selling themselves on the corner.

The pillars of the community are pathological liars and criminals. Enticing people into overvalued securities for the vig.

We’re not talking about the wolf of the wall street dumpster.

We are talking about the private network of debt rating agencies who were selected by the Federal Government to price they’re trillions of dollars of issuance. The bond market went from the rock of Gibraltar to the rock that weights down the body.

We deserve a Postal Service bank.

A VERY GOOD idea. I know from personal experience the Postal Inspection Service were sharp, well trained (starting with a 4 year degree as an entry level requirement), and dead serious. (Although they could easily spot a run -of -the mill management vs worker beef and brush it off, as I found out a couple times)

Like in the Matrix, they were everyone, and no one. Had their own secret entrances, galleries, and private exits onto work room floor for busts. I saw one, a guy was taking gramma’s $20 out of Xmas mail. And yes, they had many with accountant degrees.

If they have been gutted like a lot of other Federal Agencies, they would have too be brought back up to pre-1990s strength.

I imagine some would scream “Socialist” (or Commie), which seem to have been equated in a lot of BSd minds.

Since they don’t have to make shareholder profit, they could also reduce the “fraction” in “fractional banking”, the basic source of all our problems, IMHO.

Like why is 2% inflation needed or normal??????

Increase the fraction…but I think everyone got the gist of it.

PS-A string of afterthought comments seems to both our MOs sometimes. Guess it’s OK, not deleted.

Not to poop on your party but the FED just announced an emergency loan program for banks to ease the contagion risk. In addition, regulators say SVB customers will get all their deposits. Money printer go brrrrrrr

Davis,

You need to read the details, in terms of brrrr

https://wolfstreet.com/2023/03/12/silicon-valley-banks-uninsured-depositors-bailed-out-crypto-signature-bank-shut-down-all-depositors-bailed-out-senior-execs-fired-all-shareholders-some-bondholders-bailed-in/

The way it seems to work, with lots of tough love in the statement:

1. The Fed gives the money to the FDIC as needed.

2. The FDIC makes all deposits available on Monday.

3. The FDIC then sells the assets of the banks, which takes some time.

4. The difference between the cost of bailouts of the depositors and the proceeds from the asset sales is the actual amount the FDIC lost.

5. The FDIC charges other banks a “special assessment” to cover those losses, “as required by law.”

6. And it may then pay the Fed back with those funds it collected from other banks?

“….For UP TO A YEAR”

Unlike its more byzantine efforts to rescue the banking system during the financial crisis of 2007-08, the Fed’s approach this time is relatively straightforward. It has set up a new lending facility with the bureaucratic moniker, “Bank Term Funding Program.”

The program will provide loans to banks, credit unions, and other financial institutions for up to a year. The banks are being asked to post Treasuries and other government-backed bonds as collateral.

The Fed is being generous in its terms: It will charge a relatively low interest rate — just 0.1 percentage points higher than market rates — and it will lend against the face value of the bonds, rather than the market value. Lending against the face value of bonds is a key provision that will allow banks to borrow more money because the value of those bonds, at least on paper, has fallen as interest rates have moved higher.

LOL, yes?

Do companies pay of thier credit ratings? Or do investors pay for credit ratings to talk up thier books? All this credit rating effort can’t be for free.

Is there a conflict of interest possible?

It’s not only Silicon Valley. There are many banks in Seattle that deal big with VCs, startups and Tech companies. My bank CEO sent a mail yesterday to “Assure” me that while my bank is good partners with SVB, they are way safer. Only thing it did was to reinforce my resolve to reduce cash below $250K.

Only thing is cash is so hard to deploy! You can lose it in so many places. A lot of folks may say bonds are safe, but I feel there is a big possibility that interest rates keep increasing.

Yes, companies pay Moody’s, S&P, and Fitch to rate their bonds. And yes, that is a huge conflict of interest, and yes, this was a huge theme during the Financial Crisis when their AAA-rated MBS collapsed, and nothing ever got fixed.

This dates back to around 1974 to my recollection, when Congress passed that law providing for credit rater accreditation.

I think it was the SEC changing the relationship. Prior to that, prospective investors paid the ratings agencies to perform independent analysis of companies. Now, the companies in question pay to get the ratings, resulting in the corruption.

Can rating agencies ever be truly accurate? The rating itself impacts the entity being evaluated. An upward/downward feedback loop can easily result. How do rating agencies allow for market emotional swings? How timely must they be, accurate as of the last 24hrs, a few hours/days? Seems an impossible job, except for very stable conditions, but as we have seen, conditions can change very quickly. So a once solvent bank becomes insolvent within days. Not to mention the conflict of interest of having the evaluated companies paying them.

It was enough to open the latest SIVB 10-K filling to figure out the risk embedded in the HTM portfolio during rising rates.

Moody’s had 13,460 employees, as of December 2021. There is really no excuse for rating agencies to default on their rating function.

What’s the name of that movie. Um um. Now I remember, The Big Short.

It’s hard to believe that some carrion-consuming law firm hasn’t turned this into a class action.

…whiffs of, what was it called?, oh yeah: ‘protection racket’, but as practiced by the more genteel…

may we all find a better day.

“If we don’t give them the ratings, they’ll go to Moody’s right down the block.”

Short-term treasuries = zero default risk (well, maybe, we’ll see in a couple of months) + negligible interest rate risk.

If you don’t like managing these yourself, you can get an insured cash sweep vehicle — FDIC insured while investing in short-term treasuries, no $ limits — but you are taking on some 3rd party risk.

Amen. Also, the demands being made now show the vice of the current system: demands are being made that the US government guarantee all bank deposits, unlimited as to amount, even CCP members or other depositors. That means that ALL Americans would suddenly become collectively liable for GINORMOUS, trillions of dollar sums for all recklessly run banks: over 250,000 per depositor (not just the 250,000 within the FDIC insurance limits) and for FREE!

That is why many commentators, and I, regarded the Dodd-Frank, fake reforms as a boondoggle: the depositor bail ins ultimately supposedly to be used after other funds were exhausted were political, poison pills: they were designed to coerce more free money out of the US taxpayers, because congress persons would feel the pressure to bail the depositors out (even for uninsured sums over 250,000) once those depositors faced bail ins to avoid panics. This is how federal liabilities (over $211 trillion already as estimated many years ago) become unsustainable!

I know that letter.

If you put it into your wood stove, it is sort-of useful.

The entire financial system is one giant fraud. Moody’s was also rating all of the subprime junk last housing bubble at AAA. They should have been shut down.

Beyond this, the banks don’t even have capital reserve requirements anymore. And there’s no more “mark to market,” either. All of this after the 2008 crisis.

Nothing was learned alright. In fact, they decided to double down and go even harder.

There are “capital” requirements, but there are no longer “reserve” requirements.

Reserves has to do with how much cash banks have on deposit at the Fed, which is a liquidity measure. There are now $3 trillion on deposit at the Fed (the Fed calls them “reserves”), which is a huge amount, and which was the reasons reserve requirements were removed because they were small to begin with (the erstwhile “required reserves”). Before the Financial Crisis, required reserves were below $50 billion. When they were lifted in 2020, there were $200 billion. Compared to $3 trillion in reserves today.

Banks such as Silicon Valley Bank get shut down when they fall through the capital requirements because they’re deemed insolvent by then.

I am sorry, I meant “reserve requirements.” Thank you for clarifying. I wish I could change it.

No problem. Gave me an excuse to explain the difference. It does come up every now and then 😍

Inflation on Station.

I read an article today that talked about how the US guverment wants as many small regional banks to fail as possible, which creates Big merger opportunities for the already “too big to fail” Big Banks. Then it’s an easier path for the implementation of a CBDC.

I can’t help but believe this is all part of the plan. I also think it’s wise to remove oneself from the banking sector as much as possible. Bail ins will become s common theme.

DoubleD,

There is a line of thinking that the G would actually be happier with 80% fewer banks to regulate (down to 1000 from about 5000 now…there were 15000 in 1990…).

Post implosion 1.0 the G made it a lot harder to get new bank charters but, after a pause, was pretty okay with letting bank mergers get restarted.

My guess is that the G thinks it could focus more closely on many fewer banks, and “influence” them more closely as the front for central bank macro operations.

(Note that SVB was 15th largest bank…so much for the “laser focus” argument…)

(Although the other 4000 banks are so relatively small the Fed/FDIC can probably just ignore them from a macro perspective…but they still have to send examiners out to make sure those smaller banks aren’t utterly looting).

If the US had ‘only’ 1000 banks it would have still have 10 times the number of banks per person of Canada. Try and think of any other businesses with ten times the separate companies, not branches, per person. It’s not pizza joints or dry cleaners.

At 5000 the US is grossly overbanked. Note that after the demise of SVB, not a small bank, there is all kinds of concern about ‘small regional banks’. But why are there so many? Does Pleasantville need not just a branch but its own bank?

Parenthetically, it would be interesting to know if the number of US bank regulatory personnel is 50 times per person larger. 5000 is a lot of banks to supervise.

Commercial Real Estate: There is a saying in real estate that you make your money when you buy the property and realize it when you sell it.

The last Federal Reserve “stress test” had commercial real estate substantially losing value. That overpriced real estate was essentially sold to the banks by their loans, so the banks are going to need those huge reserves to cover the loses they will realize.

The residential real estate, less than 5 units, was purchased by the Federal Reserve through Mortgaged Backed Securities (MBS); however, there will be no problem with the banking system as that huge bubble of MBS was originated by Federal agencies and the taxpayer is directly responsible for loses not the banks; a huge improvement in banking since the last financial panic, maybe even planned.

So why aren’t the bank reserves available for SVB? Isn’t that the point of creating “excess” reserves. There should be a Wolf Street for Dummies. I don’t get any of this, including the SVB stock symbol listed on the Stuttgart exchange. Why is the financial stock separate from the bank stock? Apparently one business with assets waning is Landvest, a real estate and forestry management company, that’s not a tech startup. And what does all this have to do with Silvergate, in La Jolla, Ca., which has exposure to crypto and is also on the ropes? Is that what contagion means?

1. “reserves” = cash that banks put on deposit at the Fed. Only the Fed calls this bank cash “reserves,” the banks call them “cash” or “interest-earning cash” or similar on their books.

2. Borrowing from the Fed at the “Discount Window.”

SVB probably withdrew all of its cash deposits at the Fed (reserves) to fund the withdrawals by its own depositors. Close to the end, it had no cash at the Fed (no reserves)

Borrowing at the Discount Window might have occurred (this is not disclosed by bank, and we don’t know), but the Fed requires that a bank is solvent in order to use the DW, and this bank was deemed insolvent, so it couldn’t borrow at the DW anymore, if it ever could.

SVB had subsidiaries in the UK, Germany, China, and other countries. Some of them floated some of their shares at the local exchanges. For example, the SVB entity in the UK floated some shares in the UK, and those share stopped trading on Friday, the BoE is going to declare the entity insolvent and shut it down. I don’t think Germany has taken that measure yet. The China entity, which is a joint venture with a Chinese firm, seems to be still up and running.

Thanks Wolf, I assumed that reserves were a pool. Did SVB have RRPO outstanding? Finally does the activity of Founders Fund, Peter Thiel, pass the smell test? Maybe it wasn’t all on Moody’s credit ratings?

Nothing in this entire deal passes the smell test. The whole thing is reeking.

I think that is an important point… An illiquid bank that is still solvent can borrow from the FED to solve the liquidity issue. An insolvent bank can not. During the PennCentral crisis (1970?) the overnight corporate paper market dried up, and the big banks were able to provide corporate funding in place of that market because the FED was able to assure their liquidity via the DW (and some other reg changes like suspending Q, etc)

Wolf,

I heard a report that SVB had borrowed $15B at the San Francisco Fed early last week. They said the $15B was ~20% of the capital at that Fed bank. If this is true, then the first money recovered from bond sales will go to the SF Fed.

Also this analyst said SVB had no Chief Risk Officer and no hedges were in place to protect against the bond losses. Others have reported there was a CRO but she spent her time on diversity issues, not risk management.

It reminds me of how “analysts” upgrade a stock after it’s gone up by 30%. Good job guys!

Also, if you read any offering document, the rating agencies make very clear that they’re not responsible for anything and that you can’t rely on their ratings for anything. They’re really useless except for insurance companies and pension funds that by law can often only invest in rated securities. Nobody else actually thinks they’re worth anything.

Do the rating agencies bear any legal liability

Nope. The boilerplate engagement letters they make everyone sign make that very clear.

And the true absurdity is that all the key info to see the looming disaster was easily available on line via the mandatory quarterly banking reports…as multiple *next day* problem bank analyses have been generated (with a big assist from Factset).

Literally within one day, there have been multiple analyses identifying 20 to 100 banks with roughly similar SVB “underwater portfolio”/hot money depositor base problems.

If any ratings agency had even done a half assed job of analysis (of online records!!) they could have started downgrading 6 months ago.

And…a true analyst would have screamed about bank portfolio impairment/hot money after the second Fed rate hike…all of this is actually pretty damn straight forward.

cas127, on the flip side, the Fed created this problem. Without years of ZIRP, the banks’ supposedly safe investments in bonds and treasury bills wouldn’t be underwater.

Einhal,

I agree, 20 years of delusional ZIRP has poisoned the valuation sea in which all investments swim (ie, artificially drop the discount rate via money printing (inflation) and the DCF formula dictates all asset values increase…until discount rate normalizes…then valuations implode. See also, 2008).

But.

After 20 years…everybody and their dog in financial services *knows this*…so there is little excuse not to *mitigate* risks (diversify savings across invts/banks, lower invt risk profile, etc.).

SVB (and every bank) should have been feverishly working asset-liability mgt for the past year (at least)…ALM is *the core bank function*.

ZIRP handed banks a lot of crappy choices (what low yielding, risky invts/loans to hold in bank portfolio? 4% junk bonds? Grossly inflated MBS?…But the banks could have done a lot better – just shift to a lot of short-term Treasuries as they rose over the year…maybe a lot of banks did…if so, and they announce it clearly, the runs may stop. Ditto the uninsured bank account holders, whose CFOs could have simply Googled CDARS, Treasury ETFs/Funds, etc. Protecting short term Corp savings is the definition of the job of corporate Treasurer/CFO).

As with implosion 1.0, Fed ZIRP created the environment for catastrophe…but people were warning about it then and *many, many* more were warning about it pre Implosion 2.0.

But a certain segment of the investment community absolutely insisted on speculating wildly on the back of ZIRP (see insane inflation) and apparently had absolutely zero plan for post-ZIRP.

That is the part that is unforgiveable.

Absolutely correct! They learned how to double down, and go even harder! Anyone that didn’t see the start of this, will soon be howling at the moon. Let’s keep it rolling!

QE by design, encourages speculation, the reach for yield.

Once a bank is in trouble and has to sell their most liquid assets, they do have mark to market value because they have been sold. Having valued these assets at purchase price and avoiding “mark to market” did not help them at all and they had to realize the loss all at once instead, when they could least afford recording a big loss. Maybe the old rules were better.

If ratings agencies were doing their job and rating American debt at junk folks wouldn’t be thrilled with losing 2 to 10% annually on gvt treasuries. PT Barnum and Bernie Madoff were so right, only, now there are more suckers than ever!

Learned? Learning is not a helpful variable in a corrupt “game”.

Its possible that banks will fail more and more and This will lead the way for CBDC.

If only the other owners of banks, who have run them into insolvency with reckless gambles, could also lose all ownership to them like the apparently, relatively blameless owners of SVB are losing all ownership of SVB and its assets. America needs banks but not their recklessly greedy bank owners. They should be forced into a shortened version of Chap. 11 and liquidated or reorganized with their creditors becoming their NEW owners —which is what happens to legitimate (not politically connected) companies when they become insolvent.

How many crooks are currently still operating legally insolvent banks because they do not possess the moral fiber of the SVB control group? I suspect many.

If some reports are accurate, e.g. as to comtrol group members selling their shares recently, forget my compliment as to their good “moral fiber.” Am I the only one who remembers Rule 10b-5 and other securities laws? At least, it feels good that the bank control groups are acting as I have always expected. I apparently was a fool to believe recent, media reports as to their being innocent! LOL.

Most larger bank shares are owned by institutions and indirectly, by the beneficiaries and fund participants, not directly by “fat cats”.

But at least the insider/equity-holder fatcats are “first off the gangplank” – at least partially satiating the alligators below.

The alligators will still eat many/most/all unsecured bank creditors (and a fraction of a fraction of the $250k+ depositors) but better that the alligators swallow all of the insiders (whole) first.

Actually, the FDIC resolution system/process is fairly well designed/executed (as a result of many, many, many earlier goat rodeos) but right now the G needs much better *public explanations* of how things operate in practice.

For one, discussing how acquiring banks are encouraged to take over failed banks (via loss sharing agreements, etc) would help stop the rapidly rising panic over aggregate, assumed-100%-loss among every uninsured account holder in the entire US banking system.

Yellen needs to get her hobbit ass out front and do at least a Geithner-level job (ie, stop short of literally pissing her pants on camera).

Also pointing out that rising rates are only going to *reduce* (not 100% destroy) bank invt portfolio values (even SVB lost like 15%, nowhere near 100%).

All this should be do-able.

A mere “reduction” in a banks’ assets of 15% is fatal to a bank’s solvency: I doubt that there is now any bank with a 15% equity cushion after all assets are marked to market. Critically, equity holders in control of major banks could have faced PERSONAL liability, before the last, so called “reforms” for operating insolvent banks and paying themselves in illegal distributors— for years in many cases.

The bank mergers are NOT free to taxpayers. The purchases by one bank of a known insolvent bank are very harmful to ALL US taxpayers: the “white knight” acquiring bank is always a heavily, government-or-Fed-bribed bank and has government guarantees on all of the acquired, insolvent bank’s liabilities.

The depositor bail ins, which admittedly occur after the FDIC funds and all other US banks’ funds are first taken, are “well designed”—- to force the US government to insure even deposits over 250,000 and even those of crooks like of drug dealers, con men, other banksters, kleptocratic Putinists, CCP kleptocrats, etc., TO AVOID BANK RUNS. That is what was just announced.

The government thus just caved, as the ” reformers ” must have planned in their designs of “reforms,” just as it caved in 2008-2009 after Lehman Brothers. Instead, piercing of the bad banks’ corporate veils could have put the price of bailouts on the billionaires controlling the banks to go off financial cliffs. If the banksters had been forced into personal bankruptcies en masse, the banks would now not engage in so much gambling: bankers should not be able to continue to gamble risk free with effective government “guarantees” due to ultimate, government bailouts.

Such an easy fix ,make all executive,s forfeit their assets when they corruptly,steal ,as selling stock 2 weeks ago. No insider info my ass . Taxpayers will bail this shitshow out AGAIN.Where does it end

The pension administrators and other persons running institutions into the ground, so regularly, should be regularly wiretapped, because as the Libor Scandal showed, the financiers collude and collude and collude —-a lot.

Amen!

This entire “system” in the US has morphed into a rigged shell game where the rich have hijacked the government and are taking everybody else for a ride. And the moment one of their little Ponzis blows up, they cry for a taxpayer bailout and get it.

I am noticing more and more comments on social media sites like Twitter and Youtube where people are fed up with bailouts and are crying for all of these people/companies to burn. People love that SVB blew up and a bunch of rich people potentially lost billions. Eat your losses, pigs.

Did they lose though, or it is simply an average Joe with workplace 401Ks managed by financial groups?

Top institutional owners of SVB:

The Vanguard Group, Inc. 10.85%

SSgA Funds Management, Inc. 5.22%

BlackRock Fund Advisors 5.18%

Alecta Pension Insurance Mutual 4.46%

Those funds will still collect their maintenance fees as if nothing happened.

What’s great is it’s really showing all those “free market” “crypto bro” “hard money” “self-made billionaire” “taxation is theft” “libertarian” types who say the Feds can do no right, really really getting enthusiastic about state intervention to prop up their bad bets, even if they have to print the money to do it, because now suddenly it’s all one interconnected system and we have to maintain the integrity of the market.

Like the folks (Larry Summers, et al) out there who previously want to say federal student loans are immutable and essential to discipline people from making bad investments, but now the good ole boys club needs a lil bailout so they don’t have to sell their vineyards in Napa or second houses in New Zealand.

Classical Crony Capitalism: Privatize the profits, socialize the losses.

It’s pretty funny to see the Libertarian tech bros demanding SVB be bailed out by government before Monday so they can make payroll.

Even Mark Cuban is now complaining Federal regulators were too lax with SVB.

Libertarians are asking for bailouts??

Most SVB clients seem social justice, virtue signaling Cali celebrity and tech population.

LOL Peter Thiel and his huge megaphone? When it comes to their money, they’re all the same. They all want bailouts.

I haven’t seen any reports of him calling for bailouts. Have you? Or just speculating?

Didn’t he just withdraw his money and ask his connected startup ventures to do the same?

OK, I stand corrected. He didn’t call for a bailout. He just told his companies to yank their money out, which precipitated the bank run that caused the bank to collapse.

Thank you for the correction.

Peter Thiel will get the infamy for lighting the fuse. Won’t you however agree, the charge was all loaded in there ready to blow up anytime?

charge = high withdrawal rates by tech clientele, bond holdings that were losing value, poor risk management…

“He just told his companies to yank their money out” which is perfectly consistent with the two foundational Libertarian ethics of “Me First” and “Let them eat cake”.

Nice well deserved thumping you gave Nacho, HowNow!

Too bad “Most SVB clients seem social justice, virtue signaling Cali celebrity and tech population” is so damned poorly written it couldn’t be exposed and thumped as well.

There are many degrees of hypocrisy, but these “libertarians” are probably at the top.

Already seeing talking heads on twitter (including an elected representative from California) crying for bailouts.

I was too young to get what happened in 2008 at the time but if it happens again I will lose the last bit of hope in the financial system (assuming I still have it in the first place). aaagh

Public official…Swalwell…CCP-Spy-Fang-Banger/Shut Up Non-Nuke US Citizens Swalwell…of course.

Classic catch-22 with no way out once sentiment changes.

Door A: Let the depositors eat their losses as they should and have downstream dominoes fall including many insolvencies in the “start-up ecosystem” which mostly should exist anyway. It’s disproportionately based upon cheap money and losses lending form a fake economy.

Door B: Bail-out the depositors and their rich backers with the justification of saving jobs. Set precedent to bail out all depositors in the future leading to moral hazard “out the wazoo”. It’s already been on increasingly steroids since the 1987 crash.

There is no “Door C”.

Door C: another bank buys SVB at a nice discount, just like what happened in 2008. Isn’t anyone going to speculate on who it might be? Hint: who was telling firms to pull their money out of SVB a few days ago, which led to the final collapse…

Agreed…the FDIC has tools to incentivize acquirer banks (loss share agreements, etc)…and the actual underlying bank invt portfolio losses were like 15%…not 100% so there is a pretty decent chunk of residual value.

Hell, the VC community *itself* could/should/may Cobble together its own rescue/wind-down acquirer (as the allusion to Thiel above hints at…).

But somebody in a position of power (Wolf?…only sorta kidding…) needs to point this all out before hysteria gets worse.

Depositors are made whole even unisured

From what I understand, SVB didn’t try to hedge any of their positions. In other words, they did absolutely zilch to derisk their fixed-income portfolio. Seems like a rather incompetent move for such a relatively large bank.

That bank was so recklessly managed all around it’s breath-taking. Free money had turned these people’s brains to mush.

One more idea for the name: Brain Mush Bust

…mebbe ‘The Re-Peter Principle’?

may we all find a better day.

I looked through the bios on their executive team. Scary. The chief risk officer doesnt even have a finance background, just some degrees in public administration and poli sci. The President is a CPA with a bus admin BA. The Chief Credit officer has a BA in econ from Colby. These people all look like a bunch of connected fail up types that managed to work through the corporate systems of various companies and never even learned the basics of banking.

That said, if I try to be generous, maybe they just thought that the Fed balance sheet explosion last time left rates low, so this strategy would have worked if it weren’t for that pesky inflation! ha. Then they figured, oh look, its coming down fast, we are in the clear, thinking the pivot was soon and the markets would go back up and the money would roll in again. Or maybe they had such a long history with these companies that even in the bad times, in previous tech busts, everyone hung around and the bank didnt have big losses it needed to paper over. Or maybe they didnt realize the dbag clout of a Peter Thiel who might just be happy to have himself and his friends make out ok running away from this problem.

I dunno. It was one thing to have this kind of balance sheet prior to the inflation, but doing nothing after it took off, knowing for sure the Fed is going to raise rates and cause you a headache, that I cant seem to figure out. Perhaps if they had tried earlier to announce that theyd be raising capital, before the situation got sideways, they might have been able to do so. But their timing was awful on that as well.

My other worry is, how many other banks are in this same situation, with a mismatch on duration, and seeing a whole bunch of start ups go under, and a bunch of others pulling there funds and redistributing them if all in one basket. It’s a bit of a musical chairs situation, depending on whether some bank sees mostly outflows during a reshuffle and not a lot of inflows. Plus, the money is going to dry up more from VC no matter what, so that makes me think more banks are at risk. Marketwatch said 20 are high risk :

well, Monday morning is sure going to be interesting. I smell a bailout. Which sickens me. But I dont think they will risk contagion. As for the problems a bailout causes, well, that is another story.

It’s also hard to imagine that the people running Lehman and Bear and WaMu and AIG and Wachovia were complete morons, but in hindsight, they were. It really makes you wonder what’s next

When it comes to administrative financial jobs, college degrees have nothing to do with competence.

You can put a bunch of doctorates in the room and they can still be collectively moronic when it comes to making decisions. Yes there are a lot of jobs that are for the well-connected and certain degrees from certain institutions and a clubby environment insulate a large class of people from ever knowing what it is like to toil for a living.

But all of this has nothing to do with anything other than this institution being asleep at the wheel. Failure to diversify, failure to invest adequately, failure to have a back-stopped growth plan. All blinded by the allure of cheap money.

These fools are placed ,to run stuff they are too ignorant to run . They’re just puppets for rich ,well connected ,corruption. But at least he got out with 260 million .With no insider knowledge.Makes me laugh Rome is falling fast

The president of SVB, Joseph Gentile, was a former CFO at Lehman’s Global Investment Bank

I got serious FTX vibes, gotta wonder if SVB execs were into drugs and orgies too. I read one reliable source that when he dealt with SVB in the 2000s he was surprised by all the drug use.

Kernbern Asked:

“It’s also hard to imagine that the people running Lehman and Bear and WaMu and AIG and Wachovia were complete morons, but in hindsight, they were. It really makes you wonder what’s next”.

Wolf answered:

“Free money had turned these people’s brains to mush”.

There are a lot more “mush heads” out there than just SVB. Unfortunately, many of them gamble with our investments in some form or another.

kernburn & creditgb,

I worked at Bear in MBS in the early 1990’s. They thought they were geniuses because the money was pouring in, but the demise was clearly on the horizon. I could see it and thought the end was at most 5 years away, it took 15 years because they were able to refinance every bad deal until they couldn’t.

I think of it as, they were holding on, expecting that Fed pivot any day now, but it didn’t come in time to rescue them from their bad decisions.

Haven’t they heard, “The Fed can remain irrational (inexplicably non-pivoting), longer than you can remain solvent”?

It’s like an appraiser of property. If his appraisals are too low and ruin many real estate deals, he will no longer get any business. Same pressure as the credit ratings agencies discussed above…

Dishonesty, rigged games, corruption ruins capitalism/free markets. Unfortunately, this is anything but new. And really, maybe expecting something else of the human species is silly.

Tony,

Total BS. This is not happening this time around. Look for some other boogyman.

What’s truly amazing is that rating agencies even exist today, after all the damage they helped create with GFC — how is it possible anyone relies on their lies, which connect to corporate lies, which turn into marketing hype to lure consumers into traps, which connects to sec, FDIC, Fed and then, you step back and think, wait, we’re aren’t talking about crypto shitcoins, this is the entire Wilshire 5000 and everything called wall street, who’s been busy buying up every property in America, as Congress trades options.

This is all insane!

Meanwhile, svp deposit agreement

b. Limitation of Liability. Except as otherwise stated in the Agreement or as specified by law, we will be liable to you only for

damages arising directly from our intentional misconduct or gross negligence. “Ordinary care” requires only that we follow

standards that do not vary unreasonably from the general standards followed by similarly situated banks. Our policies and

procedures are general internal guidelines for our use and do not establish a higher standard of care for us that is otherwise,…. Blah blah blah, bullshit

Ity’s not a deposit agreement, it’s actually a customer creditor agreement. Supposed “depositors” are actually loaning their money to the bank, hence unsecured creditor.

First site I have seen this mentioned. What does that tell you? Once again Wolf is out front.

Wolf, I am curious, did any other financial institutions get down graded at the same time due to potential contamination? Or are they waiting for them to go bust also before changing the rating.

Moody’s determined that SVB was no longer able to pay for the rating.

This US bribe news will make many overseas companies new clients for Moody or S&P. Still they will miss the old boys network effect plus the domestic political angles from America.

I’m told several regional banks have been put on double secret probation by Moody’s today.

I did notice a lot of suits road tripping.

I get Moody’s upgrades and downgrades in the email every day. But it’s not a complete list. For example, the downgrade of SVB from investment grade to default wasn’t in my inbox (maybe too toxic).

So I checked manually for First Republic — just to use as an example because it’s under pressure. It is still rated investment grate by all three. I didn’t see a downgrade over the past few days. The current ratings were affirmed in December.

Value Line still has SVB’s financial strength rated “A.” I guess they’ll get to it Monday.

Morningstar no longer has it rated.

The SVB website accounting statements are gone. Their corporate webpage was taken over by the government. They left this message:

“On Friday, March 10, 2023, Silicon Valley Bank, Santa Clara, CA was closed by the California Department of Financial Protection & Innovation. Subsequently, the Federal Deposit Insurance Corporation (FDIC) was named Receiver. No advance notice is given to the public when a financial institution is closed.”

The SEC’s Edgar data base has all the filings, including quarterly reports (10-Q) and annual reports (10-k). The 2022 10-K is the last big report SVB filed.

The data base is searchable by company name or stock ticker. And it brings up the landing page for the company and lists all the recent filings. You can sort and search the filings. It’s easy to use. I use it all the time, and I link to these SEC filings in my articles because those links will still be good years after the company disappears.

Wolf – doubtless auto-c, or does ‘investment grate’ imply something’s circling the drain?

may we all find a better day.

I’ve heard someone somewhere say something about how “Nothing Goes to Heck in a Straight Line.”

I might have to check in with them and see if they want to update that phrase for this special occasion.

An asterisk will suffice.

Maybe the expression about going bankrupt gradually at first and then suddenly applies here too.

Pretty weak stuff on the credit evaluation side. Sloppy and careless. But it’s hardly the only thing we’re doing wrong in this country these days.

On my next off days from work I’m thinking of starting a new credit rating agency, I know competition is tough but my overhead is tiny, apartment is only 1500/MO, I eat like 400-600 of food a month and I can probably rate all the companies in the Nasdaq with my dartboard before lunch. I’ll need a bit of a break to do Dow Jones because I have a bad shoulder from Baseball in my youth.

You may want to partner with someone who can provide a blindfold.

How – stoppit, yer killin’ me!

may we all find a better day.

25 years ago there was a small credit rating company here in the USA that did a good job. I can’t remember their name, or find them online. But they called the problems at companies like Enron well before Enron collapsed.

Maybe they went broke, or were bought out?

Ya think Motley Fool is about ready to make that leap? They already charge for hot tips, I think.

Long time since the original online stock game.

Maybe these rating agency types will have to go back to their old jobs as realtors and used car salesmen.

These major rating agencies will never embarrass even thought making such a poor rating judgement. What on earth got these so call professional investors willing to take their words without made their own due diligent. Perhaps they just earn a fees from these whack retail investors and they always a winner even thought those companies go under.

The whole narrative to have rating agency to made investors better informed shown it is just a tools to loot investors. These ill judgement hardly hold accountable by the involving authorities.

Story floating around

SBV employee bonuses right before collapse

I went out to dinner a couple of years back with several people, two of which happened to work mid-level at S&P Global Ratings.

It will not surprise anyone to learn, perhaps, that they took zero interest in travel, good food (besides its prestige value), didn’t read anything besides industry stuff, and made boring conversation. One of them didn’t even know what The Onion was.

Anyway, that few hours explained a lot to me about the 2008 crash.

I read Jeffries and other firms or hedge funds offering 60-70 percent to depositors at SBV for their deposits.

Like Potter

They probably looked at this very carefully. Which tells you that uninsured depositors are likely to get a smaller haircut than what the hedge funds are offering (they’ve got to make some money on this).

BTW, the way I read the reporting on this, they’re all over the place. Some funds are offering to buy the claims at a “discount” of 70%, meaning a 70% loss for the depositor. Others are offering liquidity of up to 80% of the claim (meaning a 20% loss), in exchange for a guarantee from the VC or PE firm backing the startup.

So this is still evolving.

Meanwhile, there is reporting on Bloomberg, based on sources, that the FDIC and the Fed are discussing setting up a fund to backstop all bank deposits (but bail in stockholders and preferred holders and possibly other investors as is the case with SVB). So not an investor bailout as last time, but just a depositor bailout. I have no idea what will come of it.

They should just change the capital structure of banks and make deposits senior secured, above everything else, and then deposit insurance would be minimally needed. Let bondholders figure out how to get their money back. They can demand a higher yield for taking that risk.

Only if their cash-burning money losing corporate borrowers can pay them back, which means it has to be a rather short-term loan or else they will need to roll it over, at best.

The funds are banking on claimants being made whole through bailout. They are working off the logic of asymmetrical payoff and the timing needs of current depositors (near-term/making payrolls) and their own less urgent return requirements.

Nothing to do with precision of the analysis of recoveries.

As I said…

All offers are now OFF the table since the FDIC pays all depositors 100%. So no hedge fund or other fund made any money buying these certificates at whatever cents on the dollar because they haven’t even been handed out yet, and won’t be handed out.

Again, as I said, the offers were based on timing (need now vs ability to wait) and make-whole. Hedge funds were not stepping in with superior analytics on recoveries, just those two concepts.

The fact it was short circuited is inconsequential to the intent.

Interesting.. Aside from all of it, I wonder if there is anything political or whatever behind the scenes?

According to their website and publications SVB was one of the main and one of the few banks supporting and facilitating Chinese money being invested in US tech. (&, IDK, maybe other investments? Like RE?)

“We see a new emerging pool of eager Chinese investors – companies, individuals and indigenous funds – looking to put their money in U.S. technology companies.

The trend is only poised to grow, predicted Ken Gullicksen, Chief Strategy Officer at Evernote, who led the company’s expansion to China three years ago. “High-quality indigenous Chinese investment funds now have licenses to invest in the U.S., and they are looking for deals,” he reported. Large private equity funds in Hong Kong and Singapore also are in the hunt for U.S. opportunities.

[…]

“In another positive cross-border development, a small number of non-Chinese and joint-venture banks now can offer products and services in renminbi, the local Chinese currency, which should ease transactions. Among them is SPD Silicon Valley Bank, a 50/50 joint venture between SVB and Shanghai Pudong Development Bank that is headquartered in Shanghai.”

Evidently there is a freak out in China as well over the closure and the Chinese joint venture SPD Silicon Valley Bank is beside itself trying to reassure everyone that everything is OK.

Well, that just stinks! I like some of the A and B bond yields. We rely on many layers of risk management including that rating. But obviously that rating isn’t absolute after SLV. There is always an element of gambling no matter how thoroughly we evaluate it. I hate to get out of my bonds and preferred that pay ~7.5%. But maybe the 5.1 treasuries are safer.

Most corporate bonds are actually junk. It doesn’t matter how big the company is or their reputation. Look at their balanced sheet, leveraged to the gills.

The ones that are making a lot of money now may or do have high interest coverage ratios but that can and will change in a hurry, once the economy heads south.

For others, they will consistently pay higher rates as they mostly refinance now that the long-term credit cycle has turned.

Maybe they can merge with the remaining shell of FTX and rename themselves Superfailgate Bank and Crypto Clearing House.

I keep most of my savings in a credit union. I really don’t know what goes on inside of these institutions, but somehow I feel that a credit union is more dedicated to protecting the little guy’s savings and less to executive greed and financial shenanigans.

Everyone that owns a home in this comment section has been gaslighted by third party home inspections. Why bring this comparison up? Third party home inspections (e.g., stock/company ratings) are a way to make the buyer (e.g., stockholder) feel good about a large purchase. The third party inspectors are usually in the hip pocket of the real estate agents. Naturally, a buyer’s agent (e.g., investment broker) wants the house to sell and the referred third party inspector dances around potential defects (e.g. poor construction = poor investment).

Ultimately brokers gets their commissions, buyers get subpar investments, and the third party inspectors keep their reciprocal relationships in tact with the agents. Real estate agents in concert with inspectors perpetuate the fake value of investments. Let me repeat, investment brokers in concert with rating groups perpetuate the fake value of investments.

Bottom line for the history books: Everyone is complicit in buying and selling fake narratives to bolster their bottom lines until the real news breaks. Then everyone clutches their pearls and says, “Why me?!”

I will agree with you that many real estate agents will do whatever it takes to grease the tracks, but your comment appears to be conflating inspectors with appraisers…and portraying buyers as cognitively impaired lambs who have no agenda of their own.

I am not a realtor, inspector or appraiser.

Appraisers are hired to investigate the fair market value based on what similar houses recently sold for.

(Buyers can view the appraisal report and check the comps for themselves!)

On the other hand, inspection reports can actually be leveraged to beat up greedy sellers and get a discount. Ask me how I know.

I’m not here to defend inspectors, appraisers or realtors, as they all have a horse in the race and all are susceptible to corruption. Just like doctors and pharmaceutical companies.

Inspectors are often incentivized to nitpick. The ones I have hired understand that they’re more likely to get a 5 star review if they nitpick every inch of the house.

Meanwhile, at the U.K. Svb branch, tons of people lobbying to get a bailout, rushing around looking for cash before Monday. One almost wonders if those pension funds that didn’t fail a few months ago, are suddenly re-exposed to new hedging risks from new bets placed by the previous morons that were using leverage to take advantage of dumb old people.

From U.K.

The letter notes that SVB UK’s insolvency represents an “existential threat to the UK tech sector” as the majority of these firms hold money at the bank. The letter adds that the degree of the loss could cripple the startup ecosystem and set things back by 20 years, adding that if the UK tech sector sneezes, the rest of the economy will catch a cold and worse.”

“It is vital that the government looks to intervene to ensure the continued success of the sector,” as many of these firms may be forced into liquidation

* let them eat zombie cake and die

I’m sure (and really hope) someone realized that all this couldn’t have happened, for example, in Europe. In that area you simply cannot have a similar mismatch between short term (deposits) and long term (investments). It’s the basic of every, healthy balance sheet. In a bank it should be a must.

Again, in a highly sophisticated financial market like the US one, they “forgot” some simple rules and regulations.

Unfortunately, US it’s still highly unregulated and wild. Probably lobbies are very strong and bribing up and down, left and right.

All the best,

Donato

I’m sure you’re right. Remind me again, do you bank with Deutsche Bank or Credit Suisse?

LOL. Donato probably moved an account to Credit Suisse after the Barings collapse.

Mainly Bangor Savings Bank! :)

SVB and Credit Suisse are not comparable at any level. Again, that kind of mismatch is not allowed in Europe. We see now the consequences for the ordinary bank account holders.

European banks just make straight up bad loans. No need to mismatch duration.

Does Donato happen to live in Iceland by any chance?

Do you refer at their banks crisis of more than 10 years ago ? Some executives are in prison and regulators acted many strict reforms.

I hope you are not comparing Iceland and California economies.

No. Just teasing about the high level of competence among European financiers vs American ones. Both need to learn how to be productive rather than parasitic.

Ratings shenanigans and virtual ring fencing and mystical unicorn magical accounting wizards, and Humpty Dumpty and the BOE, all here to make the world a better place — thank you God for allowing zombie idiots to run amuck.

A version of the draft letter, seen by the Guardian, warned that the majority of the signatories were this weekend “running numbers to see if we are technically insolvent” after losing deposits at SVB UK.

It explained that the tech sector is highly interconnected and the loss of deposits had the potential to cripple the sector, with many business at risk of falling into insolvency overnight.

It is understood that the Bank of England’s decision to place the subsidiary of the collapsed US lender into insolvency on Friday night will override any requests to withdraw or transfer funds to other banks – even if they had been filed, but not executed, by the time authorities stepped in.

It means that most of the lender’s 3,500 customers will see the bulk of their deposits at SVB UK wiped out, despite having been promised by UK chief executive Erin Platts on a Zoom call on Friday afternoon that the bank would continue operating next week as usual.

Sorry Mr W

At this point the ratings agencies have all the credibility of the multi-page Special Advertising Sections you used to see in magazines that pretended to be editorial content.

As everyone is taking a close look at the balance sheets of the banks,

it is clear that there are lot of big “phantom” assets on the books.

The Available for Sale is at least marked to market and the losses have been taken out of equity as AOCI. While one understands the rationale for not marking to market the HTM securities, the top three (JPM, BAC, & WFC) have staggering losses. B of A seems to be holding tons of long dated Treasuries, and its LOSS on HTM is 109 billion dollars. If there is a run on B of A, (extremely low chance), on day 1, its assets would be written off by this amount. (Sure, the treasuries would rally and mitigate the suffering!)

WFC has 36 billion loss on HTM and JPM has 41 billion.

Wolf, any thoughts??

All figures from latest 10K.

Even WFC has $186 billion in total equity; $152 billion in Tier 1 equity; and $133 billion in common equity Tier 1 (10-K). These banks have huge capital cushions to absorb a lot of losses, and they will have a lot of losses, and their shares will go down. But people hoping for WFC or JPM to collapse, well, I don’t think that’s likely. SVB was very special case. That’s how I see it.

JPM and WFC are systemically important banks and have stricter regulatory requirements than SVB. It was reported SVB kept itself under the 200B cap to avoid the more stringent regulation.

As a 20-something “bulge bracket” investment banker in the 1990s, junior-most member of the team, I was seconded to interface with the Moody’s guy on a corporate bond deal to check a box. I earnestly engaged the 30-something guy to convince him of my client’s bona fides. He gave me a withering beat-down for wasting his time by taking the whole exercise WAY too seriously. And here’s our invoice! The ratings agency scam became screamingly obvious in 2008, but A) was an open secret for at least two decades before that and B) even after the global meltdown, nothing really changed.

I don’t buy anything other than UST, but if I did, I’d look at the CDS premiums, bond prices, and spreads over “risk free” (UST for USD) debt before I’d ever rely on a credit rating.

These three change all the time and I know it’s short term. It’s also a much better warning signal.

Talks of the Fed, FDIC, and banks discussing a backstop fund for calming down any panic bank withdraws… No doubt this will be used as Fed put evidence 🤦

However maybe it’s more of the Fed can’t have this thing break until inflation is defeated so higher for longer🤞

To no one’s surprise, there are calls from prominent figures to bail out SVB with taxpayer funds, due to concerns about “job creators” (startups with uninsured deposits >$250 can’t make payroll), contagion fears, etc.

Does anyone know if this is something the Biden admin / FDIC / Federal Reserve can do unilaterally, or does it require new legislation from Congress?

The interesting thing is that SVB shareholders and preferred stock holders have already gotten bailed in. They’re NOT getting bailed out. Maybe the uninsured depositors, which might face a loss between (my guess) 0% and 20% on their deposits will be assured that they won’t lose money on their deposits. But the bank investors have gotten crushed already.

This is very different from the Financial Crisis when bank shareholders, and preferred holders, and bondholders were made whole, including Warren Buffett. That stank to high heaven. To my knowledge, no one is calling for bailing out investors.

IMHO bank deposits should by definition be at zero risk at all times. Safety is why deposits are placed with a bank instead of being kept in a mattress or invested in stocks. If there was zero risk of any loss on any deposits, there is a compelling argument that this run on SVB would have never occured.

Your preference will make systemic moral hazard even worse. It’s been building up for over a century.

With or without it, instead of periodic “panics”, the future holds a “fat tail” catastrophic systemic failure which even with all the obvious signs, practically everyone will call it a “black swan” and “unexpected”.

I get that most people aren’t equipped to evaluate bank safety. Doesn’t change what I am telling you.

Under the current system, at most, deposit insurance should be limited to a relatively nominal amount per depositor (not account). $250K is already far too much.

The real solution to your problem is to actually require “deposits” to be deposits. Your “deposit” is actually a loan to the bank, which most including you may not even know. That’s why they can lend it out and pay you interest.

If deposits could not be lent out, there would be no need for insurance, but bank customers would no longer get “free” checking and have to pay the bank to store their money.

The government doesn’t want people to use cash so it’s in their best interest to keep everyone calm and make them believe banks are the safest place to keep your money.

But in the Financial Crisis, the government got all of its TARP money back, plus interest, plus profit on the exercise or sale of warrants. The so-called bailouts were really a special tax levied on strong banks (the majority) to clean up the mess at a handful of weak banks.

Tarp was peanuts compared to what the Fed did. The Fed did all the bailouts that made Tarp, Buffett, and all investors a ton of money. It did it by printing trillions of dollars and buying assets with it, driving up asset prices, including those of private-label MBS that had collapsed. Without that, Tarp would have shown steep losses, as would have all other investors.

BS. It was a handout to save a bunch of crooks who should have been sent to prison instead of given a blank check by the even more crooked treasury department at the time. Too big to fail should not exist.

So did the Fed make or lose money on the assets they purchased during the 2008 crisis?

Most media speculation about potential bailouts concern the uninsured deposits, not SVB’s shareholders. (SVB investors know they’re toast, which is why shares tanked on Friday.)

1) The $250k FDIC insurance cap is not exactly a secret. It’s stated prominently on the paperwork with every new account opening.

2) The uninsured depositors include a mix of both businesses & wealthy individuals. You can make a case for bailing out the businesses who need to make payroll, but what about the billionaires?

3) Some hedge funds are making offers to uninsured depositors to buy out whatever assets they had at ~60% of original face value. They’re making calculated bets that recovery of 70%+ is likely – which would sting but isn’t catastrophic. If that’s the case, taxpayers shouldn’t need to be on the hook for the remainder.

Totally agree. It’s not like this hasn’t happened before.

One article online noted that 93% of depositors had over $250,000 in deposits, as it was a bank for the super wealthy clients (hobby vineyard rich) and super wealthy VC funded companies (Peter Thiel rich).

Goes along the fears of too big to fail and heads the rich win, tails you bottom 99% lose, and thus such fears are valid as there has been a history of such crony capitalism for many years as the elites are clueless on how this dissolves social contracts and trust in the system.

I’d willing to bet that the super wealthy get 100% of their deposits by the time all is said and done, as Yellen is saying the USA won’t bail out the bank, but CNBC is saying “regulators would step in would be to create a backstop for uninsured deposits”.

Maybe I’m wrong and Apple will use half of its cash hoard and bail out their fellow tech neighbors in good faith? Or will it be the bottom 99% bailing them out instead via “backstops”?

Per CNBC:

Financial regulators are discussing two different facilities to manage the fallout from the closure of Silicon Valley Bank if no buyer materializes, according to a source close to the situation.

One way that the regulators would step in would be to create a backstop for uninsured deposits at Silicon Valley Bank, using an authority from the Federal Deposit Insurance Act, according to the source. The move would also touch the systemic risk exception that allows the Fed to take extraordinary action to stem contagion fears.

“…it was a bank for the super wealthy clients (hobby vineyard rich) and super wealthy VC funded companies (Peter Thiel rich).”

Exactly, which is why over 90% of people had never even heard of a bank so big. Rich people stuff. Let them eat their losses. If anybody should understand the $250,000 rule, it’s them. I am sick and tired of the wealthy getting bailouts.

I’m especially glad the preferred stockholders got wiped out. The Silicon Valley practice of issuing super duper shares above the common is another way of defrauding the common stockholders.

But Kramer says Silicon Valley bank was a buy a few weeks ago.. he wouldn’t ever be wrong would he?

He was equally “correct” about Bear Stearns in 2008 when he loudly proclaimed “don’t move your money from Bear.”

Amazing he is still on the air and continues to have an audience. The carnival barker of Wall street strikes again.

Right up there with S&P, Fitch, Moodys…

10 days ago on youtube BNN Bloomberg puts up this video tittled

Expect a long-term bullish run for Canadian banks if there isn’t a deep recession.

Heck, that’s a straight line.

🤣

Explains exactly why SVB intervention absolute reqd….asap

Don’t think any amount of ‘ preparation’, or appropriate financial position by SVB, could have saved the day……and to be rated appropriately by Moody’s reqd really focusing on the peculiarities of SVB, not the regular stats on reserves, loans, etc.

I think this venture person says 42 billion taken out the Friday morning…or something equally startling.

SVB bond portfolio unrealized losses :

1) “Available for sale” unrealized losses reduce equities, but exclude, hidden from earnings.

2) “Held to maturity” unrealized losses are excluded from both

earnings and equities.

3) SVB pyramid of fakes caught the eyes of short seller.

On Dec 31 2022 SBV unrealized losses “held to maturity” were $15B out of a $92B portfolio and $16.3B equities.

4) Total assets = total liabilities + share holders equities.

When the total liabilities/equities ratio is high and retained earnings are either negative or fake the short sellers will get u.

5) Short sellers have a lot of work to do in 2023.

I see that tech startup types would park their cash-burn pile in a bank like SVB?

Is there any reason they wouldn’t just buy USA treasuries on various durations to release funds at maturity as expected to be required?

If they need more, sell early (and possibly at a loss), need less, re-invest in treasuries?

Why are these tech cos exposed to a bank’s capital reserve risk?

Aren’t short dated treasuries sufficiently liquid?

If they also had loans from SVB, the loan agreements reportedly required the companies to keep all their deposits at SVB.

Sounds almost illegal. I despise banks. Over the course of the past few years, people have reported banks have begun asking their depositors what the money was for that they were withdrawing, like they might just decline them if they don’t like the answer. How about “none of your fuc*ing business” or “because it’s my fuc*ing money, that’s why?” Rant off.

That happened to a friend of mine a couple months ago. He was going to buy a boat and the bank asked him to fill out paperwork saying where the money is going.

He said “please close all my accounts and provide me a cashier’s check so I can take my business elsewhere”. They backed down on the “requirement”.

Ah, that’s a reason I wasn’t expecting.

So the big deposits that aren’t insured with FDIC are those exact same loans, which they couldn’t move elsewhere even if they’d wanted to.

Given the dash of support for these businesses to remain solvent, assuming they’re that important, it’s odd that they can’t attract better sources of credit.

Which leads me to believe the support isn’t for ‘poor old tech businesses’, but ‘quick, stem the cash outflows and loss of confidence in the system’

One thing to note about bond ratings is that all of the ratings levels are just opinions–except for the “D” rating (or C for Moody’s), which is based on fact, namely that default has occurred…

Great article! US ratings agencies have lost credibility just like US Treasuries where’s the downgrade? Oh It was Covid next it’s Russia and China taking down our banks… get ready these guys are ready to blame and take your money.

Thanks guys ! (seriously !!) After posting, started thinking that Banks lend money !! so not all of that $10 to $500 million in start-up money would be “on deposit”permanently (my previous poor thinking). SVB made ‘bad investments’ and that’s the biggest reason they failed ! Like some said, they bought 10 Year Treasury’s at a bad time/price, and their value declined, thus when selling those Treasury’s to cover withdrawls, SVB ‘lost money’. (Now I understand better ! Thanks ! )

“The Big Short” with Steve Carrell, great film !! Are there ‘topless clubs’ in Silicon Valley ? where dancers each have several accounts at SVB ? LOL

What a mess, and how to design a system to prevent this ?

In regards to the past.

The “Bush I Real Estate Scam”: The Appraisers were ‘pushed’ to ‘illegally/criminally’ overvalue commercial properties, on which too large a loans were made by certain Savings & Loans, then when Bush I ‘pushed’ The Fed to raise interest rates, many of those loans went into default. The FDIC stepped in and declared a number of S&L’s “technically insolvent” and ‘took them over’. Bush I then created the RTC, the Resolution Trust Corporation, to handle the ‘fire sale’ of ‘assets’ and powerful “Insiders” cherry-picked the best of the commercial properties for “nickels on the dollar” and the Taxpayers “picked up the tab”. This was about an $800 Billion RE Scam.

In the “Bush II Real Estate Scam”: as the property Appraisers were now under a ‘microscope’ of ‘oversight’, they had to do things differently. This time they ‘criminally’ overvalued the borrowers !! (instead of overvaluing the property !). “The Big Short” does a great job of illustrating this. This was about a $3 Trillion Scam !!! Unfortunately, a lot of ‘fake mortgages’ were also created and ‘shuffled’ into the $100 million ‘mortgage pools’ that were then rated Triple A, AAA, by ‘rating agencies’ ! (Just like SVB was ‘rated’) As many small investors can’t afford to buy an entire $100 million ‘pool’, these $100 million pools were “sliced and diced” into $20,000 to $100,000 ‘pieces’ and sold around the world to individuals, and some foreign governments even bought entire $100 million pools for their government pension plans etc, as they were AAA Rated !!! The problem was, No one was making the monthly payments on the ‘fake mortgages’, and so the interest payments to investors started to decline, as the mortgage pool wasn’t making the income expected. Then when the ‘real mortgages’ went into default due to the ‘teaser rate’ being re-set to the ‘real interest rate’, 5 to 7 years later, and the borrowers unable to make their now almost double in size monthly payment, the Principal value of the ‘pool’ stared to decline as well !

The ‘fake mortgages’ problem was the impetus for when Bankruptcy Court proceedings tried to determine “who actually owned” the property in question, Bank Mortgage Departments could NOT determine ‘who owned the property’ !

Catherine Austin Fitts documents this very well !

As Wolf writes about RE bubble I, and now RE bubble II, are we heading in to Bank Crisis II ? (as the Bush I RE Scam would be Bank Crisis I )

Forgot to mention; When the B-II-RE-Scam was ‘revealed’ several foreign governments were about to ‘go to war’ with the US over this giant ‘rip-off’ !! And that’s why the US Treasury (The Fed) had to give Fannie Mae and Freddie Mac, a $3 to $5 Trillion “Line of Credit” to buy-back those ‘fake mortgage’ pools from foreign governments and foreign investors !

“Not learned a thing since the Financial Crisis… That’s how worthless these credit ratings are”

Because the right people didn’t got to JAIL for fraud during the GFC.

There was some guy on CNBC whining about how so many startups are going to be unable to make payrolls and how their deposits were beyond FDIC guaranteed amounts, so they need a government bailout.

Think the right people will got to jail this time?

Nah…

When the S&Ls blew up in the 1980s, triggering a big government bailout, some of the head honchos were indicted and went to jail. That may have been the last time this happened to folks that are responsible for this type of thing.

IIRC Wolf,,,

Only those ”old and olde boys” who ”crossed” the dynasty then in charge did ANY jail time..

WE, in this case WE the really and truly conservative INVESTORs WE can only hope that these current events will end up with some very clear restrictions on ”insider” investors making the rest of us investors, no matter how careful, look like the suckers PT Barnum cited.

Where’s Bill Black when you need him the most.. He still up to the the task of ‘tough canine doggedly punctures non-contritious speeding fat tire(s)’ investigations/convictions??

The S&L blowup was predicted in May 1980 when the DIDMCA turned 38,000 nonbanks into banks.

I was a long distance mover back then and remember moving a bank president to Palm Springs, he paid cash and changed the delivery address at the last minute, didn’t want any record of it on the bill of lading. I think he had a false mustache and maybe his real name was “John Doe” but I was skeptical.

William Black who was involved in the indictment of about 1000 in that scandal, author of the book, “The Best Way to Rob a Bank is to Own One: How Corporate Executives and Politicians Looted the S&L,” is in two outstanding Bill Moyers interviews about the GFC which can be found on YouTube.

Not sure that svb had or was required to have a living will for resolution, but FDIC required many large banks to prepare for flash bankruptcy.

Here’s a partial glimpse, indicating that tax payers are to be shielded from stupid bank management

While we believe a BAC bankruptcy is highly unlikely, we are nevertheless prepared to execute an orderly

resolution, without government assistance or taxpayer funds, with a fully operational Resolution Plan built on a

solid foundation of resolution planning capabilities. Over the last ten years, we have developed comprehensive

resolution planning capabilities that have continued to evolve and have been incorporated into our business-as-