OK, “least geeky ever,” I mean I don’t know that, but you get the idea. Fed governor Jefferson outlines the differences in a lecture at Harvard.

By Wolf Richter for WOLF STREET.

I have long been covering and analyzing the Consumer Price Index (CPI), and its various sub-indices, released by the Bureau of Labor Statistics; and the Personal Consumption Expenditures (PCE) Price Index, released by the Bureau of Economic Analysis, the entity that puts together the national accounts that go into GDP. The Fed uses the PCE price index as yardstick for its inflation targeting.

Both the CPI and the PCE price index dished up nasty surprises in January and December, driven largely by a jump in services inflation – and services are where the majority of consumer spending goes (here’s my discussion of CPI for January, note the spike in services inflation in the third chart; and here is my discussion of the PCE price index for January, note the spike in services inflation in the first chart).

But there are big differences between the two indices, including that the year-over-year increases in the PCE price index are usually lower than those of CPI. This has to do with what data the indices draw from, their weights, and how the indices are constructed.

Fed Governor Philip Jefferson, speaking via video at a Harvard University economics class, outlined the differences in an easy-to-consume way. The lecture covered other topics as well, and was long. I will exclusively focus on the relatively brief discussion of the differences between CPI and the PCE price index (the entire lecture is here).

The below are excerpts from Fed Governor Jefferson’s speech, and the charts are from his presentation:

“Both indexes measure inflation using a specific basket of goods and services consumed by households. These baskets are similar but not identical across the two measures.

“Both measures also weight each item in their basket roughly in accordance with its expenditure share. That is, the more households spend on an item, like rent, the higher the weight it receives in the overall index. The weights are broadly similar across the two indexes, but, again, there are some important differences.

“First, the PCE price index has a broader scope than the CPI. The CPI is limited to expenditures that households pay out of pocket, while the PCE price index covers a broader set of goods and services as it seeks to cover prices for all consumer expenditures in the national income and product accounts (NIPA). For example, the PCE price index includes prices of the health services provided to households through Medicaid, while the CPI excludes these items.

“Second, the PCE price index and the CPI use different weighting systems. The PCE price index, which is more comprehensive than the CPI, estimates expenditure shares using the national income and product accounts, while the CPI measures expenditure shares using a separate survey of households, the Consumer Expenditure Survey. This leads to some differences in expenditure weights that can at times be important.

“For example, the share of medical services is notably higher in the PCE price index (partly because the PCE price index includes more kinds of medical expenditures), and the share of housing services is noticeably smaller (because overall expenditures are larger in the PCE price index). As a result, when health-care services or housing services inflation behave differently than other prices, this can lead to differences in PCE versus CPI inflation.

“Another difference in the weights is that the PCE price index uses time-varying weights, while the official CPI keeps weights fixed for a year. The PCE price index weights change to reflect changes in the goods consumers buy. For instance, at the start of the pandemic, the CPI was still giving the same weights to cruise ship and airline fares, even though no one was traveling.

[Here is my discussion on how the changed weights of CPI made CPI worse, with charts for the major CPI categories of their weights over time]“The time-varying weights in PCE also account for substitution behavior. Suppose the price of apples goes up and the price of oranges stays the same. Consumers are then likely to substitute apples with oranges.

“In contrast, the CPI does not capture substitution behavior because the basket of goods consumers purchase is updated only once a year (instead of every month) and reflects expenditure patterns prevailing two years ago.

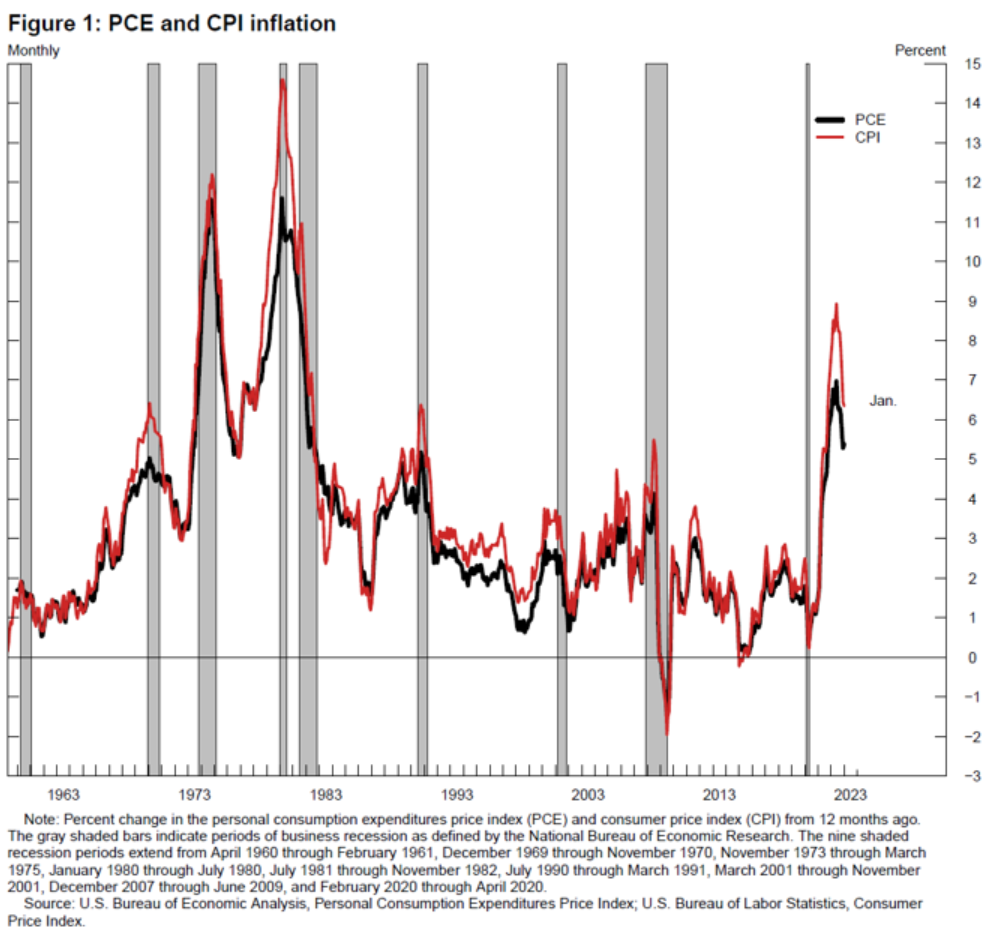

“The substitution effects captured by the PCE price index is one reason why PCE inflation (black line) is, almost always, lower than CPI inflation (red line), as you can see in figure 1. [Chart via Federal Reserve].

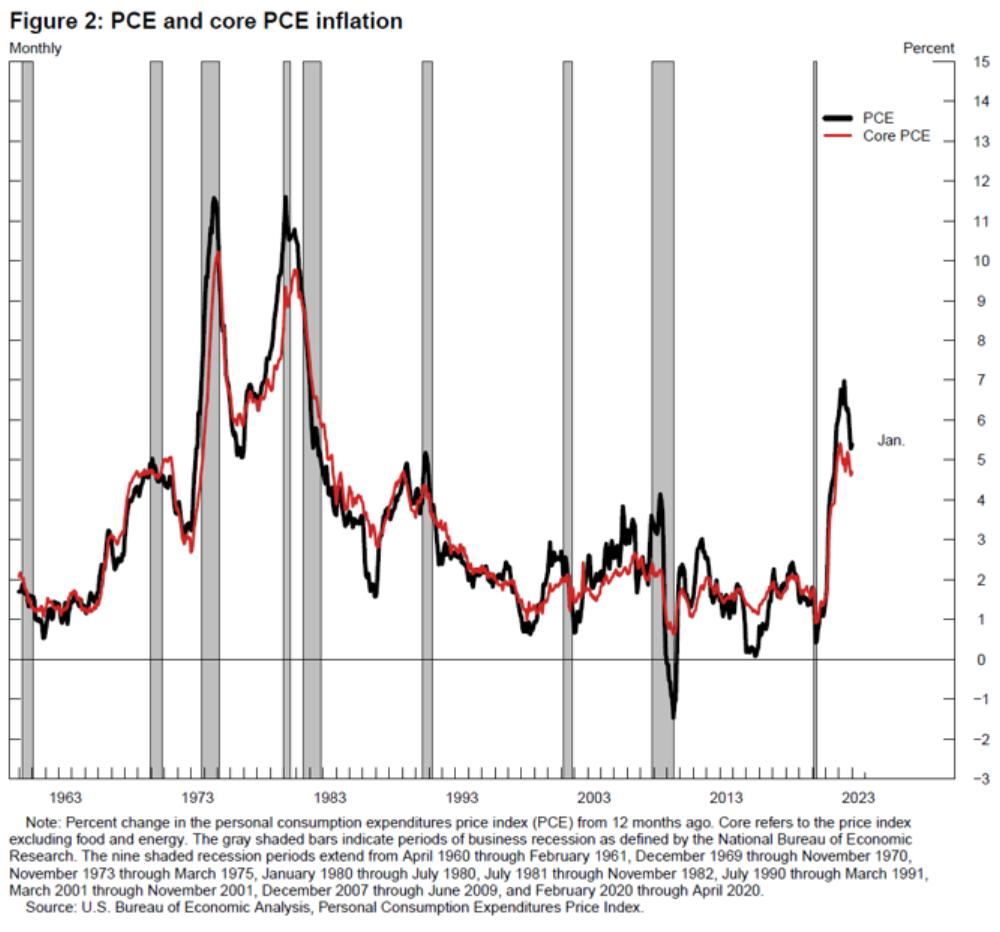

“As I mentioned earlier, there are both total and core PCE price and CPI indexes. The core subindex is the total index excluding food and energy prices. Food and energy prices are more volatile than other prices, which makes total inflation more volatile.

“This volatility is evident in figure 2. You can see the black line (total PCE price index) exhibiting more drastic ups and downs than core PCE price index, the red line in the graph, and many of the sharp movements are short lived. In other words, the volatility in the total PCE price index makes it harder to discern trends (longer-lasting movements) from transitory movements.

“In addition, food and energy prices often depend on factors that are beyond the influence of monetary policy, such as geopolitical developments (for example, those associated with fluctuations in energy prices) or weather or disease or war (for example, in the case of food prices). [Chart via Federal Reserve].

“In summary, the differences between CPI and PCE price indexes are important. The FOMC has chosen to target the PCE price index because it is broader and it captures more accurately what households are actually consuming. In addition, food and energy account for a significant portion of household budgets, so the Federal Reserve’s inflation objective is defined in terms of the total PCE price index, but the Fed monitors the core PCE price index, as well as other inflation indicators, in order to identify evolving inflation trends.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“In addition, food and energy account for a significant portion of household budgets, so the Federal Reserve’s inflation objective is defined in terms of the total PCE price index, but the Fed monitors the core PCE price index, as well as other inflation indicators, in order to identify evolving inflation trends.”

That’s interesting. I thought the FED focused on core PCE for its inflation objective.

Thanks for writing about this.

Yes, I thought so too. In its projections, the Fed always includes PCE and core-PCE. The core-PCE is less volatile, doesn’t go up and down as erratically as the headline PCE. A spike and then collapse in energy prices can cause huge gyrations in the headline PCE, which can turn negative on a fuel price collapse, as we have seen (see first chart), and the core PCE doesn’t really react. So it makes sense to use core-PCE as a target.

But over time, PCE and core PCE probably average out pretty closely. I think what he was saying is that the Fed targets 2% PCE inflation, but is looking at the more stable core-PCE to see where it is because the headline PCE is so erratic. That’s how I interpreted it.

Sounds like the PCE includes welfare, or other government entitlements in its calculations. “… the PCE price index includes prices of the health services provided to households through Medicaid, while the CPI excludes these items.”

Logically, subsididised rent, food stamps, maybe military (food, clothing, and shelter), utility subsidies, etc. All making a nation that is completely squeezed by inflation for essentials.

No, you’re misreading your own quote. PCE does NOT include “welfare” and “entitlements,” but it includes Medicaid which is a form of health insurance, and health insurance is included more broadly in PCE than in CPI, and weighs more heavily too. The CPI includes health insurance in a bizarre way (which requires huge annual adjustments that we’ve discussed here at length) but doesn’t include Medicaid.

I’m confused by that. Medicaid is a welfare program. Medicare is an insurance program, but Medicaid is a welfare program.

We can call it insurance or we can call it a firetruck. Doesn’t change the fact that it’s welfare.

Not arguing for or against. Just calling it what it is.

How can PCE not include welfare while it does include welfare?

Any government benefit program, including medicare, is welfare. Even though it’s funded through targeted taxes and fees rather than general fund taxes doesn’t change this fact. Here are a few ways medicare differs substantially from traditional insurance:

1. The taxes paid through employee/employer contributions are completely unconnected to the future “insurance” coverage individuals receive. This occurs in several ways, such as the there being no cap on the amount of income subject to the medicare tax. On the other side, spouses qualify for benefits even if they never contribute to the system. Families with a nonworking spouse don’t pay extra taxes to cover the nonworking spouse’s coverage.

2. When medicare was implemented the initial beneficiaries paid little or nothing into the system because the taxes were implemented when the system began. They were covered without paying for the “insurance.”

3. People qualify for coverage based on qualified earnings over only 40 quarters, but everyone must pay into the system as long as they work. True insurance would never be structured this way, because workers with short careers benefit at the expense of workers who work much longer.

Any large scale government benefit program is welfare in the sense that some people pay a disproportionate share of the cost for the benefit of other people. Medicare uses the language of “insurance” to make the program palatable to more people. I intend to claim my benefits when I turn 65, and I’ve paid into the system as required, but I accept it’s a form of welfare. It’s just a welfare program that most people derive benefits from and therefore has broader support across the population.

Why don’t you rage about corporate welfare then? Why is it only bad when the poor get government money, and it’s great when companies whose shares you have in your 401k get government money?

Medicaid is health insurance, pure and simple. It’s shitty health insurance that few doctors take. It doesn’t matter who pays for health insurance, it’s still health insurance, whether it’s your employer that pays for it, of you that pays for it, of the government that pays for the gold-plated health insurance of members of Congress, or the government that pays for the health insurance of the rank and file, or the government that pays for health insurance of teachers, or for the poor. Why is it suddenly an “entitlement” when it is health insurance for the poor, and it’s not an “entitlement” when a hugely more expensive plan is paid for members of congress? Hypocrisy?

I just wanted clarification about the PCE containing welfare or not.

And, that makes me a raging poor-people-hater hypocrite deserving of a double barrel bazooka.

Okey dokey. Fire away. I can take it ;-)

Halibut,

Mr. Wolf is great at interpreting data and clearly writing about it in terms that are easily understood by most people, but he is not without his own biases. Welfare is welfare. I’m not sure why something called “an insurance program” by the government can’t be welfare in reality. And sure… there is plenty of corporate welfare to go around but I fail to see where anyone was arguing for it. I didn’t take you for a poor people hater, just saying.

The military is a welfare program. The Federal highway system is a welfare program. Fire departments, police, air traffic control, EPA, DHS, CIA, etc. are all “welfare” programs. These are not included in PCE or CPI but should be.

From a U.S. govt. bls.gov web page: “ CPI sources data from consumers, while PCE sources from businesses. The scope effect is a result of the different types of expenditures CPI and PCE track. For example, CPI only tracks out-of-pocket consumer medical expenditures, but PCE also tracks expenditures made for consumers, thus including employer contributions.”

“outlined the differences is an easy-to-consume way”

I think you meant “in”

Yes, thanks.

“The time-varying weights in PCE also account for substitution behavior. Suppose the price of apples goes up and the price of oranges stays the same. Consumers are then likely to substitute apples with oranges.”

Doesn’t cause some distortion? If we did buy ribeye steaks but now we buy canned Spam, yeah, we’re spending less because inflation is clobbering us; not because it’s getting better…

Or did I misunderstand that?

“Doesn’t cause some distortion?”

Yes, and as he pointed out, it’s one of the reasons why PCE inflation runs lower than CPI inflation.

Parsing the delicate differences between CPI and PCE.

We must be getting closer to the end…even the beginning of the end will do from here.

I’m trying to give you a better understanding of what we’re talking about when we discuss CPI and PCE, which I discuss every month. Nothing to do with “end.”

I thought you might be interested in learning something. But maybe not.

Halibut…

Agreed.

The example of apples and oranges is a lateral example. The real substitution is as you suggest….too expensive, go to the lesser product.

Not apples to oranges but ground beef to ground chicken. Next will be “hamburger helper” sans the hamburger.

That substitution is an intentional low reading bias. Take out the expensive ..substitute the lesser price. How can that be considered a comparison over time of the price of items?

That is exactly why so many of us argue that the govt deliberately chooses to under-measure inflation, which is the loss of value of our currency. When the govt discounts inflation because of changing consumer behavior it allows the perpetual downhill slide in such things as quality of food, services, etc. For example, measuring the cost of a loaf of bread in 1923 made with simple, what we consider “organic” ingredients now would cost like $8, but since consumers continually shift to the cheaper bread (myself included), a comparable bread would still be considered to cost around $1.50. Or am I wrong? I know they do those “hedonic quality” adjustments for things like better automobile and electronics technology all the time but I doubt they use it in a reverse capacity for other things we spend money on like food. It is a complex topic when you base inflation on human behavior vs some sort of constant references, even if it is a basket of simple, fundamental items such as gold, bread, milk, meat.

Wolf,

I appreciate the work you put into this…but does it alter the gut intuition that housing sector inflation is going to almost always swamp/dominate almost everything because of housing’s heavy weighting (and rightfully so).

So while it is interesting to learn about other sectors, a quick-and-dirty analysis of American struggles could be accomplished by eyeballing the monthly Zumper/ApartmentList reports (leveraged landlords vs everybody else…)

(I know that 65% America homeownership (ie mortgage indebtedness…) complicates the distributional impact…but as the past yr has shown, levered paper SFH gains can evaporate – and then some – very quickly. See also, 2008…By beating honest interest rates into unconsciousness for 20 years the Fed has created a perpetually – if not *continuously* – unstable economic environment for 90%+ of Americans (those not realizing they have to spend their lives on perpetual hair trigger Fed watch just not to get slaughtered…)

According to the St Louis Fed, PCE since January 1980 increased 318.61% while All Urban CPI increased 383.3%, or 64.7% more, quite a significant cumulative effect.

It would be enlightening to see per capita cumulative income gains over the same period.

My intuitive sense is that Fed rate cycling makes life for 90%+ of Americans a Sisyphean exercise (home asset appreciation=low savings return, high savings returns=collapse in home asset value, Boulder up hill then Boulder down hill then Boulder up hill…)

It is a way of creating the illusion of economic progress (something is always going up!) without the reality (because something is always going down at the same time).

Unless the mass of Americans become timing-attuned interest rate speculators, they are left marching hard…in place.

I don’t know Wolf. The black line and the red line in the first chart look awfully close. I would bet the r2 (correlation) would be in the high 90s.

Sure, we can be retrospectively “precise” in defining the differences, but the bottom line is that the FED is often “inaccurate” in its forecasts, no matter what metric of inflation is used.

Give me better decision making, not better metrics.

Even armed with such insightful metrics, the FED still failed in its decision making. The first mistake was inhaling from the MMT bong that unleashed the M2 monster. The second was relaxing in the faux comfort of “transitory” inflation.

Time will tell whether the improbable goal of a soft landing – with “higher for longer” consequences – is the third strike.

I’m with you, Auld K. That’s a lot of thin slicing and dicing, to arrive at very precise numbers….only to then be “managed” by the bluntest of blunt tools, interest rates. And poorly, at best. I’d rather they worry less about which version to follow, and worry more about managing it.

According to Cleveland Fed real time Inflation tracker, today is the first day where core PCE is running the hottest of the 4 inflation gauges.

Historically it would appear to be typically running the slowest.

Looks like inflation isn’t dead after all😬

At least its Transitory.

/s4s

Wolf,

Thank you for taking the time to break this down for us.

Government bureaucrats love central planing because it give them a cushy job and fat salary.

What is getting published as “the consumer price index” represents a statistical hodgepodge. It can be concocted in almost any way. These macroeconomic numbers suffer from the illusion that the properties of an object—called “the economy”—could be objectively observed and measured.

Looks like the PCE closely tracks the CPI. and the CPI has been decelerating over the last 6 months.

U.S. Postal Service workers just got a 10 cent an hour COLA because the CPI-W 1967 only increased 0.46% over the last 6 months.

Is the following inflationary? CBO has predicted Government to grow from 31 trillion now to 45 trillion in 2032. Usually the CBO predictions are about 10 to 20% lower than what actually occurs. So in 2032 Government debt will probably be around $50 – $52 trillion. Crazy that it was only 22 trillion just 3 years ago and 10 trillion in 2009.

So we should see government debt go from 10 trillion in 2009 to 52 trillion in 2032. 5x in just 23 years. A housing bust and a COVID pandemic juiced this debt but the money has been spent.

Where does this lead use? Will the debt binge ever end?

Wait! If the PCE does NOT include welfare and entitlements, then the assertion that inflation hurts everyone but hurts the poor the most is not a true statement. It is the income level just ABOVE those that qualify for welfare that suffers the most? Trying to clarify. . .

This is confused. The PCE price index is a measure of inflation (price changes), nothing else. It’s not a measure of income or whatever.

Has anybody asked these evil pieces of trash why they have an “inflation target” to begin with? Trying to push 2% inflation yearly is stealing from the masses. Now they’ve got it ramped up over 4x that. I absolutely despise these people. All of them. I hope one day we see them all in prison.

DC

Remarkable that the masses have been “gaslighted” into accepting 2% inflation as “stable prices”. It is as if we are still in “emergency mode” from 2009.

And the 2% goal is to be stacked upon the 9% spike that is now baked in.

2% is NOT stable prices.

And what we have seen in prices is well off the 2% trajectory, so one might ask “where is the push for price rollbacks”? Missing. Telling.

The media is in on it too. I read a Bloomberg piece yesterday where the author actually stated that Congress set 2% as the Fed’s mandate.

In a real world, the inflation target should be zero. Why not?

There needs to be more QT. Sell MBS outright.

Thanks for standing up for the less fortunate there wolf. Politicians get people riled up with the buzz words. But what everyone forgets is it’s just all accounting!

No one should stand up for Big Sugar though, cuz Big Sugar just makes us all Fat!

“PCE price index includes prices of the health services provided to households through Medicaid, while the CPI excludes these items.”

Does this include insurance premiums? My wife and I pay $13,000+/yr for premiums. That should be a gigantic weight in the index. Actual medical expenses add significantly on top of that.

… sorry, $15,000+ in premiums, and that is not Medicaid.

Yes. That’s part of health insurance.

You got me stuck on the 10 year now Wolf.

Mohamad El-Erian just had an interview where he said the FED can’t get to 2% without crashing the economy.

“You need a higher stable inflation rate. Call it 3 to 4%”

So people buying the 10 year at 4% are essentially making nothing for the foreseeable future.

I guess the FED being the White Knight and slashing rates will make them big money??? Pivot Crowd bets :/

Somewhat related to CPI yardsticks, from very recent San Francisco Fed paper:

A policy tightening equivalent to a 1 percentage point increase in the federal funds rate can reduce rent inflation up to 3.2 percentage points over the course of 2½ years. This translates to a maximum reduction in headline PCE inflation of about 0.5 percentage point over the same time horizon.

Great artickle!

Still, I wonder what PCI and PCE really measure.🙄

Price rises, shift in spending pattern, shift in price between different items, change in purchasing power or?

PCE uses geometric weighting in its substitution strategy. This creates a downward bias.

Yes, that’s what the article said, what Fed governor Jefferson said.

Lenin once pontificated to the effect that he would destroy capitalism, and presumably capitalists, by making their money worthless.

Inflation cannot destroy real property nor the equities in these properties, but it can and does capriciously transfer the ownership of vast amounts of these equities thus unnecessarily accelerating the process by which wealth is concentrated among a smaller and smaller proportion of people.

The concentration of wealth ownership among the few is inimical both to the capitalistic system and to democratic forms of government. A financial oligarchy and a government of, by, and for the people, simply cannot exist side by side.

Spencer wrote: ” Lenin once pontificated to the effect that he would destroy capitalism, and presumably capitalists, by making their money worthless.”

Wrong. It is thought that John Maynard Keynes made that up in 1919, and was referring to how WWI German reparations would play into the Communists hands.

If you want a real Lenin quote about the Central Planners on Wall Street, and their planning:

“The Capitalists will sell us the rope with which we will hang them.”

― Vladimir Ilich Lenin

for those into a geeky, technical explanation, the price index for personal consumption expenditures is a chained price index based on 2012 prices = 100, and it’s shown in Table 9 in the full pdf the monthly income and outlays report… here’s January:

https://www.bea.gov/sites/default/files/2023-02/pi0123.pdf

that PCE price index rose from 125.124 in December to 125.899 in January, giving us a month over month PCE inflation rate of 0.61939%, which BEA rounds to a 0.6% increase when they report it..

applying that 0.61939% inflation adjustment to the increase in January PCE shows that real PCE rose by 1.1353% in January, which the BEA reports as a 1.1% increase:

(18,050.7 / 17,738.2) / (125.899 / 125.124) = 1.01135317

when those PCE price indexes are applied to a given month’s annualized PCE in current dollars, it yields that month’s annualized real PCE in chained 2012 dollars; those chained dollar figures are then carried to Table 3 in the GDP report, which is typically published a day earlier than the detailed income and outlays report..

As the standard of living continues to deteriorate due to rising prices and people substitute Alpo for ground beef, the PCE will shout, “What inflation? Prices are stable. Stop your whining.”

Greg,

I mean… Your comment is just sensational and dumb. People are rich in the USA.

You should travel more. There are genuinely poor people in the world.

A lot of people live in houses that are worse than the shed in your backyard.

I’ve never met an American who genuinely needs food (although they do exist). It’s usually children who have food poverty due to adults substance abuse.

Does the deterioration of purchasing power suck? Yes.

Are people eating dog food? No.

Or kids don’t eat because of mentally disabled parents also

34 million Americans are “food insecure” according to the FDA. Poverty is a massive problem in America. America is better off than most, but hardly all, other countries, though. This is not a reason for celebration. The richest country in the world should not see 10% of its population worrying about getting enough to eat.

CPI and PCE inflation/inflammation, I thought I read Fed MBS…

Part of the plumbing related to Treasury yields dancing higher (in addition to serious supply shortage)??

Liberty Street Economics

MARCH 24, 2014

Convexity Event Risks in a Rising Interest Rate Environment

Allan M. Malz, Ernst Schaumburg, Roman Shimonov, and Andreas Strzodka

Conversely, MBS holders will find the duration of their MBS extending when rates increase, which they may choose to offset by selling Treasury notes or bonds, or by paying fixed in swaps. If sufficiently strong, this hedging activity can itself cause interest rates to rise further, and further increase duration for MBS holders, inducing another round of selling of Treasuries.

A Convexity Event Averted

A sudden initial rise in medium- to long-term rates can therefore trigger a self-reinforcing sell-off in Treasury yields and related fixed income markets, fueled by MBS hedging—a phenomenon known as a convexity event. During a convexity event, MBS hedgers collectively attempt to decrease duration risk by selling Treasury securities or paying fixed in swaps.